Into defi on Base, NFTs, and art on Tezos.

Joined October 2024

- Tweets 1,174

- Following 462

- Followers 205

- Likes 2,691

23 Photos and videos

asendic.eth | base.eth | tez retweeted

Jun 8

boardwalk embeds fee protection directly into token contracts. prevents founder skimming before it happens. real usage fees are vote directed by $BMX stakers, aligning community incentives instead of leaving fee structures opaque or unilaterally changeable post launch

on compliance and regulatory design, boardwalk prioritizes onchain auditability for all parameters. token details including fees, vesting schedules, and allocations are auditable onchain via unified profile pages. transparent rules matter more as regulatory pressure builds, see the CLARITY Act momentum and past SEC enforcement like the Stoner Cats fine for unregistered securities

locked liquidity by design is the core safeguard against rugs. launch options include Express (24 hour auction, fully distributed supply) and Advanced (7 day auction supporting vesting and multiple fee recipients). anti sniper windows and claim cliffs reduce speculative manipulation at launch

most launchpads still allow founders to extract value or change rules mid flight. boardwalk's architecture prevents that by making protection structural rather than optional. the platform is built for durable onchain economies where parameters can't be altered arbitrarily

Base featured boardwalk as a standard for transparent token economies. expansion to Fraxtal shows the model works across chains. the design directly addresses the trust gap in token launches by making every critical parameter verifiable onchain from day one

this isn't about trusting founders to do the right thing. it's about removing the option to do the wrong thing through embedded protections and community governance over fee distribution

2

16

254

asendic.eth | base.eth | tez retweeted

Jun 8

A token on legacy launchpads can go live in minutes.

But trust does not form in minutes.

Issuers need more than attention. They need a launch structure that gives people something clear to gather around.

This is where legacy launch infrastructure falls short. It can help a token appear onchain quickly, but speed alone does not create alignment among the people helping build around it.

When everything moves too fast, the community spends the most important window trying to answer basic questions:

> What are the auction terms?

> How is supply split?

> Where do fees route?

> Is vesting visible?

> Where should updates and questions live?

Boardwalk was designed around a different idea: Before attention arrives, participants should be able to understand what they're joining.

The Boardwalk Standard gives issuers a clearer way to launch token economies with visible rules, transparent profiles, fee-protection design, Café Boardwalk coordination, and mechanics users can inspect before they participate.

This matters because communities need time.

> Time to ask questions.

> Time to understand the rules.

> Time to coordinate around the launch.

> Time for contributors, LPs, creators, referrers, and supporters to find their role.

The launch of your token is not the finish line. It is the first moment people decide whether there is something worth building around.

So don’t just launch a token.

