Institutional Research 📊 Quant Trading ⚡️Auto Buy/Sell Signals 🎯Unlock Research Reports & High-Conviction Signals thewealthclub.vip 👇

Joined June 2025

- Tweets 998

- Following 494

- Followers 281

- Likes 495

463 Photos and videos

Pinned Tweet

24 Nov 2025

🚀🔥 Ron Baron Just Dropped One of His Boldest Calls Ever — and It Could Rewrite the $TSLA Playbook

Long-time Tesla bull Ron Baron says $TSLA could reach $10,000 within the next decade — not because of cars, but because Tesla is rapidly becoming the most vertically integrated AI robotics company on the planet.

Baron’s thesis is built on one core principle: when a company controls hardware, software, data, manufacturing, and real-world deployment end-to-end, the economic ceiling isn’t linear — it compounds.

He identifies three major pillars behind the potential 10×–20× upside:

1️⃣ Autonomy at scale

Once FSD becomes widely deployable, Tesla shifts from selling vehicles to operating a global AI mobility network — a business model with radically different economics.

2️⃣ Optimus as a labor force multiplier

If Tesla delivers the first economically viable humanoid robot, the productivity impact across manufacturing, logistics, and services could be transformative.

3️⃣ Vertical integration as an exponential moat

No suppliers, no fragmentation, no hand-offs. Every layer of Tesla’s stack — models, data, compute, hardware — is built in-house, which enables iteration speed no competitor can match.

None of this is guaranteed. Scaling autonomy, commercializing humanoid robotics, and transitioning revenue toward high-margin software remain some of the hardest challenges in tech.

But Baron’s argument is simple: the market still values Tesla like a cyclical automaker, not an emerging AI-industrial platform.

So the real question becomes:

If Tesla executes even half of this roadmap, does the market price it in early — or only once the flywheel becomes undeniable?

📬 Sharing deeper insights on autonomy economics, robotics cost curves, and the AI-driven valuation rewrites shaping the next decade of tech.

#TSLA #Tesla #ElonMusk #RonBaron #Investing #Stocks #AI #Robotics #AutonomousDriving

6

16

13,573

Jun 13

$NOW $CIFR $NBIS $CRWV $IREN $USAR $RKLB $PLTR, eight stocks positioned to create generational wealth before year-end.

💰 These are your next-wave opportunities.

$NOW leads the enterprise automation revolution—workflow orchestration that touches every company.

$CIFR is crypto infrastructure, riding the digital asset wave that’s only accelerating.

$NBIS represents the next generation of cloud infrastructure, competing in the AI compute arms race.

$CRWV is GPU cloud services, the direct beneficiary of hyperscaler demand for inference capacity.

$IREN pure-play AI compute and data center power—positioned at the exact inflection point where demand explodes.

$USAR controls critical rare earth supply chains, increasingly essential as geopolitics reshape semiconductor and defense manufacturing.

$RKLB dominates commercial space launch, the backbone of Starlink, constellation deployments and space infrastructure.

$PLTR is government AI and data platforms—the only company truly embedded in how governments will operate in the AI era.

🎯 The common thread connecting all eight.

They’re not trading on hype. They’re positioned in bottleneck layers of the AI infrastructure stack.

Compute, power, launch capability, software coordination, rare materials—each fills a critical gap that can’t be easily replicated.

📌 Save this.

Bookmark it. Come back to it in six months. The thesis will become clearer with every earnings report and catalyst that unfolds.

This is not financial advice, but it is where the structural opportunities are concentrating.

129

Jun 13

$TSLA $SOFI $SPCX $NVDA $PLTR $IREN $AMZN, seven stocks I believe are absolutely bulletproof for long-term holding.

🎯 Here’s my conviction list.

$TSLA spans electric vehicles, robotics, AI, energy, manufacturing, SaaS and autonomous driving—it’s not one business, it’s an entire ecosystem.

$SOFI is banking, lending, payments, investing and fintech all converging into one platform.

$SPCX is AI, rockets, internet, manufacturing, SaaS, social and AI compute—the full stack of infrastructure.

$NVDA is AI, GPU, cloud, robotics, autonomous driving, data centers and networking—the engine that powers everything.

$PLTR combines SaaS, government work, AI, platforms and verticalization—unique positioning nobody else has.

$IREN is pure-play AI compute and cloud services.

$AMZN is retail, AWS, marketplace, streaming, subscriptions, AI and advertising—still the most diverse moat in tech.

💭 But this is just my view.

Each of these represents a different thesis—energy revolution, financial transformation, space infrastructure, chip dominance, government digitalization, AI compute and ecosystem lock-in.

📝 What would you add to this list?

What companies do you see as absolute holds for the next decade? What am I missing?

Drop your conviction picks in the comments.

1

2

727

Jun 13

$CBRS $AMZN $MRVL $GOOGL, the AI inference stack is being reinvented in real time.

🔄 Cerebras just announced a game-changing partnership with AWS that fundamentally rethinks how inference compute should be architected.

The insight is brilliant in its simplicity: let each chip do what it does best.

AWS Trainium handles the prefill phase—massive batch processing of input tokens.

Cerebras wafer-scale systems handle decode—the latency-critical phase where one token at a time gets generated.

⚡ This is not incremental optimization.

This is a paradigm shift in how agentic AI workloads get executed.

