The ETH must flow

Joined March 2018

- Tweets 4,875

- Following 1,386

- Followers 1,570

- Likes 58,812

550 Photos and videos

Pinned Tweet

24 Nov 2025

1/ Been thinking a lot about this lately:

What if the cycle everyone was waiting for actually ended in early December 2024 and we’ve already been in a bear market for almost a full year? The OTHERS chart (total crypto market cap excluding the top 10 coins) is the best way to visualize this.

3

7

1,196

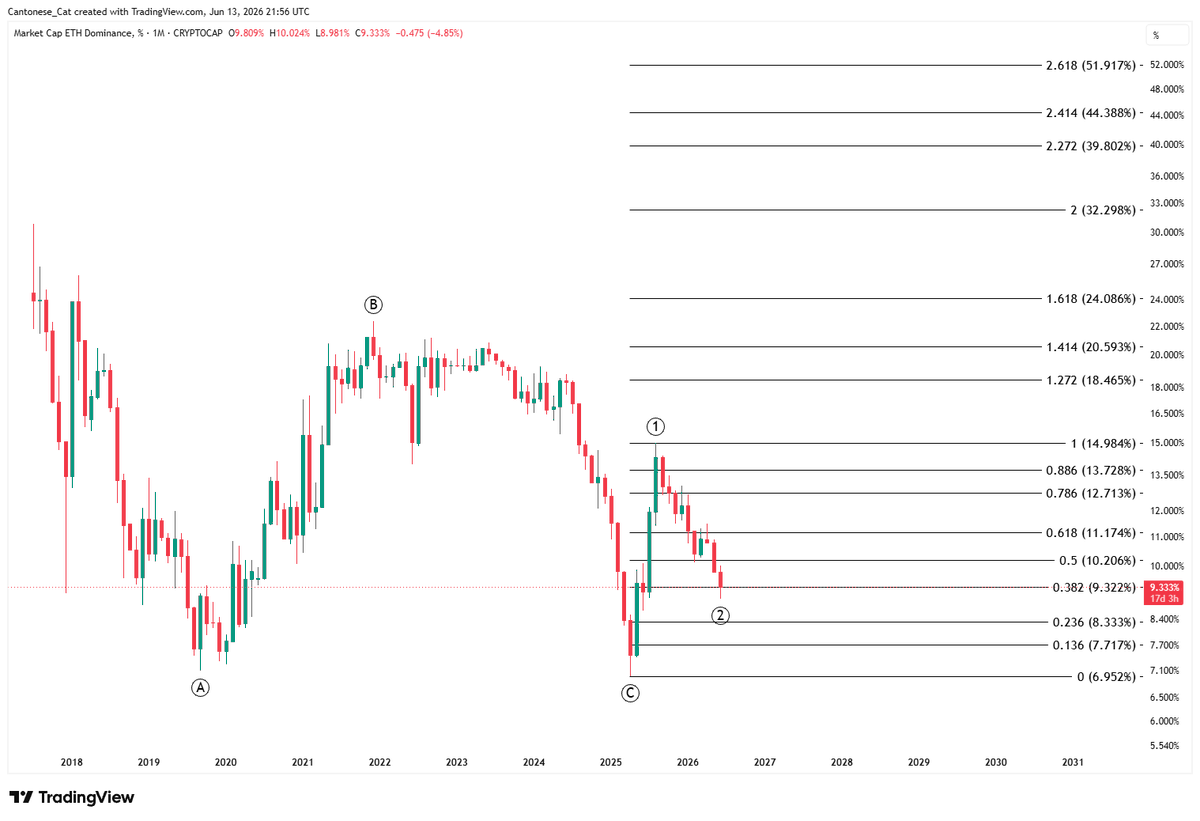

Imagine the smell when ETH.D reaches the 1.618 extension level

1

7

203

Culgin.eth retweeted

I need you to stop scrolling and try to understand something.

@jvisserlabs hasn't been perfect on everything, but he has called markets much more accurately than most. For decades.

The whole market has been two steps behind him on AI investing since this all started.

What is Jordi buying right now?

Ethereum.

Jordi Visser is buying $ETH.

Not loudly. Not even aggressively. He's just calmly building a position while everyone else top blasts AI.

Read this over and over until you understand what's happening here.

Two of the most prominent macro analysts alive, who built their careers at Goldman and Morgan Stanley, agree on this.

Raoul said Ethereum was, "fking obvious."

You don't have to agree with them on everything. I'm not telling you what to do.

What I am saying is simply, try to understand this.

Jun 13

Jordi Visser: The third wave of crypto is already being set up - and most people are dumping at exactly the wrong moment.

"The third wave of crypto, I already know what it is."

