Joined August 2023

- Tweets 1,955

- Following 333

- Followers 1,394

- Likes 1,657

59 Photos and videos

Bill McGill retweeted

Jun 12

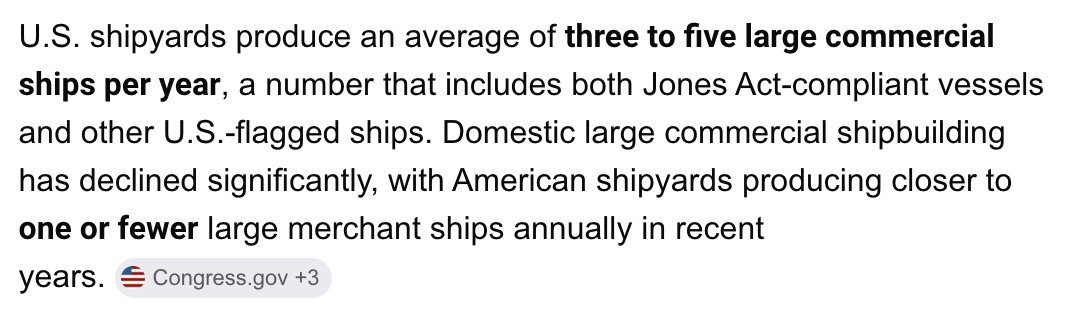

Are these American made ships in the room with us now?

The Jones Act is the bedrock of the U.S. maritime and shipping industry.

@TransportDems are protecting American-made ships and jobs as costs continue to rise from the Administration’s war with Iran.

Community note

The U.S. ship building industry is “near collapse” according to the GAO, despite the Jones Act being in place since 1920.

Today, U.S. ships cost 5x as much as foreign ships.

U.S. flagged commercial ships declined 94% from 1960-2025, while the global fleet doubled.

gao.gov/assets/gao-25-…

nytimes.com/2025/05/27/bus…

maritime.dot.gov/sites/marad.do…?

kentclarkcenter.org/surveys/the-jo…

2

24

216

12,159

Jun 8

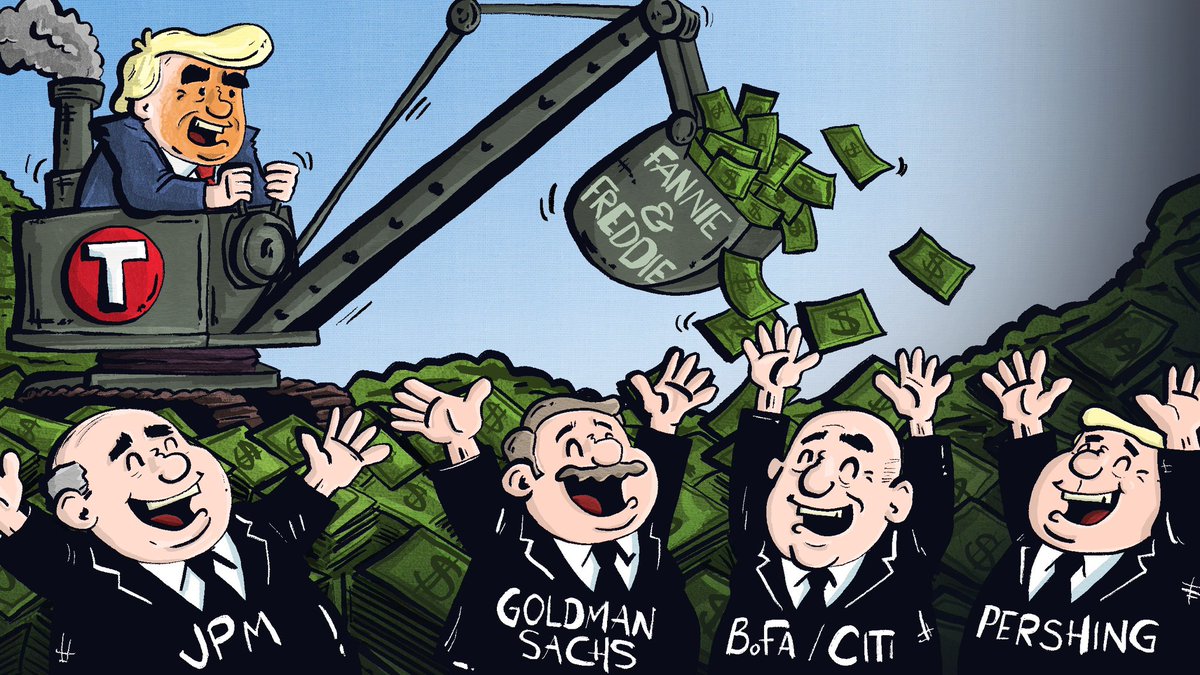

The one constant is banks. Money never goes out of style.

