Joined March 2026

- Tweets 800

- Following 96

- Followers 28

- Likes 775

9 Photos and videos

Got a new 2-step ladder for the home today.

Told herself there is instructions with it for her if she wanted to read them...😀

And I stopped short of telling her, for fear of being put in the dog house, that it supports up to for 150kg, which of course she is well within...😀

1

Frank Square 🇮🇪 retweeted

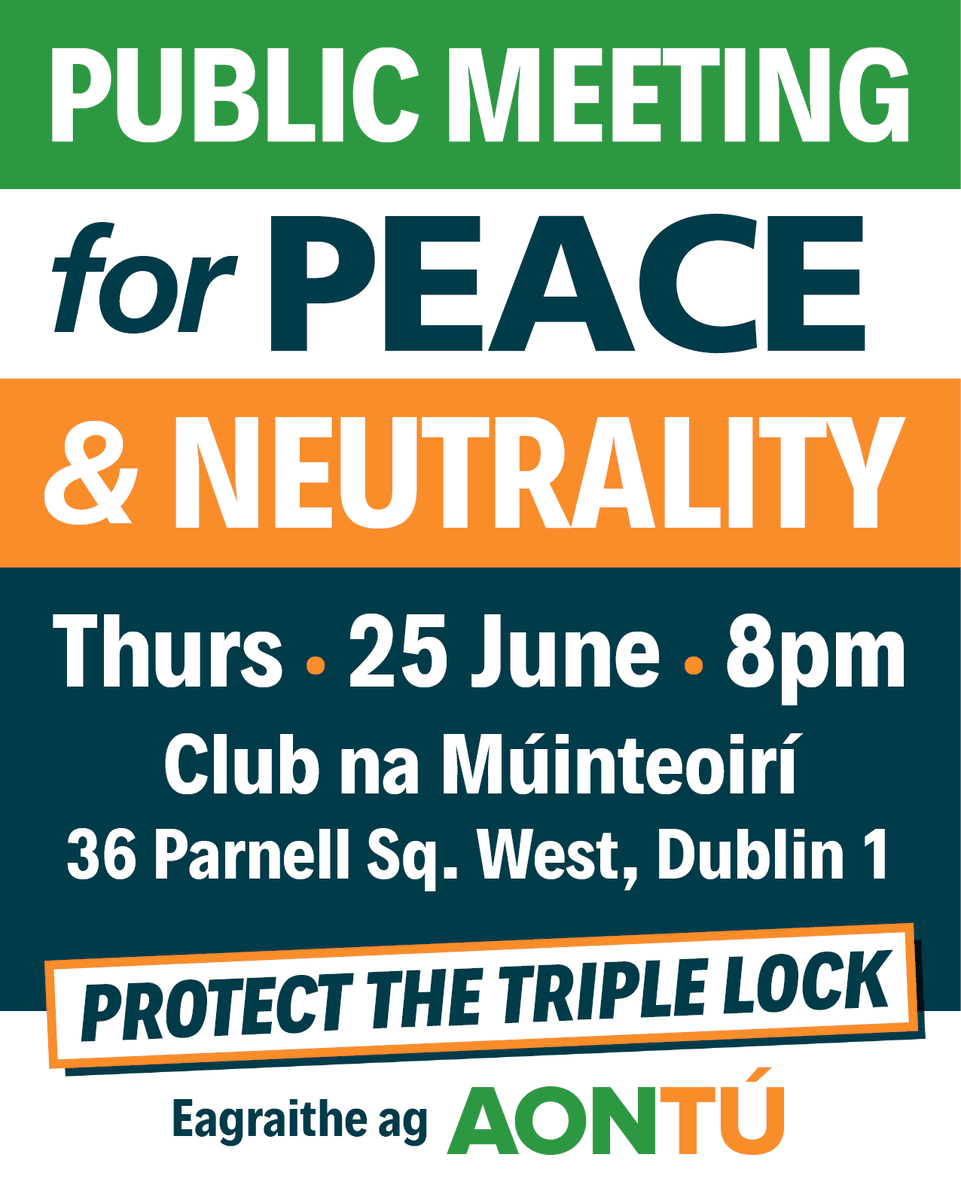

The government seeks to end Irish Neutrality.

Another sovereignty swap with the EU.

Please help the push back.