Financial guardrails (transactions, velocity of money) will be essential for billions of "token-hungry digital employees."

When the physical capex trade peaks, capital needs somewhere to go.

"If Nvidia and all of these companies stop going up, probability of crypto going up goes up much faster."

FT @RaoulGMI @jvisserlabs @RealVision.

4

14

84

15,700

Jun 13

It is easy to replicate speed and scalability but it is extremely difficult to do the same for decentralization.

Very few understand this

To think Ethereum is easily replicated completely misses the mark on what Ethereum actually is

Yet many a VC or Bitcoiner will try and tell you otherwise

But as we see time and time again, these ‘killer’ projects will fade away after the hype

The beauty of Ethereum lies in its decentralisation and origin story

And again, Bitcoiners will have you believe something else and will yell ‘premine’ as loudly as they can

But, again, this misses the mark

The power of Ethereum lies within the innocence of its organic and grassroots growth, just the same as Bitcoin

A decentralised network supported by enthusiasts, not knowing if what they are supporting is actually valuable or not

This can not be replicated today

Time is the one thing VCs can’t buy

There is no second best I love you

2

9

516

Jun 13

Everyone gets to buy ETH at the price they deserve

Would you be saying this if ETH was $10K?

@TrustlessState and i squared off on Ethereum for 30 mins yesterday.

I think i'm getting to him.

1

46

Culgin.eth retweeted

Jun 12

ETH investor Stanley Druckenmiller: “Our whole payment system will be stablecoins in 10-15 years”

BitMine (BMNR), the ETH treasury company chaired by Tom Lee, holds almost $10 billion of ETH. Legendary investor Stanley Druckenmiller is listed among key backers like Founders Fund, ARK's Cathie Wood, and Bill Miller. This aligns with his recent bullish comments on stablecoins and blockchain payments:

“Blockchain and the use of stablecoins — if you want to throw crypto and tokens into that — are incredibly useful in terms of productivity. I assume our whole payment system will be stablecoins in 10-15 years. Efficient. Quicker. Cheaper.”

28

122

690

112,841

NICE

The evolution of money is underway.

Fidelity Digital Dollar (FIDD) is a stablecoin issued by Fidelity Digital Assets, National Association, a subsidiary of Fidelity Investments.

Get in touch to learn more: go.fidelity.com/XNvH1q

1

6

43

3,807

Jun 12

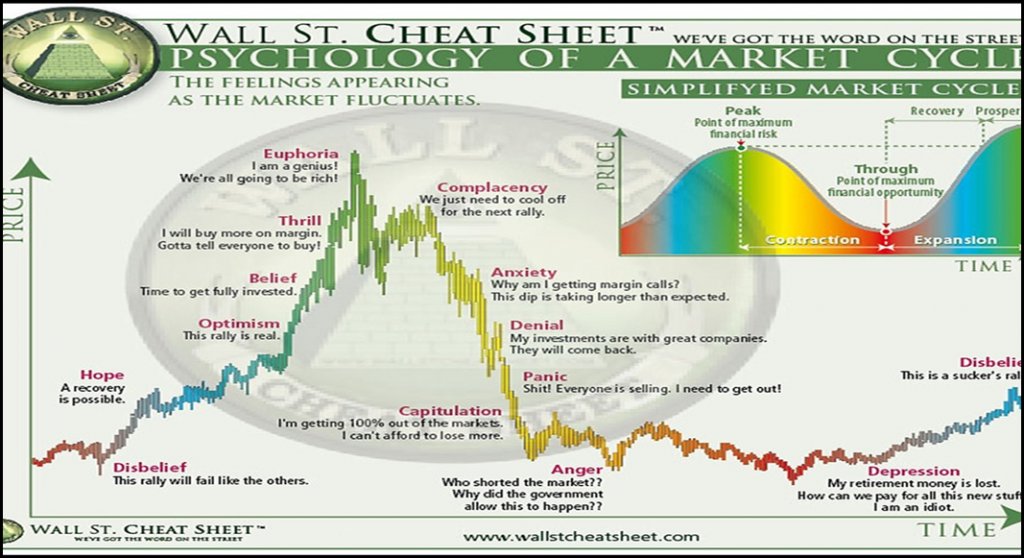

Feb was the Panic Capitulation Anger and we are probably in depression now.

Good period to accumulate for the longer term. Feeling much more comfortable to shill crypto to my normie friends at these prices.

Jun 11

.@JustDeauIt found something that doesn't fit the bear market narrative.

bitcoin:native broke below the 200-week moving average.

Yet sentiment never reached the panic levels we saw in February.

“People were more scared in February.”

