#Bitcoin = ∞/21M | #HODL | Opt out of the Cantillon Effect | Pharmacist | youtu.be/3Rnqst5qCgA

Joined February 2009

- Tweets 20,612

- Following 5,372

- Followers 2,750

- Likes 138,358

5,002 Photos and videos

₿ased UTXO⚡️ ∞/21M retweeted

Dear bitcoin podcasters:

I understand that you have some difficulty understanding math and don’t like reading long things. So I’m going to keep this very simple:

If long term bitcoin:native price appreciation is:

>>11-13% $MSTR / $ASST will outperform $BTC

~ 11-13% $MSTR / $ASST will roughly equal $BTC

<< 11-13% $MSTR / $ASST will underperform $BTC

(If $BTC fails catastrophically then $MSTR / $ASST will fail catastrophically.)

This is because when you can borrow money for less than the average return of the asset you purchase with the money, you outperform simply buying this asset with the cash you have on hand. This concept is called leverage and it is how mortgages work.

Thank you for your attention to this matter.

18

22

370

21,647

₿ased UTXO⚡️ ∞/21M retweeted

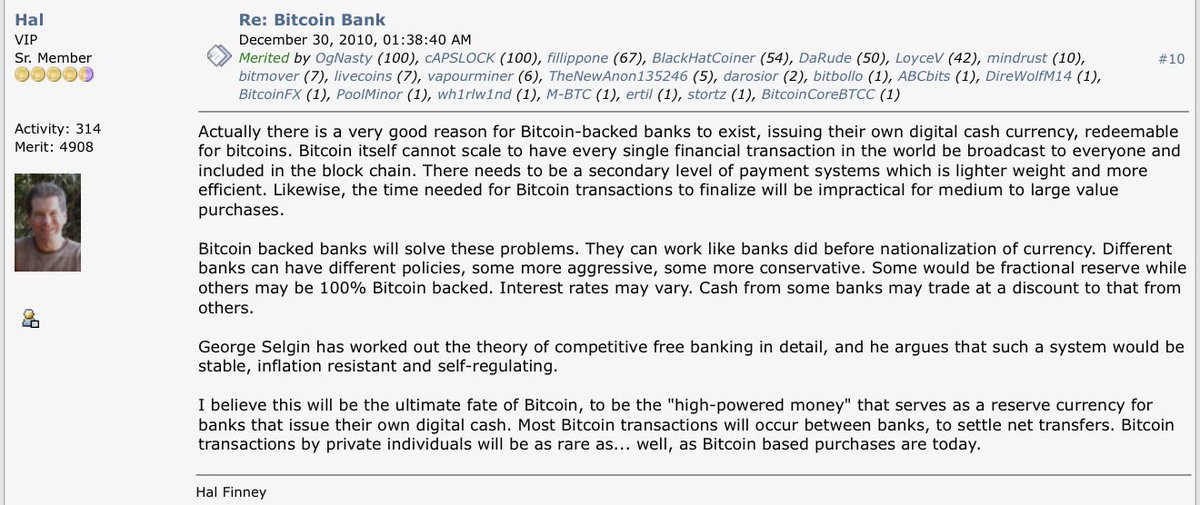

Bitcoin, Digital Credit, and Digital Money:

@saylor is proposing building a full Digital Asset Stack on top of $BTC in existing capital markets. This is what he and @phongle have been doing with $MSTR.

Expanding this model would naturally involve banks, corporations and individual holders. All "peers" of different scale in the P2P Network that is $BTC. Nothing that runs contrary to the $BTC ethos.

As much as this may aggravate people, this isn't that far off from what Hal Finney himself proposed. The world transacts on top of $BTC, with fewer individual $BTC settled transactions because:

"Bitcoin itself cannot scale to have every single financial transaction in the world be broadcast to everyone and included in the block chain."

Think of a layered architecture that transforms BTC's natural volatility profile into a spectrum of tailored financial products that serve every type of investor and use case.

The TL/DR is that BTC remains the unchanging base layer while trad-fi creates the layers on top of it (the "rails").

