Founder & CEO of Casper Studios: An AI Services Firm, Ex -LinkedIn BD

Joined January 2020

- Tweets 1,255

- Following 1,507

- Followers 791

- Likes 14,716

124 Photos and videos

Pinned Tweet

17 Apr 2025

Thanks for having me on the pod @nathanbarry!!

17 Apr 2025

Today on the podcast, I talk with Jay Singh about how creators can thrive in the age of AI.

You’ll learn about:

- AI tools that will save you hours today

- How to build systems that leverage your expertise

- Frameworks for turning your data into valuable automated outputs

@JSingh_08

1

1,271

jaysingh retweeted

Best way to understand what's happening in software is to understand what happened in media.

With internet & platforms, the cost of creation went to zero. Supply skyrocketed.

Consumers had more choice than ever before, which created a long-tail of niches, introduced a new standard for "good", and made trusted distribution the most valuable currency.

54

64

517

126,287

Jun 6

Casper Studios has been named a Select Service Partner in the @AnthropicAI Partner Program! Our team is now certified to deliver Claude for customers. This is a huge milestone for the team!!

What does this mean?

1.) First, our whole team is "Claude certified". We've spent the past few months attending virtual and in person training to get up to speed on all things Claude. This is a whole new service area. How do you set up Claude? How do you think about Skills? What about how to drive usage of those skills. Lots of great content that the team shared with us to get up to speed.

2.) Second, we have an amazing team to work with on the Anthropic side. Our POCs have been Jeremy Maranitch and Apricot Tang, who have been awesome about sharing best practices, ecosystem insights, etc.

3.) We can bring their team in to support our clients and they can bring us into their clients to help implement Claude (change management, governance, and more).

We're very bullish on this ecosystem. Super excited about what is next :)

77

May 25

Had a SVP of a $300m PE backed port co say last week "we're thinking of buying Claude/Codex, but don't want to until we have the right partner to help implement". Think we'll see more of this.

Just because you bought Claude doesn't mean your team will use it. Enterprise Claude (or Codex) is just the starting point. To get value, companies need training, education, and concrete examples of how AI changes the way people do their jobs.

Without that the rollout becomes another tool launch: power users get ahead, skeptics don't care, and leadership has no visibility into what's happening across the company.

We're finding a growing niche of our work is helping companies make better use of the enterprise Claude subscriptions they bought, or are thinking of buying. LMK if you need help :)

54

May 14

Hearing the same

47

May 14

Had a mid-cap fund ask me: "If we introduced you to 100 portfolio companies tomorrow, how would you handle it?"

After I stopped sweating and took a few deep breaths, here's what one part of what I shared (can’t share all the secrets yet haha):

Do what Aaron is saying. Start educating and training at the undergrad and grad level on these skills. The jobs are going to be plentiful over the next few years. I'd also partner directly with governments (especially outside the US) to help them train their people to do this work too. Then work with companies to hire those folks. The appetite to train their people, especially with the jobs in the country that may be disrupted with AI (eg call centers, BPOs, etc), is high.

We're already in conversations with a few government bodies globally on this, particularly in places where we already have strong base of talent.

The value exchange is: we help you figure out what to train your people on, and a portion of those people we can help match to the right jobs - whether with us or with other firms scaling their hiring.

Talent is the bottle neck right now. Ironic since the narrative is that the jobs are all going away. At least right now some may be but others are growing a lot.

May 14

If I were a college career counselor or in career services, I’d quickly be figuring out how to get students to understand these forward deployed engineer jobs exist and how to get them.

The requirements are a mix of deep technical skills, often CS majors or minors. You must be great at understanding problem solving, how to have systems thinking, and have a strong business acumen. The kicker, of course, is to make sure you’re very deep in AI agents; you need to have fluency in coding agents, MCP, CLIs, Skills, and so on.

Hundreds (thousands?) of technology companies will be hiring for these roles, same with any consulting and IT services company, and the vast major of mid-size and large enterprises will be hiring for this talent internally as well.