18

46

130

2,737

Frank Square 🇮🇪 retweeted

Jun 14

🇮🇪🚨

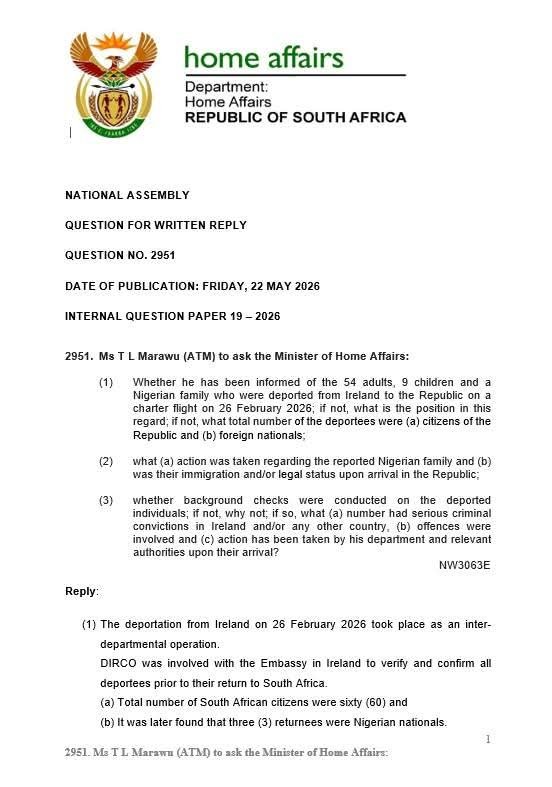

The "South African" family that was deported from Ireland this year have been arrested in South Africa as they were Nigerians who illegally obtained SA passports 🇳🇬

These Nigerians scammers were plastered all over Irish media and used as a sob story by media & NGOs

Jun 12

The Department of Home Affairs has confirmed that the Nigerian family deported from Ireland earlier this year was taken into custody upon arrival at OR Tambo International Airport.

Responding to questions raised by ATM, the department stated that the family was transferred to Lindela Repatriation Centre before being deported to Nigeria.

Authorities allege that the family had entered Ireland using fraudulently obtained South African passports.

71

1,106

2,913

62,142

Frank Square 🇮🇪 retweeted

€90 million is a massive amount of money.

44

149

715

9,100

Frank Square 🇮🇪 retweeted

Children need safeguarding.

This is outrageous.

“𝐀𝐛𝐬𝐨𝐥𝐮𝐭𝐞𝐥𝐲 𝐬𝐡𝐚𝐦𝐞𝐟𝐮𝐥”: 𝐋𝐞𝐚𝐝𝐢𝐧𝐠 𝐂𝐡𝐢𝐥𝐝𝐫𝐞𝐧’𝐬 𝐑𝐢𝐠𝐡𝐭𝐬 𝐋𝐚𝐰𝐲𝐞𝐫 𝐂𝐨𝐧𝐝𝐞𝐦𝐧𝐬 𝐏𝐥𝐚𝐧𝐬 𝐓𝐡𝐚𝐭 𝐂𝐨𝐮𝐥𝐝 𝐒𝐞𝐞 𝐕𝐢𝐭𝐚𝐥 𝐅𝐢𝐥𝐞𝐬 𝐎𝐟 𝐂𝐡𝐢𝐥𝐝𝐫𝐞𝐧 𝐓𝐚𝐤𝐞𝐧 𝐈𝐧𝐭𝐨 𝐒𝐭𝐚𝐭𝐞 𝐂𝐚𝐫𝐞 𝐁𝐲 𝐓𝐮𝐬𝐥𝐚 𝐃𝐞𝐬𝐭𝐫𝐨𝐲𝐞𝐝

One of Ireland’s best known human rights lawyers @GarNob specialising in children’s rights has strongly criticised the Government’s handling of the transition to the new national Guardian ad Litem (GAL) service, warning that vital records relating to vulnerable children may be lost.

Responding to a report by Kitty Holland in The Irish Times, solicitor Gareth Noble described the situation as “absolutely shameful” and accused Minister for Children Norma Foley of pursuing a model that would bring the representation of children in care proceedings under direct State control while failing to protect historic records created by independent GAL services.

Noble expressed particular concern that organisations such as Barnardos, Tigala and Gallore, which currently hold extensive files relating to children involved in care and family law proceedings, are being wound down without arrangements to transfer much of the information they have gathered over many years.

