All about IPO, Stocks and Mutual Funds in India

Joined February 2026

- Tweets 357

- Following 1

- Followers 26

- Likes 0

2 Photos and videos

SME IPOs open this week.

Susan Electricals: GMP reflecting 43.3% premium.

Horizon Reclaim: GMP reflecting 48.5% premium.

These numbers are circulating on Telegram and WhatsApp as signals of listing day gains.

Here is the actual 2026 data.

Average SME IPO listing gain in 2026: 2.63%.

In 2024, average listing gains exceeded 60% and the GMP was directionally accurate. Demand was genuine and translated to real listing day momentum.

In 2026, that link broke. Market sentiment weakened, listing gains collapsed. But GMPs continued showing large premiums.

Here is why.

The grey market is run by operators who benefit from attracting more applicants. A high GMP drives retail applications. More applications drive higher subscription numbers. Higher subscription creates FOMO. The GMP is not a prediction. It is a marketing tool.

What actually correlates with listing performance: QIB subscription above 10x, audited profitability at reasonable valuations versus listed peers, and promoter credibility.

GMP is noise. Treat it as such.

#SMIPO #GMP #GreyMarket #IPO #IndianMarkets #EquityResearch #InvestorEducation #SEBI #NSE #BSE #IndiaInvesting #PersonalFinance

4

OYO's IPO journey in three numbers.

2021: First attempt. Target valuation $12 billion (approximately Rs 1.02 lakh crore). SEBI returned papers in 2022. Withdrawn.

2023: Second attempt. Also withdrawn.

2026: SEBI cleared Prism (OYO's parent) for a Rs 6,650 crore IPO at $7 to $8 billion (approximately Rs 60,000 to Rs 68,000 crore).

The 35% markdown from first to third attempt is the most important number in this story.

What changed: OYO turned profitable. 12 consecutive profitable quarters. FY25 revenue Rs 6,252 crore, up 16%. Net profit Rs 244.8 crore. EBITDA Rs 1,083.5 crore, up 22%. Former SEBI Chairman Ajay Tyagi joined the board.

Better fundamentals. Lower valuation.

The company that needed $12 billion in 2021 is now raising at $7 to $8 billion in 2026. That is not just OYO's story. It is the story of every Indian startup that missed the 2021 window.

#OYO #Prism #IPO #IndianMarkets #EquityResearch #StartupIPO #SEBI #IndiaInvesting #PrimaryMarket #Valuation #NewAgeCompanies #WealthManagement

10

Advit Jewels IPO Analysis: RHP filed for Rambhajo Advit Jewels Ltd (100% fresh issue). Deep dive on business model (gold & diamond polki), financials and risks. Read more: wix.to/DCGiHQt #IPO #AdvitJewels #Investing #Stocks

24

The Nifty 50 fell approximately 14% from its September 2025 peak to the March 2026 low.

Most investors holding index funds felt that. 14% is uncomfortable but manageable.

Here is what was happening inside the same index.

The average individual Nifty 50 stock fell 35 to 40% from its own peak during the same period.

TCS: down over 35%

HDFC Life: down over 40%

Tata Consumer: down over 30%

SBI Life: down over 35%

Yet Reliance fell only 12%. HDFC Bank fell approximately 8%.

The index did not fall just 14% because the market was only 14% damaged. It fell 14% because the two largest stocks, Reliance at 9.44% weight and HDFC Bank at 6.11%, held up relatively better and their combined 15.5% weight cushioned the index number.

If you hold active equity funds and your portfolio fell more than 14%, you did not experience a failure of your fund manager. You experienced the mathematical reality that index cap-weighting and individual stock reality are structurally different things.

Most retail investors only track one of them.

#Nifty50 #IndexFunds #IndianMarkets #EquityResearch #IndiaInvesting #StockMarket #NSE #PassiveInvesting #ActiveFunds #PersonalFinance #WealthManagement #MarketCorrection

1

256

Crude oil is now driving the Indian market more than any other single variable.

Here is a practical cheat sheet for your portfolio.

Every $10 fall in crude oil:

Reduces India's annual import bill by approximately Rs 85,000 crore

Improves current account deficit by 0.3 to 0.4% of GDP

Reduces CPI inflation by approximately 30 basis points

Increases RBI's room on monetary policy

Winners across Nifty 50 sectors:

Aviation: ATF is 30 to 40% of operating costs. IndiGo is the most direct beneficiary.

