The official Twitter feed of London School of Finance and Law (LSFL) Library and Media Centre @LSFL_ProfDev

Joined October 2020

- Tweets 103

- Following 346

- Followers 85

- Likes 154

6 Photos and videos

9 Oct 2023

The digital archive portal of @royalsociety @RSocPublishing is now available with 400 years of scientific history👇

#ScienceInTheMaking

24 Apr 2023

We are happy to announce the launch of our permanent digital archive portal #ScienceInTheMaking! Travel through 400 years of scientific history, from the earliest illustrations of dinosaur fossils to revolutionary scribblings from Newton, Hooke and Halley: royalsociety.org/news/2023/0…

17

18

4,714

LSFL Library and Media Centre retweeted

25 Sep 2023

Study "Business Administration, Finance and Law" at London School of Finance and Law!

Read more about the qualification: courses.lsfl.org.uk/professi…

You may be eligible for tuition funding.

#Finance #Accounting #Auditing #Taxation #TaxLaw #Business #Management #Economics #Research

24

23

4,799

LSFL Library and Media Centre retweeted

15 Sep 2023

Tax Policy Reforms 2023: Discover the latest tax policy reform trends in 75 countries and jurisdictions examined by OECD.

Read a full report here:

oecd.org/tax/tax-policy-refo…

#Tax #Taxation #TaxTwitter #TaxPolicy #TPR2023 via @OECDtax

13

13

3,599

LSFL Library and Media Centre retweeted

African Union plans to launch its own credit ratings agency as the "big three" ratings agencies – Moody's, Fitch and S&P Global Ratings – do not fairly assess the risk of lending to African countries.

Read more: reuters.com/world/africa/afr…

#Economics #Finance #Investment #Banking #AU

10

11

3,545

Since 2017, Public Trust in Tax survey has explored global views on corruption and tax. Discover the key role accountants play in combating corruption and the public’s thoughts on their tax systems and those involved: bit.ly/BuildingTrustInTax

1

20

21

1,045

New findings show that tax reforms have been one of the key policy tools used by governments to protect households and businesses from decade-high inflation levels.

📘🗞️Find out more in 𝑇𝑎𝑥 𝑃𝑜𝑙𝑖𝑐𝑦 𝑅𝑒𝑓𝑜𝑟𝑚𝑠 2023➡️ oe.cd/tpr2023

#TPR2023 #taxpolicy

19

24

5,832

Four Sustainability Challenges for the Accountancy Profession 🌱

Challenge 2️⃣ - Global System ISSB Adoption 🌎

Watch this short video to hear IFAC CEO Kevin Dancey's thoughts on the steps we need to take to achieve this long-term vision of a global reporting system 📽

21

22

4,979

LSFL Library and Media Centre retweeted

6 Sep 2023

London School of Finance and Law offers a wide range of CPD courses, advanced diplomas and professional qualifications for tax practitioners.

Learn more: courses.lsfl.org.uk/tax-law/

#Finance #Taxation #TaxLaw #TaxTwitter #Law #CGT #CorporationTax #IncomeTax #VAT #InheritanceTax #VAT

26

25

267

LSFL Library and Media Centre retweeted

Study Investment and Wealth Management at London School of Finance and Law!

Read more about the course: courses.lsfl.org.uk/investme…

You may be eligible for tuition funding.

#Finance #Economics #Investment #PersonalFinance #WealthManagement #Education #CPD #Research #UK @LSFL_Money

