Know what you own why. Fundamental analysis. Against the herd. Members get my concise 12-page stock-research reports. ⬇️

Joined June 2022

- Tweets 18,656

- Following 290

- Followers 3,112

- Likes 16,251

1,824 Photos and videos

Pinned Tweet

7 Reasons You Should Subscribe to my Newsletter

When I launched Financial-Engineering.net, the investing world was already drowning in noise. Today it’s deafening.

Here’s why my newsletter reports earn a permanent spot in serious investors’ inboxes:

📈📈📈

1

2

1,303

Alan Gałecki – Financial-Engineering.net retweeted

Jun 13

For our American fans

1,229

4,597

101,839

2,916,858

Alan Gałecki – Financial-Engineering.net retweeted

Jun 12

I remember before the USA World Cup in 1994 there was talk that they wanted to split the game into quarters for Ad breaks. It was laughed off by the footballing world. Well they’ve done it in 2026 covertly with the introduction of the water break in each half. Tricked us all.

137

674

7,785

164,943

Hope no one confused the tickers 📉

Virgin Galactic $SPCE has now lost about one third of its value today 📉📉 Ouch! 🤮

243

That still values it at about 40x future sales with unclear profitability… 👇

(After today’s surge to above 2 trillion USD)

159

Not popular, but:

The football (yes, football) World Cup should be limited to 16 nations max and be a tournament of 2–3 weeks.

Like in the distant past.

Not a huge commercial with some kicking attached to it.

