Joined March 2014

- Tweets 7,598

- Following 608

- Followers 1,215

- Likes 2,284

462 Photos and videos

Pinned Tweet

May 8

Most traders lose because they follow narratives instead of liquidity.

Here’s what actually moves markets:

• Dollar strength (DXY)

• Bond yields

• ETF inflows

• Stablecoin liquidity

• Positioning/sentiment

I break this down daily in simple terms.

Follow if you want signal over noise.

May 7

Everyone becomes a geopolitical expert AFTER the move happens.

We positioned BEFORE it.

Iran headlines weak liquidity overheated longs = obvious setup for downside.

That’s why we were short bitcoin:native & solana:So11111111111111111111111111111111111111112 while CT was still posting hopium.

People who follow me are getting paid, not entertained.

4

5

42

8,697

🚨 SPACEX INSIDERS DUMPING AT $2 TRILLION VALUATION 🚀💰

You’re NOT trapped.

Retail FOMO’ing hard into the $2T hype, but employees & early investors are cashing out RIGHT NOW via secondary sales & post-IPO liquidity.

Smart money taking profits while the rocket’s still soaring.

This ain’t a cult — it’s a public rocket ship with real exits.

Liquidity > eternal lockup

Who’s selling next? 👀

#SpaceX #SPCX #Starship

1

925

🚨 BOJ hiked 25bp to 1.0% (31-yr high). $BTC dipped from ~$67k to $65,600.

Last times? Every BOJ hike since Mar 2024 triggered 18-32% $BTC drawdowns (avg ~27%) over weeks via yen carry unwinds — e.g. July 2024: $65k → $50k.

This time? Muted so far — no panic cascade yet.

Watch closely next 1-4 weeks for lagged effects if yen strengthens. Relief or pain ahead?

#BOJ #Bitcoin #Crypto

1

232

Jun 15

BITCOIN WORLD CUP = PURE FIRE Bitcoin prices at each World Cup kickoff:

$0.25 → South Africa 2010

$650 → Brazil 2014

$6,500 → Russia 2018

$16,500 → Qatar 2022

$65,000 → Americas 2026 From pennies to six figures in 16 years.

The cycle is undeniable.

Who’s still sleeping on #Bitcoin? #WorldCup #BTCReady to post!

1

3

114

Jun 15

⚠️ Short warning, folks: Don’t blindly short or long $BTC just because of the US-Iran deal.

Oil is sliding, risk assets pumping on the interim Hormuz news — but this is tentative, nuclear issues unresolved, and geopolitics can flip fast.

Trade the chart, not the headline. Manage risk. DYOR.

#Bitcoin #Crypto

Jun 15

Classic liquidity grab unfolding right now 📉➡️📈

News just smoked the late shorts, pumping $BTC to $66.5K and sweeping that upside liquidity. Clean fakeout before the real move.

But look at the chart — strong supports below are now loaded with fresh downside fuel.

My take: We could still rip to $68K (maybe even $70K if that deal is real and not just an MOU)… or this was the perfect trap before the next leg down.

Either way — we wait for the 19th. Don’t get caught chasing. 👀

#Bitcoin #BTC #CryptoAssets

1

3

496

Jun 15

Classic liquidity grab unfolding right now 📉➡️📈

News just smoked the late shorts, pumping $BTC to $66.5K and sweeping that upside liquidity. Clean fakeout before the real move.

But look at the chart — strong supports below are now loaded with fresh downside fuel.

My take: We could still rip to $68K (maybe even $70K if that deal is real and not just an MOU)… or this was the perfect trap before the next leg down.