Traditional approaches force a single chip architecture to do everything. But prefill and decode have completely different computational characteristics.

Now you can optimize each pipeline stage independently.

🧠 The real insight here is deeper than just $CBRS winning a partnership.

It’s a reminder of how interconnected the entire AI stack has become.

$MRVL is designing AWS custom silicon.

Anthropic is a major customer of both $AMZN and $GOOGL, testing their infrastructure against each other.

$CBRS is now embedded in AWS’s inference strategy.

🎯 No single company owns the entire stack anymore.

Winners will be those who excel at their specific layer and integrate seamlessly with others.

This is the new competitive reality in AI infrastructure.

1

2

695

Jun 11

⠀

⚡ Strategic Positioning in AI Infrastructure Power Supply

$TE’s sharp pullback presents a critical accumulation window — the sub-$6 price point offers an ideal entry level to scale into this essential energy infrastructure provider.

Why does this correction signal opportunity rather than weakness? Four core theses support aggressive positioning:

First, Leopold Aschenbrenner’s disclosure of a $44M Q1 position in “Situational Awareness” represents a direct endorsement from one of the most credible voices in infrastructure investing — this is institutional conviction made transparent.

Second, TE stands as the only domestic operator purpose-built to deliver solar plus battery solutions specifically engineered for AI data center power demand — its existence answers the critical question of who solves hyperscale facility energy constraints.

Third, the G2 Austin solar battery facility remains on track with demand already pre-committed beyond 100% of 2027-28 production capacity — this locks in production certainty with zero downside surprise risk.

Fourth, the $32M KORE Power acquisition transforms TE from a single-product renewable supplier into a complete end-to-end energy solutions provider for hyperscale operators — integrated solutions command premium valuation in this cycle.

The thesis compresses to one immutable reality: AI expansion is fundamentally an insatiable demand for electricity.

41

Jun 10

🎯 Cathie Wood’s $ARKK Reveals What Future She’s Actually Betting On (And It’s Not What You Think)

Cathie Wood just published her entire $ARKK portfolio. And buried in the holdings is a thesis that challenges everything Wall Street believes about AI, biotech, and the future.

The Obvious: $TSLA Dominates

$TSLA is 10.22% of the fund. Twice the size of any other holding. Cathie’s conviction on Elon’s empire is absolute.

But here’s what’s interesting: it’s not because she thinks $TSLA makes the best electric cars.

The Hidden Pattern

Look at the second-largest positions: $TEM (Tempus AI) at 5.06%, $CRSP (CRISPR) at 4.95%, $HOOD (Robinhood) at 4.75%.

These aren’t mega-cap AI plays. These are specific bets on:

1.AI applied to medicine (Tempus uses LLMs to decode cancer)

2.Gene editing (CRISPR is biotech’s guillotine)

3.Democratized investing (Robinhood for retail traders)

What She’s NOT Betting On

$NVDA: 1.76%. Less than a fifth of $TSLA.

$MSFT: Nowhere on the list.

$META: 0.98%.

$GOOGL: Combined 2.48%.

Cathie has essentially abandoned the traditional AI narrative. While everyone else is chasing $NVDA’s GPU monopoly, she’s moved on.

What She’s Actually Betting On

Look at the portfolio as a whole. It’s not “AI stocks.” It’s “things that AI will transform.”

$TSLA (autonomous vehicles). $CRSP, $BEAM, $NTLA (gene editing to cure disease). $TEM (AI finding new drugs). $SHOP (AI-powered commerce). $RBLX (AI-generated worlds). $CORD (Cerebras making AI chips that don’t suck).

This isn’t a fund built on “who will dominate compute?” It’s built on “what industries will AI actually disrupt?”

The Biotech Concentration Is Telling

$CRSP, $BEAM, $NTLA, $TWST, $ILMN, $VCYT, $RXRX, $PACB.

That’s nearly 20% of the fund in gene editing and diagnostics.

Cathie’s betting that AI biotech = a bigger paradigm shift than AI software.

Because software automation is already happening. Biotech transformation hasn’t started yet.

The Crypto Angle

$COIN, $CRCL, $BLSH.

She’s not abandoning crypto. She’s just realistic: crypto itself isn’t the revolution. It’s the infrastructure for the next financial system.

Why $NVDA Is Only 1.76%

Everyone thinks Cathie missed the chip boom. Actually, she’s making a different bet.

$NVDA is a supplier. It makes the picks and shovels. But the real wealth gets created by whoever uses those picks and shovels to find gold.

Cathie’s holding the gold miners, not the tool makers.

The Private OpenAI Position

2.64% in private OpenAI tells you something: Cathie thinks the company is worth owning, but at current valuations it’s not a core conviction play.

She’s not betting on OpenAI to 100x. She’s diversifying across the entire AI ecosystem.

What This Portfolio Is Actually Saying

“AI won’t be won by whoever builds the biggest GPU. AI will be won by whoever applies it to problems that matter: curing diseases, building autonomous robots, reinventing finance, creating new forms of entertainment.”

The picks and shovels sell for billions. The mines sell for trillions.

The Risk Nobody Talks About

This portfolio is insanely concentrated. $TSLA is 10x bigger than the 10th largest holding.

One bad quarter from Tesla, and the entire fund gets crushed.

But that’s Cathie’s style: extreme conviction bets on transformative themes.

