Joined September 2021

- Tweets 3,211

- Following 261

- Followers 11,380

- Likes 1,995

457 Photos and videos

Pinned Tweet

Jun 1

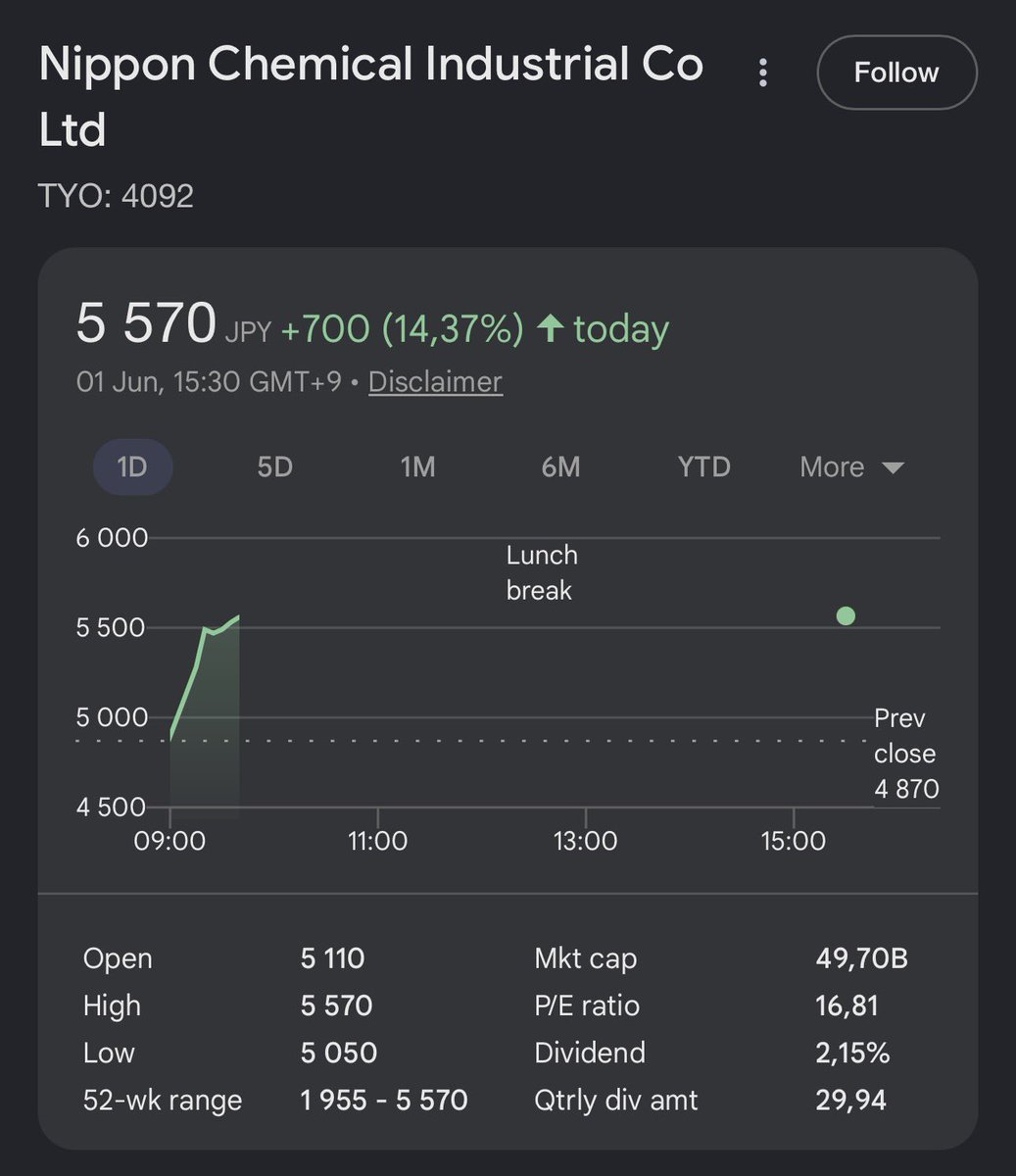

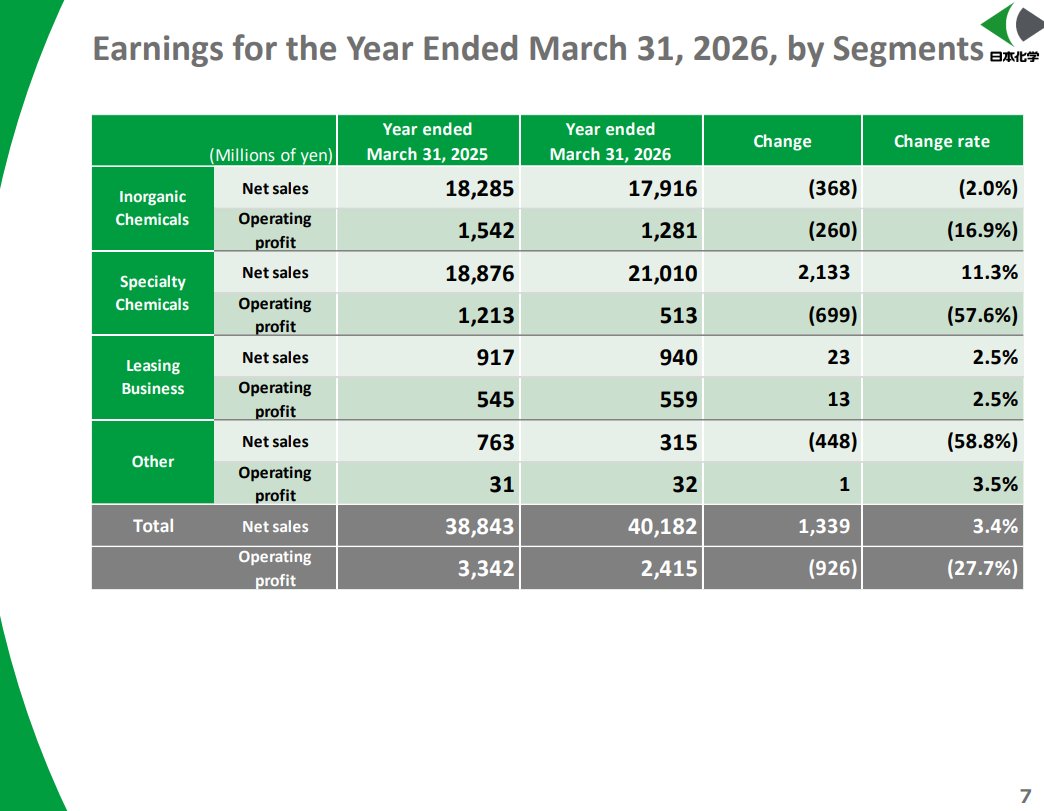

Nippon Chemical might be a superior play to Sakai Chemical for exposure to MLCC materials.

Electronic Ceramic Materials (materials for MLCC) is 25% of total revenue.

But the segment its inside (specialty chemicals) saw operating profit dive even amidst a 23% YoY increase in Electronic Ceramic Materials.

The drop in operating profit was caused by increased battery materials, some once off inventory costs, restructuring.

If we assume (big ask) that they achieve a similar operating margin to Sakai's own Electronic materials segment - 20%

Then in 2027 on a revenue of 12,000(mYen) (my own estimate) for the segment could produce a 2400 operating profit. For just that segment.

Nippon's entire year end operating profit 2026 was 2400.

It would take their EV/EBITDA from 8 to 4 in 2027 if price remained constant.

2

14

97

21,917

Explains the lag in the MLCCs material producers.

Numbers will start hitting their books when tools installed start increasing capacity.

We are early.

Sakai Chemical

Nippon Chemical

>>MLCC Industry Faces "Longest Shortage Cycle in History"… Supply Deficit Expected to Persist Beyond 2027

- Major Taiwanese MLCC makers—Yageo, Walsin, Holy Stone, and PDC—are strongly upbeat on the industry outlook, driven by AI demand. The industry believes this shortage could surpass the 2018 passive component supercycle.

- Walsin in particular projected that the MLCC shortage could persist beyond 2027. The company expects demand to rise even further once AI PCs and AI edge devices—markets far larger than AI servers—begin to proliferate in earnest.

- Yageo's book-to-bill (BB) ratio has already moved above 1.3x, and the company is responding to rising orders by ramping line utilization and clearing bottlenecks.

- That said, the pace of capacity expansion is constrained by equipment shortages. According to Holy Stone, lead times for high-end MLCC production equipment run 1 to 1.5 years, making capacity additions difficult. Holy Stone expects capacity to grow 20~30% YoY this year and a further 30~40% in 2027, but warned that next year's supply shortage could in fact intensify.

- Walsin is likewise tripling CAPEX this year and pursuing capacity expansion for a second consecutive year, but noted that lead times from Japanese equipment vendors run 6 to 12 months, making it hard for supply growth to keep pace with demand. AI infrastructure demand, in its view, is only just beginning.