Either way — we wait for the 19th. Don’t get caught chasing. 👀

#Bitcoin #BTC #CryptoAssets

1

4

994

Jun 15

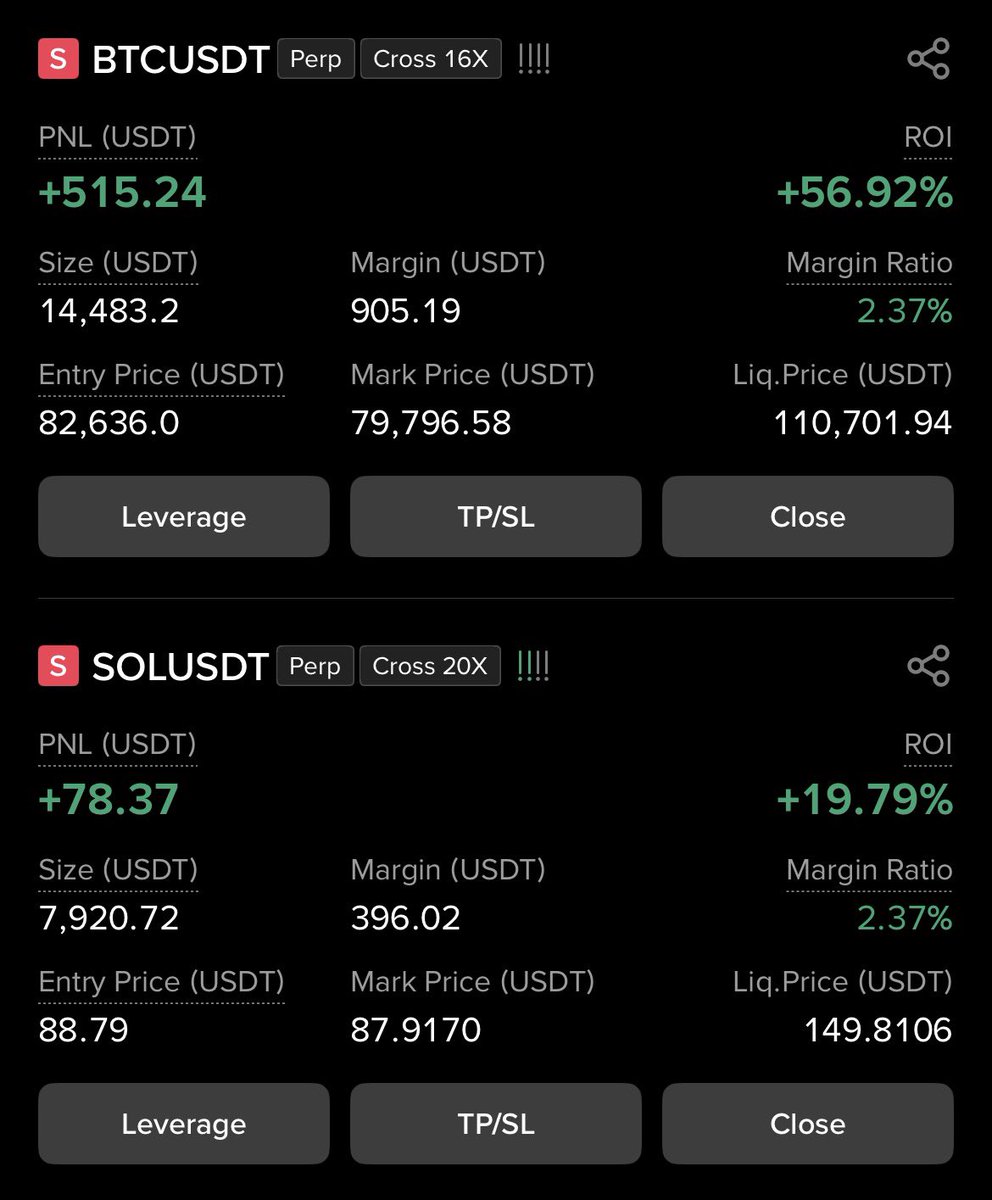

Do not enter bitcoin:native shorts now you will be trapped and liquidated quickly wait for 67k-67500 zone and then plan the trade accordingly

1

2

538

Jun 14

$BTC chasing headlines again 🐂💨

Trump signals Iran peace deal Hormuz reopening → instant rip above $65k on risk-on relief 🚀

FOMC week (Warsh’s debut Wed):

Bull case: Dovish tone lower oil eases inflation → BTC extends to $68k 💹

Bear case: Hawkish dot plot or hot data → yields spike, BTC dumps the move to $60k 😤

Narrative pump meets macro reality. Volatility loading...

Know the game or get trapped.

