📈 Stock Market Analyst | Sharing high-growth stock opportunities, market insights & investing

Joined June 2009

- Tweets 4,946

- Following 91

- Followers 7,091

- Likes 21,355

288 Photos and videos

Pinned Tweet

Jun 17

📱 WhatsApp: wa.me/16096496887

Markets are moving fast — and positioning matters more than narratives.Most mistakes in U.S. equities come from misreading risk, not missing ideas.

I focus on:

liquidity & macro regime shifts

AI / growth leadership

positioning vs fundamentals

risk & portfolio structure

If you want a second opinion on your positioning or portfolio, you can reach me on WhatsApp.

I try to respond when I can.

$QQQ $NVDA $TSLA $AAPL $MSFT $META $AMZN#StockMarket #Investing #Trading #WallStreet #Equities #Macro #Finance #Stocks #AI #ArtificialIntelligence #Semiconductors #TechStocks #RiskManagement #Portfolio

142

SpaceX IPO Unlocks Massive Spillover Winners — 5 Stocks Set to Benefit

SpaceX’s IPO is more than just a single listing — it’s a liquidity and valuation reset for the entire space ecosystem. With a multi-trillion-dollar valuation and massive capital earmarked for Starlink, Starship, and orbital infrastructure, the ripple effects extend far beyond SpaceX itself.

The most direct winner is Alphabet, which holds a ~6.1% stake in SpaceX. At current implied valuations, that stake alone is worth over $100B , effectively turning an “illiquid private bet” into a real, mark-to-market asset that now meaningfully impacts earnings visibility.

Beyond that, the opportunity is spreading across the space value chain:

Rocket Lab (RKLB) benefits from rising launch demand in the small-to-medium payload segment, where SpaceX is less dominant.

Kratos (KTOS) stands to gain from expanding demand in satellite ground systems and defense-linked space infrastructure.

Intuitive Machines (LUNR) is positioned around lunar logistics and deep space communications, tightly aligned with Starship-era missions.

AST SpaceMobile (ASTS) benefits indirectly as satellite connectivity becomes a broader institutional narrative, and has already started leveraging SpaceX launch capacity.

That said, while the narrative is extremely strong, expectations are also becoming more forward-priced. In space infrastructure, execution, capital intensity, and launch dependency still matter more than story.

Bottom line: SpaceX IPO is a major liquidity catalyst for the entire space stack, but winners will be selective — not every “SpaceX-adjacent” name will translate into durable returns.

Not financial advice, just personal opinion.SpaceX IPO Unlocks Massive Spillover Winners — 5 Stocks Set to Benefit

SpaceX’s IPO is not just a single-company revaluation — it’s a structural reset for the entire space economy. With massive capital flowing into Starship, Starlink expansion, and orbital infrastructure, the spillover effects extend across the full space value chain.

The most direct beneficiary is Alphabet, which owns ~6.1% of SpaceX. That stake alone is now worth well over $100B , turning an illiquid private holding into a major mark-to-market asset.

Beyond that, the broader ecosystem winners include:

Rocket Lab (RKLB): key player in small-to-mid payload launches, benefiting from rising launch demand

Kratos (KTOS): exposed to satellite ground systems and defense-linked space infrastructure

Intuitive Machines (LUNR): positioned in lunar logistics and deep-space communications

AST SpaceMobile (ASTS): satellite-to-phone connectivity, benefiting from broader satellite deployment growth

SpaceX ecosystem enablers (launch satellite supply chain): including ground, software, and comms infrastructure providers that scale with Starlink/Starship buildout

The key point: SpaceX doesn’t just lift direct partners — it expands the entire addressable market for space infrastructure.

Bottom line: strong multi-layered tailwind, but winners will be selective and execution-driven rather than purely narrative-based.

Not financial advice, just personal opinion.

30

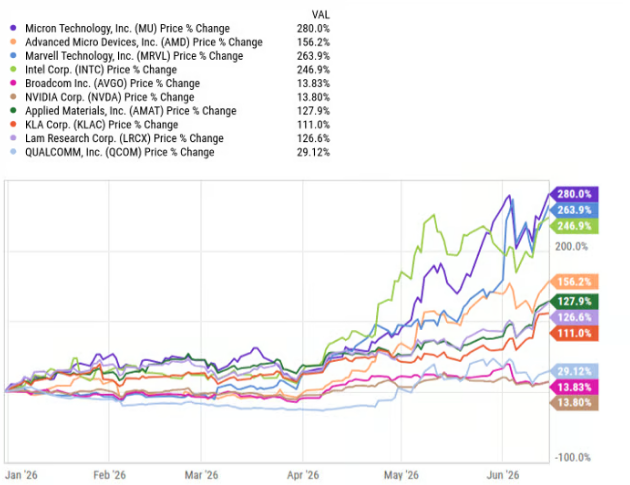

iShares Semiconductor ETF is set to significantly outperform the S&P 500 in 2026 — but is it still worth buying now? The answer may surprise you.