One great example of opportunity for highly technical talent out there.

64

May 12

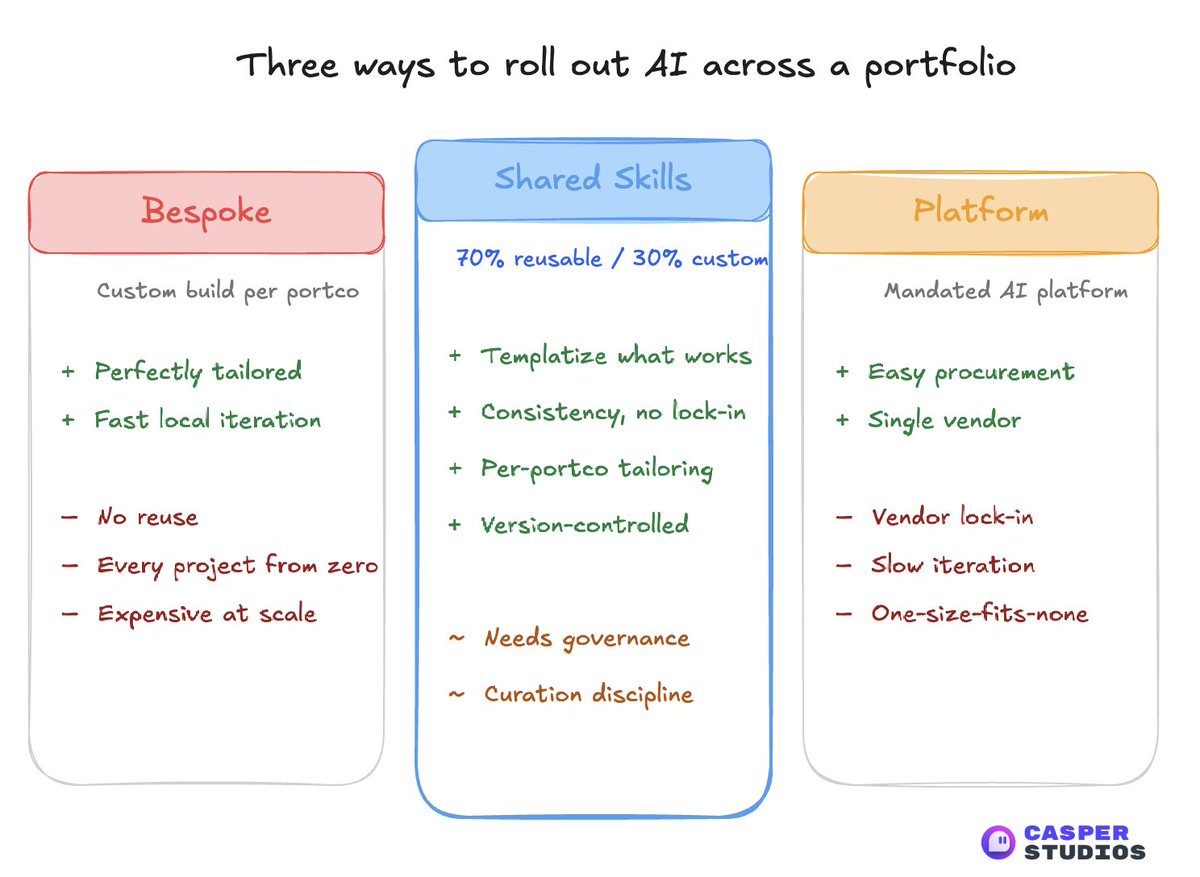

Over the past few months, I’ve spoken with 5 PE funds and their operating partners. One recommendation keeps coming up: build a shared library of AI skills that can be deployed across the portfolio.

Most services portcos need SOW generation. Finance teams need AP invoice automation and data agents that can run SQL on internal databases. Engineering teams need security agents that can review code before release. Every company is unique, yes, but their problems may not be.