2

162

Alan Gałecki – Financial-Engineering.net retweeted

Jun 12

Yes

18

17

200

12,776

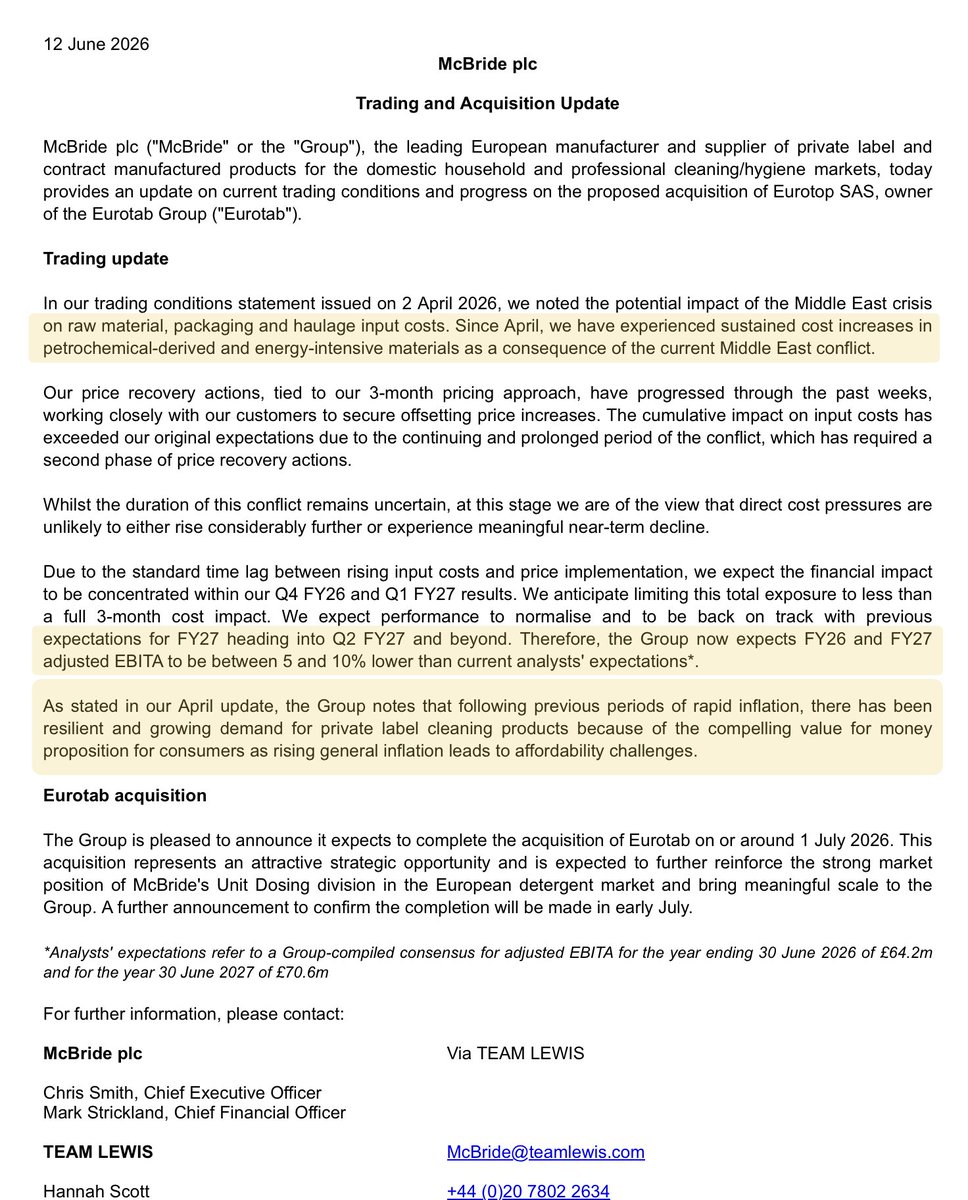

$MCB.L McBride plc with an important update

2 things:

- costs pressuring more than expected —> guidance hit

- demand for private labels remains strong

MCB for was an active idea for my blog‘s members. I closed the case, though, as it looks just in time after a solid run.

1

184

Alan Gałecki – Financial-Engineering.net retweeted

Korrekt!

Und Gewinner bleiben nicht oft die ganz großen Gewinner, wie diese Graphik von @ThierryBorgeat wunderbar zeigt.

