Investment Research @0xuclub // @gate_ventures newbie // opinions are my own

Joined August 2020

- Tweets 1,614

- Following 2,646

- Followers 2,105

- Likes 11,559

208 Photos and videos

Pinned Tweet

24 Apr 2025

夥拍 @daoandinvest Alvin哥代表 @0xUClub 參加,獲益良多,亦榮幸獲得 Open Research 組別冠軍,算是 2年投研生涯的一大里程碑。

分析寫這麼詳盡,到頭來不忘提自己 - 知行合一 - 到底長篇大論後,係咪能夠說服自己 ape in (?)

@HyperliquidX 亦是自己花費不少資金的地方,絕不紙上談兵🤣 基本面的確紮實 風險亦寫在投研裡面了 -metaera.hk/contents/212976

當然投研的主軸還是想從 HL 出發,檢視 PerpDEX 市場的轉型,文章最後亦會提到,希望大家睇到最後🤣

24 Apr 2025

经过激烈角逐与专业较量,本届PKUBA首届全球行业研究竞赛圆满落幕!感谢所有参赛团队与选手为区块链和加密领域带来独到见解和前瞻研究。现将各赛道获奖名单公布如下:

🛤️ Meme文化与市场研究赛道

🥇 一等奖

选手: Clare

作品名称: 《AI Agent Meme已死?从Web2技术爆发到Web3链上文化迁移的信号》

🥈 二等奖

选手: 巫天骐,陈润楠

作品名称: 《洞察Memecoin发行平台:Pump.fun引领的变革与创新》

选手: ZengQi, YuXiaoxiao

作品名称: 《从玩笑到资产:Web3 迷因经济的崛起与未来趋势》

🥉 三等奖

选手: CruxZhou, Dyan

作品名称: 《解构“无锚化交易” : Memecoin 的底层共识机制》

选手: Treap

作品名称: 《Memecoin政治经济学批判》

选手: 杨俊豪

作品名称: 《注意力经济如何驱动MEME价值上涨——从孙宇晨4500万买香蕉谈起》

选手: 付齐双,项悦欣,张宝量

作品名称: 《Meme币生态的崛起与变革:如何在 Web3 时代走向公平与繁荣?》

选手: 汪宗勤,蕭子彥

作品名称: 《迷因幣之符號象徵、社群結構與情緒分析 –以Pepe、Trump為例》

🔍 宏观市场与加密货币研究赛道

🥇 一等奖

选手: 雷双Jessie

作品名称: 《从“草莽”到“华尔街化”:比特币定价逻辑的范式转移 ——基于宏观经济周期、美股联动与山寨币分化的结构性分析》

🥈 二等奖

选手: Harry

作品名称: 《日渐拥挤的比特币期现套利市场——影响与风险》

选手: 吴贝妮,张逸萍,陈亦维

作品名称: 《万物RWA的监管边界》

🥉 三等奖

选手: Freya

作品名称: 《从欧美加密监管体系看 <Genius Act>》

选手: 王宏,曹亚东,孙英杰

作品名称: 《宏观市场与加密货币分析——经济周期与股票波动率视角》

选手: QISheng

作品名称: 《山寨币价格波动影响因素研究》

选手: 张于海,Walter,Aryan

作品名称: 《去美元化浪潮下的加密资产:机遇、挑战与金融体系的未来》

选手: 缪超豪,王漱渤

作品名称: 《从宏观经济不相关到宏观经济相关——比特币的“登堂入室”之路》

⚡ 比特币生态赛道

🥇 一等奖

选手: Moose

作品名称: 《BTCFi范式重构:比特币再质押驱动的流动性革命》

🥈 二等奖

选手: Jelly

作品名称: 《当比特币的区块奖励消失会发生什么?》

🥉 三等奖

选手: Crypto绿头怪

作品名称: 《解密Bitlayer:破局BTCFi的基建之路》

选手: Chauncey Liu

作品名称: 《数字黄金的破茧之路:解码比特币生态的范式革命》

选手: Junli Deng

作品名称: 《从数字黄金到表情包画布:代币时代比特币的文化演进》

🔗 通用链技术赛道

🥇 一等奖

选手: Adrian, Larry

作品名称: 《多链时代的互操作性基础设施与用户需求变革》

🥈 二等奖

选手: D50,pzq,Sugar

作品名称: 《共识算法的自我进化:AI双模型驱动的PoW/PoS多链优化》

