Joined March 2021

- Tweets 326

- Following 116

- Followers 24

- Likes 242

5 Photos and videos

Tee G retweeted

Exactly. Are we overvalued? Will we grow OI with 18mo runway and tons of things coming together after 8 years? Run your valuation and cast your lots in the market.

But accuse me of criminal fraud in an 8am market manipulation report full of lies and misstated basic facts, I’ll burn down your entire network down in principle as a little side quest in building smarter markers.

2

10

41

578

Tee G retweeted

..and ISV logic controls (you think TT/Trayport/CQG systems etc let someone make wash trade entires?!) …and our mandated market surveillance system data

…and the controls of heavily regulated FCMs which is the only way to trade, ..and institutional trade desk compliance (only institutional investors with compliance trade through regulated FCMs and global ISVs on our exchange).

It’s like these morons traded an offshore crypto exchange once or something and think that the first clearinghouse regulated in over a decade, with execs in the business at the top levels for decades (or its regulator or FCMs/ISVs) has no idea what they’re doing or can somehow wash trades or turn on and off trade volumes even if they wanted to.

The whole thing is so idiotic, so easily falsifiable, so illogical, only a desperate stock manipulator plays this hand (and only moron CIOs can’t do the mental cycles to think a regulated exchange and clearinghouse with these resumes and this ecosystem needs to justify the demanded response from a stock manipulator)

2

7

27

485

Tee G retweeted

Jun 13

Anatomy of a Reverse Pump and Dump Conspiracy Vol II

(short and distort operation)

They execute their market manipulation through “clever” typos and horrendously misstated financials (that a 5th grader with AI could have caught in editing), while grasping at straws elsewhere (perhaps that’s even the point? ..keep regulators focused on the nothing burger tweet threads while the stock operation was the material financials mistakes in the report…notice how their 🗑️🔥 financials comments weren’t the main part of the Twitter story with a company funded for 6 quarters with growing [world class institutional] onboarding, products and OI).

This report doesn’t need to stand the test of time because it’s a 30min stock [manipulation] operation that works or fails on the first trading day, the short seller is already working to cover the morning of the stock manipulation (see exert from a Bloomberg article from another short and distort operation testimony below—the hedge fund and shady shell game company with the newsletter are interchangeable). ..Every pattern seen in our stock the weeks before and morning of matches the article.

We have all of the reverse pump and dump data captured for regulators, Morgan Stanley, etc.

They already failed their operation in the market IMO, but now their next task is to try and avoid ankle bracelets as all the rats start to turn on each other (this newsletter and the funds will be slippery across jurisdictions though, a big part of the operation). Had a number of great conversation around Toronto yesterday. Mr. S will have his face plastered on a wanted poster around Toronto on Monday. Many capital markets people in Toronto want to see these guys hang as well, tired of Canada’s bad reputation, but haven had the neurodivergent CEO with the global regulator relationships that we do. All information is coming to light already (especially with my key plant pulling the pieces together).

We coming

Jun 12

Your “accidental” typos and materially misreporting financial information while focusing your “smoking guns” grasping at straws (hours before a maket moving event), and the 10x normal dumping and covering operations won’t age well either. Nor will your conversations in Toronto. Better hope they treat you better than other “hit squad” newsletter writers thrown under the bus when the swamp creatures all head for the exits. You’re getting played, buddy.

And no need to contact our regulator (but good luck if you do), they will already have our market surveillance and market maker programs, but we appreciate you sending that slop to probably the most stringent (and intelligent) regulator on the planet, who can’t be hoodwinked or run around like other jurisdictions your clients operate in (and I would suspect won’t tolerate any of the incentives that drive you to produce “accidental material typos” in all of that slop).

(This is the one and only time I will respond to you outside of legal channels btw, so enjoy it and distort it all you want—your information game is obviously dirty and unethical, and I believe in real time markets digesting this garbage before the lawyers do…so hope you and the swamp creatures who don’t know how to build, and only destroy, feel confident dying on that hill of slop that a 5th grader with AI could debunk and refute)

9

11

83

20,792

Tee G retweeted

Jun 11

Took me about 4 hours to write. Hope I gave some justice to the misrepresentation of Abaxx in the report.

$ABXX.TO

4

22

123

10,196

Tee G retweeted

Jun 11

@viceroyresearch and other $ABXX shorts seem singularly focused on today's trading metrics, but that misses the broader investment case entirely.

