USMC 79-82 / 0311 / Conservative. Don’t care for DM’s. Retired

Joined October 2022

- Tweets 16,386

- Following 1,241

- Followers 1,204

- Likes 23,465

47 Photos and videos

The argument that AI labs should be owned by the state because they use the public power grid and rely on national security is a spectacular display of selective logic.

Every single commercial enterprise on Earth runs on public infrastructure! Amazon and FedEx dominate the interstate highway system built by taxpayers. Walmart uses municipal roads and public utility grids for its thousands of stores. Boeing relies on the national security apparatus to protect its intellectual property from foreign states.

We do not nationalize Amazon or take a 75% stake in Walmart because they use the roads. They pay for that infrastructure through corporate taxes, fuel taxes, and commercial utility rates. AI data centers do not get free electricity; they pay astronomical, regulated enterprise rates to energy companies. If using public infrastructure entitles the state to 75% ownership, then the government technically owns the entire S&P 500!!!

1

1

3

67

Bill retweeted

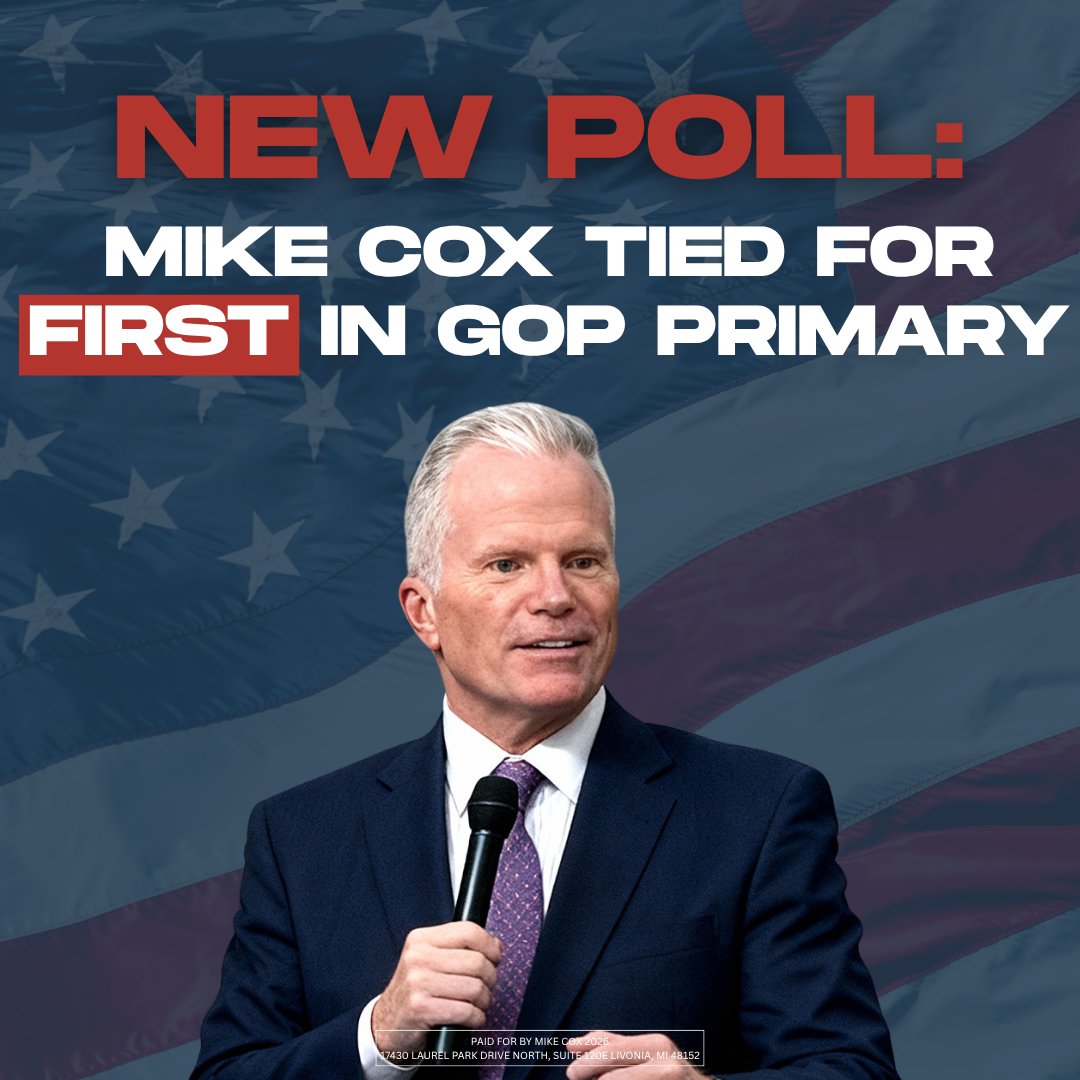

🇺🇸 BREAKING: A new poll shows our campaign is tied for FIRST place in the Republican primary.

