Bootstrapping token networks @1kxnetwork

Joined October 2019

- Tweets 1,746

- Following 722

- Followers 3,739

- Likes 5,981

14 Photos and videos

Very timely reminder of the Cost of Trust.

If you haven't read our thesis yet, I suggest you give it a read: 1kx.capital/thesis

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

2

178

Christopher retweeted

Jun 11

The useful version of an AI agent is also the risky one.

It can read private context, take in outside inputs, and act.

In this clip, 1kx Partner @_weidai explains why that combination makes prompt injection much more than a chatbot problem.

More in Cost of Trust 2.0: 1kx.capital/thesis/cost-of-t…

4

2

17

7,774

Jun 10

Our last startup almost got deplatformed by an App Store reviewer on a bad day. We waited two weeks with no path to appeal.

That was my cost-of-trust moment.

Cost of Trust 2.0 thesis live: 1kx.capital/thesis/cost-of-t…

Jun 10

35% of US employment is spent creating trust.

Auditors, notaries, attorneys, courts, custodians, compliance officers. Trust-establishing work is the single largest category in the modern economy.

It is also being repriced.

The repricing started in financial infrastructure. Custody costs heading to zero. Cross-border settlement collapsing from days to seconds. Aave hit $44B in custody at peak (late 2025) at zero fixed cost.

It hit AI a second time. The Hong Kong CFO who got on a Zoom call with deepfakes of his CEO and the board, and wired $20M. AWS outages caused by AI agents managing production clusters without human oversight.

AI is the most powerful trust-eroding technology we have built. Trust intermediaries built on human schedules cannot keep up with fraud produced on machine schedules. The cost of creating fakes goes to zero. The value of verified trust goes up exponentially.

And it is opening categories that were not possible before. Permissionless conversion-based advertising. Hallucination-proof knowledge graphs. Programmable insurance.

Eight years of investing. One argument.

Cost of Trust 2.0, our 2026 thesis. Read it: 1kx.capital/thesis/cost-of-t…

35% stat: "The Cost of Trust: A Pilot Study," SSRN.

Aave peak TVL: DefiLlama.

AWS outages: The Guardian, February 2026.

5

148

The game theory of "exploiting" the Zcash bug is much more complex.

"If the Zcash bug were exploited, we would have seen a large outflow from the Orchard pool."

No, it's not that simple.

A sophisticated hacker would not have just withdrawn from the shielded pool and sold tokens. Why? Because once they are out of the pool, there is basically no way to launder a large sum of money.

The orchard pool itself is actually the best way to launder counterfeit ZEC. The best scenario for a hacker is if (1) they remain the only party with counterfeit ZEC and (2) the Orchard pool remains in operation (not drained), so the hacker can launder the ZEC slowly (say, direct OTC within the Orchard pool over a longer period of time).

Can we rule this out? Yes, this can be ruled out if we ask most ZEC holders in Orchard to withdraw (i.e. drain the pool).

Another angle of attack that could have been executed which is hard to rule out: the hacker could have taken a large but ordinary-looking short position on ZEC after finding the exploit. This strategy is even plausibly deniable--you can reap rewards from knowing about the exploit early with little risk. Since there's a liquid perp market on ZEC, it's possible to "hide" a significant short position (worth millions) without moving markets significantly or leaving suspicious traces.

A sophisticated hacker could have run a combination of the two strategies above.

38

31

217

57,784

Christopher retweeted

Jun 3

Thank you @money2020!

The last 48 hours have been a whirlwind.

We caught up with our partners, made hundreds of new connections, and shared key WalletConnect Pay milestones.

So much more to come.

Jun 3

RIGHT NOW: WalletConnect CEO @Houlgrave takes the stage at @money2020 with our partner @ingenico and @dfnsHQ.

The big question: are stablecoins at the point of sale hype or reality?

The answer is an obvious yes.

The mechanism? WalletConnect Pay.

Global reach through Ingenico.

8

4

51

2,090

There are two distinct quantum x crypto market opportunities.

1. Post-quantum security for digital assets. The goal here is to offer security guarantees for *existing* 2.6T of crypto assets. Yes, one cannot do this without upgrading chains. But you can try to offer as much added security as possible.

2. Quantum-native blockchain. Quantum compute is actually a value-creating technology: NISQs, even with just hundreds of noisy qubits, can be used for optimization problems, and as logical qubits emerge & gate fidelity improves, there is the possibility of quantum one-time programs & quantum cryptography. Even just a PoQW (proof of quantum work) L1 blockchain as the baseline is extremely interesting from a new "post-quantum" non-sovereign SoV asset standpoint.