As @chamath said on the All-In panel:

"That theme of you rebuild it in the modern era and you unbundle the incumbent, that has a lot of legs. And in a regulated market, that has a ton of legs."

That's exactly what Abaxx is attempting.

For decades, exchanges like ICE and CME have benefited from regulated markets and powerful network effects, but they're also classic incumbents: legacy technology, high fees, and business models built in a different era.

The question isn't whether Abaxx's volumes or OI today are large enough. The question is whether a modern exchange and clearing platform can capture meaningful market share in commodities that are becoming increasingly global, complex, and digitized.

If FMX can challenge CME in rates, why is it impossible to imagine a next-generation exchange challenging incumbents in energy, PM, and environmental markets?

Most investors are analyzing Abaxx as if it's a quarterly earnings story. This is an infrastructure story. The value is in the network being built, the products being launched, the clearing relationships being established, and the ecosystem that could exist years from now.

We're still extremely early. Outside of a small group of commodity and energy specialists, barely anyone in the broader North American tech and growth investing community is even aware of $ABXX.

This story isn't in the ninth inning. It's still in the first.

youtube.com/watch?v=V0lFjTWx…

4

6

35

8,281

Tee G retweeted

Jun 9

I like the stock. And I’ll be buying more.

Markets are funny. Nothing but the growing net shorts had anything available to sell under $55 for all of Q2 until [checks notes] the company raised $ 69mm at $54.25 and completely derisked the balance sheet through the rest of the transformational growth and ramp up period through 2027; nothing was for sale before…but now we can buy below 50, at Q1 prices again, like the Q2 fundamental breakout growth and new product rollouts didn’t even happen!

It was the third week of March when the stock price was last here, when the 50ma Exchange ADV was less than a one-third of today’s ramp up (and just take a look at the rest of Q2 PRs and derisking since then).

Abaxx isn’t an economic cyclical or tech momentum stock (even though we’re being traded that way since the TSX listing) — we are a QoQ fundamental derisking, blocking & tackling, “NAV unlocking” stock as we take the probability of our benchmark contracts succeeding from “~20% priced in now”, to something much higher through end of 2027 with no financing overhang and a significant s/d deficit of shares IMO for those who will want to own that asymmetric call option through each quarter of derisking (plus the tech value unlock), versus those who just trade/flip/want to exit.

I don’t believe there is much real supply to materialize below $60 (or even analyst consensus pre-tech of ~$85), and 1 in 4 shares sold in second half of May were new net shorts again.

So much more just up ahead. I like the s/d. I like the stock.

#29ers $ABXX

8

18

140

13,650

Net/Net: this is BIG. As we saw last year, this year’s August update call (2Q26 results) will probably be the trigger for the next leg up in the $ABXX.TO story, as more details of the imminent access to Chinese, US and EU traders emerge.

ANALYSIS: The onboarding of multiple Chinese FCMs on top of the US/EU bank FCMs previously announced means that, as the onboarding flywheel gets into high gear, the increase in volumes will enter the exponential leg of “s-curve” of contract adoption. The volume breakout should be evident by late 3Q to mid 4Q, rising from the 12k/day currently onto the 100k/d by mid 2027, IMO.

We're at a fully diluted MktCap of US$1.7bn, down approximately 20% from its peak in early May, as the capital increase seems to have brought forward the latent institutional demand, combined in recent days increased short-selling (from the “$2bn market cap and no revenue” thesis). All this has been suppressing the share price, effectively subsidizing long term holders increasing their positions. This won't last long...

NEWS: @abaxx_tech’s CEO announced that their Singapore future’s exchange expects to onboard US and Chinese FCMs in 3Q26. In the case of China, he specifically mentioned 3 FCMs in the pipeline. Mizuho, the leading LNG infrastructure financer and an early backer of Abaxx’s LNG contracts, is expected to onboard by late 3Q or early 4Q 2026.

Abaxx and China: for years Abaxx shareholders were wondering how long they would need to crack into the Chinese trade flows. Their location in Singapore was to offer a geopolitically neutral bridge for the trading of the global energy transition commodities (LNG, battery metals, carbon, etc) and PMs (gold, silver) with a strategic foothold next to the world’s leading consumer and price influencer. The idea is to offer off-shore USD-denominated contracts with physical delivery to complement the massive onshore volumes traded on the SHFE. Abaxx setup offices in HK and Beijing in late 2024 and announced a partnership with the Qingdao International Energy Exchange for LNG trading in Sept 2025, creating expectations of a significant boost to traded volumes from linkages to the world’s leading markets in metals and energy. This is about to start to happen!

