Pro-Humanity Anti-Imperialist 💕 We must RESIST the Corporate Political Oligarchy & help birth The New Multipolar World of Peace 🌏 #ProtectPainPatients

Joined March 2020

- Tweets 25,159

- Following 1,072

- Followers 3,853

- Likes 129,892

7,083 Photos and videos

Pinned Tweet

Has anyone bother to ask Prof Jeff Sachs of Colombia Uni who was made head of a multi year “Lancet Investigation” why he did NOT know that his Lancet Team “researching COVID lab leak in Wuhan” included those who ran EcoHealth Alliance for years? 🤷♀️

Took me 5 min on my phone 🤔

2

10

316

Marianne Elizabeth 🕊️ retweeted

That’s a keeper! 💯

Here’s a few more I collected in the last few days for all to save, share etc 🙏

2

3

4

61

Marianne Elizabeth 🕊️ retweeted

And here we are!

110

1,876

8,716

48,459

Marianne Elizabeth 🕊️ retweeted

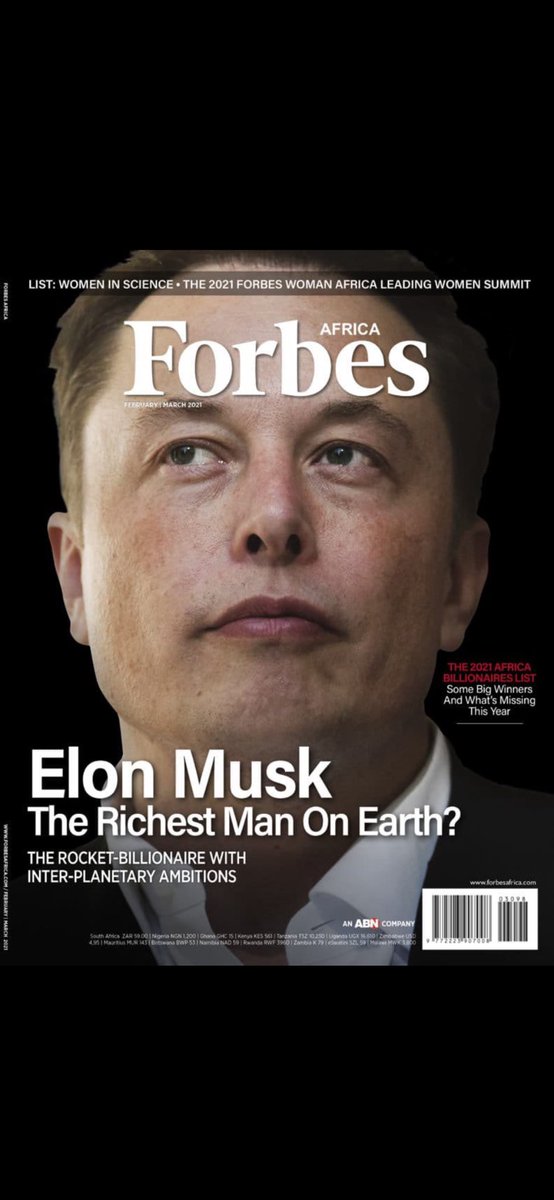

Logros del capitalismo: crear un trillonario.

Logros del socialismo chino: sacar a 850 millones de personas de la pobreza.

No tengo nada más que decir.

