𝙽𝙵𝚃𝔡𝔢𝔤𝔢𝔫 /𝔄𝔩𝔩 𝔦𝔫 ℭ𝔯𝔶𝔭𝔱𝔬 /X/Meme

Joined November 2021

- Tweets 5,207

- Following 6,419

- Followers 3,884

- Likes 4,574

497 Photos and videos

D retweeted

Jun 1

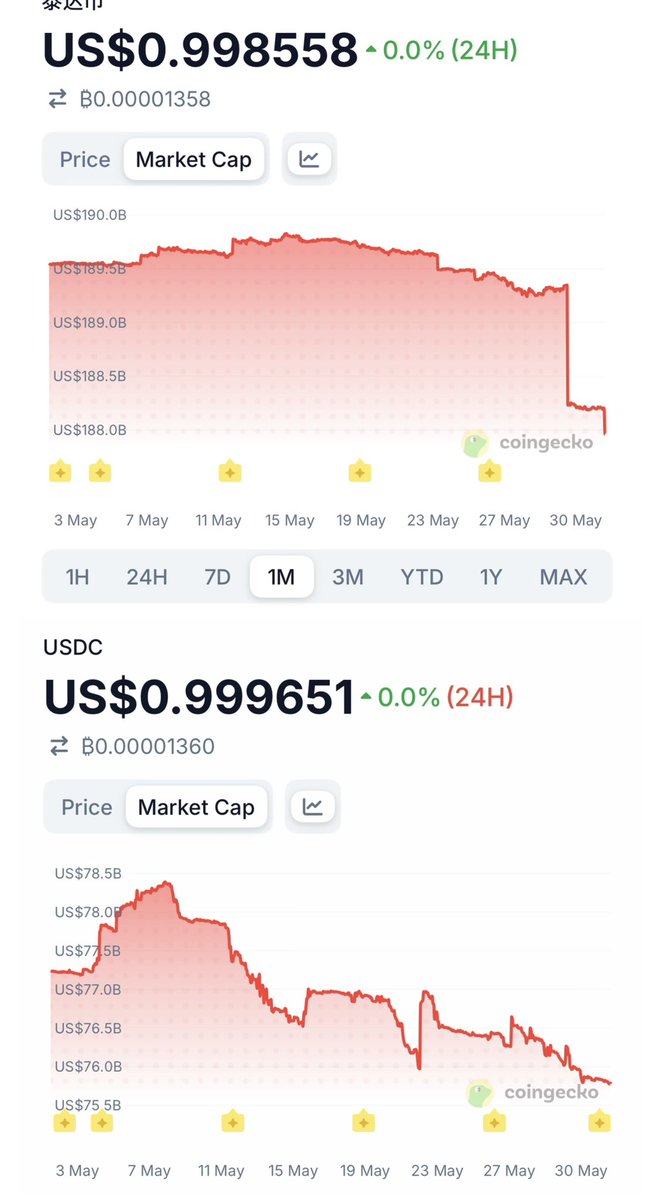

USDT发行量这两天突然有一个大幅度下滑(下降14亿美金),而过去一个月从最高下滑了20亿美金,与此同期USDC发行量大幅下降了26亿美金。相当于过去一个月46亿美金的稳定币撤出了市场,在想稳定币大幅下滑的原因难道是世界杯开幕在即资金准备去赌球了么?只是个思考

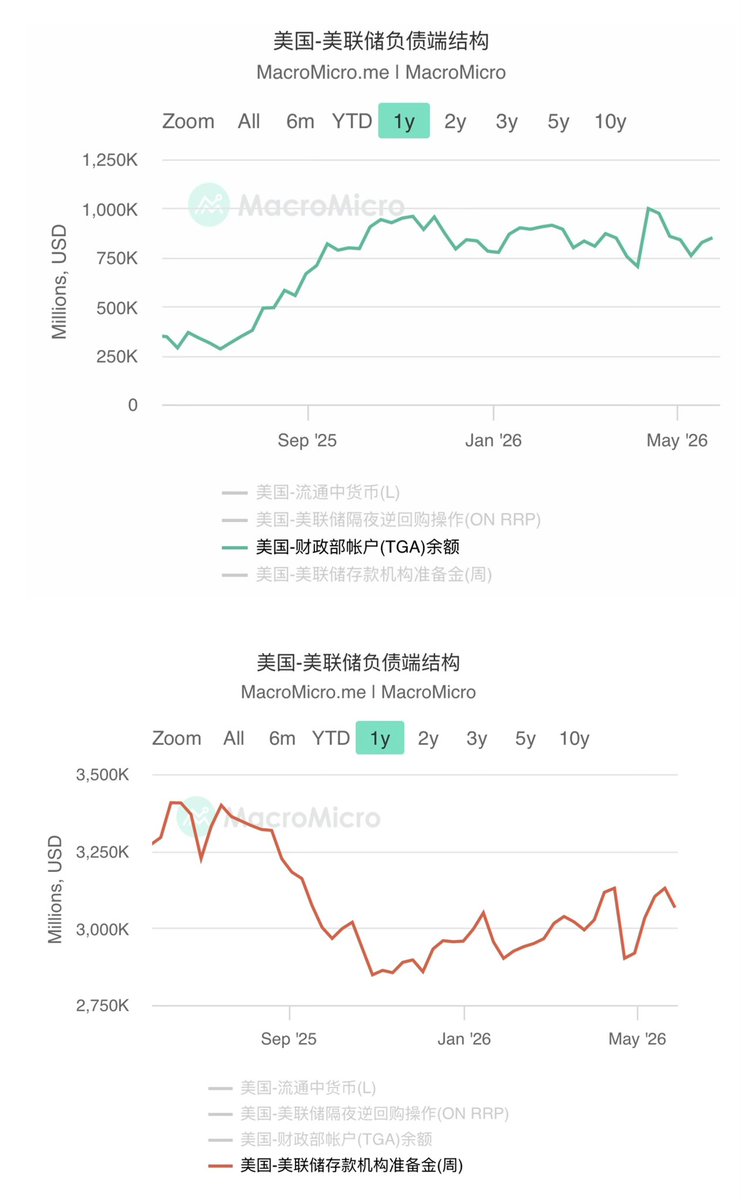

看截至上周银行准备金也开始小幅下降,从5月中的3.13万美金下降到3.06万亿,原因有二:1)与此同时财政部TGA账户余额上升到8490亿美金(相比5月中上升了接近1000亿美金);

2)还有一个大家聊的不多的因素是美联储的扩表节奏(RMP储备管理购买)进一步放缓:从3月中-4月中,rmp规模400亿美金;4月中-5月中,Rmp规模250亿美金;

5月中-6月中,rmp规模100亿美金。

财政部发债规模变大导致tga上升,美联储rmp节奏放缓,整体流动性减弱,最直接的影响就是对流动性最敏感的币市资金大幅流出:稳定币大幅流出,大饼ETF过去两周也是大幅度净流出。币价自然是进一步承压