Michiganders are rallying behind our campaign because they want a governor who will eliminate the income tax, lower costs, crack down on crime, and fight for working families.

The more voters learn about our record and our vision for Michigan, the more support our campaign earns.

Since March, ours is the only campaign that has gained support in the polls, and we're continuing to climb while others are losing ground.

6

17

59

2,213

Bill retweeted

Jun 11

NEW AD: My dad taught me to never back down from a fight.

That's why I took on the Big Utility Companies trying to jack up rates on customers.

They lost. We WON.

I'm running for Governor because I know we can beat the Lansing politicians, eliminate the income tax, get prices down, and save Michigan, but only if we're willing to fight.

➡️ Check out our new ad out today and join the fight: mikecox2026.com/get-involved

7

22

71

2,017

Bill retweeted

Jun 11

🔥🔥🔥

The difference in the race: lots of candidates talk a big game.

Only Mike Cox has a record of being willing to fight for working families & seniors.

➡️ mikecox2026.com/willing-to-f…

Jun 11

NEW AD: My dad taught me to never back down from a fight.

That's why I took on the Big Utility Companies trying to jack up rates on customers.

They lost. We WON.

I'm running for Governor because I know we can beat the Lansing politicians, eliminate the income tax, get prices down, and save Michigan, but only if we're willing to fight.

➡️ Check out our new ad out today and join the fight: mikecox2026.com/get-involved

2

7

650

Bill retweeted

Jun 10

.@JohnJamesMI is as dishonest as he is selfish.

Lying to voters and misquoting President Trump is exactly what a dishonest, career politician does.

President @realDonaldTrump and Republican leaders asked James to put the mission first and help keep the House Majority.

In classic John James fashion, he put himself first and the team last, then lies to voters to get what he wants. 👇

Jun 10

THREAD⬇️

NEW MISLEADING AD WON'T ERASE @JohnJamesMI RECORD ON TRUMP

John James is spending hundreds of thousands of dollars on deceptive ads, featuring a past clip of @POTUS to falsely imply his support for John James for Governor.

President Trump has NOT endorsed John James for Governor, in fact, he asked James to keep his seat in the House of Representatives to help keep the GOP Majority.

7

18

46

1,477

Bill retweeted

Jun 8

End it, don’t mend it.

Jun 8

*TRUMP’S $100,000 H-1B VISA FEE THROWN OUT BY JUDGE

465

3,853

32,474

770,935

Bill retweeted

Jun 4

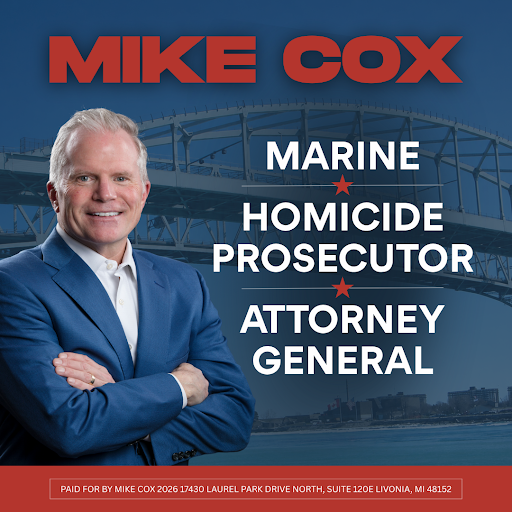

I served as a United States Marine, spent 13 years as a prosecutor, including leading the Homicide Unit in Detroit, and then served as Michigan's Attorney General.

I've spent my career putting criminals behind bars, standing up for victims, taking on powerful interests, and delivering results for the people of this state.

When Michigan needed someone willing to fight, I never backed down. And I never will.