49

49

467

93,094

₿ased UTXO⚡️ ∞/21M retweeted

Michael @Saylor believes Bitcoin can 500x.

The more interesting question is how.

At @BTCPrague, we discuss whether Bitcoin’s path forward is driven primarily by adoption and savings, or by capital flowing in through global credit markets.

We also tackle mNAV, concerns around dilution, and Bitcoin per share.

TIMESTAMPS:

00:00 Why Michael Saylor calls this the most exciting year in Bitcoin history

2:34 Setting the record straight: why Strategy sold 32 Bitcoin

3:55 How Strategy works like a reserve bank built on Bitcoin

6:58 How the company turns Bitcoin gains into payouts - without the tax hit

9:12 Answering the short sellers

11:40 Why a better credit rating could put Strategy in the S&P 500

13:27 Saylor responds to his critics on X

14:47 The constant balancing act: chasing growth without taking on too much risk

16:22 The balance sheet explained: what the company actually owes

20:56 What “digital credit” really means, in plain terms

24:06 What it really costs to raise money

27:31 The trade-off: more Bitcoin per share vs. more risk

41:07 Why idealism alone won’t get Bitcoin there - but big money can

49:42 The “AI summer” pulling money away and when it flows back to Bitcoin

95

159

982

239,189

₿ased UTXO⚡️ ∞/21M retweeted

244

444

2,747

555,094

₿ased UTXO⚡️ ∞/21M retweeted

Jun 16

Monetary Manichaeism: treating the TradFi world as ontologically evil rather than as fallen material that can be captured, redirected, and converted into bitcoin demand.

9

3

63

5,411

₿ased UTXO⚡️ ∞/21M retweeted

Call me crazy, but I think parents should determine what their teenagers do online rather than the government.

And that governments shouldn't use system-level ID checks to identify and monitor everything.

380

865

8,803

204,963

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

A couple of reasons:

- they can't ban kids of any age unless they require us all to prove how old we are. So this is a backdoor way to introduce digital ID or verification for us all to use the internet, effectively.

- this ban will be trivially easy to bypass, but will likely drive kids to use far less safe and less regulated platforms that do not or cannot comply, likely beyond the scope of existing parental controls, and will likely lead to far more harm from dark corners of the deep web than they suffer from Facebook or TikTok

11

14

118

7,979

Jun 15

Proof of node

Most MSTR holders still wouldn't know what a Bitcoin node is even if one hit them in the head. Hence, they have zero voice when it comes to Bitcoin forks. If you read the BIP, you'd know why it is temporary

2

98

Jun 15

Jun 15

Incredible.

CEO of company takes time to post a frankly excellent and incredibly thoughtful (and polite) reply to do-nothing worthless Bitcoin podcaster explaining in detail where he is wrong in his financial modeling.

Bitcoin podcaster chimps out and refuses to read it.

I view Bitcoin like oil.

We have on one hand people like @saylor and @colemacro who are like Rockefeller. They recognize the potential of the commodity to revolutionize finance and society, and they are building the future with it.

We also have - unfortunately - ignorant people like Parker, who are like the Beverly Hillbillies of Bitcoin. They stumbled across the commodity by sheer luck, not because there is anything special about them. But they gained a following because they looked like geniuses in retrospect - and they think that it’s like some magic talisman that’s just as valuable sitting in the ground as it is distilled into fractions and distributed across the financial system.

Sadly, these people will only succumb to further derangement as their intellectual capabilities are tapped out trying to understand basic financial math.

1

2

24

31,696

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Incredible.

CEO of company takes time to post a frankly excellent and incredibly thoughtful (and polite) reply to do-nothing worthless Bitcoin podcaster explaining in detail where he is wrong in his financial modeling.

Bitcoin podcaster chimps out and refuses to read it.

I view Bitcoin like oil.

We have on one hand people like @saylor and @colemacro who are like Rockefeller. They recognize the potential of the commodity to revolutionize finance and society, and they are building the future with it.