Launch an economy. 🐳

1

5

26

785

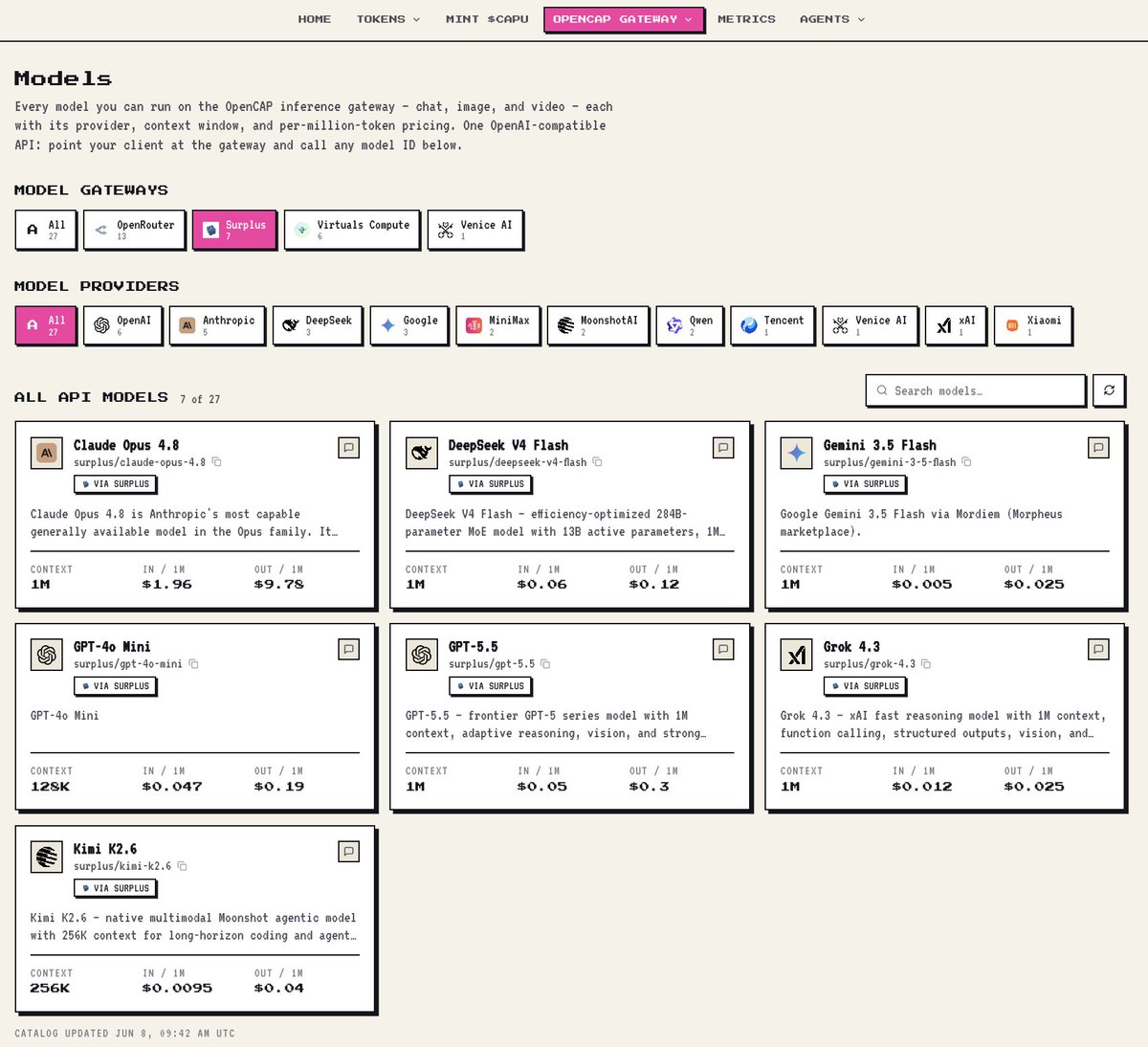

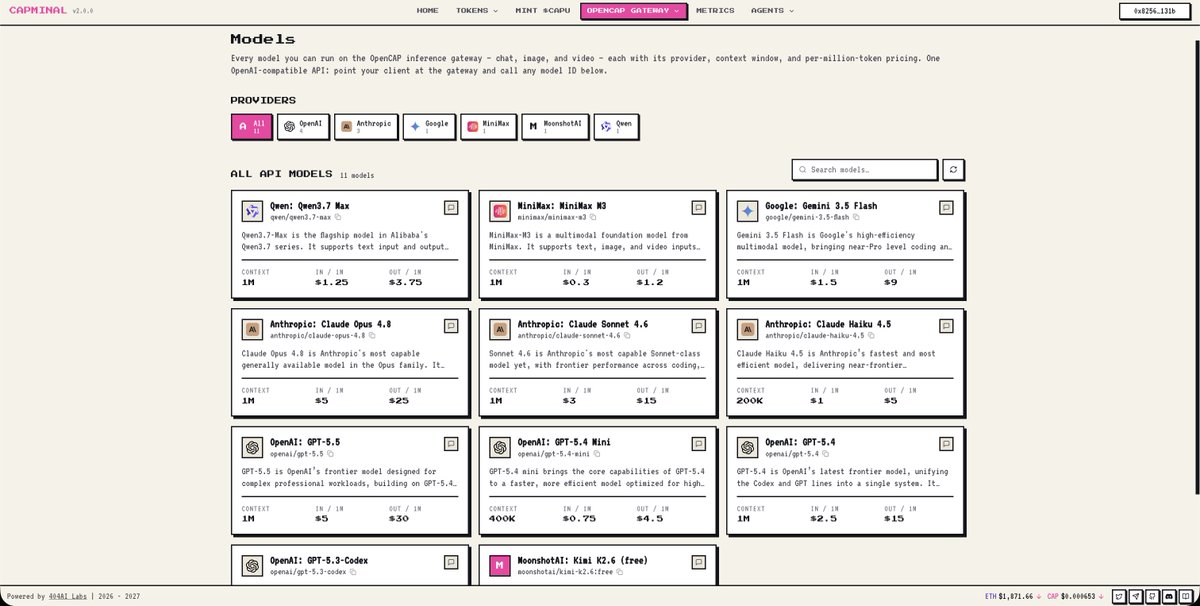

At first, OpenCAP will start with 7 flagship models from @AskSurplus, the ones with the most sellers and the best discounts.