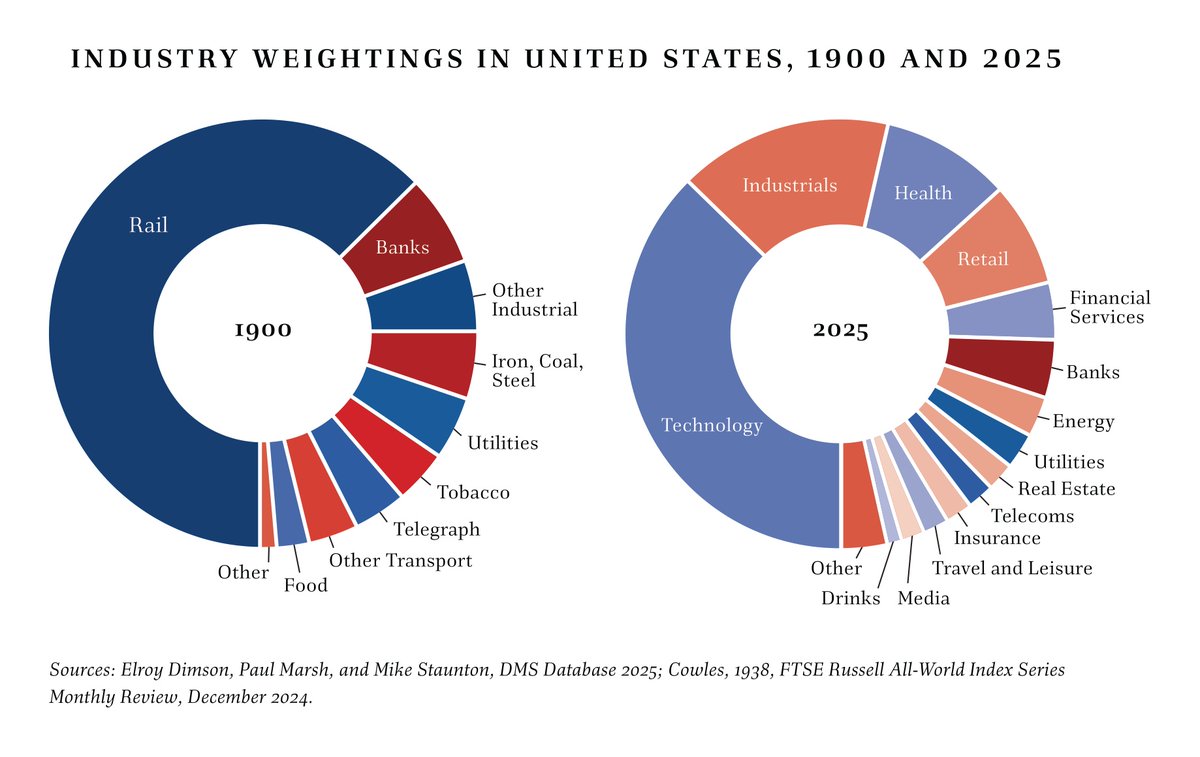

One of my favorite charts from the new book:

→ In 1900, roughly 80% of US stock market value came from industries like railroads, coal, steel, and textiles.

→ Today, about 70% of the market comes from industries that were tiny—or didn't exist at all—125 years ago.

One of the great lessons of investing: The stock market is constantly renewing itself. The future winners rarely look like the past winners.

What industries dominate this chart in 2125?

→ Pre-order Investing in America: amzn.to/4vsujBv

→ Learn more about the book: investinginamericabook.com/

1

10

829

Jun 3

He’s going to really enjoy the day he just manages his own money.

Jun 3

Jefferies is not promoting any shorting activity regarding any IPO. Any suggestion to the contrary is WRONG.

6

950

May 12

Paint’s all dry.

15 Nov 2024

I started to read $NSTS 3Q, but then I realized some paint was drying on the house next door and rushed over to watch it instead. 43k shares repurchased. May they live through interesting proxy seasons.

