Financial freedom advocate I Outdoor enthusiast I Proud Father and American. Personal account.

Joined June 2020

- Tweets 2,130

- Following 1,470

- Followers 23,274

- Likes 7,102

31 Photos and videos

Brian Quintenz retweeted

1/9

We saw it with crypto, we're seeing it with AI, and we're seeing it with Prediction Markets:

* We over regulate markets that are hot-button issues.

* Activity gets pushed activity offshore.

* Offshore unregulated entities exploit US consumers.

* The US ends up with all of the pain point and none of the benefit.

Jun 11

America should be leading the world in prediction market innovation — not pushing it offshore to unregulated platforms that leave consumers unprotected.

9

7

41

11,660

Brian Quintenz retweeted

The Committee of Five—John Adams, Benjamin Franklin, Thomas Jefferson, Robert Livingston, and Roger Sherman—was appointed to draft the Declaration of Independence 250 years ago today.

Jefferson's draft of the document is here at the Library, and will be featured in a new exhibition opening July 3.

ALT A view of Thomas Jefferson's rough draft of the Declaration of Independence, hand-written with edits placed throughout. Held in the Library of Congress Jefferson Collection. Photo by Shawn Miller.

ALT A view of Thomas Jefferson's rough draft of the Declaration of Independence, hand-written with edits placed throughout. Held in the Library of Congress Jefferson Collection. Photo by Shawn Miller.

ALT A view of Thomas Jefferson's rough draft of the Declaration of Independence, hand-written with edits placed throughout. Held in the Library of Congress Jefferson Collection. Photo by Shawn Miller.

68

1,890

6,322

169,288

Jun 11

Gary Gensler deliberately sought an intergalactic reach for the CFTC through Dodd Frank. Now he’s saying that didn’t mean a few things he doesn’t like. The law is the law. Exchange-traded event contracts, on all things, are within the agency’s jurisdiction.cnb.cx/4vClc17

6

6

45

4,797

Brian Quintenz retweeted

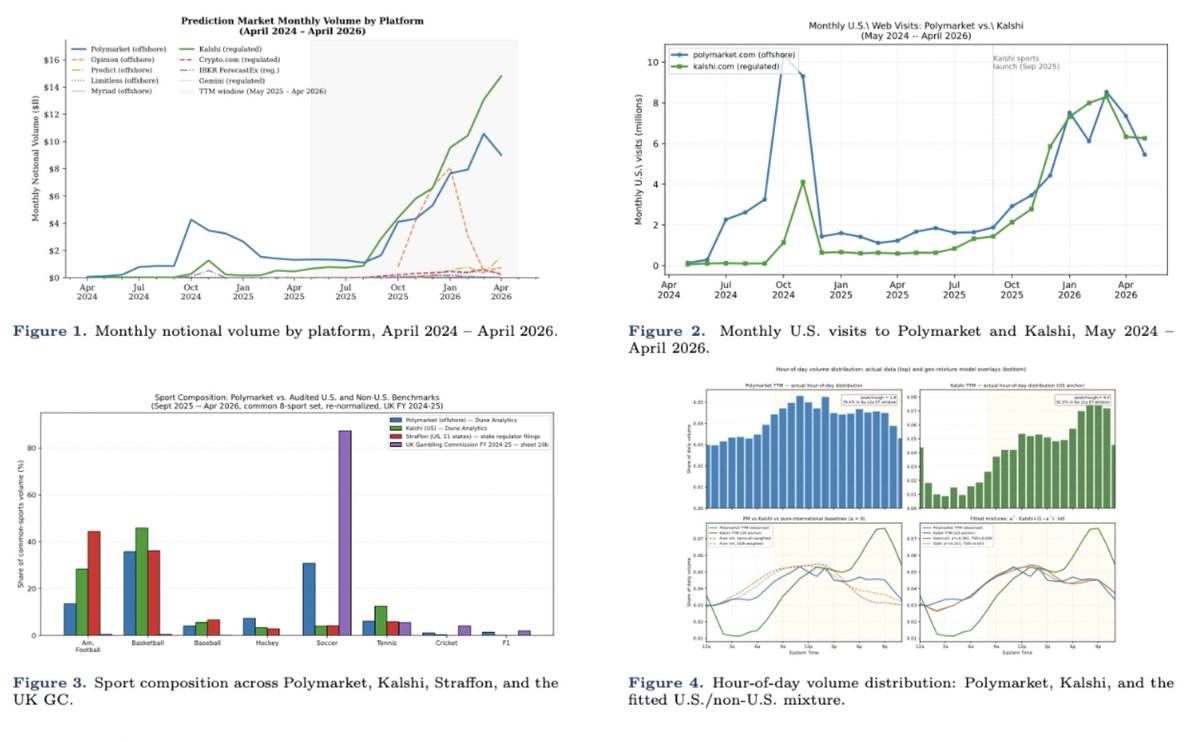

Americans are using VPNs to access unregulated, offshore prediction market platforms that offer contracts on death and war.

