Joined December 2020

- Tweets 10,874

- Following 1,555

- Followers 1,108

- Likes 24,668

132 Photos and videos

Jacob Bigelo retweeted

Jun 8

🚨🇫🇷📺 FLASH

SÉQUENCE CHOC !

Affaire Lyhanna : Un père de famille INTERPELLE VIVEMENT Gérald Darmanin et FUSTIGE Emmanuel Macron en direct à la télévision 🤯 :

« Je paie des impôts et, en fait, vous faites quoi avec ?! Je vous ai écoutés parler, vous me dites : "la 7e puissance mondiale". J’EN AI RIEN À FOUTRE ! Demain, ça arrive à ma fille, je le traque, et je vous traque tous ! Je règle le problème moi-même ! Vous avez la trouille de faire un référendum concernant la peine de mort. On ne touche pas aux enfants. Je ne sais pas dans quelle langue il faut que vous compreniez ces choses-là.

Il a fallu ça (la mort de Lyhanna) pour que ça provoque un sursaut ! Mais jusqu’à quand ? Il va y en avoir d’autres puisqu’on a des pédocriminels dehors, dans la nature, et ça ne choque personne, y compris votre patron en premier [Emmanuel Macron]. Il préfère faire une photo avec les joueurs de l’équipe de France alors que ça vient d’arriver au même moment [l’affaire Lyhanna].

Vous avez un comportement qui me donne envie de gerber ! Regardez l’état de la France : dehors, c’est le zoo, c’est le Far West et il ne se passe rien ! Qui juge l’incompétence des magistrats et des juges ? Qui ? »

(BFM TV)

648

8,194

34,435

1,678,317

Jacob Bigelo retweeted

Jun 5

Sigh.

I keep telling retail Swedish Hedge Funds how important $SIVE is to CPO, but people don’t listen.

Enough retail holders got shaken off, and

now JP Morgan managed to buy up a massive stake in Sivers (purely institutional).

JP Morgan went from .4% ownership last month to 5% ownership this month…

May 9

The US/West now controls majority of the shares of $SIVE.

With Goldman Sachs/JP Morgan/Morgan Stanley and other US institutions entering.

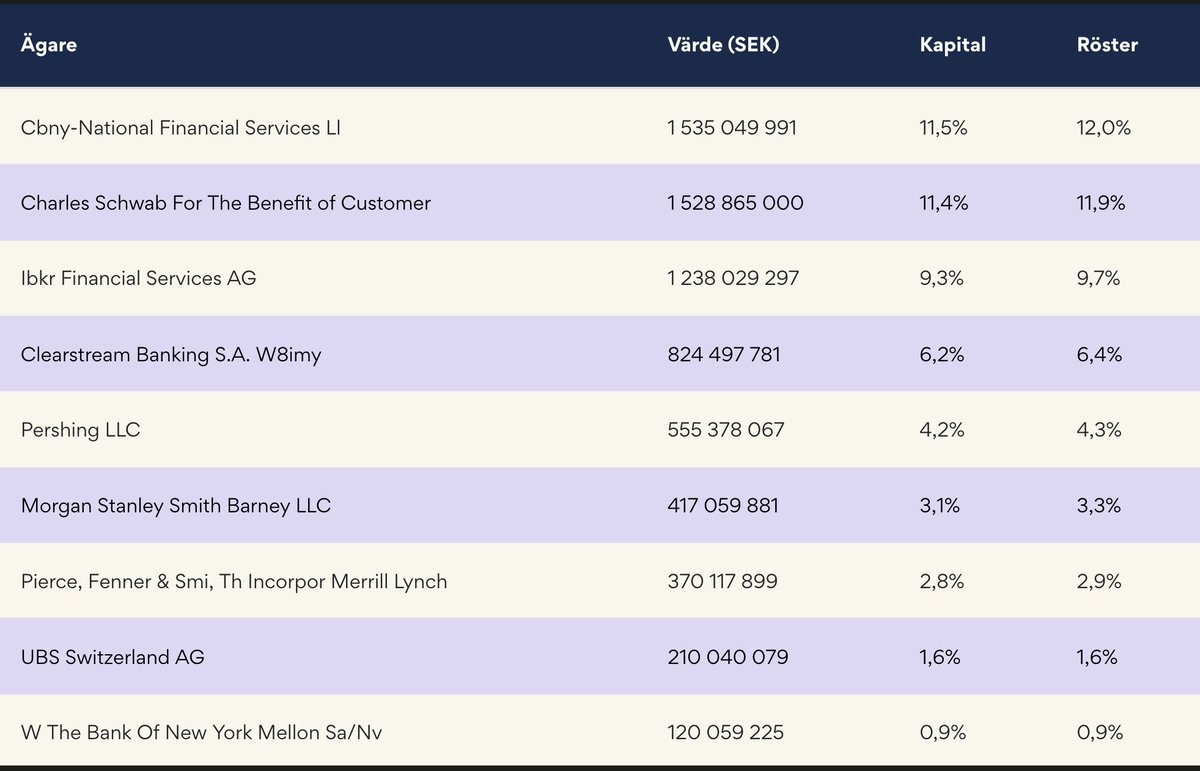

US/West 46.8%:

- Fidelity: 11.5% (retail)

- Charles Schawb: 11.4% (retail)

- $IBKR: 9.3% (primarily retail)

- BNY Mellon: 4.2% (retail)

- Morgan Stanley Smith Barney: 3.1% (Retail/Wealth management)

-Bank of America: 2.8% (retail/Wealth management)

- BNY Mellon: .9% (institutional)

- Morgan Stanley Client Assets: .7% (institutional)

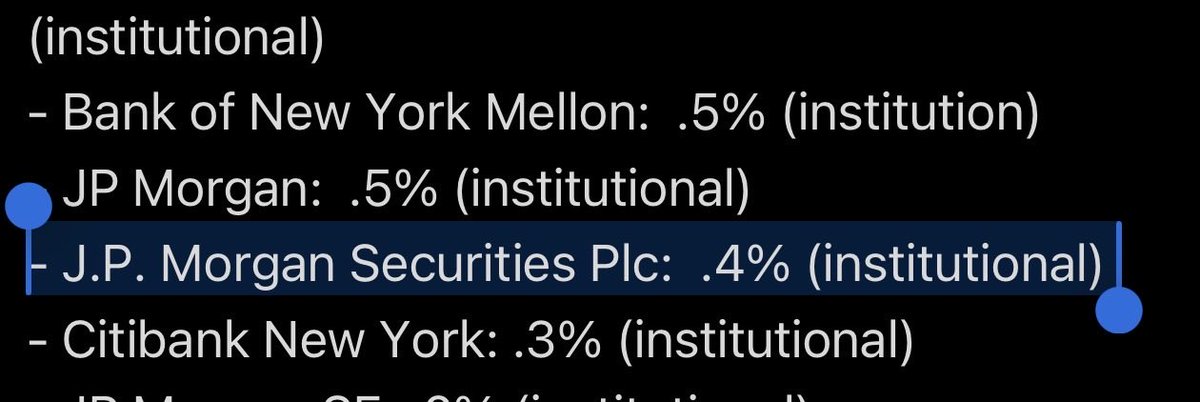

- Bank of New York Mellon: .5% (institution)

