17 Photos and videos

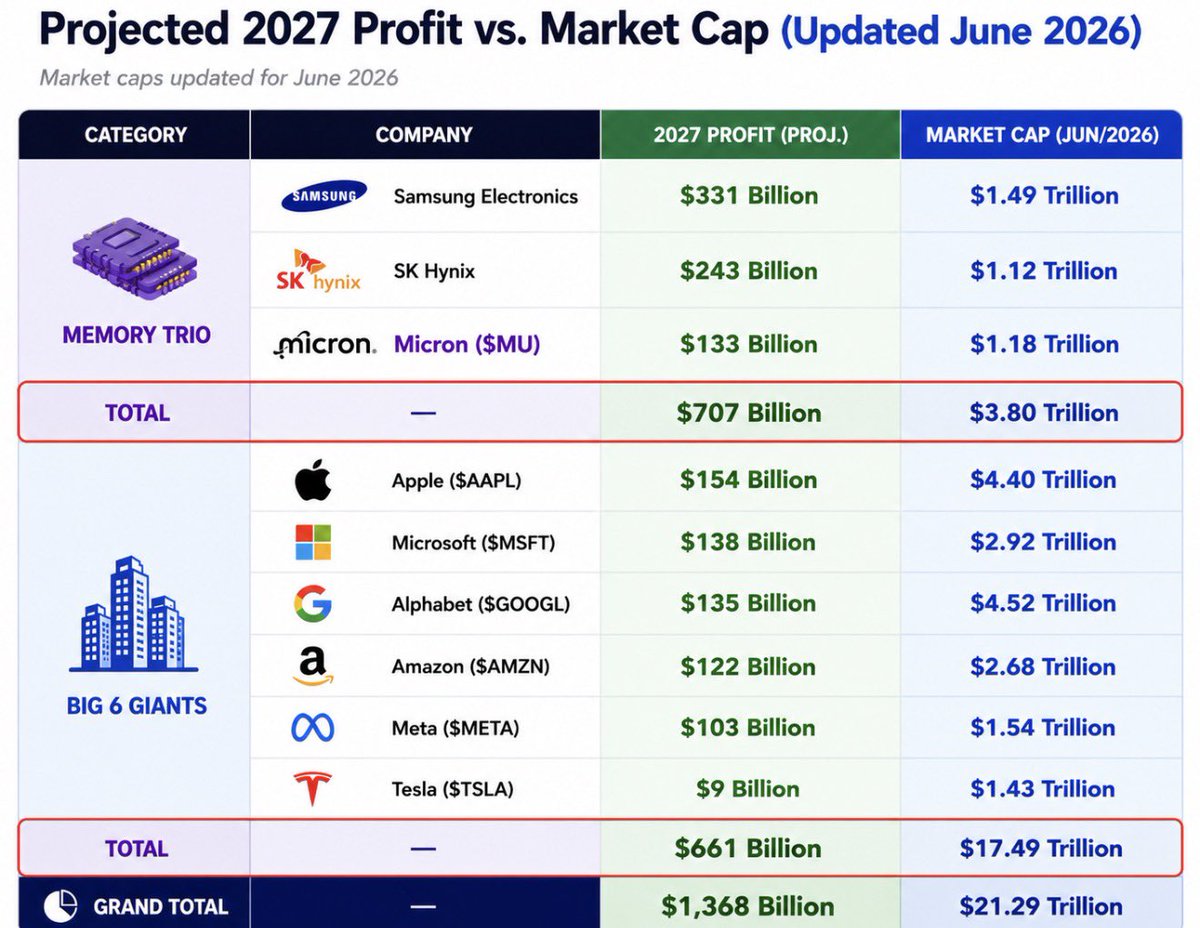

$MU: The Textbook Definition of Margin Expansion. Micron is the best example. Micron ($MU) is what it looks like in real life.

As AI demand accelerates, Micron isn’t just growing revenue—> it’s growing higher-margin revenue. HBM, high-performance DRAM, and AI infrastructure memory are becoming a larger percentage of the business, creating a powerful earnings $flywheel.