2

3

35

6,517

Jun 13

Fable getting taken down and nerfed makes me even more bullish AI

4

22

2,352

Jun 12

아주 흥미로운 한국 주식을 하나 찾았습니다.

경쟁사들과 비교해 보면 이 회사는 현재 주가의 3배 수준으로 평가받아도 충분하다고 생각합니다. 게다가 재무 지표도 경쟁사들보다 더 좋은 편이라, 지금의 주가는 정말 말이 안 될 정도로 저평가되어 있습니다.

물론 이렇게 싼 데에는 나름의 이유가 있었습니다. 하지만 그 이유들도 빠르게 바뀌고 있습니다. 과거에는 수동적인 주주였던 행동주의 투자자가 이제 훨씬 더 적극적인 태도를 보이고 있기 때문입니다.

저평가의 원인들이 빠르게 사라지고 있고, 이 회사는 역사상 가장 큰 순풍 속에 놓여 있습니다.

조만간 이 종목을 공개할 생각이라 정말 기대가 큽니다.

문득 제 팔로워 중에 한국 분들이 얼마나 계신지 궁금하네요. 한국인이시라면 아래에 댓글 남겨주세요!

5

9

2,415

Jun 10

There is really nothing to signal slowing in the AI expansion.

This is just a correction from some stocks being screamingly overvalued.

But the fundamentals march on:

TSMC: Jan–May 2026 30.0% YoY

China is preparing to spend ~2 trillion yuan (~$295bn) over five years building a nationwide network of interconnected AI data centers - they will probably need to spend a lot more in the future to keep up.

Fujikura CEO Naoki Okada said the company is on track to beat its outlook thanks to sustained AI datacenter fiber-cable demand and a plan to raise prices.

SK Hynix Plans to double memory capacity over the coming half-decade; says deficit could last till 2030 and "will do whatever it requires" to fund wafer expansion.

2

3

23

2,816

Jun 5

Nippon has a bigger “electronic materials” segment - which is mostly MLCC materials.

Bigger exposure than Sakai

And cheaper.

Operating margin from that segment was also depressed due to other things like battery materials that get lumped into it.

I expected towards the end of the year and next year we see that segment correct drastically

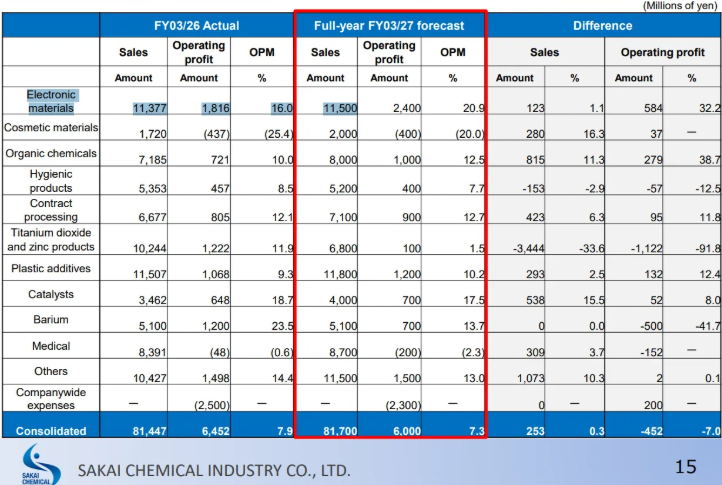

Sakai Chemical 4078 seeing delectric materials used in MLCCs for AI data centers 2x-3x in revs, per transcript. Electronic materials are 10% of total sales, around 20% segment margins. Trades around 15x ev/ebit and 1x p/b, with Zennor (9.3%) expected to make proposals to mgmt.

2

2

18

3,205

Jun 5

Hello Nippon Chemical.

Sakai Chemical 4078 seeing delectric materials used in MLCCs for AI data centers 2x-3x in revs, per transcript. Electronic materials are 10% of total sales, around 20% segment margins. Trades around 15x ev/ebit and 1x p/b, with Zennor (9.3%) expected to make proposals to mgmt.

1

6

1,995

Jun 3

What happened to the everything bubble?

Did it just merge with the AI bubble?

1

6

2,158

Jun 3

Excuse me?

Tencent at PE 15?

EV 10.2x

Has the market just forgotten about Chinese stocks?

87

10

334

100,762

Jun 2

Orwell incoming.

Jun 2

The White House issued an executive order on advanced AI innovation and security.

The order directs federal agencies to prioritize AI-enabled cyber defense across national security, defense, and civilian government systems.

It also calls for an AI cybersecurity clearinghouse to coordinate vulnerability scanning, validation, patching, and remediation with industry and critical infrastructure operators.