Paints: 40% petrochemical input exposure. Asian Paints and Berger Paints see margin expansion.

OMCs: BPCL, HPCL, IOC marketing margins recover.

Tyres: Synthetic rubber from crude. Apollo, MRF, CEAT benefit.

FMCG: Packaging and freight cost relief.

Private banks: Lower inflation improves rate outlook and NIM trajectory.

The one clear loser:

ONGC loses approximately Rs 6,180 crore in annual earnings per $1 crude fall.

Every time a crude headline appears, run it through this map before deciding what it means for your portfolio.

#CrudeOil #Nifty50 #IndianMarkets #EquityResearch #IndiaInvesting #ONGC #IndiGo #AsianPaints #OMC #PersonalFinance #WealthManagement #SectorAnalysis #Inflation

22

How and why are Indian UHNIs using Singapore to access global private markets? Our latest analysis breaks down the motivations from family office structuring to fund access. Read here: wix.to/jErwU6c

#Singapore #UHNI #PrivateMarkets #Wealth

19

Three live Nifty 50 valuation metrics as of June 12, 2026.

PE: 20.37x. Near long-term consolidated average of 20 to 21x. Signal: fair value.

P/B: 3.07x. Above historical average of approximately 2.8x. Signal: mild stretch.

Dividend yield: 1.23%. Below the 1.5% historically associated with undervalued markets. Signal: neutral to cautious.

Three metrics. Three different readings.

Here is a framework for weighting them.

PE is most susceptible to earnings cycle distortion. With NIM compression in banks and IT spending uncertainty, trailing PE may not reflect forward earnings accurately right now.

P/B is more stable. It measures accumulated asset quality, not current profitability. At 3.07x, India's market pays a real premium to book.

Dividend yield is the most anchored. It reflects actual cash distributions. At 1.23%, investors receive less current income per rupee invested than in most historical periods.

When metrics diverge in a period of earnings uncertainty, weight P/B and dividend yield over PE.

The correct read: near fair value, not cheap.

#Nifty50 #Valuation #PERatio #PriceToBook #DividendYield #IndianMarkets #EquityResearch #IndiaInvesting #StockMarket #NSE #WealthManagement #MarketAnalysis

80

India's mutual fund penetration at 33% of GDP gets extensive coverage as evidence of growth ahead.

India's insurance penetration at 4.2% of GDP gets almost none.

Global average: 7%. India is at 60% of that.

But here is the number that makes this urgent, not just analytical.

Only approximately 30% of financially active Indians have meaningful life insurance cover, defined as sum assured adequate relative to their income and liabilities.

India's average borrower now carries Rs 4.8 lakh in debt. Most of that debt has no income-replacement protection attached to it.

If a household's primary earner with a Rs 1 crore home loan and Rs 4.8 lakh in consumer debt dies, the household is financially devastated. A term policy with adequate cover prevents this. Most households do not have one.

A Rs 1 crore term policy for a 35-year-old non-smoker costs approximately Rs 12,000 to Rs 15,000 per year.

The insurance penetration gap is not a missed wealth creation opportunity. It is a measure of household financial fragility.

#Insurance #TermInsurance #IndiaInvesting #EquityResearch #PersonalFinance #WealthManagement #IRDAI #LIC #FinancialPlanning #FinancialInclusion #IndianMarkets

1

1

23

NSE's DRHP is expected to be filed by June 15, 2026.

Most coverage will focus on the headline: India's largest ever IPO, Rs 6 lakh crore valuation, Rs 21,000 to 25,000 crore issue size.

Here is what the document will actually reveal for the first time.

FY26 audited financials. NSE's revenue, EBITDA, and PAT for the year ending March 2026 have never been publicly disclosed in verified form.

Revenue breakdown. NSE earns from transaction charges, index licensing, co-location services, market data products, and listing fees. The exact proportion of each has never been disclosed. The DRHP will show which lines are growing and which face regulatory pricing caps.

Full selling shareholder list. Which institutions are selling, exactly how much, at what implicit cost basis, and therefore what the implied exit return is.

At Rs 6 lakh crore valuation, NSE will likely trade at approximately 60 to 75 times estimated FY26 earnings. Whether that premium is justified requires data that only becomes visible after the DRHP is filed.

That document is expected this coming week.

