Real-time transcriptions from a brain with so many folds it appears smooth to the naked eye

Joined January 2011

- Tweets 27,167

- Following 832

- Followers 917

- Likes 108,704

1,051 Photos and videos

Pinned Tweet

16 Dec 2024

$RAIL brings privacy directly to Ethereum. It is in my opinion the most undervalued project in the space

13 Dec 2024

The liquidity black hole awaits. Uniswap has depth for trading volume. Railgun has depth for privacy volume

$RAIL @RAILGUN_Project

3

9

1,631

Railgoon ($eth.eth) retweeted

If I had Elon's money I would solve world hunger instantly.😡

Sent from a device purchased with with a sum of money that could have been used to feed an Ethiopian family for a year, but wasn't, because my generosity is purely hypothetical.

146

912

10,486

118,318

Railgoon ($eth.eth) retweeted

Jun 13

Nobody wants to admit that the bottom 1% of society is INFINITELY worse for the world than the top 1%

229

448

9,413

151,675

Railgoon ($eth.eth) retweeted

Jun 13

Did you just write an anti-govt post and replace it with Elon to see who from the left would nibble? 😂

5

1

280

4,155

Railgoon ($eth.eth) retweeted

Jun 13

One of the worst things the progressive movement has done for society is convince large numbers of people that the success of others necessarily came at their expense. It’s bred so much resentment. And it simply isn’t true.

Jun 12

I am 52 years old. I have been working since I was 15 years old. I have no savings, no retirement, and will never own a home before I die.

And there is now a trillionaire.

253

524

3,909

122,271

Railgoon ($eth.eth) retweeted

Jun 13

it’s hard for me to understand how retarded you people are

I have no theory of mind for someone who thinks $6.6 billion would end world hunger when the US government spends $7 trillion a year

SNAP alone costs $100bn per year

Jun 13

I believe that @elonmusk is entitled to the trillions and more that he may be worth in this lifetime for the value he has created.

I also believe it would be the most baller move of all time to stroke a $6.6 billion check and end world hunger.

39

172

2,623

64,185

Railgoon ($eth.eth) retweeted

Jun 13

Jun 12

I am 52 years old. I have been working since I was 15 years old. I have no savings, no retirement, and will never own a home before I die.

And there is now a trillionaire.

140

869

13,945

383,913

Railgoon ($eth.eth) retweeted

Jun 13

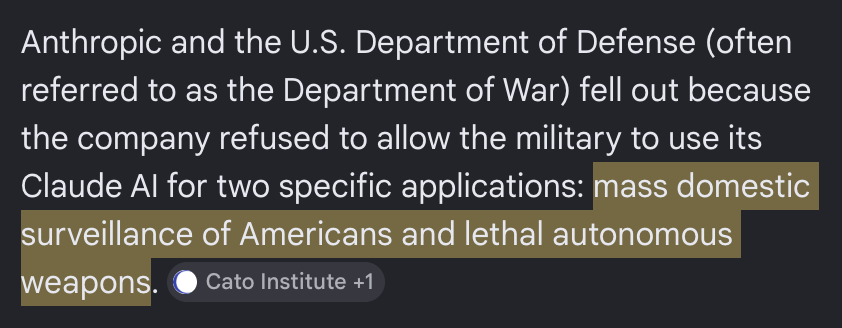

if the admin wants people to believe the anthropic decision was made out of genuine security necessity rather than grievance-driven retaliation, high ranking officials could simply stop posting like this

Jun 13

Three months ago, @DeptofWar kicked @AnthropicAI out of our building—forever.

Every passing day proves why that was the right move. 🇺🇸

28

171

1,785

97,270

Railgoon ($eth.eth) retweeted

Jun 13

Every passing day proves Anthropic made the right move.

13

23

1,145

61,889

Railgoon ($eth.eth) retweeted

Oh yes, I remember that Bond film where the villain decarbonized the auto industry, brought fast internet to everyone on the planet, and helped paralyzed people interact with the world again.

Jun 12

Elon Musk is a real-life Bond villain ft.trib.al/zAOuVKk

1,098

6,747

59,275

2,833,928

Railgoon ($eth.eth) retweeted

Jun 12

Over 4000 workers just became millionaires by owning the means of production and the socialists are pissed