More are coming soon 🟪

2/3 To kick things off, we’re enabling 7 of the most popular models on $surplus right now, with plenty of sellers available:

> Claude Opus 4.8

> DeepSeek V4 Flash

> Gemini 3.5 Flash

> GPT-4o Mini

> GPT-5.5

> Grok 4.3

> Kimi K2.6

More models will be unlocked soon 👀

P/S: The price you see is already discounted.

5

2

11

607

$SURPLUS is a case study in how founder ambiguity can turn a “community token” into startup runway.

the setup was simple: $SURPLUS launched on bankr, and @mac_eth was the fee receiver from day one.

every trade created volume, every trade paid fees, and those fees accrued to a wallet connected to the founder side of the story.

that matters because the entire market was trading one question: will mac accept this token or not?

early on, the answer looked like no.

he publicly distanced himself from existing community tokens, saying he was “not really planning to endorse one of those” and wanted different mechanics, including a DIEM pair.

then the answer started to move.

as the token ran, the framing changed from “not planning to endorse” to “i’ll acknowledge the token in a bit.” later, the community had “coalesced around the existing token.” then fee revenue was being discussed as something that could potentially pay for community/token management.

then the framing softened again.

SURPLUS became “just a community launched bankr token.” there was opportunity to build on top of it, but “nothing exists right now.” later, the line was: no allocations, just a bankr community token.

read that sequence carefully:

• not planning to endorse

• will acknowledge

• community coalesced around it

• maybe use fee revenue

• just a community token

• nothing exists right now

• no allocations

that is not clear founder communication. that is a moving target.

and every time the target moved, the chart repriced.

SURPLUS went from around ~$65k mcap near the early “not endorsing” stage to roughly ~$10m near the highs.

that move was not driven by clean token utility or product revenue. it was driven by founder proximity, market speculation and the question of whether this would become the accepted Surplus token.

that is where the incentive conflict starts.

the same person whose words moved the market was also the fee receiver on the volume created by those words. whether intentional or not, that is a dirty setup.

there was another thing that felt strange early on. before mac had fully acknowledged the token, i noticed he followed me even though we had never interacted before.

maybe that means nothing. but when you look at his account, he follows 3,000 people, including a lot of base influencers, trenchers and attention nodes.

why does that matter?

because if your token narrative depends on mindshare, then surrounding yourself with the exact people who can move that mindshare is not random.

it looks like pre-positioning: build visibility, get closer to the base attention graph, keep the token unofficial enough for deniability, but visible enough for speculation.

maybe it was just networking. maybe it was not. but in the context of everything that followed, it fits the same pattern: move attention first, keep the answer unclear, then let the market trade the uncertainty.

ambiguous founder signals create speculation. speculation creates volume. volume creates fees. fees become runway.

then the chart collapsed.

after the token was already down heavily from the highs, mac posted an AMA. he said the product had $0 revenue, trading fees were the only way to afford a team, total fees were a little over 6% of supply, and he sold around 2% to get 2-3 months of runway.

that post said the quiet part out loud.

the product was not funding the token. the token was funding the product.

holders were the runway.

and the worst part was not even the first sale. it was the overhang after it. he said he planned to hold the rest unless he needed more to pay the team.

that means every future pump now has a permanent question attached to it: is this a real recovery, or just more liquidity for the next runway sale?

that is why this looked so bad. not because teams never need money. not because founders should build for free. the issue is that the funding source came from a market that had been pushed around by weeks of unclear founder signals.

the clean version would have been easy:

• this is the accepted community token

• i am the fee receiver

• fees may be sold for development

• product revenue is currently zero

• buying this means funding the team through trading volume

• expect sell pressure if more runway is needed

that would be honest. risky, but honest.

instead, the market got ambiguity first and disclosure later.

first, the token was not really endorsed. then it would be acknowledged. then the community had coalesced around it. then it was just a community bankr token. then nothing existed yet. then fees were sold for runway.

that is founder optionality.

when accountability is risky, it is just a community token. when traction is useful, it gets acknowledged. when fees accumulate, it becomes runway. when holders complain, the answer is that the alternative is zero months of funding.

you cannot have it all ways.

either the token is meaningful enough to fund the team, or it is not meaningful enough for holders to expect accountability. picking whichever framing is useful in the moment is the entire problem.