3

26

74

1,156

Bill retweeted

Jun 4

$IREN: Rapidly Rising Cost of BTM Gas Turbine

Gas turbines and associated pipeline and equipment are now 3m-4m/MW based off Wells Farm research from @ShanuMathew93! That's not even including the cost of natural gas. Without a major pipeline or source of natural gas nearby, liquified natural gas is needed which is 15 cents/kWH.

The market has rewarded $BE for producing MWs in the form of fuel cells which are good for 5 years and BE sells them in 10 year service contracts aka fuel cells as a service. Eventually IREN's MWs will be valued too. I mean why pay 4B/GW in BTM Gas Turbine equipment when you can get grid connected power at rates opex same or lower than generating from natural gas in many states?

Margin calculation wise, grid connected datacenter build is 10m/MW so BTM Gas Turbines is an increase of 30-40% on upfront capex which eats directly into profits.

Heavy Redundancy Factor

With a redundancy factor of 30-40% needed, many MWs of capacity can't even be used. Who cares if you have a 1.1 PUE datacenter if you are BTM Gas Turbines? The 1.1 PUE datacenter effectively became 1.1 * 1.4 = 1.54 PUE. And yes it's multiplicative because you need redundancy in the gas turbines for the AUX load like cooling too.

People will figure out this is much more important than the cost of electricity. BTM is a very expensive solution.

I never believed in the tokens/MW metric because really it should be tokens/(GPU HBM) because cost of GPUs and HBM which is still the dominant factor here but BTM screws over any token/MW metric too once you factor in redundancy needed.

Why were Gas Turbines considered before $BE Fuel Cells and Smaller Engines like Reciprocal Engines?

Gas power plants last 25 years. In the case of NBIS's 2.6B for 328MW, BE Fuel Cells are 7.4m/MW for 10 years only. When normalized to 20 lifetime of datacenter, gas turbines are 2.8m/MW-20yrs while BE Fuel Cells are 14.4m/MW-20yrs!

Fuel Cells also have a redundancy factor 31% as NBIS is getting 250MW of usable power and 78MW of the fuel cells are for redundancy. That makes a 1.1 PUE datacenter effectively 1.1 * 1.31 = 1.44!

Smaller engines are in-between cost curve of Gas Turbines and Fuel Cells which is why NBIS attempted to use Bergen Cruise Ship Engines before they switch to $BE Fuel Cells.

Impact on IREN

Market doesn't reward IREN for hoarding GWs. When IREN converts the GWs to compute and the cost effectiveness of grid connected power over BTM Gas Turbines or Fuel Cells is apparent, IREN will be rewarded. Jane Street Algos and Wall Street Analyst rewards hard metrics like revenue, margins, and profit, not capacity to be built in the future like MWs.

IREN is seeing painful delays now on GPU deliveries which back up their entire datacenter bring up schedule. On the backend, however, having this huge power portfolio will allow IREN to build out the fastest unburdened by BTM buildout time on top of DC buildout time.

Thanks to @alanbialo for pointing out this post to me.

May 28

Interesting color from Wells Fargo on an expert call re: BTM:

>"The expert noted equipment costs were ~$2,200 per kW for an aeroderivative turbine and ~$600-700 per kW for a reciprocating engine. Total install costs are north of ~$3,000 per kW approaching $4,000 per kW. Reciprocating engine projects require a high level of insulation (e.g. engine hall) due to noise levels - a factor that drives comparable total costs despite lower equipment-specific costs."

>" Our expert noted redundancy needs to be roughly 40% for BTM data centers to maintain data center uptime, implying a 1 GW data center would require another ~400 MW of power."

10

25

229

60,752

Bill retweeted

Jun 1

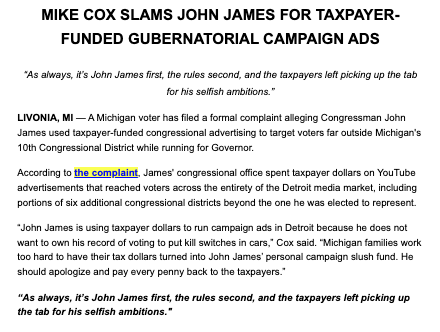

.@JohnJamesMI is using taxpayer dollars to run campaign ads in Detroit because he does not want to own his record of voting to put kill switches in cars.

