Earn stable, transparent, real yields on your stablecoins backed by Asia Credit

Joined February 2024

- Tweets 1,553

- Following 363

- Followers 14,745

- Likes 3,404

382 Photos and videos

Pinned Tweet

24 Nov 2025

🚨 Mu Digital is LIVE 🚨

We provide your access gateway to unlock Asia's $20 trillion credit market. Investments previously reserved for institutions and high net worth individuals can now be accessed onchain.

We offer two ways to earn:

🐂 Asia Dollar (AZND): for users looking for capital preservation

🐂 muBOND: for users looking for yield amplification

All products backed by Asia governments and corporations. Deal sourcing by ex–investment bank executives who seek to ensure the highest level of risk management, transparency and safety.

Our products are DeFi composable with a number of exciting product integrations underway.

Powered by @monad

Check us out here: app.mudigital.net

22

16

111

41,018

➥ Project Spotlight - Week 23/2026

Here are 9 handpicked projects you'll want to explore.

➢ @prism_lp

➢ @MarketCardsHQ

➢ @ZEITFinance

➢ @MuDigitalHQ

➢ @zipcodenetwork

➢ @unimarketsdotio

➢ @AskSurplus

➢ @Raflux_io

➢ @TheGachaGrid

Powered by @getmoni_io and @_dexuai

Below you will find brief summaries for each.

Let's dive in!

…

— 📌 | Prism

Prism powers Spectrum, the launchpad for creating on-chain index tokens/ETFs (AI baskets, TCG cards, gold, BTC, stocks, and more). Creators earn 30% of fees forever, and trading fractionals burns facets, making the system deflationary. Recently launched BaseAI index by @IroraCapital and Base Inference Growth Index.

Hold $PRISM and automatically earn ~60% of fees 5,000 NFT “facets” that represent protocol ownership.

…

— 📌 | Market Cards

Market Cards is an on-chain platform for fractional ownership of high-value real-world sports & TCG cards. Users can trade slices of expensive graded cards (e.g. one-of-one Superfractors) with instant liquidity instead of waiting for full buyers.

…

— 📌 | Zeit

Turns prediction markets into perpetual, composable DeFi assets. Creators tokenize any belief/view into vault tokens (EIP-4626 based) with mark-to-market valuation, on-chain transparency (Arweave reports), omnichain redemption (LayerZero), variable fees paid in vault tokens, and built-in liquidation engine. Like structured ETF-style epochs for prediction market exposure.

…

— 📌 | MuDigital

Real-yield product where you deposit stablecoins and earn stable, transparent yields backed by Asia Credit (real-world credit assets from the fastest-growing global market), recently partnered with Pendle for advanced yield strategies.

…

— 📌 | ZipCode

Zipcode is Bittensor Subnet 46, the Real Estate Intelligence & Finance Network. Building real estate data oracles, property intelligence, and infrastructure to unlock on-chain RWA/tokenization at scale. Includes a sync engine for real estate data.

…

— 📌 | Unimarkets

Unimarkets is a Prediction markets aggregator, positioned as “the Bloomberg terminal for global prediction markets.” Helps users discover, compare, and allocate across prediction markets worldwide.

…

— 📌 | Surplus

Decentralized spot marketplace for AI inference built by @mac_eth. Buy frontier model inference (Claude, OpenAI, etc.) at big discounts or earn by selling your unused compute/GPUs.

…

— 📌 | Raflux

Raffle marketplace for TCG collectors on Base. Win graded cards (slabs), crypto, and more via fair Chainlink VRF raffles. Focused on high-end Pokémon and other TCG slabs.

…

— 📌 | Gacha Fund

Weekly “Gacha Grid” where seat taxes/fees accumulate into a pot. Every Friday they rip Slab packs (graded TCG cards) with the fees. Flywheel: Pull slabs → cards go to Dutch auction for seat holders (price drops up to 15%) → unsold return to Slab → all revenue buys & burns $GACHA. Pure deflationary loop.