26

23

3,637

LSFL Library and Media Centre retweeted

21 Aug 2023

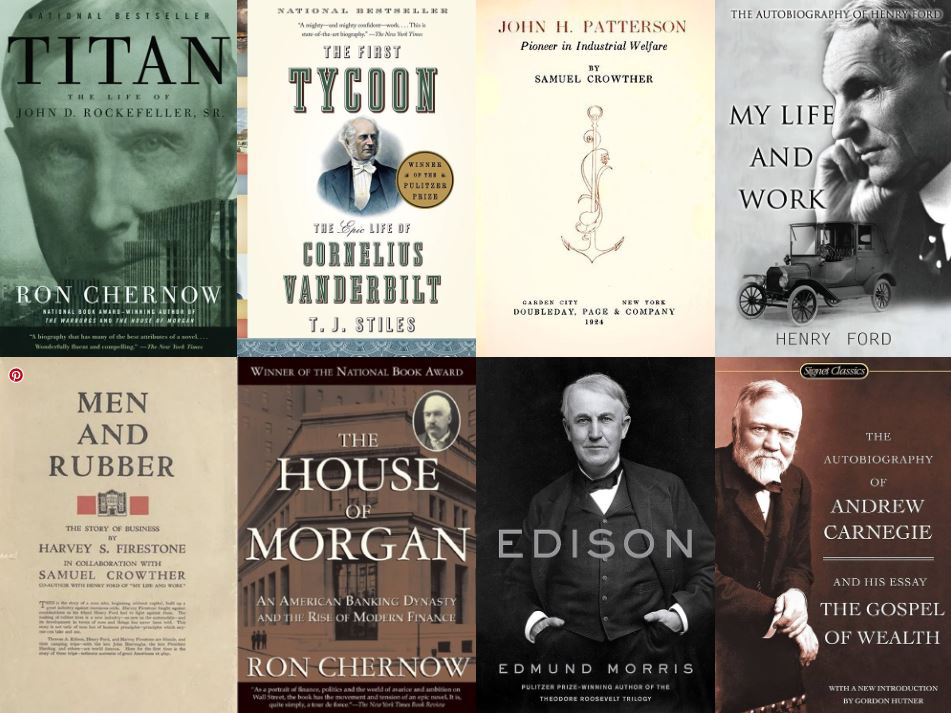

"Where I got a lot of my education from was reading history. I'd go back & read about Edison, Ford, Rockefeller, J.P. Morgan. The period between 1870-1920 is really interesting." Marc Andreessen

Rockefeller

Vanderbilt

Patterson

Ford

Firestone

JP Morgan

Edison

Carnegie

👇

23

428

2,199

334,992

LSFL Library and Media Centre retweeted

21 Aug 2023

Useful notes for any accountant dealing with real estate transactions by @rledbetterCPA:

#RealEstate #Accounting #TaxTwitter

19 Aug 2023

CPAs and real estate pros speak a different language.

Knowing key terms and how they impact taxes is critical to giving good advice.

Here is the list I share with my team on what they need to know:

1) Operating Agreement - aka: OA, LP Agreement, LPA, LLC Agreement.

The governing document of the partnership. In addition to various legal matters, it includes the income and loss allocation language we need to review to complete the tax return.

It should also include the debt allocation language that impacts loss allocations.

2) Deficit restoration obligation - aka: DRO

One of the primary criteria for safe harbor allocation methods to be deemed to have Substantial Economic Effect. A DRO is an unconditional obligation for a partner to restore his negative capital account balance.A DRO is treated like equity for purposes of allocating losses on a pro-rata basis. A DRO must be unconditional and not a “bottom dollar” guarantee.

A DRO is not implicit if a debt guarantee exists. Meaning just because a partner guarantees a loan does not mean that they then have the ability to negative into their capital account. A DRO must compliment the guarantee.

3) Qualified Income Offset - aka: QIO

This is an alternative test to the DRO within the confines of the Safe Harbor allocation methods. It means that loss may not be allocated to a partner that will create or increase the amount of deficit in their capital account. Additionally, if a partner inadvertently goes negative in their capital account (distributions, etc.) that income should be allocated away from other partners with positive capital accounts to that partner with a deficit.

4) Capital account -

THIS IS NOT BASIS; tax basis includes tax-basis capital accounts debt allocated to that partner. A capital account includes the amount of cash / property contributed, plus tax-basis adjustments (§754), plus/minus tax income/loss, less distributions.

Absent a DRO, or minimum gain, a partners capital account cannot go negative. In rare cases, there will be no alternative but then the QIO will come into effect as soon as a partner has a positive capital account.

Capital accounts must be maintained by the partnership.

5) PropCo - aka: single purpose vehicle (SPV), single property entity (SPE)

This is the entity that holds the underlying asset. Some structures will use an additional layer of a single member LLC that holds the asset being invested in. This is done for risk purposes.

6) OpCo -

This is often the entity that manages the property, or receives acquisition fees. Often this can be the S-Corp for tax planning.

7) General Partner - aka: GP, sponsor, syndicator

This is the individual or entity that puts the deal together. They are responsible for bearing up front costs, getting the bank funding lined up, raising equity, identifying the property, managing / overseeing the management of the property.

The GP is usually the party that receives a promote.

8) Pursuit costs -

These are soft costs (legal, engineer, etc) that are paid by the GP to determine if the asset is worth buying. These are incurred before investor money and if abandoned represent an expense.

If the property is eventually purchased, they are allocated to the underlying asset.

9) Promote - aka: carried interest (or carry)

This is a special allocation of the underlying partnership income that usually happens when a certain hurdle has been met on the investment.