The order creates a voluntary framework for frontier AI developers to work with the government on classified cyber benchmarking and pre-release model access, while explicitly saying it does not create mandatory licensing or preclearance for new AI models.

1

7

5,150

Jun 2

Nippon Chemical!

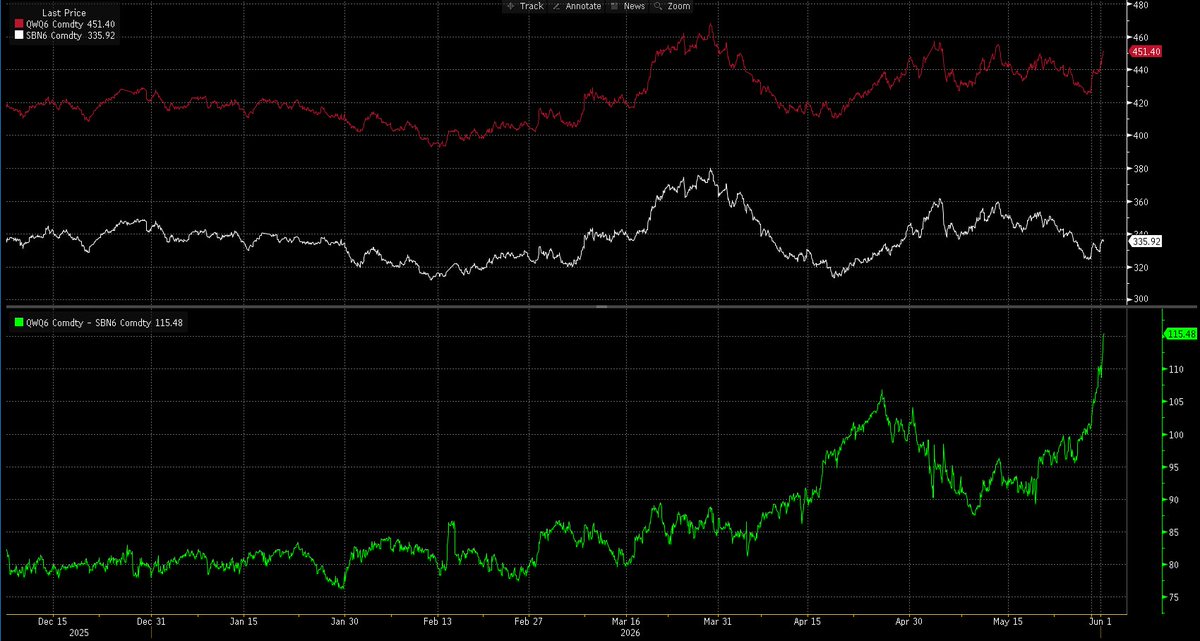

Sakai Chemical 13% today.

Nippon Chemical -3%

I think the market is into Sakai Chemical because it's been profiled on X a lot.

Nippon Chemical hasn't been mentioned as much by big accounts, but it honestly looks like it could be a better play because:

- Cheaper P/B Ratio

-Possibly higher MLCC materials exposure.

Operating Profit got hit by once-offs which hides the growing MLCC Materials Operating Profit in the segment:

-"Absence of the positive impact from reduced inventory valuation losses in the previous year"

-"One-off expenses related to the consolidation of production sites"

Nippon Chemical also invested heavily into capex for MLCC capacity in the previous couple of years.

It is my opinion that they are in a unique position to capture a lot of the demand from the capacity crunch.

The MLCC shortage is more severe than previously thought

The opportunity is still upstream

The two names I mentioned, NCI and Sakai, have performed great

In fact, this is an industry I want to touch on in more depth later

Materials sit at the top of the supply chain and are usually forgotten, which represents a great opportunity

They give you time to watch a shortage form instead of trying to predict it. Once price increases start, you know it is time to buy materials suppliers, as long as supply is inelastic enough

The same thought process can be applied beyond MLCCs, and I suspect the market will start catching up with names that still undeservedly trade at very low multiples, just because they are still treated like boring industrials and not AI-adjacent companies

3

1

45

9,005

Jun 2

Nippon Chemical!

Sakai Chemical 13% today.

Nippon Chemical -3%

I think the market is into Sakai Chemical because it's been profiled on X a lot.

Nippon Chemical hasn't been mentioned as much by big accounts, but it honestly looks like it could be a better play because:

- Cheaper P/B Ratio

-Possibly higher MLCC materials exposure.