Abaxx and US/EU traders: So far volumes on the exchange had been limited to traders in smaller Asian markets (particularly Indian gold traders). With the onboarding of several bank FCMs, including a leading US bank FCM that services the global energy trading complex (as mentioned in the 1Q26 call), we will see Abaxx' contracts begin to be traded by the US/European investor base. These energy traders not only want access to Abaxx LNG contracts, but also to its growing roster of wind and solar contracts.

Do your own DD as this is certainly NOT investment advice!

Jun 8

China is happening. Three FCMs in the works. And if you think India made a difference, now we’re talking about the largest metal trading market in the world (and key emerging LNG players as well). Anyone still looking at Abaxx as a “wait and see” doesn’t understand this team, this opportunity, and that we are simply in the blocking-and-tackling stage to significant growth for years to come.

9

68

3,428

Tee G retweeted

Jun 8

China is happening. Three FCMs in the works. And if you think India made a difference, now we’re talking about the largest metal trading market in the world (and key emerging LNG players as well). Anyone still looking at Abaxx as a “wait and see” doesn’t understand this team, this opportunity, and that we are simply in the blocking-and-tackling stage to significant growth for years to come.

5

19

117

13,060

Tee G retweeted

Take the Labrador iron assets, clip a 1% royalty, put the royalty into a new company: "RoyaltyCo". Abaxx keeps 80% and spins out the remaining 20% to shareholders. Shorts have to cover as they can't produce the "RoyaltyCo equity". Costs maybe $50k/yr in ongoing filing costs.

6

3

21

1,055

Tee G retweeted

The distributions can be phased, too.

Very interested what the big guy @JoshCrumb thinks.

1

1

8

249

Tee G retweeted

May 27

All good. Headline is “Canadian bought deal”, reality under the hood is that it is some incredible long only funds and ATB Cantor hustled for 9 months for a great deal and got paid for the inbound. Clean deal and great book.

[better to raise money with clean market window and good momentum when nobody expecting it, than try to take it all off the table with potentially no window and everyone expecting it..ie Abaxx c2024]

5

24

453

Tee G retweeted

May 27

Correct. They were very aware of the situation going in and how to handle it internally with their desks. As I mentioned, book was full before it went live, sales desk wasn’t even part of the process so any PR inbounds from undesirables not getting a fill

4

37

653

Net/Net: another opportunity lost to properly market the Abaxx tech story, generate a 5x-8x demand to get a premium pricing at the expense a slightly higher dilution. The deal rewards committed institutions who've bought in the market, without proper price discovery. One day Abaxx will escape the Canadian markets trap (heavily weighted towards financials, energy, mining…), just not today.

The News: Earlier today, after the close, @abaxx_tech announced a CAD$50mn bought deal to sell 922k shares @ CAD$54.25 (1.06mn shares and CAD$57.5mn gross proceeds after 15% overallotment). The pricing was a 12.5% discount to today’s closing price and a 4.4% discount to the avg price over the past calendar month.

Who got the shares? The deal was apparently placed among institutional investors who’ve been actively buying shares in the market: “Earn your long-term hold shares or buy in the market” according to Abaxx’ CEO Mr. Crumb, apparently rewarding LT Hodlers of the shares, ensuring no flowback vs the discount to the last traded price. Shortly after the announcement, the size of the oversubscription (from inbound share requests) was about 3x (and expected to be higher at the close of the deal), despite that this was not a marketed deal. This reflects unmet demand from potential new institutional shareholders that Mr Crumb expects will turn to the open market to build their positions.

Uses of proceeds: The transaction funds over 1 year of Opex, extending Abaxx’ cash runway beyond 2027. The uses of proceeds will largely fund the @abaxx_exchange’s operating cashflow and the Opex required to fuel the go to market of Abaxx’ tech products (MarketOS, Agents , etc).

Why now? Part of the rationale for the timing of the deal was the risk of deteriorating market conditions later this year. Rising LT US$ interest rates and the incoming energy crunch from the conflict in the middle east, let alone a resumption of all-out hostilities, raised the specter of the company running low on cash amidst an economic shock that @CommodMkt labels larger than Covid-19. This was probably the overriding concern that drove this deal. Without a successful launch of MarketOS (T 0 collateral) with the onboarding of the energy trading complex, it's probably too much to ask for a better valuation.