1

4

184

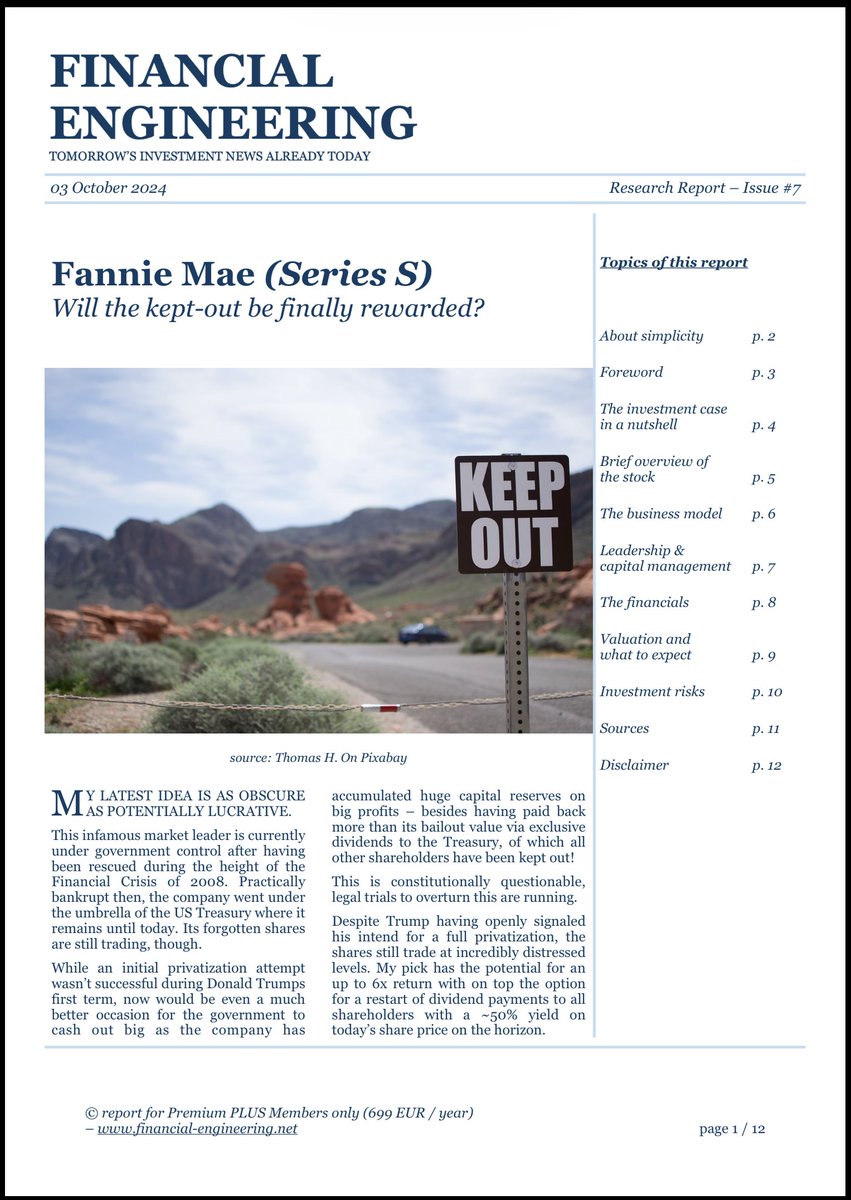

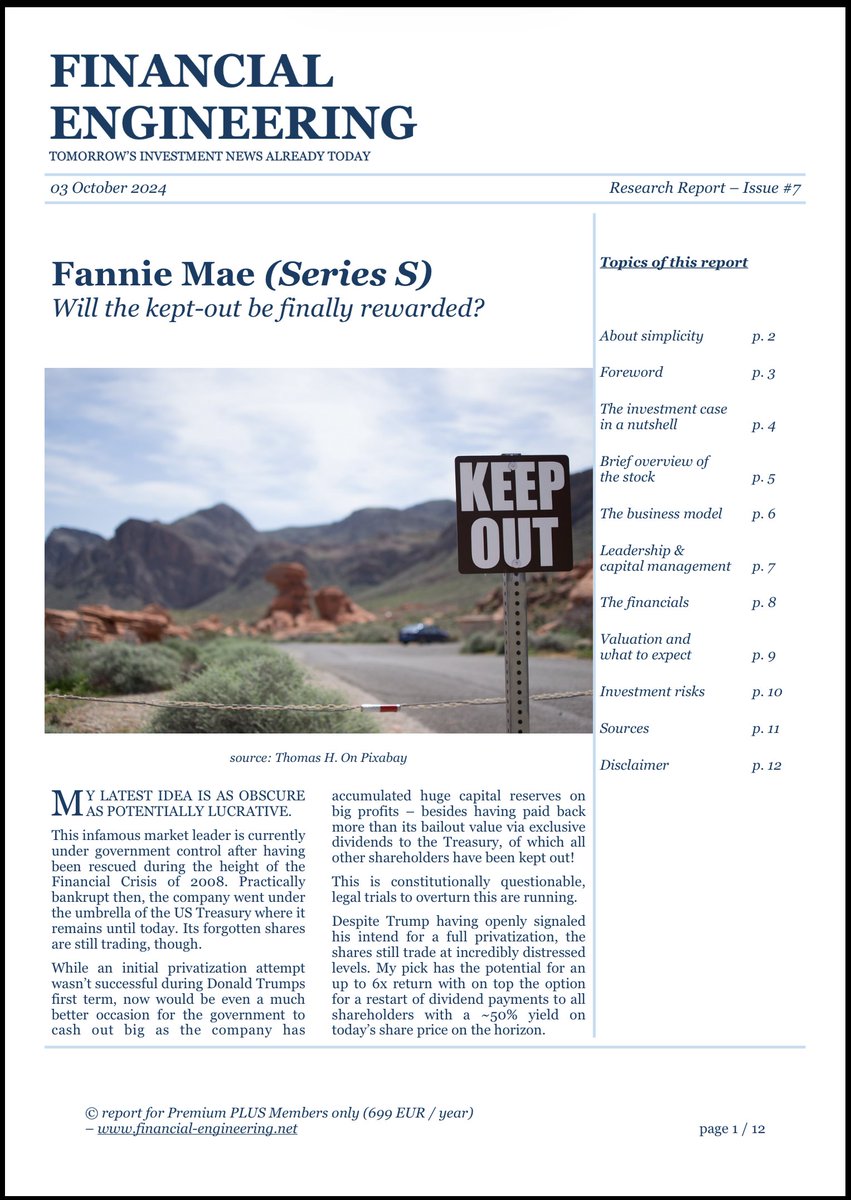

not too long ago, my timeline was flooded with exclusively bullish calls for the coming IPO of Fannie and Freddie.

it was another “safe bet” where “nothing could go wrong”.

it shows once again one thing: when your timeline is spammed with a certain very one-sided call — better be at least skeptical.

It proves to listen to the gut, one’s second brain.