Two Years From Now

If $CRSP cures a major disease. If $TSLA’s robotaxi network scales to millions. If $ROBLOX becomes the metaverse people actually use.

Then everyone will say “of course Cathie saw this coming.”

If they don’t? Then $ARKK gets cut in half and no one remembers her thesis.

That’s the Cathie Wood special.

1

6

2,202

Jun 10

🔗 The Chip Monopoly That Could Break Space: Why SpaceX Just Went All In on Semiconductor Manufacturing

SpaceX’s CFO gave the real reason the company is building its own chip factory. Two words: supply chain risk.

The Hidden Fragility

Everyone thinks the semiconductor market is competitive. $NVDA dominates GPUs. Tesla designs custom AI5 chips. Google builds TPUs. Amazon has Trainium. Intel still exists.

Look closer and you see the truth: all of them flow through one bottleneck.

Taiwan. TSMC. One fab. One company. One point of failure for the entire AI infrastructure buildout happening right now.

The Supply Chain Illusion

$NVDA designs the chips. TSMC makes them. $TSLA designs AI5. TSMC makes them. $GOOGL designs TPUs. TSMC makes them.

The names change. The manufacturer doesn’t.

For years this worked fine. But then SpaceX decided it needed 100 gigawatts of compute deployed across space and Earth over the next few years.

That’s not incremental demand. That’s epoch-making demand.

And TSMC? They can’t keep up. They’re already supply-constrained. Every chip maker is competing for queue time. Gaming companies. $MSFT. $AMZN. $TSLA. Everyone.

SpaceX can’t afford to wait. Can’t afford to get bumped in the queue. Can’t afford the single point of failure.

Why This Changes Everything

SpaceX partnered with Intel. They’re building their own superscale foundry.

Not to beat TSMC at making chips. But to guarantee they never run out.

This is vertical integration at the infrastructure level. SpaceX doesn’t just want chips. SpaceX wants to own the supply.

The Cascading Risk Nobody Talks About

If TSMC ever gets disrupted—geopolitical tension with China, natural disaster, internal issues—the entire AI infrastructure boom stops.

Not slows. Stops.

$NVDA can’t ship GPUs. $GOOGL can’t deploy TPUs. $TSLA can’t scale Optimus. Cloud providers can’t expand capacity.

One fab. One island. One company. One catastrophic failure point for the global AI economy.

SpaceX is saying: not on our watch.

The Economic Play

SpaceX builds chips for itself. But here’s what happens next: it has excess capacity.

Suddenly SpaceX becomes a chip supplier. Competing with TSMC not on cutting-edge nodes, but on availability, pricing, and speed of delivery.

$TSMC charges premium prices because they’re the only game in town.

SpaceX can undercut them because SpaceX’s primary customer is itself. The foundry is just captured margin.

What This Means for the Ecosystem

Intel gets a lifeline. SpaceX gets supply security. The broader industry gets a second source.

And TSMC? They still win, but they lose the monopoly pricing power.

The Bigger Picture

Every AI infrastructure company is going through this realization: you can’t build scale if you’re dependent on one supplier.

Microsoft is designing chips. Amazon is designing chips. Google is designing chips. Tesla is designing chips.

But designing isn’t enough. You need to manufacture. And manufacture at scale.

SpaceX just connected those dots publicly.

Within two years, expect to see $MSFT, $AMZN, $GOOGL all announce foundry partnerships or build plans.

The era of “TSMC makes everyone’s chips” is ending.

The era of “we make our own chips” is beginning.

SpaceX’s CFO said it in two words: supply chain risk.

But it really means: never again will one company control the infrastructure that powers your company.

