AI & Markets. Yale/HBS. For sports/more check out @DavidMTodd

Joined January 2025

- Tweets 475

- Following 679

- Followers 138

- Likes 764

8 Photos and videos

AI/Markets-DT retweeted

Jun 13

I’ve had a number of conversations with folks inside and outside government about the current situation with Anthropic, and here is what I believe to be true:

— As we know, Anthropic publicly released its Mythos class models earlier this week under the commercial name Fable.

— Fable is Mythos with guardrails. But if those guardrails fail, then you’ve exposed Mythos and its advanced cyber capabilities to people who shouldn’t have them. (Keep in mind that Anthropic itself widely promoted the idea that Mythos was a cyberweapon and needed to be regulated as such. They asked for government regulation of Mythos and championed the guardrails on Fable. If there is a vulnerability — big or small — it is Anthropic’s responsibility to patch.)

— A highly credible trusted partner of both Anthropic and the USG who was testing Fable came forward with a jailbreak of those guardrails. The Admin asked Dario to fix the jailbreak or de-deploy the model. Dario refused.

— In their blog post, Anthropic defended its decision by saying the jailbreak isn’t serious. That is not what the trusted partner and the USG believe; nor is that kind of minimizing language consistent with Anthropic’s brand as the AI safety company. It’s difficult to fathom how they could claim a jailbreak allowing operability of a cyber weapon could be defined as not “serious.”

— In the past, Anthropic has always said that safety must be top priority and taken super seriously. In this case, Anthropic prioritized the continued offering of the consumer model over safety.

— In reaction, the Admin issued the export control. The Admin did this reluctantly. It’s been very surprised that Anthropic hasn’t wanted to cooperate with a reasonable safety request (ie fixing the jailbreak issue). Anthropic’s reaction is very much at odds with their branding and ethos as a safe AI research community.

— The Admin’s hope now is that Anthropic remediates the safety issue, the export control is lifted, and Fable goes back into general release. The Admin wants all of this to happen as soon as possible. It is frankly bewildered that Anthropic hasn’t wanted to comply with safety requests that it previously said were its highest priority.

— Those trying to misdirect and tie this action to the prior DoW/Anthropic issues are wrong. The Admin values Anthropic’s technical capabilities and feels that this issue, while serious, should be easily resolved. The ball is in Anthropic’s court.

2,172

3,192

25,049

7,502,091

AI/Markets-DT retweeted

Jun 13

Tyler Cowen on the Fable/Mythos event. The issue with point 5 is that we are probably less than a year away from powerful RSI. Once automated researchers reach parity, the USG 𝘤𝘢𝘯 nationalize the labs and run them effectively, without any of the people currently working there.

Jun 13

A few thoughts on the recent Mythos brouhaha: marginalrevolution.com/margi…

53

55

656

85,406

AI/Markets-DT retweeted

Jun 2

Here's the talk on neutral atoms and qday youtube.com/watch?v=XEGK0Ot1…

5

30

307

105,891

AI/Markets-DT retweeted

Jun 2

Today a crazy quantum story just got wilder.

On March 31, the Google Quantum AI team published a landmark result on Shor's algorithm for elliptic curve cryptography. Technically, the paper was a bombshell: a dramatic 10x improvement over the state-of-the-art. As a stunt and wakeup call to the blockchain space, those optimisations were illustrated on secp256k1, the elliptic curve underlying Bitcoin and Ethereum signatures.

But perhaps the most striking part of the paper was sociological, not technical. Instead of following standard academic process, the optimisations were kept secret, hidden behind a zero-knowledge (ZK) proof. Google's accompanying blog post mentions they "engaged with the U.S. government". The ZK proof demonstrates the existence of algorithmic improvements without leaking details. Academic censorship with ZK, a historic first!

As a co-author of the Google paper I witnessed some of the context surrounding this censorship. To be honest, multiple aspects of that context don't sit well with me. As much as I believe the general public ought to know more, I am limited in my ability to whistleblow. Though let me be clear about one thing: the Google team's professionalism has been absolutely exemplary, and they deserve nothing but praise.

Censorship has a way of backfiring. The Streisand effect, where an attempt to bury something only draws more attention to it, is exactly what's unfolding today. First, Google's key optimisation has been rediscovered by the French. And in a thrilling turn of events, a collaborative Shor-at-home challenge just launched. The initiative, available at ecdsa[.]fail, breached a new Shor world record in a matter of hours.

Let's start with the rediscovery. Just two months after Google's paper, French quantum expert André Schrottenloher cracks the main secret optimisation. His paper, titled "Optimized Point Addition Circuits for Elliptic Curve Discrete Logarithms", landed on the arXiv today. Big congrats to André, who beat several other nerdsnipped experts to it. In a blog post also published today, Craig Gidney, the world expert on Shor optimisations, revealed that he'd been sitting on this very optimisation for a whole year under censorship pressure.

Interestingly, André missed a handful of minor optimisations, both from Google's original publication and from improvements found since. It's plausible there's still plenty of juice left to squeeze out of Shor, and this is exactly what the ecdsa[.]fail challenge is about. The verifier program developed for the ZK proof does double duty, automatically filtering for valid submissions. Dozens of compounding small and micro improvements are rolling in. As of the time of writing there's an 8.4% improvement to Google's circuit, as measured by the product of logical qubit count and Toffoli gate count. Nice!