Now, we finally know how big this market is. New data from @harrydcrane shows this could be a $133 billion problem:

2

2

14

1,794

Brian Quintenz retweeted

Jun 11

America should be leading the world in prediction market innovation — not pushing it offshore to unregulated platforms that leave consumers unprotected.

Jun 11

Research Brief: Estimating U.S. User Activity in Offshore Prediction Markets

Key Findings:

- $ 11-27B of Polymarket volume May 2025-April 2026 is attributed to U.S. users

- $ 11-34B of all offshore volume came from U.S. users

Full report below:

cranezeng.com/prediction-mar…

6

6

36

22,054

Brian Quintenz retweeted

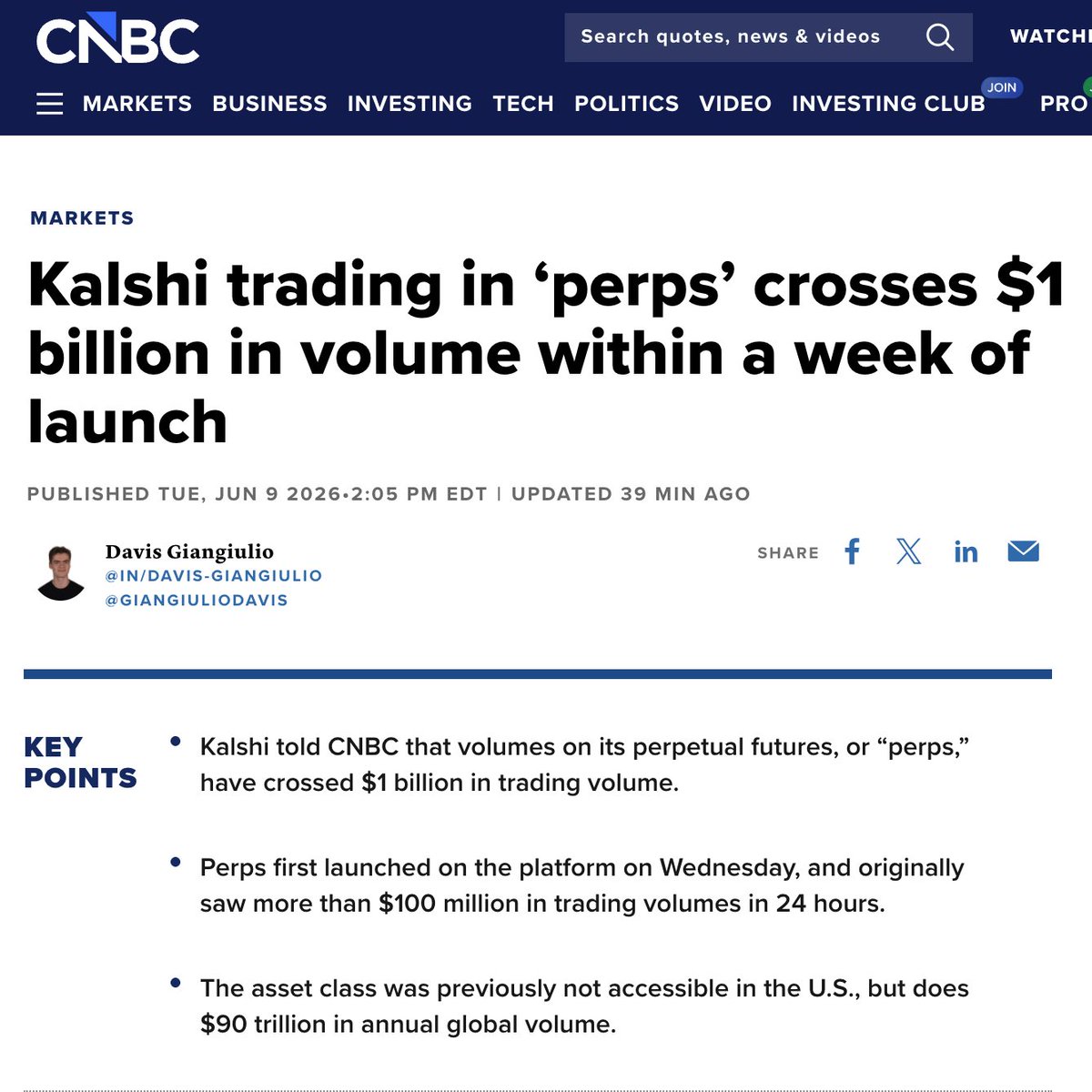

Jun 10

Actually, $1b in 24h volume 😉

Took 1 week for Kalshi Perps to get to $1B, and we haven't even launched publicly yet

Prediction markets took 3.5 years to get to $1B

43

17

209

57,428

Brian Quintenz retweeted

Today, we announced that Kalshi will now require employment information in order to trade in certain markets.