The playbook is: implement agents at one portfolio company, learn from it, then templatize it and roll it out across similar companies. The goal is a skill that is 70% reusable and 30% customizable.

That creates a middle ground between “rolling out a platform” and doing everything bespoke. If you try to push an AI platform across the portfolio the way firms have done with Salesforce in the past, I don’t think that’s the right move.

You want the benefits of a platform: consistency, templates, and easier implementation, without the lock-in: slower iteration, less tailored products, and too much dependence on one system.

Right now, I think skill files and workflows that live in an independent repo, like GitHub, are the best way to do that. They give you the repeatability of a platform without forcing every company into the same rigid software product.

This is still early. Most funds haven’t operationalized it yet, and many portfolio companies are still behind on AI implementation. DM me if you want to chat about what else we're learning.

1

1

48

May 1

Private Equity and AI implementation is having a moment right now. Both OpenAI and Anthropic are pushing hard to partner with PE firms to deploy their models into portfolio companies and drive enterprise AI adoption. OpenAI is in advanced talks with Advent, Bain Capital, Brookfield, and TPG on a JV; Anthropic is running a parallel play with Blackstone, Permira, and Hellman & Friedman.

Both are modeled on Palantir's forward-deployed playbook — teams embedded in portfolio companies. Those are hundreds if not thousands companies in scope. Both labs are pushing hard because they're each targeting IPOs this year. Nailing this story matters for investors.

We've been getting connected to these firms over the past few quarters. We've been building the relationships for a while but most funds were still exploring slowly. It's all coming to a head now: they're finally ready to connect us to their portfolio companies, and I think the OpenAI/Anthropic partnership moves are a big part of why.

We're hiring across:

-Strategy folks to do discovery work up front

-PMs to implement AI across portfolio companies

-BD / Sales folks to help me manage relationships and find value across the portfolio

If you have any interest in deploying AI into PE, now is the time to jump in. Let me know if you want to go after this together.

1

75

Apr 23

Was talking with a friend at a large VC fund a customer at another an asset manager today. Went into the Thoma Bravo and Medallia news from yesterday. Sharing notes / the "so what" below.

TL;DR

-Thoma Bravo handed Medallia to its lenders. $5.1B of equity, gone.

-Thoma Bravo bought Medallia in 2021 for $6.4B. About $3.4B of equity, $3B of debt. Five years later the company couldn't service its debt. Lenders (Blackstone, KKR, Apollo, Antares) took the company in a "debt-for-equity" swap. Thoma Bravo's equity went to zero.

Three things broke at once

1.) Rates. Medallia's debt was "floating rate". In 2021 the all-in rate was around 4.5%. Interest expense was $135M a year. As rates rose, that bill more than doubled to $278M. An extra $143M each year w/o that big of a change in revenue.

2.) Multiples. Software businesses like Medallia traded at 15-20x EBITDA in 2021. Today they trade at 8-12x (maybe even less). Even with flat EBITDA, enterprise value compresses 30-40% from multiple contraction alone.

3.) AI. Medallia's core offering is customer experience. Collect survey and feedback data across every touchpoint (web, call center, email, in-store), run text analytics on the unstructured stuff, build dashboards for ops and CX leaders, feed it back into workflows. That used to be a moat. You needed the survey infrastructure, the NLP models, the integrations, the enterprise sales motion. Hard to replicate. AI-native versions do most of this better. An agent can read every call transcript, every support ticket, every review, every chat in real time. No traditional survey needed.

Any one of these alone may have been okay. Together they create the zero.

The more interesting point from PE land.

PE firms can't control rates. They can't control multiples. The only variable they control is EBITDA. And in a world where AI is both the biggest threat to SaaS moats and the biggest lever for EBITDA improvement, the firms that figure out AI inside their portfolios will have very different outcomes than the firms that don't.

How we're thinking about it at Casper Studios is shifting too. I'm for sure biased but I see this as a tailwind for the business.