Revenue Growth Margin Expansion Operating Leverage = Explosive Earnings Growth. Every new AI server requires dramatically more memory than traditional computing infrastructure. As demand accelerates, Micron benefits from:

🔹 Higher DRAM pricing

🔹 Massive HBM demand growth

🔹 Increasing data center mix

🔹 Stronger product pricing power

🔹 Expanding gross margins

🔹 Operating leverage at scale

As revenue grows, manufacturing and operating costs are spread across a much larger revenue base. The result is that profits grow substantially faster than sales.

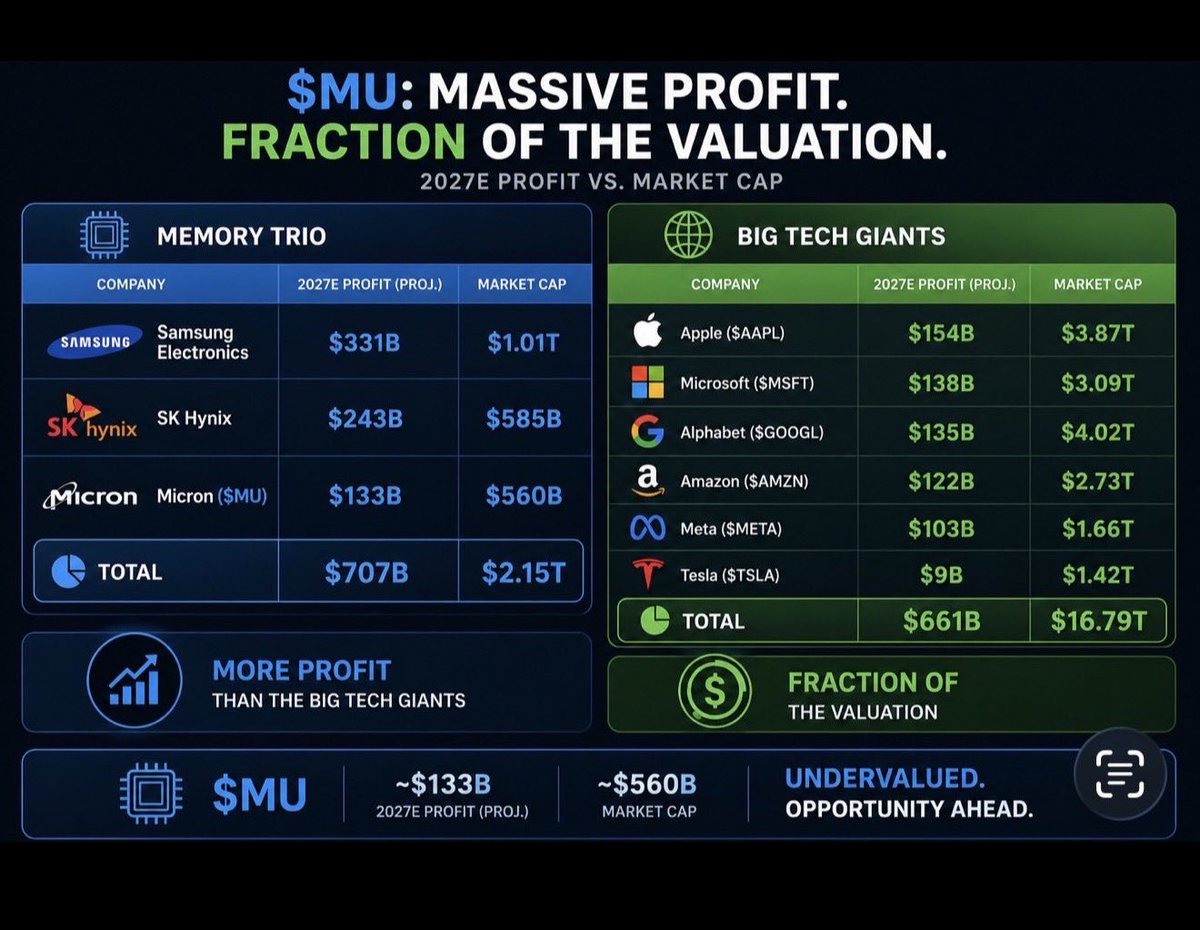

When revenue rises and margins expand simultaneously, profits can grow dramatically faster than sales. That’s exactly what this chart is showing. By 2027, Micron is projected to generate $133 billion in profit. Let that sink in.