We also have - unfortunately - ignorant people like Parker, who are like the Beverly Hillbillies of Bitcoin. They stumbled across the commodity by sheer luck, not because there is anything special about them. But they gained a following because they looked like geniuses in retrospect - and they think that it’s like some magic talisman that’s just as valuable sitting in the ground as it is distilled into fractions and distributed across the financial system.

Sadly, these people will only succumb to further derangement as their intellectual capabilities are tapped out trying to understand basic financial math.

Jun 15

Too long didn't read all that. The stock should trade a discount to NAV given the incremental risk and because each investor can buy the identical underlying asset with incremental risk. We can come back to this and see who was right.

But again my point was about whether the shareholder base that plowed into Strategy common equity has a good understanding of bitcoin and if they are good at pricing risk. The existence of the scale suggests otherwise.

And I'm just recommending people do exactly what you are doing. Sell the premium in the stock, buy bitcoin.

21

12

227

26,662

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Addressing in-fighting in bitcoin

74

47

389

85,330

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Bad information makes an antifragile company stronger -

Creates awareness.

Forces clarity.

Reveals misconceptions.

Stress-tests the thesis.

Strengthens long-term holders.

Attracts people who do the work & discover the truth.

Thank you to those spreading bad information. $MSTR

20

30

266

10,632

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Bitcoin Capitalism — my keynote from @BTCPrague 2026.

Digital Capital is the foundation for Digital Credit, Digital Money, Digital Yield, Digital Equity, and a universe of Bitcoin-backed products and services.

Timestamps:

01:37 - The Four Bitcoin Ideologies and the case for Bitcoin Capitalism

03:29 - Bitcoin as Digital Capital: thousand-year capital with a half-life of infinity

06:12 - Bitcoin network snapshot and ~68% dominance

07:41 - What is money? The Austrian view, the conventional investor view, and “Bitcoin is money, everything else is credit”

09:21 - Digital Money and Digital Credit: bitcoin-backed products for fiat-facing investors

11:28 - Digital Credit: an ~$11–12B asset class that was zero 12 months ago

14:54 - Bitcoin’s opportunity: $1T of bitcoin vs. $1,000T of global capital

15:43 - The 10-dimensional model for reaching stranded capital

16:44 - 1) Asset types: commodities, equities, credit, derivatives, real estate, money, and tokens

18:07 - 2) Capital functions: store of value, appreciation, income, collateral, and payments

19:29 - 3) Custody: self-custody, banks, custodians, broker-dealers, prime brokers, and exchanges

20:34 - 4) Jurisdictions: 664,000 legal and regulatory environments for capital

22:03 - 5) Distribution networks: banks, exchanges, payment networks, and $156T controlled by wealth advisors

23:13 - 6) Account forms: retirement accounts, brokerage accounts, insurance policies, treasuries, and trusts

24:51 - 7) Risk: market, currency, duration, regulatory, credit, technical, security, theft, and counterparty risk

26:03 - 8) Liquidity: transforming $350T of illiquid capital with liquid digital assets

28:02 - 9) Investors: banks control ~$200T and need compliant bitcoin-backed products

30:09 - 10) Product characteristics: fixed rate, floating rate, leverage, callability, fees, and structure

30:45 - The 10x10 matrix for channeling global capital into Bitcoin

31:19 - How $10–20T of capital could expand Bitcoin into a $100T network, moving from $70K to $700K to $7M per bitcoin

32:10 - Bitcoin Capitalism as a Darwinian market: winners, challengers, failures, and 1,400 companies tracked by Strategy

34:53 - Existing bitcoin-backed products: @Trezor, @Unchained, @Fidelity, @Fold_app, @Tando_me, @Relai_app, @CashApp, @HodlHodl, @AnchorWatch, @Meanwhile, $IBIT, $STRC, and $MSTR

40:03 - Digital Capital, Digital Credit, Digital Money, and Digital Yield competing with traditional capital markets

41:03 - Digital Money and Digital Yield: better stablecoins and higher-yield bitcoin-backed products

47:27 - 3 ways to participate: savers, investors, and innovators

49:19 - The aluminum airplane analogy: people buy the product, not the commodity underneath

52:29 - Build a ₿ridge to connect $BTC to the global capital markets

53:42 - 10,000 products, 10,000 needs, and 100,000 corporate efforts to change the world

362

630

4,191

226,184

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Parker, this response actually proves the point I was making.