Operating Profit got hit by once-offs which hides the growing MLCC Materials Operating Profit in the segment:

-"Absence of the positive impact from reduced inventory valuation losses in the previous year"

-"One-off expenses related to the consolidation of production sites"

Nippon Chemical also invested heavily into capex for MLCC capacity in the previous couple of years.

It is my opinion that they are in a unique position to capture a lot of the demand from the capacity crunch.

The MLCC shortage is more severe than previously thought

The opportunity is still upstream

The two names I mentioned, NCI and Sakai, have performed great

In fact, this is an industry I want to touch on in more depth later

Materials sit at the top of the supply chain and are usually forgotten, which represents a great opportunity

They give you time to watch a shortage form instead of trying to predict it. Once price increases start, you know it is time to buy materials suppliers, as long as supply is inelastic enough

The same thought process can be applied beyond MLCCs, and I suspect the market will start catching up with names that still undeservedly trade at very low multiples, just because they are still treated like boring industrials and not AI-adjacent companies

3

2

24

5,192

Davy retweeted

Jun 1

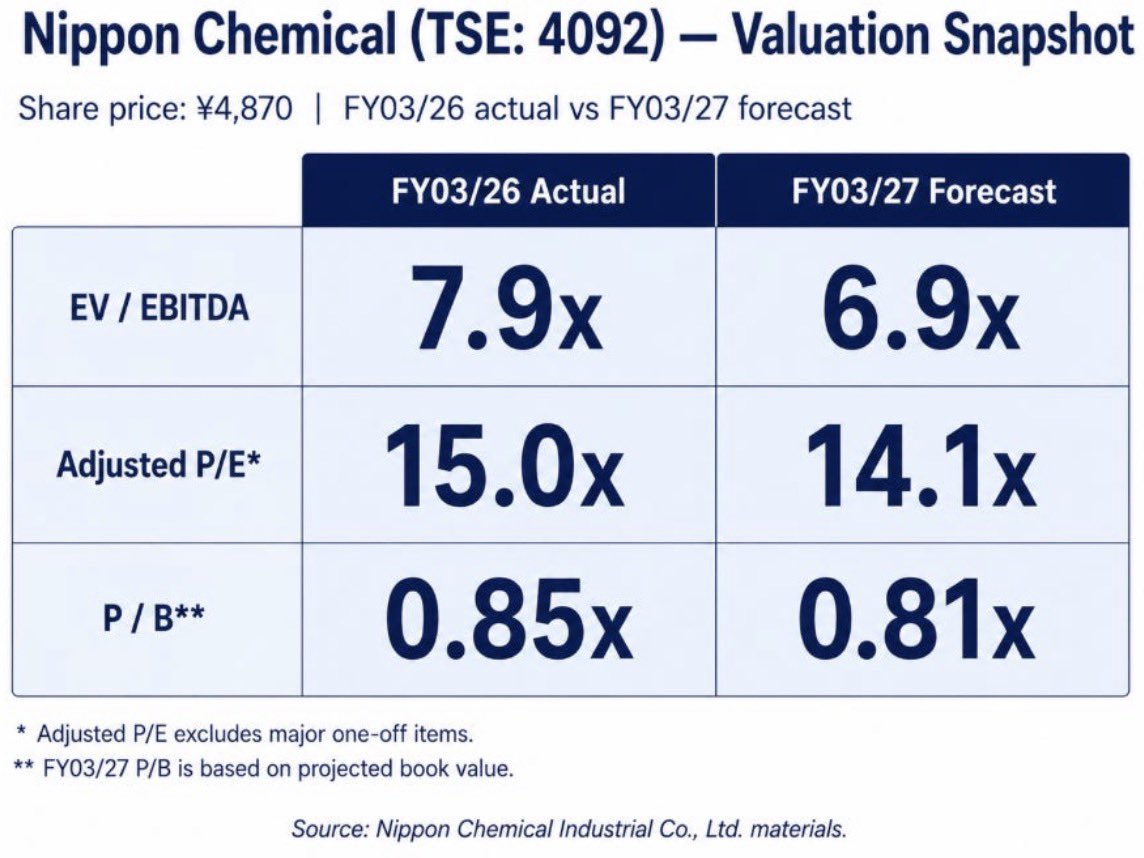

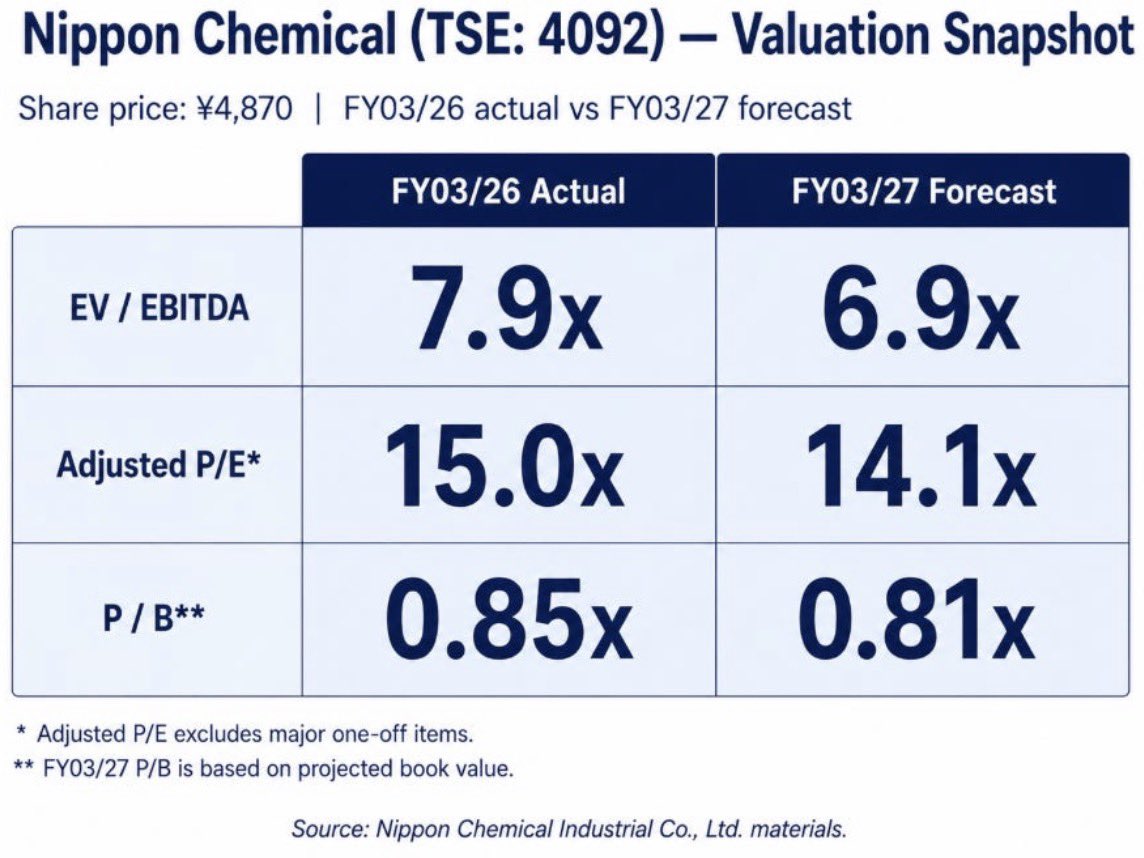

Nippon Chemical 4092.T is still trading below book which is quite striking.

Their electronics segment (mostly MLCC materials exposure) tanked in operating profit in 2026 but ceramics went up.