According to these projections, Micron would generate:

✅ More profit than Meta ($103B)

✅ More profit than Amazon ($122B)

✅ Nearly the same profit as Alphabet ($135B)

✅ Within $5B of Microsoft ($138B)

I can see $MU Reaching levels as high as $3000 this yr, potentially 4,000 in 2027.

They have so much cash now, they can literally Fund any new semis lines without raising capex. ✅

53

$PURR will be buying a lot more hype, they are like a second AF.

This was likely them last night as it fits previous patterns, today another strong day for them.

A lot of supply absorption from them and the AF

Its not if, but when. Time just has to do its work, and price will get to the destination

1

123

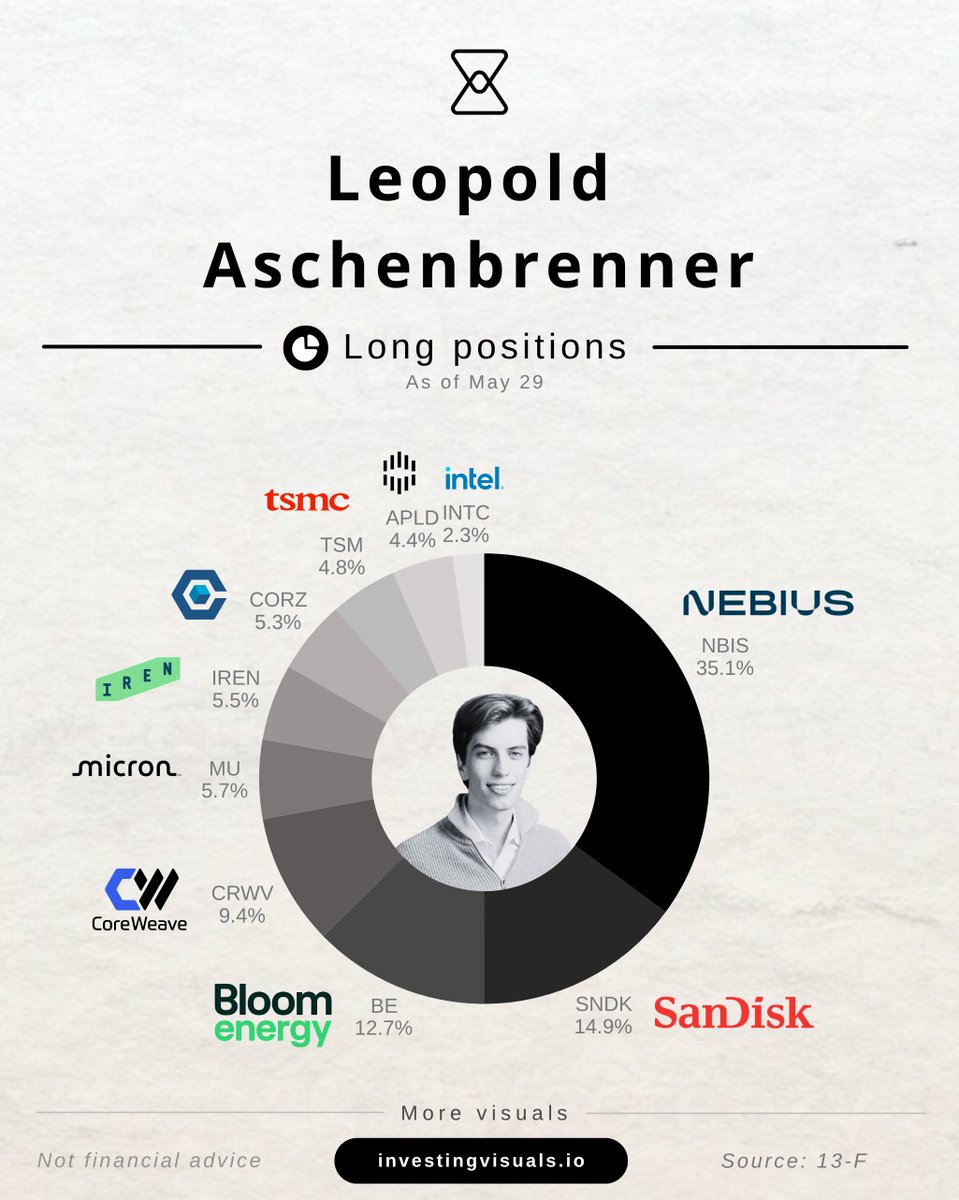

Mustafa retweeted

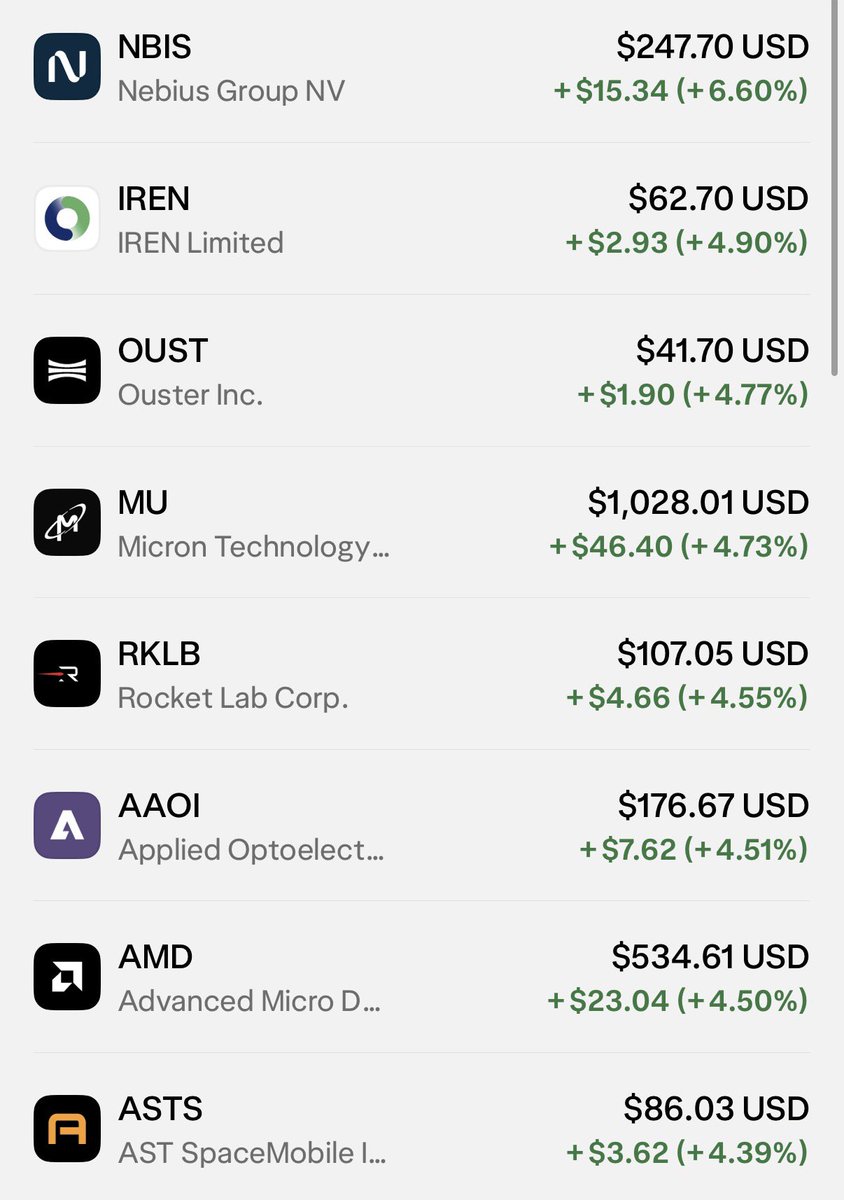

Pre market ripping on Iran deal & my high conviction stocks leading

$NBIS — Nebius: GPU neocloud renting AI compute to hyperscalers.

$IREN — Bitcoin miner pivoting to AI datacenter/GPU cloud hosting.

$OUST — Ouster: lidar sensors for autonomous vehicles, robotics, industrial.

$MU — Micron: memory chips (DRAM/HBM) riding the AI demand wave.

$RKLB — Rocket Lab: small-launch rockets plus growing space-systems business.

$AAOI — Applied Optoelectronics: optical transceivers for datacenter and broadband networks.