22

8

268

9,300

Mu Digital retweeted

Jun 5

Morpho is quietly becoming the universal backend for onchain credit instruments and exotic stablecoins 🦋

Here are some interesting assets that been shipped in the last few months that you probably missed:

- $pathUSD as @tempo 's native stablecoin and gas fee token

- @deel upcoming stablecoin

- @coinbase lending market in the background

- $mf-ONE from @MidasRWA , tokenizing @FasanaraDigital's private credit instrument

- $muBOND is a token from @MuDigitalHQ , focused on Asian-based fixed income assets onchain, like bonds and credit instruments

- solana:3b8X44fLF9ooXaUm3hhSgjpmVs6rZZ3pPoGnGahc3Uu7 a warehouse lending facility for HELOCs (home equity lines of credit) originated by @FigureMarkets

- $wjAAA wrapped version of JAAA (Janus Henderson's tokenized AAA CLO fund on @centrifuge ), offering high-quality, floating-rate AAA collateralized loan obligations

very interesting growth, and i can see you guys extrapolating where this is going next

1

2

18

4,821

Mu Digital retweeted

12

11

72

20,738

Mu Digital retweeted

Jun 2

Asian credit is now a tradeable fixed-income asset onchain.

In this article, we break down how Mu Digital's $AZND tokenizes Asian sovereign and corporate credit, while @Pendle_fi unlocks yield trading and fixed-rate strategies.

Read the full guide 👇

coingecko.com/learn/mu-digit…

16

24

61

11,261

Mu Digital retweeted

May 29

Private Credit is starting to look like one of the most important RWA categories in DeFi.

But the interesting part is not just TVL. It is how different the top protocols already look.

@centrifuge is still the clear scale leader with around $1.38B TVL, $5.15M fees in the last 30 days, and ~$412K revenue. Large TVL, real fee activity, and multi-chain distribution across 10 chains make it the center of gravity for private credit today.

@HastraFi is the interesting growth case. It already has ~$374M TVL and generated ~$1.46M fees in 30 days, but reported revenue is still $0. That does not mean the model is weak. It likely means the protocol is still prioritizing growth, yield pass-through, and distribution before revenue capture.

@Securitize is smaller by TVL at ~$196M, but its revenue quality stands out. It generated ~$613K fees and ~$112K revenue in 30 days, with deployment across 13 chains. That suggests a different kind of strength: institutional rails, broad distribution, and better revenue capture relative to fees.

@KAIO_xyz and @MuDigitalHQ show the long tail is also worth watching. KAIO is still small, but fees equal revenue. Mu Digital has only ~$19M TVL, yet generated ~$243K fees in 30 days, which is unusually high relative to its size.

So the real signal is simple: Private Credit is no longer just one RWA bucket. It is becoming a real DeFi market with different winners in different layers.

⭢ Centrifuge leads on scale.

⭢ Hastra shows strong growth and fee activity.

⭢ Securitize looks stronger on revenue capture.

⭢ KAIO and Mu Digital show smaller players can still compete through efficiency and higher fee intensity.

That is why Private Credit is more interesting than tokenized bonds right now. Bonds have more market cap, but Private Credit has more DeFi behavior.

It has credit risk, duration, collateral structure, repayment risk, yield sources, and revenue models that DeFi can actually price, split, route, and rebuild into new products.

The next RWA winners may not be the protocols with the biggest TVL alone. They will be the ones that can turn real-world credit into active onchain markets.