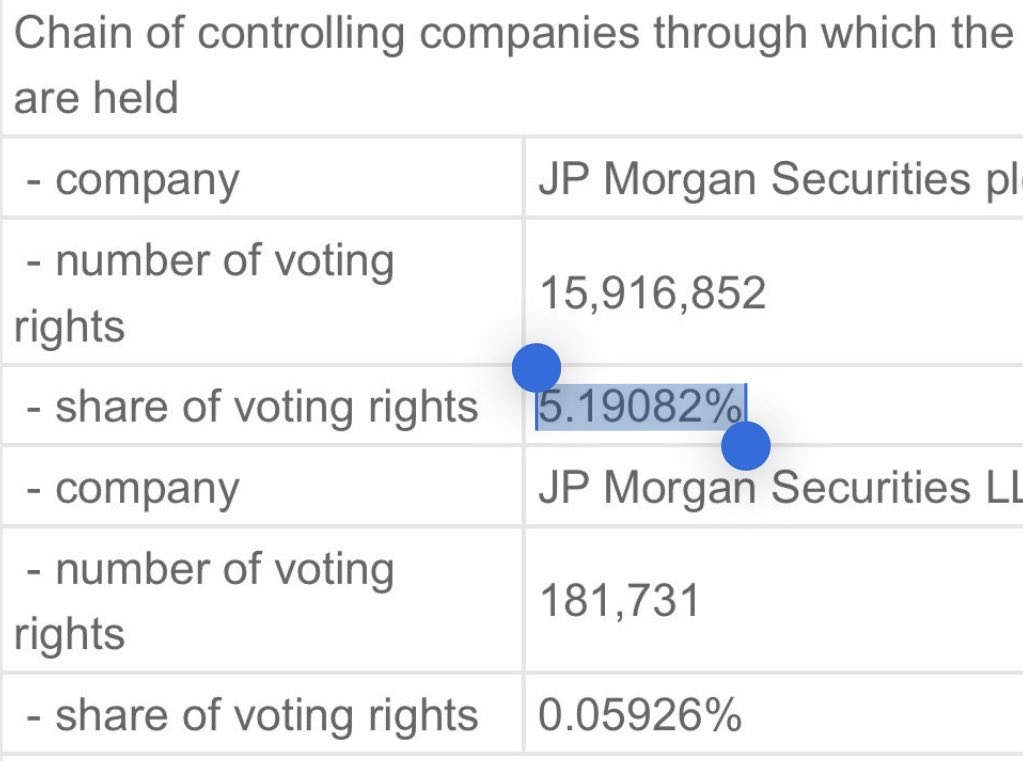

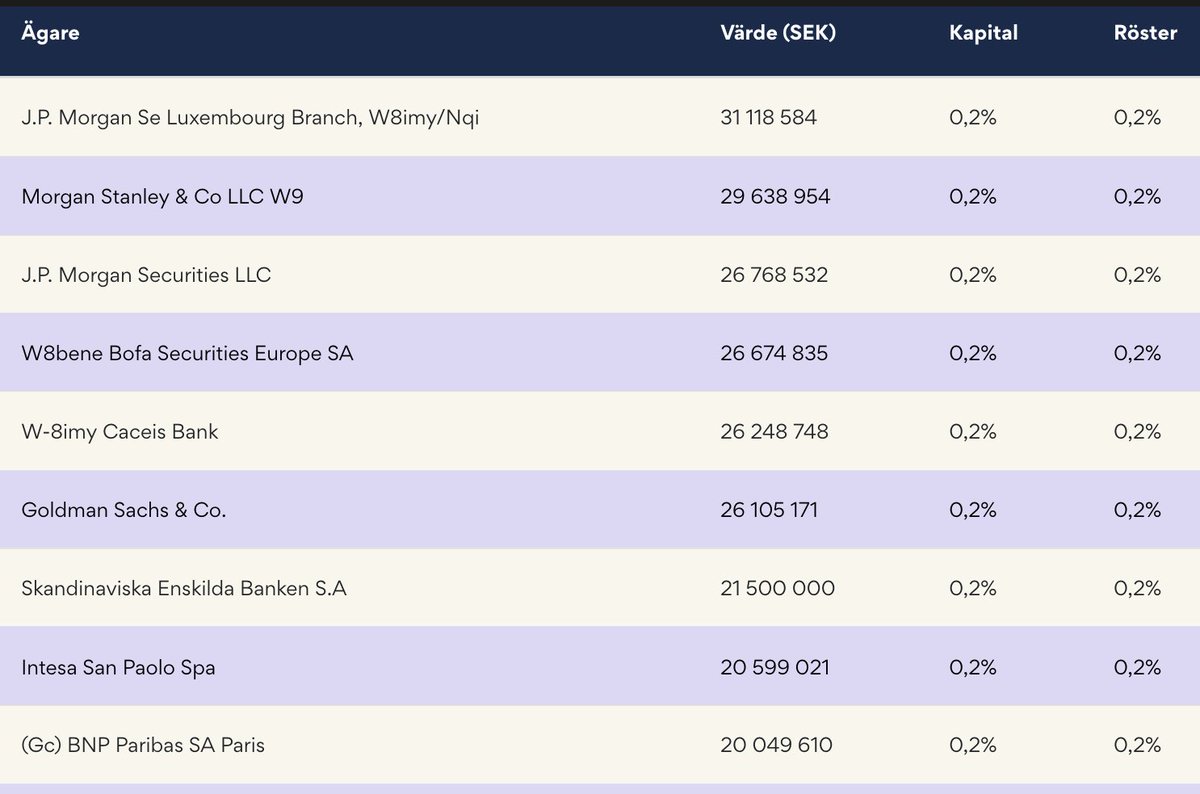

- JP Morgan: .5% (institutional)

- J.P. Morgan Securities Plc: .4% (institutional)

- Citibank New York: .3% (institutional)

- JP Morgan SE: .2% (institutional)

- Morgan Stanley: .2% (institutional)

- JP Morgan Securities: .2% (institutional)

- BoFA Securities: .2% (institutional)

- Goldman Sachs: .2% (institutional)

- Goldman Sachs International: .1% (institutional)

- Cbny-Rja-Client Asset - .1% (retail/wealth)

Large % now owned US retail shareholders (eg. $IBKR on behalf of clients, probably majority retail some institutions).