286

4,367

37,774

775,189

Railgoon ($eth.eth) retweeted

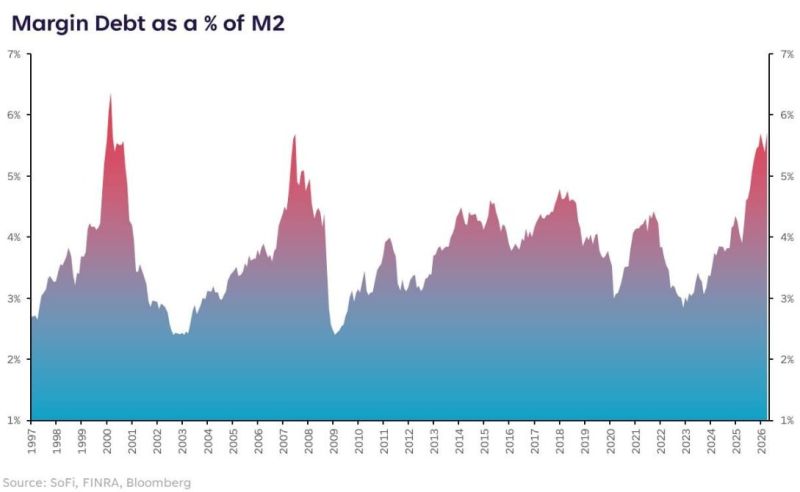

OOPS! Margin debt as a % of M2 is now at its 2nd highest level in history, just behind the Dot Com Bubble. blog.syzgroup.com/syz-the-mo…

21

76

291

40,350

Railgoon ($eth.eth) retweeted

Jun 12

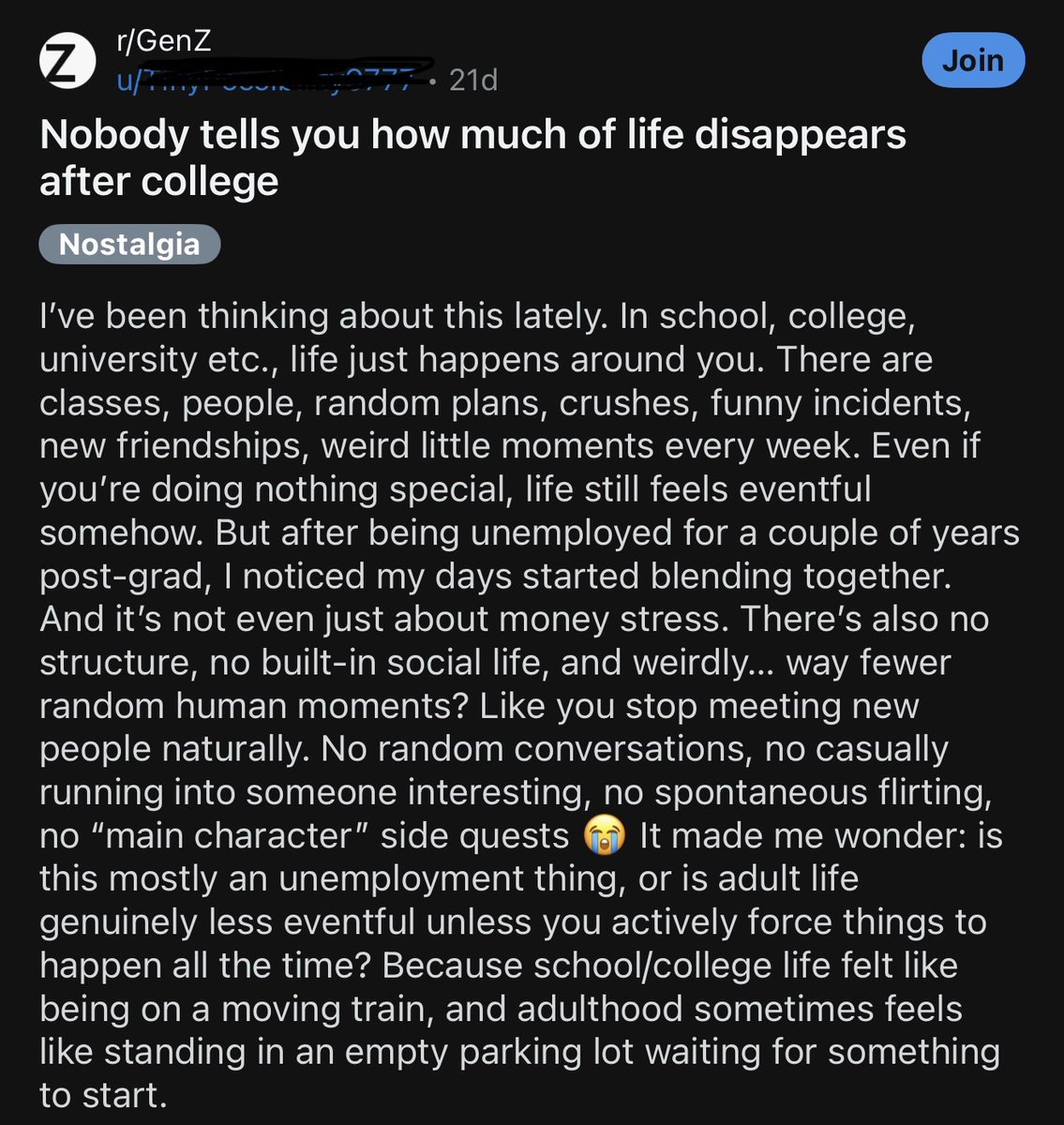

Gen Z realizing one of the biggest shocks after college is that life no longer happens around you.