For example, if an investor has invested $1MM and has received $1MM 8% annual IRR in distributions back to them, the OA may call for the GP to then receive 10% of all future distributions and the LPs to then take 90%.

When the promote is allocated upon an exit event (sale) it often represents capital gain and thereby is a more tax efficient compensation to the GP.

10) Waterfall -

This is the distribution section of the OA. It is referred to a waterfall because it lists out hurdles (i.e. a stated rate of IRR that must be met, or stated amount of distributions returned) that must be met before GPs can receive a promote.

There are often several hurdles that when met, incrementally increase the amount of the promote (a common starting one is “20 over an 8” which means the GP is allocated 20% of distributions after an 8% IRR is provided to the LP money; but additional layers may be “30 over a 10”, etc.)

Waterfalls will vary by sponsor and asset class depending largely on risk profile of the underlying asset.

11) Preferred equity - aka: mezzanine debt, mezz debt, pref equity

This is a class of equity investors that have a stated rate of guaranteed return or first right to returns (distributions). Many times this class of equity does not participate in losses and is seen often with targeted capital account method.

Mezz and pref may be further segregated by the types of collateral included with each class of equity - but the key point for taxes is the preferred return usually tagged to these.

12) Acquisition Fee -

This is calculated as a % of the asset value (purchase price). This is due to the GP upon closing and represents one of the ways GPs are compensated and make money.

13) Deferred acquisition fee -

This is a tax strategy whereby the GP waives their right to be paid an acquisition fee and instead receive it as an increase in their promote. This strategy converts current ordinary income into future capital gain. However, important language should be included in the OA such that this is not construed as equity for a service (taxable phantom income).

14) Non-recourse debt -

This is debt that is not guaranteed by a partner of the partnership.

15) Non-recourse deductions -

These are losses financed with non-recourse debt. These happen only when equity (cash contributed by investors) has been depleted.

These often follow the last hurdle in the waterfall - but the OA should speak to that.

16) Qualified non-recourse debt - aka: QNR, QNRC

This is debt that meets certain criteria:

(i) which is borrowed by the taxpayer with respect to the activity of holding real property,

(ii) which is borrowed by the taxpayer from a qualified person or represents a loan from any Federal, State, or local government or instrumentality thereof, or is guaranteed by any Federal, State, or local government,

(iii) except to the extent provided in regulations, with respect to which no person is personally liable for repayment, and

(iv) which is not convertible debt

What’s unique about QNR debt is that it is at-risk for basis calculation purposes. This allows for additional flexibility in allocations and distributions that otherwise would be taxable.

17) Minimum gain -

The amount of gain that would result if a property was sold at net book value. It is calculated as total non-recourse debt less net book value of the secured assets (buildings land). This gain is allocated to partners according to how the OA allocates non-recourse debt and non-recourse deductions (usually profit sharing / promote ratios)

This gain, when it occurs, tags to a specific partner’s basis and allows him to go negative in his capital account without a DRO. When the amount of minimum gain decreases, for specific reasons, the partner would be subject to Minimum Gain Chargeback - which is an allocation of income to the partner for the amount of reduction in minimum gain.

The OA must include these terms and allocations.

18) Hard Money -

This is a specific type of private debt that is meant as a bridge or temporary financing solution. It usually bears higher interest rates (subject to usury laws) and is secured by the underlying property.

14

15

443

LSFL Library and Media Centre retweeted

21 Aug 2023

Study "Taxation: Corporation Tax" at LSFL!

View the course programme here: courses.lsfl.org.uk/taxation…

#Tax #Taxation #CorporationTax #UK #TaxTwitter @LSFL_ProfDev @LSFL_TaxLaw @MyTaxesPlus

18

18

157

LSFL Library and Media Centre retweeted

20 Aug 2023

Of 225 jurisdictions around the world, only six increased their top corporate income tax rate in 2022, a trend expected to hold steady as countries have more efficient tax types to turn towards.

Read more here: taxfoundation.org/data/all/g…

#Tax #TaxLaw #TaxTwitter via @TaxEDU_

1

16

16

285

LSFL Library and Media Centre retweeted

19 Aug 2023

See how tax policies can impact our life, from the buildings we live in and the cars we drive to what we eat and wear: taxfoundation.org/taxedu/edu…

#Tax #Taxes #Taxation #TaxHistory #TaxPolicy #PublicPolicy #TaxTwitter with @MyTaxesPlus via @TaxEDU_

18

19

202

LSFL Library and Media Centre retweeted

18 Aug 2023

Take one of our courses in financial planning and wealth management to learn how to save your and your clients' money!