The new but smaller JP Morgan Goldman Sachs, and Citibank % positions are likely hedge funds or other institutions trying to build positions.

Europe & Switzerland: 11.3%

- Clearstream: 6.2%

- UBS Switzerland: 1.6%

- Six SIS: 0.8%

- Euroclear Bank: 0.8%

- Saxo Bank: 0.6%

- BNP Paribas: 0.6%

- Caceis Bank / Intesa San Paolo: 0.2% each

- KBC / LGT / Julius Baer: 0.1% each

Swedish ~8.49%:

Försäkringsaktiebolaget Avanza Pension - 4.76%

Nordnet Pensionsförsäkring - 2.73%

Skandinaviska Enskilda - .2%

SEB Life International - .1%

Nordea Bank Abp - 0.7%

Canada/UK/Middle East ~.6%:

First Intl Bank of Israel - .3%

Royal Bank of Canada - .1%

Royal Bank of Canada - .1%

HSBC - .1%

A special thank you to the Swedish Media doing the work of US institutions:

The West now has ~58.7% ownership. Swedish is now down to 8.49% due to local media.

I wonder if they realized what they've done now scaring off local investors now that it's changed hands to US institutions/investors?

The West have now acquired majority of the float before the CPO supercycle.

You can also start to see US institutions like JP Morgan or Goldman Sachs building start positions (on behalf of institutional investors), probably off of US retail taking profits. This is likely after $SIVE reached a certain MC threshold for fund mandates.

But a large % of it is still owned by US retail on places like $IBKR and Fidelity. (this is what I call frontrunning the institutions)

TLDR:

$SIVE went from majority:

-> Swedish retail ownership

-> US retail ownership

-> gradual US Institution ownership as US retail takes profit or sells (if they figure out a way to scare off US retail like the Swedish media did).

437

135

2,362

1,552,195

Jacob Bigelo retweeted

Quand Wall Street manque de cash, elle vend ses gagnants 🥇

La séance du jour n’est pas vraiment une surprise. L’or, l’argent, les valeurs liées à l’IA, les semi-conducteurs, certaines cryptos…tout semble baisser en même temps. Et pourtant, les fondamentaux n’ont pas changé en quelques heures. Nvidia ne s’est pas soudainement transformée en mauvaise entreprise et l’or n’a pas perdu son statut de valeur refuge. Alors pourquoi cette impression de vente généralisée ?

La réponse est souvent beaucoup plus simple qu’on ne l’imagine : quand la volatilité augmente et que les appels de marge apparaissent, les investisseurs ont besoin de récupérer des liquidités rapidement. Et dans ces moments-là, ils ne vendent pas forcément leurs erreurs. Ils vendent ce qui est encore en gain. Les actifs qui ont le plus monté deviennent alors les premiers distributeurs automatiques de cash du marché.

C’est ce qui explique pourquoi des actifs qui n’ont absolument rien en commun peuvent parfois chuter ensemble. L’or, les métaux précieux, les géants de l’IA ou même certaines cryptomonnaies peuvent être victimes du même phénomène : une réduction du levier et une recherche urgente de liquidités. Dans ces phases, les marchés ne réagissent plus seulement aux nouvelles économiques, mais aussi aux contraintes financières des investisseurs eux-mêmes.

Et c’est probablement ce qu’il faut retenir de ce genre de séance. Une baisse généralisée ne signifie pas forcément que le scénario de fond est remis en question. Parfois, le marché ne dit pas : « les actifs sont devenus mauvais ». Il dit simplement : « j’ai besoin de cash ». Et dans l’histoire des marchés financiers, les grandes purges de levier ont souvent été violentes…mais rarement éternelles 😉

16

25

238

26,743

Jacob Bigelo retweeted

Jun 3

$TE shows how heat, vacuum pressure and precision engineering turn glass, EVA and solar cells into a fully sealed solar module.

This lamination step protects the cells, improves durability and supports the bigger push to become a leader in American solar manufacturing.

35

111

1,216

130,107

Jacob Bigelo retweeted

Jun 3

$SIVE는 어제오늘 나온 뉴스로 투자 포인트가 더 선명해진 상황임.

핵심은 간단함.

Sivers는 완성된 광모듈을 파는 회사라기보다, AI 데이터센터에서 데이터를 빛으로 주고받을 때 필요한 “레이저 광원”을 만드는 회사에 가까움.

쉽게 말하면 이거임.

AI 데이터센터 안에서는 GPU, CPU, ASIC 같은 칩들이 엄청난 양의 데이터를 서로 주고받아야 함.

예전에는 이걸 구리선, 즉 copper로 연결했음.

그런데 AI 서버 규모가 커질수록 copper는 한계가 커짐.

속도, 전력, 발열, 거리 문제가 생김.

그래서 업계가 점점 “전기로만 연결하지 말고, 빛으로 연결하자”는 방향으로 가고 있음.

이게 CPO, optical I/O, silicon photonics 같은 흐름임.

여기서 중요한 건, 빛으로 데이터를 주고받으려면 먼저 안정적인 빛을 만들어주는 레이저가 필요하다는 점임.

Sivers가 노리는 자리가 바로 이 부분임.

첫 번째 호재는 GlobalFoundries 쪽임.

GlobalFoundries는 세계적인 반도체 파운드리임.

이번에 GF는 Sivers의 laser array를 자사 silicon photonics reference design에 통합한다고 발표함.

쉽게 말하면, GF가 고객들에게 “AI 데이터센터용 광연결 구조를 만들려면 이런 설계를 참고하세요”라고 보여주는 기본 설계 안에 Sivers의 레이저가 들어간다는 뜻임.

이게 의미가 큼.

당장 대량 매출이 확정됐다는 뜻은 아님.

하지만 Sivers가 GF의 silicon photonics 생태계 안에서 laser source 후보로 올라갔다는 뜻임.

또 Sivers laser array는 GF의 SCALE 플랫폼에도 사용될 예정임.

SCALE은 GF의 CPO용 silicon photonics / advanced packaging 플랫폼임.

즉 Sivers는 단순 LPO나 LRO 쪽만이 아니라, CPO와 차세대 데이터센터 optical interconnect 쪽에도 노출되는 구조임.