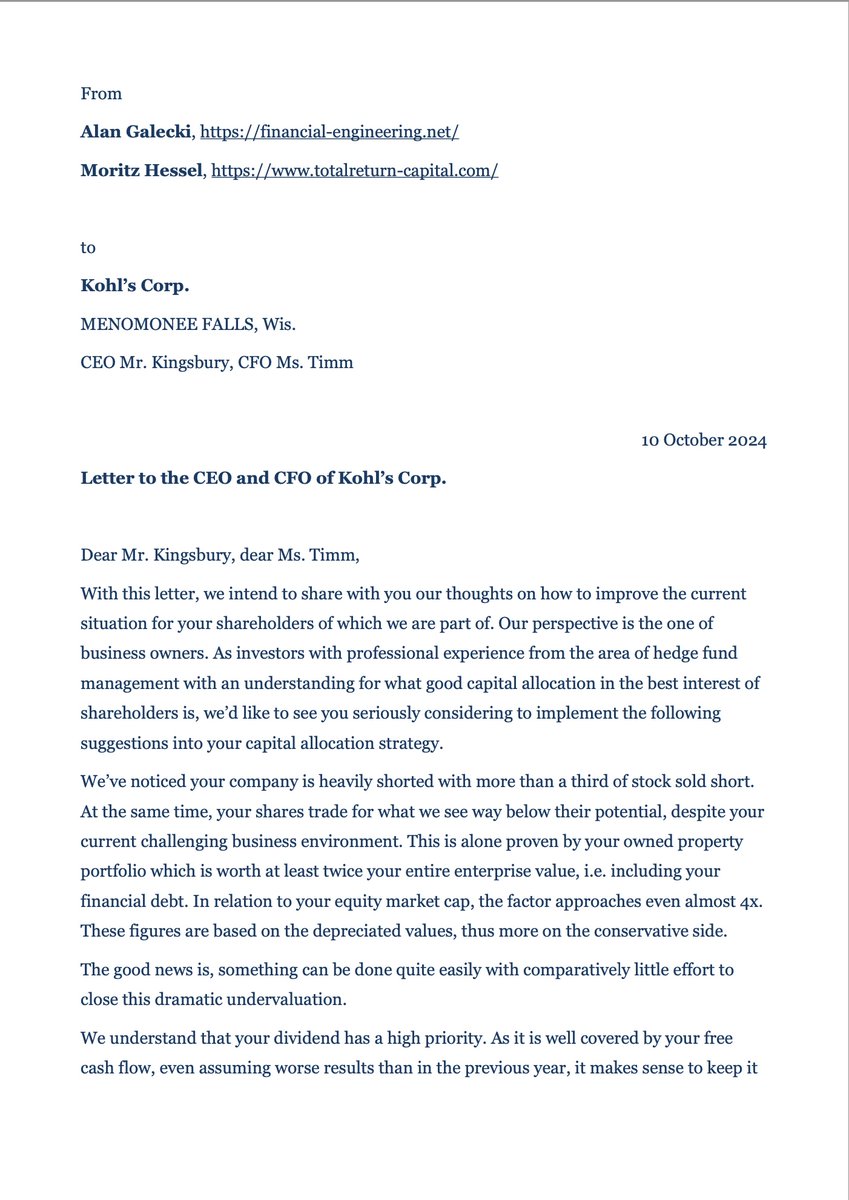

Between October 2024 prior to the election and 31 December 2024, I had $FNMAS as an active case on my blog for my students.

in my closing update I wrote that the IPO might not come.

2.5 years later, many things point to exactly that — after greedy retail investors bought another “safe bet with huge upside”.

3

322

Yes.

Not catching what too many are pitching.

Jun 12

holy shit the $ADBE conference call was a complete dumpster fire.

CEO/CFO checked out

SEMRUSH ... lol haven't used that in 10 years

Freemium model? WTF??

This is PayPal 2.0

Influencers will pump it and no one will make money

1

298

💯 worth a read 👇

Jun 11

Peter Lynch would have HATED everything about this SpaceX IPO.

I know because I worked with him at Fidelity in the 1980s. Companies like this came across our desks all the time - the hot story, the charismatic founder, the trillion-dollar promise.

The answer was always the same:

Pass, move on, and find a REAL business.

Today, SpaceX prices at $135 a share. $1.77 TRILLION valuation while all the numbers that actually matter look TERRIBLE.

"Long shots almost never pay off."

Peter spent his entire career proving this. He made his money on Dunkin' Donuts, Taco Bell, Hanes, Chrysler - businesses you could walk into, understand in 30 seconds, and value off a napkin. He avoided the hot moonshot stocks of his era because the math never worked.

SpaceX is one GIANT long shot...

- Starship has to work at scale

- Starlink margins have to hold as the satellite competition floods in

- xAI has to catch OpenAI and Anthropic in a race it is currently losing

- Mars has to generate returns inside our lifetimes

Every one of those is a coin flip. But the $1.77 trillion price tag assumes ALL FOUR are near-certainties.

Peter taught me a stock should be describable in a sentence a sixth-grader could understand. SpaceX cannot be described in a paragraph an MBA can understand.

What even is SpaceX? Is it a rocket company? A satellite internet company? An AI company? A defense contractor? A Mars colonization project?

The honest answer is yes to all five. Which means no real answer at all.

That alone would be enough for Peter to pass.

He also had a soft spot for what he called the boring profitable company. His favorite example was Kellogg's. As he put it, no matter how bad things get, people still eat cornflakes.

Now look at SpaceX.

It lost $4.9 BILLION in 2025. The xAI division alone burned $6.36 billion at the operating line. The only segment actually making real money is Starlink, at $11.4 billion in revenue.

Strip out Starlink and you are left with a money furnace.