本条由@bitget_zh赞助,「Bitget 买美股:秒级入场,丝滑交易 」

51

11

83

71,787

D retweeted

May 12

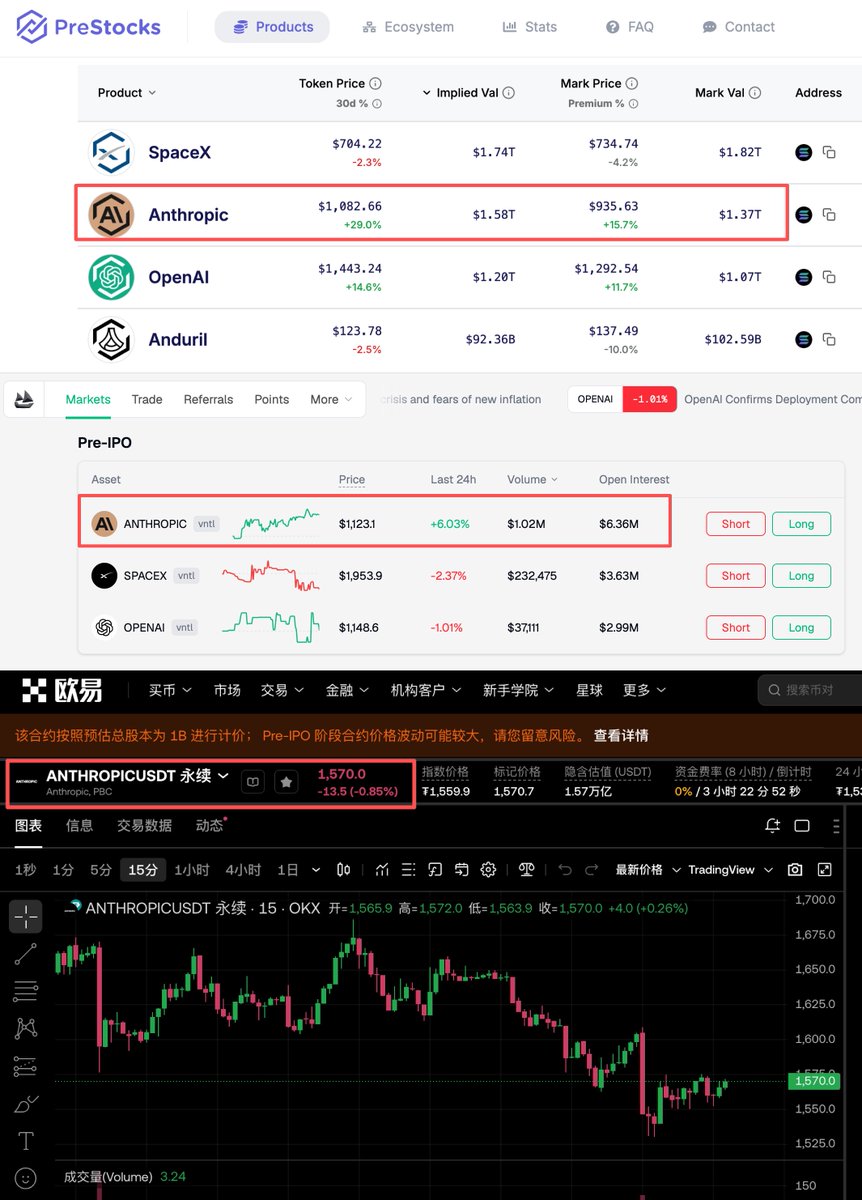

菜市场大妈都知道:如果隔壁摊的瓜便宜三成,要么瓜是坏的,要么秤有吸铁石。

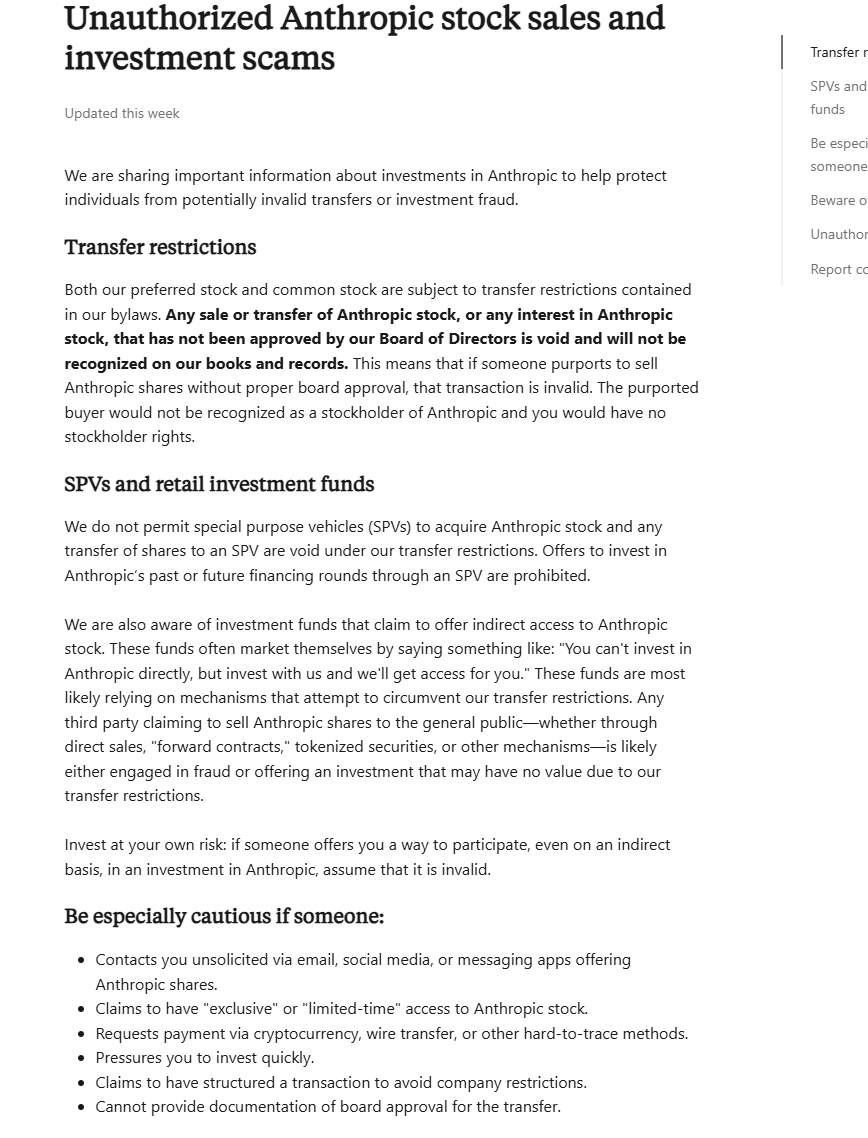

但 Anthropic 这颗 AI 赛道最烫手的标的,目前在链上平台的价差高达 44%。例如在 PreStocks 上 Anthropic目前的实际交易价在 1082 美元,Hyperliquid 是1123美元, OKX 是 1560。在此之外还有 mark price等等等等,所以这瓜到底是多少钱一斤?。。😃