We're working with a few large-cap PE portfolio companies right now. The work is interesting and intense (!). There's a ton of pressure to drive EBITDA improvement fast, to get to a better multiple and a better story. Some are moving fast. Some aren't. It's been fascinating to be in the middle of it.

I can't share much more than that, but this is the most top-of-mind conversation I'm having right now. A few months ago I wouldn't have said you're late. Today, at a minimum, this should be a topic in every exec meeting.

The next few years of PE (and funds, and private credit) are going to be interesting. DM me if I can share any insights we're picking up in the space.

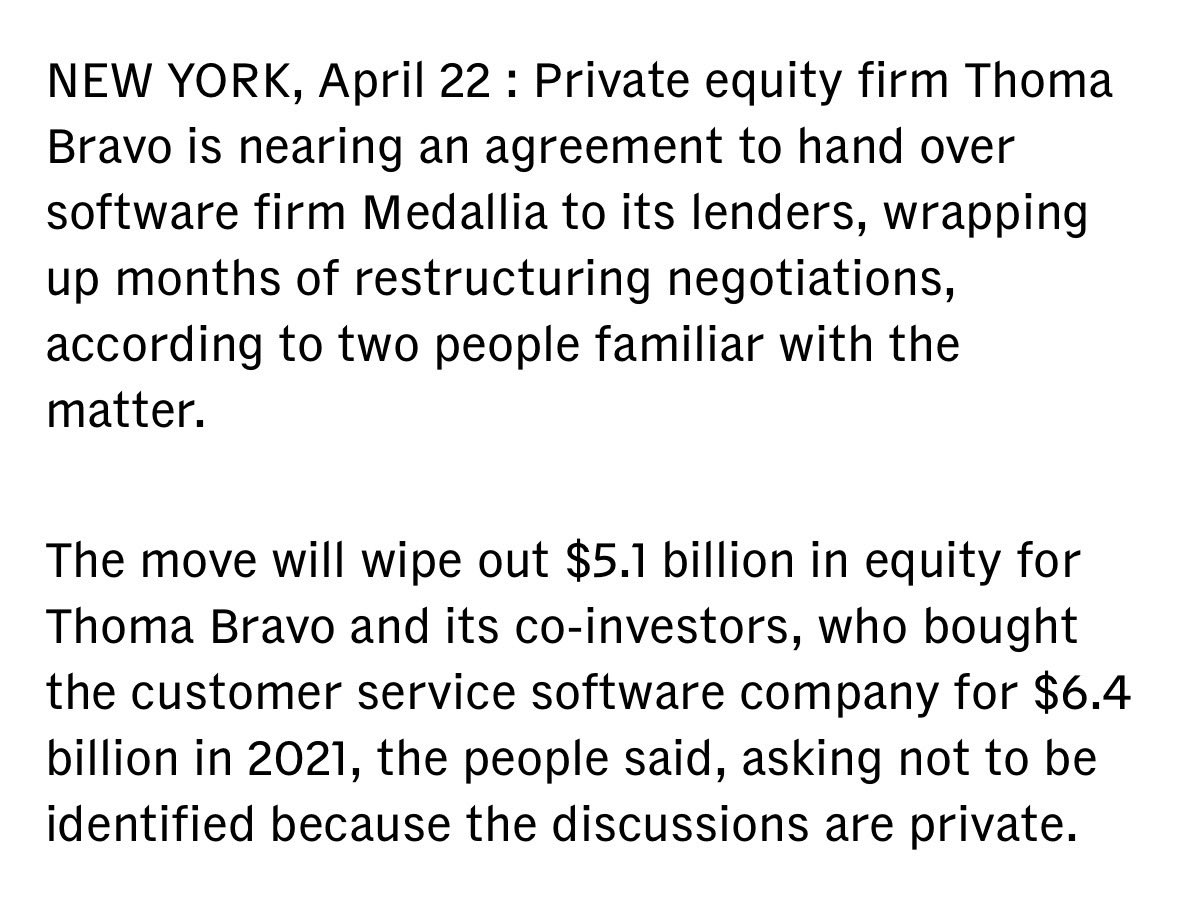

Apr 22

Thoma Bravo is reportedly handing over the software company Medallia to creditors after restructuring negotiations failed to materialize