2,760

4,946

23,461

625,617

Marianne Elizabeth 🕊️ retweeted

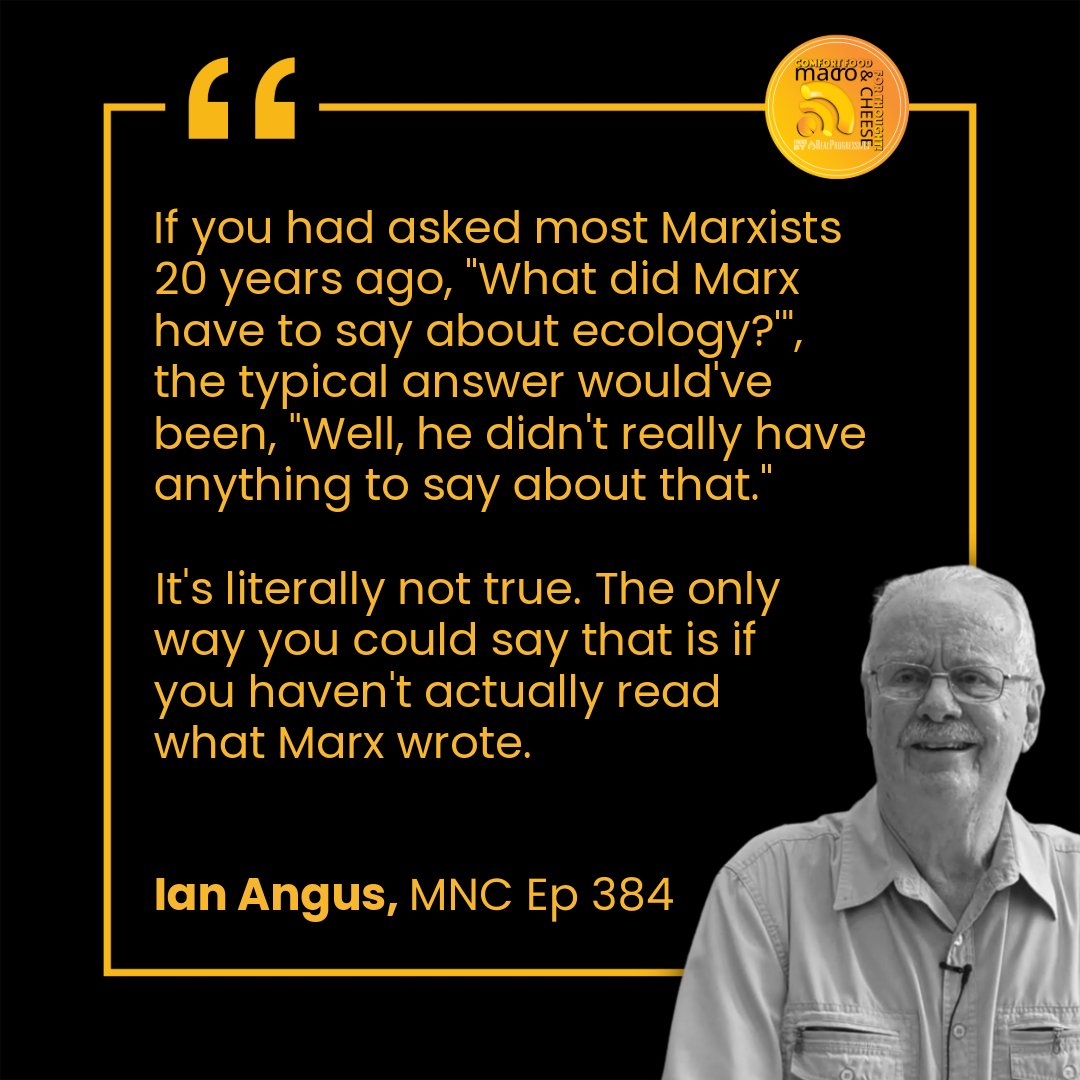

Episode 384 – Metabolic Rifts: Capitalism’s Assault on the Earth System with Ian Angus. New full episode of #MacroNCheese on our free #Substack below. 👇