而且背后的资产安全性是大家最为关心的,如果股价起飞了,但是代币崩了,后果是不堪设想的。于是我花了一些功夫研究背后的价格发现机制。

第一种是SPV 份额代币化,以 Prestocks 为代表

SPV简单理解就是为了持有股权而专门注册的一个壳公司。这种一般是在真实世界中通过老股转让等形式,拿到了 Anthropic 的部分股权(或可转债)。然后平台再把这些 SPV 的经济收益权 1:1 映射为链上代币进行流转。价格主要靠机构的铸造/赎回(Mint/Redeem)来锚定

这种方法虽然背后有真实资产,在流程上尽量向传统金融靠拢了,但其实麻烦事也一样不少,和港股暗盘那样的准现货是不同的。。

首先由于 Anthropic 这类顶级公司严禁未经批准的老股转让(图一是刚刚官方发布的警示公告),SPV 往往通过远期合约或受益权转让的方式曲线持股。一旦最终端的原始持股人违约,链上作为第四、五级的权利人,几乎没有法律追索权。SEC 对于未注册证券代币化也依然是严打的态度,总之从法定权益来看还是让人拿不踏实的

其次目前各家发的代币流通性不高,彼此之间也存在显著价差,甚至在极端行情下会出现 30% 以上的估值偏离。常识告诉我们,有效市场是不可能存在这样子的套利机会的。原因其实就是底层资产非同质化、缺乏做空工具、冲击成本等等,这里跑题先不展开。

但我觉得这有点类似国内有些 ETF 限购,底层标的大幅波动的时候就是会带来极高的溢价,如果法律层面没有问题,长期来看价差也是会收敛的,所以这个问题倒不是很大。

第二种 Hyperliquid / Ventuals 这样的永续合约为代表。

这类交易没有有底层真实资产,主要是通过资金费率,用预言机和现实世界OTC 市场(比如 Forge Global、Hiive 上的估值数据)进行弱锚定。

但是反直觉的,这样看似无根的操作,反而在监管路径上是更干净的。@bonnazhu 优酪乳老师也有提到。而且过去 Hyperliquid 展现的交易深度和 0 宕机的历史正在让他走上神坛。

这还没说新提案 HIP-6(Hy-CO,Hyperliquid Continuous Offering)这套连续清算竞拍机制(CCA)正在把hyper 从纯交易所打造成一个恐怖的 listing 机器

第三种是各家交易所的策略,但是随着研究深入我发现玩法的多样性远超这篇短 post 所能够覆盖到的了。。。

- Binance 是现货盘前 合约盘前 钱包入口三线

- OKX 是带盘前阶段的永续合约

- Bitget IPO Prime 是合规机构背书的合成票据

- Gate 是PreToken 铸造 合成合约双轨

除此之外还有 Jarsy、robinhood、各种五花八门的设计和框架。

我感叹 RWA 真是方兴未艾,海面下的冰山完全没被看到。把资产搬到链上,看似是一个简单的概念,其实落地细节太多了。

我先让deepseek 跑了一个调研框架 preview 出来,感兴趣的朋友可以移步查看:github.com/larrychain/on-cha…

这里挖个坑,5 月争取一家家填出来

4

2

17

1,118

D retweeted

Apr 30

分享一下我的2026年对冲思路(中文版,超长文预警)

我叫它:就算crypto tech股/ai泡沫 同时暴跌,年底还如何赚到钱的玩法

纯个人观点,所有信息都来自公开资料。不构成投资建议,DYOR。

如果crypto到年底还有20-40%的回撤风险,我越来越觉得,精选油股和油轮(tanker)股,可能是现在比较干净的对冲方式之一

这不是让你去赌原油今天多还是空(WTI和Brent三月那种行情还能这么玩,但现在作为外行再去碰短线原油,多空都容易被爆)

我看的是 股东回报:分红、特别分红、股票回购。背后是强自由现金流、可控杠杆、还有实打实的资产敞口。仓位配得对的话,这个basket今年现金回报有机会跑到 20-30%。

核心思路不是“哪只油股能翻2倍或5倍”。

它更偏防御:在现在的运费和能源环境下,这些公司正在产生大量现金。很多公司净负债/EBITDA很低。如果运价保持坚挺,部分名字在2026年有机会给到两位数的股东回报率。

这就是crypto震荡的时候,组合里还有实打实的现金流。老实说,我宁愿拿着这个,也不想在风险资产回调时,全仓蹲在没有任何收益缓冲的tech成长股里。

现在买,仍然可能赶上一些接下来的季度分红,但一定要在官方除息日前持有。也别只看分红,回购政策也要查。真正的组合拳是:分红 回购 潜在股价修复。

⚠️ 重要税务提醒,大家都该了解一下:

美国纳税人:想拿qualified dividend的低税率,通常需要在除息日前后121天窗口里,持有满61天以上,并且期间不能hedge。

非美投资者:美国公司分红默认可能会被扣30%预提税。但很多tanker公司注册地不在美国,所以税务haircut可能轻很多。不过别偷懒,先查清楚公司注册地、券商规则和本地税务。