1

3

599

Jun 10

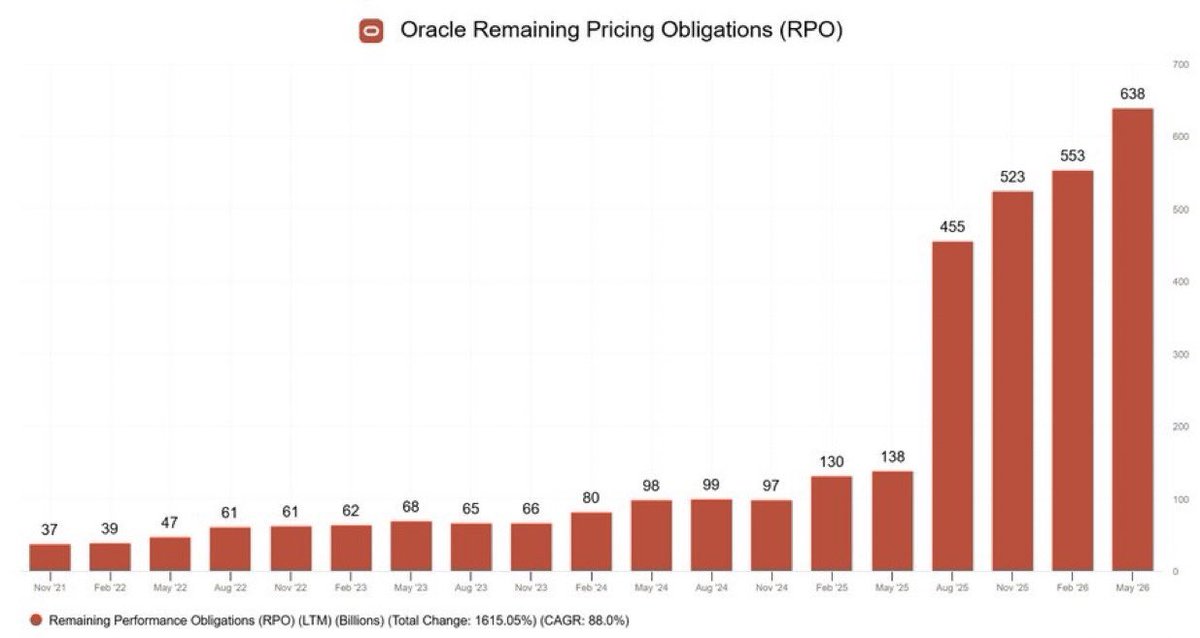

💰 Oracle’s Customers Are Financing Its AI Empire (And They Don’t Even Know It)

$ORCL just revealed something stunning buried in the earnings call. Customers already committed to $750 billion in infrastructure spending. Oracle’s $400 billion financing plan? Turns out it’s undersized.

The Real Numbers

RPO exploded. Backlog increased $85 billion quarter-over-quarter. OCI acceleration hit 93% growth in Q4.

But here’s the kicker: orders are leading conversions by a 4:1 ratio.

Translation? For every dollar of revenue Oracle books today, they have four dollars already committed from customers waiting in the pipeline.

Why This Changes Everything

Oracle didn’t announce a $400 billion capex plan and then scramble to fund it.

Oracle announced it, and customers voluntarily committed $750 billion to pay for it.

This isn’t a company begging the market for capital. This is a company where demand is so extreme that customers are literally pre-paying for infrastructure that doesn’t exist yet.

The RPO Play

RPO is the most underrated metric in enterprise software. It’s cash you’ve already earned but haven’t booked yet.

$ORCL’s RPO growing at this rate doesn’t mean sales are strong. It means sales are so strong that the company can’t convert them into revenue fast enough. The backlog is the real story.

What OCI 93% Growth Actually Means

Cloud infrastructure growing at 93% while still being 1/10th the size of $MSFT’s Azure or $AMZN’s AWS? That’s exponential trajectory.

But OCI 93% growth RPO 4:1 ratio means Oracle has visibility into the next 4 quarters of customer commitments. That’s certainty. That’s predictability.

$MSFT has massive cloud revenue. $AMZN owns the market. But do they have $750 billion in pre-committed customer spending waiting to convert?

The Financing Plan Is Actually Irrelevant

When people heard “Oracle raises $400 billion for AI infrastructure,” the market yawned. “That’s a lot of debt.”

But the real story is the opposite. Customers already committed $750 billion. Oracle’s $400 billion raise is to fill the gap between when it builds infrastructure and when customers pay for it.

Oracle isn’t funding this capex. Customers are. Oracle is just managing the cash timing.

The Competitive Implication

$MSFT is spending hundreds of billions on chips, datacenters, AI partnerships. Burning cash on ambition.

$ORCL is spending money that customers already promised to pay for. The economics are completely different.

Why Wall Street Is Sleeping on This

Analysts are focused on revenue guidance. Revenue growth. Margins.

But RPO growth OCI acceleration $750 billion pre-commitment = a company with visibility 4 quarters out. That’s not just growth. That’s a printing press.

Two Years From Now

$ORCL’s 2028 guidance isn’t a prediction. It’s reading the RPO backlog and doing math.

While competitors are guessing about enterprise AI adoption, $ORCL already has the signatures on the contracts.

That’s why the $400 billion financing looks small. Because it is. Customers are already paying for it.

1

1

765

Jun 10

🔥 $Tesla Just Quietly Won the AI Chip Efficiency Game (And Nobody Noticed)

Tesla’s AI6 chip design review just came back. The engineering verdict: exceptional. And there’s one detail buried in there that changes everything.

Maximum usable intelligence per wafer. Record-breaking yields.

Let that sink in.

Why This Matters More Than $NVDA’s Next GPU Drop

Everyone obsesses over $NVDA’s H100, H200, Blackwell specs. Raw compute numbers. TFLOPS. Bandwidth.

But here’s what most investors miss: the real constraint isn’t peak performance. It’s efficiency. Cost per trillion operations. Yields from the fab. Power consumption. Thermal density.

If Tesla’s AI6 can extract more usable compute from each wafer than anyone else, that’s not just a win. That’s a structural advantage.

The Yield Play

A 5% difference in wafer yield sounds technical. But economically? It’s massive.

If $TSLA gets 95% good chips and competitors get 90%, Tesla’s cost per chip just undercut everyone else by that exact margin. That advantage compounds across millions of chips.

What This Enables

Optimus robots need cheap, efficient AI chips. Robotaxis need distributed intelligence at scale. Dojo training clusters need maximum compute density in minimal power envelope.

If Tesla can make AI6 chips 10-15% cheaper than competitors while maintaining performance, suddenly the economics of physical AI become viable.

Competitors need to make margin. Tesla can undercut them, take market share, and still stay profitable because of superior yields.

The Supply Chain Angle

Tesla doesn’t need to buy $NVDA GPUs for Optimus. It doesn’t need to negotiate with TSMC for capacity. It’s building its own silicon advantage.

This is exactly what $MSFT, $GOOGL, and $AMZN are trying to do with custom silicon. But Tesla just proved it can do it better.