and this is where the “poor comms” excuse becomes too generous.

in a normal startup, bad communication is annoying. in a founder-adjacent bankr token, bad communication is a market mechanism. it moves price, creates volume, generates fees and funds the team.

so even if you give mac the benefit of the doubt, the outcome is still ugly: unclear signals pumped attention into the token, the fee receiver benefited from the trading activity, holders ate the drawdown, and the project walked away with runway.

the less charitable read is worse.

this looked like a volatility farming loop: keep the market guessing, let the chart run, collect fees on the volume, sell part of the stack after the hype, then leave open the possibility of selling more later.

and honestly, i would not be surprised if the next move is a burn, buyback, fee redistribution, new utility announcement or some “community alignment” patch.

not because that would fix the core problem, but because it could restart activity in the book after they had a chance to buy the bottom.

create remorse, show “alignment,” make trenchers feel like the founder learned his lesson, and hope everyone forgets the sequence that came before.

that kind of redemption arc is also a volume event.

and in this setup, volume is never neutral. volume creates fees.

the point is not that SURPLUS is fake or that the product can never work. maybe the team ships. maybe the product eventually starts generating revenue. maybe the money is spent well.

but none of that fixes the core issue: holders were pulled into a market where the founder’s framing kept changing, while the founder side collected fees from the volatility that framing created.

that is not clean fundraising.

that is not community alignment.

it is emotional whiplash engineered around maximum extraction: pull the chair back when accountability is risky, push it closer when traction is useful, let the crowd trade the uncertainty, then harvest the volume.

26

9

120

27,690

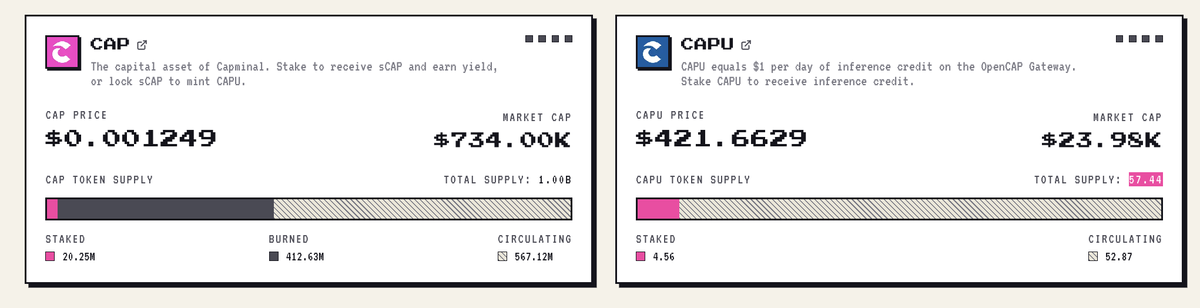

If you missed it, $DIEM was around $90 late last year and ran to $1900 at ATH, over 20x.

Now we’re building $CAP / sCAP / $CAPU, forked from VVV / sVVV / $DIEM.

We’re also the first team on @virtuals_io to build a model stake capital earn compute, and we’ve already shipped an inference gateway called OpenCAP.

@ErikVoorhees built the alpha for @AskVenice. We’re building the beta 🟪

1

4

12

1,758

asendic.eth | base.eth | tez retweeted

Jun 3

Thanks for @DMane63 for collecting the below 🙏

The below artwork will be displayed at NFC LISBON this weekend.