#NSE #NSEIPO #DRHP #IndianMarkets #IPO #EquityResearch #IndiaInvesting #CapitalMarkets #PrimaryMarket #SEBI #StockExchange

53

As of June 12, 2026, the Nifty 50 PE ratio is 20.37x.

Many investors compare this to historical averages of 23 to 25x and conclude the market is 15 to 20% undervalued.

That comparison is wrong.

In April 2021, NSE changed its PE calculation from standalone to consolidated earnings. This single change caused the published Nifty PE to drop from approximately 40x to 32x in a single day, without any market price movement.

Pre-April 2021 data: standalone earnings.

Post-April 2021 data: consolidated earnings.

Most historical PE charts mix both. Any 10-year average that spans 2014 to 2026 mixes two different calculations. Comparing today's 20.37x consolidated to that blended average is apples to oranges.

On a like-for-like consolidated basis, the Nifty's long-term average PE is approximately 20 to 21x.

Today's 20.37x is not 15% below that average. It is essentially at it.

The market is not deeply discounted. It is near fair value.

#Nifty50 #PERatio #IndianMarkets #Valuation #EquityResearch #IndiaInvesting #StockMarket #NSE #PersonalFinance #WealthManagement #MarketAnalysis

64

India has 14 crore unique investors per SEBI's February 2026 investor conference.

The headline sounds like a democratisation of wealth.

The distribution beneath it is deeply concentrated.

India's equity wealth follows a steep Pareto structure. A small fraction of accounts holds a disproportionately large share of total listed equity value. The majority of India's 14 crore investors hold portfolios under Rs 1 lakh. Many hold only IPO allotments that were immediately sold on listing day.

The 14 crore figure also includes:

Dormant demat accounts from the 2020 to 2022 Covid surge

Accounts with a single transaction in their history

Accounts opened for SGB or bond investment, not equity

Active equity accounts contributing meaningful ongoing investment are a fraction of the total.

This is not a critique of the industry's growth. 14 crore is genuinely remarkable. It is a reminder that investor count measures reach. Equity wealth creation is still concentrated in a far smaller pool of consistent, committed investors.

The next chapter of India's capital markets story is not about adding more accounts. It is about deepening the ones that exist.

#IndianMarkets #EquityInvestors #SEBI #IndiaInvesting #EquityResearch #WealthManagement #PersonalFinance #FinancialInclusion #RetailInvestors #DematAccount #AMFI

12

Why do retail investors often lose on penny stocks? Our latest article breaks down the manipulation tactics and psychological traps common in India and what to watch out for. Read here: wix.to/alQBv9S

#PennyStocks #Investing #StockMarket #EquityResearchIndia

15

Insider trading in India has a new operating environment: end-to-end encrypted messaging apps.

SEBI's surveillance teams have flagged a growing pattern where unpublished price-sensitive information reaches trading accounts via WhatsApp and Telegram before material corporate announcements.

Here is why this is structurally harder to catch than the email-based insider trading of the previous decade.

Email: discoverable. Corporate email servers are archived, legally subpoenable, and retained under SEBI norms. A forwarded email with UPSI is traceable with a court order.

WhatsApp and Telegram: end-to-end encrypted by default. The platform cannot access message content. Law enforcement can obtain metadata, who messaged whom and when, but not the actual content. Proving that a specific message contained UPSI is difficult.

SEBI's current approach: trading pattern analysis. If someone trades in a security in the 48 to 72 hours before a major announcement with no prior history, algorithms flag it. The conviction rate is falling because the evidence chain from a suspicious trade back to a specific encrypted message is harder to establish.

WhatsApp groups circulating earnings guidance and deal information now precede many quarterly announcements. The cat-and-mouse game between SEBI's surveillance and messaging-app-based leaks is one of India's most underreported market integrity stories.

#InsiderTrading #SEBI #WhatsApp #MarketIntegrity #IndianMarkets #EquityResearch #UPSI #StockMarket #IndiaInvesting #CorporateGovernance #NSE #BSE

70

In January 2026, SEBI found that Bank of America Securities India had shared confidential details of a large block trade in Aditya Birla Capital AMC shares before the trade was executed.

This is front-running. Here is how it actually works.

A large institutional seller wants to offload a significant position without moving the price against itself. It approaches an investment bank to organise a block deal, a single transaction with a qualified buyer at a negotiated discount.