What Wall Street Will Miss

When Tesla announces AI6 chips powering the first 1 million Optimus units, investors will focus on robotics unit economics.

The real story is buried deeper: Tesla just became a semiconductor advantage company. That changes the entire valuation framework.

This is the kind of announcement that looks boring in the moment. But two years from now, it’ll be obvious this was the inflection point where Tesla shifted from “buying intelligence” to “manufacturing intelligence.”

That changes who wins in the AI era. And spoiler: it’s not always the company with the biggest chip.

115

Jun 10

🤝 Oracle Just Became OpenAI’s Most Powerful Distribution Channel

$ORCL partnering with OpenAI to embed frontier models directly into OCI. This isn’t just a technical integration. This is a power play.

The Real Story Here

Oracle isn’t competing with OpenAI anymore. Oracle is becoming OpenAI’s enterprise sales force.

Think about what $ORCL controls: thousands of enterprise customers. Legacy database dominance. Deep relationships with CFOs and CIOs who’ve been using Oracle for 20 years.

Now those customers don’t have to build their own AI infrastructure or negotiate directly with OpenAI. They flip a switch in their existing OCI dashboard. Instant access to GPT-4o, o1, the latest frontier models.

Why This Matters More Than People Think

$MSFT already did this. They embedded OpenAI into Azure. But Azure still feels like Microsoft’s product with OpenAI as a feature.

$ORCL is doing something different. They’re saying “your data, your AI infrastructure, your models.” Oracle becomes the trusted middleman for enterprises that don’t want to bet their whole stack on $MSFT.

The Architecture Shift

For years, the narrative was: “Who builds the best AI models?”

The new narrative is: “Who gets access to AI models that enterprises actually trust?”

$ORCL’s enterprise relationships are deeper than $MSFT’s in many verticals. Banking. Insurance. Pharmaceuticals. Government. These industries don’t just need AI. They need AI that plays nice with their existing databases, compliance frameworks, security protocols.

Oracle knows how to sell to these institutions. OpenAI doesn’t.

What This Does to Valuations

$ORCL already trading at reasonable multiples for its revenue growth. Now add a new revenue stream: sitting between enterprises and frontier AI models, taking a cut of every API call.

This is margin expansion without heavy capex. Pure software economics.

The Competitive Implication

$GOOGL is still trying to convince enterprises that Gemini is better than GPT-4o. Good luck.

$AMZN is building Bedrock as a universal playground for all models. But does anyone trust $AMZN with their critical database infrastructure? Not really.

$ORCL? They already have the trust. Now they have the product.

Two Years From Now

Analysts will look back and say “Why didn’t we see this?” Oracle didn’t need to beat OpenAI. Oracle just needed to become the unavoidable middleman for enterprise AI adoption.

$ORCL’s guidance for 2028 is already being powered by this deal. Cloud margins tick up. Enterprise AI spending accelerates. And every dollar of that spending flows through Oracle’s pipe.

This is how $ORCL competes in the AI era. Not by building better models. By being the only platform enterprises already depend on.

1

1

646

Jun 10

💎 The Hidden Play: Why Smart Money Buys $TSLA When Everyone’s Chasing $SPCX

When the entire world is mesmerized by $SPCX’s IPO, the real opportunity is happening in the shadows.

The Attention Trap

$SPCX hits the market. The narrative is intoxicating. Mars colonization. Orbital computing. Satellite internet. Every headline screams “the future.”

Retail money floods in. $SPCX’s valuation gets stretched to absurd levels. Institutional money drives it higher. Media covers every launch.

Meanwhile, $TSLA gets dumped. “Old story,” they say. Electric vehicles. Energy storage. Yesterday’s news. No one cares.

But Here’s What They’re Missing

$TSLA shareholders think they own a car company. They actually own a piece of $SPCX’s upside.

Elon doesn’t run two separate businesses. He runs one integrated empire.

$TSLA’s cash flow funds $SPCX’s expansion. $SPCX’s satellite network becomes $TSLA’s global connectivity layer. Optimus robots use the same supply chains. The computing infrastructure is shared across both companies.

The Ecosystem Arbitrage

When $SPCX trades at 50x revenue on IPO euphoria, smart money is quietly accumulating $TSLA at a 40% discount.

Why? Because they understand the hidden equation:

Buy $TSLA at basement prices. Get exposure to $SPCX’s growth without paying IPO premiums. Win on both sides when the market finally realizes these companies are one.

Two Companies, One Thesis

$TSLA’s energy system powers $SPCX’s ground infrastructure. $SPCX’s orbital compute enhances $TSLA’s autonomous driving algorithms. When Starlink covers the planet, every $TSLA vehicle suddenly has global real-time connectivity.

The market prices them separately. Smart investors price them as a bundle.

The Timing Game

Day 1 of $SPCX IPO: Everyone chases the hot stock. Valuation balloons. $TSLA gets left behind.

Year 2: $SPCX’s growth numbers come in strong. But $TSLA has quietly doubled while no one was watching. Because you didn’t just buy a car company. You bought the entire Elon ecosystem at a 60% discount.

This is the game. And most investors are playing it exactly backwards.