Michigan families work too hard to have their tax dollars turned into John James’ personal campaign slush fund. He should apologize and pay every penny back to the taxpayers.

Jun 1

🚨FRAUD: "A Michigan voter has filed a formal complaint alleging Congressman @JohnJamesMI used taxpayer-funded congressional advertising to target voters far outside Michigan's 10th Congressional District while running for Governor."

Let's say the quiet part out loud: John James is using taxpayer-funded House communications to run campaign-style ads because his campaign can’t afford to do it itself.

The law is clear: official communications are for constituents, not for bankrolling a candidate’s statewide campaign.

It’s entirely obvious that John James isn’t built for primetime.

After $200 million spent and wasted on two statewide losses, and a disastrous start to his third attempt, it’s time for Republicans to move on from the @JohnJamesMI experiment.

5

44

107

2,299

Bill retweeted

May 30

THIS IS WHY WE VOTED FOR TRUMP‼️

In my opinion, this is still the best pro Trump speech I’ve ever heard, and it was by the very liberal Michael Moore. 👀

277

1,989

7,092

243,835

Bill retweeted

May 29

$IREN: What to Monitor in 2026

Revenue

No doubt $IREN is rich in power, what $IREN investors need to focus on is revenue. The demand is certainly there, it's about getting GPUs online. Even the rate at which $IREN can sign contract is bottleneck by getting GPUs online because getting GPUs online derisk your ability to meet timelines to sign the next contract.

So what you see in $CRWV is that at the beginning they were really fast and then started slowing down. At first, a Neocloud will 2x revenue every quarter but then the ramp are bounded by the physical world. The benefit of having alot of power is that you'll be able to keep growing at a high rate until you ran out of power or your colocation provider(s) hits their limits. However, that's not $IREN's challenge. $IREN needs to get it's ramp -> cashflow -> ramp feedback loop going. Getting slow GPUs slowed down the whole ramp as you are doing theory based preparation for your datacenter until you get the GPUs and then problems can be uncovered sequentially.

Benchmarks

2024 was $CRWV's ramp year:

Q4 2023: 116m

Q1: 188.7m ( 62.7% QoQ)

Q2: 395.4m ( 109.5% QoQ)

Q3: 583.9m ( 47.7% QoQ)

Q4: 747m ( 27.9% QoQ)

Q1 2025: 981m ( 31.4% QoQ)

2025 was $NBIS ramp year:

Q4 2024: 37.9m

Q1: 50.9m ( 34.3% QoQ)

Q2: 105.1m ( 106.5% QoQ)

Q3: 146.1m ( 39% QoQ)

Q4: 227.7m ( 55.9% QoQ)

Q1 2026: 399m ( 75.2% QoQ)

What Will Move the Stock

To look what will move Neocloud stocks, I admit that $NBIS has done a fantastic job this year. What $NBIS executed well objectively was:

1. Sign a 12B Meta Contract with 15B Extension Option

2. Back up their capability to fulfill the contract by hitting revenue numbers and critically showing acceleration in revenue growth. Observe how $NBIS Q1 2026 earnings show an acceleration to 75.2% revenue growth.

I monitor the whole industry to figure out what's going on and for $NBIS, I got to give credit where credit is due, $NBIS put up the GPUs and in this market it doesn't matter if you pay colocation or whatever, getting the GPUs up and showing revenue growth is what the market wants to see from early stage Neoclouds.

IREN's Revenue

IREN's ramp was suppose to start in Q4 2025 but really it's Q1 2026 because we couldn't get GPUs delivered on time due to HBM shortgage which snowballed the whole ramp process back.

Using currently delivery guidance, here are my calculations for the next few quarters revenue:

Q1: 33.6m

Q2: 100.8m (200% QoQ)

Q3: 207.6m (106% QoQ)

Q4: 385.4m (85.6% QoQ)

Q1: 843.8m (118.9% QoQ)

Q2: 1454.7m (72.4% QoQ)

Q1 Calculations: Reported in Q1 earnings

Q2 Calculations: PG exited Q1 with 307m run rate (page 19 of 10Q in source 1 - also screenshotted 1st picture) from the financial digging that @_Sgr_A_Star did and should be at 500m run rate by end of quarter. With linear ramp, (307 500/2)/4-qtr = 100m.