In a post on X, he argued that the first action of the new State operated service appears to be refusing to accept large volumes of historic and current information about children that has been collected by GALs. He warned that records containing crucial details about children’s lives, experiences and wishes could effectively disappear from the system.

The criticism follows growing concern among GAL practitioners that thousands of files containing children’s letters, drawings, personal reflections and accounts of traumatic experiences may have no secure archival destination when the new service begins operating on 23 June. Practitioners fear that, in the absence of a legal mechanism for transfer or retention, some records could ultimately be destroyed.

Noble’s intervention adds to mounting pressure on the Department of Children to establish a solution that preserves these files. Campaigners and child welfare advocates argue that the records form an important part of many children’s personal histories and may prove invaluable to them later in life as they seek to understand their experiences in care and child protection systems.

His comments highlight a growing debate over whether the transition to the new GAL service risks sacrificing decades of independent advocacy records at the very moment the State is assuming greater responsibility for representing the voices of children before the courts.

1

12

19

367

Frank Square 🇮🇪 retweeted

A female 'Muslim' lawyer from Jordan supports "Honor Killing" on live television. 😱

She asserts that, if a father discovers something negative about her daughter and slaughters her, it is natural and their right. 🤬

She would not object to this practice. 🫣

This is Islam. ☪️

Jun 13

Low IQ Muslim Woman from Algeria says, "A man who doesn't beat his wife isn't a real man".

60% of Algerian women think a husband has the right to beat his wife. 🤡

157

1,817

3,880

61,124

Frank Square 🇮🇪 retweeted

Jun 14

Elon Musk just called out the EU’s biggest lie on “democracy.”

As Ursula von der Leyen lectured the world, Musk hit back: “If democracy is the foundation of freedom, why isn’t your position as EU leader directly elected by the people?”

Unelected bureaucrats imposing mass migration, net zero extremism, and speech crackdowns on 450 million citizens — with zero accountability.

This isn’t democracy. It’s slow-motion dictatorship.

The people are waking up. The EU’s days are numbered.

Agree?

375

2,372

5,884

59,929

Frank Square 🇮🇪 retweeted

HORRIFYING: Yasmeen Khan, owner of a beauty salon, offered free courses to young Christian and Hindu women to lure them in. Once there, she drugged their drinks. When they lost consciousness, she called her husband Mohammed Khan, who raped them while she stood watch at the entrance.

They recorded the abuses to blackmail them and force them to have relations with more Muslim men. When questioned, Yasmeen justified the crimes by saying that helping to rape "infidel girls" would lead her to Paradise.

This is Islam.

1,559

20,880

53,746

2,133,479

Frank Square 🇮🇪 retweeted

🚨 SHOCKING DISCOVERY THEY BURIED:

Hydroxychloroquine doesn’t just fight viruses — it turns viruses into precision-guided cancer killers. It allows viruses to attack cancer cells while leaving healthy cells completely untouched.

This comes straight from Dr. Richard Urso (ophthalmologist and member of America’s Frontline Doctors) in a powerful presentation. Why was this information suppressed and the data obscured?

Because a cheap, decades-old drug that could selectively destroy cancer would be catastrophic for the multi-trillion-dollar cancer industry.

They don’t want you to know this. They want you dependent on expensive treatments forever.

The truth is out. Share it before it gets buried again.

247

12,892

25,629

444,593

Frank Square 🇮🇪 retweeted

Welcome new followers 🙏 - the why?

Enda Kenny, @EUCssrMcGrath all promised an Irish Banking Inquiry that would expose “reckless and outrageous” decisions, be free from political motivation and generate “new insights.”

In practice, inside that Inquiry, I saw - as explained to @ArturNadol7566-:

🔹copious evidence withheld

🔹documents heavily redacted

🔹crucial witnesses being questioned without the relevant evidence

🔹other important witnesses excluded

🔹disabling conflicts of interest ignored

🔹lines of inquiry - particularly on liquidity & solvency - shut down

I had walkout in April 2015, waiting for protected disclosures to be reviewed - rather than risk lending my name to a managed exercise in mega damage limitation (otherwise known as a cover up of all cover ups).

However, my identity was lifted in early 2016 to sanitise a pre‑cooked narrative - along with other experts who were no longer there, with one having walked out in May 2015, in solidarity with me.