Data via @DefiLlama

May 26

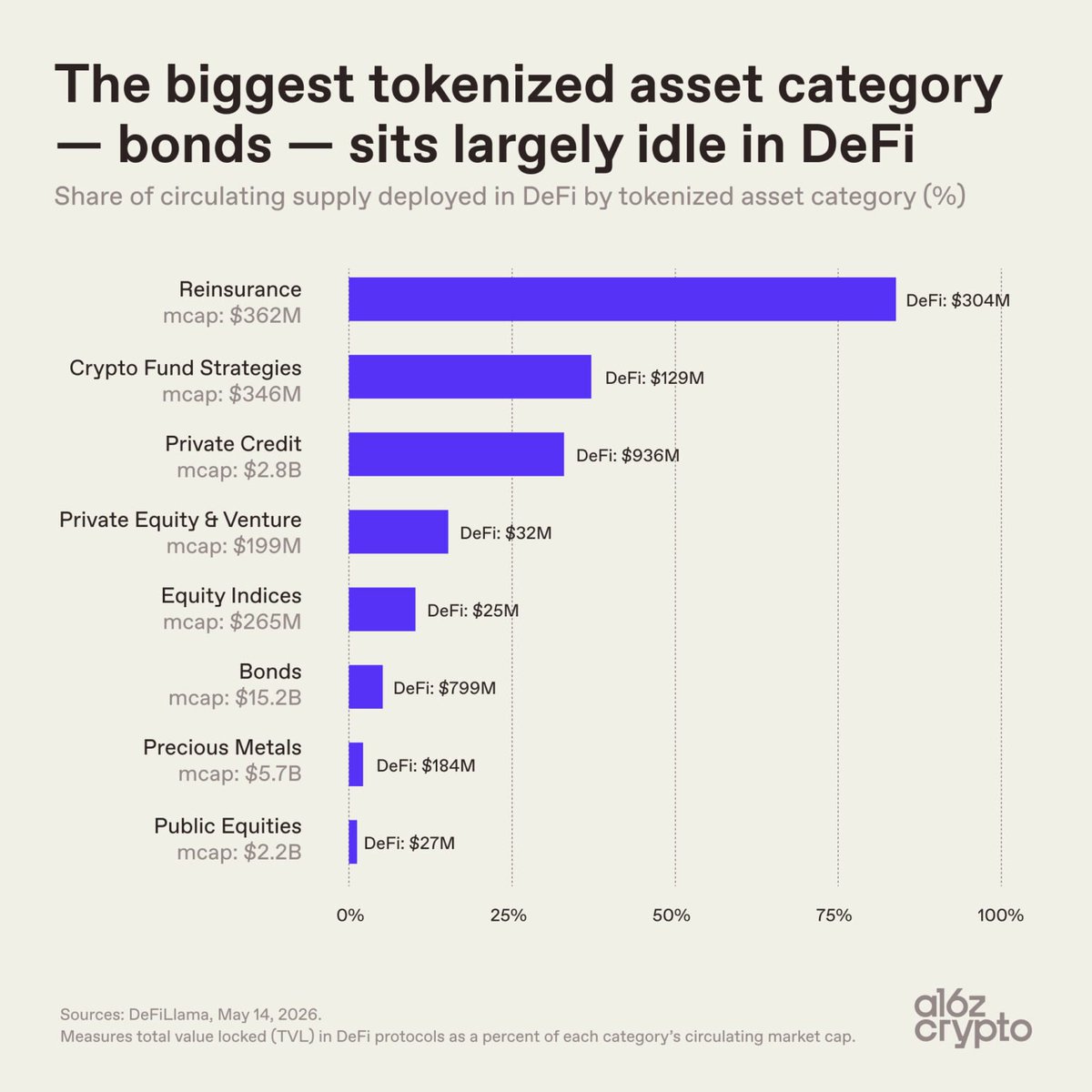

Not every tokenized asset is equally onchain.

Bonds are by far the largest tokenized asset category with $15.2 billion in market cap. But only about 5% of that supply is being used in DeFi. Precious metals look similar: they’re onchain, but mostly just sitting there.

Smaller categories look different. Reinsurance tokens have 84% of their supply deployed in DeFi, while private credit sits at 33%. This makes sense: The categories with the highest DeFi usage were built for DeFi from the start, through protocols like Nexus Mutual and Maple Finance.

Much of what gets called “tokenization” today is actually closer to digitization: moving records onto blockchains without unlocking much more new functionality. This matters because one of the core value propositions of onchain financial systems is composability.