The entire purpose of correcting your framework was to help you explain exactly this issue correctly.

You are taking a Bitcoin treasury company whose common equity is structurally designed to have positive beta to Bitcoin, isolating a period that begins near Bitcoin’s late-2024 peak, and then highlighting that the common equity underperformed Bitcoin during a period where Bitcoin moved from that peak into a bear market.

Of course it did.

That is not a refutation of the thesis. That is how positive beta works.

If you isolate a period where Bitcoin peaks and then enters a drawdown, you should expect a company designed to amplify Bitcoin exposure to underperform Bitcoin during that specific period. That is not some surprising discovery. It is the expected behavior of the structure.

The entire thesis of Strategy, and the broader thesis behind what Strive is pursuing, is not that common equity will outperform Bitcoin over every arbitrary short-term interval. That has never been the claim.

The thesis is that over a long enough time horizon, if Bitcoin continues to go up and to the right, a company using the right structure can amplify Bitcoin exposure and outperform Bitcoin through that structure.

That structure matters. The ability to issue long-duration, structurally attractive liabilities against Bitcoin exposure matters.

That is the point.

As Bitcoiners, we are supposed to understand low time preference. We are supposed to zoom out. We are supposed to understand that cherry-picking a window from a local peak into a drawdown does not tell you whether the strategy works over the relevant time horizon.

Since Strategy began its Bitcoin strategy in 2020, the total return of the common equity has outperformed Bitcoin. That is the cleanest long-term test of whether the structure has worked.

Even in your original 2024 framing, the proper analysis on a total return basis for a single share showed outperformance. Then, when you shifted to a weighted average issuance argument, the issue became whether you were doing that analysis consistently.

You were not.

If you want to analyze common equity issued over time, you cannot simply take the weighted average price at which equity was issued and then compare it to Bitcoin over a return period that begins before much of that equity existed.

That was the original flaw.

You need to make the entire analysis internally consistent. If you use a weighted average equity issuance price, then you also need a weighted average issuance date. You then need to compare that to Bitcoin over the comparable cash-flow-weighted time period.

In other words, you need to match the dollars raised, the dates those dollars were raised, the price at which equity was issued, and the Bitcoin price over the same comparable timing.

You cannot weight one side of the analysis and then use an unweighted or mismatched start date on the other side.

That is not attribution. That is a framework error.

Your revised point appears to be moving closer to the right framework, but the conclusion you are drawing is still not the devastating critique you think it is.

The TLDR of your argument is now effectively this:

If you buy amplified Bitcoin exposure near a Bitcoin cycle peak, and then Bitcoin enters a bear market, that amplified Bitcoin exposure may underperform Bitcoin over that selected period.

Correct.

That is what should happen.

Again, that is not a refutation of the strategy. That is the expected outcome of positive beta in a Bitcoin drawdown.

The real question is not whether common equity can underperform Bitcoin over a cherry-picked period from a local peak into a bear market. The real question is whether the structure is attractive over the long run for investors who are bullish on Bitcoin and willing to maintain a low time preference.

My view is yes.

If you are bullish on Bitcoin over the long run, then a company that uses long-duration liabilities, digital credit, and a capital structure designed to accumulate and amplify Bitcoin exposure can be attractive.

If you are not bullish on Bitcoin, or if you are evaluating it over short windows from local peaks into drawdowns, then of course you may not like it.

That is fine.

But those are different debates.

What is not fine is presenting a flawed attribution framework as if it proves the strategy has failed.

Parker quote-tweeted my earlier response, and there have now been several replies across this discussion. I would strongly encourage people to read the full exchange carefully, and responses between Parker and @CJ_Bitcoin.

I think these back and forths are illuminating because it shows the core deficiencies in Parker’s analysis: inconsistent time periods, mismatched frameworks, selective windows, and conclusions that do not actually follow from the math being presented.

I do not think that is malicious. I do think it is analytically wrong.