Market integrity is a more than just a lofty goal for us. It’s the reason we collect identification info from every trader, why we surveil our markets 24/7, and why we continue to expand our capabilities to prevent, detect, and punish misconduct.

The work is never done, but we are proud to mark yet another big step today in leading the prediction market industry on the issue of integrity.

news.kalshi.com/p/kalshi-mar…

6

15

72

9,970

Brian Quintenz retweeted

A few weeks ago @ABC and @AaronKatersky came to Kalshi's New York City HQ to take a closer look at our surveillance and market integrity systems in action. We spoke at length about how Kalshi operates our regulated exchange and monitors for insider trading, including the importance of collecting Know-Your-Customer information from all traders and setting up 24/7 surveillance systems to catch bad actors.

Big thanks to the team at ABC for spending time with the people whose hard work makes Kalshi's surveillance and enforcement possible.

6

16

77

18,040

Brian Quintenz retweeted

Danny Moses explores the power of prediction markets, using Kalshi to forecast economic trends and stock moves. bit.ly/4oanaTY

3

2

10

11,776

Brian Quintenz retweeted

Can't wait for Brazil's 6th star.

History remembers the winners.

Witness it live.

2 tickets to the final. $1 million prize pool.

kalshi.com/wc

24

11

329

50,716

Jun 5

.@FTC

EXCLUSIVE: A top Polymarket executive sent hundreds of thousands of dollars — and likely more — to social media influencers from left to right.

One influencer says Polymarket wrote posts for them to share on X and asked them to promote specific bets.

politico.com/news/2026/06/05…

2

1

26

9,592

Jun 5

This is the right move and should be finalized. But Kalshi already prevents this from occurring.

Jun 5

🇺🇸 NEW: Rep. Bryan Steil plans to add language barring lawmakers from trading on prediction markets to the House GOP's stock ban bill.

3

1

15

4,822

Today is the first day US retail and institutions can trade BTC with leverage.

From regulatory approval, to live in prod within 2 business days.

Kalshi.

Bitcoin Perpetuals are now live for trading.

The First American Perpetual Future.

Only on Kalshi.

14

1

74

12,938

Brian Quintenz retweeted

Jun 3

Prediction market Kalshi has reported former Rep. George Santos to prosecutors over a bet he made on himself, a person familiar with the investigation says. apnews.com/article/george-sa…

108

383

2,539

399,259

Jun 3

Robust pricing references make it a lot easier for OTC desks to serve clients with customized off-exchange hedges. Very cool to see Galaxy use Kalshi’s markets to price these risks at institutional size.

Today, we're launching institutional OTC prediction markets trading through our Global Markets desk.

Hedge funds, family offices, and other institutional clients can now access prediction market liquidity at sizes and with a level of discretion suited to institutional scale.

7

26

3,967

Today, we're launching institutional OTC prediction markets trading through our Global Markets desk.

Hedge funds, family offices, and other institutional clients can now access prediction market liquidity at sizes and with a level of discretion suited to institutional scale.

16

21

142

72,180

Brian Quintenz retweeted

Jun 2

47

54

416

57,517

Jun 2

Jun 2

Legal review is moving forward after further discussions.

This dispute is no longer only about one trader or one losing position. It may raise serious legal issues across multiple jurisdictions because Polymarket created the market, wrote the rules, accepted real user funds, and then appears to be applying a disclosure-timing condition that was never clearly written into the market.

Under U.S. contract law principles, including the implied covenant of good faith and fair dealing, parties must perform agreements in a way that does not undermine the reasonable expectations created by the written terms. U.S. law also recognizes contra proferentem, meaning ambiguous language is generally interpreted against the drafter. If Polymarket drafted “sells any Bitcoin by May 31,” then it should not later benefit from ambiguity by treating it as “discloses by May 31.”

This issue may also be relevant under consumer protection and unfair terms frameworks in other jurisdictions. Under the UK Consumer Rights Act 2015, unfair terms and unclear consumer-facing terms can be scrutinized where they create imbalance against users. Under EU consumer contract principles, standard terms must be drafted in plain, intelligible language, and ambiguity is generally interpreted in favor of consumers. Similar good-faith and fair-dealing concepts also exist in common-law jurisdictions such as Canada, Australia, and Singapore.