두 번째 호재는 Ayar Labs 쪽임.

Ayar Labs는 NVIDIA NVLink Fusion 생태계에 합류했다고 발표함.

NVLink Fusion은 NVIDIA가 AI factory 안에서 GPU, CPU, ASIC, XPU 같은 여러 칩들을 더 빠르고 효율적으로 연결하기 위해 밀고 있는 생태계임.

Ayar는 여기서 CPO / optical I/O 기술을 제공하는 쪽임.

쉽게 말하면 NVIDIA AI factory 안에서 칩들끼리 데이터를 빛으로 더 빠르게 주고받게 해주는 역할임.

여기서 Sivers와 연결되는 지점은 Ayar의 SuperNova external light source임.

Ayar의 구조는 크게 보면 TeraPHY optical engine SuperNova external light source 조합임.

optical engine이 데이터를 빛으로 주고받는 엔진이라면, external light source는 그 엔진에 필요한 빛을 공급하는 심장부에 가까움.

Sivers는 이미 Ayar SuperNova에 들어가는 16-wavelength DFB laser array를 공동 데모한 이력이 있음.

즉 Sivers는 Ayar의 optical I/O 구조에서 레이저 광원 쪽 파트너로 연결되어 있음.

논리 구조는 이렇게 보면 쉬움.

NVIDIA는 NVLink Fusion 생태계를 키우고 있음.

Ayar는 그 생태계에 CPO / optical I/O 기술로 합류함.

Sivers는 Ayar SuperNova external light source에 들어가는 DFB laser array 파트너임.

GF는 Sivers laser array를 silicon photonics reference design과 SCALE CPO 플랫폼에 통합함.

그래서 결론은 이거임.

SIVE가 NVIDIA에 직접 공급 확정됐다는 뜻은 아님.

Ayar의 NVIDIA 발표문에 Sivers 이름이 직접 나온 것도 아님.

그래서 “SIVE = NVIDIA 직접 공급주”라고 말하면 과장임.

하지만 반대로 SIVE를 단순 400G / 800G / 1.6T LPO·LRO 회사로만 보는 것도 너무 좁은 해석임.

이번 뉴스의 핵심은 Sivers가 AI 데이터센터 optical I/O 생태계에서 “빛을 공급하는 레이저 회사”로 점점 더 명확하게 자리 잡고 있다는 점임.

여기서 또 중요한 건 희소성임.

레이저 회사가 전 세계에 아예 몇 개 없다는 뜻은 아님.

일반 광통신용 레이저를 만드는 회사는 여러 곳 있음.

하지만 AI 데이터센터 CPO / optical I/O용 레이저는 요구 조건이 훨씬 까다로움.

그냥 빛만 내면 되는 게 아님.

여러 파장의 빛을 안정적으로 내야 함.

출력도 충분해야 함.

열에도 안정적이어야 함.

silicon photonics와 optical engine 구조에 맞게 붙어야 함.

그리고 나중에는 대량 생산까지 가능해야 함.

즉 핵심은 “레이저를 만들 수 있냐”가 아니라, “AI scale-up용 CPO / optical I/O 구조 안에서 검증된 multi-wavelength DFB laser array를 공급할 수 있냐”임.

이 영역에서는 후보가 훨씬 제한적임.

AI CPO / optical I/O 쪽에서 실제 고객 구조 안으로 들어간 몇 안 되는 upstream laser array 후보임.

이게 SIVE의 희소성임.

정리하면 이거임.

SIVE는 NVIDIA 직접 공급 확정주는 아님.

하지만 GF를 통해 silicon photonics reference design과 SCALE CPO 플랫폼에 노출됐고,

Ayar를 통해 NVIDIA NVLink Fusion CPO / optical I/O 생태계에 간접 노출될 가능성이 생겼음.

그래서 SIVE는 LPO / LRO만의 회사가 아님.

LPO / LRO CPO optical I/O external light source laser array 옵션을 가진 회사임.

AI 데이터센터가 커질수록 copper 한계는 더 커지고, optical I/O와 CPO 필요성은 더 커질 가능성이 높음.

그 구조에서는 데이터를 빛으로 바꾸는 optical engine도 중요하지만, 그 엔진에 안정적으로 빛을 공급하는 laser array도 같이 중요해짐.

현재 단계에서 가장 합리적인 해석은 이거임.

SIVE는 아직 NVIDIA 직접 공급 확정이나 대량 매출 확정 단계는 아님.

하지만 GF와 Ayar를 통해 AI 데이터센터 CPO / optical I/O 생태계의 핵심 laser array 후보로 점점 더 선명해지고 있음.

이건 SIVE thesis를 강화하는 호재임.

개인 기록 / 투자 조언 아님

15

33

211

17,167

Jacob Bigelo retweeted

Jun 2

$TE: ☀️🇺🇸 T1 Energy's Progress in Austin Texas Where the Birth of America's Solar Comeback is Taking Shape

Rockdale Municipal Development District:

We are thrilled to share that T1 Energy Inc. has started to go vertical with the construction of their G2 plant at Sandow Lakes Ranch.

This $425 million phase 1 of what is expected to be an $850 million project looks to create around 1,800 new manufacturing jobs in the Rockdale, Texas area when the project is fully complete.

The plans are for this first phase to be producing solar cells by the end of the year with the first batch of new hires starting shortly. This is truly a transformative time for this community and we are excited to be part of T1's journey.

Original Post: linkedin.com/posts/we-are-th…

4

35

317

22,965

Jacob Bigelo retweeted

Jun 2

Breaking news! 💥

Sivers $SIVE & GlobalFoundries $GFS Advance AI Data Center Optical Solutions

Tue, Jun 02, 2026 07:00 CET

Sivers’ laser arrays to support GlobalFoundries’ silicon photonics platform and SCALE™ optical engine solutions targeting a $25B Pluggable Optics market by 2030

Kista, Sweden – June 2, 2026 – Sivers Semiconductors AB (STO:SIVE), a global leader in photonics and wireless technologies, today announced a strategic collaboration with GlobalFoundries (Nasdaq: GFS) (GF), to develop advanced silicon photonics solutions for the high-growth AI infrastructure market.

