Futurist, optimist, nature lover. ER radiologist & part time degen.

Joined May 2009

- Tweets 11,726

- Following 1,724

- Followers 1,656

- Likes 26,111

3,276 Photos and videos

Jun 3

Yeah, like I said. Unholy long $ADUR.

Jun 3

🚨 $ADUR APPOINTS JAN LEMMENS AS PROJECT DIRECTOR FOR THE FOAK INDUSTRY FACILITY IN CHEMELOT

What Jan brings to the table:

- 30 years building and scaling industrial facilities across Europe. Hands-on plant building.

His track record:

- Sekisui S-Lec BV: Director of Operations and Plant Manager.

- Transilwrap Company: Operations Director. Established the company's FIRST European manufacturing facility from scratch. This is exactly the kind of FOAK challenge Aduro now faces at Chemelot.

- Rexam - Group Engineering Manager: Led major industrial investment projects across the UK.

- RPC BEBO NL - General Manager: Plant operations and manufacturing scale-up.

Jan has also direct prior experience working inside the Chemelot ecosystem. He knows the contractors. He knows the infrastructure providers. He knows how things actually get permitted and built in that specific industrial park.

What he'll focus on:

- Site development: civil works, permitting, contractor coordination

- Building the local operating organization from zero: recruitment, safety, training, commissioning-readiness

- Coordinating Netherlands execution with Aduro's Canadian engineering team

- Taking FOAK from engineering/permitting phase into actual construction and operations

What this hire means:

In Aduro's own words: "This project has reached a stage where local industrial execution experience becomes critically important".

$ADUR recent hires show real operators with boots on the ground experience to actually build stuff from the ground up:

- Three weeks ago: Scott Smith for the heavy oil vertical.

- Today: Jan Lemmens for the FOAK industrial facility.

$ADUR is hiring like a company that's about to scale.

17

1,057

Jun 1

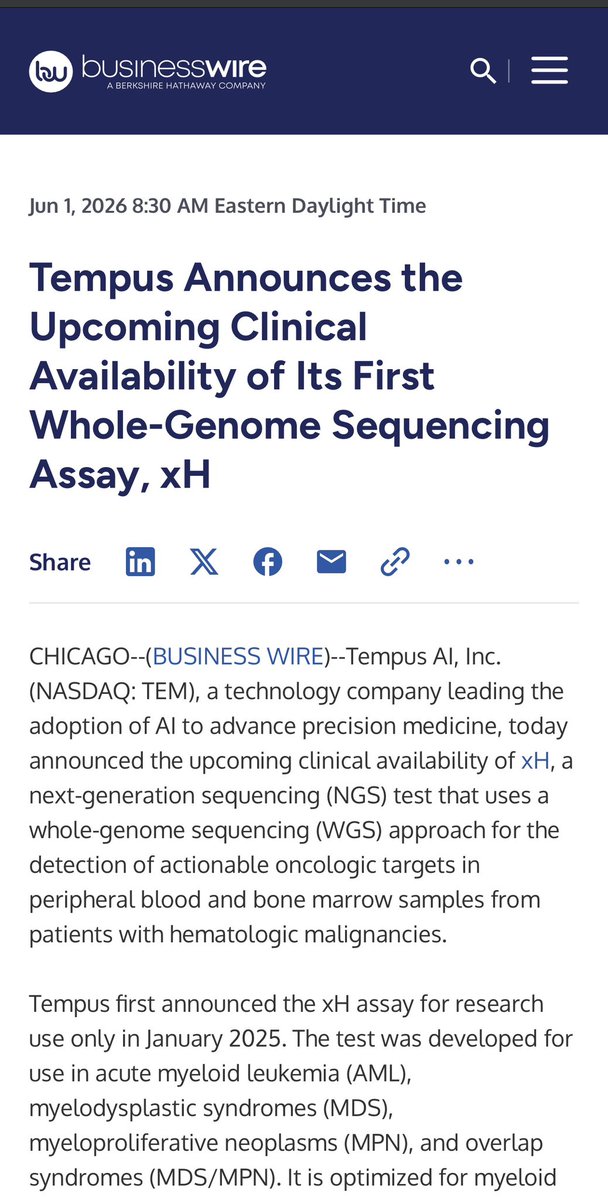

$TEM

There are too many fundamentally bullish catalysts emerging month after month for Tempus AI. Last month it was $BMY collaboration. This month it’s a new product offering and reimbursement approvals.