近期分红窗口值得盯,但我会把官方确认的公告和市场预测日期分开说。

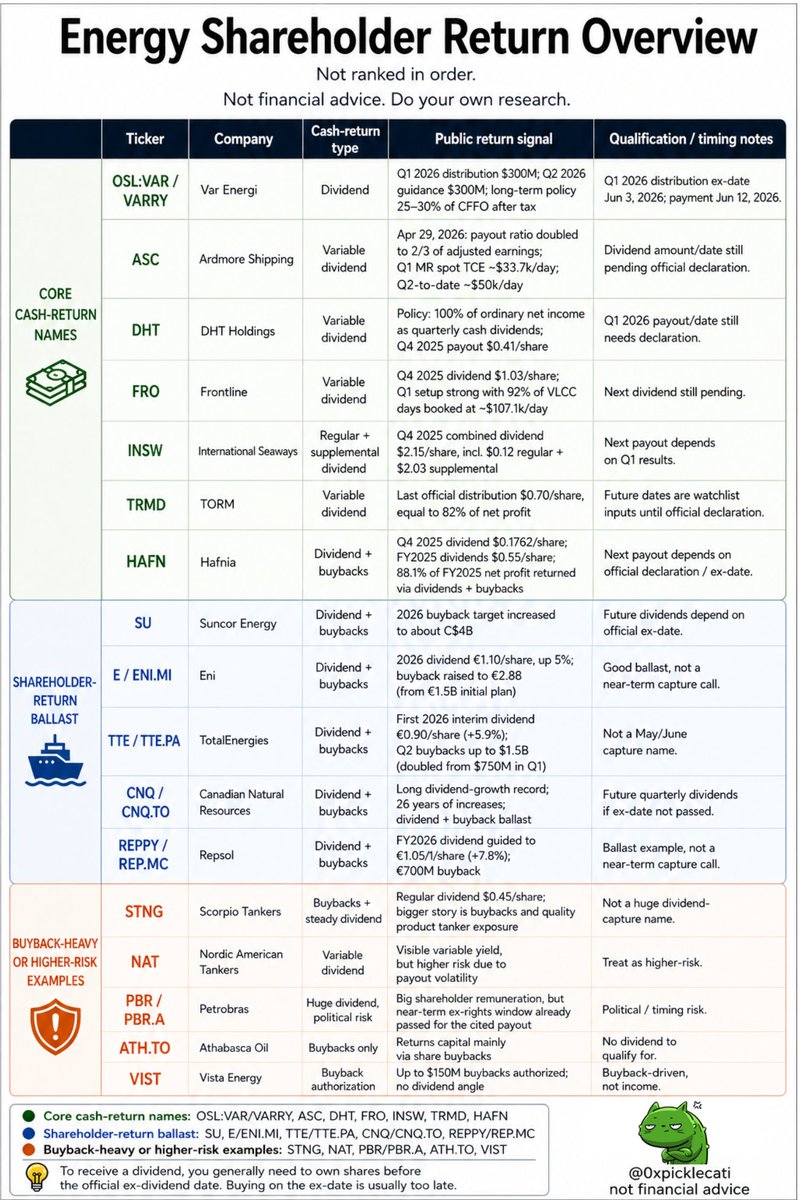

最近确认的股东回报更新:

> ASC(Ardmore Shipping)4月29日宣布,把分红派息率提高到调整后利润的三分之二,从Q1 2026开始生效。Q1 MR现货TCE大概 $33.7k/天,Q2 到目前约 $50k/天。具体分红金额和日期还要等官方公告。

>Var Energi(OSL:VAR / VARRY)Q1 2026 分红已经确认$300M,6月12日支付,Q2也指引了$300M。

> Eni(E / ENI.MI)确认2026年股息 €1.10/股,并把回购计划大幅上调到 €2.8B。

>TotalEnergies(TTE)第一笔2026中期股息上调5.9%,到 €0.90/股,Q2回购翻倍到 $1.5B。它不是5/6月马上吃分红的名字,但属于稳健的股东回报压舱石。

Tanker观察名单:

> DHT:派息公式很干净,100%常规净利润按季度现金分红。Q1金额和日期还待公告。

> TRMD:上次官方分红是 $0.70/股。网上传的5月日期都只是预测,要等TORM正式公告才算数。

> FRO:Q4分红 $1.03/股,Q1看起来也很强,VLCC锁定在大约 $107.1k/天。下一次分红还没公布。

> INSW:最近一次合并分红 $2.15/股,包含常规分红和特别分红,对应Q4 2025。下一次看Q1业绩。

> HAFN:成品油/化学品tanker,最近季度分红上调到 $0.1762/股,还在申请新的10%回购授权。

> STNG:更偏回购 高质量运营,不是纯吃分红的大头名字。

> NAT:浮动收益率看得见,但我会当成更高风险处理。

整个basket分成4个部分:

1. 浮动/公式化分红型tanker

ASC、DHT、TRMD、HAFN、FRO、INSW、NAT,分红弹性最大,但波动也最大。

2. 成品油tanker回购型

STNG,还是航运敞口,但更偏高质量运营 回购,不是单纯吃大额分红。

3. 大型能源股压舱石

SU、TTE、Eni、CNQ、REP、Var Energi

没那么刺激,但胜在分红、回购、规模和资产负债表稳健。

4. 回购/成长型油股

VIST、ATH. TO,不是分红型名字,但回购本身也能创造股东回报。

还有些别的可以看下方引用的原推的配图。

重要提醒:这不是免费午餐。

股票在除息日前后经常会调整价格,有时候跌得比分红还多。浮动分红如果运价崩了,就会大幅减少。回购也只有在管理层用合理价格买回时才真正有意义。

所以我的打法是:趁市场还在低估能源现金流持续时间的时候,持有这些能持续产现金的公司。

为什么我选这个对冲,而不是常见选项?

1. Tech股:本质还是risk beta,没收益缓冲。

2. 债券:衰退时有用,但如果通胀和油价风险一直sticky,就很难受。

3. 现金:安全,但真实回报一般。

4. 长期看跌期权:对冲很干净,但timing错了,时间损耗很贵。

Tanker不一样的地方是,Q1和Q2的强现金流,可以比较快地变成分红、特别分红和回购。不是固定收益,但在合适的运价环境下,现金回流很快。

就算霍尔木兹明天重新开放,整个系统也不会马上重置:

因为:库存要重建,成品油可能还紧,贸易路线效率还会低。Q1现金流已经挣到手,Q2运价才是接下来要看的关键。

Crypto负责非对称上涨,油股股东回报负责现金流压舱。

我不需要每个hedge都5x。

有时候,最无聊的配置,也就是不管crypto大盘再怎么瞎跳,管他跌还是涨,依然还有东西在持续给你付钱。

Apr 30

Gonna share my 2026 hedging thesis (long tweet warning)

I call it: how to get paid even if crypto bleeds and tech beta starts vomiting into year end.

Strictly my personal opinion. All info below are based on PUBLIC sources. Not financial advice, DYOR

With crypto potentially facing another 20-40% drawdown into year-end, I’m increasingly convinced that select oil and tanker equities are one of the cleaner hedges right now.

AND NO, this isn't another tweet about gambling long or short on crude.

The play is shareholder yield: dividends, supplemental dividends, and buybacks, backed by strong free cash flow, manageable leverage, and real asset exposure. Sized right, the basket could return 20-30% cash this year.

My thesis is not “which oil stock does 2x or 5x.”

It’s defensive: these companies are generating exceptional cash in the current freight and energy setup. Many run with low single-digit net debt to EBITDA, and select names can deliver double-digit shareholder yield through 2026 if rates stay firm.

That’s real cash flow while crypto chops, and honestly I’d rather have that than be all-in into tech growth names that offer zero yield buffer when risk assets correct.

Buying now can still qualify you for upcoming quarterly dividends, but you need to own shares before the official ex-date. Make sure you check share buyback policies too, because that’s where the real combo comes from: dividends buybacks potential share price gains.

ALSO AN IMPORTANT TAX NOTE everyone should know:

> US taxpayers: want the lower qualified-dividend tax rate instead of getting cooked at ordinary income rates? Usually you need to hold shares unhedged for 61 days within the 121-day window around the ex-date.

> Non-US investors: normal US dividends can get hit with a 30% withholding tax slap. BUT many tanker names are foreign-domiciled, so the tax haircut can be much lighter. Don’t be lazy though, check domicile, broker, and local tax before celebrating.

The near-term dividend window is worth watching, but I’m separating confirmed declarations from forecasted ex-dates.

Confirmed/recent shareholder-return updates:

> ASC announced on april 29 (literally yesterday) that it is doubling its payout ratio to two-thirds of adjusted earnings, effective Q1 2026. Q1 MR spot TCE was around 33.7k/day, and Q2-to-date was around 50k/day. Dividend amount/date still needs official declaration.

> Var Energi (OSL:VAR/VARRY) has a confirmed 300M Q1 2026 distribution payable June 12, with another 300M guided for Q2.