The point is simple: if a platform writes the market, controls the interface, defines the resolution sources, and takes fees from users, it cannot later rely on an unwritten condition to defeat the ordinary meaning of its own rule.

The rule said “sells.” It did not say “discloses,” “files an 8-K,” “announces,” or “publicly confirms before May 31.”

I will continue preserving evidence, improving legal materials, speaking with counsel, and pursuing every lawful path available.

If the rule says “sells,” then the event is the sale.

2

1,489

Brian Quintenz retweeted

Jun 2

Legal review is moving forward after further discussions.

This dispute is no longer only about one trader or one losing position. It may raise serious legal issues across multiple jurisdictions because Polymarket created the market, wrote the rules, accepted real user funds, and then appears to be applying a disclosure-timing condition that was never clearly written into the market.

Under U.S. contract law principles, including the implied covenant of good faith and fair dealing, parties must perform agreements in a way that does not undermine the reasonable expectations created by the written terms. U.S. law also recognizes contra proferentem, meaning ambiguous language is generally interpreted against the drafter. If Polymarket drafted “sells any Bitcoin by May 31,” then it should not later benefit from ambiguity by treating it as “discloses by May 31.”

This issue may also be relevant under consumer protection and unfair terms frameworks in other jurisdictions. Under the UK Consumer Rights Act 2015, unfair terms and unclear consumer-facing terms can be scrutinized where they create imbalance against users. Under EU consumer contract principles, standard terms must be drafted in plain, intelligible language, and ambiguity is generally interpreted in favor of consumers. Similar good-faith and fair-dealing concepts also exist in common-law jurisdictions such as Canada, Australia, and Singapore.

The point is simple: if a platform writes the market, controls the interface, defines the resolution sources, and takes fees from users, it cannot later rely on an unwritten condition to defeat the ordinary meaning of its own rule.

The rule said “sells.” It did not say “discloses,” “files an 8-K,” “announces,” or “publicly confirms before May 31.”

I will continue preserving evidence, improving legal materials, speaking with counsel, and pursuing every lawful path available.

If the rule says “sells,” then the event is the sale.

11

9

262

15,749

Brian Quintenz retweeted

Jun 2

Can’t wait to read @matt_levine ‘s take on this one. As I’ve already tweeted, this is insanity. Either this should have resolved “yes”, or the contract should have stopped trading at midnight on may 31.

Jun 2

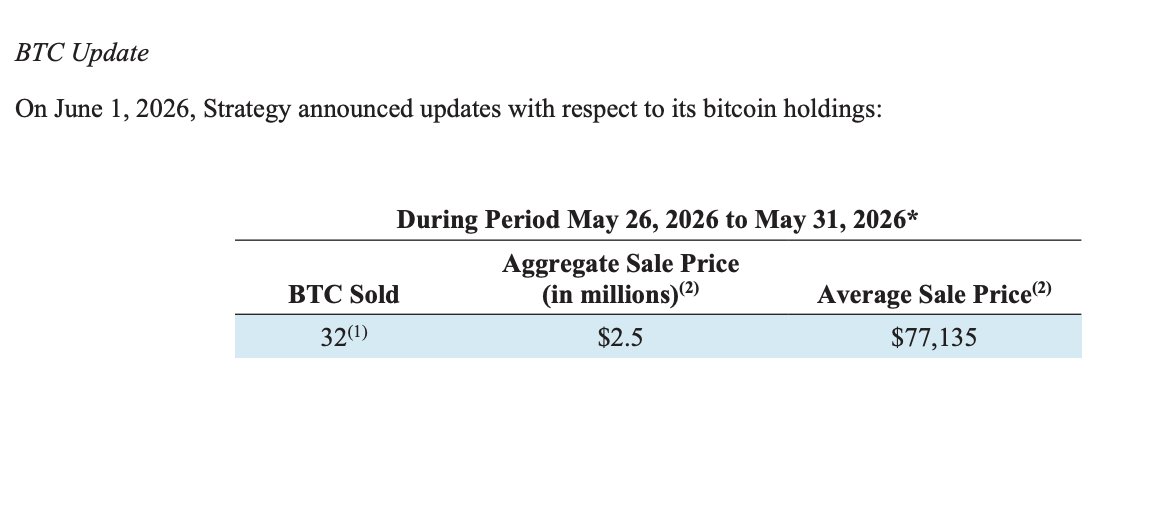

I was just scammed for $500K by Polymarket.

I am "willo2", the top holder of YES on "MicroStrategy sells Bitcoin by May 31st".

Here's what happened:

21

22

334

42,797