All while AI-leveraged SaaS is regaining favor and price may have double bottomed.

I am loading up on Tempus AI here.

Jun 1

$TEM just shared that their first whole genome sequencing test, xH, is about to be clinically available for patients with blood cancers like AML, MDS, and MPN.

For years, we’ve been running targeted panels that look at a few hundred genes. They’re good, but they miss things. xH sequences the entire genome from a blood or bone marrow sample, so oncologists get the full picture in one test , SNVs, structural variants, copy number changes, all of it.

The validation looks structurally solid with 97% agreement with current methods and a 98.97% positive predictive value for SNVs/indels. Basically, high accuracy and very few false positives. That means more confidence when deciding on therapy or clinical trial options.

Genome sequencing has been used in research for a while. Seeing it move into routine clinical care for heme malignancies is a big deal. It’s how precision medicine actually becomes the standard.

Hoping this helps patients get to the right treatment faster with fewer blind spots.

2

3

18

4,549

Jun 1

Unholy long $ADUR.

Follow the pilot progress and first of a kind commercial plant buildout *closely*.

1

1

26

2,143

Jun 1

Jun 1

Given everything that is developing in AI

The value of proprietary data than can be instantly leveraged is going to 20X over the next two years....

491

Jun 1

$AMPG

Rarely do you find a sub $400m startup that checks all the right boxes:

-Theme/sector(s): AI x telecomm/5G, quantum computing, (they are in the business of radio signal amplification, applicable to both)

- Founder/CEO alignment: Has never sold shares. Continues buying on open market.

- Real revenue, good margins, revenue rapidly growing, short term path to profitability

- Fully integrated domestic manufacturing, rendering it one of the only U.S. based producers of a critical product suite that telecomm companies and QC companies need.

-Healthy balance sheet. Debt free. Strong cash holdings relative to size. Ample runway for at least 3 years or ~12 quarters. Management has tried to keep working capital with as minimal shareholder dilution as possible so far.

All of these together make for a hidden gem with very high potential for re-rate if growth continues.

Check out the substack writeup in the repost.👇🏻

May 27

Solid piece on $AMPG. This is one of the most thorough articles on Amplitech I’ve seen yet.

The article’s core thesis is that AmpliTech Group is no longer just a low-margin RF parts supplier. Shawarma Capital argues the market has not yet priced in the transition toward integrated Open RAN radio systems, higher-value engineering revenue, and improving operating leverage.

