The AI industry (or at least their ops teams) has known for years that existing grid infrastructure was insufficient for what’s coming. But that doesn’t mean there aren’t solutions.

At Data Leaf we propose one such idea…

Detailed explanation of the U.S. data center frenzy: 45 GW, $2.5 trillion in investment—who is building and who is funding it?

An infrastructure race driven by artificial intelligence is unfolding across the United States.

Barclays’ October 31 report projects that the total installed capacity of large data center projects currently planned in the U.S. exceeds 45 gigawatts (GW), and that this building boom will attract more than $2.5 trillion in investment.

The report identifies the main drivers of this expansion as OpenAI’s “Stargate” project, Amazon, Meta, Microsoft and Elon Musk’s xAI. To train and operate increasingly complex AI models, these companies are planning and building compute clusters at an unprecedented pace.

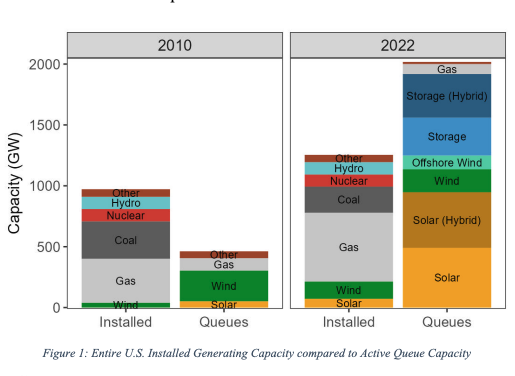

This is not only an “arms race in compute” among Big Tech; it also presents an unprecedented challenge to America’s power infrastructure. Surging electricity demand is crashing into the “power wall” of the existing U.S. grid. Grid capacity shortfalls, permitting delays, and supply constraints are combining to push these tech companies toward a “Bring-Your-Own-Power” strategy.

Big Tech leads: Stargate, hyperscalers, and xAI driving construction

According to Barclays’ tracking, a handful of tech giants sit at the core of this 45 GW construction frenzy.