That divergence is worth paying attention to 👇

5

415

Jun 12

If Ethereum becomes the dominant settlement layer, ETH functions less like a stock and more like a scarce reserve commodity-money hybrid — closer to spice (in the Dune universe) than to a typical asset.

Jun 11

The augment that ETH is just a gas token to prevent spam therefore it’s worthless is nonsense.

Claude charge by token is also a way to prevent spam (especially from the subscription plan).

The point is that llms are actually useful and therefore the token and its equity is valuable.

ETH will also be valuable once we bring DeFi back, the real DeFi.

4

9

80

3,596

Jun 12

What if this is Apr 2025 but playing out over a longer duration?

ethereum:native

1

1

16

692

Culgin.eth retweeted

Jun 11

⚡️This print is the war premium photographed in transit through the pipeline, and the divergence inside it is the entire story.

Headline 1.1% against 0.7% expected, while core misses at 4.9% against 5.4%.

A fifty basis point downside miss on core YoY is a large miss, the kind that moves a regime read.

Strip the energy shock out and the real signal appears: pass-through is failing. Core goods fell outright at the consumer level. Wholesale margins are compressing. Producers are eating the war premium instead of passing it on, because demand is too weak to accept the pass-through. That is a slowdown wearing an inflation print’s clothing.

Put the energy shock back in and the pipeline is on fire. Both are true at once because they are two different phenomena sharing one index: a geopolitical supply shock layered on top of a cooling core economy. The number contains a war and a slowdown, and the market that trades the headline will misprice the second one.

The “Fed is trapped” framing is the consensus read, and it has the logic inverted.

The print untraps them.

Rate policy cannot reopen Hormuz, cannot clear mines, cannot restart tanker traffic. Hiking into a supply shock buys nothing on headline while crushing a core economy where margins are already absorbing the damage. Meanwhile the core miss hands Warsh exactly the analytical cover his position requires: he can stand at his first meeting on the 16th and say the underlying trend is contained, the headline is a war tax that monetary policy cannot fight, and patience is the credible posture.

A chair installed by a president who wants cuts, walking into his first FOMC with core missing by half a point. This print is his permission slip, delivered five days early.

The deeper structure: the inflation trade and the Iran trade have now fully merged into one trade.

If core is contained and margins are absorbing the shock, then the entire remaining inflation problem is the war premium, and the war premium resolves through the deal, not through the Fed. Which means the actual reaction function for US inflation currently runs through Doha and Lebanon, not through Eccles. The Fed’s mandate has been functionally outsourced to foreign policy for the duration of the containment process.

And follow that one step further, because this is where the regime shows itself. The administration controls the deal that controls oil that controls headline inflation, and it installed the chair who decides how to respond to that inflation. Both ends of the inflation problem, cause and response, are now held by the same actor. Trump can manufacture the disinflation headline by closing the deal, then collect the rate cuts from the chair he appointed, and the data will validate the whole sequence because core was genuinely contained underneath.

That is the institutional mutation in live operation: monetary policy as a downstream variable of White House statecraft, with the data cooperating.

Jun 11

PPI 1.1% MoM, Exp. 0.7%

PPI Core 0.4% MoM, Exp. 0.5%

PPI 6.5% YoY, Exp. 6.4%

PPI Core 4.9% YoY, Exp. 5.4%

2

6

67

22,244

Culgin.eth retweeted

Jun 11

Looks like the options thing is happening already!

See also: various people thinking through and building different versions of the idea in the thread: ethresear.ch/t/building-inde…

Though I do strongly urge that if any of these get on mainnet quickly, we formally verify it first. I hope @vyperlang and/or github.com/lfglabs-dev/verit… folks ( @Fricoben) can help!

(Also, now is a good time to be thinking about robustness-optimized oracles)