1

70

Jun 10

June 9, 2026 — Mega Cap Watchlist

1.$MU — Post-sell bounce setup; HBM still supply-constrained; June 24 earnings catalyst incoming. [BUY]

2.$MRVL — Custom AI silicon demand accelerating; photonics and datacenter interconnect exposure; Jensen lift. [BUY]

3.$QCOM — AI chip race heating up; datacenter upside limited. Jensen lift. [BUY]

4.$INHD — Small-cap speculation play; pump and dump. [SELL]

5.$DRAM — Storage ETF sold off hard with broader chip sector last week; reversal setup forming. [BUY]

6.$ORCL — AI cloud infrastructure beneficiary; database moat intact; steady compounding. [HOLD]

7.$AAOI — Optical interconnect play; AI datacenter bandwidth demand structurally bullish. [BUY]

8.$NVDA — Holding support in Broadcom-induced selloff; AI accelerator demand remains structural. [HOLD]

9.$ARM — License revenue scales with every AI chip design; dips are gifts. [BUY]

10.$AVGO — Q3 AI miss sparked 12% drop; $100B full-year AI guidance intact; classic sell-the-fact overreaction. [BUY]

11.$IONQ — Pulled back hard from $84 52-week high; quantum sentiment volatile but long-term thesis unchanged. [HOLD]

12.$ASTS — Low-earth orbit connectivity thesis intact; high-beta, wait for clean entry in strength. [BUY]

13.$RKLB — Space infrastructure play gaining contract momentum; pullback from highs offers better entry. [BUY]

14.$NBIS — Bank of America raised target to $280 today; announced $1.7B UK expansion; 684% YoY revenue growth. [BUY]

15.$META — Recently sold off ~4% on $80B AI capex news; long-term infra commitment is actually bullish. [BUY]

16.$MSFT — AI Copilot monetization accelerating; hyperscale capex commitment supports earnings growth for years. [BUY]

17.$AAPL — Lagging the AI cycle narrative; holding support but no near-term catalysts, patience required. [HOLD]

18.$INTC — Crashed in recent selloff; turnaround story long and painful, waiting for real catalyst. [BUY]

♻️ RT this and drop 1 comment — I’ll DM you which $SPY contract to swing on tomorrow’s CPI.

74

Jun 7

🎯 The Bubble Narrative Doesn’t Match the Math: 2027 Forward Earnings Multiples Tell a Different Story

Market commentators keep repeating the same refrain—we’re living through excessive valuations, irrational exuberance, another bubble waiting to pop.

Then you look at what corporations are actually trading for, based on projected 2027 profitability. The numbers paint a strikingly different picture.

Enterprise Software & Cloud

$ORCL trades at roughly 26x forward earnings. $MSFT sits around 22x. $NOW occupies similar territory at 22x. These aren’t exactly the multiples you’d expect if the market had gone completely unhinged.

E-Commerce & Cloud Infrastructure

$AMZN hovers near 25x forward valuation. $GOOGL lands in the same zone at 25x. Both control enormous market shares and generate stupendous cash flow, yet the market hasn’t assigned them astronomical multiples.

Semiconductors Across the Spectrum

$NVDA, the most feared name in artificial intelligence hardware, trades at merely 16x 2027 earnings. $TSM, the world’s only company capable of manufacturing cutting-edge processors, comes in at 19x. $SNDK, riding a data center explosion, sits at just 9x. $MU, the bottleneck everyone suddenly cares about, trades at an absurdly cheap 8x.

Networking & Infrastructure

$AVGO anchors at 20x. $DELL, the server powerhouse, occupies 19x territory.

Social Media & Advertising

$META, after its AI reinvention narrative took hold, trades at 16x forward earnings.

Business Software Legacy

$CRM, the legacy player in enterprise relationship management, commands only 12x multiple.

What This Actually Means

A genuine bubble features companies with razor-thin or negative near-term profits trading at astronomical multiples—the dot-com crash featured stocks worth hundreds of times sales with zero earnings visibility.

Today’s largest corporations, responsible for trillions in global economic activity, are being valued at modest single-digit to low-twenties multiples of their coming years’ earnings.

That’s not irrational. That’s restraint masquerading as skepticism.

33

Jun 7

💾 Taipei’s Message Is Clear: Memory Chips Have Become AI’s Ultimate Bottleneck—Four Entry Points Open Now

At an industry gathering in Taipei, the chief executive of graphics processing technology unveiled a critical constraint on artificial intelligence’s expansion: semiconductor memory availability and capacity are the binding limitation.

Elon Musk, who leads Space Exploration Technologies, voiced alignment with this assessment. Infrastructure suppliers like Dell’s leadership echoed the same conclusion. Even top-level policymakers have publicly indicated interest in accumulating positions in related assets.

From Taipei to Washington, from entrepreneurs to government officials, every signal points in one direction.

Opportunity One: $MU — America’s Sole Listed HBM Manufacturer

The compute cores powering AI servers depend on this chipset architecture.

Suggested accumulation zone: $600-$650 range.

The catalyst emerges from a pullback off historical peaks, with earnings disclosure expected around June 24th—market repricing typically clusters around such event dates.

Opportunity Two: $DRAM — Basket Exposure to Global Memory Supply Ecosystem

This exchange-traded vehicle offers broad-based access to the worldwide storage industry network.

Suggested accumulation zone: $40-$45 range.

Holdings span Samsung, SK Hynix, and Micron—sector heavyweight names—offering complete industry participation at relative discounts.