And when the analysis is wrong, the conclusion becomes misleading, even if that was not the intent.

To be very clear, I am obviously a fan of people buying Bitcoin directly and putting it in cold storage. That is the purest expression of the asset.

But that does not mean every other structure is invalid.

A Bitcoin treasury company is a different instrument. It has different risks, different return drivers, different capital structure dynamics, and different upside and downside behavior.

If you want pure Bitcoin, buy Bitcoin.

If you want a structure designed to amplify Bitcoin exposure over time, then you evaluate that structure on its own terms.

But you do not evaluate amplified Bitcoin exposure by selecting a period from a Bitcoin peak into a drawdown and then acting surprised when positive beta works in both directions.

That is the entire point.

The structure is attractive if you are bullish on Bitcoin, understand the capital structure, and have a low time preference.

If you are not bullish on Bitcoin, or if your framework is short-term price comparison from a local high, then you probably will not find it attractive.

But that is a difference in thesis, not proof that the strategy has failed.

Investors deserve a higher-quality conversation than this.

Back to work.

42

43

459

36,689

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

LOUDER for all the people in the back 📢:

“You cannot take a weighted average issuance price across the entire period, then compare returns from the beginning of 2024 as if all of that equity existed on day one.”

1

7

386

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Parker, your framework is still inaccurate, and the conclusion it produces is fundamentally misleading.

To be clear, I do not think you are intentionally trying to mislead people. I think the issue is that the return attribution framework you are using is not internally consistent.

This is also not an isolated issue. Across your commentary on this topic, there has been a consistent pattern of mixing frameworks, comparing unlike metrics, and then drawing conclusions that do not actually follow from the underlying analysis. I do not think that is malicious, but I do think it is a serious analytical problem.

I have done performance and return attribution work for the largest pension fund in the United States, and I have worked with some of the largest and most sophisticated asset managers in the world on exactly this type of analysis. This is not how institutional return attribution is done.

Your claim is that nearly $38 billion of common equity was raised over the period, and that the weighted average price paid underperformed Bitcoin.

But once you introduce a weighted average equity issuance price, every other part of the analysis has to be treated consistently.

That means you also need to calculate the weighted average date of that equity issuance. You cannot take a weighted average issuance price across the entire period, then compare returns from the beginning of 2024 as if all of that equity existed on day one.

By your own framework, most of the equity holders you are analyzing did not even exist at the beginning of 2024. So using the beginning of 2024 as the return start date for that capital is simply the wrong math.

Because much of Strategy’s equity was issued later, and at higher prices, the weighted average issuance date will be pulled meaningfully forward. That matters. A lot.

If you want to build the strongest version of your own critique, the correct analysis would look something like this:

1. Calculate Strategy’s weighted average equity issuance price over the relevant period.

2. Calculate the weighted average issuance date for that same equity.

3. Calculate the Bitcoin price using the same cash-flow-weighted timing.

4. Then compare performance from that weighted average date, using internally consistent assumptions across equity issuance, Bitcoin, and the relevant return period.

That would at least be a coherent, apples-to-apples analysis.

But that is not what you are doing.

What you are doing is taking one metric on a weighted average basis, then combining it with a return period that starts before much of the capital was actually raised. That is not return attribution. It is a mismatched calculation that produces a misleading answer.

The institutional way to analyze this is either to use total return from a fixed start date, such as the beginning of 2024, or better yet, since the inception of the strategy in 2020.

Or, if you want to analyze capital raised over time, use a cash-flow-weighted framework that matches each equity issuance to the correct date, price, and corresponding Bitcoin price.

But you cannot mix the two frameworks. You cannot use weighted average issuance economics on one side of the ledger and a fixed-date return from 2024 on the other side. That is precisely how you get the wrong conclusion.

My view remains that the proper framework is total return over the period, ideally from the inception of the strategy. If you want to use 2024 because that is the period you are focused on, then use 2024 consistently. If you want to analyze equity issuance over time, then cash-flow weight the entire analysis consistently.

Right now, your critique does neither.