There have been quite a number of teams building 1 (pq security), but 2 (quantum-native chain) is quite overlooked, and where most of the value creation will happen.

8

2

22

2,861

Christopher retweeted

May 12

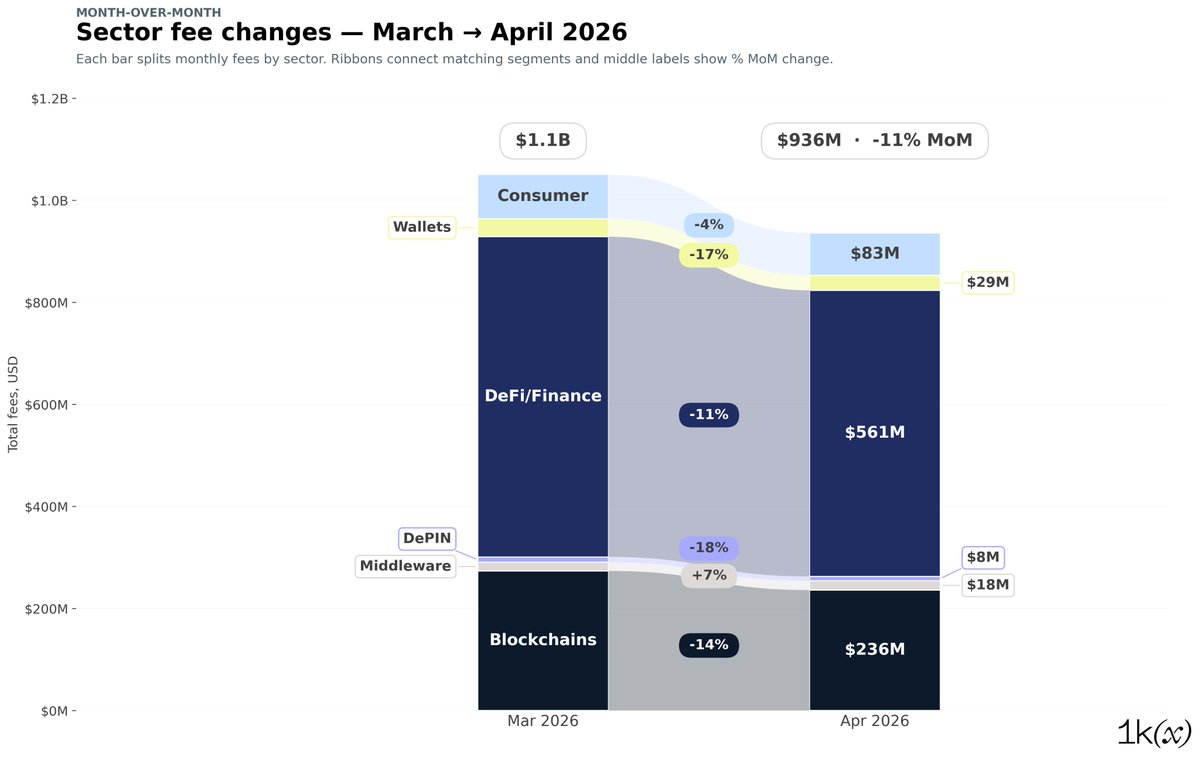

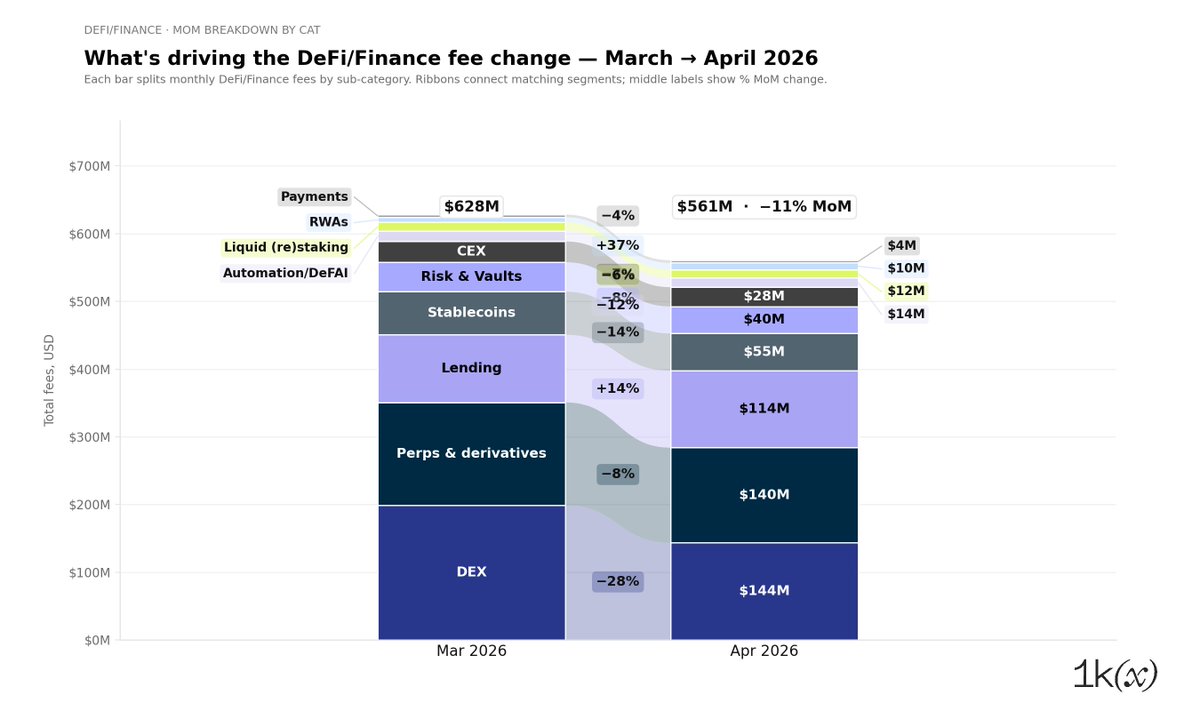

April fee data from the 1kx Onchain Revenue Report (1,000 protocols tracked). Aggregate fees are down (-11% MoM, -20% YoY) as market volatility decreased both vs. March (Iran-uncertainty calming) and vs. last year’s Trump tariff-related moves, causing DEX and MEV-related fees to drive most of the declines.

It's a mixed picture on the category and protocol level, though.

• DeFi/Finance -11% MoM is a mixed bag:

--> Perps lost, e.g. @HyperliquidX -15%, though other markets gained, e.g. @Polymarket >3x in fees (largest gainer overall)

--> Lending markets gained in fees, led by @aave (due to utilization increase - see here: x.com/KoschigRobert/status/2…)

• L1 fee dispersion is widening. @ethereum 2x, @Zcash and @trondao up, while MEV-driven builders like @titanbuilderxyz give back March’s gains. Mostly a vol-compression unwind from March’s Iran-uncertainty spike.

• Middleware 7% growth driven by @chainlink and @CatFeeio

• DePIN 18% Fee decline almost entirely caused by @AethirCloud

• Wallet sector down 17% in fees, mainly due to interfaces like @AxiomExchange (-24%), @tradexyz (-18%). Even @phantom’s fee decline is mostly from their perps-trading interface

• Consumer overall flat-ish -4%, though bifurcation in Launchpads: @fourdotmemezh, @bonkfun, @farcaster_xyz with 50-80% declines in fees vs. @Pumpfun, @BagsApp positive. @printr as a new entrant

So what for 1kx: the decline in trading activity is in line with the compression in market volatility. Continuous growth in emerging DeFi categories like RWA is consistent with our Onchain Finance overweight. Prediction markets entering a fee-generating phase (Polymarket >3x) is consistent with our Frontier Applications thesis. Launchpad bifurcation tells us the consumer category is sorting itself.