Meanwhile Dutch lawyer and whistleblower - Hester Bais @Wftproof - please follow - was uncovering how banks across Europe were abusing OTC derivatives and collateral and masking massive collateral shortfalls, inflating balance sheets and recycling pledged assets in what she describes as a coordinated “Worst Bank Scenario” fraud, with hidden under‑collateralisation running to hundreds of billions in each major jurisdiction and trillions globally.

Bais’ findings also showed that derivatives offered to bank customers as “protection” were not being used to limit risk, but instead to make windfall profits through deception.

This mirrors activities in Ireland and across many other EU countries including the U.K. as uncovered there - by @stevemiddi1 & @BankConfidenti1

Non-independent judiciaries facilitated the recovery of assets by banks from defrauded victims in numerous jurisdictions.

False pleadings were also routinely filed in court, misrepresenting the banks’ activities as routine.

Separately, ordinary borrowers were subjected to systematic mortgage abuse: undisclosed restructures / recoding; mis allocation of payments, deliberate mis‑calculation of interest and arrears, strategic overcharging and manufactured defaults used to justify repossessions.

These practices were not peripheral and they sat at the heart of how banks monetised distress - yet the Inquiry’s structure and evidential constraints meant the lived realities facing small businesses and mortgage holders were sidelined, while institutional narratives were carefully curated and amplified.

Regulators allowed these activities to persist - or oversaw wholly inadequate supervision - note Ireland’s constrained Tracker Mortgage Examination.

So this systemic abuse of Irish bank customers was ongoing in parallel with the Irish Banking Inquiry - supposedly set up to confront what had happened to lead us to crisis - while actors knew the methodologies being implemented to shore up crippled balance sheets by unsuspecting customers.

The constitutional property rights of the Irish were removed, in a yet unknown covert agreement, and the effects are evident every day in our courts.

Borrowers who did not default, were grossly overcharged, duped by derivatives & in some cases still managing to offer to redeem loans - are facing paramilitary style evictions in this country.

Even where banks acknowledge that no loan document was signed - in their own paperwork- they will still aggressively enforce with judicial oversight. Forged signatures/ composite documents- can in this country still permit recovery of assets.

The risks associated with having debt and a mortgage in this country are poorly understood.

1

26

44

813

Frank Square 🇮🇪 retweeted

14h

🚨🗣️New: Zlatan Ibrahimovic on Vinicius Junior refusing the mandatory halftime interview with FIFA at the World Cup:

“People are shocked that Vinícius walked away from a halftime interview. I am shocked that anyone thinks he should have stopped in the first place.

Halftime is not a television studio. Halftime is not a podcast. Halftime is not a red carpet. Halftime is the heartbeat of a football match.

For 45 minutes, players are warriors in a storm. They run, they fight, they suffer, they bleed. Then they get 15 precious minutes to recover, to breathe, to listen, to think. And FIFA wants to spend part of that time chasing soundbites? That is like pulling a Formula 1 driver out of his car during a pit stop and asking him how the race is going.

And FIFA’s idea is to shove a microphone in the player’s face and ask, ‘How do you feel?’

How do you think he feels? He’s exhausted.

This is modern football’s biggest disease. Everything is content. Everything is sponsorship. Everything is television. The match hasn’t even finished and they’re already trying to manufacture headlines.

They tell us they care about player welfare. Really? Then why are players playing more games than ever? Why are tournaments expanding? Why are injuries increasing? And now they want halftime interviews too? The hypocrisy is unbelievable.

Halftime is sacred. It belongs to the players and the coaches. That’s where games are won. That’s where tactics change. That’s where injuries get treated. That’s where leaders speak. It is not a media circus.

And don’t tell me this is for the fans. Fans want better football, not a tired player giving a robotic 20-second answer because somebody sold another broadcast package.

Vinícius understood that. He chose football over public relations.

The funniest part? They threaten him with a fine. A fine. As if that changes the principle. If I were there, I’d pay it too. Because some things are worth more than money.

If FIFA really had their way, they’d put microphones in the dressing room and call it innovation.

Football should come first. Not content. Not commercials. Not corporate greed.

For once, a player pushed back. And that’s exactly why so many people are angry.”