🥉 三等奖

选手: 陈伟

作品名称: 《TON生态机制与估值浅析》

选手: Jason Hu

作品名称: 《通用链技术的“前世今生”》

选手: 徐晟凯,邓峰,蒲泓宇

作品名称: 《传统以太坊区块链的改进——以太坊分片和有向无环图(DAG)》

💡 Open Research赛道

🥇 一等奖

选手: Ryan Tung,Oscar Chang,Alvin Ku

作品名称: 《深入剖析 Hyperliquid 及 HyperEVM生态的发展,审视去中心化衍生品交易平台的转型》

🥈 二等奖

选手: ziying

作品名称: 《去中心化科学(DeSci):区块链技术驱动的学术研究新范式》

🥉 三等奖

选手: MaggieL

作品名称: 《Web3中的AI代理:自主程序的演进与未来》

选手: Aranna Dang,Derek Zhou

作品名称: 《蒙尘的珍珠:公共领域许可证的前世今生与未来》

💥 Exposure激励计划

🥇 一等奖: @JessieLeiShuang

🥈 二等奖: @0x_ARAY

🥉 三等奖: @harry_xymeng

再次衷心祝贺所有获奖团队和选手!期待大家在未来继续探索,推动行业向更高标准迈进!

再次感谢所有评委 @JunboPeng @0xkevinhe @jelly6617 @baby_fisherman @RomeoKuok 、阿佘对本次 PKUBA 首届全球行业研究竞赛的支持,让我们期待更多优秀的研报作品与创新!期待未来与大家携手前行,共同推动加密行业的发展与进步!

25

4

61

11,669

seen some takes on "i'd buy SPCX in 3 months at a lower price"

sure - but that's on a fundamentally different thesis

the thesis at open should be entirely based on flow - val doesn't matter

because you have a stock that has

- 4.2% float

- o/w only 20% to retail -> this means 0.8% possible sell pressure (rest to long-only)

- o/w >50% won't sell given flipping policy / natural hodler -> 0.4% possible sell pressure

while index funds are expected to buy 20bn / 1%

1% >> 0.4%

it's like elon launches at coin with 99.6% control while a DAT is coming in 2 weeks. insanity

58

20

319

118,127

Hyperliquid (Tradexyz) traders predicted the exact opening price of SpaceX.

The Hyperliquid SpaceX perp was trading at 171 just 1 minute before they announced the starting price of $171 per share.

app.hyperliquid.xyz/trade/xy…

109

180

1,274

157,266

lmao

Susquehanna International Group’s prediction market desk took its biggest sports loss making markets during the Knicks’ Game 4 NBA Finals comeback Wednesday, while Kalshi reported a record day for volume.

Susquehanna’s losses, a source familiar with the situation says, were almost entirely on the game-winner market.