The nerdsnipping ran deeper than anyone expected. Over the last few weeks it became clear it extended well beyond André and other quantum experts. Behind the scenes, a small army of amateurs quietly got to work. Inspired by Karpathy-style autoresearch, they turned AI on Shor. Ironically, the verifier program for the ZK proof makes an ideal reward function for AIs. The barrier to entry for this modern style of research is refreshingly low, with several non-experts, even a teenager, finding nice optimisations. Get in touch if you'd like to join a Telegram group with fellow autoresearchers :)

Part 2: neutral atoms and qday

The story doesn't end with Google. On the same day Google went public, a stealthy startup called Oratomic published its own Shor paper in a coordinated release. It made a splash, ultimately becoming the most upvoted paper on scirate[.]com, a website ranking arXiv papers.

Oratomic's claim was wild. By building on Google's logical optimisations and applying custom physical optimisations for neutral atoms, they claimed just 10K physical qubits were sufficient to run Shor's algorithm on secp256k1. That number is mind-bogglingly low.

Knowing essentially nothing about neutral atoms when Oratomic's paper landed, I was intrigued and decided to learn more about the tech. I fell straight down the rabbit hole and spent a couple hundred hours on the topic. I got a little obsessed and watched every YouTube video I could find and spoke to a bunch of experts.

My conclusion? The tech is real, very real. Even Google recently decided to start a neutral atom lab, a notable pivot from their sole focus on superconducting qubits. If you care about qday, i.e. the day a quantum computer will break the first piece of cryptography in production, neutral atoms demand your attention. I shared some of my learnings on Shor and neutral atoms in a 30min talk at the ZKProof cryptography conference. You can find it on YouTube by searching "zkproof neutral atom".

Here's an interesting observation about this duo of breakthrough papers: neither Google nor Oratomic say a word about what their results mean for qday. No timelines. Zero. Nada. That is especially baffling given that the whole point of whitehat quantum cryptanalysis is to inform qday estimations and help the general public make good decisions.

So let me attempt to partially fill the silence, similarly to what Scott Aaronson did in his April 29 post. Given everything I know, including scary non-public information, I now put the odds of qday by 2032 at 50%. 10% by 2030.

Anecdotally, the US government has its own date: 2035. Originating at the NSA and later adopted by NIST, it's when branches of the US government will be disallowed from using quantum-vulnerable cryptography. In plain language: with hindsight, that date is a joke and should be discounted entirely. I don't see how NIST avoids being forced to pull it forward by years.

Part 3: post-quantum cryptography

There are good reasons to sound the alarm today, but please do not panic. Rushing carelessly towards immature post-quantum cryptography is a recipe for disaster. IMO a good target date for migration is 2029, roughly 3.5 years out. 2029 happens to be the date selected by Google, Cloudflare, and the Ethereum Foundation.

These days most of my time goes to safely migrating Ethereum towards post-quantum cryptography as part of the broader lean Ethereum effort. There's a lot to do. We need to rip out and replace BLS signatures at the consensus layer, KZG commitments at the data layer, and ECDSA signatures at the execution layer.

The plan to get there is compelling, and is based on hash-based cryptography. Within the Ethereum Foundation we've developed a Swiss army knife called leanVM (github[.]com/leanEthereum/leanVM) powered by the magic of hash-based SNARKs. Thanks to truly exceptional work by Emile, Thomas, and others, its performance is derisked. Regarding security, leanVM is a jewel, a minimal zkVM crafted for end-to-end formal verification and maximum security.

Want to help? There are two $1M initiatives. First, the Proximity Prize (proximityprize[.]org). Solve a long-standing mathematical conjecture in coding theory, improve hash-based SNARKs, and go home a millionaire. Second, the Poseidon Initiative (poseidon-initiative[.]info), offers $1M for breaking Poseidon, the SNARK-friendly hash function.

408

1,128

6,247

3,705,672

AI/Markets-DT retweeted

May 26

I have been very impressed by @SemiAnalysis_ . I think of myself as a wide ranging systems engineer, looking for value at every level from the chip specs to the user interface, but SA exposes me to additional levels of "the system", both above (datacenters) and below (semiconductor fabrication). It probably puts me in "just knows enough to be dangerous" territory.

Neat things I learned today:

Some of the 800VDC datacenter design choices leverage parts commoditized by electric vehicles.

There is now a SiC MOSFET that can operate on 10kV electricity, opening up the possibility of working directly with medium (ha!) voltage AC power transmission lines without stepping down.