So next year, if the one offs and battery materials stabilize, could look FAR better for the segment.

It’s not all exposure to AI - Server though. It’s also consumer electronics, automotive etc.

But AI server MLCCs will mostly likely need the high end stuff- which is made using the hydrothermal or oxalate process.

Sakai uses hydrothermal to produce BaTiO3 Nippon uses Oxalate.

Also robotics which arrives in a few years is sure to stimulate far more demand.

It looks really good here.

Also, as an added bonus, the company has a facility (from 2022) that makes high purity red phosphorus- used for optics.

Jun 1

Nippon Chemical might be a superior play to Sakai Chemical for exposure to MLCC materials.

Electronic Ceramic Materials (materials for MLCC) is 25% of total revenue.

But the segment its inside (specialty chemicals) saw operating profit dive even amidst a 23% YoY increase in Electronic Ceramic Materials.

The drop in operating profit was caused by increased battery materials, some once off inventory costs, restructuring.

If we assume (big ask) that they achieve a similar operating margin to Sakai's own Electronic materials segment - 20%

Then in 2027 on a revenue of 12,000(mYen) (my own estimate) for the segment could produce a 2400 operating profit. For just that segment.

Nippon's entire year end operating profit 2026 was 2400.

It would take their EV/EBITDA from 8 to 4 in 2027 if price remained constant.

2

14

64

14,488

Jun 1

Finally my war hedge is going to pay off!

1

7

2,437

Jun 1

Market woke up to the opportunity this morning.

Jun 1

Nippon Chemical 4092.T is still trading below book which is quite striking.