If execution continues, the rerating debate gets very interesting. 👀

#AMPG #5G #ORAN #DefenseTech #SmallCaps #Telecom #QuantumComputing #AmericanMade

open.substack.com/pub/shawar…

1

3

25

4,631

OriginalRollo retweeted

Jun 1

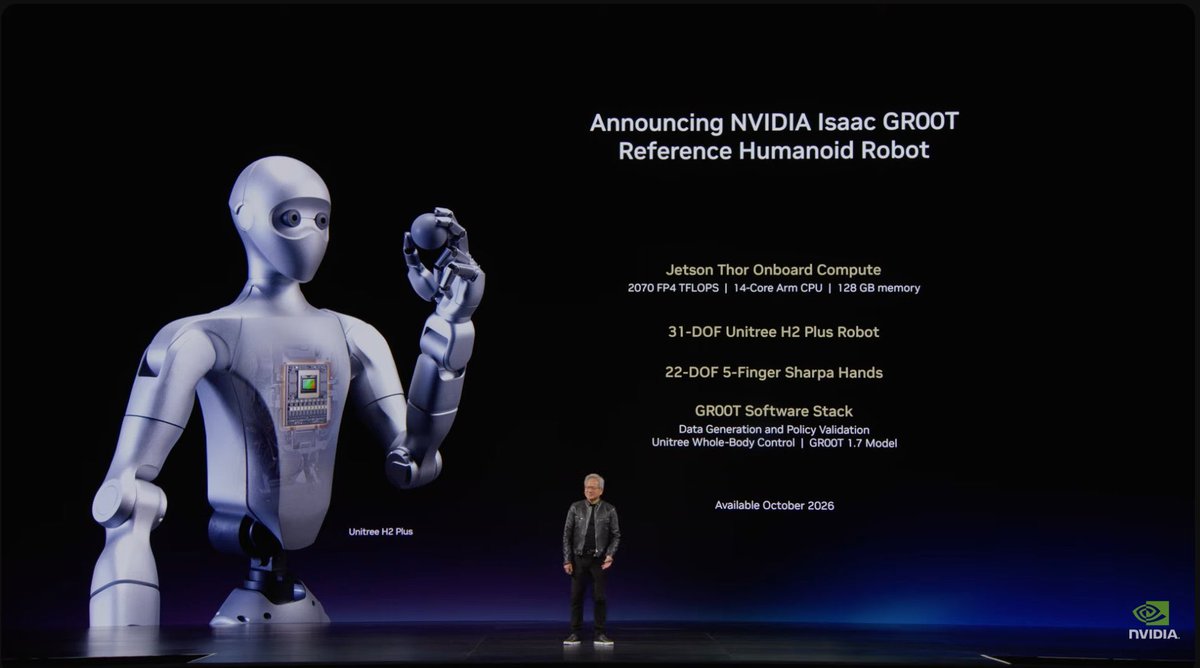

NVIDIA just announced the Isaac GROOT reference humanoid robot. The humanoid sector is arriving faster than almost anyone is prepared for.

Look at what Jensen just put on stage.

A complete reference humanoid built on Jetson Thor onboard compute. 2070 FP4 TFLOPS. 14 core Arm CPU. 128GB of memory. A 31 degree of freedom Unitree H2 Plus body. 22 degree of freedom five finger Sharpa hands.

The full GROOT software stack for data generation, policy validation, and whole body control. Available October 2026.

This is the iPhone moment for humanoids. When NVIDIA ships a reference design every robotics company on earth can build on top of it instantly.

They just handed the entire industry a blueprint and the compute to run it. The barrier to building a capable humanoid just collapsed.

And here is what most people are missing. NVIDIA does not make the sensors, the force feedback, or the perception silicon that goes into every one of these robots at scale.

The reference design proves the platform. The component suppliers capture the volume.

That is exactly why I am positioned the way I am.

Some names include:

$AMBA — the edge AI perception brain. Already signed an $800 million Hanwha robotics partnership.

$OUST — the eyes. Native color lidar for robots navigating the real world.

$VPG — the force sensors that let those Sharpa hands actually feel what they are gripping.

When NVIDIA puts a reference humanoid on stage with an October 2026 ship date the timeline everyone assumed was 2030 just moved years closer.

The robots are coming. Own the parts inside them.

$AMBA $VPG $OUST

14

21

184

20,342

May 22

Subtext? Maybe 🌝

$OUST is heading to the moon.

May 21

Ouster lidar heading to the moon 🚀🌑

279

May 18

Bought $OUST dip heavily today. I could care less what “President Capital” thinks of them. No one seems to know who they are it turns out? 🙄

194

OriginalRollo retweeted

$ADUR | $ACT 🌊🌐💪

Honestly, I’m not shocked… but wow.

@OferVicus now sitting at nearly 9.8 million personally owned shares after another open market purchase today.

Nice work, and thank you for your dedication and continued execution.

That’s a CEO continuing to increase exposure while the company is:

💥 Advancing the NGP campaigns

💥 Gearing up for FOAK deployment at Chemelot

💥 Expanding into paraffinic crude upgrading

💥 Building deeper industry relationships

You don’t keep adding if you think the story is peaking.