86

132

3,028

505,947

AI/Markets-DT retweeted

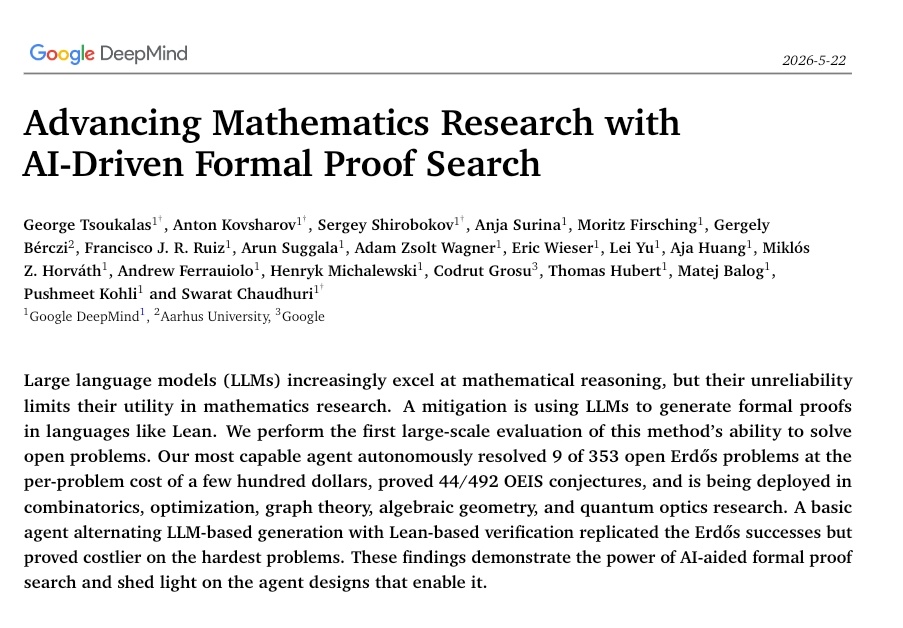

Another 9 open Erdos problems solved, this time by DeepMind team.

Interesting loop of LLM - Lean agents working autonomously, and only after it's verified formally, going through human review.

80

400

2,740

675,689

AI/Markets-DT retweeted

May 22

Everyone is focusing on the soaring memory cost in the Vera Rubin rack. But the real shocker in this Morgan Stanley slide is actually power, because the industry is now talking about moving from roughly 120kW per rack today toward potentially 600kW per rack by the Vera Rubin Ultra generation in 2027, which is an almost unimaginable escalation in power density within an incredibly short period of time.

To put this into perspective, many traditional enterprise datacenters historically operated at only a few kilowatts per rack, while even modern hyperscale campuses today often consume only tens of megawatts in total facility power draw. But once you begin deploying hundreds or thousands of 600kW AI racks simultaneously, the math becomes almost absurd because a large-scale Vera Rubin Ultra cluster could eventually consume gigawatts of electricity, effectively rivaling the energy demand of a mid-sized city.

And this is where the market still massively underestimates the second-order implications of the AI boom, because the bottleneck is no longer simply semiconductors, GPUs, or memory supply. The bottleneck increasingly becomes electricity itself.

The US power grid can barely keep up with current AI infrastructure demand already, while transmission congestion, transformer shortages, substation constraints, cooling limitations, permitting bottlenecks, and aging grid infrastructure are becoming increasingly visible across major datacenter hubs. Importantly, grid infrastructure cannot scale at semiconductor speed. You can accelerate chip production with enough capital expenditure and engineering talent, but building transmission lines, substations, generation capacity, cooling systems, and interconnection approvals often requires many years due to environmental reviews, local opposition, labor shortages, and physical construction constraints.

This is precisely why we continue believing the AI buildout is not a two-to-three-year investment cycle, but instead a decade-long industrial transformation that increasingly resembles the buildout of railroads, electricity networks, and telecom infrastructure during previous industrial revolutions.

And this is also why energy infrastructure is quietly becoming one of the most important and underappreciated AI trades globally.

The winners are no longer just GPU companies. The winners increasingly include utilities like Constellation Energy and Vistra, nuclear-related plays like Oklo and NuScale Power, gas infrastructure companies like Kinder Morgan and Williams Companies, grid and electrical equipment suppliers like GE Vernova, Eaton, Schneider Electric, and Vertiv, as well as transformer, cooling, and datacenter infrastructure providers that now sit directly inside the physical backbone required to support next-generation compute.

Hyperscalers themselves are starting to understand this reality. Companies like Microsoft, Amazon, Alphabet, and Meta are no longer simply software companies buying servers. They are increasingly becoming quasi-energy infrastructure companies because securing long-duration power availability is becoming strategically inseparable from securing compute capacity itself.

That is why nuclear power is quietly returning to the center of the conversation. Hyperscalers may eventually fund or directly partner on nuclear generation projects out of pure necessity because renewable intermittency alone cannot reliably support ultra-high-density AI clusters operating continuously at scale.

In many ways, AI is beginning to collide with physical reality. You cannot run trillion-dollar next-generation compute infrastructure on transmission systems and grid architectures that were largely built decades ago for a completely different industrial era.

The semiconductor story may have started the AI race, but energy infrastructure may ultimately determine who wins it.

36

145

799

225,781

AI/Markets-DT retweeted

Gavin Baker: "I've been optimistic that the fundamental shortage of wafers, which is really controlled by Taiwan Semi, will prevent a bubble."

"If Taiwan Semi did what Jensen wanted, Nvidia could sell $2 trillion of GPUs in 2026 or 2027.