368

6,953

38,767

1,009,856

Frank Square 🇮🇪 retweeted

Jun 10

Ireland's fate was sealed on the 26th June 2024 when our Politicians voted to opt into the EU Asylum and Migration Pact. There is now no magic wand to reverse this betrayal of the Irish people by their Public Representatives. There is no Protocol 21 opt out. Any Bill presented to the Oireachtas to withdraw is meaningless, as European law takes precedence over domestic legislation. The only way now is to leave the EU.

Any Opposition Politician who tells you otherwise, is just giving false hope. Playing on the anxiety and desperation of many Irish people who are fearful about the future of our ancient land. This false hope is just another form of betrayal. As a consequence we are now in serious danger of moving into an era where (almost) no Politician will be trusted by the People.

It is time now to consider a rejection of the current political system and to bring forward new proposals for Direct Democracy and People Power. This current political system no longer serves the interests of the Irish people.

It is not only the Establishment that must be held to account but also each and every Opposition Politician. We can start Direct Democracy by the establishment of local community networks to take back power by holding all Public Representatives to account. Currently, we are all being played by Politicians. Power belongs in the hands of the People. There is a serious imbalance which must be restored.

As we see through the empty theatrics of these political actors,we must demand ACTION. Start by putting pressure on local Councillors and TDs to apply for a full exemption under Article 62 of the EU Migration Pact AMMR (relocation quotas). Ireland is already under significant migratory pressure. Poland's Government applied for and got an exemption, but the Irish Government has so far failed to do so. The time for action is now. The power is in your hands.