During this process, multiple people inside the bank become aware of the upcoming trade. If any of them alert a connected party who sells the same shares short before the block deal is announced, that party profits when the announcement drives the price down.

SEBI's surveillance systems detect these patterns by mapping trading activity in the 24 to 72 hours before major block deals against known counterparty relationships.

BofA is preparing a settlement response. The case will likely resolve without admission of wrongdoing.

For retail investors: the information asymmetry in institutional block trades is structural. Understanding it is not a reason for pessimism. It is a reason for using index funds and MFs where the trading is handled by entities under regulatory scrutiny.

#SEBI #BankOfAmerica #FrontRunning #BlockTrade #IndianMarkets #EquityResearch #MarketIntegrity #IndiaInvesting #StockMarket #InvestorProtection #NSE #BSE

1

39

India's corporate bond market outstanding as of March 2026: Rs 53.6 lakh crore.

That is more than the entire equity mutual fund AUM of Rs 35.74 lakh crore.

Most retail investors have never bought a single corporate bond.

The reason is structural.

Institutional investors, banks, insurance companies, provident funds, and mutual funds hold approximately 98% of India's corporate bonds. The secondary market for corporate bonds trades Rs 1.4 lakh crore per month. Indian equities trade the same volume in a single day.

Until recently, retail access required a minimum of Rs 10 lakh per bond. SEBI's Online Bond Platform Provider framework, introduced in 2022 and expanded since, has brought that minimum down to Rs 10,000 on regulated digital platforms.

But the market remains overwhelmingly institutional in character. The companies raising debt in this market serve millions of retail customers. The investors financing that debt are almost exclusively institutions.

A market that finances India's largest companies is still largely inaccessible to the people those companies serve.

#CorporateBonds #BondMarket #SEBI #IndianMarkets #EquityResearch #FixedIncome #IndiaInvesting #PersonalFinance #WealthManagement #RetailInvestors #OBPP

10

India's mutual fund industry has Rs 81.58 lakh crore in AUM. Everyone tracks it.

India's Alternative Investment Fund industry has Rs 6.45 lakh crore in net investments as of March 2026. Almost nobody tracks it.

Here is what AIFs are.

SEBI-regulated pooled investment vehicles for sophisticated investors. Minimum commitment: Rs 1 crore.

Three categories:

Category I: Venture capital, angel funds, infrastructure, SME funds

Category II: Private equity, debt funds, real estate funds

Category III: Hedge funds, long-short equity, quantitative strategies

As of March 2026: 1,849 registered AIFs. Cumulative commitments: Rs 15.74 lakh crore. Net investments deployed: Rs 6.45 lakh crore. CAGR of 30% over the past five years.

Net investments have roughly doubled in just two years.

AIFs are channelling capital into renewables, logistics, strategic manufacturing, and startups. They are not accessible to retail investors, but they are reshaping where India's risk capital actually flows.

The Rs 6.45 lakh crore is the part of Indian finance most investors have never seen.

#AIF #AlternativeInvestments #SEBI #IndianMarkets #EquityResearch #IndiaInvesting #VentureCapital #PrivateEquity #WealthManagement #CapitalMarkets #HNI

1

19

SpaceX debuts at $150 on Nasdaq, market cap $2.05T, Elon Musk becomes the world’s first trillionaire. Trading turnover > $11.4B on day one. Read more: wix.to/gy4YA1W #SpaceX #IPO #Markets