But there is a limit where consumers would consume so much that you'd probably be in an overbuild.

And you are starting to see companies go to Intel and Samsung.

A lot of this may come down to the degree to which Taiwan Semi can maintain a lead over Intel and Samsung and the pace at which they expand capacity.

If I were to watch one thing to understand whether there's a bubble, it's Taiwan Semi's capacity decisions.

There's a Goldilocks zone where they expand enough to make it hard for Intel or Samsung to emerge as a second source, but they also keep the fundamental constraint on wafers that helps us avoid a bubble."

This is my sixth conversation with @GavinSBaker.

As always with Gavin, the conversation covers a lot of ground, but we spend the most time on watts and wafers.

We discuss:

- Why the wafer shortage may prevent an AI bubble

- Data centers in space (reframed)

- Elon's Terafab and the new chip companies challenging Nvidia

- Usage-based pricing

- The disaggregation of GPUs

- DRAM, frontier tokens, and open source

Enjoy!

Timestamps:

0:00 Intro

7:55 Anthropic and OpenAI Valuations

12:58 Watts, Wafers, and Infrastructure

14:39 Orbital Compute and Data Centers in Space

22:49 Avoiding the AI Bubble

28:26 Terafab and the Future of US Manufacturing

32:16 Returns to the Frontier

37:23 Continual Learning

42:03 New Chip Companies

48:52 Extending GPU Lifespans and Private Credit

51:22 The Application Layer

57:32 The Token Path and Open-Source Dynamics

1:01:37 Cybersecurity

1:05:46 Diversity Breakdown

1:11:59 Assessing the Big Tech Players in AI

1:19:02 Geopolitics, Personal Safety, and the AI Horizon

33

89

941

540,215

AI/Markets-DT retweeted

May 20

Banger take

Gavin Baker: "I've been optimistic that the fundamental shortage of wafers, which is really controlled by Taiwan Semi, will prevent a bubble."

"If Taiwan Semi did what Jensen wanted, Nvidia could sell $2 trillion of GPUs in 2026 or 2027.

But there is a limit where consumers would consume so much that you'd probably be in an overbuild.

And you are starting to see companies go to Intel and Samsung.

A lot of this may come down to the degree to which Taiwan Semi can maintain a lead over Intel and Samsung and the pace at which they expand capacity.

If I were to watch one thing to understand whether there's a bubble, it's Taiwan Semi's capacity decisions.

There's a Goldilocks zone where they expand enough to make it hard for Intel or Samsung to emerge as a second source, but they also keep the fundamental constraint on wafers that helps us avoid a bubble."

31

35

838

170,050

AI/Markets-DT retweeted

May 19

Personal update: I've joined Anthropic. I think the next few years at the frontier of LLMs will be especially formative. I am very excited to join the team here and get back to R&D. I remain deeply passionate about education and plan to resume my work on it in time.

7,989

11,150

150,232

27,570,657

AI/Markets-DT retweeted

May 15

From DGX to DSX — NVIDIA’s Secret Weapon Is $IREN

DGX was the pivotal turning point that transformed NVIDIA from a chip company into a systems company. From the original ambition of creating a “unified data center standard,” DGX encountered resistance from the hyperscalers. They refused to adopt NVIDIA’s unified standard and instead developed their own chips, frustrating NVIDIA’s vision of becoming the dominant systems platform of the AI era. Google is perhaps the most notable example: after initially falling out of the core AI race, it rapidly recovered and mounted a full-scale counterattack, at one point nearly matching NVIDIA’s market capitalization and challenging NVIDIA’s status as the “godfather” of AI.

DGX failed to conquer the cloud giants’ strongholds. NVIDIA’s massive sales still primarily came from individual GPU chips, while its plan to establish DGX as a new systems standard combining GPUs and software did not succeed. However, strategically, DGX laid an extremely important foundation for NVIDIA. Customers could reject the complete DGX system, but they still had to remain compatible with NVIDIA’s software management stack, otherwise GPU performance could not be fully utilized. As a result, technologies such as NVLink, NVSwitch, and Base Command matured alongside the market, enabling NVIDIA to evolve from simply selling GPUs into a company with full-stack platform control capabilities, while solidifying its dominance in scientific computing and private cloud markets.

Entering the Blackwell era, the physical limits of power consumption, interconnect complexity, and liquid cooling made it impossible for the industry to continue operating independently. NVIDIA formally introduced the standardized AI factory architecture known as DSX, positioning it as the optimal path for building large-scale AI data centers.

From this point onward, DGX evolved into DSX.

In other words, it evolved from a “single-machine AI supercomputer” into a “data-center-scale AI factory standard,” completing the transition from standardizing one machine to standardizing an entire factory.

During the Blackwell generation, AI training systems pushed power consumption, interconnect complexity, and thermal management close to physical limits: single rack power draw surpassed hundreds of kilowatts, NVLink/NVSwitch topologies became dramatically more complex, and liquid cooling shifted from optional to mandatory. In theory, this generation already required a standardized architecture like DSX. However, the supply chain ecosystem was not yet mature, and no partner possessed the full engineering capability necessary to build a true “system-level AI factory.” As a result, DSX remained only a concept and reference design.