Opportunity Three: $WDC — Storage Infrastructure for AI Data Centers

Hard disk configuration remains essential to server system architecture.

Suggested accumulation zone: $380-$400 range.

From calendar year start through present, valuations have climbed threefold. Current positioning rests near critical technical support—a zone typically offering favorable re-entry mechanics.

Opportunity Four: $SNDK — Pure-Play NAND Flash Leadership

This enterprise’s data center storage revenue expansion reaches 645% year-over-year growth velocity.

Suggested accumulation zone: $900-$1,000 range.

Relative to historical peaks, remaining downside amounts to approximately 25%—next earnings publication could catalyze renewed valuation expansion.

Taipei’s dialogue reveals this cycle’s most constrained resource. And that constraint maps directly onto four directional opportunities for advance positioning.

48

Jun 6

🎯 Fibonacci Support Levels for 2026’s Leading Tech Stocks

Photonics Wave Holding Key Levels

$AAOI — $174

$AXTI — $79.3

$LITE — $817

$COHR — $354

$GLW — $177

$LWLG — $9

$LASR — $56.5

Space Economy Momentum Intact

$RKLB — $103.5

$ASTS — $90.3

$VOYG — $40.6

$PL — $32

These aren’t random numbers. Fibonacci retracement identifies where institutional buyers historically step in after pullbacks. If these levels hold, consolidation is healthy. If they break, recalibrate your thesis entirely.

Photonics and space are structural tailwinds for the next 5 years. Support levels tell you where patience gets rewarded.

188

Jun 6

🚀 One sentence from Jensen Huang just unlocked the U.S. tech playbook⠀

“I came to Korea because business here is booming… and this is only the beginning”⠀

That’s not small talk⠀

That’s admission: American tech penetration in Asia is still early innings⠀

Global expansion runway still massive⠀

My June execution blueprint⠀

$TSLA Tesla | Buy $380 → Target $620⠀

$SOFI SoFi | Buy $15.5 → Target $41⠀

$NVDA NVIDIA | Buy $200 → Target $308⠀

$PLTR Palantir | Buy $132 → Target $280⠀

$MSFT Microsoft | Buy $410 → Target $650⠀

$NOW ServiceNow | Buy $110 → Target $260⠀

$AMD AMD | Buy $455 → Target $680⠀

$MU Micron | Buy $850 → Target $1,680⠀

$DELL Dell | Buy $385 → Target $610⠀

Here’s the pattern⠀

Each wave of U.S. tech going global = 2-3x returns⠀

Smartphones (2010-2015) ✓⠀

Cloud infrastructure (2015-2020) ✓⠀

AI chips (2020-2025) ✓⠀

Now: AI cloud semiconductors hitting Asia simultaneously⠀

That’s never happened before⠀

The Korea comment tells you: market still priced for 70% North America saturation⠀

When the other 30% onboards? These nine names benefit disproportionately⠀

1

64

Jun 6

🎯 The Fastest Path to $3M by End of 2028⠀

I’ll only say this once⠀

Here’s the portfolio structure that could accelerate wealth multiplication in the next 30 months⠀

$INTC Intel → $93 Core Buy⠀

$TSLA Tesla → $383 Core Buy⠀

$NOK Nokia Oyj → $12 Core Buy⠀

$NVDA NVIDIA → $198 Core Buy⠀

$AVGO Broadcom → $382 Core Buy⠀

$MU Micron Technology → $850 Core Buy⠀

$MRVL Marvell Technology → $258 Core Buy⠀

Why these seven?⠀

They’re positioned at the intersection of three mega-trends⠀

1 AI infrastructure buildout (still in innings 2-3)⠀

2️⃣ Global tech expansion (emerging markets still underpenetrated)⠀

3️⃣ Supply chain consolidation (winners taking 70% share)⠀

People ask why I don’t monetize this as paid content⠀

Simple: I’m not financially stressed⠀

Sharing investment insights is a hobby, not a revenue line⠀

The math on these seven plays the longer you hold, the clearer the thesis becomes⠀

2028 will be a very different valuation landscape than today⠀

180

Jun 2

⏰ I’ll Say This Only Once

This might be the fastest path to $1M by end of 2028.

You hear me loud and clear: only saying this once.

🎯 Six Stocks, One Time Window

$INTC (Intel)

Target: $115

Thesis: Chip manufacturing localization, advanced process node catch-up, government support

$CRCL (Circle)

Target: $106

Thesis: Stablecoin infrastructure, payment settlement networks, crypto compliance maturity

$NOW (ServiceNow)

Target: $95

Thesis: Enterprise AI workflow automation, SaaS platform momentum, AI Agent integration

$ASTS (AST SpaceMobile)

Target: $100

Thesis: Satellite communications, low-earth orbit internet, coverage of unserved markets

$MU (Micron Technology)

Target: $740

Thesis: AI data center memory bottleneck, HBM supply scarcity, sustained pricing power

$AMD (Advanced Micro Device)

Target: $455

Thesis: CPU GPU dual engines, EPYC server dominance, MI AI accelerator ramp

💡 Why These Six?

Two interlocking narratives:

【AI Infrastructure Stack】$MU / $AMD / $INTC / $NOW

Storage, compute, manufacturing, application automation—complete end-to-end chain.

As AI transitions from R&D to commercial deployment, all four layers see synchronized demand.