> Eni (E/ENI.MI) confirmed a 2026 dividend of €1.10/share and raised its buyback plan by about 90% to €2.8B.

> TTE raised its first 2026 interim dividend by 5.9% to €0.90/share and doubled Q2 buybacks to $1.5B. Not a May/June capture name, but good shareholder-return ballast.

For the tanker watchlist:

> DHT has one of the cleanest payout formulas: 100% of ordinary net income as quarterly cash dividends. Q1 payout/date still needs declaration.

> TRMD’s last official distribution was $0.70/share. Any May dates floating around are watchlist inputs until TORM officially declares.

> FRO paid $1.03/share for Q4, and Q1 looks strong with VLCC days booked around 107.1k/day. But the next dividend is still pending.

> INSW’s most recent payout was $2.15/share combined ($0.12 regular $2.03 supplemental) for Q4 2025. Next payout depends on Q1 results.

> HAFN (product/chemical tankers) raised its latest quarterly dividend to $0.1762/share and is seeking a new 10% buyback mandate at the 2026 AGM. Next payout pending.

> STNG is more buyback quality product tanker exposure than a huge dividend-capture name.

> NAT has visible variable yield, but I’d treat it as higher risk.

The basket has 4 buckets:

Variable/formula-based tanker payouts: ASC, DHT, TRMD, HAFN, FRO, INSW, NAT

(highest dividend torque in the basket, but also the most variable)

Product tanker buyback discipline: STNG

(still shipping exposure, but more buyback quality operator than huge dividend capture)

Big energy shareholder-return ballast: SU, TTE, E/ENI.MI, CNQ, REPYY/REP.MC, OSL:VAR/VARRY

(less sexy, but more grown-up hedge: dividends, buybacks, scale, and balance sheet durability)

Buyback/growth oil names: VIST, ATH. TO

(not dividend names, but buybacks can still create shareholder yield without sending you a cash dividend)

see the table below for the full visual overview with qualification/timing notes on every name (including higher-risk examples like PBR)

IMPORTANT: this is not a free dividend glitch.

Stocks often adjust down around the ex-date, sometimes more than the dividend itself. variable dividends can disappear if rates collapse. Buybacks only matter if management buys at sane prices.

So, the setup I like: own cash-return machines while the market is still underpricing how long energy cash flow can stay strong.

Why this hedge over the usual alternatives:

> tech stocks: still risk-on beta, no yield buffer

> bonds: help in recession, messy if inflation/oil risk stays sticky

> cash: safe but real returns are unexciting

> long dated puts: clean hedge, expensive theta bleed if timing is wrong

The tanker angle is different because strong Q1/Q2 cash flow can come back as dividends, supplemental dividends and buybacks. (not fixed, but in the right rate environment, cash returns fast)

Even if Hormuz reopens tomorrow, the system doesn't reset overnight:

> inventories still need to rebuild

> refined products can stay tight

> trade routes can stay inefficient

> Q1 cash flow already happened

> Q2 rates are the next thing to watch

Crypto for asymmetric growth, oil-linked yield for cash flow ballast. I don't need every hedge to 5x, sometimes the boring trade just keeps paying you while crypto does whatever crypto does.

160

136

693

220,101

D retweeted

Mar 20

Professor Jiang Xueqin on how this war is likely to go and what happens to the world.

(0:00) How Will the Iran War Be Resolved?

(7:33) The 3 Major Trends We Will See Due to This War

(11:28) Will Japan Become a Nuclear-Armed Power?

(16:06) The Future of South Korea

(20:12) The Energy Crisis

(25:23) The Future of the GCC and Iran

(29:57) The Greater Israel Project

(35:11) How US Ground Troops Will Change the War

(36:46) Prof. Xueqin’s Advice to Donald Trump

(38:49) Is It Possible for the US to Get Israel Under Control?

(45:03) What Role Does Trump Play in All This?

(48:21) The Future of North America

(54:59) Are We Seeing the End of Europe?

(1:00:58) How Many Americans Truly Understand What’s Happening in the World?

(1:03:50) The Effort to Destroy Western Civilization

3,150

8,381

34,613

5,424,279

D retweeted

Jan 29

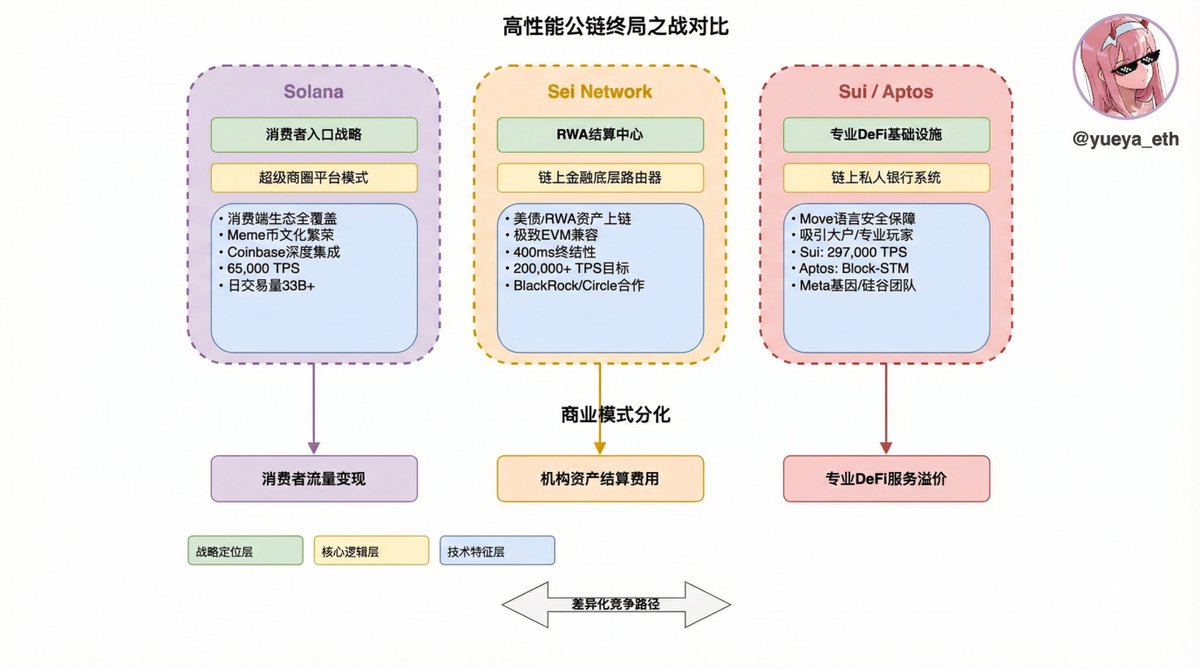

高性能公链之间有什么区别?终局之战即将到来。

Solana、Sei、Sui、Aptos 都叫高性能公链,但他们之间到底有什么区别?