Q3 Calculations: 125m from PG and H1 Handoff stated by Dan to be in Q3 which I will take to be July. I'll take August Sept of 124m from H1 so 124m * 2/3 = 82.6m.

Q4 Calculations: 125m from PG; 124m from H1; assuming we get Mackenzie handed half way through the quarter = 432.8/4qtr/2-halfway = 54.1m; assuming we get 2/3 duration of H2 and 1/3 duration of H3 and H4 get's handed over at the very end of the quarter, we only count the 2/3 H2 1/3 H3 = 124m. Sum = 427.1m

Q1 2027 Calculations: 125m from PG, 485m from H1-4, 108.2m from Mackenzie, CF = 40.6m, half duration of Nvidia Childress site = 85m.

Q2 2027 Calculations: 125m from PG, 485m from H1-4, 108.2m from Mackenzie, 40.6m from CF, 170m from Nvidia Childress, 1/2 duration of Block 7-9 is 330.9m, SW1 50MW IT is 195m

Share Price

IREN's ramp started late but having the power supply abundantly clear, means that the ramp can sustain high % growth for longer because power is not the bottleneck.

If IREN can have report 385.4m quarterly revenue for Q4 2026 it will mirror NBIS 399m quarter where most of its revenue was either H100/H200s and bare metal to MSFT with colocation payments so margin are similar. With an SW1 contract in hand, it would match the Meta 12B with potential 15B extension contract NBIS has. In this case, market is giving NBIS an 55B valuation.

Let's give 5B for NBIS 25% Clickhouse stake at 20B next round valuation even though at 15B valuation now. The rest of NBIS's subsidiary the power they secured is rough equal to value of IREN's power portfolio (I know must IREN investors wouldn't make this trade off let's just call this even to make comparisons easy, you can do whatever adjustments you want). IREN Q4 2026 report will be which would be 50B (current NBIS market cap) / 22.89B (current IREN MCap) * 64.07 (current IREN stock price) = $139.95/share. Q4 earnings is early Feb 2027 but IREN also has higher sustain revenue growth rates due to it's power abundance but since Q4 earnings is Feb 2027, let's take 20% of for the time delta between EOY 2026 and earnings report for Q4 2026 to have a target of $111.96 share price for EOY 2026.

The really strong year for IREN will be 2027 as it sustains high growth rate and not be stuck in early ramp pains.

Sources

(1) iren.gcs-web.com/static-file…

35

44

437

55,272

Bill retweeted

May 28

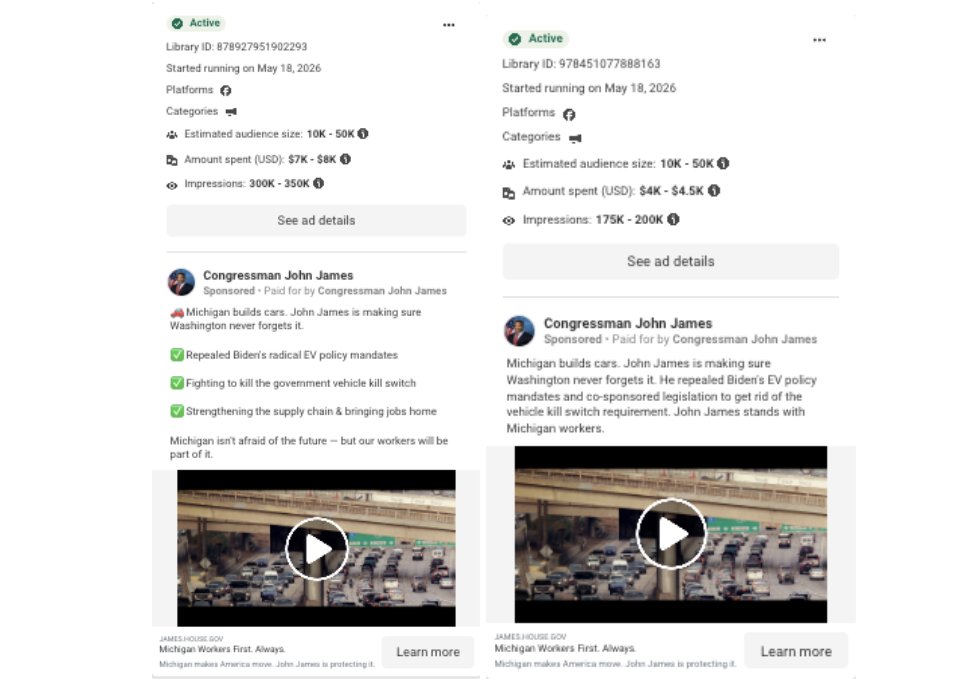

🚨 ICYMI 🚨

@JohnJamesMI is spending TENS OF THOUSANDS of YOUR tax dollars to run advertisements…

bragging on himself for “fighting to kill the government kill switch” which he voted FOR less than 6 months ago.