A Missed Opportunity: A properly marketed deal would have generated 5x-8x... and a premium not a discount, IMHO. Then again I’ve never run a company, but I've seen properly marketed deals generate the type of demand and liquidity (yes, selling to HFs and short-sellers) that incites lowly allocated accounts to buy in the aftermarket. This is the unmet demand that can’t be bothered to buy 5-10k/day for who knows how long to build a position, in full knowledge that their investment committees would turn down the investment opportunity. Low liquidity begets low liquidity, and LT Hodlers, while welcome, are only going to add to the closely held nature of this company (shout out to the #29ers). The effective free float remains low, which could be explosive, as we expect top line growth to fuel this story.

The company is rewarding the institutions that bought with the short-sellers liquidity, minimizing dilution at the price of taking a big discount, probably close to the VWAP of these funds’ purchases. Quid pro quo here? You bet, nothing wrong there.

What about the index buying? The last time around, the increase in borrow supply from new passive holders fueled the increase in net shorts, which remain low in relative terms (despite being large vs ADTV), allowing them to deploy their price suppression strategies and pray for a way out. Expect more of the same in the next inclusion rounds from the Karens short under the “100x trailing revenue” rationale...

#29ers $ABXX $ABXXF

4

1

33

5,055

Tee G retweeted

May 21

Both are partially right.

1) OI is low because you have to have physical market makers (who can make/take delivery) and financial market markers (spreads and volume). We have this in precious but it’s still just a handful. It drops off significantly end of month from both our expiry window, as well as Comex expiry windows where a lot of traders are arbing and trading against. In VCMCarbon we also have physical makers/takers (unlike a major competitor who literally wrote a contract spec where there was no available “physical” to their spec, nobody to make/take registry transfer). LNG and Lithium is close. When, not if on building OI and deliveries.

2) But volume does matter. Bank FCMs don’t even start onboarding until they can seen the liquidity and tight spreads needed for institutional flows. Thats about 20k per day from what we learned at Boca (which is when many flipped the green light end of March to submit clearing applications and/or find carry broker connections). And arb revenue against other markets, even if it slows end of month, is still rev.

3) Finacial futures startups (MiaEx ext) aren’t relevant here from a V/OI perspective due to #1. And we’re the first full stack physical clearinghouse perhaps ever (new contracts, new clearinghouse FCMs/ISVs connect, new tech, all from scratch, takes time). And physical commodities liquidity is winner take all (see #1 again), financial futures and equities are replicable and all compete (even though best liquidity pools still take most). We aren’t listing copies of WTI to take market share, we’re ramping up our own products with no competition (other than carbon).

4) So the billion dollar question where these threads all started….What should be forward priced into the stock based on the risk/reward of above, runway/dilution, and where V/OI is at?

Should you go long or short on early volume/low OI versus market cap?

If you think we don’t have the clearing members and physical market makers onboarding and we don’t know what we’re doing, and we won’t through the low budget runway we’re operating on ($_30mm annual “burn” to wait on this “option” is literally nothing on our market cap & the backers we have, ~2% dilution per year). Remember, we already sunk all captial for a 1mm ADV exchange, dilution behind us, pre-built. And now look at how I’ve managed dilution for 6years WITHOUT revenue and ramp up, on-boarding momentum; you think now is where I’m going to dilute uncontrollably and lower the probability of a 1mm ADV NAV that I still own 10% of? If we hit it anytime in the next 7 years you’re going to make [many] multiples on your shares here (Lol, or the moron-take that I’m just going to pump & dump my future 4/5-figure stock into an index…Claire, ms. 4%. zero-DD).

(This is all the conservative take btw, competing on the incumbents web1 playing field, we’ll still go up multiples from here…but they can’t even play on the MarketOS Web3.5 playing field we are building, in that we are 1 of 1 and will be coming to take existing markets and liquidity as well).

Alright cool, so now let’s get back to addressing the morons shorting an illiquid call option now, with a month plus to cover liquidity, on shares that can’t be pried out of the cold dead hands of me, [major family offices and institutions] and people that have held for 4-5yrs because they understand the simple math we’ve set up. I guess some people don’t know how to do forward probabilities and share counts, can’t see the flood of institutions now wanting limited stock—for them they can go ahead and short the coin toss in a heavily skewed coin and cry FRAUD (lol, we literally have NYMEX people that have been building markets for 5 decades, Goldman partners that helped build Brent, ICE, former head of CME metals and energy, former head of product launching clearport, head of DME / Omani crude, co-head Goldman Asia…and and…all in on a pump and dump and not here to build markets hahahaha)

6

11

53

1,664

Tee G retweeted

May 17

Wow, I couldn’t disagree more with something that ICE CEO Jeff Sprecher said in this interview today. This is such a massive tailwind for Abaxx that I don’t believe is understood or factored into our market and valuation at all. I’ll go over this more in our quarterly call this week.