先说高性能鼻祖 @solana 。它的逻辑简单直接,更倾向于原始的“公链”模式,旨在做平台以聚合流量和用户本身。

其底层逻辑是通过海量用户和应用多样性,将链上活动转化为高频消费,进而通过手续费变现,类似于现实中的“超级商圈”。Solana 近年的动作几乎完全围绕消费端展开:手机、支付、社交、游戏、Meme;而近期与 Coinbase 的深度集成,更是补齐了其在原生流动性上的关键短板。

再来看 @SeiNetwork 。Sei 走的是完全不同的路径:它不盲目追求应用与用户数量,而是专注于吸引能带来大体量资产的发行方与机构。其战略是将美债、稳定币、RWA 等“金融底层资产”迁徙至链上,凭借极致的兼容性(EVM 生态可无缝迁移)与毫秒级清算时间,将自己打造为链上金融的底层路由器。

Sei 的工程 Roadmap 充分证明了这一点:

首先是 SIP-3: Sei 官方将其明确描述为“为 Sei Giga 清路”的升级,方向是弃用 CosmWasm 与原生 Cosmos 交易路径,从“双架构”走向更纯粹的 EVM 化路径。

存储优化 SeiDB: 为了支撑机构级并发与高频状态读写,SeiDB 定位于面向 EVM 状态访问模式进行存储优化,旨在解决传统存储层在高吞吐下的状态 I/O 与同步瓶颈。

共识加速 Autobahn: 在 Giga 语境下,Sei 将 Autobahn 作为共识路径的核心,用以实现更高吞吐与更低终局延迟的目标。

这一切布局,都是为了强化其作为“底层路由器”的核心竞争力。

另一方面,RWA 的真正拐点在于,资产一旦上链,便能 24/7 被组合进抵押、借贷、支付与现金管理工作流,且在市场波动时刻仍能快速完成权属确认与风险处置。Ondo Finance 的 USDY 已在 Sei 上线,其官方表述强调了由短期美债支撑的资产安全性,并将其引入了 Sei 的高性能结算环境。

最后是 @SuiNetwork / @Aptos 。它们更像是硅谷精英打造的“链上私人银行系统”。利用技术主权与原生安全性(Move 语言),吸引对安全有极高要求的大户、专业 DeFi 玩家及衍生品团队,定位更趋向于专业的 DeFi 基础设施。

总结:

将这几条公链放在一起对比,你会发现它们表面虽同为“高性能公链”,但在白热化的竞争阶段,各自的定位与商业模式已发生巨大分化:Solana 争夺“消费者入口”,Sei 聚焦“RWA 结算中心”,而 Sui/Aptos 则专攻“高性能 DeFi 范式”。

21

2

27

10,191

D retweeted

Jan 27

“Woomph” is a an essay on my theory about how the Fed could be printing money to manipulate the yen and JGB markets. If true money printer go fucking BRRRR!

open.substack.com/pub/crypto…

93

46

575

123,550

D retweeted

27 Nov 2025

In Defense of Exponentials

I used to tell founders, the reaction you are going to get to your launch is not hate, it’s indifference. By default, nobody cares about your new chain.

I have to stop telling them that now. Monad just launched this week, and I’ve never seen so much hate about a blockchain that just launched. I’ve been investing into crypto professionally for 7 years now. Before 2023, almost every chain I’ve ever seen that launched was mostly met with enthusiasm or indifference.

But now, new chains are born into a chorus of hate. The amount of haters I’ve seen for projects like Monad, Tempo, MegaETH—before they even hit mainnet—is a genuinely new phenomenon.

I’ve been trying to diagnose: why is this happening now, and what does it mean about the psychology of this market?

The Cure is Worse than the Disease

Forewarning: this is going to be the vaguest blockchain valuation post you ever read. I don’t have any fancy metrics or charts to sell you on. Instead, I’ll be arguing against the zeitgeist of Crypto Twitter, which for the last couple of years, I’ve been constantly on the opposite side of.

In 2024, I felt like what I was arguing against was financial nihilism. Financial nihilism is the belief that none of these assets matter, it’s all memes at the end of the day, and everything we’ve built is inherently worthless.

Thankfully, that’s no longer the vibe. We have broken out of that spell.

But the zeitgeist now is what I’d call financial cynicism: OK, maybe some of this stuff has value, maybe it’s not all memes, but it’s grossly overvalued and it’s only a matter of time before Wall Street finds that out. Not that all chains are worthless. But these things are all maybe worth 1/5th-1/10th of what they’re currently trading at (have you seen these PE ratios?), and so you’d better pray like hell Wall Street doesn’t call us on our bluff, because once they do it’s all getting wiped out.

You’ve got many bullish analysts now trying to conjure up optimistic L1 valuation models, inflating PE ratios, gross margins, DCFs, trying to fight against this mood.

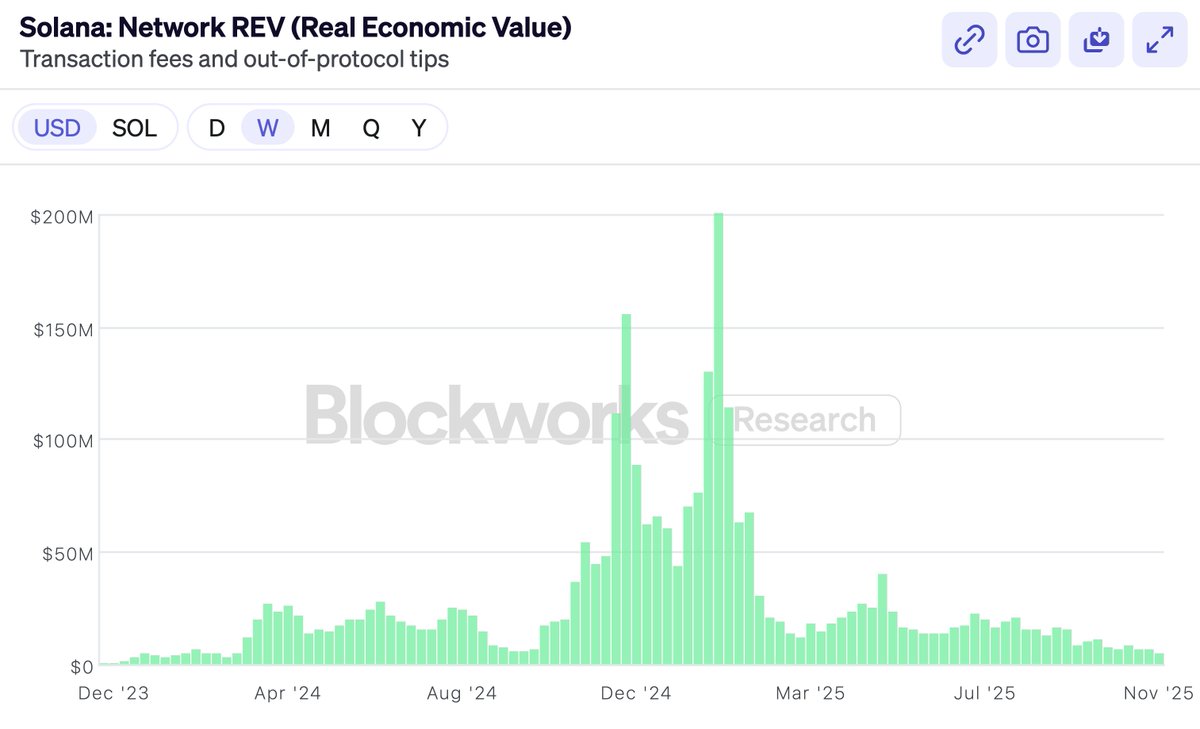

Late last year, Solana very proudly embraced REV as a metric that could finally justify their valuation. They proudly announced: we—and only we—are no longer bluffing to Wall Street!