Apr 28

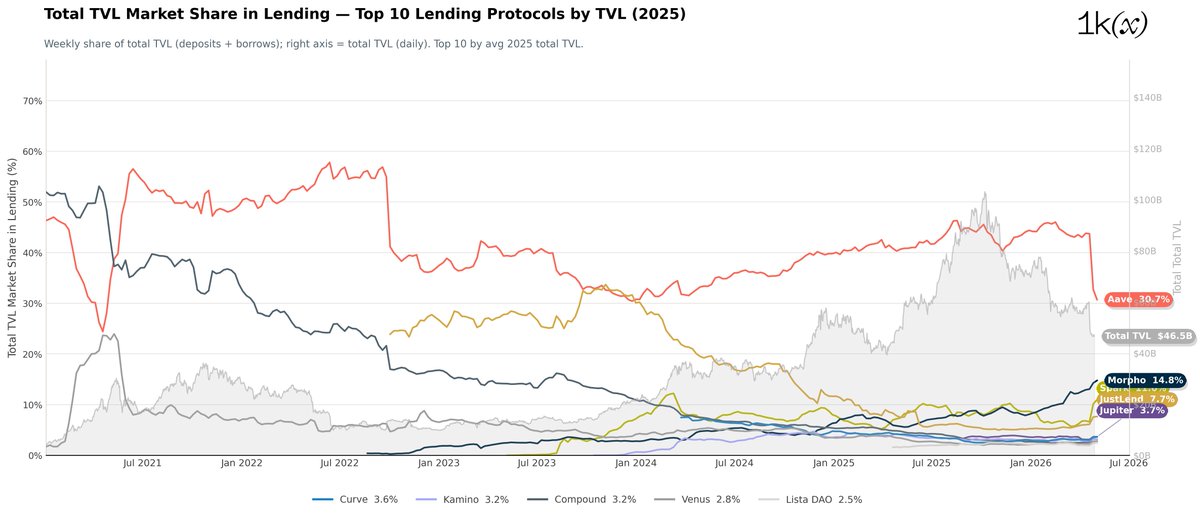

Update on lending markets:

@aave's share of TVL amongst lending protocols drops towards all-time lows, whilst @spark and @Morpho are gaining

8

5

25

5,024

Meet Event Rush, provided by @42space! Opinions are now tokenized.

Buy and sell event tokens on sports, news, crypto, and more.

Changed your opinion? Change the token.

Start now on Binance wallet ⤵️

binance.com/en/support/annou…

153

107

487

140,345

Christopher retweeted

May 18

Looking forward to @CVConf_ discussing the latest on DePIN economics with @Tech_Metrics , @Powerledger_io and @onocoyRTK

See you next week!

2

8

253

Osero has raised $13.5M, led by @SkyEcosystem and @Plasma.

We're building the savings account for where your stablecoins already are.

303

82

696

227,947

Christopher retweeted

May 8

Last week, 1kx Founding Partner @lalleclausen joined the "In Stablecoin We Trust: The Future of the Dollar" roundtable at the @MilkenInstitute Global Conference. A few takeaways.

Stablecoin payment volume (excluding bot activity) averaged $49B per day in Q1 2026, up 110% year over year and compounding at 50% CAGR over the past five years. That puts daily stablecoin payments above Visa (~$44B) and Mastercard (~$30B). Supply outstanding crossed $273B by quarter-end, up 28% YoY.

The growth is structural, not cyclical. Stablecoins are lower-friction payment rails picking up where the decline in correspondent banking has left off, and they offer better payment experiences for companies and individuals than the existing system delivers.

One of the most interesting threads of the discussion was about trust. The trust that US institutions and the dollar generate is, in effect, expressed through market adoption of USD-backed stablecoins worldwide. It is very hard for any other country, currency, or political system to replicate that. Whether a jurisdiction can produce a stablecoin that earns free-market adoption is becoming a useful signal of institutional credibility.

The build-out is happening in two layers. First, companies that handle the friction of integrating stablecoins into existing payment flows and treasury operations. Second, new banks being built that will flatten that friction into everyday treasury and payment work. Both layers are where we have spent the past several years deploying.

The closing analogy stayed with us. Stablecoins are to blockchains what email was to the early internet. Email was foundational, but it was never the point. Today, stablecoins are how we send a digital dollar back and forth. Blockchains will enable programmatic trading, clearing, and settlement of every existing financial instrument, plus financial primitives that weren't possible before.

Payments first. The rest is coming.

#MIGLOBAL

6

3

28

5,441

May 4

Speedrunning on becoming irrelevant

The European Commission literally just dropped a research on how to collect more taxes without making you angry enough to leave.

TLDR: higher wealth taxes, inheritance taxes exit tax is coming

1

3

172

Christopher retweeted

Apr 30

1kx will be at the @MilkenInstitute Global Conference in Los Angeles, May 3 to 6, where @lalleclausen joins the roundtable "In Stablecoin We Trust: The Future of the Dollar."

Milken brings together the CIOs, allocators, bank and asset-manager leadership, policymakers, and market infrastructure builders shaping the next decade of capital markets. This year, stablecoins and tokenized cash have moved from side panels into the core agenda: treasury, settlements, collateral, and liquidity.

We published our Cost of Trust thesis in 2019, arguing that blockchain reduces the cost of establishing trust to near-zero. What we're seeing now is institutions actually paying for that trust reduction at scale, in stablecoins, tokenized cash, and the settlement infrastructure underneath them. That these questions sit at the core of Milken's agenda rather than its periphery shows how concrete the shift has become.