This is a $5.1 billion equity wipe out for the firm, who bought the business for $6.4 billion in 2021

Largest creditors include Blackstone, KKR, Apollo, Antares and Ares

This loan was last marked anywhere between 70c to 100c on the dollar, according to most recent BDC filings from them

2

221

Apr 21

"There's a limit to the number of software you need to build that looks like an app on your phone; there's an unlimited amount of software you need to build that looks like a background system process that's connecting different data sources, automating workflows. That's where the work is going to go." - @levie

We've shifted from using our coding agents to build software to mostly using them to build other agents. Claude has made this easier, and form factors like MD files and skills have accelerated it.

I don't think the total number of web and mobile apps necessarily declines - it likely keeps growing. But the relative growth of agents embedded in internal workflows will probably be something like 10x what we have today, simply because building them has become much easier.

Apps aren't going away; they'll just look small, relative to the internal agent market forming around them.

33

Apr 17

sometimes the contract also has a 30 day terms of convenience too 😂

Apr 17

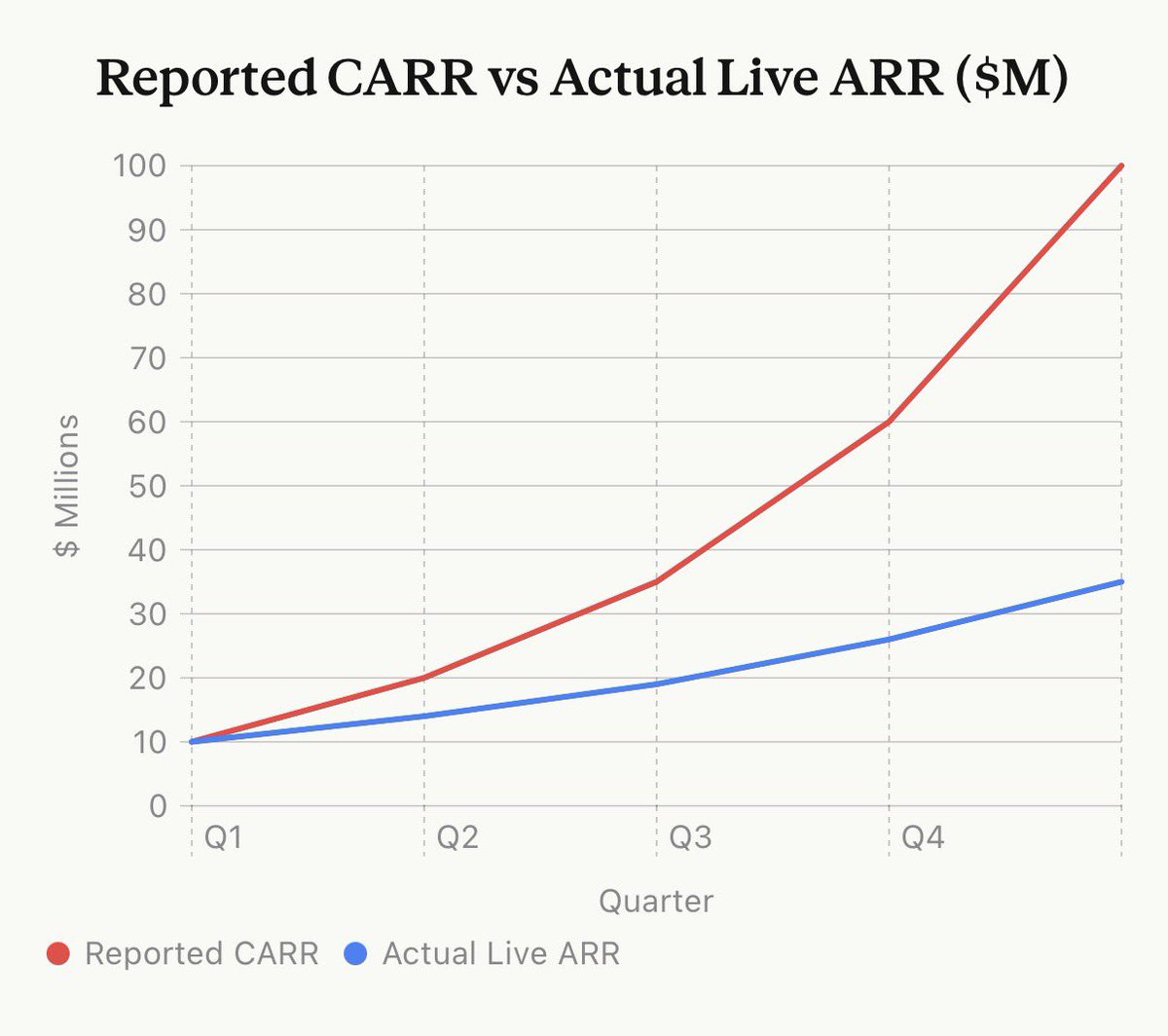

It’s time to expose a huge scam in AI startups: Contracted ARR

The reason many AI startups are crushing revenue records is because they are using a dishonest metric

The biggest funds in the world are supporting this and misleading journalists for PR coverage.

The setup: Company signs 3-year enterprise deals. Year 1 is discounted (say $1M), Year 2 steps up ($2M), Year 3 is full price ($3M).

They report $3M as “ARR” — even though they’re only collecting $1M right now.

The worst part: The customer has an opt-out option at 12 months! It’s not actually a 3 year contract.

In the chart below, by Q5 the company is trumpeting ~$100M “ARR” to press, while actual cash-generating, in-effect ARR is ~$35M. That’s ~3x inflation.

On top of this, enterprise AI companies are bundling full-time “forward deployed engineers” into deals massively reducing margins, sometimes producing Year 1 negative margins.