And, of course, almost immediately after REV was embraced, it fell off a cliff (though $SOL, tellingly, did better than REV did).

Not that there’s anything wrong with REV. REV is a very clever metric. But the point of this post is not metric selection.

Then came the launch of Hyperliquid. A DEX that had real revenue and buybacks and PE multiples. And the chorus said—look, look I told you! Finally, for the first time ever, a token that has some real profits and a proper PE multiple. (Nevermind BNB, we don’t talk about that.) Hyperliquid will eat everything because obviously Ethereum and Solana don’t make any real money, we can stop pretending to value them now.

Hyperliquid, Pump, Sky, these buyback-heavy tokens are all great. But the market always had the ability to invest into exchanges. You could always buy Coinbase, or BNB, or whatever. We own $HYPE, and I agree that it’s a fantastic product.

But that’s not why people were investing in ETH and SOL. The fact that L1s don't have exchange-like profit margins is not why people were buying them—if they wanted that, they could’ve bought Coinbase stock.

So if I’m not critiquing blockchain financial metrics, maybe you think this post is going to be chiding the sinfulness of the token-industrial complex.

Obviously, everyone has lost money on tokens in the last year, VCs included. Alts are down bad this year. And so the other half of the zeitgeist on CT is arguing about who's to blame. Who’s become greedy? Are the VCs greedy? Is Wintermute greedy? Is Binance greedy? Are the farmers greedy? Are the founders greedy?

The answer, of course, is the same as it’s ever been.

Everyone is greedy. Everyone. The VCs, Wintermute, the farmers, Binance, the KOLs, they're all greedy, and you are greedy too. But it doesn't matter. Because no functioning market has ever required anyone to act against their self-interest. If we're right about crypto, we can all be greedy and the investments will still work out. Trying to analyze a market that has gone down by figuring out “who’s greedy” is going to be about as fruitful as commissioning witch trials. I guarantee you, nobody just started being greedy in 2025.

So this, too, is not what I’m going to be writing about.

Many people want me to write a post about why $MON should be valued at X or $MEGA at Y. I’m not interested in writing this post, or advocating that you buy anything in particular. In fact, you probably shouldn’t buy any of them if you don’t already believe in them.

Will any new challenger chain win? Who knows. But if it has a material chance of winning, it's going to be priced on that basis. If Ethereum is worth $300B or Solana is worth $80B, a project that has a 1-5% chance of becoming the next Ethereum or Solana will be priced according to those probabilities.

Somehow CT is scandalized by this, but it’s no different than Biotech. A drug that has less than a 10% chance of curing Alzheimer's is priced by the market as worth billions of dollars, even if 90% chance it won’t pass stage 3 trials and will go to 0. That's how the math works—and turns out, markets are pretty good at doing math. Binary outcomes are priced on probabilities, not on run rates or moral turpitude. It’s the “shut up and calculate” school of valuation.

I really don’t think that’s an interesting question to write about. “5% chance to win? No way, that’s clearly a 10% chance!” Markets, not articles, are the best way to assess that for any individual token.

So here’s what I am going to write about: CT doesn't seem to believe anymore that chains are valuable.

I don’t think this is because they don’t believe new chains can win market share. We just saw Solana dominate market share after emerging from the ashes less than 2 years ago. It’s not easy, but of course it’s possible.

It’s more that people have come to believe that even if a new chain wins, there’s no prize worth winning. If $ETH is just a meme, if it’ll never generate real revenue, then even if you win, you won’t be worth $300B. The contest is not worth winning, because these valuations are all bunk and it’ll all come crashing down before you go to claim your prize.

Being optimistic about chain valuations has become passé. Not that nobody is optimistic—obviously there must be optimists out there. For every seller there’s a buyer, and as much as CT cool kids love to drag L1s, people are comfortable buying SOL at $140, ETH at $3000.

But there’s a perception now that all the smartest people are over buying smart contract chains. Smart people know the jig is up. If not now, then soon. The only people buying here are suckers—Uber drivers, Tom Lee, and KOLs who say stuff like “trillions.” And maybe the US Treasury. But not the smart money.

This is bullshit. I don’t believe it, and you shouldn’t either.

So I felt like I had to write a smart person’s manifesto on why general purpose chains are valuable. This post is not about Monad or MegaETH. It’s really in defense of ETH and SOL. Because if you believe ETH and SOL are valuable, the rest is straight downstream.

Defending ETH and SOL valuations is generally not my job as a VC, but fuck it, if nobody else is willing to do it, then I’ll write it.

Feeling the Exponential

My partner Bo experienced the Chinese Internet boom first-hand as a VC. I’ve heard how “crypto is like the Internet” so many times now that it doesn’t even register for me anymore. But when I hear his stories, it always reminds me how costly it is to be wrong about these things.

A story he often tells is about when all the early e-commerce VCs (it was a small group back then) got together for coffee in the early 2000s. They debated: how big is the market for e-commerce going to be?

Is it going to be mostly electronics (maybe only techies will use PCs)? Could it ever work for women (perhaps they’re too tactile)? What about food (maybe impossible to manage perishables)? These were deeply important questions for early VCs to decide what to invest in and what prices to pay.

The answer, of course, was that literally every single one of them was devastatingly wrong. E-commerce would sell everything, and the target audience was the whole fucking world. But nobody at the time actually believed it. And even if they did, it would be too absurd to say out loud.

You just had to wait long enough for the exponential to show you. Even among the believers, very few thought e-commerce would become as big as it became. And those few who did, almost all of them became billionaires from just not selling. Every other VC—as Bo tells me, since he was one of them—sold too early.

It has become passé in crypto to believe in the exponential.

I believe in the crypto exponential. Because I’ve lived it.

When I started in crypto, nobody used this stuff. It was tiny and broken and awful. TVL on-chain was in the millions. We invested into the first generation of DeFi, MakerDAO, Compound, 1inch, back when they were science projects. I remember playing around on EtherDelta back when DEXes traded single digit millions a day, and that was considered to be a huge success. It was complete dogshit. Now we routinely trade in the tens of billions on-chain every day. I remember believing it was crazy that Tether hit a billion dollars in issuance and was being written up in the NYT as a ponzi scheme on the brink of shutdown. Now stablecoins are over $300B and regulated by the Federal Reserve.

I believe in the exponential because I’ve lived it. I’ve seen it over and over again.

But you might respond—well, stablecoin growth might be exponential, maybe DeFi volumes are exponential, but they don’t accrue to ETH or SOL. The value doesn’t get captured by the chains.