By the Vera Rubin era, NVLink 6, NVSwitch 6, and NVL72 rack systems formed a scalable, reproducible interconnect foundation, finally giving DSX the conditions necessary for practical deployment using NVIDIA’s full-stack technology. But that alone was still insufficient. To fully realize DSX, the industry also required:

High-density interconnected rack architecture capabilities

Large-scale liquid cooling expertise and construction experience

GW-scale single-site campuses with stable long-term power supply

These became the necessary conditions for constructing a flagship DSX factory.

And only one company in the world possesses all three simultaneously.

At this point, IREN enters the stage.

Beyond those three core requirements, IREN possesses several additional strategic characteristics:

Grid-based power supply.

First, grid power solves the stability problem. To become a flagship DSX standard site, power interruptions and voltage fluctuations are unacceptable. Large-scale grid infrastructure provides industrial-grade voltage stability guarantees. Second, relying on the grid offers superior cost economics. Third, it provides regulatory compliance as public infrastructure, removing the unpredictable risks often associated with behind-the-meter (BTM) power systems, which frequently carry “gray-area” or temporary characteristics and therefore lack sufficient long-term reliability.

GW-scale infrastructure.

This enables the creation of multiple DSX modular standards. Small and medium-sized data centers become trivial by comparison — deployments from 10MW to over 1GW can all be standardized. This makes IREN the ideal flagship demonstration platform. We already know there will likely be SW2 and potentially additional nearby expansion sites. The total power capacity is enormous. DSX only truly begins with Rubin, and the upgrade path beyond that will continue for many years.

Therefore, possessing ultra-large campus-scale sites within a single region is critically important. This advantage makes IREN the one unavoidable choice for NVIDIA. No other company possesses such massive strategic power infrastructure concentrated within a single region.

The long-term significance and moat of such infrastructure can hardly be overstated. Small scattered sites stitched together — even if they collectively total several GW — are simply incomparable to IREN’s grid-connected GW-scale campuses concentrated in single regions.

Green energy.

As global concern over AI energy consumption rises, future “carbon footprint” metrics will become core evaluation standards for sovereign AI procurement. IREN’s long-term commitment to renewable energy allows NVIDIA’s DSX standard to become not only “the most powerful,” but also “the greenest.” This is critically important for attracting national-level infrastructure customers.

Owned land and expansion capability.

DSX requires data centers to be constructed from the ground up, including specialized transformers, ultra-heavy rack support systems, and complex liquid cooling pipelines. Only companies with full ownership of their land can customize AI factories entirely according to NVIDIA’s blueprint without facing endless approval bottlenecks or third-party building restrictions.

Vertical integration and data center engineering expertise.

IREN is not merely a data center operator. It is one of the only vertically integrated companies in the industry that owns everything from greenfield development, site development, power procurement, to operations and maintenance. For a DSX flagship factory, NVIDIA needs a partner capable of rapidly executing its “reference designs.” IREN’s model of “designing, building, and operating everything itself” dramatically shortens the timeline from blueprint to first deployed GPU.

Liquid cooling capability.

DSX is fundamentally a liquid-cooled era architecture. Liquid cooling becomes a central requirement. IREN already possesses high-density rack deployment experience through the Horizon project. Its Chief Innovation Officer is one of the most influential and experienced engineering experts in the United States in data center liquid cooling, high-density thermal architecture, and ASHRAE standards systems. He joined IREN specifically to help establish standards.

Long-term operational data accumulation.

IREN has years of operational experience managing large-scale, high-heat-density facilities running at full load. The physical environment of Bitcoin mining is remarkably similar to AI inference: both involve 24/7 full-load operations with extreme thermal output. This long-term expertise in managing massive electrical and thermal loads is, in reality, an extremely competitive advantage within the industry.

From the analysis above, one can understand why IREN possesses such uniqueness and strategic importance in NVIDIA’s DSX ecosystem, while also inferring the likely development path of DSX itself:

DSX will likely follow a “top-down” design philosophy.

Using IREN’s massively scalable GW-scale sites and specialized engineering capabilities, NVIDIA can define a flagship standard that is “multi-scale, most advanced, most efficient, and greenest,” then deconstruct that blueprint into modular, reproducible AI factory units. In the future, whether it is a GW-scale campus or merely a company operating a single row of racks, as long as they purchase NVIDIA’s “DSX-certified package,” they could theoretically produce tokens with the same efficiency as IREN.

This strategy of “defining the upper limit, then distributing the standard downward” reflects NVIDIA’s true ambition to control the global AI infrastructure ecosystem.

IREN’s Sweetwater site — along with future surrounding expansion campuses — could become the incubation base for future AI intelligence factories. The scale of this project may become one of the largest engineering undertakings in human industrial history:

“Intelligent factories produce intelligence, and DSX defines how those factories are built and run.”

This concept has already moved beyond theoretical logic into actual execution. The reason I am able to describe this vision is because I have been observing this direction consistently for a long time. In reality, developments do appear to be moving this way.