Peter would have looked at this and bought Kellogg's instead. He would have laughed at the idea of paying $1.77 trillion for a company that loses money everywhere except one segment.

By the time a hot company hits the public market, the institutions have already taken the upside and the public is being handed the bag.

Just look at this offering:

30% allocated to retail investors worth $22.5 BILLION. That's triple the industry norm.

I have seen this with Pets .com, Webvan, Snap, Peloton, Robinhood, Coinbase, and many more.

Every one of them was the future on day one. And every one of them destroyed retail capital after the hype faded.

SpaceX enters the Nasdaq-100 15 days from now. MSCI inclusion starts tomorrow.

An estimated $22 to $27 BILLION in mechanical, forced buying from index funds is the entire short-term bull case.

Peter built his career getting into stocks BEFORE the institutions arrived. He believed your edge came from being early.

SpaceX is the opposite - every passive index fund in America is about to be forced to buy this thing at $1.77 trillion whether they want to or not.

The smart money is NOT buying SpaceX today.

You shouldn't either.

1

324

Alan Gałecki – Financial-Engineering.net retweeted

Jun 11

When Nokia engineers examined the original iPhone in the summer of 2007, they found a 2-megapixel camera with no flash, no autofocus, and no video. Their flagship phone, released three months earlier, had a 5-megapixel Carl Zeiss lens (the optics brand used in Leica cameras), autofocus, an LED flash, and video recording. Nokia beat Apple on every camera specification. Nokia also no longer makes phones.

Apple's advantage came from three engineering decisions, none of which appeared on a spec sheet. Speed was the first. Nokia's camera took 6 seconds just to open the app, with the whole process reaching 8 seconds before a first photo could be taken. Apple chose fixed focus deliberately, locking the lens at a fixed point where anything from arm's length to the horizon stays sharp. With the autofocus delay gone, the whole process took under 2 seconds from pocket to saved photo. For the actual photos people take of people and places, that speed was worth more than 3 extra megapixels.

The second decision was matching resolution to the actual use case. A 2-megapixel image is 1,600 by 1,200 pixels. The iPhone's own screen in 2007 was 320 pixels wide. The most common destination for a camera phone photo was a text message or an email with a file size limit. Apple sized the sensor for where photos were going, not for what looked best on a product box.

The third decision was the path from shutter to shared. Sharing a photo on the Nokia N95 meant opening the image, pressing Options, choosing Send, picking Bluetooth or email or a picture text, and working through sub-menus from there. On iPhone, every photo went straight into a built-in album, swipeable with a finger, emailable in two taps. Apple designed the camera as a communication tool first.

Nokia held roughly half of global smartphone sales in 2007. By 2013, that number had collapsed to single digits. Microsoft bought Nokia's phone business for $7.2 billion and wrote off virtually the entire investment as a loss within 15 months. Digital camera shipments peaked at 121 million units in 2010 and fell 94% by 2023. Apple became the company most closely linked to the phrase "digital camera" in media analysis by 2013, built from a sensor that lost to Nokia on paper.

The Nokia engineers who analyzed that first iPhone were right that the numbers didn't add up. The market had simply stopped counting them.

29

261

2,769

766,448

Exactly 👇

Extremely aggressive, sacrificing the balance sheet for… what?

Short term headlines.

Jun 11

$CRM average buyback was at $194

This is honestly one of the most irresponsible corporate finance actions i've ever seen in my life

Like they literally tried to time the exact market bottom with their entire borrowing capacity