1

212

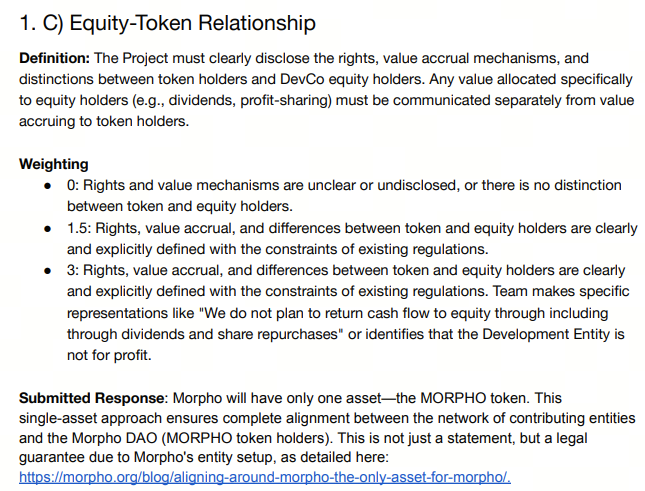

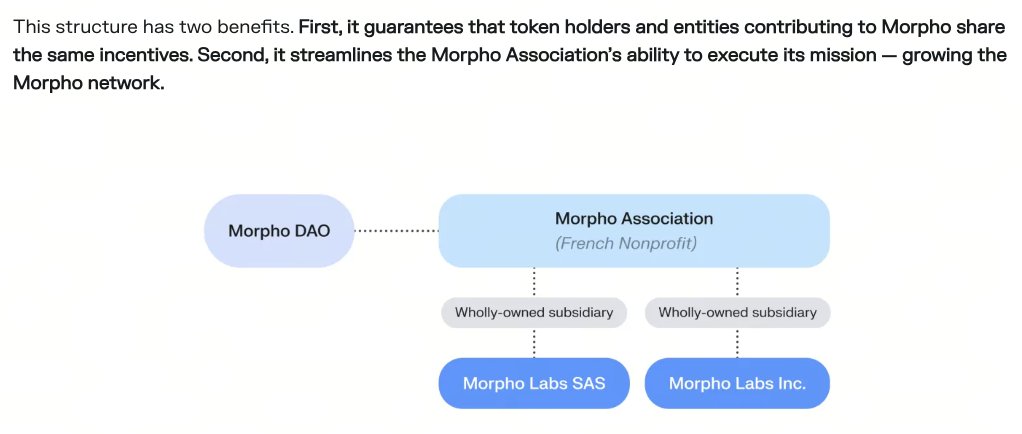

原来 Morpho 是没有股权的,这 1.75 亿美元的投资应该是直接购买代币的吧。期待 Morpho 重振 Token Play。

2

4

1,023

Holycrap this feels like peak degen crypto days again

Proud to share that @solana is now the presenting sponsor of the World Series of Poker, the first in 15 years and only 3rd in their 59 year history.

When we thought about what kind of bets we could make to grow Solana, poker was a standout:

- 100m monthly players; bigger than golf and tennis combined

- Fastest growing game in Asia

- The biggest “sport” where capital and economy are central to its gameplay

- Future of trading looks more like poker than traditional finance

- Many poker pros integrate crypto in their lives already, from settling private games to staking

We approached @WSOP to see how we could collaborate deeply and came away ready to go all in.

We are building together on a number of fronts:

- Bringing WSOP back to @ESPN live in August with Solana front and center through the entire experience, broadcasting to 400 million households worldwide

- Streaming 150 hours live from Vegas on Solana

- SOL Solana stablecoins exclusively for tournament buy-ins and payouts (already processed millions in the last week!)

- Collaborating to bring poker staking into the crypto era, as well as prediction markets and other frontier products

- Creating content together to educate traders on the game and poker players on trading onchain

Poker is a game I’ve loved for 20 years and I’m personally excited to bring these two adjacent worlds together.

1

153

世界杯即将到来!0xU与42陪你看球啦!