2

1

9

2,126

May 12

I don’t know, man. I’ve met Brenda and she’s not all that observant and the things she does observe don’t seem to factor into even community bank relationship-based loans. I know Joe G. can show you a pretty chart demonstrating that $1B asset banks have lower NPL and charge off rates than $50B asset banks, even when comparing like to like loan categories (it’s not just % of resi loans to total loans driving the lower loss rate), but I don’t think Brenda has much to do with it. The CRE LTVs do. The reach for NIM on inventory financing does. In fact, when banks do fail, the FDIC loss rate on small community banks is absolutely breathtaking compared to FDIC loss rates on larger community and regional banks. And those stunning small bank losses are, in fact, very much due to “relationship” lending.

May 12

Brenda has worked at this bank for twenty-seven years and she knows which farmers are three months behind on their equipment loans but still good for it and which ones are current on paper but won't make it through the winter, and she knows that Mr. Henderson's weekly deposit should be exactly $2,847.12 every Friday unless he sold extra calves that week, and she knows that the Peterson kid's checking account went negative three times last month which means he's probably using again, and she knows that the widow Morrison always withdraws exactly $300 every second Tuesday for her grandson's piano lessons even though the grandson is now thirty-four and lives in Denver, and this knowledge lives in her head and nowhere else because there is no field in the core banking system for "Morrison withdraws $300 for dead grandson" or "Henderson's deposit timing correlates with cattle market" or "Peterson family addiction patterns affect loan performance," and when the acquisition closes next month Brenda will train her replacement for exactly forty-seven minutes on how to process a wire transfer and how to order new checks and how to run the daily cash report, but there is no training manual for twenty-seven years of watching the same families grow up and fail and get married and default and die, and the acquiring bank's efficiency experts have calculated that eliminating her $47,000 salary will improve the cost-to-income ratio by thirty-six basis points, and they are correct about the math and completely wrong about everything else, and Brenda will clean out her desk on a Friday afternoon and take her coffee mug and her photos of her grandkids and walk out of the building where she has spent more waking hours than her own home, and the bank will continue operating and the customers will learn to use the ATM and the drive-through and the mobile app, and the new systems will process transactions faster and more efficiently than Brenda ever could, but no computer will ever know that Henderson's late payment means he's probably getting divorced again, and no algorithm will recognize the early warning signs in the Peterson kid's account activity, and no spreadsheet will track the subtle rhythms of a rural economy that Brenda could read like sheet music, and six months later when three farmers default in the same week and the loan committee wonders how they missed the warning signs, there will be no one left to explain that the signs were all there if you knew how to look, but the person who knew how to look got eliminated for efficiency.

4

1

18

5,560

May 8

"Total assets decreased $27.7 million, or 3.1%, to $877.2 million at March 31, 2026 from $904.9 million at December 31, 2025, due largely to a decrease in cash and cash equivalents, securities and loans."

So assets decreased due to all of the assets decreasing. Thanks for the insight, chief.

1

10

1,408

May 6

I'd rather 10 men get sexually harassed by attractive LevFin MDs with cannons than have one get an undeserved $1MM payoff.

May 6

Breaking: JPMorgan offered a former banker $1 million to settle his lurid sex claims weeks before he filed a lawsuit that has captivated Wall Street on.wsj.com/3QOz6OR

1

16

3,395

Bill McGill retweeted

May 1

This is just getting silly now. Looking at the most recent TWO/CCM amendment, TWO owes CCM about 75c/sh (25c CCM has paid UWM already and another 50c for the amended termination fee) if it goes with UWM.

So if Bill hits Matt’s 12.00 bid - using first names highlighting how personal this is for the parties involved - he actually ends up with 11.25 vs CCM’s current 11.30. That’s not going to happen. This bid is just meant to show Bill up and POSSIBLY make CCM pay more, which they be fools to even consider.

2

3

2

1,134

Apr 21

What the hell? Where are the AT1 investors’ cookies?

Apr 20

I have built a spreadsheet. It has 847 rows. Each row is a community bank in the United States with a market cap below $200 million, a price-to-tangible-book ratio under 0.85, a non-performing loan ratio below 0.4%, and a CEO who has been in the role for at least twelve years. I update it every Sunday from 6 AM to 11 AM while my family attends church without me. I have visited the headquarters of nineteen of these banks in person. I have eaten a complimentary lobby cookie at each one. The cookies are how you can tell. A bank with a good cookie is a bank that respects its depositors. A bank with a stale cookie is a bank that will be acquired within 36 months at a 40% premium. I am never wrong about the cookies. The cookies have never lied to me. The cookies are the only thing left that tells the truth.