40

6

72

4,914

May 27

Asia is the new yield frontier

@CoinGecko just covered how Mu Digital and @pendle_fi are bringing Asian credit yield onchain

🐂 PT-loAZND → fixed yield

🐂 YT-loAZND → leveraged yield trading

Full article:

coingecko.com/learn/mu-digit…

7

8

39

6,389

Stablecoins are evolving into yield-bearing financial products.

Private credit, reinsurance, Treasuries, institutional lending all becoming accessible onchain through @RWAFoundation_ members products.🔥

@plumenetwork @onrefinance @MuDigitalHQ @Securitize @maplefinance

May 21

Holding stablecoins and watching them do nothing?

Some RWAF teams are building ways to bring real-world yield onchain.

Nest by @plumenetwork - Stablecoin vaults accessing tokenized Treasuries, private credit, and institutional RWAs

@onrefinance - Onchain reinsurance yield. ONyc combines underwriting income collateral yield with returns designed to be less correlated to crypto markets

@MuDigitalHQ - Asian credit

markets onchain. AZND targets stable yield from Asian fixed income, while muBOND offers higher-risk exposure to tokenized credit pools

@Securitize - Institutional RWA infrastructure powering products tied to firms like BlackRock & Hamilton Lane, including new RWA-backed stablecoin initiatives

@maplefinance - One of DeFi’s most established institutional credit protocols. syrupUSDC provides yield from institutional lending across multiple chains

Your stablecoins can do more than sit idle.