2

14

14

294

Marianne Elizabeth 🕊️ retweeted

Jun 14

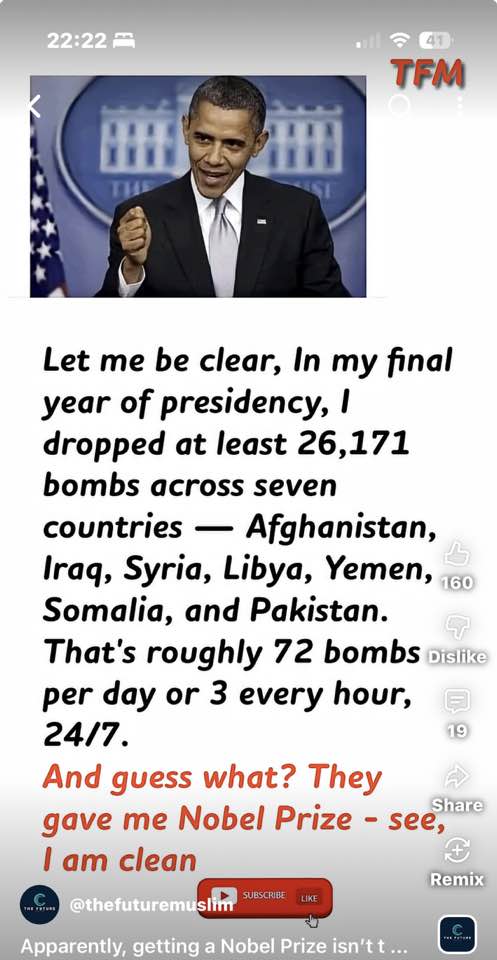

Never forget that she called for the killing of Palestinian journalists a very long time ago.

2

2

81

1

Marianne Elizabeth 🕊️ retweeted

Jun 14

10 MOST EMBARRASSING HEADLINES IN THE BIOLABS SCANDAL

The world was told repeatedly that no US biolabs existed in Ukraine—such claims were “disinformation” from Russia, China, and from right-leaning people in the US.

That's what NBC, BBC, AFP, AP and others told the planet repeatedly.

But this week, US spy chief Tulsi Gabbard admitted that there WERE biolabs in Ukraine and elsewhere, they WERE US-funded, and they WERE experimenting with deadly viruses like ebola and sars.

Russia, China, and the US rightwingers had been right all along.

Also, as it became apparent that they existed, many media companies switched to a highly imaginative narrative saying that the Pentagon was funding overseas biolabs experimenting on killer viruses for “peace and health” reasons.

Because everyone knows that the Pentagon is all about peace and health, right? (sarcasm alert)

Check out these 10 headlines that media companies are surely praying have been forgotten!

46

457

912

25,070

Marianne Elizabeth 🕊️ retweeted

Jun 14

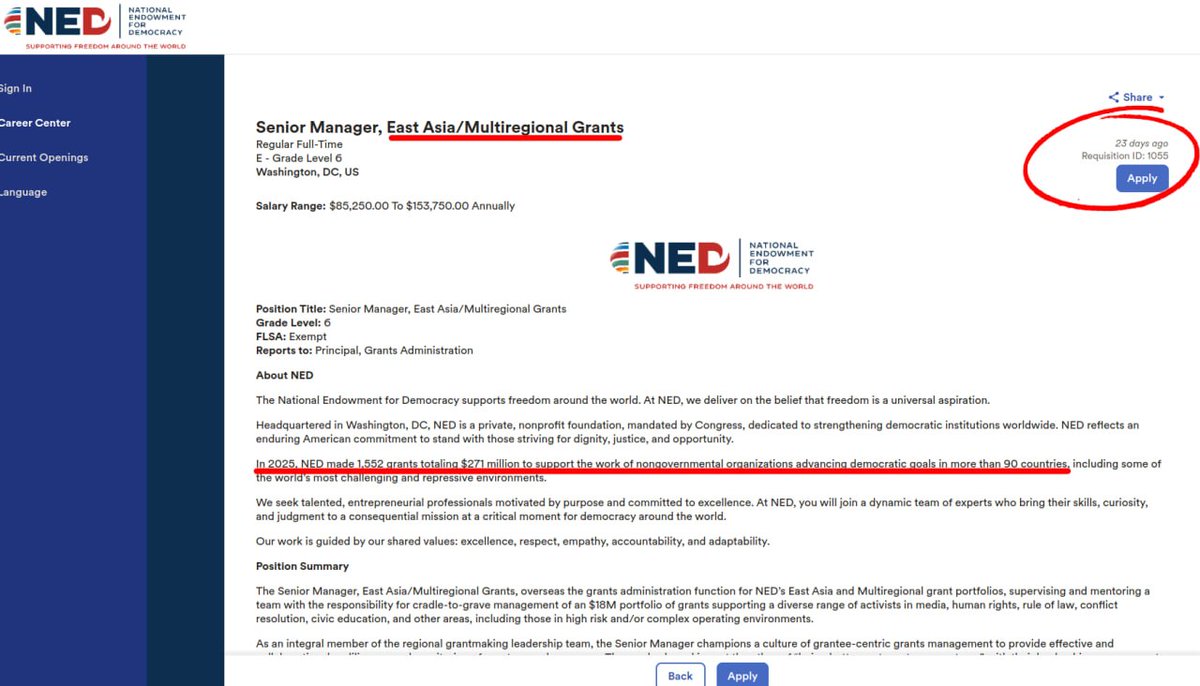

For those who thought the Trump admin "closed down" the National Endowment for Democracy.