The broader historical backdrop behind the emergence of the DSX system comes primarily from three major forces:

First, the rapid development of the AI industry has positioned DSX at the center of a major inflection point in compute infrastructure. DSX is a natural product of the industry reaching a new stage of maturity. AI is no longer confined to internal model training inside a few hyperscalers. The entire world now requires AI compute — including sovereign AI, enterprise private AI, neo-clouds, AI inference platforms, agent networks, token factories, vertical-specific models, and national AI infrastructure.

Many countries — particularly in the Middle East, Europe, and Southeast Asia — are unwilling to place core AI workloads inside the public clouds of U.S. tech giants due to data sovereignty concerns. Through DSX templates, NVIDIA can help these nations rapidly build their own “national AI factories.” Hyperscalers can no longer monopolize AI infrastructure. This has become one of the most important changes of the past two years, and it forms the foundational soil for DSX to grow.

Second, hyperscalers themselves are now constrained by power, land, permitting, transformers, and cooling systems. They are no longer in a state of unlimited expansion. AI inference also requires broader distributed deployment. In the future, there will be large numbers of regional AI factories, national AI nodes, and enterprise private clusters whose operators do not want to rely entirely on hyperscalers. Meanwhile, Google TPU, Amazon Trainium, and Microsoft Maia are all rapidly advancing. Over time, they may reduce GPU purchases, form closed ecosystems, and sell their own AI services externally — creating a strategic threat to NVIDIA. Therefore, NVIDIA must cultivate a “non-hyperscaler AI ecosystem.”

Third, by the Blackwell and Vera Rubin eras, single-rack power consumption has already reached the 100kW–200kW range. Traditional air cooling, cabling, and power topology can no longer support these systems. This means that if data centers are not built according to NVIDIA’s DSX standards — system-level liquid cooling, GB200 NVL72 architecture, and related infrastructure — they simply will not be able to run the highest-efficiency compute systems. In other words, physical laws themselves are forcing the market to adopt NVIDIA’s standards. DSX effectively becomes the “entry ticket” to the AI era.

Under this backdrop, DSX attempting to define the entire AI factory standard becomes a completely natural progression. It encompasses GPU architecture, network topology, liquid cooling standards, power design, rack standards, software orchestration, inference optimization, and token factory production pipelines — reflecting an ambition to turn AI compute into something like an “industrial iPhone operating system.”

After understanding the broader context, one can then better appreciate the deeper strategic meaning behind IREN’s acquisition of Mirantis.

To build a standardized flagship DSX factory, IREN already possesses massive GW-scale physical infrastructure, liquid cooling capability, and engineering expertise, but it still lacked the software layer needed to bridge “hardware” and “cloud services.” Mirantis perfectly fills this gap. Its deep experience in OpenStack, Kubernetes, and bare-metal management enables IREN to transform DSX into a directly usable cloud platform, allowing customers to immediately deploy AI workloads out of the box.

For NVIDIA, this acquisition enables its key partner IREN to free DSX from dependence on AWS, Google, and other cloud giant software ecosystems, establishing an independent vertically integrated stack. For IREN, the acquisition elevates it from a power and infrastructure supplier into a true “neo-cloud” platform capable of delivering sovereign AI and national-scale AI infrastructure.

Mirantis will also integrate NVLink topologies and DSX-specific features directly into software orchestration, enabling AI factories to achieve automated scheduling and token-level operational stability.

Although CRWV and NBIS also possess software with somewhat similar functionality, their stacks are largely designed for internal use and are difficult to standardize for export. Mirantis, by contrast, is inherently a cloud-native software company serving global customers. This allows IREN to transform DSX into an exportable “software-defined AI factory” template.

Its core product, k0rdent, can unify bare metal, virtual machines, and Kubernetes management while deeply optimizing for NVIDIA GPUs — a capability IREN could not realistically develop internally.

One could speculate that NVIDIA itself encouraged this acquisition (especially given how inexpensive the deal appeared, with IREN seemingly receiving extraordinary value). The ultimate objective may be to give DSX an independent software control layer outside AWS and Google while creating a sovereign AI solution deliverable globally. Mirantis upgrades IREN from a hardware host into the software brain of DSX, while giving NVIDIA a strategic ally in global AI infrastructure that is open-source-oriented, conflict-free, economically aligned, and technologically synchronized.

NVIDIA choosing not to acquire Mirantis directly — instead allowing IREN to do so — likely centers on avoiding antitrust concerns, maintaining delicate relationships with hyperscalers, and ensuring the software layer remains closely aligned with practical AI factory operations. An IREN acquisition appears as ecosystem collaboration rather than market domination.

At the same time, Mirantis software must deeply integrate with IREN’s GW-scale power, liquid cooling, and operations systems, making IREN the more efficient owner.

Financially, NVIDIA benefits through warrants tied to IREN’s growth without needing to bear integration costs itself. Through this strategy, NVIDIA effectively supports the emergence of a fully aligned DSX flagship manufacturing partner while preserving its own asset-light structure and strategic control position.