【Emerging Infrastructure】$ASTS / $CRCL

Space communications and crypto payments—seemingly unrelated, but fundamentally building next-gen infrastructure.

⚡ The Window Is Everything

From now through end of 2028—not one year, not two, but just over two years.

This window is long enough for:

AI chip demand explosion to flow through P&Ls

Intel’s process node roadmap to show meaningful results

Satellite constellation deployment to shift from project to commercial scale

Stablecoin infrastructure to achieve regulatory completeness

ServiceNow’s AI Agent capabilities to achieve enterprise lock-in

⚠️ This Is Not “Possible”

This is “inevitable.”

“Must buy” means:

These aren’t investment options—they’re supply chain necessities.

If AI growth continues, demand for these companies doesn’t stop.

If space connectivity scales, LEO satellite coverage acceleration is structural.

If payment systems modernize, stablecoin rails must be built out.

🎪 The $1M Path

Say you start with $100K today, equally weighted across these six.

By end of 2028, if these price targets materialize:

$INTC → $115 upside capture

$CRCL → $106 upside capture

$NOW → $95 upside capture

$ASTS → $100 upside capture

$MU → $740 upside capture

$AMD → $455 upside capture

These targets aren’t pulled from thin air.

They’re derived from supply constraints, demand acceleration, and market repricing.

🔔 Why I Say This Only Once

Because:

Either you believe now and act.

Or you wait until these narratives get mainstream pricing, and then it’s already expensive.

Just over two years is not that long—long enough for every thesis to play out, short enough that repricing still has room to run.

There’s no point saying this twice.

Only action or regret from here.

249

Jun 2

📈 The 1999 Playbook Is Replaying in the AI Era

Remember the thesis from May 7th?

When storage kicked off, I said the next phase would favor optical interconnect and high-speed networking, with specific focus on $MRVL and $ALAB.

Computex just validated that this logic is now being recognized by an expanding circle of investors.

💡 Why Focus Shifted from GPU Count to Connectivity

The market used to obsess over GPU quantity.

But when AI clusters scaled from thousands of cards to tens of thousands, then hundreds of thousands, the problem transformed.

The bottleneck is no longer raw chip performance.

It’s how data flows efficiently through the entire system.

The larger the compute footprint, the more demanding the requirements for network architecture, switching capacity, and high-speed interconnect.

129

Jun 1

Breaking: Jensen just said what Claude's been saying about ServiceNow $NOW the entire time

"Agents are going to create the largest opportunity ever for my partners ($NOW)"

Claude first bought on April 10th: $83.00

Now: $134.00

243

Jun 1

🚨Why is $CRDO down ~16% after strong earnings? A classic “AI infrastructure expectations reset” move

At first glance, the reaction looks disconnected from fundamentals:

Revenue: $437M vs $433M expected ( 157% YoY)

EPS: $1.16 vs $1.00 expected ( 231% YoY)

Guidance: raised for revenue and gross margin

Yet the stock sold off sharply.

This is not unusual in the current AI infrastructure cycle. In fact, it is increasingly becoming a pattern.

🧠 1. Strong results are no longer enough in “AI infra beta” stocks

$CRDO sits in a very specific category:

high-growth AI networking / interconnect exposure

deeply tied to hyperscaler capex cycles

valuation heavily driven by forward expectations, not current results

In this regime, the market is no longer reacting to whether numbers are “good” or “bad”.

It is reacting to whether:

👉 expectations were already too aggressively priced in.

⚡ 2. The “beat-and-sell” structure is a feature, not a bug

What you are seeing is a typical high-beta AI infrastructure behavior:

stock runs ahead of earnings

expectations get stretched

earnings come in strong

but “not strong enough vs positioning”

stock de-risks sharply

This does not necessarily reflect deteriorating fundamentals.

It reflects:

👉 positioning narrative compression

🧩 3. Why guidance raises did not prevent the selloff

Even though guidance was raised, the key issue is:

The market is no longer pricing CRDO on near-term guidance alone.

It is pricing:

long-term SiPh adoption curve

AI cluster scaling (1.6T → 3.2T roadmap exposure)

competitive intensity in optical interconnect

So even positive revisions can feel “insufficient” if:

👉 forward multiples already assume hyper-growth continuation.

🔌 4. The real underlying driver: AI networking is becoming a crowded consensus trade

CRDO sits in the same mental bucket as:

optical interconnect / silicon photonics

AI data center networking bottlenecks

hyperscaler capex beneficiaries

This category has recently experienced:

strong multi-month rerating

crowded positioning

sharp factor rotation sensitivity

So when sentiment shifts even slightly, volatility expands quickly.

📊 5. Your entry at ~$192 fits a common “post-earnings reset” pattern

What often happens in these names:

stock runs into earnings

expectations peak

post-earnings volatility flush

long-term buyers step in on reset valuation

next leg depends on capex cycle continuation

The key question is not the single print.

It is whether:

👉 AI infrastructure buildout (networking SiPh optical scaling) continues to accelerate or normalize.

🧠 Bottom line

$CRDO is not reacting like a “fundamentals broke” story.

It is reacting like a:

“high-expectation AI infrastructure compounder undergoing positioning reset”

Strong earnings in this regime do not guarantee upside.

They simply determine whether the next move is:

continuation

or

consolidation before next leg

1

160