Here is a job listing: workforcenow.adp.com/mascsr/…

14

26

600

🤭

1

1

32

Marianne Elizabeth 🕊️ retweeted

This is why Jacobin has a multi-million dollar annual operating budget.

Jun 14

China has “witnessed the greatest stretch of growth and poverty alleviation in human history”; provides an absolute guarantee of food, housing, clothing, clean water, modern energy, education and healthcare to all of its 1.4 people; has emerged from extreme backwardness to being a science and technology superpower; is leading the world in green energy; and has achieved living standards comparable with the West.

Our friends at Jacobin ask: but at what cost?

These geniuses have realised that the exploitation of labour still takes place in China and that, in an enormous developing country, a lot of jobs are somewhat more onerous than sitting in an air-conditioned office in New York cranking out anti-China rubbish.

6

39

240

9,289

Marianne Elizabeth 🕊️ retweeted

Carl Menger's barter story is one of the most successful myths in economics.

The problem is not that it is theoretically possible. The problem is that there is little historical or anthropological evidence that societies actually developed money this way.

As David Graeber pointed out, anthropologists spent more than a century searching for examples of economies organized around pure barter and repeatedly came up empty. What they found instead were systems of credit, debt, obligation, and social accounting. People kept track of who owed what long before coins or commodity money became widespread.

The familiar story of a blacksmith searching for a farmer who wants horseshoes is largely a thought experiment. Real communities were not collections of strangers conducting spot transactions. They were networks of ongoing social relationships where obligations could be recorded and settled over time.

Historically, money often emerged alongside institutions capable of measuring and enforcing debts. Temples, palaces, kingdoms, and states maintained accounts, levied taxes, and denominated obligations in units of account long before everyday markets were dominated by coinage.

Coinage itself was frequently linked to states paying soldiers and then demanding taxes in the same currency. This created demand for money not because markets spontaneously selected it, but because political authorities structured the monetary system around it.

The historical record suggests that credit came first, coinage came later, and barter usually appears at the margins when monetary systems break down, not at the beginning of economic history.

The real myth is not that states played a role in the development of money. The real myth is that money emerged from a world of isolated traders solving the double coincidence of wants problem through spontaneous market evolution alone.