Sivers Semiconductors’ laser arrays will be integrated into reference designs built on GF’s silicon photonics platform. The collaboration supports a range of optical connectivity architectures, including co-packaged optics (CPO), linear pluggable optics (LPO), and other emerging data center interconnect solutions. Sivers’ laser arrays will also be available in GF’s Silicon Photonics Co-packaged Advanced Light Engine (SCALE™) platform for next-generation optical sub-assemblies and light engine architectures. GF’s SCALE CPO solution combines integrated photonic devices, coarse and dense wavelength-division multiplexing (CWDM, DWDM) and advanced packaging enablement to improve bandwidth density and system scalability.

news.cision.com/sivers-semic…

52

135

933

160,553

Jacob Bigelo retweeted

May 28

$TE is trying to become the face of American solar manufacturing.

Its Stage 3 layer assembly process uses 182 robots across 5 layers to build solar modules with machine-level precision designed for decades of real-world performance.

39

145

1,613

196,084

Jacob Bigelo retweeted

May 29

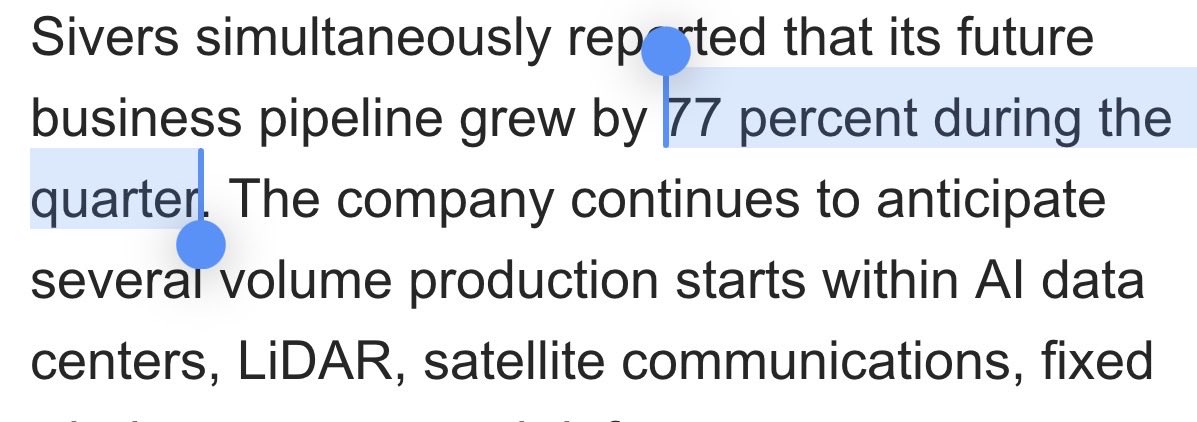

$SIVE basically took their entire revenue pipeline.

In the entire company’s history.

Then grew that by 77% in the first 3 months.

Thats by far the clearest indication of the inflection of the CPO supercycle.

It’s probably going to look exponential from here on out.

May 29

Only thing to look at with $SIVE earnings is forward growth.

Nobody cares about pre-development contract earnings from 2025 or last quarter, especially for qualification cycle optical players.

Having 77% growth of opportunity pipelines (revenue volume ramp projections), to $799m

In a quarter is absolutely incredible growth. And, I’d expect to see that continue compounding.

“The company continues to anticipate several volume production starts within AI data centers” (photonics/lasers).

Is also very positive and validates the thesis about volume ramp for photonics.

Now next thing to look at is earnings call transcript, once they’re indexed, which is the most important signal of what’s to come.

Overall, very positive.

129

103

1,602

484,002

Jacob Bigelo retweeted

May 29

Only thing to look at with $SIVE earnings is forward growth.

Nobody cares about pre-development contract earnings from 2025 or last quarter, especially for qualification cycle optical players.

Having 77% growth of opportunity pipelines (revenue volume ramp projections), to $799m

In a quarter is absolutely incredible growth. And, I’d expect to see that continue compounding.

“The company continues to anticipate several volume production starts within AI data centers” (photonics/lasers).

Is also very positive and validates the thesis about volume ramp for photonics.

Now next thing to look at is earnings call transcript, once they’re indexed, which is the most important signal of what’s to come.

Overall, very positive.

158

108

1,624

614,705

Jacob Bigelo retweeted

May 28

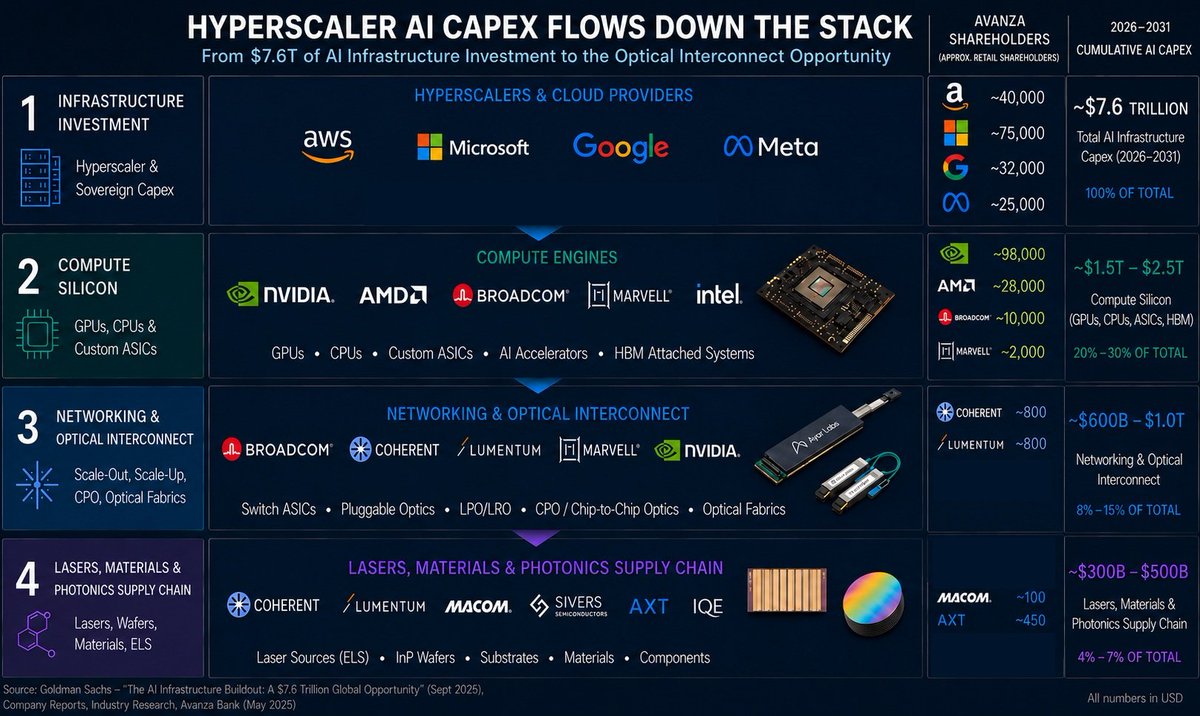

$SIVE is the most compelling CPO/photonics exposure to me.