62

299

683

17,617

Frank Square 🇮🇪 retweeted

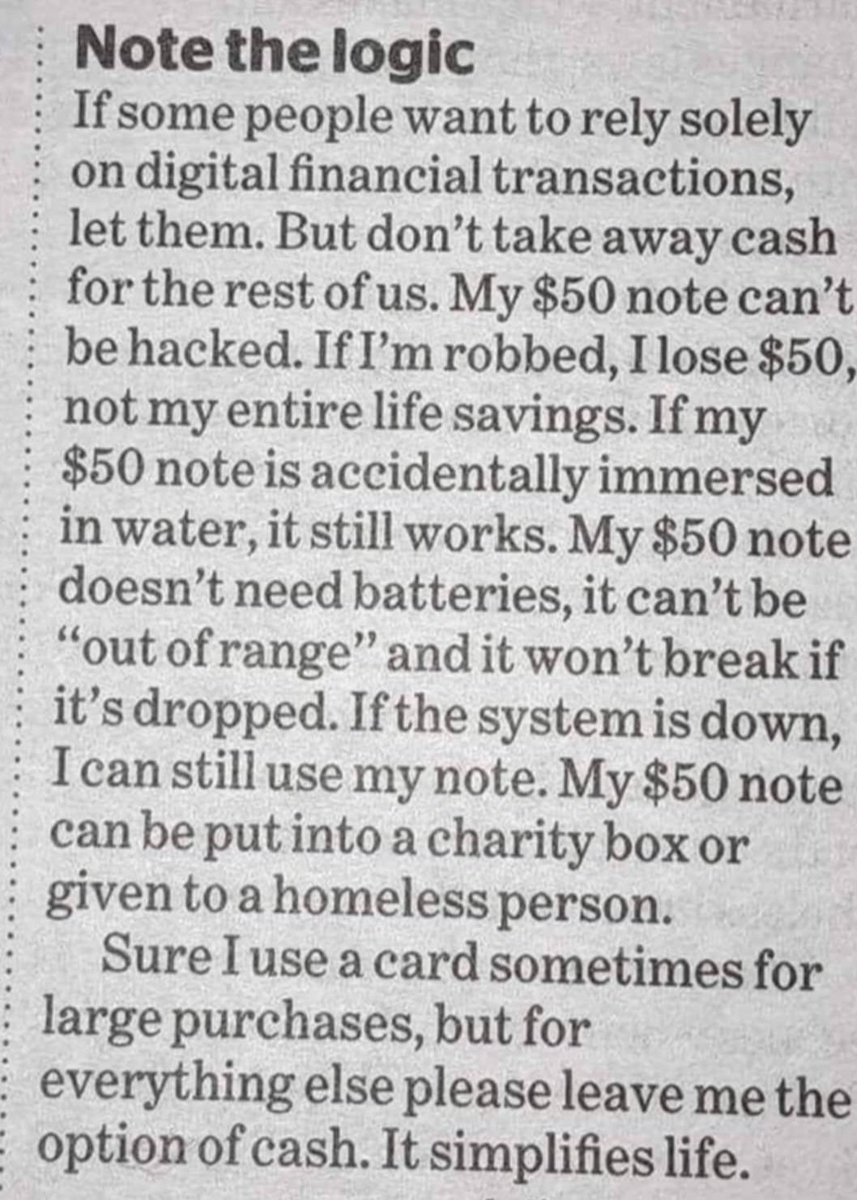

Jun 12

If you have a Gmail account, you need to read this.

Google's AI now scans your emails and attachments, bank statements, tax files, medical letters, all of it. It turned on by default, and there's a class-action lawsuit over how.

Here are 5 moves to shut it off, the switch is hidden in two places:

366

14,772

46,499

8,458,626

Frank Square 🇮🇪 retweeted

Jun 11

In a major development for financial sovereignty, Swiss voters have dealt a massive blow to the push for digital currencies and the central banking agenda championed by European Central Bank President Christine Lagarde.

34

159

522

7,951

Frank Square 🇮🇪 retweeted

Jun 11

We sent the Taoiseach a copy of a petition that has been signed by well over 60,000 Irish citizens.

It calls on the government not to participate in the EU Migration Pact.

The EU migration pact is bad for Ireland.

It does not have public support.

aontu.ie/stop-the-eu-migrati…

71

331

1,852

18,561

Jun 12

Simulation is alive & well going by seeing those real, grown men diving, taking up the foetal position and rolling over as if they were seriously hurt at the World Cup matches I have seen so far.

Then, they get up, are grand & play away again till the next dive & roll. Seriously!

23

Frank Square 🇮🇪 retweeted

A higher percentage of migrants are in receipt of benefits in Ireland than Irish nationals.

But they claim that migrants are "no more likely to claim welfare"

The ESRI, pretty good at manipulating statistics.

17

174

642

10,127

Frank Square 🇮🇪 retweeted

Jun 11

A JUDGE HAD NO WORKERS RIGHTS

Claire Gilham was a district judge in Warrington. She spent her days dealing with some of the most difficult civil and family cases in the North West. People going through divorce, debt, custody battles. The kind of work that matters.

The courts she worked in were a mess. Unsafe buildings. Overworked staff. Budget cuts so deep that basic safety was gone. Violent people in courtrooms with no security. She even received death threats.

She reported it. Formally. In writing. To the people above her.

Their response was remarkable. They told her the problems she was describing were not really problems. They were just her personal working style. She was then bullied and loaded with extra work for daring to speak up.

So she did what any reasonable person would do. She took the Ministry of Justice @MoJGovUK to an employment tribunal.

Here is where it gets truly absurd.

A judge in England has no whistleblower protection. None. The law that protects workers who speak out about wrongdoing did not cover judges because judges are classified as office-holders, not workers.

The person sitting in court enforcing the law for everyone else had fewer legal rights than almost anyone sitting in front of her.

She lost at tribunal. She lost at the Court of Appeal. She started a crowdfunding campaign just to keep the case alive. Most people would have stopped.

She did not stop.

In October 2019, after seven years, @UKSupremeCourt ruled in her favour. Unanimously. Five judges, zero dissent. The law was rewritten to protect judges who blow the whistle. And the ruling went further, helping workers across the public and private sectors who had been denied the same protection.

One judge. No institutional backing. Fighting the entire Ministry of Justice with a crowdfunding page. She changed the law for everyone.

@guardian @BBCNews @lawgazette @thetimes @UKSupremeCourt - Gilham v Ministry of Justice [2019] UKSC 44

22

356

844

15,435

Frank Square 🇮🇪 retweeted

Jun 11

BREAKING: A Toronto police officer has been murdered after executing a search warrant on an Iran-back Hezbollah Kta’ib cell in Canada.

960

7,259

17,938

413,716

Frank Square 🇮🇪 retweeted

Jun 11

Israel has murdered 3 TIMES MORE Lebanese civilians in the past few weeks than Israelis killed on Oct 7th.

And A HUNDRED times more kids.

Just in Lebanon.

A deranged state armed and funded by the west.

Terrifying evil.

224

3,422

8,502

73,975