Re

Tar

Dio

1

328

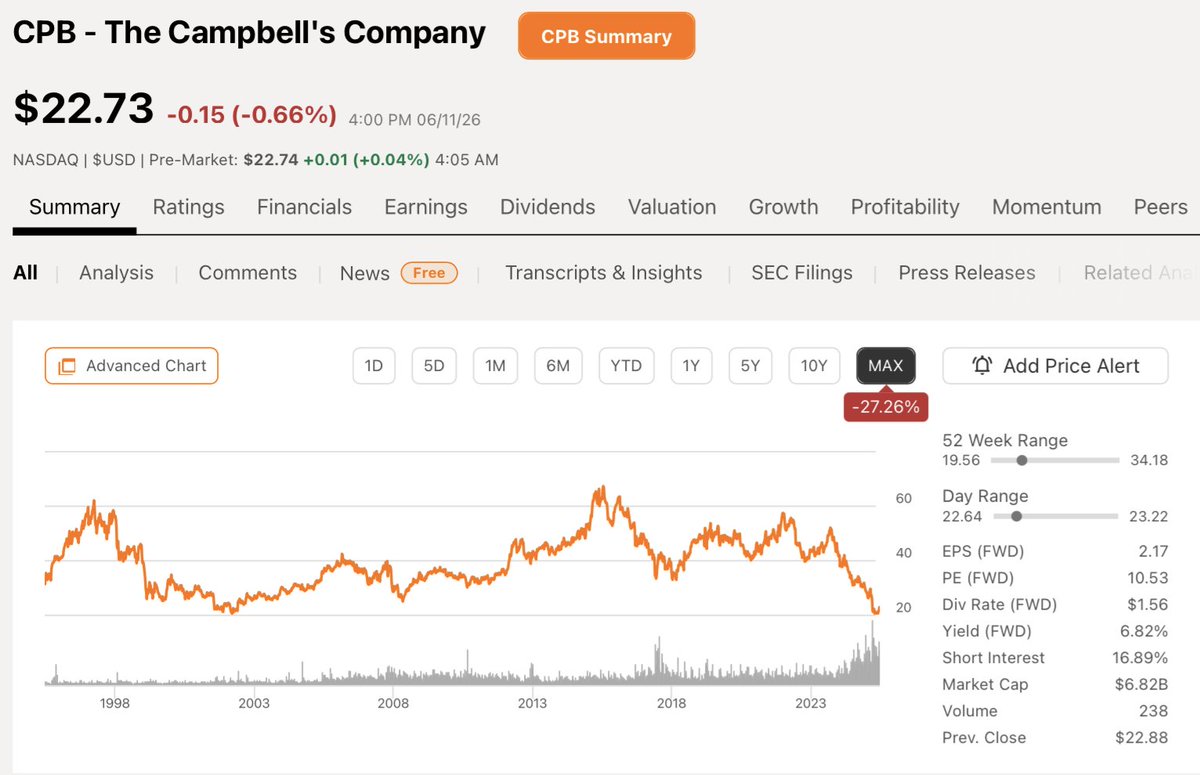

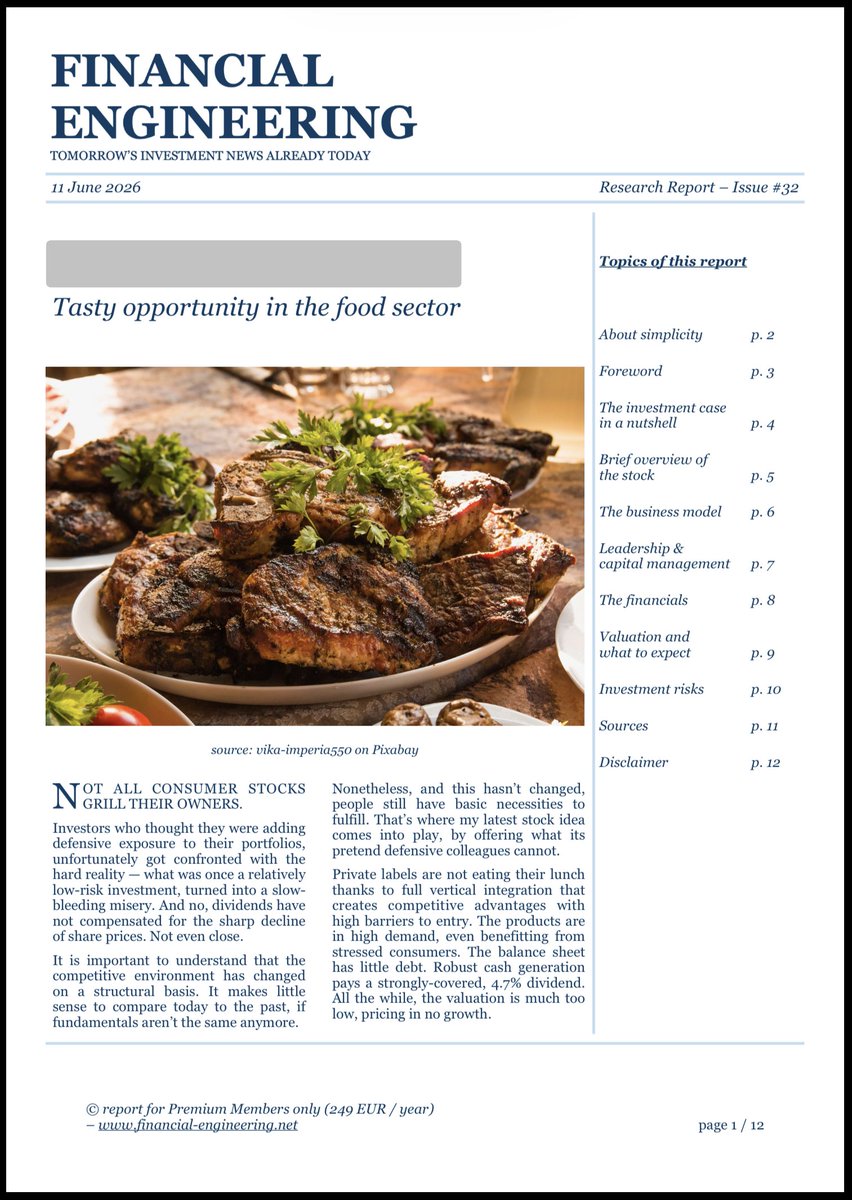

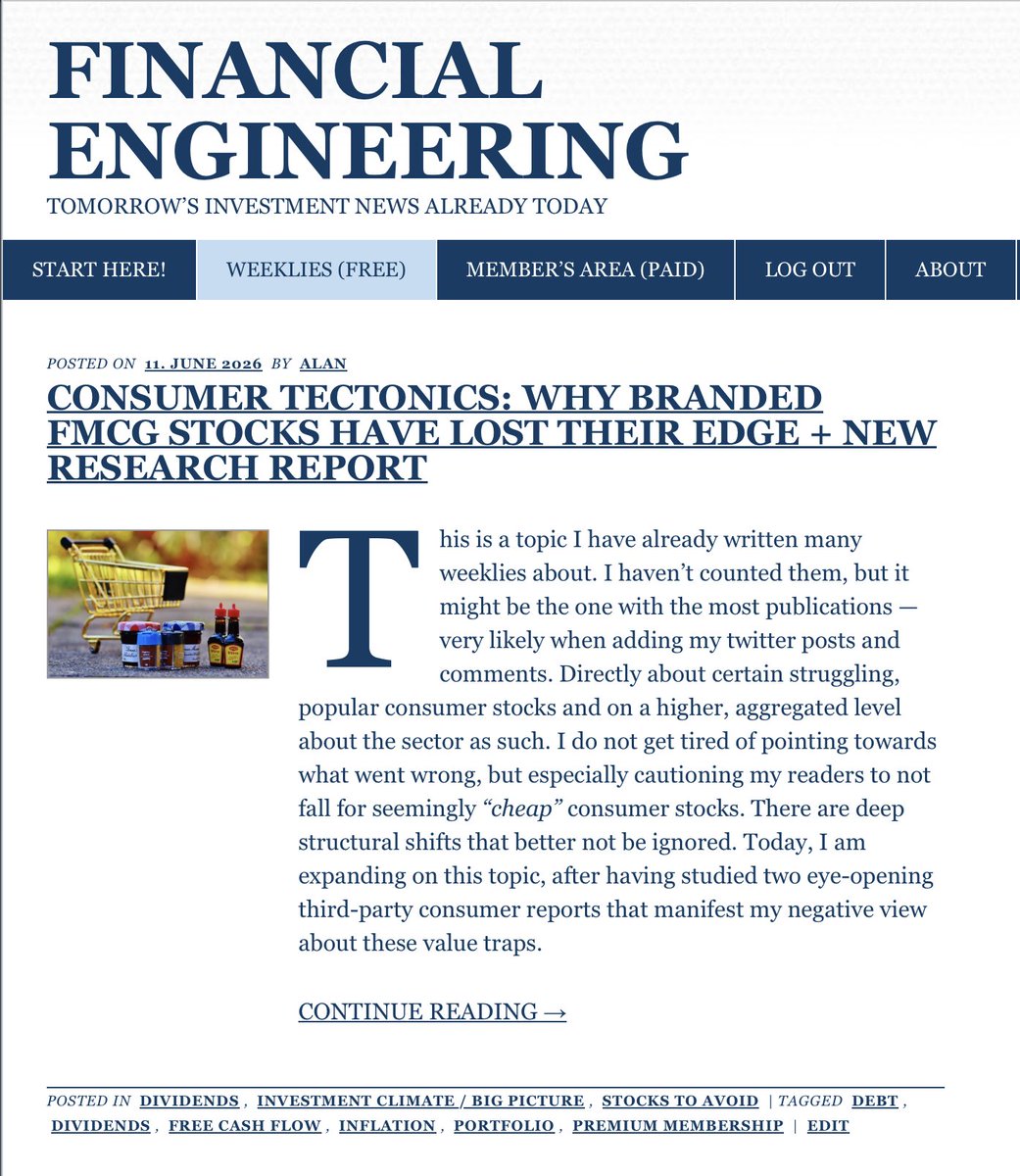

Earlier today, I dropped my latest research report, discussing a tasty case in a blood-shed sector:

consumer staples / food

many trade near multi-year or even -decade lows…

this one isn’t participating in bringing-shareholders-to-the-slaughterhouse.

member-exclusive.

link to my blog in my bio

1

1

171

… but the buybacks …😁

1

7

1,306

Alan Gałecki – Financial-Engineering.net retweeted

I can tell you.