At some point customers are going to start triggering their opt-out clauses or aggressively negotiating down Year 3 pricing.

And a wave of enterprise AI companies may collapse.

1

82

Apr 12

Have you noticed the paradox in the job market? Every good company in AI is complaining about not finding enough people to service demand. On the other side, tech companies are laying off thousands. What’s going on?

The people are there to help implement AI. The system to train them doesn’t exist yet.

There are experienced professionals across every industry whose roles are shrinking. Not because they lack talent, it’s because the work itself is changing faster than anyone can redeploy them.

At the same time every company we talk to is desperate for people who can implement AI. Demand is so far ahead of supply that clients are getting back-ordered; especially for AI services firms like us.

But I think gap between these two groups is way smaller than people think.

Someone who’s sharp, moves fast, open minded and knows how to figure things out in ambiguous environments, that person can be deploying AI in weeks/months if you put them in the right system.

They just need to be shown the way.

And honestly? That’s a skill issue on us. The companies building in AI. We’re the ones posting JDs asking for years of experience in Claude Code even though that barely existed a year ago LOL.

The companies that can hire top talent, equip them on how to use AI, then deploy them to companies who need AI, will be massive companies.

41

Apr 2

We’re almost 30 people now. I find myself stepping back a lot just observing the quality of talent we’ve built at Casper. I joke that I probably wouldn’t even get hired here anymore lol. Entrepreneurship is a vehicle for incredible experiences. Building a team has been the most rewarding part so far.

1

2

65

Apr 1

building of these if you wanna jam @thesamparr :)

Apr 1

The agency business model just got really interesting.

Shaan and I were talking about this thesis called "service as a software" on MFM.

I always thought running an agency was a huge pain in the ass.

But AI flips the math.

The old model requires an army of humans to get things done, which meant low margins and low multiples.

So you replace the human labor with AI, where one person can do the work of seven.