Check it out for yourself: mikecox2026.com/news/john-ja…

1

10

14

1,911

Bill retweeted

May 27

You can't make this up. @JohnJamesMI votes for the Biden-era "Kill Switch" mandate and then spends YOUR tax dollars to brag about opposing it.

This kind of shameless hypocrisy is what makes people sick of politicians.

Hardworking Michigan families are busting their tails to pay their bills, and John James thinks their tax dollars should be used to bankroll his political damage control operation.

It’s arrogant, self-serving, and an insult to every taxpayer in this state.

May 27

RELEASE: JOHN JAMES SPENDS TENS OF THOUSANDS OF TAXPAYER DOLLARS TO BRAG ABOUT OPPOSING HIS OWN VOTE

Former Michigan Attorney General Mike Cox today slammed Congressman John James for his latest self-dealing stunt, using taxpayer-funded congressional resources to run campaign-style ads attacking the Biden-era “Kill Switch” mandate that James himself voted to protect earlier this year.

3

27

59

3,073

Bill retweeted

May 27

RELEASE: JOHN JAMES SPENDS TENS OF THOUSANDS OF TAXPAYER DOLLARS TO BRAG ABOUT OPPOSING HIS OWN VOTE

Former Michigan Attorney General Mike Cox today slammed Congressman John James for his latest self-dealing stunt, using taxpayer-funded congressional resources to run campaign-style ads attacking the Biden-era “Kill Switch” mandate that James himself voted to protect earlier this year.

1

3

17

2,100

Bill retweeted

May 26

As Attorney General, I took on drug companies that ripped off seniors and taxpayers, recovered hundreds of millions of dollars, and created the first MichiganDrugPrices.com so people could compare prices and save money.

As Governor, I’ll keep fighting to lower costs, hold Big Pharma accountable, and put more money back in the pockets of Michigan families.