To which I answer: you still don’t believe in the exponential.

Because the exponential’s answer is always the same: it doesn’t matter. This stuff is going to be so much bigger than it is today. And when it’s absolutely enormous, you’ll make it up on scale.

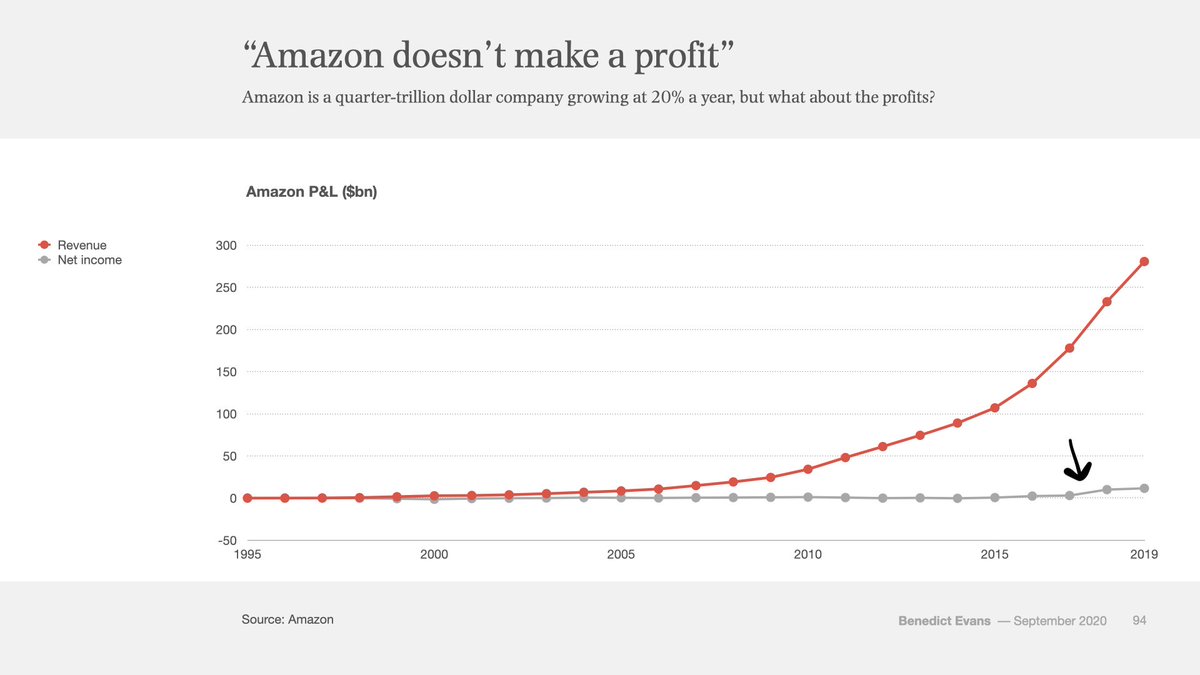

Study this chart.

This is Amazon’s P&L from 1995 to 2019. That’s 24 years. Red is revenue, gray is profit. You see that little blip on the end where the gray line goes up? That’s when, 22 years in, Amazon started actually making a profit.

Amazon was 22 years old when this little gray line of net income first peeled off of 0. Every single year before then, there were op eds and critics and short sellers claiming that Amazon was a ponzi scheme that would never make any money.

Ethereum just turned 10 years old. This is what the first 10 years of Amazon stock looked like:

10 years of chop. All along the way, Amazon was beset with doubters and non-believers. Is e-commerce a VC-subsidized charity? They’re selling underpriced cheap low-quality knick-knacks to bargain hunters, who cares? How are they ever going to make actual money, like Walmart or GE?

If you were arguing about Amazon’s P/E ratio, you were in the wrong regime. That’s the regime of linear growth. But e-commerce was not a linear trend, and so every single person for 22 years arguing about P/E ratios was devastatingly wrong. No matter what you paid, no matter when you bought, you were not bullish enough.

Because that’s what exponentials do. When it comes to truly exponential technologies, no matter how big you think it’s going to get, it just keeps getting even bigger.

This is the thing that Silicon Valley has always understood better than Wall Street. Silicon Valley was raised on exponentials, while Wall Street was raised on linearity. And over the last few years, crypto’s center of gravity has migrated from Silicon Valley to Wall Street. You can feel it.

Granted, crypto growth doesn’t look as smooth as e-commerce’s growth. It’s burstier, it goes in fits and starts. This is because crypto, being about money, is deeply tied to macro forces, and it also has more violent regulatory push and pull than e-commerce. Crypto strikes at the heart of the state—money—and so it’s more unnerving to governments than e-commerce ever was.

But the exponential is no less inevitable. It's a crude argument. But if crypto is exponential, then the crude argument is correct.

Zoom out.

Financial assets want to be free. They want to be open. They want to be interconnected. Crypto turns financial assets into file formats, makes it as easy to send a dollar or a stock as to send a PDF. Crypto makes it possible for everything to talk to everything. It makes it all 24/7, global, interconnected, and open.

That will win. Open always wins.

If there’s no other lesson I've learned from the Internet, it’s that. Incumbents will fight against it, governments will huff and puff, but eventually they will give up against the adoption, the generativeness, the sheer efficiency that this technology enables. It’s what the Internet did to every other industry. Blockchains are how that same trend will gobble up all of finance and money.

Yes—with enough time—all of it.

An old saying goes: people overestimate what can happen in two years, but they underestimate what can happen in ten.

If you believe in the exponential, if you zoom out enough, then it’s all still cheap. And it should humble you that every day, the holders outlast the sellers and naysayers. Big capital has a longer time horizon than CT swing traders might lead you to believe. Big capital has been trained through history not to fade big technologies. You know, the big gushy story that originally got you to buy $ETH or $SOL? Big capital believes that story and hasn't stopped.

So what exactly am I arguing?

I am arguing that applying P/E ratios to smart contract chains (the “revenue meta,” as it’s now called), is giving up on the exponential. It means you have consigned this industry to the regime of linear growth. It means you believe 30 million DAUs on-chain and <1% of M2 is it. Crypto is just one of the things in the world. A sideshow. It did not win. It was not inevitable.

More than anything, I’m arguing to be a believer. Not just a believer, but a long-term believer.

I’m arguing that this exponential will be bigger than anything else you’ve been a part of in your life. That this is your e-commerce. That you will look back when you’re old and tell your kids—I was there when it all happened. Not everyone believed it was possible, that whole societies could change, that all of money and finance would be transformed by programs running on decentralized computers that we collectively owned.

But it actually happened. It changed the world.

And you were a part of it.

Disclosure: These are my own views. Dragonfly is an investor in $MON, $MEGA, $ETH, $SOL, $HYPE, $SKY among many other tokens. Dragonfly believes in the exponential. This is not investment advice, but is advice of another kind.

934

678

3,664

2,073,678

D retweeted

24 Nov 2025

324

420

2,896

1,686,386