At the same time, private equity firms are shifting their budgets away from SaaS to buy up these new service companies.

A traditional agency that might run on 40% gross margins, is now an AI service biz that hits 75% and gets tech multiples.

Wild shift.

66

For agentic systems founders and dev tools founders:

People do not want to pay for raw markdown and they shouldn't have to.

But they may pay for orchestration, hosting, updates, collaboration, portability, analytics, and managed execution.

These can be great businesses.

286

142

2,498

175,434

Mar 12

Hi @AnthropicAI team - Jay here from of Casper Studios. Consider this my not-so-subtle application to become one of your partners.

Who are we?

Casper Studios is a ~25-person AI services firm. Our core team blends product, strategy, and engineering experience from top-tier consulting firms and industry-leading technology companies including LinkedIn, PwC Strategy&, Amazon, Accenture, Bain, and Elliott Management

Who we work with:

-Hedge funds managing $2B in AUM

-A $10B ARR revenue healthcare provider

-Financial services firms with $20B AUM

-Oh and Netflix, where we helped ship what became the second-largest voice AI activation to date with 400k calls

So what:

We’re growing 25% month over month with a team of technical leads and product strategists focused on implementation. And across almost every enterprise client we work with, we’re already recommending and deploying Anthropic and Claude. So in many ways this partnership is already happening :)

DM me - let us support! Also for friends reading this if you know anyone at Anthropic comment them below hehe

1

94

Mar 8

Preach - @nathanbarry is a huge inspo. Not included below is how kind he is!

Mar 7

I think @nathanbarry is an entrepreneur everyone should look up to.

- $50m plus ARR bootstrapped business

- awesome family

- does things his way

I’ve known him since 2012. He’s this way for over ten years.

1

44

Mar 6

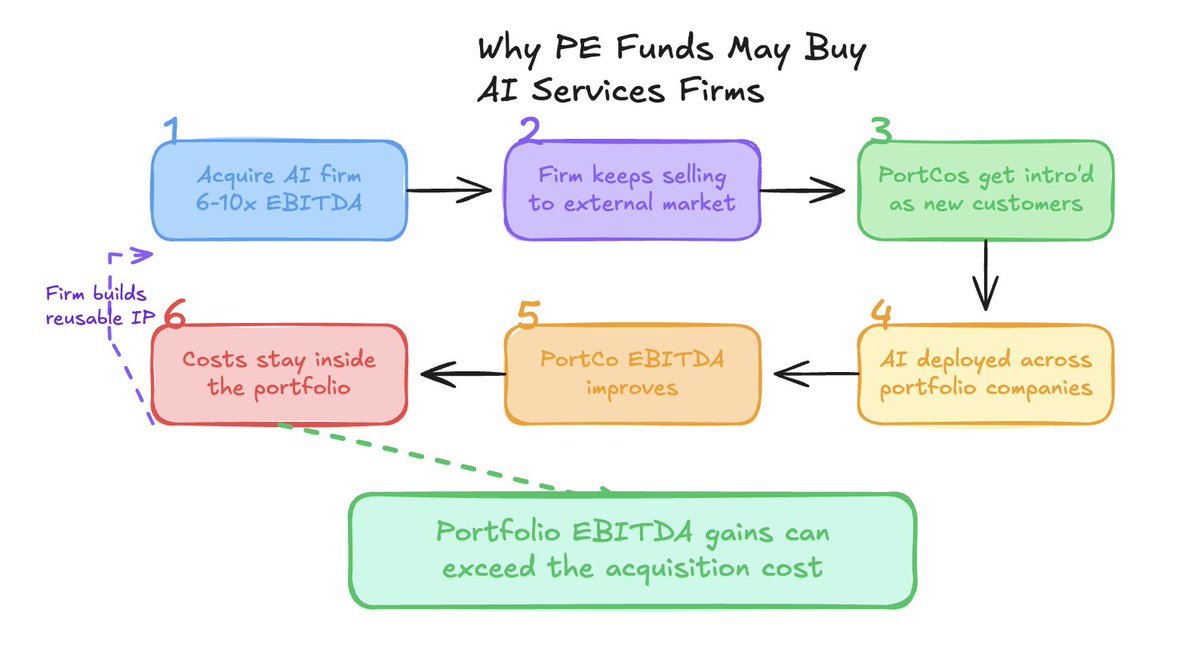

Chatted with 5 PE funds this week. I think some of them that want AI implemented across their fund/portfolios may decide it’s easier to buy that business rather than hire it repeatedly. Let me explain...