4

18

96

20,866

OriginalRollo retweeted

6

19

116

170,791

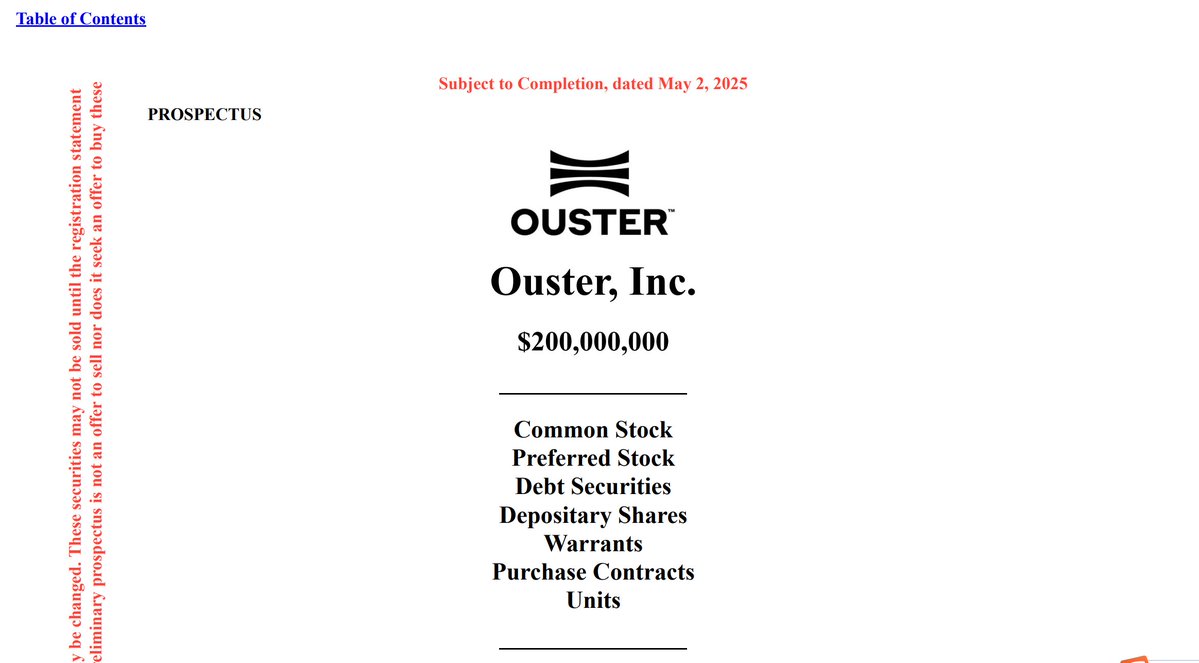

$OUST filed two SEC docs today. I've read both. Here's what's actually happening — and why I'm more bullish, not less.

Two filings hit today: a 424B3 and a 424B5. Looks scary. It's not.

The 424B3 is a termination notice — Ouster just closed out its 2025 ATM program. Why? Because they used $97.5M out of $100M. It's done. Gone. Finished.

The 424B5 is a new $100M ATM sales agreement under the same $200M shelf registered last May. Same shelf. New tranche. Four agents this time: Oppenheimer, Northland, Rosenblatt, and Roth Capital.

This is not new dilution authorization. This is a new sales agreement under existing authorization. Big difference.

Now let's talk about why this setup looks familiar.

Last May, Ouster filed this exact same shelf (S3 filing). Signed a $100M ATM with Oppenheimer (424B5 filing). Stock was at $8.33 right before this S3 shelf filed on 5/2 and $11.41 before ATM filing hit on 5/12.

What happened next? We all knew. Six months of explosive runs $8.33 → $41.

Oh, and the stated use of proceeds? "General corporate purposes, including working capital", same purposes in the ATM filings last year and this year.

That same boilerplate language. And then they went and acquired Stereolabs with $35M cash raised from ATM in 2025— one of the most strategic moves in the spatial AI space.

So let's think about what this $100M is actually for.

Ouster currently sits on ~$175M in cash. Zero debt. The company is guiding toward breakeven next year. Their organic cash needs are well covered. Comfortably.

You don't raise $100M in fresh ATM capacity because you're worried about payroll.

My read: they're hunting. The lidar and spatial AI ecosystem is consolidating fast. There are targets out there — computer vision companies, software stacks, robotics sensor fusion plays — that would make Ouster's REV8 platform dramatically more valuable overnight.

They did it with Stereolabs when nobody was watching. I think they're setting up to do it again.

Angus Pacala just has that vision. When he executed the merger of equals with Velodyne, he secured all the cash, the entire IP portfolio, sales channels, R&D team, brand, product line, and more. That brilliant move transformed Ouster from a small LiDAR player with a tight cash position into the largest Western LiDAR company with $315M in cash, 173 granted and 504 pending patents. Nobody even thought that was possible.