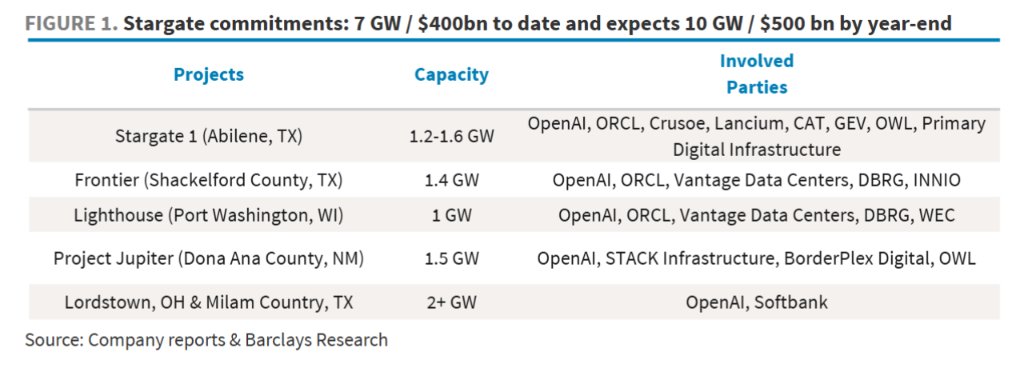

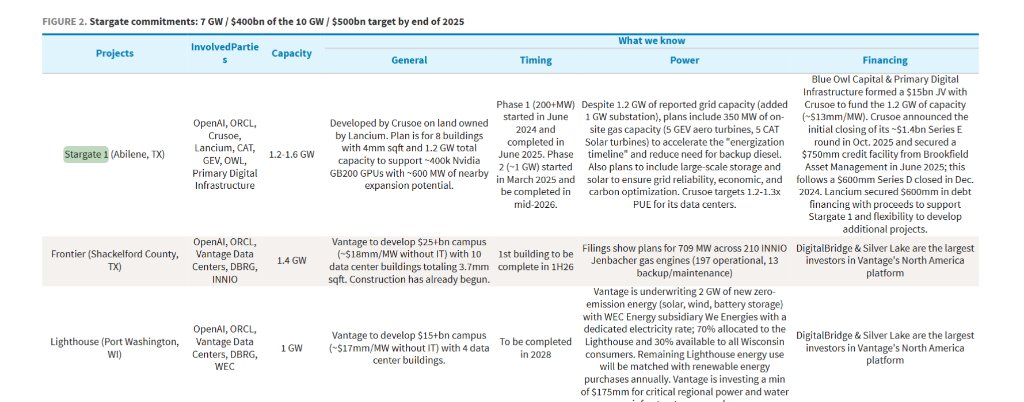

OpenAI and the “Stargate” project: The project has set a target of 10 GW and $500 billion in investment by the end of 2025. Roughly 7 GW of capacity has been committed, centered on states such as Texas and Wisconsin, with partners including Oracle, SoftBank, data-center developer Vantage, and Crusoe.

Meta: It is pushing multiple “Titan Clusters,” notably the 1 GW-class “Prometheus” project in Ohio and the “Hyperion” project in Louisiana, which has plans to expand to as much as 5 GW.

Amazon: It added 3.8 GW of capacity globally in the last 12 months and is expected to double that again by 2027. Based on this, Barclays estimates that roughly 13 GW of capacity could be added in the U.S. alone between 2026 and 2027.

Microsoft: It is building a 900 MW AI facility in Wisconsin and planning multiple similar projects in other parts of the United States.

xAI: In Memphis, Tennessee, it is expanding a data center to 1.4 GW, to be used for training the Grok model.

The price of this investment feast is extremely high. According to the report, data center construction costs (excluding IT equipment) have surged to more than $17 million per MW. Using OpenAI’s “Stargate” project as an example, investment commitments for 7 GW of capacity alone exceed $400 billion, and the per-MW cost (including IT equipment) reaches $57 million, underscoring the enormous capital intensity of AI infrastructure.

Pressure from the “power wall”: Grid bottlenecks spark on-site generation models

Grid constraints are the most serious challenge currently facing data center construction. The Barclays report emphasizes that even when grid interconnection approvals are obtained, project developers are strongly inclined to build on-site generation to pull forward the “energization date” and to secure power reliability.

A representative example is the “Stargate 1” project. Although it has already received approval for 1.2 GW of grid interconnection, it plans to deploy about 350 MW of on-site natural-gas generation capacity. The report explains that this step is intended to “accelerate the project’s energization schedule” and reflects a desire to adopt natural gas rather than diesel as the long-term emergency power source.

To cope with the millisecond-scale, rapid power fluctuations that come with AI workloads, the industry is adopting an “all-weather solution.” For example, Meta’s “Prometheus” project uses a combination of gas turbines, gas reciprocating engines, and diesel engines to handle baseload supply, power-variation response, and fast-start emergencies, respectively. Such hybrid power solutions are becoming the industry trend.

Who is paying: Capital and costs behind trillion-dollar outlays

Behind the massive investment lies a complex financing structure and steadily rising costs. In addition to the tech companies’ own capital expenditures, private equity and infrastructure-focused funds play a central role. For example, Blue Owl Capital has formed a $15 billion joint venture with Crusoe to finance the “Stargate 1” project.

At the same time, the Energy-as-a-Service (EaaS) model is on the rise. Energy companies like Williams sign long-term power purchase agreements (PPAs) with data center operators and invest billions of dollars to build and operate dedicated generation assets.

Williams invested $2 billion in Meta’s “Prometheus” project and signed a similar $3.1 billion contract with another major customer. This shows a growing tendency among data center operators to outsource the development and operation of energy assets to specialized companies.

Supply-chain challenges: Equipment lead times and labor shortages as wild cards

Explosive demand is putting massive pressure on the power-equipment supply chain. Citing a document, the Barclays report notes that as market demand has surged, prices for medium- and large-frame gas turbines have risen 50% in less than two years, and lead times have lengthened significantly. Manufacturers such as GE Vernova and Caterpillar are ramping up, but they remain hobbled by parts procurement and labor shortages.

Some companies are also choosing to acquire used or “in-box” (unused) equipment to sidestep long order queues. For example, Fermi America purchased Siemens gas turbines that were not used in an LNG project, securing valuable generation capacity for data-center use.