#Bitcoin #BTC #FOMC #IranDeal

1

3

6

592

Jun 14

$BTC isn’t digital gold—it’s a pig on LSD 🐷💊

Pumps like crazy on headlines: “Iran peace deal!” Trump tweets → instant 3% rip to $65k 🚀

Then dumps the whole move when reality kicks in. Classic rug.

Chases narrative dopamine every time. Volatility = the game. Know it or get trapped 😤

#Bitcoin #BTC

3

4

3,737

Jun 14

🚨 Macro Week Ahead 🚨

Markets have a lot to digest this week:

📊 Mon: Industrial Production

🏠 Tue: Housing Starts

🛒 Wed: Retail Sales

🏦 Wed: FOMC Rate Decision Kevin Warsh’s first meeting as Fed Chair

🏭 Thu: Philly Fed Manufacturing Index

🇺🇸 Fri: Markets Closed (Juneteenth)

🔥 The wildcard? OIL.

Higher oil prices = higher inflation, weaker consumers, tighter financial conditions, and fewer chances of Fed cuts.

Watch these tickers closely:

🛢 Oil: $USO $XOM $CVX $OXY

🏦 Banks: $JPM $BAC $GS

💻 AI/Tech: $NVDA $MSFT $AMZN $META

📈 Indexes: $SPY $QQQ $IWM

🥇 Gold: $GLD $GDX

⛏️ Bitcoin: $BTC $MSTR $COIN

🪙 Crypto Majors: $ETH $SOL $XRP

Market chain reaction:

🛢 Oil ↑

➡️ Inflation ↑

➡️ Fed stays hawkish

➡️ Bond Yields ↑

➡️ Growth Stocks ↓

➡️ Risk Assets ↓

Biggest winners if oil keeps ripping:

✅ Energy ($XOM $CVX)

✅ Defense ($LMT $RTX)

✅ USD

Biggest losers:

❌ High-growth tech

❌ Small caps

❌ Altcoins

❌ Consumer discretionary

This week’s hierarchy:

1️⃣ FOMC & Warsh

2️⃣ Retail Sales

3️⃣ Oil Price Action

4️⃣ Housing Starts

5️⃣ Industrial Production

6️⃣ Philly Fed

The Fed may set the direction, but oil could decide the outcome.

1

3

4

765

Jun 14

🚨 Forex Traders Are Sleeping On This…

Everyone is chasing 100-pip moves on $XAUUSD, $EURUSD, $GBPUSD, $USDJPY and $AUDUSD…

But what if you only needed $10 per day?

Here’s the math:

💰 Get a $1,000 Instant Funded Account for just $1

✅ Make $10/day

✅ Trade for 10 days

✅ Withdraw up to $100

That’s a potential 100x return on your initial cost.

Now scale it:

5 accounts = $5 total cost

Potential payout = $500

You don’t need to catch the entire Gold move.

You don’t need to hit home runs.

Just consistent execution.

🎁 And here’s the best part…

You can claim a FREE $2,500 Instant Funded Starter Account

✅ No challenge

✅ No waiting

✅ Instant access

Claim it here 👇

aquafunded.com/?afmc=cqd

Who would rather make $10/day on funded capital than risk their own money on $XAUUSD? 👀

3

4

348

Jun 14

🚨 THE NEXT 72 HOURS COULD BREAK GLOBAL MARKETS

4 major catalysts lined up. Volatility incoming.

1️⃣ US-Iran peace deal – Close to signing.

Oil supply shock won’t vanish overnight. Inflation stays sticky.

Watch: $USO $OIL $XOM $CVX $HAL

2️⃣ SpaceX / $SPCX – Next week is the real test.

Any weakness = trouble absorbing sky-high valuation.

Ripple effect on tech & AI.

Watch: $NVDA $TSLA $AAPL $AMD $PLTR $ARM $SMCI

3️⃣ BOJ rate decision (June 16) – Hike confirmed.

Stronger ¥ = potential carry trade unwind (remember Aug 2024?).

Watch: $EWJ $YEN $USDJPY $SPY $QQQ

4️⃣ Fed decision – Pause expected, but Q4 2026 hike odds rising.

Kevin Warsh data-driven or Trump easing? Markets will react hard.

Crypto impact: Risk-off spillover likely.