A full-scale DSX rollout would potentially:

Form the foundation for NVIDIA reaching a $10–15 trillion valuation

Become the inevitable path for NVIDIA’s vision of AI intelligence factories and operational control

Represent the most economical and efficient path for AI industry development

Solve the post–Vera Rubin scaling direction for compute growth

Become NVIDIA’s only viable method for breaking out of hyperscaler encirclement

IREN becoming the sole top-level collaborator in such a massive project could not have happened spontaneously. Planning something of this scale would likely require at least a year or more of preparation. Ever since interactions between NVIDIA and IREN began to appear unusually secretive, I have noticed multiple examples suggesting unusual behavior between the two companies — almost like two people who already know each other pretending not to in public.

Overall, they likely did not want the industry to speculate too early about their true intentions, while also minimizing regulatory attention. Even IREN, once an unusually transparent Bitcoin mining company, has become more guarded. In that sense, the limited interaction between IREN’s investor relations team and the market may actually make sense.

At this point, IREN has already completed the most difficult parts of its AI industrial expansion:

High-quality, massive-scale, long-term stable power supply, still growing further

Secured supply access to the latest GPUs

Developed engineering teams and supply chain maintenance capabilities

Obtained status as a flagship manufacturing partner for next-generation AI intelligence factories

The next inevitable step is filling IREN’s enormous power capacity with high-quality customer contracts. Unlike before, however, IREN may no longer need to build a traditional sales force or aggressively market its software capabilities. NVIDIA itself would likely help facilitate customer adoption while emphasizing the superior token-generation efficiency of the DSX system, because the economic interests of both companies are now deeply aligned.

Under the DSX standard, NVIDIA could gradually evolve from a “supplier” into a “global orchestrator.” Securing partnerships with companies like Anthropic would no longer be solely IREN’s concern. NVIDIA itself has strong incentives to push major AI companies already experimenting with TPU systems toward using more NVIDIA-based infrastructure.

Second, NVIDIA holds massive warrants in IREN. Every major contract signed by IREN potentially increases its stock price, allowing NVIDIA not only to profit from GPU sales but also from appreciation in IREN’s equity value. Jokingly speaking, one could say IREN “used warrants to buy itself a world-class salesman.”

Third, the emergence of sovereign AI has opened an entirely new market. Since IREN acquired Mirantis, the term “sovereign AI” has appeared increasingly frequently. In fact, when evaluating IREN’s sites originally, many observers already noted their suitability for sovereign AI deployments. The strategic quality of IREN’s sites is fundamentally incomparable to the fragmented infrastructure assembled by many competitors.

For NVIDIA, it needs a GW-scale “pure-blood” flagship to demonstrate to sovereign AI customers globally that NVIDIA’s DSX architecture can achieve superior token efficiency.

Sovereign AI customers may not want to hand their compute, data, models, or orchestration layers to the three major U.S. hyperscalers, but they may still accept supplier sovereignty. The distinction is subtle but important. IREN’s careful positioning and boundary management become critical here. Even the Mirantis acquisition did not overextend into hyperscaler territory; in fact, sovereign AI is already one of Mirantis’ core areas. From this perspective, NBIS may actually be poorly positioned for sovereign AI because its full-stack platform structure is precisely what sovereign AI customers are attempting to avoid.

Overall, IREN appears to be positioning itself at a point that maximizes strategic optionality and economic upside. If it attempted to define itself as a fully integrated hyperscaler-like platform, cooperation with a company at NVIDIA’s level would likely become far more difficult. This partnership with NVIDIA may sacrifice some of IREN’s historical emphasis on flexibility and optionality, but technological evolution tends to follow efficiency. The emergence of the “Magnificent Seven” itself demonstrates that antitrust frameworks increasingly must adapt to technological realities.

For IREN, the most important objective during this enormous capital expenditure cycle is rapidly establishing scale advantages. These data center assets ultimately become long-term hard assets fully owned by the company. The more infrastructure accumulated now, the greater IREN’s strategic flexibility becomes in the future. From that perspective, this is an extremely rational strategy.

As IREN gradually becomes one of the standard-setters for the next-generation compute ecosystem, it could eventually open additional monetization paths such as standardized AI factory design fees, consulting and licensing revenue, and software licensing income. Compared to its core business, these may remain relatively small, but the strategic value of occupying the top layer of the ecosystem could become nearly limitless.

Many people — especially institutions — already seem to recognize these dynamics. IREN’s stock price may not have risen dramatically yet, but its trading volume appears to reveal something unusual. The volume itself has become almost phenomenon-level behavior. Meanwhile, IREN’s $6 billion ATM facility has remained active, and immediately after earnings the company issued a $2 billion convertible bond deal, later increased to $3 billion due to overwhelming demand. The intensity of demand, favorable interest rates, and high conversion prices were genuinely surprising.

If the narrative described above is even partially correct, such investor enthusiasm becomes entirely understandable. Furthermore, the remaining $5 billion of ATM financing demand will likely be sold at significantly higher prices.

At this point, CRWV, NBIS, NSCALE, and LAMBADA increasingly appear to function as alliance members within NVIDIA’s broader ecosystem. Capital markets have seen constant fighting among supporters of the three neo-cloud stocks, especially between NBIS and IREN supporters — almost to the point of ideological warfare. But IREN may ultimately represent NVIDIA’s final and most important strategic move: the piece that controls the overall board.