周四(06/11) 晚 19:30 HKT, @0xUClub 联合 @42space 为您带来世界杯前夜专题AMA

我们和您一起看透:

1. 42 的机制到底是什么, 普通用户怎么利用这套机制赚钱

2. 现在预测市场上还有哪些版块, 是真能 profit 的

3. 这个赛道最近还冒出来哪些新东西

4. 世界杯这一个月, 预测市场会怎么走 · 流量去哪里 · 钱在哪里

阵容:

· Leo @Leozayaat — @42space 创始人,带您深究背后玩法机制

· Kaylyn @kaylyn_0x — 42 掘金大队长,带您看透收益玩法

· JianAn @0xJianAn — @SmartXTerminal 产品经理,带您了解最“用户”的AI PM交易终端

· Ryan @MrRyanChi — @insidersdotbot 创始人, 聪明钱猎手,《Polymarket 套利圣经》明星作者

· Issue @issue_wong — Predict-Raven 作者, 技术极客,与您一同讨论预测市场的何去何从

主持 @dj_rxpple 00后六边形区块链战士

📅 06.11 周四 19:30 – 20:30 HKT

📍 X Space · @0xUClub

6

2

23

10,804

Disclosure: Citrinitas Capital Management Inc is an investor in Robostrategy.

citriniresearch.com/p/citrin…

21

28

331

224,673

chingchalong♣️🇭🇰|𝟎𝐱𝐔 retweeted

Jun 3

PENDLE is now live on @Revolut, the largest fintech in Europe.

20 million crypto traders in the UK, EU, Norway, Iceland and Liechtenstein now have direct access from their everyday banking app, reaching $PENDLE through regulated rails rather than DeFi frontends 🏦

27

39

269

17,037

6th sense from a 4-years crypto fish

Jun 4

At the same time that Arthur Hayes started selling, another entity related to Andrew Kang (@Rewkang ) sold 120k HYPE ($8M) in less than 30 minutes, pushing the hyperliquid:native price down more than 5%.

That entity already finished selling his stack, but Arthur Hayes, through Flowdesk, is still selling through a slow TWAP. He already has 165k HYPE left.

Just 5 minutes ago, another interesting participant appeared. Andreas Brekken (@abrkn ), founder of SideShift, also started selling 50k HYPE.

At the same time, Hyperliquid Strategies (@HypeStrat) is TWAPping more than $10M through Anchorage.

Arthur Hayes selling wallet: markets.xyz/trader/0x964f9b5…

Related Andrew Kang wallet (not confirmed): markets.xyz/trader/0x6426401…

Andreas Brekken wallet: markets.xyz/trader/0x280e93b…

2

157

chingchalong♣️🇭🇰|𝟎𝐱𝐔 retweeted

Jun 2

First Podcast Appearance in 5 years

Building a Robotics focused investment firm has been one of the most fascinating experiences of my life

Robots will be as ubiquitous as smart phones within a decade. Everyone should be paying attention and the @RoboStrategy team will be sharing much more about the most exciting developments in the industry

Not enough people are talking about physical AI and robotics.

I sat down with @rewkang, one of the best investors of the last decade, to discuss his massive bet on humanoids and robotics.

He breaks down the industry, the addressable market, multiple leading companies, and why he launched a publicly-traded fund ($BOT) focused on investing in the top private robotics companies.

YouTube: youtu.be/Q_UWD5aoJkc?si=_E7l…

Apple: podcasts.apple.com/us/podcas…

Spotify: open.spotify.com/episode/4L6…

TIMESTAMPS:

0:00 - Intro

1:28 - Why Andrew shifted from crypto to humanoid robots

3:58 - How big is the total addressable market?

8:08 - Building conviction — the $19M bet on Figure AI

16:06 - US vs. China — who wins the robot race?

28:08 - General purpose vs. specialized robots

31:05 - Where does training data come from?

40:24 - Humanoid robots in your everyday life

43:27 - Can Tesla & Elon win the humanoid race?

46:19 - Job displacement & UBI

51:15 - RoboStrategy — the publicly traded venture fund

1:11:17 - What is exciting about Apptronik?

1:13:24 - Addressing the critics

71

78

1,072

435,660

been looking into many crypto payment deals lately, feels like the playbooks are pretty similar:

stablecoin rails compliance in service jurisdictions yield product programmable APIs.

I think at the end of the day people won't care much about the tech stack (highly homogenous), its still on distribution - some directly to consumer brands/SMEs, some to PSPs/FIs.

no right or wrong, its just different layers of payment adoption.