View our courses on IHT, trusts & taxation of property and investment income here: courses.lsfl.org.uk/finance/

#FinancialPlanning #WealthManagement #TaxTwitter #UK

26

25

216

LSFL Library and Media Centre retweeted

18 Aug 2023

What do a wind farm in Indonesia, a public transit system in Egypt, and plans for clean energy and biodiversity in Colombia have in common? All are being supported by green or sustainable bonds.

Read more here: worldbank.org/en/news/featur…

#Sustainability #ESG #GreenFinance @WorldBank

13

13

139

LSFL Library and Media Centre retweeted

15 Aug 2023

"The great aim of education is not knowledge but action."

— Herbert Spencer

Choose a course or qualification at LSFL to boost your career and help your company achieve organisational effectiveness: courses.lsfl.org.uk/a-to-z-o…

Next term start date: 20 September

#Finance #Careers #CPD

27

23

280

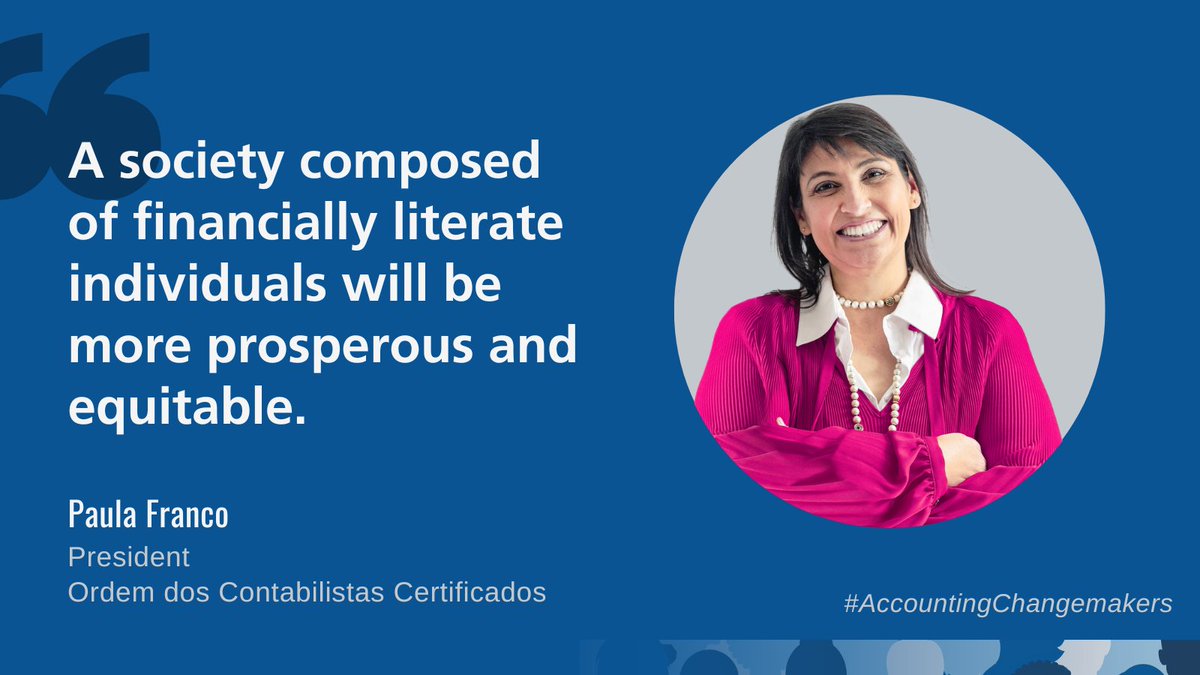

August Changemakers Series: Featuring 3 champions with a passion for financial literacy. Meet Paula Franco, President of @OrdemContab, committed to providing students with quality financial education from a young age. Learn more: bit.ly/ChangemakersPaulaFran…

17

21

1,167

LSFL Library and Media Centre retweeted

2 Aug 2023

📢🌍Introducing ISSA 5000: The proposed International Standard on Sustainability Assurance 5000, General Requirements for Sustainability Assurance Engagements. Read it here - bit.ly/ISSA5000 - and learn more in the thread🧵

1

28

43

7,870

LSFL Library and Media Centre retweeted

Max Rozenfeld is an artist and a historian of architecture. He has spent much of the war imagining how the destruction of Kharkiv presents opportunities for reinventing the Ukrainian city's future.

takumaku.com/2023/04/11/an-a…

#UrbanEconomics #Architecture #Ukraine #UkraineRussiaWar

10

12

200