$AMD — CPUs and GPUs competing with Intel and Nvidia.

$ASTS — AST SpaceMobile: satellites beaming direct-to-phone cellular from space.

6

28

182

17,067

⚡️Micron $MU price target raised to $1,500 from $660 at TD Cowen

TD Cowen raised the firm's price target on Micron to $1,500 from $660 and keeps a Buy rating on the shares.

The firm said higher DRAM content per 1GW, even after SOCAMM de-specing, along with $150 CY27E EPS, keeps them constructive and drives their new price target.

The incremental change is that CPU demand has increased buyers' expectations that pricing strength can persist into 2H:C27 versus. prior view of digestion in 1H:C27.

7

45

285

152,821

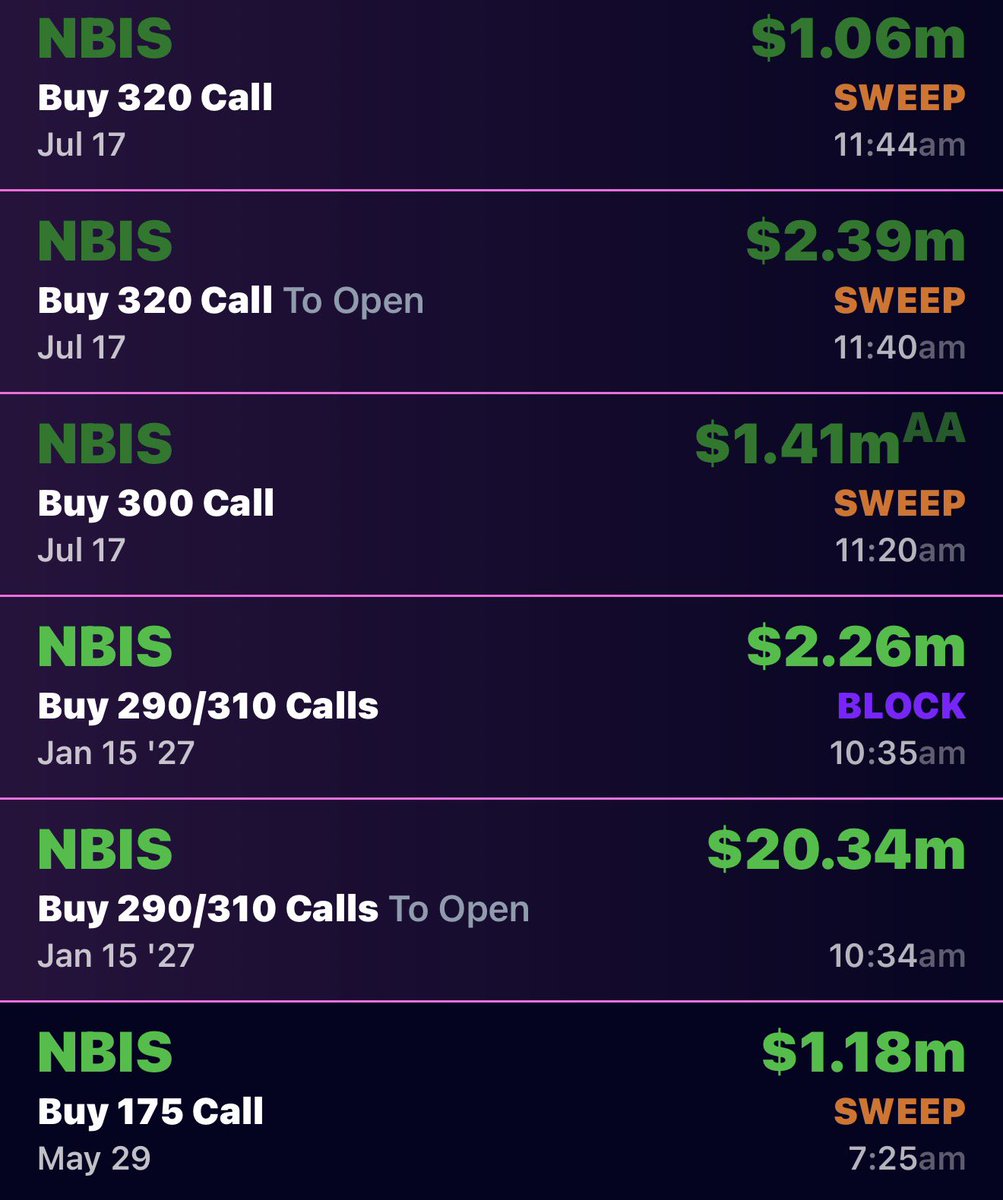

$NBIS $300 incoming 🧲

Jun 15

$NBIS reclaiming $250 premarket with Nasdaq‑100 add, Microsoft/Meta multi‑year orders, and 21% short interest sets up a squeeze window back toward the $265–$278 supply band. Balance sheet shows >$3.6B cash and extended server lives easing 2026 D&A, which supports margin optics.

I’m pressing above $250 with trims into $265–$275 and a fail line on a daily close back below $240; reload on $233–$236 if tagged. Turn uncertainty into decisions with Incite.

1

142

AI REVOLUTION

Jun 14

TOP 20 FASTEST GROWING AI INFRASTRUCTURE COMPANIES:

1. $NBIS | Nebius Group -- 521%

2. $MU | Micron -- 191%

3. $CRDO | Credo Technology -- 170%

4. $CRWV | CoreWeave -- 136%

5. SK Hynix -- 136%

6. $LITE | Lumentum -- 56%

7. $AAOI | Applied Optoelectronics -- 111%

8. $SNDK | Sandisk -- 110%

9. $IREN | IREN -- 95%

10. $SMCI | Super Micro Computer -- 82%

11. $AEHR | AEHR Test Systems -- 75%

12. $ALAB | Astera Labs -- 50%

13. $AVGO | Broadcom -- 50%

14. Samsung -- 50%

15. $NVDA | NVIDIA -- 48%

16. $MRVL | Marvell -- 35%

17. $CLS | Celestica -- 28%

18. $AMD | Advanced Micro Devices -- 30%

19. $ANET | Arista Networks -- 20%

20. $VRT | Vertiv -- 20%

YoY projected revenue growth.

Which of these are you holding?

16

Mustafa retweeted

Jun 15

$NBIS the Best Buy on the market right now and it’s not particularly close

2

1

64

3,126