The iShares Semiconductor ETF (SOXX) has had a powerful run in 2026, up more than 100% year-to-date compared to roughly 10% for the S&P 500. The surge is being driven by sustained AI infrastructure demand across the entire semiconductor stack — from memory (Micron), to GPUs (Nvidia, AMD), to equipment and networking players like Broadcom and Applied Materials.

Fundamentally, the backdrop is still strong. AI data center expansion remains in full force, and supply constraints in key areas such as HBM and advanced chip manufacturing continue to support pricing power and earnings growth across major holdings.

However, after such a strong rally, the risk-reward balance is less attractive than earlier in the cycle. A lot of future growth is already being priced in, and semiconductors remain a highly cyclical industry — once supply catches up, margins and sentiment can shift quickly. Any slowdown in AI capex or demand normalization could increase volatility significantly.

Bottom line: SOXX remains a strong long-term AI infrastructure exposure, but at current levels it’s more about managing cycle risk than chasing momentum.

Not financial advice, just personal opinion.

76

AGNC Investment After Latest Earnings: Still a Reliable Income Play?

AGNC continues to offer an extremely high dividend yield of around ~14%, which naturally attracts income-focused investors. Following the latest earnings update, the dividend still appears covered in the near term, supported by relatively stable net interest spreads that have recently improved back above ~2% after some compression earlier in the cycle.

That said, the underlying model is still highly rate-sensitive. AGNC’s earnings power depends heavily on the spread between long-term MBS yields and short-term funding costs, which means even small shifts in rate expectations or mortgage markets can materially impact future dividend sustainability. Historically, this is exactly where the risk shows up — the company has cut dividends multiple times in prior rate cycles.

From a long-term perspective, AGNC has also underperformed broader equities meaningfully, which reinforces that this is not a “buy and forget” income compounder, but more of a rate-cycle-driven yield vehicle.

Bottom line: the yield is attractive and may remain stable in the current environment, but AGNC is better treated as a tactical income position rather than a core long-term dividend holding through full market cycles.

56

Jun 17

Worried about a market pullback? These 3 dividend stocks may help reduce risk

Medtronic (MDT), Realty Income (O), and ExxonMobil (XOM) are highlighted as defensive income plays, offering dividend yields between 2.9%–5.2% with relatively low beta, suggesting weaker correlation to broader market swings.The idea is simple: healthcare demand, REIT cash flows, and energy giants tend to be more resilient through cycles. In an environment where valuations feel stretched and volatility risk is rising, these names are positioned more as capital preservation tools than high-growth assets.That said, they are not “alpha generators” in strong bull markets—they’re built to smooth drawdowns, not outperform momentum cycles.Just my personal view, not financial advice.

80

Jun 17

MercadoLibre Insider Buying: Bullish Signal or Value Trap?

A senior executive just doubled his direct stake with a ~$200K purchase while the stock is down over 30% from its highs.

On the surface, this looks like confidence—but MELI is also under margin pressure as it reinvests heavily into long-term growth (AI, fintech, logistics).

Revenue is still growing strongly (~49% YoY), but net income has slipped due to aggressive expansion spending.

At a ~2.6x P/S multiple, the valuation is starting to look interesting again—but the key question is whether earnings pressure is temporary or structural.

Insider buying helps sentiment, but fundamentals will decide the outcome.

105

Jun 16

Anthropic vs OpenAI: Which AI giant can deliver higher investor returns?

My view: if I had to choose between the two ahead of potential IPO dynamics, I currently lean slightly toward Anthropic. The key reason is its faster traction in enterprise workflows—especially AI coding—where it has already established meaningful market share and is showing signs of approaching a profitability inflection point earlier than many expected.

OpenAI, on the other hand, remains the dominant consumer AI brand with unmatched global recognition and a powerful distribution advantage through its deep integration with Microsoft’s ecosystem. However, that strength comes with a longer and more capital-intensive path to sustainable profitability, given its heavy compute costs and continued investment cycle.

From an investment perspective, this is essentially a classic “enterprise efficiency vs consumer scale” trade-off. Anthropic is currently winning where budgets are directly tied to productivity gains and engineering workflows, while OpenAI is still building monetization layers on top of massive user adoption.

That said, both companies could ultimately be long-term winners depending on execution, pricing power, and how quickly AI becomes embedded across enterprise software stacks.

Purely personal opinion, not financial advice.

133

Jun 16

📊 Market Update — AI-led Equity Structure

The market remains resilient on the surface, but internally the structure is becoming more selective.