firefly.social/post/x/206494…

452

248

1,609

251,433

Jun 11

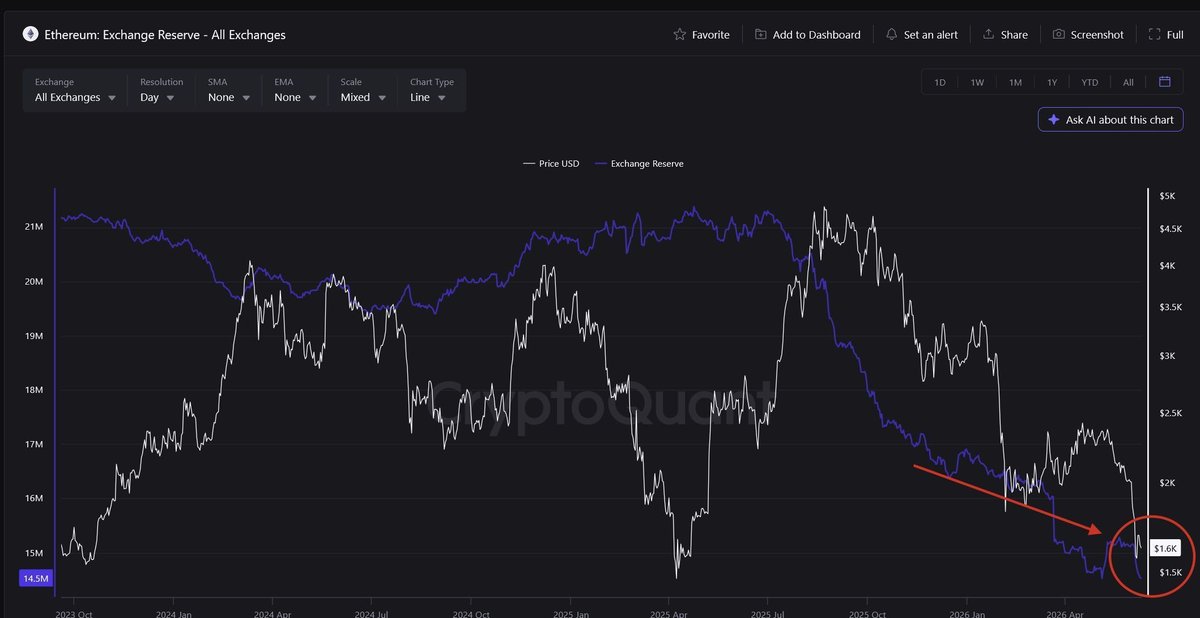

The lower the exchange supply the quicker the bounce when demand emerges.

Selling your spot ETH is one thing but shorting ETH is poor r/r at this point

Jun 11

🚨ETHEREUM'S EXCHANGE SUPPLY JUST HIT AN ALL-TIME LOW

ETH held on exchanges has fallen to just 14.5m ETH, the lowest level on record.

More than 6 million ETH has been withdrawn from exchanges since late 2023, as ETFs and corporate treasury buyers continue accumulating.

3

1

25

1,574

Jun 11

I still love Ethereum

2

28

546

Culgin.eth retweeted

Jun 10

Danny Ryan on why Wall Street cares about Ethereum's decentralization

Etherealize co-founder and a key architect behind Ethereum’s transition to proof-of-stake is asked if Wall Street institutions care about “decentralization.”

“That’s not the right word,” Danny replies. “They care about counterparty risk.”

He explains:

“They care about — in a transaction or a particular market — who can screw me over? And if the infrastructure is decentralized, nobody can turn it off, and their transactions will execute as intended . . . [that’s an] elimination of counterparty risk. That’s the operative lens of how they view the world, and if you explain how these systems work to them — and the difference between Ethereum and alternatives — they’re like, ‘Oh yeah, we do love decentralization because we have risk models and this helps us on our risk model.’”

Danny jokes:

“I’ve been looking for a customer of decentralization other than the cypherpunks I hung out with for the past 8 years, and I found it on Wall Street.”

As long as you speak the right language and frame it the right way, Ethereum’s decentralization is deeply important to Wall Street institutions.

19

47

353

22,555

Culgin.eth retweeted

Jun 10

Bitcoin spends roughly 93% of its history with more than half the supply in profit.

Currently, only 50% of supply is in profit, meaning we are in the bottom 7% of all historical readings.

These are not normal market conditions.

They are rare, uncomfortable, high-stress accumulation zones.

6

32

238

13,555

Jun 10

ETH is the easiest story for Wall Street to sell to retail when the time is right

Jun 9

Wall Street missed the $1k-$20k move in Bitcoin in 2017.

What do you think they are setting up for ETH?

C'mon THINK.

5

4

89

9,522

Jun 10

The more negative comments on ETH I get from my posts, the more bullish I get

8

3

84

2,305

Culgin.eth retweeted

Jun 9

NEW: The Official Prediction Market Partner of the @FIFAWorldCup is now powered by Chainlink.

@Predictstreet has adopted Chainlink as its exclusive oracle infra to enable accurate market resolutions & unlock instant payouts for the world's largest sporting event with 6B fans.

ADI Predictstreet has adopted @Chainlink as the exclusive oracle infrastructure for our FIFA World Cup 2026™ prediction markets.

Accurate resolution. Instant payouts. All at the speed of play.

61

291

1,337

106,683

Jun 9

Max pain is ETH outperform every other asset for the rest of the year

27

13

306

12,462

"I really think Ethereum's best time is yet to come."

The first decade of smart contracts was about building the infrastructure. The decade of real-world adoption has started, and Ethereum's role has to change with it.

@adietrichs of @ethereumfndn on the Main Stage at ETHConf.

5

24

199

6,978