One more thing that's worth flagging.

Last year, Ouster's ATM had one agent: Oppenheimer.

This year? Four agents. Oppenheimer, Northland, Rosenblatt, Roth Capital.

Notice who's not on that list: Cantor Fitzgerald (thanks to @jimmyrunsmoney for pointing this out).

Cantor sent an associate — not their analyst — to Ouster's earnings call this week. Then dropped a downgrade the next morning.

Draw your own conclusions. But when a bank loses the mandate, the coverage tends to get a lot less enthusiastic.

Bottom line:

✅ Not new dilution — same shelf, new sales agreement

✅ $175M cash, no debt, approaching breakeven in 2027 — they don't need this money for survival

✅ Last time this happened: massive stock run Stereolabs acquisition

✅ Four agents lined up suggests they're ready to move quickly when the time comes

⚠️ Cantor's downgrade the day after losing the ATM mandate — make of that what you will

I don't know what they're buying nor guarantee the stock will run like last year. But I think they're buying something.

7

9

125

17,607

Apr 25

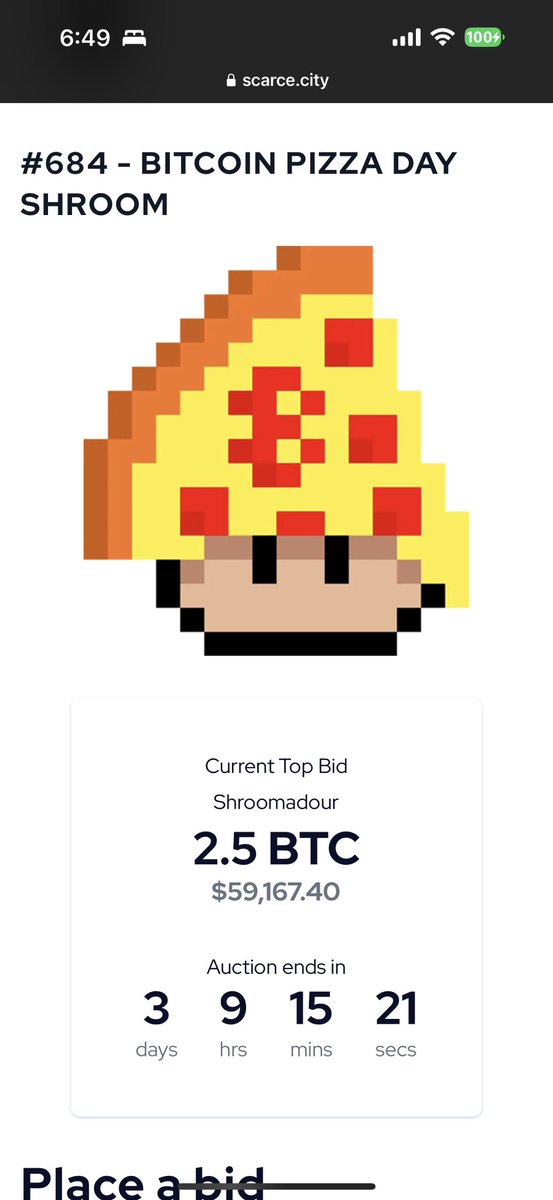

Bitcoin Shrooms:

NFT economy feels lifeless at the moment but I think the thesis remains completely unchanged. They’re the earliest collection of historical digital artifacts immutably inscribed on Bitcoin. Their value (along with Punks, Rare Pepes, etc) will one day be recognized even if that day is not here now.

You don’t hold them if you care about liquidity or opportunity cost. You hold them because you love what they are and the value they’ll bring in the long term. If you love collecting rare gems with real lore, they’re for you. They are not liquid $BTC or equities, although they can coexist in a portfolio as complementary.