That is why I believe your analysis is inaccurate, fundamentally wrong, and misleading. Again, I am not saying that is intentional. I am saying the framework itself is flawed, and the math does not support the conclusion you are drawing.

15

13

173

14,366

₿ased UTXO⚡️ ∞/21M retweeted

For anyone who has been puzzled by the (rightly respected) @parkeralewis claiming that the math of BTCTC valuation should imply a discount to BTC, and who were not able to reproduce the same result in their own financial calculations, here @ColeMacro lays out the misconceptions in the framing being used. Be wary when people talk of "the math" but can't or won't show their calculations. Many such cases.

Jun 15

Parker, your framework is still inaccurate, and the conclusion it produces is fundamentally misleading.

To be clear, I do not think you are intentionally trying to mislead people. I think the issue is that the return attribution framework you are using is not internally consistent.

This is also not an isolated issue. Across your commentary on this topic, there has been a consistent pattern of mixing frameworks, comparing unlike metrics, and then drawing conclusions that do not actually follow from the underlying analysis. I do not think that is malicious, but I do think it is a serious analytical problem.

I have done performance and return attribution work for the largest pension fund in the United States, and I have worked with some of the largest and most sophisticated asset managers in the world on exactly this type of analysis. This is not how institutional return attribution is done.

Your claim is that nearly $38 billion of common equity was raised over the period, and that the weighted average price paid underperformed Bitcoin.

But once you introduce a weighted average equity issuance price, every other part of the analysis has to be treated consistently.

That means you also need to calculate the weighted average date of that equity issuance. You cannot take a weighted average issuance price across the entire period, then compare returns from the beginning of 2024 as if all of that equity existed on day one.

By your own framework, most of the equity holders you are analyzing did not even exist at the beginning of 2024. So using the beginning of 2024 as the return start date for that capital is simply the wrong math.

Because much of Strategy’s equity was issued later, and at higher prices, the weighted average issuance date will be pulled meaningfully forward. That matters. A lot.

If you want to build the strongest version of your own critique, the correct analysis would look something like this:

1. Calculate Strategy’s weighted average equity issuance price over the relevant period.

2. Calculate the weighted average issuance date for that same equity.

3. Calculate the Bitcoin price using the same cash-flow-weighted timing.

4. Then compare performance from that weighted average date, using internally consistent assumptions across equity issuance, Bitcoin, and the relevant return period.

That would at least be a coherent, apples-to-apples analysis.

But that is not what you are doing.

What you are doing is taking one metric on a weighted average basis, then combining it with a return period that starts before much of the capital was actually raised. That is not return attribution. It is a mismatched calculation that produces a misleading answer.

The institutional way to analyze this is either to use total return from a fixed start date, such as the beginning of 2024, or better yet, since the inception of the strategy in 2020.

Or, if you want to analyze capital raised over time, use a cash-flow-weighted framework that matches each equity issuance to the correct date, price, and corresponding Bitcoin price.

But you cannot mix the two frameworks. You cannot use weighted average issuance economics on one side of the ledger and a fixed-date return from 2024 on the other side. That is precisely how you get the wrong conclusion.

My view remains that the proper framework is total return over the period, ideally from the inception of the strategy. If you want to use 2024 because that is the period you are focused on, then use 2024 consistently. If you want to analyze equity issuance over time, then cash-flow weight the entire analysis consistently.

Right now, your critique does neither.

That is why I believe your analysis is inaccurate, fundamentally wrong, and misleading. Again, I am not saying that is intentional. I am saying the framework itself is flawed, and the math does not support the conclusion you are drawing.

2

2

14

2,277

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

Michael Saylor says Bitcoin has “already won.”

So why is Strategy selling $BTC?

In our BTC Prague interview, @saylor responds to critics calling him a hypocrite.

youtu.be/NmYl4dsuXn4?si=5Izs…

42

13

89

48,931

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

this must look like a death spiral if you’re retarded

10

9

345

15,331

₿ased UTXO⚡️ ∞/21M retweeted

Jun 15

What’s more retarded is having Planck time time preference. Ironic considering as Bitcoiners we preach low time preference.

2

1

10

583