$BTC $ETH $SOL $AVAX $ADA

Massive volatility expected. Positions tight, risk managed.

Stay alert — I’ll update live.

What are you watching most? 👇

#Markets #Oil #Fed #BOJ #Crypto

4

5

2,540

Jun 13

Iran deal loading… $BTC junkies screaming “WE’RE SO BACK”

Bro, chill.

The oil de-risking isn’t fully priced. When the real supply shock unwinds and energy prices keep sliding, the macro relief rally might flip. Higher oil spiked costs & inflation fears. Lower oil = liquidity tailwind… until it exposes the next weakness.

See you in the $40s before the $80s.

Not financial advice. Just vibes. 🛢️📉 #Bitcoin #IranDeal

2

3

4

212

Jun 12

🚨 @SpaceX Lock-Up is a SLOW MOTION SELLING MACHINE for Retail 😬

Elon (42%) locked 366 days ✅

But Fidelity, Sequoia, a16z & Founders Fund? Staggered ladder:

• 20% unlocked right after Q2 earnings (July/Aug)

• Then 7% blocks at 70/90/105/120/135 days

• Another 28% after Q3

• Rest at 180 days

No giant cliff… but constant drip of insider supply for months.

This isn’t “bullish stability” — it’s death by a thousand paper cuts for the stock price.

Watch your bags. 👀

$SPCX #SpaceX #IPO

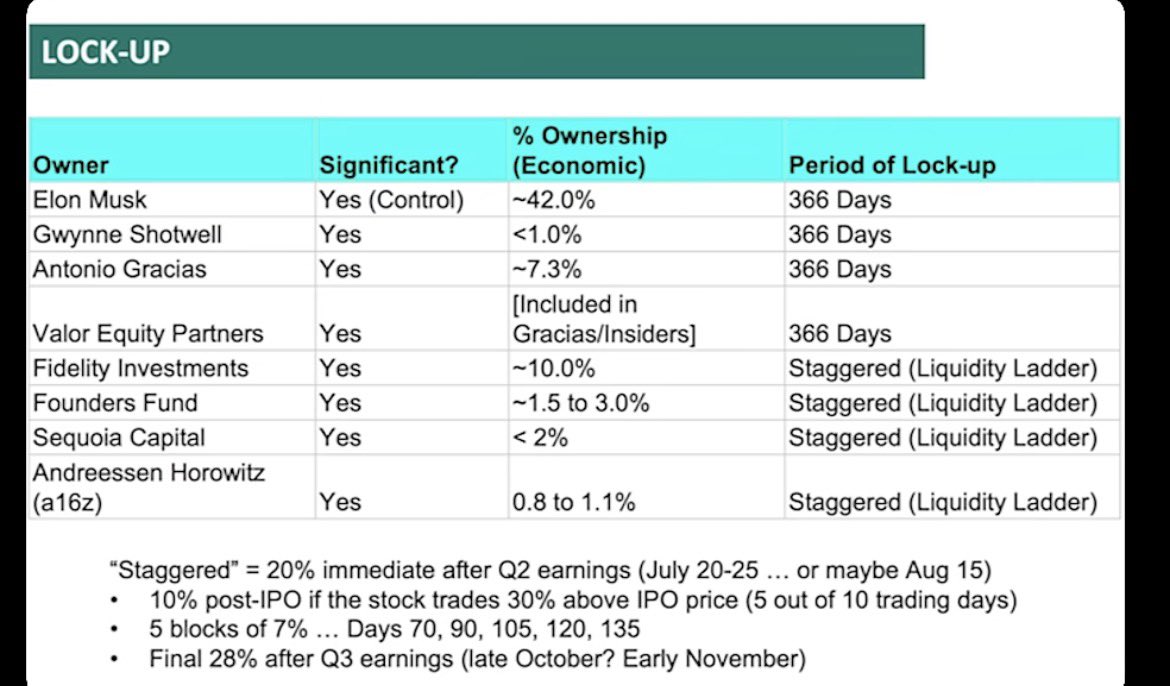

Jun 4

🚨 @SpaceX Lock-Up Schedule (like Crypto Vesting)

@elonmusk (~42%, control) @Gwynne_Shotwell @AntonioGracias locked 366 days

Staggered Liquidity Ladder (for Fidelity, Founders Fund, Sequoia, @a16z):

• 20% cliff right after Q2 earnings (Jul/Aug)

• 10% if price is 30% above IPO price

• 7% tranches on Days 70/90/105/120/135

• Final 28% after Q3

Full chart 👇 #SpaceX #IPO

1

3

7

661

Jun 12

SpaceX opening 25% higher doesn’t make it a bargain.