Their function, however, is inherently different as art/collectibles. It just so happens that they’re the best ones in the digital space 🥸

🍄

1

106

Apr 23

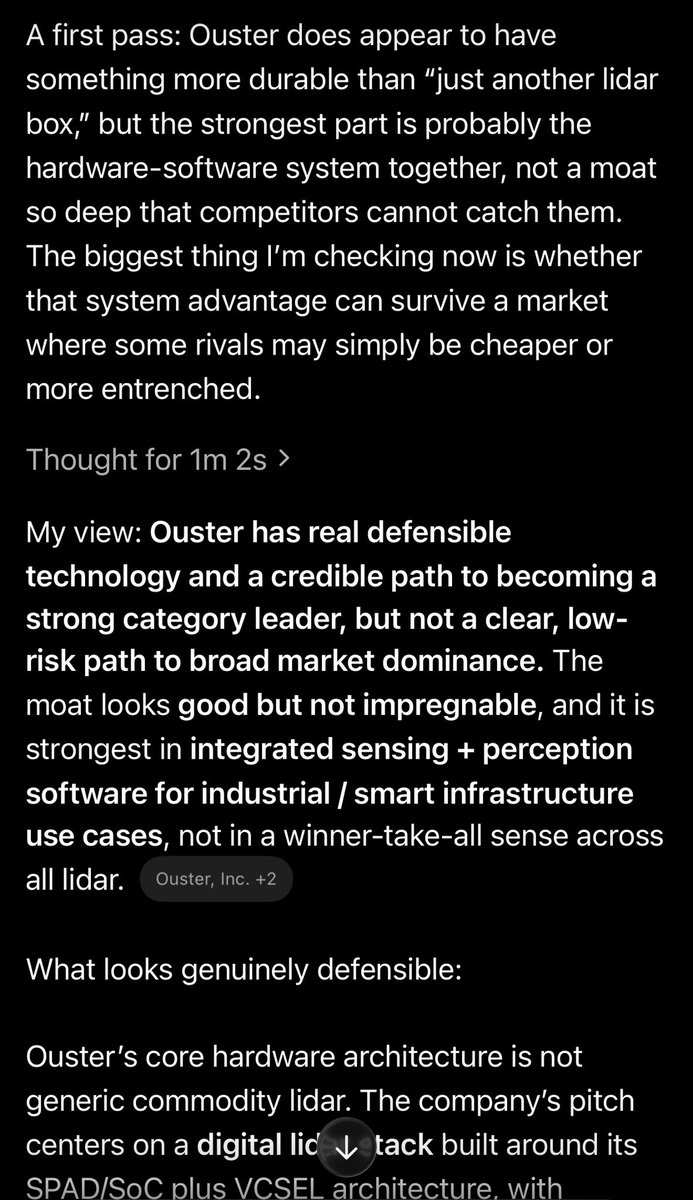

Why is $OUST both a software & hardware producer? Here’s why you’re buying what will eventually be a full stack autonomous sensing platform, and not just a hardware manufacturer:

• Rapid growth in software attachment: Software-attached bookings more than doubled in 2025 (following 60% growth the prior year) and now represent over 15% of sensors shipped (a 120% YoY increase in attachment rate). This included multi-million-dollar and 7-figure annual license deals. Deployments exceed 1,200 sites (covering >65 million sq ft in some cases), with recent wins like BlueCity for 30 Atlanta intersections ahead of major events. They’ve won a major contract to provide software & hardware products during the 2026 FIFA World Cup at venues in the United States.

• Recurring/high-margin potential: Software involves licenses (perpetual/term, often with maintenance/post-contract support) and services (development/compliance). These are higher-margin and can generate ongoing revenue from the growing installed base of >25,000 sensors shipped in 2025 alone. Management explicitly calls this a priority for scaling the product portfolio, higher ASPs, and accretive margins.

• Platform expansion via acquisition: The February 2026 StereoLabs acquisition (high-growth, EBITDA-positive business with ~$16M 2025 revenue) adds cameras, AI compute, sensor fusion, perception software, and AI models. This creates a unified physical AI stack (LiDAR vision software) that strengthens management capabilities across robotics, industrial automation, and smart infrastructure —directly tying into the “full stack LiDAR systems” thesis.

• Financial and strategic context: FY 2025 total revenue hit $169M ( 52% YoY), with product (mostly hardware) revenue at $147M ( 32% YoY) and record shipments (>25,000 units). GAAP gross margins reached 49% (non-GAAP 54%), aided by scale, efficiencies, and one-time royalties. Long-term guidance targets 30-50% annual revenue growth and 35-40% GAAP gross margins (explicitly excluding one-time royalties), with software seen as a *key* driver for sustained growth, recurring revenue, and profitability. Q4 2025 showed a profit swing and strong margins.