Their electronics segment (mostly MLCC materials exposure) tanked in operating profit in 2026 but ceramics went up.

So next year, if the one offs and battery materials stabilize, could look FAR better for the segment.

It’s not all exposure to AI - Server though. It’s also consumer electronics, automotive etc.

But AI server MLCCs will mostly likely need the high end stuff- which is made using the hydrothermal or oxalate process.

Sakai uses hydrothermal to produce BaTiO3 Nippon uses Oxalate.

Also robotics which arrives in a few years is sure to stimulate far more demand.

It looks really good here.

Also, as an added bonus, the company has a facility (from 2022) that makes high purity red phosphorus- used for optics.

1

38

4,979

Jun 1

I really do think Sakai Chemical 4078.T is a big winner here. @zephyr_z9 has mentioned the name multiple times.

It's not expensive. Especially when you factor in the growth in the MLCC market.

EV/EBITDA 7.6x

P/E adj. 18x

P/B 0.97

Operating profit holds 40% exposure to MLCC through Sakai's "Electronic Materials" Segment. Or 29% of operating profit before unallocated companywide costs.

「当社電子材料のほとんどがMLCC用途」

“Almost all of our electronic materials are for MLCC applications.”

— Sakai Chemical Integrated Report 2024.

Electronic Materials is probably 99% exposed to MLCC currently. Highest margin segment.

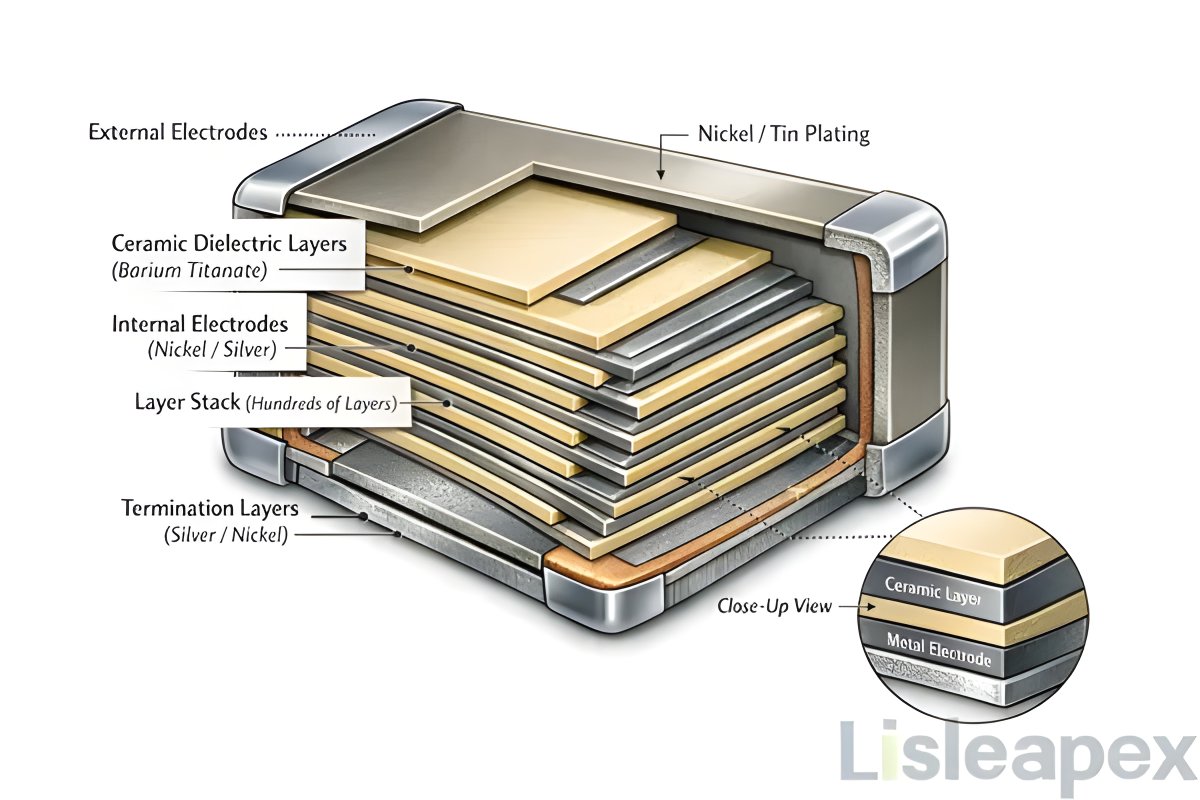

The core material is BaTiO₃ which is the highest BOM that goes into an MLCC. Around 50% of the cost.