Right now it still feels early. Most funds are exploring. Portfolio companies have bought tools, but very little has actually been implemented across the organization. Those I’m speaking with all seem slightly unclear where to begin, what to prioritize, which portfolio companies to focus on first, and what the right timeline for implementation should be.

We're starting to partner with many of these funds to help them to answer these questions.

Here's a scenario that came to mind...

Imagine acquiring an AI services firm at 6–10× EBITDA. The firm keeps operating normally, selling to external clients and growing through its own GTM channels.

But the PE fund now has access to implementation capacity. When portfolio companies start AI projects, the firm gets introduced as a potential partner.

Even if only a few portfolio companies become customers, it creates a baseline layer of demand while the firm continues to grow independently in the market. The costs that would otherwise leave the portfolio would be retained.

If AI deployment improves EBITDA across even a few portfolio companies, the return on the acquisition can exceed the purchase price of the services firm itself.

When we worked on the Netflix project with Omnicom, they were thinking about it the same way. Omnicom had previously acquired a technology agency to build internal capacity for technical development, so they could support more complex builds directly for their clients.

From the fund’s perspective, the acquisition becomes two things at once:

1.) an operating capability that can help portfolio companies (and the fund) move faster on AI

2.) a standalone services business that continues compounding

Whether this becomes a common strategy, still unclear. I'm also honestly learning more about this space myself. Challenge my POV pls!

What do you think?

72

Mar 6

one is too light

Mar 5

Within a year, every company over 50 people will have at least one person whose full-time job is building internal agents.

51

Mar 5

You've bought a bajillion AI tools. Some work. Most don't work well together. Now you're sitting on a stack of point solutions. Each solves one narrow problem but creates a new coordination problem every time you add another.

The next few months? Consolidation. Right now, all roads lead to Claude (Chat, Cowork, Code).

Let me explain.

Product designers have this concept called the Double Diamond. Start at a single point. Expand outward, explore the full problem space. Converge back to a focused insight. Expand again into solutions. Converge on the real answer. It's a framework for how complexity works - you start simple, things get messy, then they consolidate. Over and over.

Platforms follow the same pattern. Craigslist had everything in one place. Jobs, apartments, dating, rides, furniture. All on one ugly beautiful website. Then each category unbundled into its own billion-dollar company. Airbnb took rentals. Uber took rides. Tinder took dating. LinkedIn took jobs. One platform became dozens of specialized ones. That's the first expansion. Over time, those companies get huge and split apart again.

AI is in the same motion.

Two years ago every company started at the same point: "I need AI." That turned into a spending spree. A writing tool here. A coding copilot there. Legal AI. Sales chatbots. Meeting summarizers. Healthcare AI. Fraud detection. Supply chain optimization. Image generation. Customer service automation.

Workflow tools. So many tools.

That's where we've been. The widest point of the diamond.

Now the conversation is shifting. Especially with F100s. They don't need more tools. They need help converging. Redesigning systems. Taking those early bets and building an ecosystem that actually works together.

Where it goes after that is the next diamond. Nobody knows how wide it opens.

But sitting across 20 engagements right now, the pattern is clear: the value isn't the tool anymore. It's how the system is designed. That's why we don't care which AI tool you use. We care about designing the system that makes it all work.

This is where the work lives for the next 12 months. It's hard. It's change management. It requires hand-holding, time in person, trusted relationships.

We're here for all of it.

31