4

7

31

880

Bill retweeted

May 26

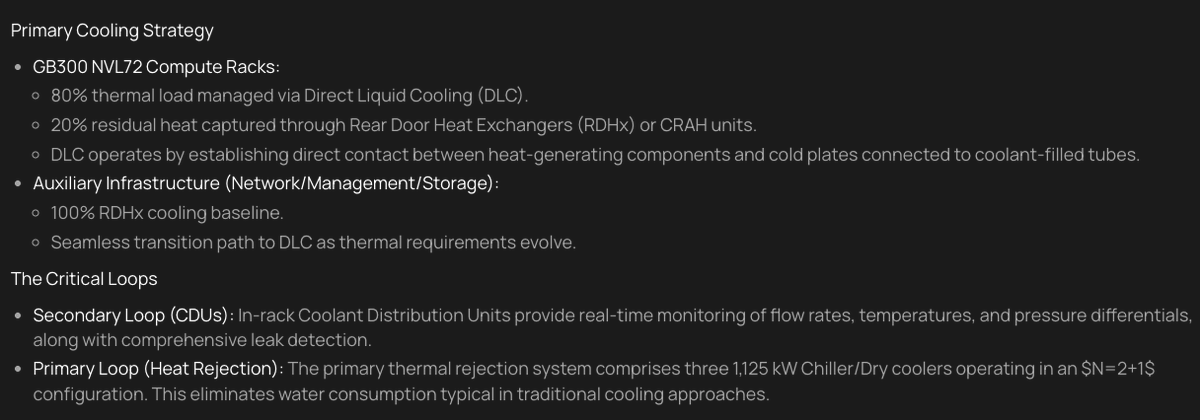

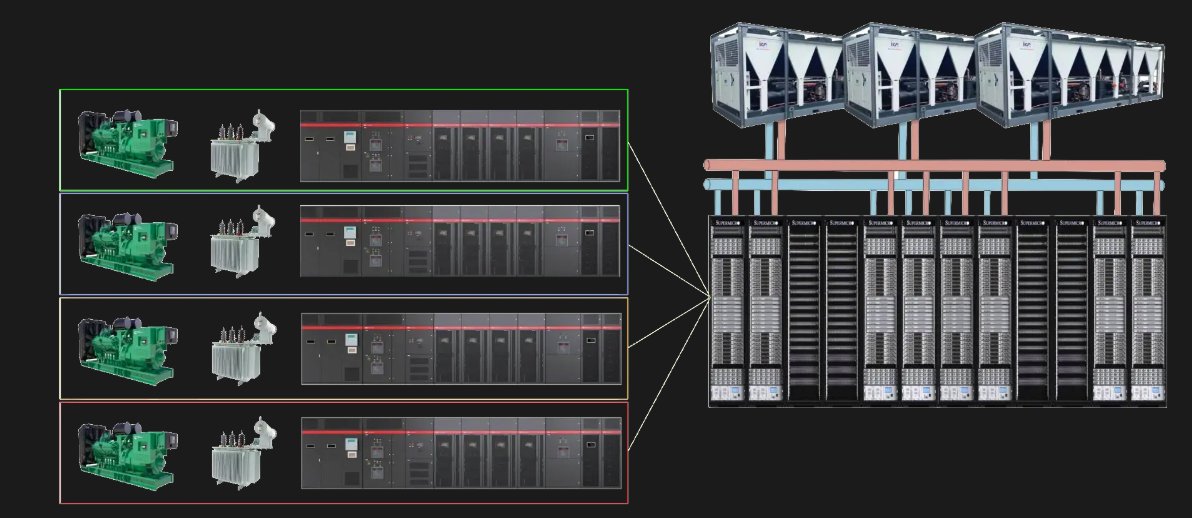

$IREN Hybrid DLC RDHx Cooling

@CernunnosCap posts can a good place to find misconceptions that to be clarified. Here he states that Horizon 1 GB300 is only using Motivair RDHx cooling.

However, Hybrid DLC RDHx Cooling is known to people who actually work in the industry (1). DLC (Direct Liquid Cooling) cools the higher heat GPUs and CPUs. RDHx (Rear Door Heat Exchange) cools the Networking, Management, Storage equipment which has lower cooling requirements.

The design tradeoff is that cold plates have very tiny channels and the to create enough flow volume, the dense cooling fluid needs to move very fast which means high pressure on the pipes. These is the steel pipes you see in the H1 liquid cooling picture. High pressure means more maintenance and operational monitoring overhead to prevent leaks.

Thus for components like Networking, Management, Storage which produce way less heat than the GPUs and CPUs, it's let RDHx do these components because RDHx has lower operational complexity. These are the flexible non-steel pipes you see in the H1 liquid cooling picture and the Motivair sample picture that @CernunnosCap provided.

Any serious engineer can see that $IREN is minimizing operational complexity and maximizing uptime with Hybrid DLC RDHx Cooling. However to the untrained eye, it's easy to cherry-pick one component and not recognize the full system about it.

(1) eliovp.com/building-the-engi…

May 26

$IREN Management is deliberately misleading retail. AGAIN 🚨

CEO @danroberts0101 posted: "Childress. Liquid cooling online."

Reality? It's a glorified air-conditioning band-aid.

Massive credit to @HotAisle for spotting the smoking gun in their own PR photo.

Here’s the brutal technical reality: @jiahanjimliu 😅👇

Those bulky units bolted to the racks are Motivair ChilledDoors.

This is NOT true liquid cooling.

It is Rear Door Heat Exchanger (RDHx) technology.

1. The Silicon Is Still Choking on Air

Inside the racks, the actual GPUs remain air-cooled. Server fans push 140°F exhaust air into the back of the Motivair door (basically a giant radiator). The door cools the room air, not the chip.

2. The Blackwell/NVL72 Math

Air is a terrible thermal conductor. When you’re pushing 1,000W per GPU and 120–132kW per rack, even an RDHx catching the exhaust structurally fails at the silicon level. You cannot run exascale-class AI through air gaps.

This is the ultimate proof of the $NBIS vertically integrated thesis🎯

Nebius isn’t bolting refrigerator doors onto a repurposed Bitcoin mine. As they scale toward their 5GW target, they’re engineering Direct-to-Chip (DtC) liquid cooling from the ground up. Cold plates sit directly on the silicon and pull heat out ~20x more efficiently than air.