20

172

435

16,140

Marianne Elizabeth 🕊️ retweeted

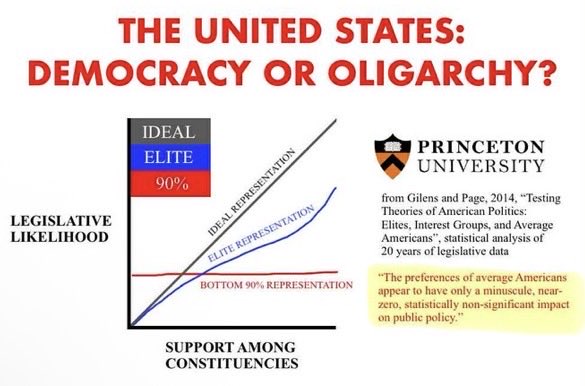

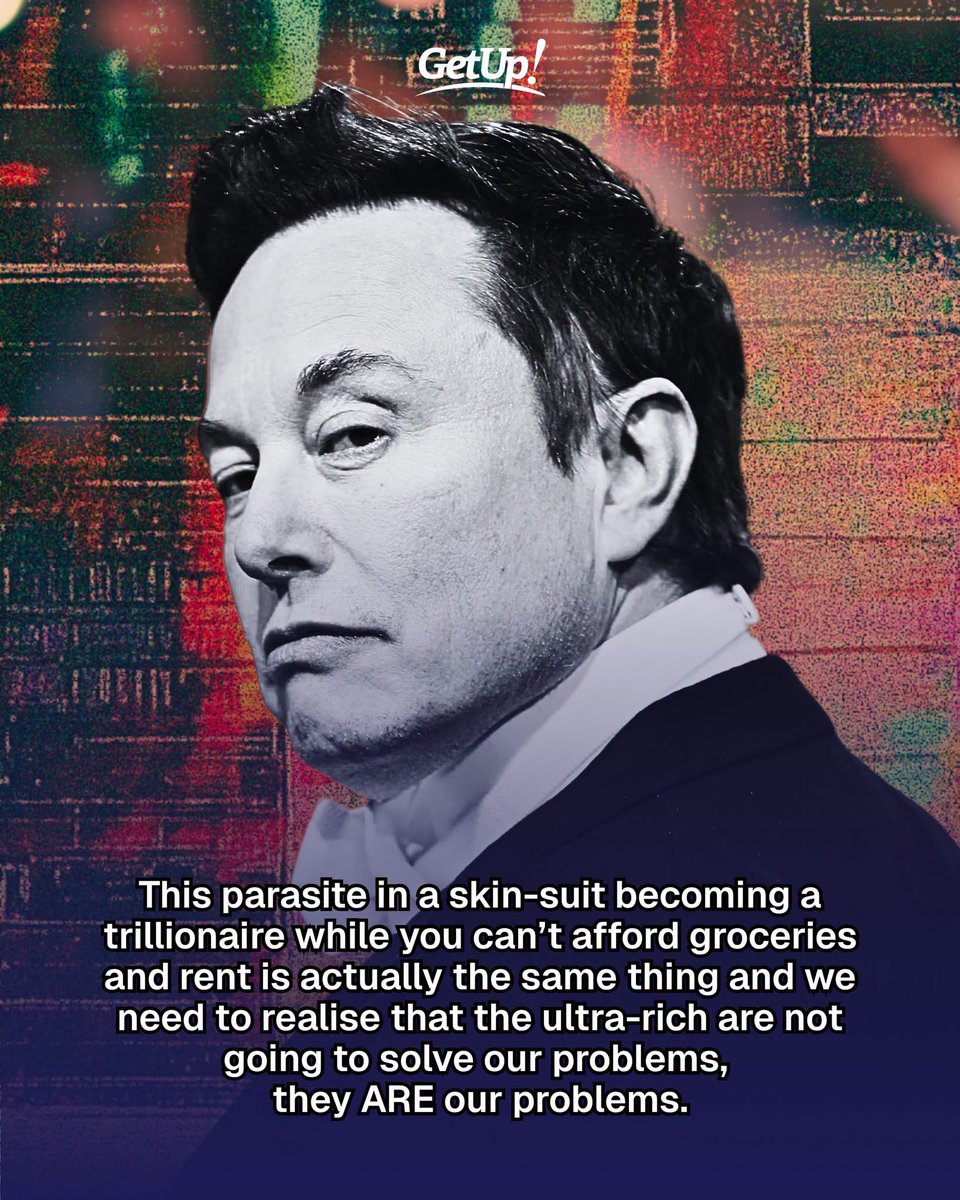

Americans get their opinions from Epstein Files Billionaires and call it "Freedom"