Addressing the disinformation: I haven’t sold and don’t plan to sell a single share.

I do think this ends up the next $80B $LITE one day from ~$2.1B.

And I personally have plans to acquire more ownership support their M&A prospects.

I believe earnings transcripts will be strongly positive.

As in the part few months we’ve discovered:

> AlChip/Amazon private placements, which is positive for Ayar -> $SIVE implying Trainium 4 design in

> Wiwynn Ayar CPO scale up

> $JBL 1.6T optical transceiver ramp with Sivers incoming faster than markets expected (with relatively dramatic moat demand as much as they can produce)

> O-Net scaling up ELS efforts with $SIVE

> $YSS acquisition of $SIVE allspace lead partner, designing Sivers into Space defense primes

> New CHIPS ACT funding for $SIVE

> $POET H2 volume ramp and their new $50m -> $500m order (with $SIVE as light source)

> information discovery around $AAPL using $SIVE lasers for next gen consumer devices

> information discovery around links to Lightelligence (went public $10B MC) Lightmatter as likely customers.

> Celestial volume ramp with $MRVL indicators.

> new customers working on TFLN with $SIVE like Lightium

> $AMD going with $GFS for CPO, and GFS listing sivers as one of two laser suppliers

> Ayar removing $MTSI / $LITE from their website and signaling $SIVE as primary source/sole source

> Ayar raising $500m for volume ramp (intel, Mediatek, Nvidia, amd etc)

> pluggable TAM expansion signaled from 2025 annual report

> Nasdaq listing expected soon

> MSCI small cap index / Nasdaq omx inclusion, making Blackrock, Vanguard and others passive buyers

> M&A signaled from 2025 annual report 2 new board members that have experience in that area

> $NOK as likely customer from 2025 annual report.

> $LITE getting cw bottlenecked from EML contracts, $SIVE signaling capacity agreements in place with Win, making the a likely bottleneck owner chokepoint in CPO sector.

All of this market research was done before earnings.

Any results is just confirmation of supply chain mapping done.

I don’t think anyone cares about former quarter revenue since $SIVE is an exceptionally compelling 2027 long, especially H2 onward.

Only thing I’m looking at are:

> TAM expansion of the overall photonics supercycle (eg. optical engine, ELS, pluggables) either from M&A or developments

> volume ramp expectations from existing companies

> Nasdaq listing timelines for more liquidity to support their M&A efforts

> any new customers signaled for CPO/Pluggables

303

218

2,409

542,259

Jacob Bigelo retweeted

May 27

$SIVE earnings Friday. Decent chance it sells off.

Stock's up 19x in a year.

Sell-the-news is a real thing.

People will take profits regardless of what's in the report. That's normal.

I'm holding anyway.

Q1 doesn't decide whether CPO ramps with Jabil in Q4.

Doesn't decide whether LiDAR revenue starts hitting the P&L.

Doesn't decide whether MSCI passive flows show up May 29 or OMX flows June 1.

Doesn't decide whether the Nasdaq NY listing brings in US capital. None of that is in Friday's numbers.

If it gaps up, selling means buying back higher.

If it sells off, MSCI and OMX passive are buying on a schedule regardless. Timing the bottom against forced demand is a tough trade.

Friday doesn't change the 2027 picture.

Holding. $SIVE

12

23

287

36,371

Jacob Bigelo retweeted

Hello Swedish people

I'm from Korea

I own more than 30K $sive shares

I know Zlatan Ibrahimovic, Alfred Nobel and Abba.

I love Sweden and Swedish short sellers. THANK YOU

36

16

412

50,947

Jacob Bigelo retweeted

May 25

$SIVE is one of those quiet companies that keeps me up at night thinking about the future. While most people are laser-focused on the obvious AI datacenter plays, I’ve been digging into Sivers and I’m genuinely excited about how their specialized tech could quietly power so many different megatrends over the next decade.

Their real strength lies in high-stability InP photonics, especially those DFB laser arrays, and efficient mmWave beamforming chips. It’s not flashy stuff on the surface, but it solves real problems around precise, compact, and power-efficient light and radio waves.

What blows my mind first is the space angle: orbital datacenters. Sivers ultra-stable lasers could become the key enablers for free-space optical links in vacuum, think connecting server racks in Starlink-style meshes with free cooling and basically zero latency. Jeff Bezos recently said that while super-aggressive timelines might be optimistic, this is definitely coming. Blue Origin’s big filing for thousands of compute satellites backs that up. If this takes off, Sivers could end up playing a hidden but important role in solving AI’s insane energy and heat challenges off-planet. That’s huge.

Closer to home, the same lasers are already heading into real production. Their strategic customer $AEVA starts volume ramp in Q4 2026, with an initial $53–138 million cumulative revenue potential. And that’s just the start, as Aeva wins more deals in robotics and industrial automation, it can grow a lot bigger. Aeva’s FMCW 4D LiDAR needs exactly the kind of lasers Sivers makes. What really excites me is the industrial robotics side: their Omni and Eve sensors give robots instant velocity plus position data so they can move safely and smartly in busy factories and warehouses. Imagine Boston Dynamics-style agility at massive scale, robots that actually “see” moving objects, avoid collisions in real time, and make human-like decisions. This feels like the moment physical AI finally becomes practical and productive.

On the defense side, Sivers is picking up real momentum. In January 2026 they won an $800k contract with a big U.S. defense player for next-gen mmWave chips aimed at drones and tactical systems. Combined with their CHIPS Act work alongside $RTX, $BAESY, and MIT, they’re supporting electronic warfare tools like advanced radar, counter-drone high-power microwave systems, and secure low-probability-of-intercept links for drone swarms. In a Golden Dome-style layered defense world, this tech provides jam-resistance and resilience when everything else gets denied. With the world the way it is, this dual-use area could become a solid, high-margin growth engine.

Even further out, they’re quietly involved in quantum-enhanced sensing via the UK-funded SPIDAR project with Toshiba, Thales, and others. Their lasers help create LiDAR with way better range, resolution, and sensitivity, perfect for robots in tough conditions and quantum positioning systems that actually work when GPS is jammed or unavailable. It’s early, but it opens doors to some very high-value future applications.

The beautiful part for me is how it all connects back to one single technology platform they’ve refined for years. Space infrastructure, industrial robotics, defense drones and EW, and quantum edges, all from the same core. Most of these are still small today, which is exactly why the upside feels so asymmetric.