1

82

chingchalong♣️🇭🇰|𝟎𝐱𝐔 retweeted

6

7

34

6,066

chingchalong♣️🇭🇰|𝟎𝐱𝐔 retweeted

Jun 3

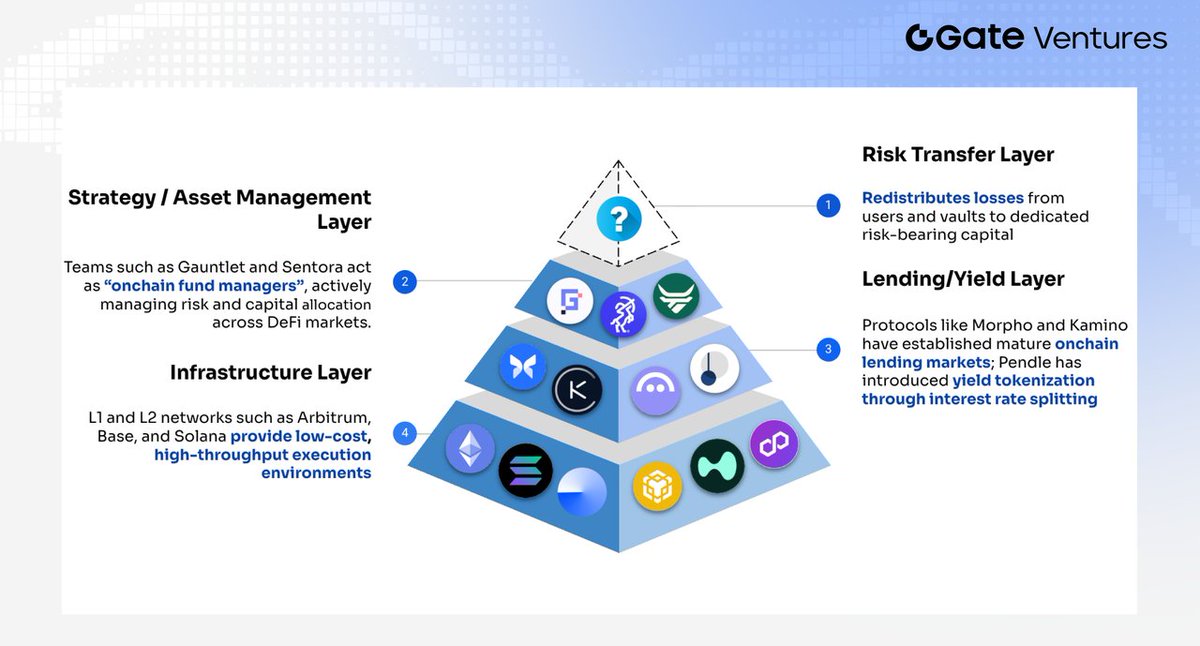

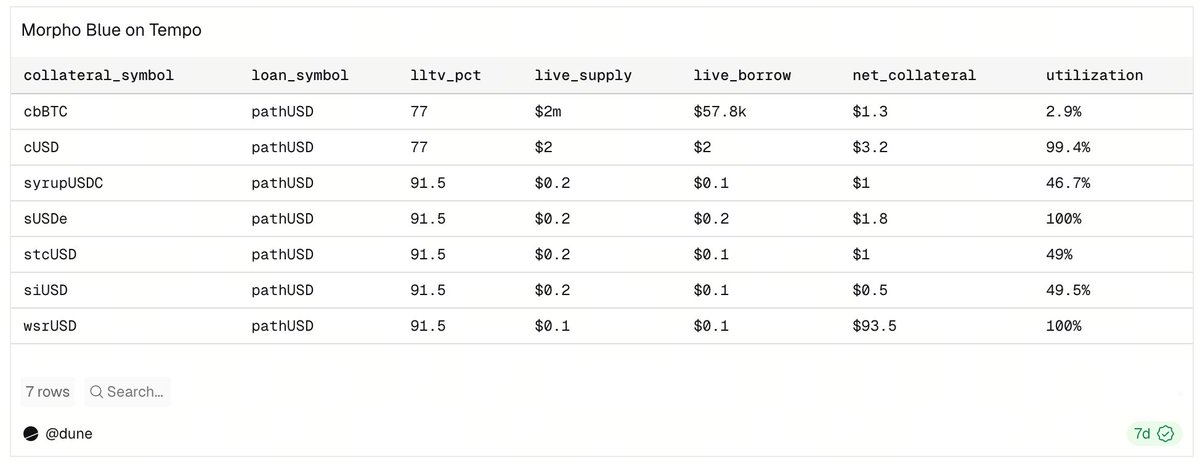

Last week, @tempo announced the integration of the DeFi lending protocol @Morpho directly into its payment infrastructure.

This allows enterprises and fintechs to lend idle stablecoins for yield or borrow against on-chain collateral without bridging assets or leaving the Tempo ecosystem.

The initial curated vaults are managed by Gauntlet and Sentora and around US$2 million of Coinbase Wrapped BTC (cbBTC) has already been deposited as collateral, making it the first supported asset on the platform.

Source: @Dune

2

6

16

1,390

$HYPE is lil bit too hyped on media that I feel like these giant holders are just looking for exiting liquidity

1

3

460

Our Crypto futures and options are officially available to trade 24/7.

With over 7,200 contracts (~$50M notional) traded in our first weekend alone, the demand for always-on markets is clear.

Read the full press release: spr.ly/6015B8iqO3 spr.ly/6014B8iqOM

3

24

93

29,354

Non-USD stablecoins could be one of the next major growth areas in crypto.

The reason is simple: businesses and consumers ultimately need to get paid, make payments, and settle in their local currencies.

While USD stablecoins improve cross-border payments, they don't eliminate the need for FX conversion and local banking rails.

That's where local-currency stablecoins come in. They bring domestic currencies on-chain, allowing users to stay in their home currency while benefiting from instant settlement and global liquidity.

This naturally leads to the rise of on-chain FX.