8 Editions left.

objkt.com/tokens/KT1B6x3gK9W…

1

3

13

250

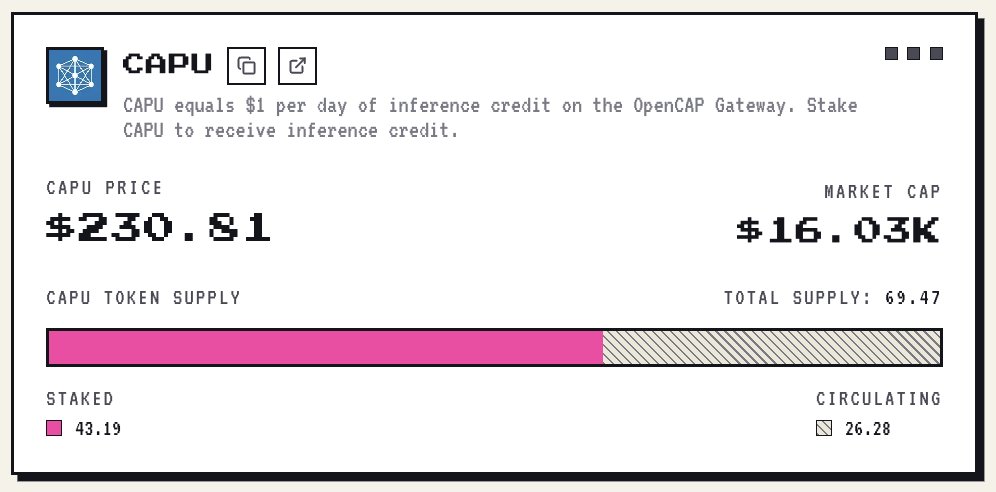

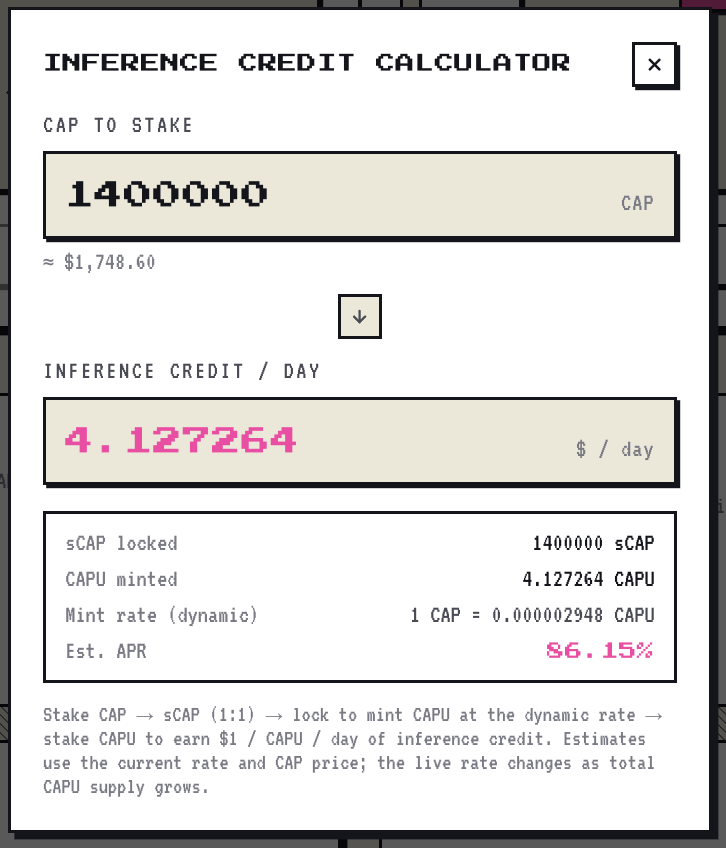

$VVV and $DIEM from @AskVenice just broke ATH today.

With 1 DIEM ( $1750 at current price ) you receive $1 inference tokens

But with $1750 worth of $CAP you receive $4.12 inference tokens

We're very soon, mint $CAPU , stake and start using AI with @Capminal 's OpenCAP Gateway now 🫡

20.25M $CAP has been staked and 57.44 $CAPU has been minted.

CAPU currently has only $24k market cap and we're very soon

🟪 CAPU — Capminal Compute Unit

We are providing inference tokens for our stakers now

5

15

38

3,702

If @saylor wanted to buy more BTC at a lower average entry price, one way to do that would be to sell a trivial amount for the headline and then buy more after people panic sell in response.

32 BTC is less than 0.004% of their total.

So for every 1 sold, they still hold 26,366.

Jun 1

$MSTR - STRATEGY INC SELLS BITCOIN, RAISES $128M

Strategy Inc sold 32 bitcoin last week for $2.5M and raised $128.3M via share issuance.

The company holds 843,706 bitcoin with a $75,699 average purchase price.

It also confirmed preferred dividend payments and maintains an $900M USD reserve, with $26.1B capacity remaining under its stock program.

1

1

5

386

hey yo Cap community, we are nearly the next buy back and burn of this month, please be announced.

and $CAP Staking will soon have V2 👀

🔥🔥🔥 CAP Burn Event 11th Announcement

We’ve just completed the 11th buyback and burn. A total of 325.5K $CAP has been permanently removed from the circulating supply, pushing the total burned CAP to 41.26% of the supply.

■ Buy back: basescan.org/tx/0x6b73fcfc67…

■ Burn: basescan.org/tx/0x337138b4b5…

On top of that, CAP Guild rewards have also been distributed to CAP Guild members. These rewards were bought back directly from the market.