$SIVE isn’t just another AI story. It’s building the hidden enabling layers for a more connected, autonomous, and resilient world. These kinds of setups, where patience meets multiple real shots on goal, are the ones that can really reward long-term believers.

What do you think, which of these hidden applications excites you the most?

6

28

168

12,421

Jacob Bigelo retweeted

May 25

$SIVE is the largest beneficiary of brand new events this weekend:

1. Sivers new NASDAQ index inclusion (OMX Stockholm):

Both Vanguard and Blackrock are new passive inflows.

With ~$60M pure buying pressure inflow, into existing float, together with MSCI next week.

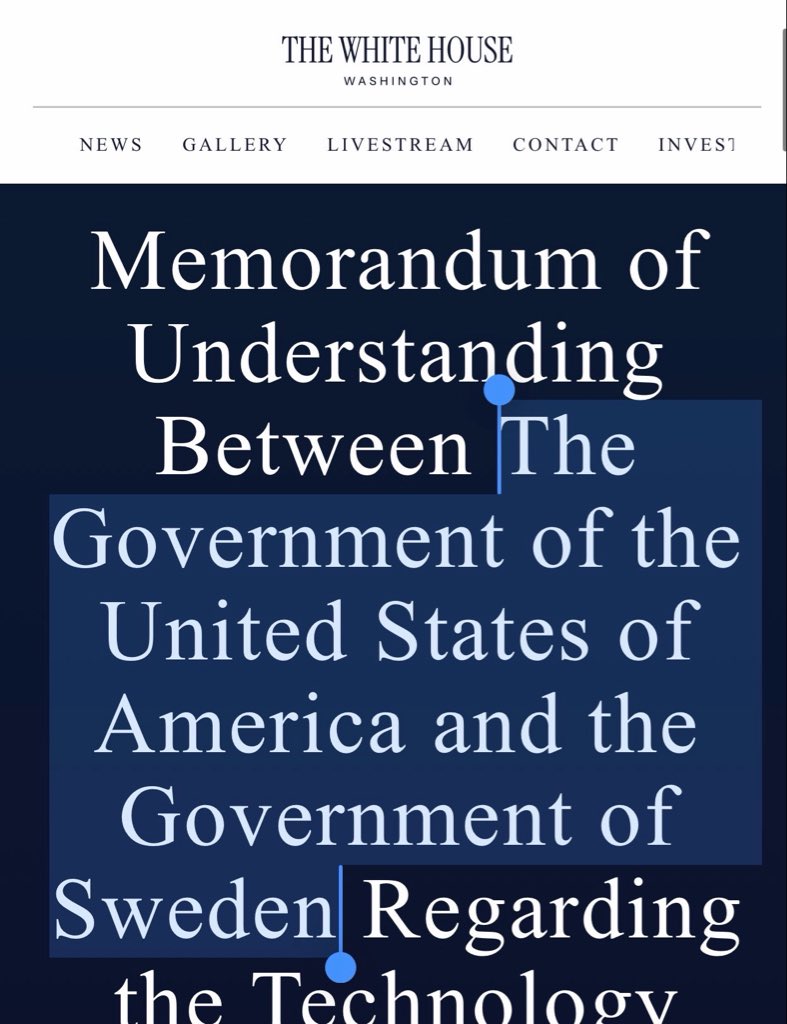

2. US Gov and Sweden sign agreement for joint tech collaboration.

$SIVE is one of the few CHIPS act recipients, and especially in Sweden.

And if you don’t remember, they received another $6.6M CHIPS act award last week.

Making $SIVE heavily supported critical to the US government.

-

TLDR: New passive institutional inflow from your largest US institutions like Blackrock/Vanguard.

Compounded with US government backing into $SIVE. Over the weekend.

Beneficial for fundamentals (revenue/TAM from Pentagon supply chains) and inflow from Blackrock/Vanguard/MSCI/NASDAQ.

Extremely bullish.

118

121

1,454

737,881

Jacob Bigelo retweeted

May 10

Bank of America JUST called nuclear, "the answer to all the world's power shortages."

If you want to become a multi-millionaire in 2 years with me, go ALL-IN on nuclear.

Here's the best nuclear stocks to buy right NOW:

1. Oklo $OKLO

2. NuScale Power $SMR

3. Nano Nuclear Energy $NNE

4. ASP Isotopes $ASPI

5. Lightbridge $LTBR

6. Centrus Energy $LEU

7. X-Energy $XE

Never miss another bull-run again. All my buy and sell signals in Discord @ stockwhale.vip.

111

220

1,821

235,195

Jacob Bigelo retweeted

May 10

10 WAYS TO BUILD AN AI POWER PORTFOLIO

1. $OKLO effectively building the “local nuclear plant” the AI economy will require by placing reactors directly next to data center campuses for 24/7 onsite generation.

2. $BE fuel-cell onsite power play helping data centers bypass the grid with dedicated energy for AI clusters with product backlog up 250% YoY to $6B.

3. $CEG nuclear baseload backbone of the AI era with a 20-year $MSFT PPA tied to the Three Mile Island restart to supply the 24/7 carbon-free power.

4. $VST hybrid power engine of AI combining nuclear, gas & storage with a 20-year $META agreement covering 2,600 MW across three nuclear plants.

5. $GEV industrial supplier rebuilding the U.S. grid providing the turbines, transformers & hardware every AI-driven upgrade cycle depends on with $163B in backlog.

6. $VRT infrastructure gatekeeper for AI compute controlling the cooling & power systems that $NVDA class clusters cannot run without with Q1 backlog up 80% YoY to ~$12.5B.

7. $EOSE long-duration storage solution for a grid under strain helping utilities smooth volatility as AI demand overtakes supply.

8. $NEE clean-energy arm of the AI buildout with largest renewable development pipeline in the country positioned directly into data center load growth.

9. $LEU only U.S. source of HALEU fuel making it essential for powering the modular reactors needed around future AI campuses backed by ~3B DOE contract.

10. $UUUU secures the domestic uranium supply chain by turning nuclear fuel into a national-security asset for the AI age.

130

497

2,753

374,746

Jacob Bigelo retweeted

May 9

The US/West now controls majority of the shares of $SIVE.

With Goldman Sachs/JP Morgan/Morgan Stanley and other US institutions entering.