20

6

117

8,864

Mu Digital retweeted

May 14

- @MuDigitalHQ brings $10mm Asia credit to ethereum in 8 weeks. 🔥

6

4

45

1,464

May 13

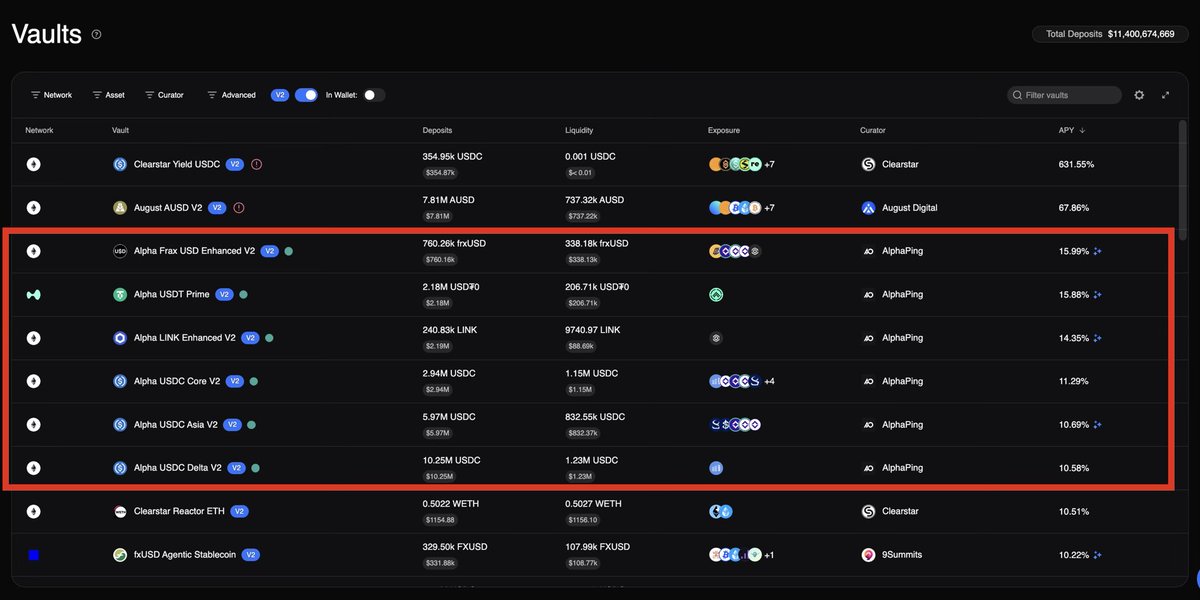

10mm in 8 weeks. Our Alpha USDC Asia V2 @Morpho vault by @0xAlphaping is cooking

Slowly at first. Then all at once 🐂

8

6

26

1,442

Mu Digital retweeted

May 11

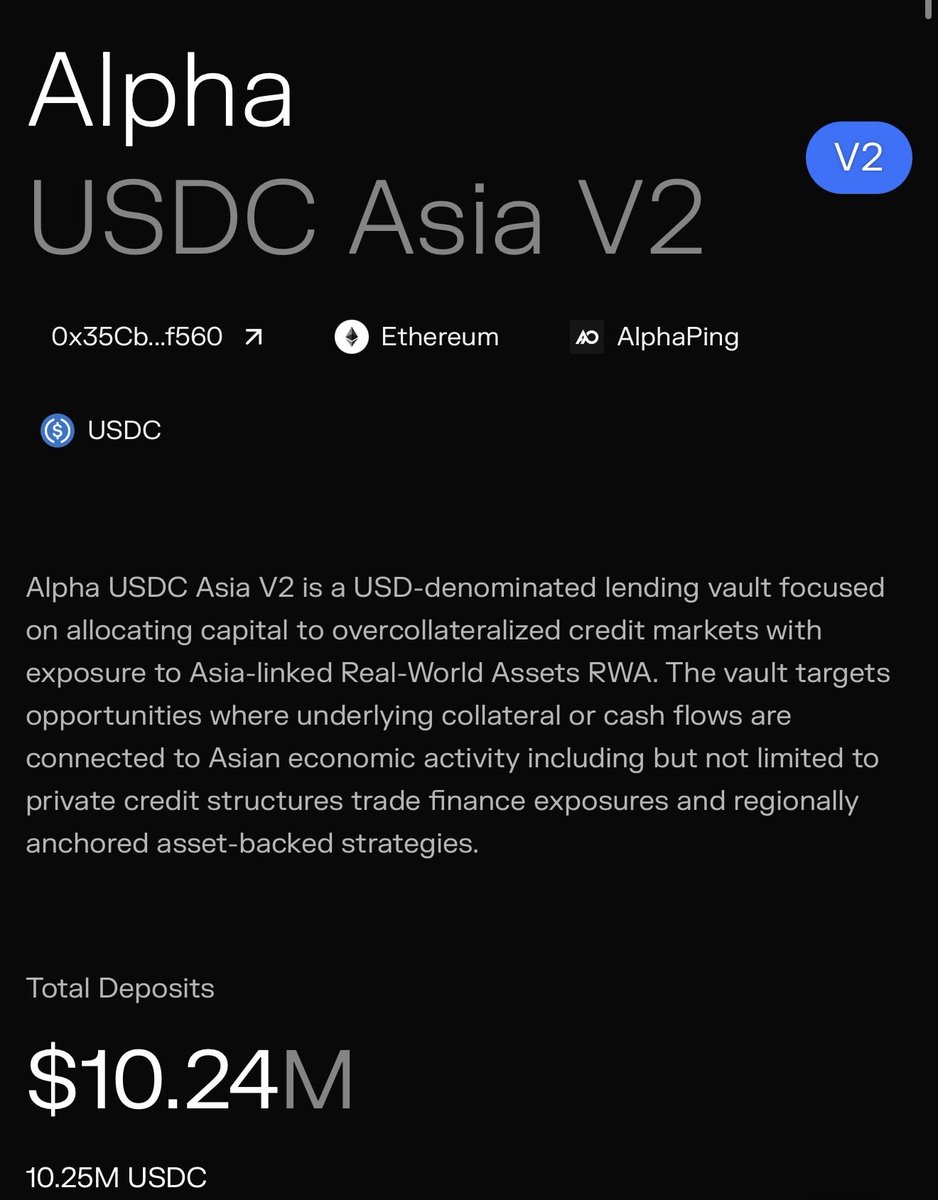

Alpha USDC Asia V2 is approaching $10M.

The RWA thesis is playing out in real time.