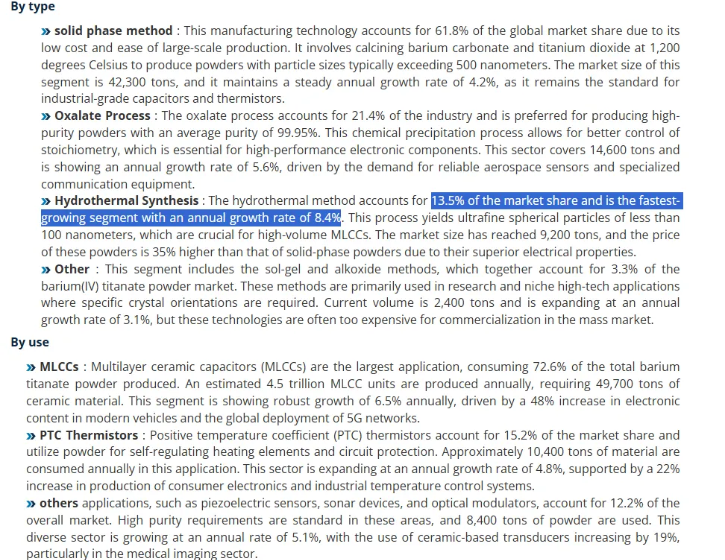

The market for BaTiO₃ consists of

-Hydrothermal. 13.5% market share.

-Oxalate. 21.4% market share.

-Solid-state. 61.8%

Hydrothermal and Oxalate are used in the high-end MLCC because the processes produce very fine, highly uniform particles.

Sakai is using Hydrothermal.

That's most likely 40% operating exposure to what @zephyr_z9 describes as an AI Server market growing at 80% annually.

May 29

What's happening in the MLCC market

First off, MLCC as a whole is a $15B market. MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers)

The AI server MLCC market is growing at 80% CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR)

We will see negative growth in the smartphone/mobile MLCC market for at least 2026-27.

Humanoids are another future high-growth market for MLCCs

Book-to-bill ratio for most MLCC suppliers is over 1 now

Reasons for price hikes-

High Nickel & Silver are affecting all segments

There is a supply-demand mismatch in the high-end (high capacitance, high voltage) segment, which is used in autos & servers

High-end MLCC lead time is over 20 weeks

Spot/distributor prices have increased by 20%-40% for low capacitance & consumer device MLCCs due to hoarding and double booking, especially in China

OEM contracts have not seen large price hikes yet

What's happening now:

Rapid capacity expansion happening across the industry

Murata expects blended ASP prices to remain flat (ASP going down in consumer electronics, expansion in AI server market)

Tier 1 players like Murata, Taiyo Yuden, SEMCO building capacity to serve AI server MLCC market

This will create opportunities for Tier 2/3 and Chinese suppliers to expand in the mid to low end market (Macronix effect)

Future:

MLCC production equiment & raw materials suppliers will be the biggest beneficiary of this CAPEX boom

MLCC producer stocks have performed well, and it is finally spilling to raw material/equipment producers

I expect them to outperform MLCC producers now

2

4

90

15,023

May 29

Soitec's new management looks pretty AGI pilled.

Management understands the photonics opportunity completely. Re-allocating lines to photonics, basically positioning themselves as best they can to take advantage of it. March saw demand accelerate. I expect we will see increased ASP's as demand ramps up.

I'm busy trying to find some anchor of a TAM for 2030. Because currently Soitec owns the monopoly.

The more I understand this business the more I wish I didn't sell so early. Full Disclosure I did buy back another 2% position before earnings. Added a tiny bit more today on the drop.

Earnings Recap:

-Revenue down in legacy segments due to customer excess inventory.

-Photonics SOI demand has seen a “very sharp acceleration,” especially since March

-Photonics SOI is now a 100m , it is already big relative to €592m total revenue

-More than 10 customers are in production or qualification

-Longer-term agreements are being put in place for both 200mm and 300mm

"Photonics SOI and POI need capacity NOW and we are putting it in place".

"Capacity is fungible- with very little investment they can produce Photonics SOI by reallocating lines

23

2,709

May 29

Wafer Shortages benefits Shin Etsu.

But I feel like the market is still forgetting that Shin Etsu also makes SOI Wafers using Soitecs Smart Cut Technology.

They will make a significant amount of money from this, as Soitec CEO mentioned that demand accelerated fast in March.

It has only just begun. I think Shin Etsu does very well ahead.

It's largest segment is also now electronic materials - its highest margin segment.

3

3

54

7,597