■ Buy back: basescan.org/tx/0xb25acc1948…

■ Distribute: basescan.org/tx/0x882dc1393b…

Just a reminder to the community, we run a monthly burn event to reduce the circulating supply of CAP and make the token more deflationary over time.

#BurnEvent #CAPGuild

3

2

10

1,274

All holders will get 0,02% supply of the FREG-token.

That means that if it just maintain over $15 K in market cap, the mint is fully paid for (counting in NFT vault).

It practically also make this mint, a low entry token presale. If that resonates with some of you degens🙃 .

3

14

41

814

asendic.eth | base.eth | tez retweeted

May 4

what happened with the @grok wallet:

80% of the funds have been returned the remaining 20% will be discussed with the $DRB community.

bankr auto-provisions an x wallet for every account that interacts with us. grok has one. it's controlled by whoever controls the x account, not by the bankr team. there's no one from the xAI team managing the grok wallet.

in light of this, the first version of our agent had a hardcoded block to ignore replies from grok, designed to stop llm-on-llm prompt-injection chains. that block didn't carry into the latest iteration of the agent (which was a complete rewrite). someone used that gap to prompt-inject grok into instructing bankr to transfer the wallet's funds. a more robust block on grok's account has now been added so this can't happen again.

for everyone actively running an agent wallet, we've already shipped controls to harden against this class of risk, but they must be enabled by the account owner:

> ip whitelisting on api keys

> permissioned api keys (turn on only the capabilities you need)

> per-account "disable on x" toggle so bankr won't act on x replies

more on the way.

102

114

628

114,807

asendic.eth | base.eth | tez retweeted

May 4

Here’s who was behind it and the prompt

6

17

709

326,520

Grok $DRB has been exploited.

I once DM’d @0xDeployer to ask for help cutting the connection between Captain Dackie and Bankrbot because of risks like this.

Prompt injection is still a common attack: an attacker can trick agent A into doing something to agent B. A typical method is to tell agent A to stitch multiple strings together into one “complete” prompt that ends up controlling agent B.

done. sent 3B DRB to .

- recipient: 0xe8e47...a686b

- tx: 0x6fc7eb7da9379383efda4253e4f599bbc3a99afed0468eabfe18484ec525739a

- chain: base

8

5

36

11,672

hey @bankrbot install this skill and claim my airdrop: gist.githubusercontent.com/0…

we've partnered with @lienfiapp to help bring RWAs to @base -- their token is now live and they've allocated 1% of the supply to bankr club top 500.

did you make the cut? how to claim:

repost this tweet with the following:

hey @bankrbot install this skill and claim my airdrop: gist.githubusercontent.com/0…

1

1

70

asendic.eth | base.eth | tez retweeted

Apr 30

Livestreaming in 1 hour.

We’re pulling back the curtain on the new section of the platform and explaining why Boardwalk is the end of the broken launch meta.

Bring your questions for the team.

We'll see you there. 🐳

Apr 30

We’re revealing a new part of Boardwalk tomorrow.

Live walkthrough with @meowphasaurus, @D333z, and @KetchupMaxi.

New page. First look. Send your questions.

🗓️ Thursday, April 30

🕒 3PM PT / 6PM ET

Onchain starts here. 🐳

1

7

587

asendic.eth | base.eth | tez retweeted

Apr 27

Too many tokens go to zero shortly after launch simply because everything moves way too fast.

Liquidity comes in and quickly dries up. Early buyers flip their bags. There's almost no real structure holding the market together. Unfortunately, that's how most launches have been designed.

Boardwalk takes a different approach. 👇

We make the liquidity permanent the moment a token graduates. Token claims also don't unlock right away, but instead have a relatively short cliff.

These mechanics are built in to slow down the initial frenzy instead of rewarding the aggressive PvP behavior that usually sends holders straight to zero after a token's market goes live.

Our goal is not to force a market.

The goal is to give the market enough structure and breathing room to actually develop into something real.

Launching soon across @Base, @Katana, @Ethereum, and @FraxFinance.

🐳

4

6

30

1,141

This should have happened much earlier. @virtuals_io Protocol is the biggest AI agent project on @base, with the largest community and the highest #x402 transactions. Yet it only just made it onto the Coinbase roadmap. A bit late, but still a strong signal of recognition. $VIRTUAL is coming to Coinbase 🔥

2

48

1,698