One is a legacy crypto facility using RDHx crutches.

The other is a purpose-built AI factory.

$NVDA $VRT $DELL #ai #Datacenters

6

8

145

30,496

Bill retweeted

May 26

$IREN: Financial Model 2.0.0

jiahanliu.github.io/IREN-Com…

Summary

With more data from IREN's Q1 earnings call on buildout cadence (1), I made significant changes to the 1.2.5 financial model so this will be the first 2.0.0 version.

True to the ethos of the original model, the App allows the user to input all relevant variables and expose the App's calculation details in real time so that the user can audit and provide feedback.

Charting

As a corollary to the guidance on buildout guidance, we are able to implement great suggestions from @StockAnalystPro to chart "share price" vs "year". Additionally, the X and Y Axises can be selected so you can plot for example "share price" vs "MWs active" or "Earnings before Tax, SGA" vs "Market Cap".

I only read charts for TA. For FA, I'm always read numbers and never charts so there's probably improvements / suggestions that can be applied to improve the charting.

GPU Pricing Improvements

Previously I did improvement as a percentage of contract topline. Thanks to @GlobalCollapse for pointing out that's non-intuitive. I removed the odd mechanism completely and provide a flat GPU pricing for different years. For example I have "B300 - 2025 Pricing" which corresponds to both the unit price and hourly rate and "B300 - 2026 Pricing" correspondingly.

The default GPU pricing are either direct IREN datapoints or linearly extrapolated as described below.

Linear Extrapolation

I do mostly linear extrapolation. For example in the case of GPU pricing, IREN always gives GPU pricing included servers, Inter-rack Networking, cabling costs while publicly available figures are per GPU or per rack. To get IREN's all-in pricing for Vera Rubins I calculate = (IREN's All-In GB300 Price in 2025) * (Market Per GPU Vera Rubin in 2026) / (Market Per GPU GB300 in 2025).

Dilution

$IREN does Convertible Debt for their Datacenter Capex and GPU Backed Debt for their GPUs. Both the datacenter capex and GPU capex are subtracted off revenue before calculating "Earnings before Tax, SG&A". In practice this is equivalent to $IREN using revenue to pay off the convertible debt before it matures. Other Neoclouds like $NBIS also issues convertibles debt since it doesn't immediately count as dilution and can be paid back in cash. CRWV has more corporate debt which has higher interest rate but non-negotiable cash redemption.

On top of that I count 10% dilution per year up to 40% in 2029 to account for slippage in buying back convertibles even with the insurance that IREN buys and cost of site works, misc. In 2030 , cashflow should be strong enough so dilution stays at 40%.

Stock Price

The 2026 ARR supports a stock price of $94.63 while 2027 ARR supports $236.44 even though 2027 having lower PE and more dilution accounted for. This is because IREN has become a priority partnered of Nvidia and will get GPU deliveries that corresponds to their full buildout cadence with buildout guidance of 1210MW by 2027, a big jump from 480MW in 2026.

Important to note is that 2027 buildout will start with contracts signed in 2026 so in H2 2026 we may see partial pricing in of 2027 buildout as contracting gives market confidence on the supply side and concrete pricing.

Delays

IREN's build out cadence is bottleneck by GPU deliveries. Full system test of liquid cooling can only begin once the GPUs arrive so late GPU deliveries means late triaging of liquid cooling bugs. Then stress test networking scripts can only be run for long amounts of time after liquid cooling system is fully validated.

As you can see there is only so much theory preparation you can do. In engineering, debugging the real hardware is a process with many sequential locks.

Other

I'm pretty busy these days so my commentary is incomplete but number savy people like @_Sgr_A_Star, @GyujinAAIG might be able to good commentary on numbers. @_Sgr_A_Star has a great model for very zoomed in tracking of earnings financials that can probably validate or invalidate some elements of my model. I welcome feedback from everyone as that's the point of this open sourced model.

22

41

300

73,450

Bill retweeted

May 15

No Trump judges, no voter ID SAVE Act, 50 bills already passed by the house in limbo.

Pardon my language, but this guy is a worthless piece of shit. He’s worse than a grifter Democrat. Fetterman has done more for the Republican platform than this weasel. Treacherous rat.

8,020

44,382

136,742

919,849