I published a report about $FNMAS in October 2024 on my blog before the presidential election.

but once Ackman started pounding the table aggressively, I closed this case again.

and this is when most people jumped in.

1

186

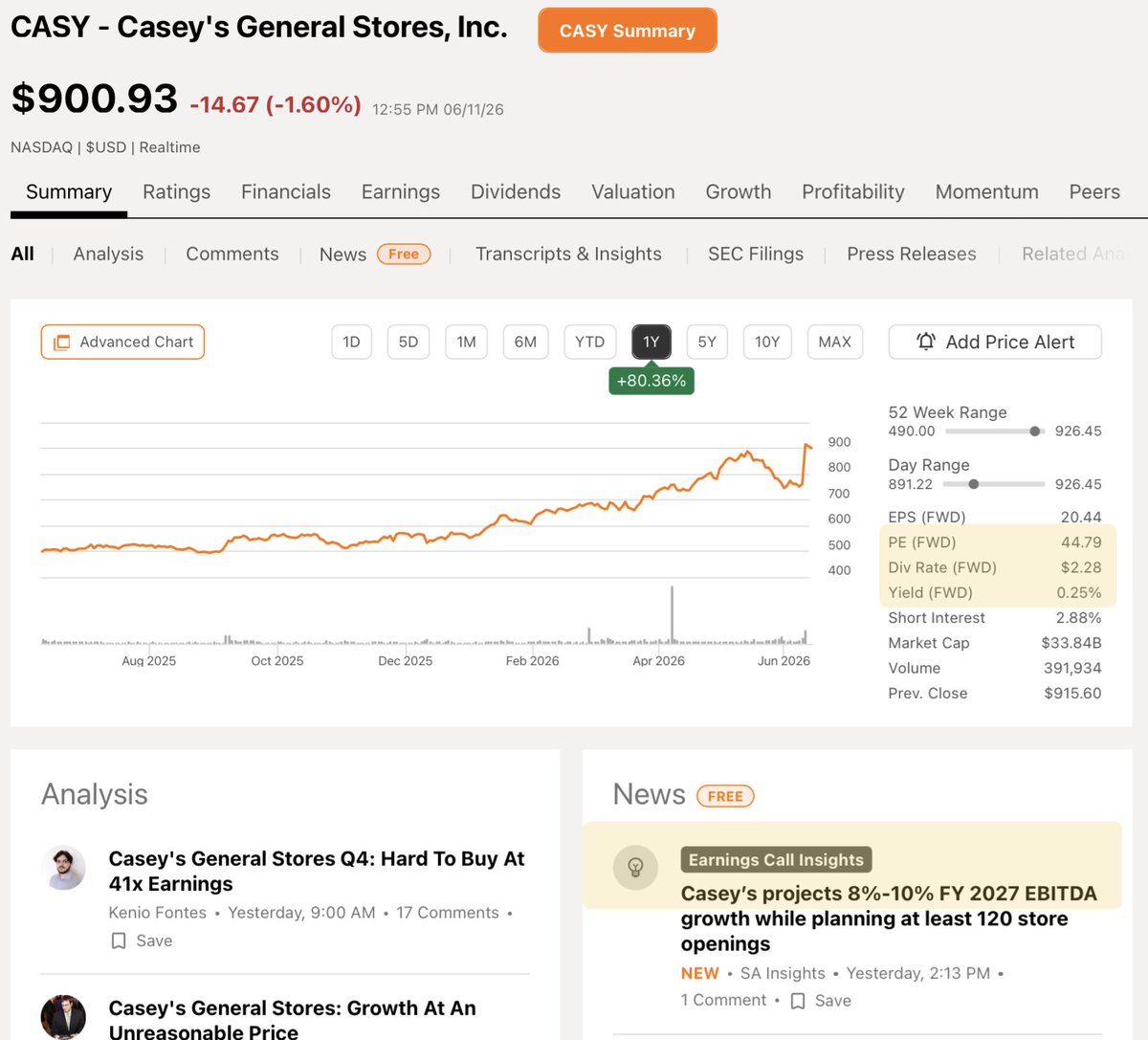

Everyone’s talking about the AI and space bubbles.

but about something more tangible.

don’t tell me this will end well…

$CASY

5

352

"Buy and hold" is one of the most dangerous pieces of advice in investing.

I already explained in the past why blindly holding forever can destroy more wealth than it creates — especially once moats erode and the world moves on.

Most "set it and forget it" investors end up bagholding losers for decades — just ask consumer-staples owners.

financial-engineering.net/wh…

1

2

182