The winners will be the structures institutions can actually hold, regulate, and plug into existing workflows. If you'll be at Milken and are thinking through what onchain finance means for your role as an allocator, issuer, or operator, our team would be glad to connect while in LA.

milkeninstitute.org/content-…

#MIGLOBAL

2

1

12

1,911

Christopher retweeted

Apr 22

The stablecoin market has 200 issuers. Most won't survive contact with institutional capital. A few are already building for it.

At the 2026 @rwasummit in Cannes, our Founding Partner @HeyChristopher moderated Stablecoin Wars: What Structure Will Win with @peterlih (@AllUnityStable), @Benjamin918_ (@CapApp), and @MartindRijke (@maplefinance).

Three builders, three fundamentally different architectural bets:

→ AllUnity is issuing MiCA-regulated euro and CHF stablecoins under a BaFin e-money license, 100% backed, legally redeemable, and designed for businesses outside the crypto ecosystem

→ Cap is targeting pension fund capital directly, arguing smart contracts can allocate credit more efficiently than human-led underwriting, at structurally lower cost

→ Maple has shifted its primary KPI from AUM to ARR, betting that fee income matters more than scale

Our read: yield efficiency and credit automation only matter if institutions can legally hold the underlying asset. Regulatory structure solves for that first.

The stablecoins that matter will be the ones connected to the productive economy. The rest will remain infrastructure for crypto, not for capital markets.

Full panel below.

youtube.com/watch?v=ZBcOMh4P…

3

6

34

11,952

A highlight of @1kxnetwork investments within our thesis on threat-resistant & compliant onchain privacy.

- @0xMiden: chain designed from the ground up for programmable privacy (ZK)

- @zksync: private & customizable prividiums (ZK)

- @inconetwork: user-friendly privacy layer for existing chains (TEEs)

- @SeismicSys: privacy-enabled EVM-based fintech L1 (TEEs)

- @ligero_inc: private account layer for all chains, custom-built for businesses (ZK)

- @0xPredicate: programmable policy infra, for privacy protocols, defi, & beyond

- @fiber_evm: private EVM wallet infra w/ a slick mobile app (ZK)

Here's the exciting bit: (at least) five of the above projects are about to go live this year!

2026 is the year for onchain privacy.

-----

At 1kx, we put our money where our mouth is.

We develop theses and partner with the best founders to realize the shared vision.

Onchain finance needs threat-resistant privacy

→ Real-world & institutional finance cannot move onchain without privacy

→ To prevent misuse (e.g. laundering of hacked funds), the only viable solution is to build threat-resistant privacy

More in my op-ed in Forbes 👇

13

23

131

22,341

Onchain finance needs threat-resistant privacy

→ Real-world & institutional finance cannot move onchain without privacy

→ To prevent misuse (e.g. laundering of hacked funds), the only viable solution is to build threat-resistant privacy

More in my op-ed in Forbes 👇

7

12

76

40,424

Christopher retweeted

EBC12 Speaker: Christopher Heymann (@heyochristopher) | Founding Partner | @1kxnetwork

Before venture capital, Christopher Heymann spent years building technology companies as a CTO. He co-founded 1kx in 2018, building it into one of the most active early-stage token funds in the market, backed by sovereign wealth funds, pension funds, endowments, and family offices.

The firm has backed over 150 projects across cryptoeconomic design, governance, and decentralized infrastructure. 1kx does not just provide capital, it embeds itself in the technical and strategic challenges founders face.

Join the leaders shaping digital assets in Barcelona on September 16-17: eblockchainconvention.com/eu…

4

12

660

Christopher retweeted

Apr 7

Proud for @1kxnetwork to lead the pre-seed for @justinmujin to build @giggles_app, a new social network that explores the intersection between video discovery and financialization.

I first discovered Giggles organically on TikTok and immediately reached out to see how well Justin had already grasped the core affordances of crypto in reshaping relationships and communities with financialization.

We spent a lot of time over several months building a relationship and concluded that we should work together.

Today, I'm proud to share our partnership publicly and am incredibly excited to watch them execute in the near term with their launch.

Apr 7

A teenage Minecraft YouTuber raised $1,234,567 for a meme prediction market called Giggles. It broke me. techcrunch.com/2026/04/07/a-…

18

8

112

17,657

Christopher retweeted

Apr 7

We’re excited to share that 1kx led the pre-seed in @giggles_app - a new kind of social network where users can buy into videos early and participate in the upside as they spread.

We think Giggles opens up a compelling new design space at the intersection of social behavior, market design, and crypto-native coordination.

Congrats to @justinmujin, @itsedwinwang, and the whole team.

Big thanks to @TechCrunch and @asilbwrites for the exclusive: techcrunch.com/2026/04/07/a-…

13

13

120

20,767