Importantly, IREN achieved this position through its own decisions and execution. It was not merely “chosen” or artificially supported. Yet at the same time, NVIDIA likely must publicly deny any direct support relationship — readers can think carefully about the reasons themselves.

NVIDIA’s earlier strategic investments were designed primarily to secure the GPU deployment ecosystem. As the DSX system matures, companies like CRWV, NBIS, NSCALE, and LAMBADA may increasingly become deployment and implementation partners.

Interestingly, during the earlier NBIS-versus-IREN debates, some NBIS supporters argued that the two companies did not need to be adversaries and might eventually cooperate — for example, IREN leasing power capacity to NBIS. Looking at things now, cooperation indeed seems possible, but perhaps in the opposite direction: IREN may ultimately become the holder of the standard itself, licensing intellectual property outward.

Finally, this article is ultimately just speculative corporate-strategy fiction — written mainly for entertainment purposes, not investment advice.

57

80

570

233,150

Palantir cofounders Alex Karp and @JTLonsdale on discovering top talent:

“To appreciate talent, you need to be within a standard deviation of that talent.”

“People think they’re within a standard deviation of the best if they’re the second best, but it’s a different universe.”

“If you have people that are only one standard deviation above, they can’t even tell the difference between 4 and 5. They have no idea what’s going on at those levels. You need people who are good enough to even appreciate it.”

“I think it’s very similar to music. Very few people can hear the blue note. Almost no one can play it. We hear the blue note on the tech talent side.”

Via @AmOptimistShow

13

46

590

85,403

May 13

Would seem incredibly significant if Dean & Anton are correct.

May 13

Anton is on point here, as always.

Policymakers and other strategists tend to implicitly assume a level of frontier AI abundance that I do not expect to materialize over the next few years. Scarce frontier AI profoundly changes the political economy of AI.

1

46

AI/Markets-DT retweeted

May 13

AI strategies everywhere hinge on widely available American frontier AI. Post-Mythos, amid compute crunches, security concerns and distillation crackdowns, that paradigm is under threat.

Today, I argue the era of widespread access to frontier AI is almost over.

39

84

621

206,009

AI/Markets-DT retweeted

May 13

Anton is on point here, as always.

Policymakers and other strategists tend to implicitly assume a level of frontier AI abundance that I do not expect to materialize over the next few years. Scarce frontier AI profoundly changes the political economy of AI.

May 13

AI strategies everywhere hinge on widely available American frontier AI. Post-Mythos, amid compute crunches, security concerns and distillation crackdowns, that paradigm is under threat.

Today, I argue the era of widespread access to frontier AI is almost over.

11

28

244

33,016

AI/Markets-DT retweeted

May 11

The Inference Shift

Agentic inference is going to be different than the inference we use today, and it will change compute infrastructure because speed won't matter when humans aren't involved.

stratechery.com/2026/the-inf…

18

70

562

203,938

AI/Markets-DT retweeted

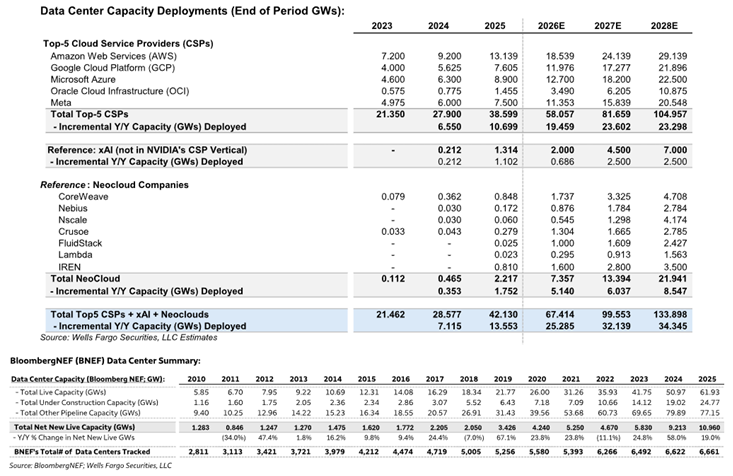

Current and forecasted data center capacity deployments in GWs by company:

Overall, by the end of 2026, 25 additional GW are expected to be deployed. By year end ’27 there should be an additional 32 GW, and by year end we should see an incremental 34 GW, bringing totals to about 134GW across hyperscalers and neoclouds per Wells

16

36

283

46,616

May 11

Circular nonsense. This is an all-time world salad. Obsession is great. Too a point. Unless it’s to achieve great things. Then it’s awesome. Extreme wealth may or may not be good. Depending your actions. Got it.

May 11

Mark Cuban just the quiet part out loud about billionaires:

Most of them are actually chill. They know they got insanely lucky.

But the ones obsessed with getting even more? Those are the fucked up ones. They’ll do almost anything for the next dollar — even though it won’t change their lives at all.

Extreme wealth doesn’t always corrupt people… but the endless chase for more often does. That said, I think successful people like Elon give the rest of us a reason to try harder — that insane drive to do impossible things can naturally turn into massive success.

Ambition isn’t the problem. It’s when it becomes greedy and soulless.

What do you think — are most billionaires normal people who got lucky, or does the game naturally reward certain personality types?

16