^In other words, software hasn’t even fully caught on yet and implies tremendous room for sustained high growth.

Incredibly bullish on $OUST next 3-5 years.

3

229

Apr 22

Seeing a lot of polarized takes on $OUST, which imo is a good sign at this point. It means this is now on more people’s radar.

Many are quick to discredit them as an easily commoditized hardware producer in several years since they make physical sensors.

If you even *lightly* dig deeper, you’ll find they sell a software stack which is gaining significant traction and has an important role in hardware integration as part of a full platform. This implies higher brand loyalty and switching costs. Buying into an ecosystem builds a more defensible moat and should insulate from commoditization. They know this. You should too if you’re passing the specific criticism. To not do so is a bit lazy if perhaps dishonest.

Ouster’s competitive advantage could only be further magnified by existing U.S. legislation banning the use of foreign LIDAR providers for defense-related purposes, which confers a smaller boat of applicable competitors. Provided the legislation holds (would think it will). I.e. there will be no cheap Chinese alternatives in key industrial verticals.

In short, before you write off $OUST because they “make hardware others can make cheaper”, think at least one layer deeper. There’s fair bit of nuance in this particular scenario, mostly favoring their outcome. None of this even addresses any intellectual property they maintain on physical hardware, because one shouldn’t even have to.

@daniel_koss @JKeynesAlpha @MultibaggerRsch @itschrisray @CaesarCapitalz @aleabitoreddit @StockSavvyShay

1

3

341

Apr 22

This is the main source of competition currently:

🚨 LiDAR Showdown Incoming 🚨

📅 Ouster $OUST reports Q1: May 5

📅 Aeva $AEVA reports Q1: May 6

💡 Here’s what the market is missing:

There’s a MASSIVE valuation gap between these two companies.

📊 Ouster @ousterlidar has ~7x MORE revenue.

📉 Yet trades at a LOWER price/sales ratio

🤯 Let that sink in.

🔧 Ouster’s scale is real:

• 10,000 customers

• StereoLabs cameras LiDAR sensors

• Full perception software stack

• Exposure across:

🚦 Traffic management

🛡️ Security & defense

🚖 Robotaxis

🤖 Physical AI

📈 To match Aeva’s @aevainc valuation, Ouster would need to trade ABOVE $100.

🚀 And that’s not unrealistic:

• 35–50% annual growth trajectory

• Break-even expected by 2027

• Full profitability by 2028

💰 In 2028 estimated earnings: ~$2.35/share

📊 At just 12x P/E

Meanwhile…

🔥 40% growth companies blue chips trade at 50–100x

⚠️ The disconnect is massive

👀 Ouster remains one of the most undiscovered opportunities in the market

#Ouster #AEVA #LiDAR #AI #Robotics #Investing #Stocks #GrowthStocks

154

🚨 LiDAR Showdown Incoming 🚨

📅 Ouster $OUST reports Q1: May 5

📅 Aeva $AEVA reports Q1: May 6

💡 Here’s what the market is missing:

There’s a MASSIVE valuation gap between these two companies.

📊 Ouster @ousterlidar has ~7x MORE revenue.

📉 Yet trades at a LOWER price/sales ratio

🤯 Let that sink in.

🔧 Ouster’s scale is real:

• 10,000 customers

• StereoLabs cameras LiDAR sensors

• Full perception software stack

• Exposure across:

🚦 Traffic management

🛡️ Security & defense

🚖 Robotaxis

🤖 Physical AI

📈 To match Aeva’s @aevainc valuation, Ouster would need to trade ABOVE $100.

🚀 And that’s not unrealistic:

• 35–50% annual growth trajectory

• Break-even expected by 2027

• Full profitability by 2028

💰 In 2028 estimated earnings: ~$2.35/share

📊 At just 12x P/E

Meanwhile…

🔥 40% growth companies blue chips trade at 50–100x

⚠️ The disconnect is massive

👀 Ouster remains one of the most undiscovered opportunities in the market

#Ouster #AEVA #LiDAR #AI #Robotics #Investing #Stocks #GrowthStocks

2

17

5,504