Asia-linked trade finance, private credit, regionally anchored assets. Real economic activity backing real loans.

This is what diversified lending looks like onchain.

@MuDigitalHQ @Morpho

4

1

19

855

Mu Digital retweeted

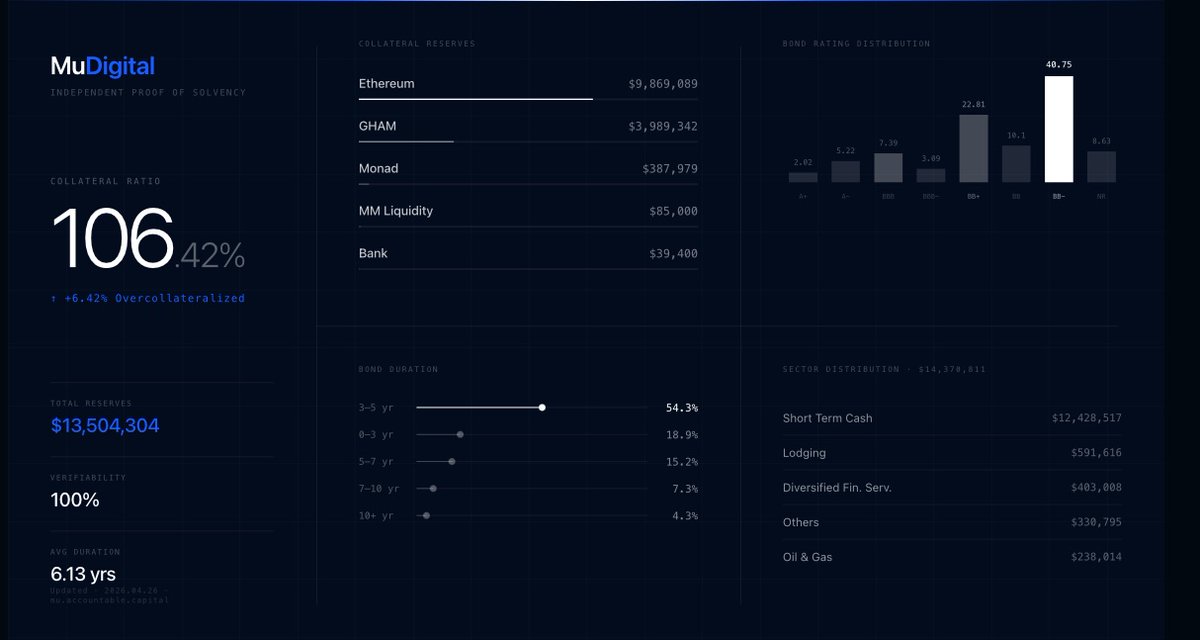

- @MuDigitalHQ is a protocol focused on bringing Asia based fixed income assets onchain through tokenization.

The platform structures credit products, such as government bonds, corporate bonds and private credit, into two onchain tokens.

AZND (Asia Dollar) represents the senior tranche backed by underlying credit assets.

muBOND represents a junior tranche designed to absorb portfolio level volatility.

Currently have around $16 million in TVL.

This structure mirrors traditional structured finance, but with full onchain transparency and verifiability.

All displayed data is sourced from Accountable, providing independent proof of solvency and real-time insight into reserves, collateralization, and portfolio composition.

8

4

40

1,657

May 4

6 weeks live. 7mm in deposits.

Check out our Alpha USDC Asia V2 vault for some of the most sustainable looping yields on @Morpho (c/o @0xAlphaping)

Wanna know how the underlying works?