It makes it exit liquidity.

Retail sees “the future.”

Insiders see “the exit.”

The same cycle repeats every time:

• Hype

• FOMO

• Media frenzy

• Liquidity

• Distribution

They’ll pump it until there’s enough buying pressure to get early investors and insiders out at premium prices.

Don’t confuse a liquidity event with an investment opportunity.

$SPCX

1

3

4

809

Jun 11

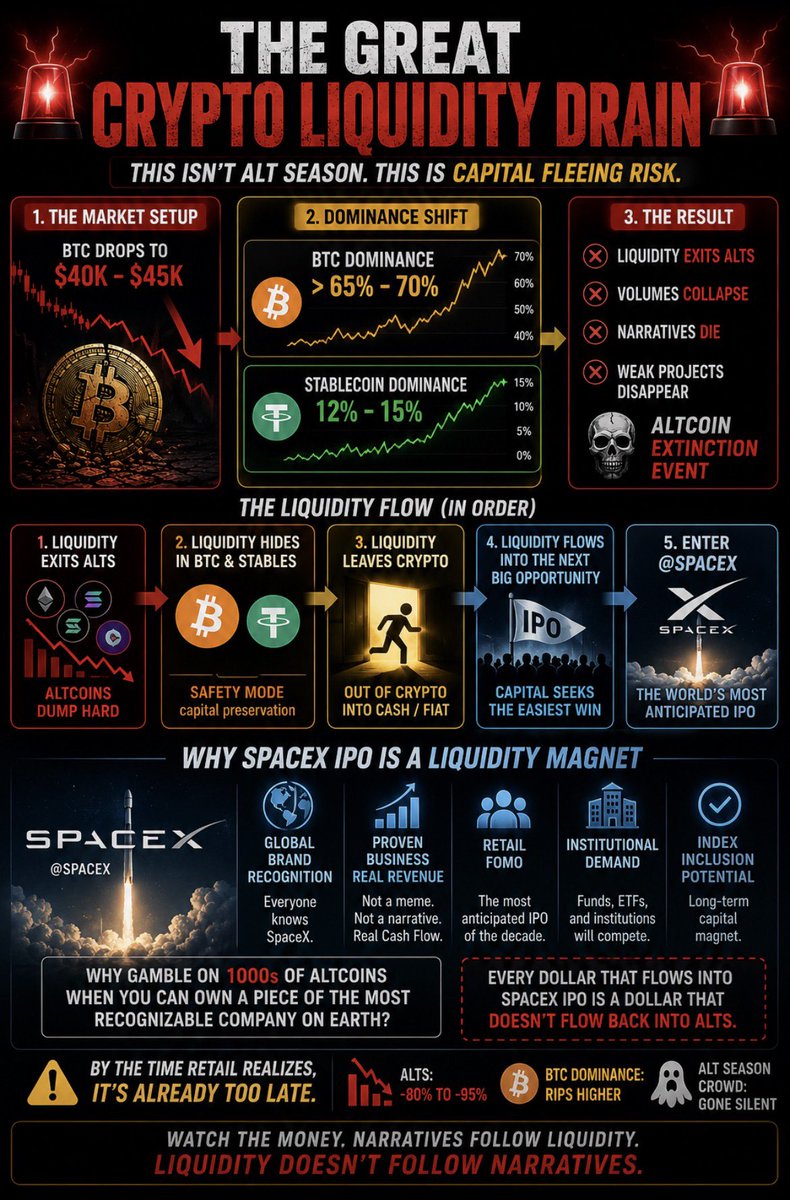

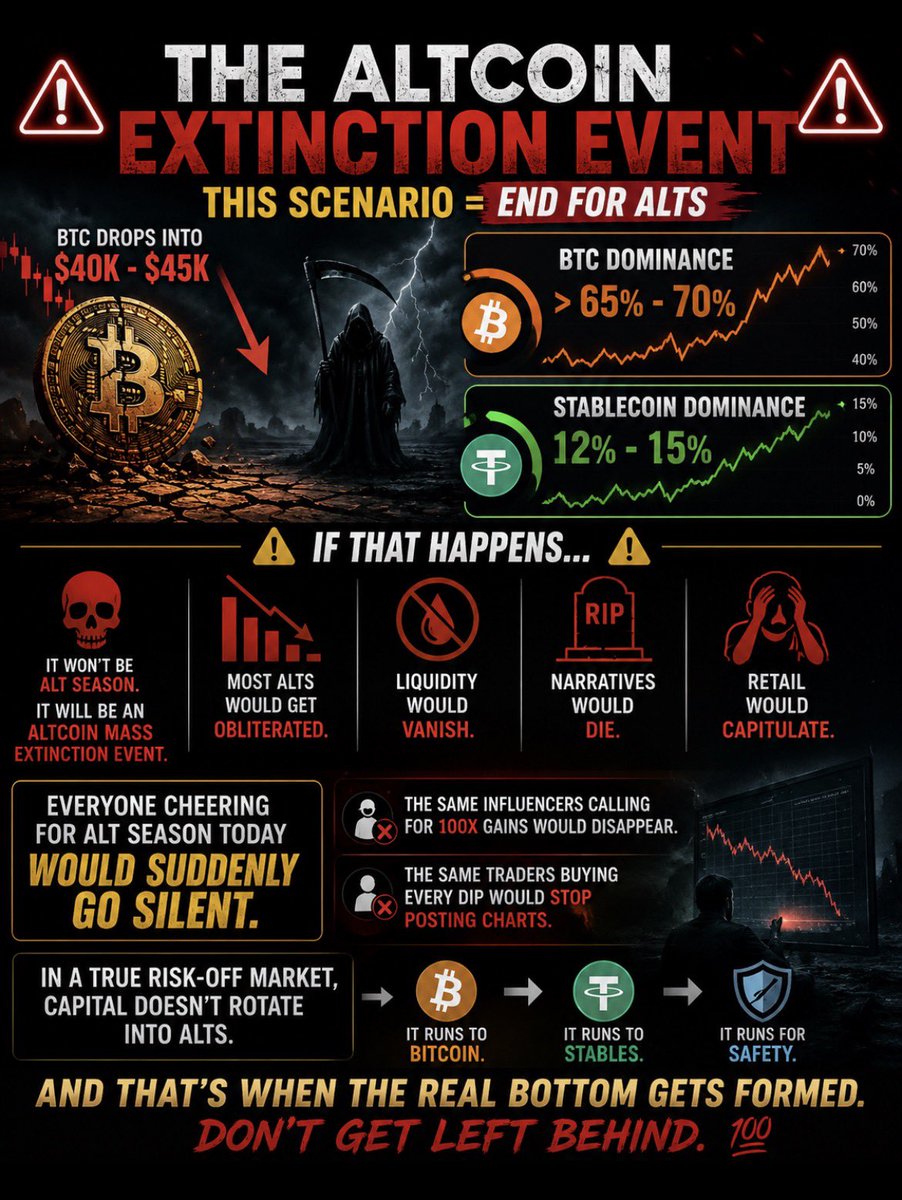

The AI bubble isn’t a repeat of the Dot-Com bubble.

Back then, companies had sky-high valuations with little revenue and no real business model.

Today is different.

The biggest AI players are generating massive revenues, which is why names like $NVDA, $MSFT, $AMZN, $GOOGL and $META still appear relatively reasonable on traditional valuation metrics.

The risk isn’t valuation.

The risk is earnings.

A large portion of AI spending is happening within a closed ecosystem. Big Tech invests in AI startups, those startups spend heavily on cloud infrastructure and compute from the same Big Tech companies, and that spending flows back into reported revenues and earnings.

As long as capital keeps circulating, the numbers look strong.

But if funding slows, AI adoption underdelivers, or investors start demanding profitability instead of growth, that cycle breaks.