$PURR your the best , I’m so happy I found you

May 28

The company holding 22.3 million HYPE issued 9% more shares last week. Normally that dilutes everyone who already owns it. This time the value behind each share went up, not down. Here is the mechanic most treasury company takes miss.

📰 $PURR updated dashboard, at hyperliquid:native $59.78:

✓ 22.3M HYPE, up from 20.8M. Cash $157.2M, up from $113.8M. Zero debt.

✓ Fully diluted shares 179.8M, up from 164.7M, a 9% increase through the ATM.

✓ NAV per share $8.29, up from $7.95 last week. Share price $8.69, a 1.05x premium to NAV.

❗️ The mechanic:

Issuing new shares usually means existing holders own a smaller slice. The exception is when you sell those shares above net asset value and put the proceeds into the asset itself. That is what happened.

PURR (@HypeStrat ) sold new shares at a premium, bought 1.5M HYPE, and its cash position still rose $43.4M on top of the buy. Share count up 9%, and net asset value per share rose rather than fell. A diluting raise would have done the opposite.

That gap is the accretion, and it is the entire point of a treasury company. The ones that work compound. The ones that do not just dilute.

🏆 The read:

The premium narrowed from 1.10x last week to 1.05x even as the treasury grew, some of that HYPE sitting below its high this week, some the market digesting a 9% larger share count.

But it held above parity, which means the market still pays up for the proxy rather than discounting it. The flywheel did its job, grow the treasury without shrinking the value behind each share.

The line to watch is parity. Above 1.00x the proxy holds. A sustained move below it is the market saying the issuance stopped adding value.

1

1

125

$MU $707 to $895 2weeks 26%

Ps, I’ve been in micron way way way before I mentioned it on X

May 8

$MU People say I'm too bullish - but I'm actually the most conservative guy holding a stock at <6 PE that's growing earnings 100% with 81% margins, in an expanding TAM >20% with revenue visibility 3 years out.

Doesn't that sound like something to be super bullish on?

1

148