US/West 46.8%:

- Fidelity: 11.5% (retail)

- Charles Schawb: 11.4% (retail)

- $IBKR: 9.3% (primarily retail)

- BNY Mellon: 4.2% (retail)

- Morgan Stanley Smith Barney: 3.1% (Retail/Wealth management)

-Bank of America: 2.8% (retail/Wealth management)

- BNY Mellon: .9% (institutional)

- Morgan Stanley Client Assets: .7% (institutional)

- Bank of New York Mellon: .5% (institution)

- JP Morgan: .5% (institutional)

- J.P. Morgan Securities Plc: .4% (institutional)

- Citibank New York: .3% (institutional)

- JP Morgan SE: .2% (institutional)

- Morgan Stanley: .2% (institutional)

- JP Morgan Securities: .2% (institutional)

- BoFA Securities: .2% (institutional)

- Goldman Sachs: .2% (institutional)

- Goldman Sachs International: .1% (institutional)

- Cbny-Rja-Client Asset - .1% (retail/wealth)

Large % now owned US retail shareholders (eg. $IBKR on behalf of clients, probably majority retail some institutions).

The new but smaller JP Morgan Goldman Sachs, and Citibank % positions are likely hedge funds or other institutions trying to build positions.

Europe & Switzerland: 11.3%

- Clearstream: 6.2%

- UBS Switzerland: 1.6%

- Six SIS: 0.8%

- Euroclear Bank: 0.8%

- Saxo Bank: 0.6%

- BNP Paribas: 0.6%

- Caceis Bank / Intesa San Paolo: 0.2% each

- KBC / LGT / Julius Baer: 0.1% each

Swedish ~8.49%:

Försäkringsaktiebolaget Avanza Pension - 4.76%

Nordnet Pensionsförsäkring - 2.73%

Skandinaviska Enskilda - .2%

SEB Life International - .1%

Nordea Bank Abp - 0.7%

Canada/UK/Middle East ~.6%:

First Intl Bank of Israel - .3%

Royal Bank of Canada - .1%

Royal Bank of Canada - .1%

HSBC - .1%

A special thank you to the Swedish Media doing the work of US institutions:

The West now has ~58.7% ownership. Swedish is now down to 8.49% due to local media.

I wonder if they realized what they've done now scaring off local investors now that it's changed hands to US institutions/investors?

The West have now acquired majority of the float before the CPO supercycle.

You can also start to see US institutions like JP Morgan or Goldman Sachs building start positions (on behalf of institutional investors), probably off of US retail taking profits. This is likely after $SIVE reached a certain MC threshold for fund mandates.

But a large % of it is still owned by US retail on places like $IBKR and Fidelity. (this is what I call frontrunning the institutions)

TLDR:

$SIVE went from majority:

-> Swedish retail ownership

-> US retail ownership

-> gradual US Institution ownership as US retail takes profit or sells (if they figure out a way to scare off US retail like the Swedish media did).

135

108

1,410

1,140,290

Jacob Bigelo retweeted

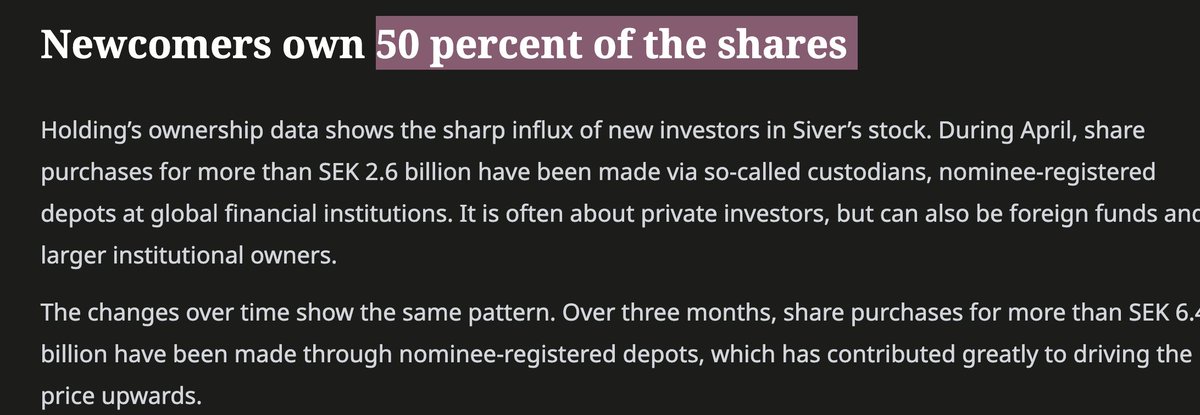

May 9

EFN reports that ~50% of Sivers Semiconductors is now held by "new investors", primarily through CBNY, Charles Schwab, Interactive Brokers, and Clearstream. Combined value: ~8 billion SEK.

efn.se/investerarna-som-pres…

It is framed as these investors are driving this on speculation. Yes maybe, that is of course possible. Or is there another angle?

My take, SEK8B..what? Hence my reaction would probably be the opposite, this could be worth investigating: What thesis are these allocators actually trading? Is it pure speculation with SEK 8B in play? Who sits on these SEK8B?

EFN however have asked "Richard Schatz, senior researcher in photonics at RISE Research Institutes of Sweden and former consultant for Sivers", for his opinion about Sivers.

So what did Mr. Richard Schatz say:

"There are several companies that manufacture these kinds of lasers, and Sivers is far from alone. I don't understand why the company has become so hyped. There are many players, not just in Europe and the US, but also in China," says Schatz.

Honestly I have been COO and CEO at Sivers for almost 10 years 2015-2024 (2015 we had 18 headcount I known everyone in the Company until 2024) and also ask Board members that was in the board many years before me, both for Sivers and former CST Global (Sivers Photonics today) and none of them can recollect Mr. Schatz. I also sent an email, asking the reporter that interviewed Mr S and asked when he claims to have been a consultant at Sivers. Without reply. This doesn't really matter, it is just shows where the digging stops.

Sivers Semiconductors is one of a handful of merchant InP laser suppliers globally. They have disclosed partnerships with POET Technologies, Jabil (1.6T LRO), O-Net, Ayar Labs and operate in the External Light Source category that scale-up CPO architectures depend on.

Either are all these US investors dramatically wrong about the photonics layer of AI infrastructure, or the institutional allocators routing through US brokerages have identified what most Swedish investors haven't yet. Maybe this is worth investigating which? To be 100% clear no one knows (not even me), who has the right hypothesis, that we might know in 2028-2030 time frame.

To help anyone intressted, I made this free and open substack to explain how the money flows. As they said in Washington follow the money...

This article also gives insight to how Swedish retail trades in the stack via Avanza.

andersstorm.substack.com/p/t…

39

68

540

173,264