..First off, I have nothing but respect for Mr. Sprecher and what he’s built. It’s nice to see an exchange founder with this mainstream airtime. And he’s been nothing but encouraging and nice to me in our few brief interactions.

But our tech approach and vision is very different. When talking about 24/7 markets and the global distribution networks for capital markets over the internet (the shared goal and endpoint for both companies, both in pilot and rollout phase now), this is what Jeff says when talking about ‘blockchain’:

“..we’re not only going to have to change our technology, but we’re going to need to change how our legal contracts work, how things settle, what happens in bankruptcy”.

Jeff perfectly articulated the impossible part out loud, which we’ve been talking about extensively over the past year. Not only does the “blockchain #RWA vision” require worse technology systems to be distributed and sold into all institutions, adding more tech operations and more layers to the existing system (more fragility) to realize this flawed-vision of centralized ‘bearer token finance’—but we’ll also need to rewrite laws (in harmonization!) across the whole global daisy chain of distribution to not have solvency gaps? For what end goal, to maximizes the value of blockchain “bearer tokens” held by crypto funds, to try and backfill the the pre-sold bag of under-utilized “blockspace markets” for an exploding number of pseudo-decentralized (but legally reversible) L1/L2 surveillance-chains with no actual business moat?

I’m very surprised that a fellow engineer, Mr. Sprecher, thinks that replacing both global financial institutions core tech, and all global legal frameworks, is the optimum path here.

At Abaxx, we have a totally different engineered path to the reach the same end state (24/7, global, digital), while needing no replacement infrastructure and no new laws.

Why? How? Our core primitive is decentralized and resolvable [private] digital identity, and real-time #LegalFinality, which is always more important than #LedgerFinality when Law (🪨) beats Ledger (✂️); as securities and asset laws can always overturn ledgers with RWA. And our systems work with existing ledgers (centralized, regulated, private blockchains, public blockchains, any), and existing laws.

Can’t wait for the market to finally see and understand this about what Abaxx Tech has built with 🆔 (and 🔜 at agentic operating speed with Agents ) in the second half of the year as our systems go live. Wow, so glad I watched this.

#29ers $ABXX #MarketOS

🇺🇸 As America approaches its 250th anniversary, the New York Stock Exchange celebrates 234 years.

“The history of this country and the history of the New York Stock Exchange are completely intertwined.”

Intercontinental Exchange CEO Jeffrey Sprecher joins Sunday Morning Futures with @MariaBartiromo to discuss the future of America’s capital markets 👇 @NYSE @ICE_Markets

3

27

113

23,090

Tee G retweeted

May 1

One small step for 🆔 , one giant leap for agent kind. 🌖

This is the start, a first library release (more to come) of what could be the biggest moon shot within @abaxx_tech. I founded Abaxx ~eight years ago with digital identity at the core, the long horizon Thing that every other Thing gets us to. Turns out our architectural vision for humans was even more important for agents (the ones acting for humans, with protecting your data with accountability, skin in the game).

Digital Identity — 🔑 to unlocking the next stage of AI (a16z)

Digital Identity — 🔑 to unlocking real time token finance (Blackrock)

Sovereign Identity — 🔑 to reversing the enshitification of the internet for the next generation (Abaxx)

Now let’s put these libraries on a Tilt-A-Whirl. #29ers Please Retweet far and wide!

#MayDay #WorldBuildersOrBust $ABXX

May 1

Meet Agents

Our first open-source release to develop the next generation of technology that will build smarter markets.

Agents are moving from tools to actors, initiating and coordinating actions across systems as delegated extensions of users and institutions.