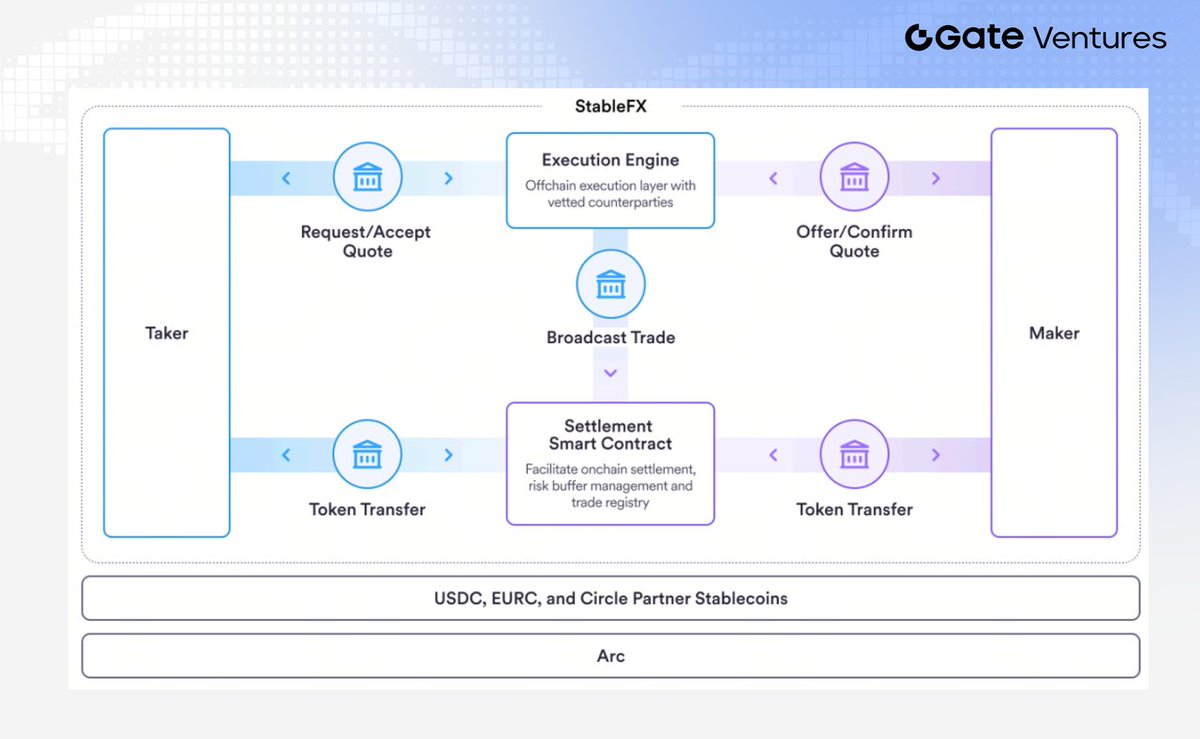

Projects like Circle's StableFX are trying to build the infrastructure needed to exchange and settle different stablecoins on-chain. Adoption is still early, largely because regulation remains fragmented and building local banking, compliance, and liquidity networks is difficult.

Ultimately, on-chain FX isn't missing currencies, it’s missing institutional-grade infrastructure. StableFX is essentially an attempt to bring traditional FX liquidity, pricing, and settlement onto blockchain rails.

非美元稳定币大概率会成为下一阶段的重要趋势。

原因很简单:在真实商业场景里,企业、商户和个人最终还是需要用本地货币来收款、付款、记账和结算。

所以,当资金流涉及不同国家、不同货币和不同银行体系时,只依赖美元稳定币,并不能完全消除外汇兑换、出入金、预存资金和本地清算等摩擦。

本地货币稳定币的价值在于:把本国货币直接带到链上。这样企业和用户既可以保留本币资产敞口,又能获得链上即时结算和跨境流动性的优势。

这也自然引出了另一个趋势:链上外汇。

用稳定币做跨境支付,本质上离不开链上外汇。但这个市场还没有真正起飞,主要有两个原因:

第一,很多国家的稳定币监管框架仍不够明确。

例如韩国多年来一直通过银行联盟和 Sandbox 探索韩元稳定币;加拿大也是在 QCAD 推出五年多后,才开始开放不依赖证券化结构的监管路径。不过,监管确定性正在明显提升,尤其是在美国 GENIUS Act 和香港稳定币条例落地之后,全球稳定币监管正在进入更清晰的阶段。

第二,非美元稳定币发行方往往需要从零搭建本地基础设施。

这包括本地银行合作、储备管理、铸造 / 赎回通道、合规流程和清算网络。不同国家的银行体系和监管要求差异很大,所以落地难度远高于单纯发行一个链上资产。

因此,链上外汇真正缺的,不只是更多币种,而是一套完整的机构级基础设施。

而 Circle 最新推出的 StableFX,本质上更像是在搭建一个链上版本的外汇网络。其核心思路是把传统外汇市场的流动性、报价机制和结算逻辑搬到链上,让不同本地货币稳定币之间可以更高效地完成兑换和结算。

for more details go check out the full article below🔥🔥

1

149

非美元稳定币大概率会成为下一阶段的重要趋势。

原因很简单:在真实商业场景里,企业、商户和个人最终还是需要用本地货币来收款、付款、记账和结算。

所以,当资金流涉及不同国家、不同货币和不同银行体系时,只依赖美元稳定币,并不能完全消除外汇兑换、出入金、预存资金和本地清算等摩擦。

本地货币稳定币的价值在于:把本国货币直接带到链上。这样企业和用户既可以保留本币资产敞口,又能获得链上即时结算和跨境流动性的优势。

这也自然引出了另一个趋势:链上外汇。

用稳定币做跨境支付,本质上离不开链上外汇。但这个市场还没有真正起飞,主要有两个原因:

第一,很多国家的稳定币监管框架仍不够明确。

例如韩国多年来一直通过银行联盟和 Sandbox 探索韩元稳定币;加拿大也是在 QCAD 推出五年多后,才开始开放不依赖证券化结构的监管路径。不过,监管确定性正在明显提升,尤其是在美国 GENIUS Act 和香港稳定币条例落地之后,全球稳定币监管正在进入更清晰的阶段。

第二,非美元稳定币发行方往往需要从零搭建本地基础设施。

这包括本地银行合作、储备管理、铸造 / 赎回通道、合规流程和清算网络。不同国家的银行体系和监管要求差异很大,所以落地难度远高于单纯发行一个链上资产。

因此,链上外汇真正缺的,不只是更多币种,而是一套完整的机构级基础设施。

而 Circle 最新推出的 StableFX,本质上更像是在搭建一个链上版本的外汇网络。其核心思路是把传统外汇市场的流动性、报价机制和结算逻辑搬到链上,让不同本地货币稳定币之间可以更高效地完成兑换和结算。

for more details go check out the full article below🔥🔥

Jun 1

USD stablecoins dominate 99% of the market.

But the other 1% just grew 16x in 3 years.

Local currency stablecoin supply is up 70%. On-chain transfer volume went from $600M to $10B. EURC is live on Aave and Visa Direct. BRLA hit $400M transfer volume in Feb 2026. XSGD is quietly settling Grab × Alipay in the background.

And @circle StableFX is now trying to connect all of them — with RFQ mechanics and PvP atomic settlement. Essentially an on-chain FX network.

The $9.6T/day FX market hasn't been disrupted yet. But the plumbing is being laid — and most people haven't noticed.

Full breakdown 👇

medium.com/@gate_ventures/th…

2

323

chingchalong♣️🇭🇰|𝟎𝐱𝐔 retweeted

@Kinetiq_xyz 这次 call 也算是打中了。

YTD 已经跑出 4.6x 涨幅,现在基本可以视为 HYPE 生态的 beta 标的。

Trade.xyz 目前没有直接可投的标的,相比之下,Kinetiq 应该是最符合 HIP-3 逻辑的一个方向。

有兴趣的话可以翻阅一下之前写过的相关研究。LFGGGG foresightnews.pro/article/de…

2

3

380

chingchalong♣️🇭🇰|𝟎𝐱𝐔 retweeted

May 28

Welcome to Gate Ventures' very first podcast episode! 🎙️

Is DeFi dead? We go deep with Sonya Kim @sonyasunkim, Co-Founder of 3F Labs @3f_xyz, on the real mechanics of on-chain RWA leverage — and why carry trade is the next explosive opportunity in DeFi.

🎧 Now available on YouTube and Spotify!

・YouTube: youtu.be/05oRWihHlAY?si=WbF9…

・Spotify: open.spotify.com/episode/0DD…

——

🔑 Key Takeaways:

✅ DeFi isn't dead? — but recent exploits set the industry back 6–12 months

✅ Stablecoin supply growing 5x faster than crypto market cap

✅ RWA is the only sustainable fix for DeFi's cyclically collapsing yields

✅ 3F's Bridge Facilitator builds your full leveraged position in one settlement cycle — no more 20-day waits

✅ Four-layer capital stack: leverage LPs, BFs, Morpho depositors & liquidators

✅ Why JAAA CLO (Centrifuge × Janus Henderson) was chosen as the first asset

✅ Founder advice: find PMF in DeFi first, then scale with TradFi distribution

——

#GateVentures #DeFi #RWA #Web3 #Podcast #3F #3FLabs

91

93

143

8,324