3

1,147

Apr 6

Am I the only person that thinks this banker should be applauded for going to work 340 times in 11 months? standard.co.uk/news/crime/hs…

1

4

429

Mar 28

$C Do you see that in the distance? That’s a CEO of a large bank that has to be bailed out every 30 years or so that is trading below TBV publicly musing about acquiring another bank. Now hand me that cannonball.

3

4

30

7,617

Mar 17

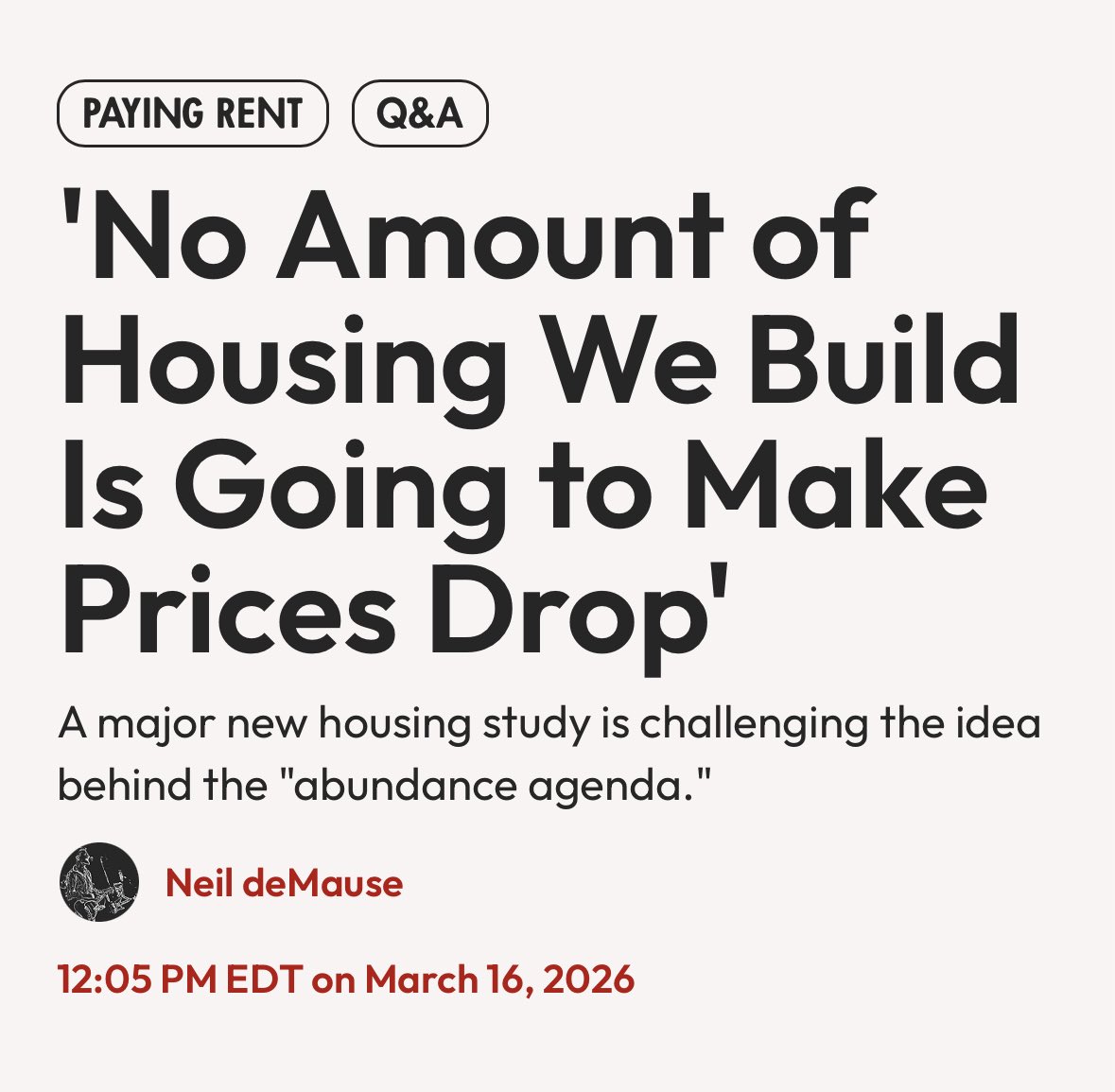

Long-term true, if your definition of affordable is < construction cost.

Mar 16

A major new study has confirmed what many of us know from reading all previous research.