Jun 14

3

5

189

Marianne Elizabeth 🕊️ retweeted

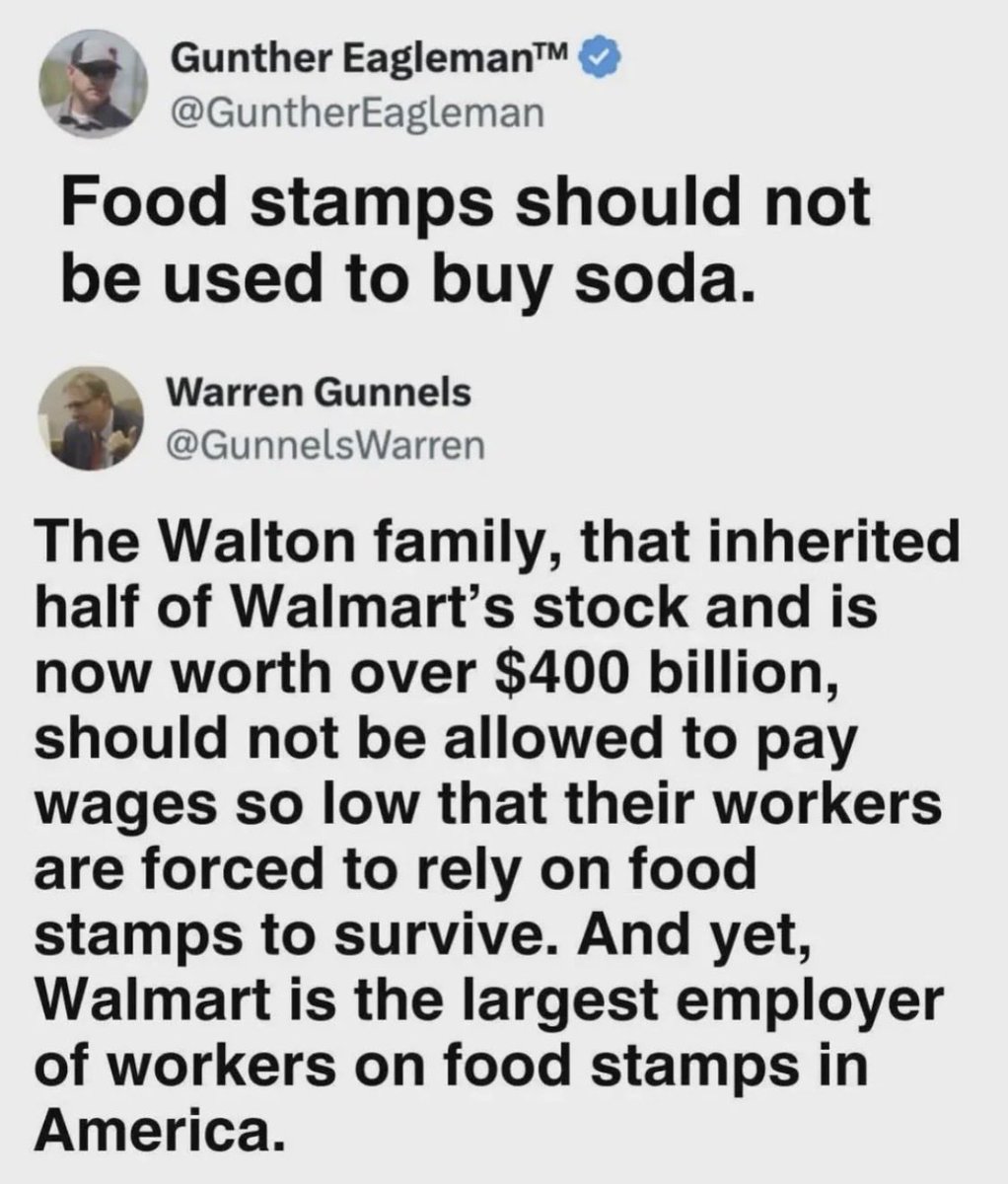

“Politicians” in the US have two qualifications lying & fundraising

Under “lying” AOC turns lying into a performance & has done on many occasions…

Here are just a few…

1

4

57

Marianne Elizabeth 🕊️ retweeted

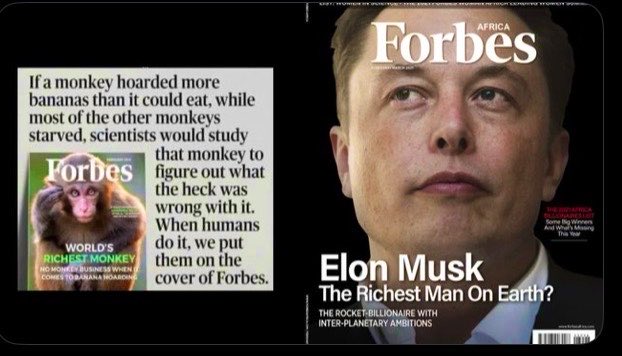

in nature if a monkey hoarded 1 trillion bananas the other monkeys would beat that monkey to death and take his bananas

2

60

262

3,103

Marianne Elizabeth 🕊️ retweeted

Good afternoon 👋

3

41

258

2,604

Marianne Elizabeth 🕊️ retweeted

Jun 13

Bloomberg is owned by the world's 18th richest man.

Billionaires emit more carbon in one hour than a poor person does in a lifetime.

This is propaganda.

163

7,642

27,645

210,500