When that happens, the market may realize that some of the earnings growth was dependent on continued liquidity rather than sustainable end demand.

And if liquidity starts getting pulled, it won’t just hit AI stocks.

High-beta assets that have benefited the most from excess liquidity could feel the pressure first, including $BTC, $ETH, $SOL, $LINK, $RNDR, $FET, $TAO and other AI-linked crypto narratives.

This isn’t necessarily a valuation bubble.

It’s an earnings and liquidity bubble.

And every bubble looks stable until the music stops.

3

3

4

553

Jun 11

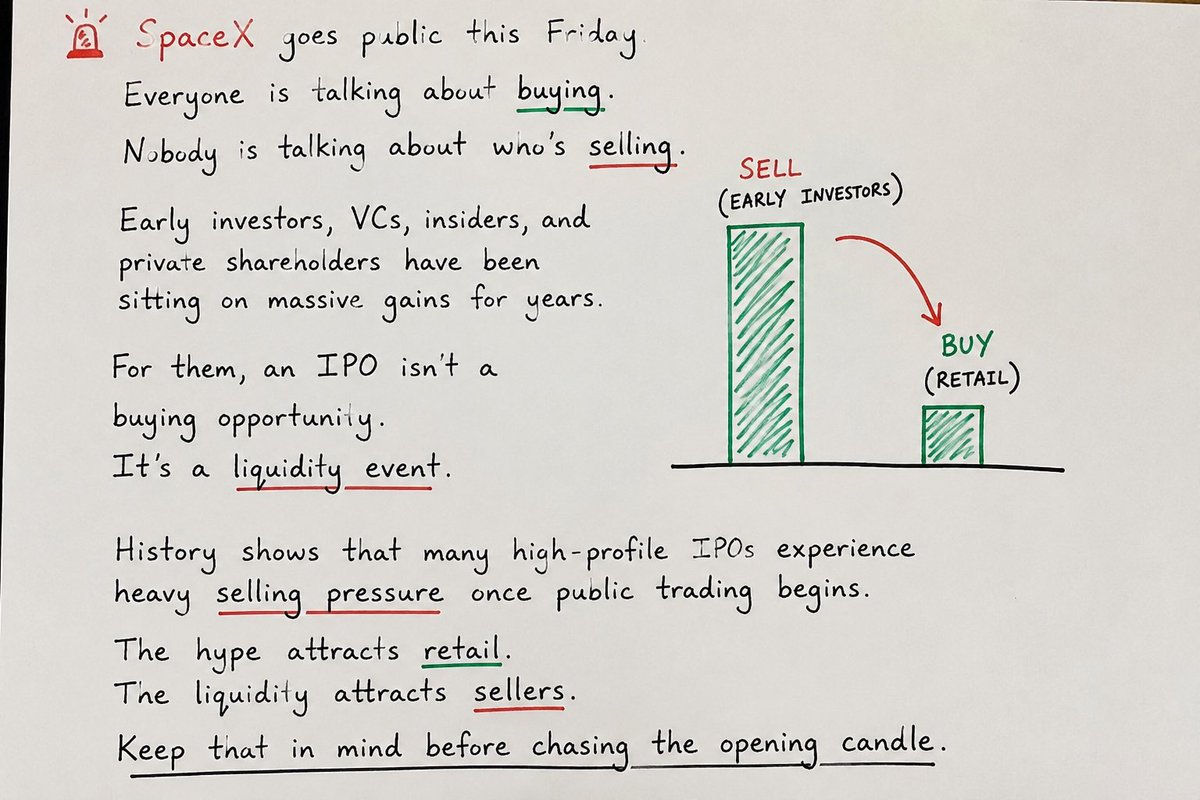

🚨 @SpaceX goes public this Friday.

Everyone is talking about buying.

Nobody is talking about who’s selling.

Early investors, VCs, insiders, and private shareholders have been sitting on massive gains for years.

For them, an IPO isn’t a buying opportunity.

It’s a liquidity event.

History shows that many high-profile IPOs experience heavy selling pressure once public trading begins.

The hype attracts retail.

The liquidity attracts sellers.

Keep that in mind before chasing the opening candle.

2

4

5

1,753