docs.mudigital.net/

Just getting started 🐂

May 4

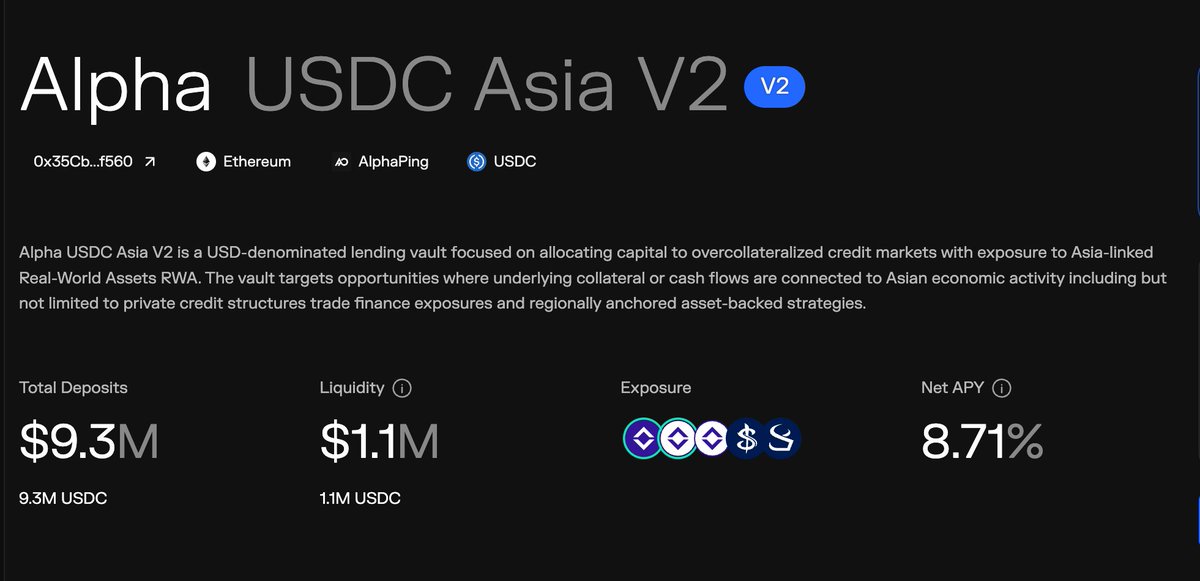

Alpha USDC Asia V2 crosses $7M.

$1M → $3M → $7M. Steady growth since launch.

USDC lending into Asia-linked RWA credit. Trade finance, private credit structures, regionally anchored collateral.

Different geography. Different collateral profile. Same curation framework.

@MuDigitalHQ @Morpho

5

3

14

1,457

Mu Digital retweeted

RWAF Sundays…

@IxsFinance - Licensed RWA tokenization & trading infrastructure

@MuDigitalHQ - Asian institutional credit yields, brought onchain

@onrefinance - Tokenized reinsurance yield on Solana

9

16

67

1,556

Mu Digital retweeted

May 2

Pretty insane to see how @0xAlphaping completely dominates the stablecoin yield on @Morpho with a track record of $0 bad-debt to date since inception.

1

4

21

882

Apr 27

Mu Digital × @Pendle_fi

Institutional grade Asia credit is now live on Pendle.

🔹 Provide liquidity to LP-loAZND

Earn base yield trading fees. Currently ~13% APY

🔹 Lock in PT-loAZND for fixed yield

~8% fixed APY, redeemable 1:1 as AZND staked in Mu Digital at maturity

🔹 Go with YT-loAZND for yield points upside

Currently ~6.95% APY on-chain yield, plus 40 loAZND Points through maturity

Real world yield. Flexible exposure. 🔗 Enter the pool here:

app.pendle.finance/trade/poo…

11

9

51

11,541

Mu Digital retweeted

Apr 21

Some RWA Foundation members & what they unlock onchain:

@MuDigitalHQ - Asian credit markets

@onrefinance - reinsurance yield

@PreStocks - pre-IPO equities

@plumenetwork - purpose-built RWA L1

@etherfuse - sovereign bonds

@IxsFinance - RWA settlement layer

27

17

124

4,060

Apr 21

For peace of mind - none of our products or vaults have any exposure to recent security incidents, including KelpDAO

All underlying assets in our Alpha Asia USDC v2 @Morpho @0xAlphaping vault are uncorrelated and remain unaffected

Stay safu fam 🙏🏼

6

4

40

1,406