We are seeing:

Index performance heavily driven by a small group of AI mega-caps

Gradual weakening in broader market participation

Valuation expansion running ahead of earnings confirmation

Increasing sensitivity to macro signals (rates, liquidity, risk appetite)

This is not a broad-based rally — it is a concentrated leadership cycle dominated by narrative liquidity.

The key question now is no longer whether AI is a theme — it clearly is.

The real issue is:

👉 Are we still in the early phase of an earnings-backed AI supercycle, or moving into a late-stage positioning trade where volatility starts to matter more?

If you’re unsure how this rotation impacts your portfolio, or want a second opinion on positioning, feel free to comment your situation — I’ll try to share a structured view when possible.

Always happy to discuss market structure and risk frameworks.

1

61

Jun 16

Before buying shares of SpaceX, please carefully read the 20 most critical words in the company’s prospectus.Key Takeaways:SpaceX IPO surged as much as ~19% on its first trading day, driven by extremely strong demand and oversubscription. However, behind the excitement, the risks remain equally clear.Core businesses: rocket launches AI infrastructure satellite internet (Starlink)

Revenue mix: Starlink has become the primary revenue driver (~$11B scale), followed by space launch services

Growth edge: reusable rockets continue to significantly reduce launch costs, strengthening its competitive moat

Key risk: massive capital expenditures (> $12B ), especially for AI and space initiatives, alongside ongoing net losses

Prospectus warning: many initiatives rely on “extremely complex, unproven, or even non-existent technologies,” including space-based AI data centers, large-scale chip manufacturing, and deep-space transport systems

Valuation-wise, the market appears to be pricing in highly optimistic long-term outcomes. Once sentiment cools, fundamentals and cash flow will likely regain dominance in pricing.As highlighted by The Motley Fool, the narrative is compelling—but uncertainty is equally significant.Conclusion (from an experienced analyst perspective): This is a classic high-optional, high-uncertainty, high-valuation trade—suitable only for investors with strong risk tolerance.Just personal opinion.

1

122

Jun 16

The Bull Run in Sandisk Is Not Over YetSandisk

(SNDK) has become a key beneficiary of the AI boom, helping explain its recent strong stock performance. Rapidly rising demand and ongoing memory shortages are driving significant sequential revenue growth.AI has created a structural bottleneck in memory chips, and Sandisk sits at the center of this constraint. NAND flash memory is essential for handling large-scale AI workloads, making high-quality storage a critical part of AI infrastructure.The company’s fundamentals continue to strengthen, and despite its strong rally, its valuation still appears reasonable relative to its growth profile.My view: the trend is still intact as long as AI infrastructure expansion continues.Just my personal opinion, not financial advice.

78

Jun 15

Roku Stock Jumps 20% — But the June 22 Index Change May Matter More Than Buyout Rumors

Roku surged ~20% on Friday after reports of a potential acquisition, but the more important catalyst is actually scheduled and confirmed: June 22 index rebalancing.

Roku will be added to the S&P MidCap 400, triggering forced buying from index funds and ETFs that track the benchmark. This creates near-certain mechanical demand regardless of takeover outcomes.

Unlike rumors, index inclusion has a fixed date and guaranteed flows—but it is still a short-term technical driver, not a fundamental change.

Meanwhile, Roku’s fundamentals are improving: platform revenue growth re-accelerated to 28%, streaming households surpassed 100M, and free cash flow is turning meaningfully positive.

However, valuation is stretched after the rally, making the setup more momentum-driven than value-driven at current levels.

My view: catalyst-driven move, but not a clear long-term entry here.

Just my personal opinion, not financial advice.

1

180

Jun 14

After WWDC, was Buffett right to sell Apple?

The debate around Buffett’s Apple reduction often focuses on timing, but from a risk management perspective, it looks more like portfolio concentration control rather than a directional mistake.

Apple’s post-WWDC AI progress disappointed the market, and the stock came under short-term pressure. But the real issue was always overexposure risk within the portfolio.

Even if he missed some upside, reducing the position helped limit single-stock risk and improve overall balance.

My view: it wasn’t about selling too early—it was about avoiding concentration risk.

Just my personal opinion, not financial advice.

61

Jun 13

The Largest IPO in Stock Market History Has Arrived—What It Means for Your Portfolio

SpaceX’s $75B IPO is a historic liquidity event and will likely drive near-term volatility across both the stock and broader indices.

Index inclusion rules (Nasdaq/Russell) may force passive funds like QQQ and Russell ETFs to buy, creating mechanical demand and short-term price pressure.

S&P 500 inclusion is still off the table due to profitability requirements, which adds some structural stability.

Short term = volatility. Long term = execution story.

I’m staying disciplined, not chasing the first move.