14

68

175

78,043

Tee G retweeted

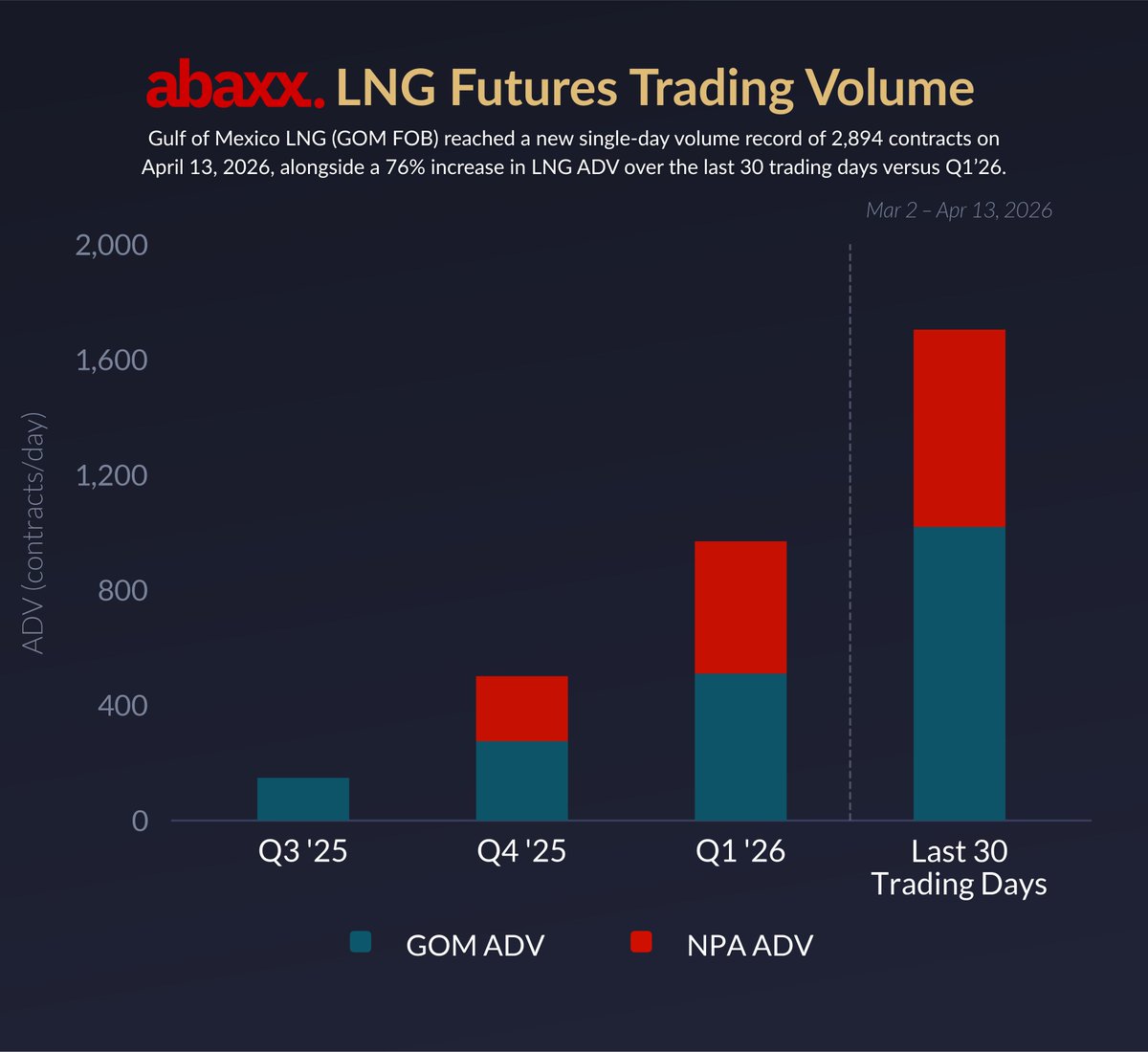

Apr 13

Gulf of Mexico LNG (GOM FOB) reached a single-day volume record of 2,894 contracts, with LNG ADV (GOM FOB and NPA DAP) increasing 76% over the last 30 trading days versus Q1’26.

8

70

1,780

Tee G retweeted

Apr 10

Yes, and in the pilot where they were involved, the FinServ lead said he wanted to quit and join abaxx, asked how he can invest if we ever spun out the tech (we get that reaction a lot on the tech side) 😂

..but yeah, we think about the integrators and scaleable distribution strategies for sure.

2

7

75

5,837

@abaxx_exchange new records today in overall volume 37,343 contracts and #LNG including pricing 5,552 contracts or almost 16 cargoes including 2,786 lots of NPA, fast closing in on JKM.

@abaxx_exchange

@Smarter_Markets

2

13

73

2,778