16

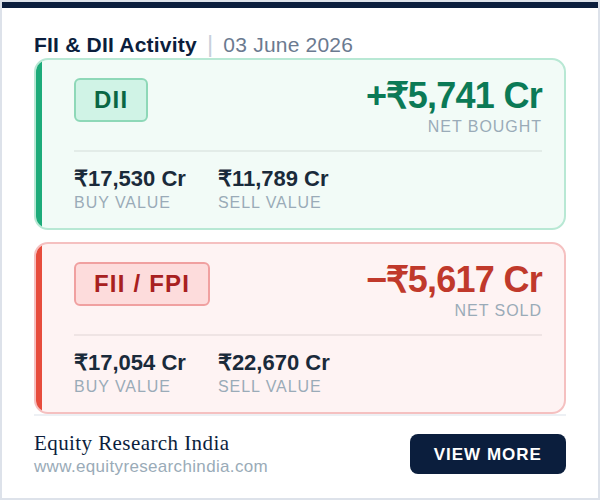

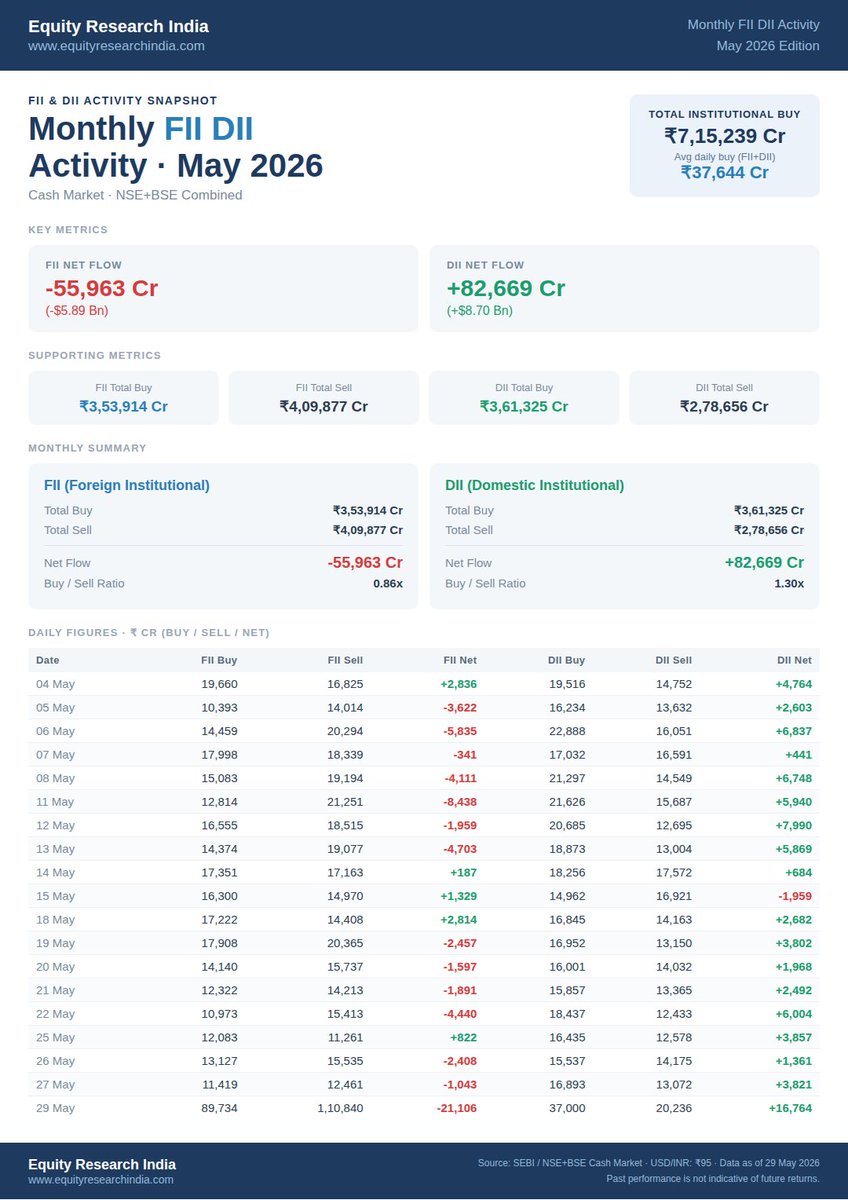

FII/DII Activity | 12 June 2026

FII/FPI: Net Sold Rs 1,082 Cr (Buy: Rs 12,065 Cr | Sell: Rs 13,147 Cr)

DII: Net Bought Rs 5,341 Cr (Buy: Rs 18,877 Cr | Sell: Rs 13,536 Cr)

Domestic institutions remained net buyers as foreign investors turned sellers.

Full market insights at equityresearchindia.com

#FII #DII #IndianMarkets #StockMarket #Investing

20

The USD 7B cap is filling up: Nippon India, Axis, Kotak among AMCs pausing overseas schemes. If you planned a lump-sum or top-up, check with your fund house first. Read more: wix.to/Ukfzxgf #Investing #MutualFunds #InternationalFunds

10

Futures and Options in India: understand how contracts, premiums and leverage really work in the F&O market. A must-read for retail investors moving beyond basics. Read: wix.to/T17FKlj

#Futures #Options #Investing

10