Just my personal opinion, not financial advice.

1

1

82

Jun 12

U.S. Stocks Face Pressure Despite Optimism on U.S.-Iran Deal

Markets are cautious: S&P down 0.31%, Nasdaq -0.53%, Dow flat. Oil dips >1% as Hormuz reopening expectations ease geopolitical risk.

Tech and semis take profits after recent gains; software pressured by Adobe news. SpaceX IPO draws attention, diverting liquidity.

Rotation signals matter more than headlines: AI and growth stocks see volatility, while space, defense, and energy remain in focus.

Short-term: expect swings around bonds at 4.5% yields. Long-term themes—Space Economy, AI Infrastructure, Energy—remain intact.

Holding cash for better entries; no chasing highs.

Just my personal opinion, not financial advice.

1

125

Jun 12

Markets are betting that diplomacy wins this round.

With reports suggesting a U.S.-Iran framework agreement is getting closer, oil is pulling back while equities continue to push higher. The S&P 500 is eyeing another green session as investors rotate back into risk assets.

For now, the market cares more about the reopening of Hormuz and reduced geopolitical risk than inflation headlines.

My takeaway: if a deal is officially signed, energy may cool off further while AI, semis, and growth stocks regain leadership. But until the ink is dry, expect headline-driven volatility.

Just my personal opinion, not financial advice.

1

81

Jun 11

Markets sold off hard as Middle East tensions pushed oil prices higher and reignited inflation fears.

AI, semis, and the Magnificent 7 took the biggest hit, but let's keep things in perspective: this looks more like a positioning reset than a fundamental breakdown.

My takeaway:

• Rising oil = short-term pressure on growth stocks

• Higher volatility = opportunity for disciplined investors

• AI capex, data center demand, and semiconductor cycles remain intact

I'm watching NVDA, AVGO, MU, AMD, and PLTR closely. If fundamentals hold through earnings season, pullbacks like this tend to create opportunities, not endings.

Stay selective, manage risk, and keep some cash ready.

Just my personal opinion, not financial advice. DYOR.

1

81

Jun 10

CPI came in as expected, the dollar weakened, but the bigger story is beneath the surface.

The market is now caught between cooling inflation and rising geopolitical risk. Oil is moving higher, bond yields remain elevated, and rate-cut expectations keep getting pushed out.

My takeaway: this isn't a risk-on environment—it's a stock picker's market.

I'm staying constructive on AI and quality growth names, but keeping some dry powder. If DXY continues to soften while yields stabilize, semis and AI could be the biggest beneficiaries.

Just my personal opinion, not financial advice.

2

112

Jun 10

AMD Stock Up 300% in 12 Months – Is It Too Late to Buy Now?

AMD has surged 300% in the past year, competing fiercely with Nvidia in AI data center GPUs. Its upcoming MI450 accelerator is supported by OpenAI and Meta, with data center revenue up 57% YoY. However, its valuation is stretched at ~109x P/E, much higher than Nvidia’s. The recent 10% pullback isn’t a clear buying opportunity, and valuation risks remain significant.

Views are my own.

1

1

127

Jun 10

Should You Buy SpaceX Stock? What You Need to Know Before the Largest IPO in History

SpaceX is set to IPO on June 12, 2026, raising a record $75 billion with an initial valuation approaching $1.77 trillion. Early trading will likely see the stock spike due to historical low float, index inclusion adjustments, and forced purchases by funds tracking the Nasdaq and Russell indices.

However, insiders have staged unlocks starting in August, which could trigger significant selling pressure. Coupled with high operating losses, extremely elevated P/S ratios (~95x), and substantial R&D costs, this suggests the initial hype may not be sustainable beyond two months.

My take: SpaceX’s IPO will likely soar initially, but the structural dynamics and eventual insider selling make it a risky proposition for most investors. Patience is advisable — let the market digest the stock before considering a position.

Disclaimer: This is strictly my personal view and not financial advice.

2

138

Should You Buy SpaceX Stock? What You Need to Know Before the Largest IPO in History

SpaceX’s IPO is set for June 12, 2026, with an initial valuation potentially reaching $1.77 trillion. While the company’s revenue is strong and losses are primarily due to heavy R&D spending, most retail investors will find it difficult to access shares at the IPO price. Historically, many highly anticipated IPOs experience early volatility and can trade below their peak soon after listing.

From my perspective, given the size, hype, and limited availability, it may be prudent to wait until the initial trading frenzy settles before considering a position. SpaceX is certainly a high-growth company, but the combination of sky-high expectations and thin retail allocation makes early exposure risky.

My advice: For most investors, patience is likely the better strategy — let the market digest the IPO and observe the price action before committing.

Disclaimer: This is strictly my personal view and not financial advice.

167