Socialists in NYC should care about this, bc Mayor Mamdani has filled his administration with developer hawks in hopes of delivering the Affordability Agenda.

It won’t.

4

616

Bill McGill retweeted

"Jamie Dimon is not lending to PC lenders. it's well known"

Jamie Dimon:

smokin grass... jamie dimon is not lending to PC lenders. it's well known. fwiw it's been a great call.

jpm won't be the pin on this grenade. cliffwater getting 14% reds a far bigger issue. $1bn per/mo equity inflow (~$2bn of PC loans per month) going to zero. that's an issue.

7

5

130

28,619

Mar 9

I keep thinking $FFBW has to be close, because even though it is still way over-capitalized at 25% CET1 to RWA, there can’t be much left to repurchase, but good for them, they found another 157k to buy back, with only 4.1MM remaining. More importantly, they made the right decision to close two small branches that failed to get any traction - I mean, if you call $2.5MM in deposits simply a failure because you don’t know any worse words for it. All steps towards the inevitable conclusion.

Mar 9

1

1

10

1,721

Mar 7

So...this account is a bank ingenue and that's not a particularly controversial statement to any bank investors. But it's not retarded. And there are a lot of retarded accounts commenting on banks This isn't the one I'd single out.

Every tweet this account puts out makes me wanna say, “Tell me you know nothing about banks without telling me you know nothing about banks.” But, ya know, ai slop….

1

13

3,955

Bill McGill retweeted

girl wearing a Citadel Equities pullover on this flight hasn’t smiled once in three hours

31

41

3,719

198,344

Feb 28

I mean, narrow-ish bank applications have been controversial for a long time and I really don't think either depositors or taxpayers would like the reason why. An interesting counterpoint, though, is the approval of FundBank. Almost as if the FRB raised it's hands and said "your clients will be the source of the run in the first place, maybe better their deposits don't back loans at all."

Feb 28

What’s it say about the state of politics when the arms manufacturer is the adult in the room.

1

1

5

2,014

Bill McGill retweeted

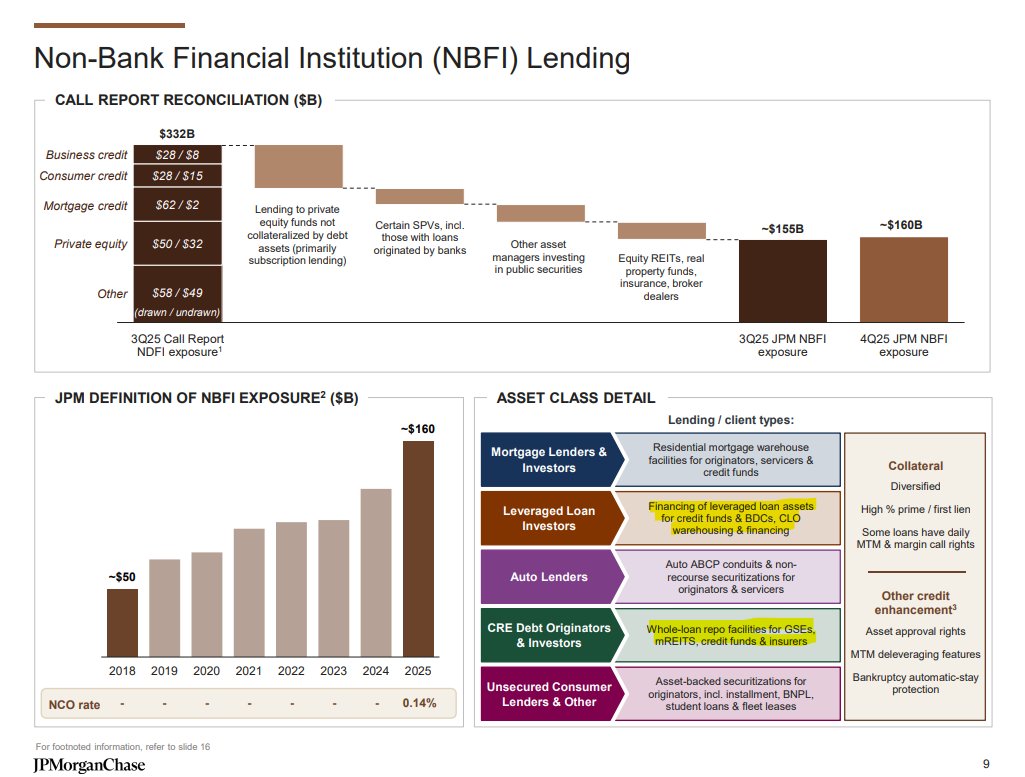

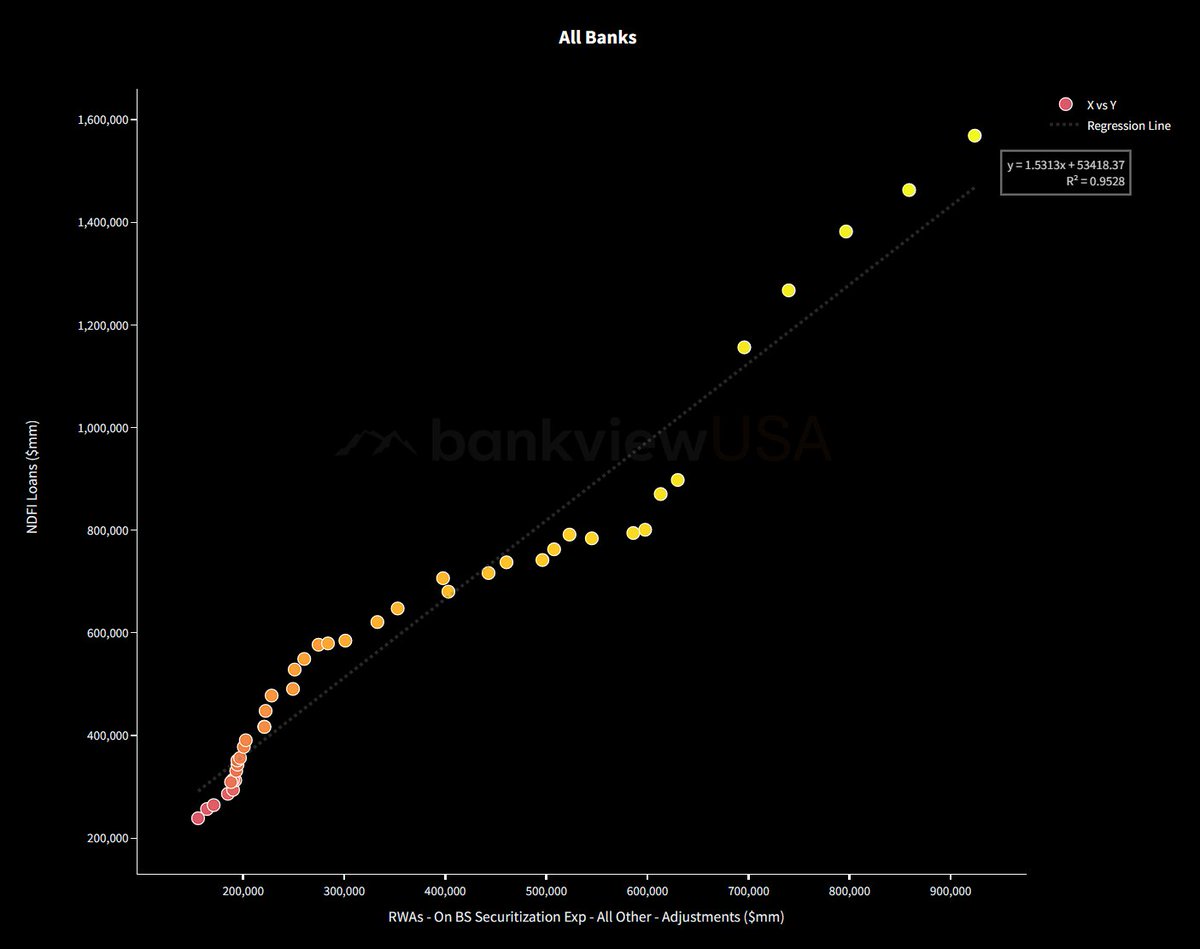

Feb 24

The biggest story in banking rn...

Favorable capital treatment from securitization rules have pushed bank lending into private credit.

#SSFA

Feb 24

A regional bank makes a $100 NDFI loan to a BDC.

The loan is collateralized by $133 of middle-market loans placed in a bankruptcy-remote SPV, and the BDC takes the first loss. The lawyers structure it so it qualifies as a securitization.

Question: How much capital must the bank set aside for this loan?

a) $8 - same as direct loan (100% RW)

b) $12 - slightly riskier (150% RW)

c) $100 - BDCs are super-risky... dollar for dollar (1250% RW)

d) $1.60 - safer because of overcollateralization (20% RW)

3

7

49

16,776