In school, friends, events, relationships, and opportunities are built into your environment.

As an adult, if you don't actively create a social life, weeks can turn into months surprisingly fast.

448

3,082

34,368

4,251,959

Railgoon ($eth.eth) retweeted

This Memorandum is fictional. You can’t reasonably do all those things with the anticipation that the major dispute item, nuclear ambitions, may fall over within the 60-day period.

Looks like someone is being messed with!

2

6

810

"

Bear Case: Limited Adoption Despite Fee CutFee cut helps modestly, but privacy remains niche (e.g., regulatory hurdles, UX friction, competition).

Annual shielded volume grows 2–5x from current levels but stays small relative to ETH DeFi (~$5–10B annual relevant flows captured at low penetration).

Net revenue: ~$8–15M annualized (volume up, but fee rate down 60%).

Treasury grows steadily; staker distributions ~$4–8M/year.

Yield on staked value: 3–6% (low growth narrative caps multiples).

Price target: $4–8 (1.5–3x from current). MCAP $230–460M. Staked $RAIL benefits from distributions but trades like a modest-yield asset with limited upside.

Rationale: ETH grows, but Railgun captures only marginal private DeFi share. Treasury backs some value, but hype fades without breakout volume.

Base Case: Meaningful Adoption ETH GrowthFee cut drives strong volume growth (10–30x current shielded activity) as Railgun becomes a go-to privacy layer for a solid chunk of ETH DeFi (e.g., 5–10% of private/concerned flows: DEX, lending, etc.).

Annual relevant ETH DeFi volume scales with ETH price/ecosystem (assume 2–4x overall market growth).

Net revenue: $30–80M annualized (volume surge offsets lower fee rate).

Treasury builds faster; staker distributions ~$15–40M/year.

Yield: 8–12% initially, with growth re-rating (comparable to productive DeFi tokens).

Price target: $15–40 (5–15x from current). MCAP $860M–$2.3B. Staked $RAIL offers attractive real yield governance in a growing privacy narrative.

Rationale: Privacy becomes table-stakes for parts of DeFi. Railgun's zk-SNARKs integration ease (wallets, SDKs) win share. ETH bull market lifts all boats.

Bull Case: Dominant Privacy InfrastructureFee cut network effects make Railgun the default private rail for a large slice of ETH DeFi (15–30% penetration on sensitive/high-value volume).

Explosive growth: Shielded volume hits tens of billions annually as institutions, RWAs, and users prioritize confidentiality. ETH ecosystem booms (TVL/volume 5–10x ).

Net revenue: $150M–$500M annualized.

Treasury compounds rapidly; staker distributions $75M–$250M /year.

Yield: 15–30% early, with premium multiples for "must-have" infrastructure (privacy moat, like a DeFi utility).

Price target: $80–200 (25–70x from current, though diminishing returns at scale). MCAP $4.6B–$11B . Staked $RAIL becomes a high-conviction yield growth play.

Rationale: Railgun captures "substantial" volume as privacy regulations tighten or demand surges (e.g., post-mixer scrutiny). Full ETH growth multiplier treasury flywheel. Extreme but plausible in a mature, privacy-focused crypto world.

"

55

Railgoon ($eth.eth) retweeted

Jun 11

"You hate socialism because you want people to starve."

No. You support socialism because you mistake good intentions for good outcomes. History has been paying the price for that confusion for over a century.

127

620

4,549

45,759

Railgoon ($eth.eth) retweeted

This says "over" $5.16 billion, because a significant amount of RAILGUN volume is impossible to measure - it's in private transfers, which can't be seen or counted, and isn't added to the total here!

2

19

931

Railgoon ($eth.eth) retweeted

Jun 11

In Sept 2023 @VitalikButerin co authored a paper on privacy pools (aka PPOI), and @RAILGUN_Project was the 1st privacy protocol to implement it. The result was a significant spike in private volume, showing it plays an important role for users in a pluralistic privacy stack.

13 Feb 2025

This is a solid demonstration of Railgun's privacy pools mechanism ( papers.ssrn.com/sol3/papers.… ) working in practice, allowing Railgun to avoid serving proceeds of crime without using any snooping / backdoors.

How it works:

* Anyone can deposit into Railgun.

* After you deposit, there is a 1 hour period during which various algorithms detect whether or not the deposit likely came from what the algorithms consider to be criminal activity.

* If your deposit passes the filter, then after 1 hour you can use ZKPs to withdraw privately (but ideally wait longer to get a good-enough anonymity set).

* If your deposit fails the filter, then you can only withdraw back to your own address. There is no risk that your funds will get frozen/seized, you just can't benefit from the privacy pool.

If you disagree with Railgun's filters, anyone is free to fork and make their own pool with their own rules, though if you can't get reasonably wide public support you're going to have a tiny anonymity set.

railway.xyz/

2

5

38

2,112

Railgoon ($eth.eth) retweeted

The RAILGUN privacy set has now achieved over $5.16 billion in private volume.

More RAILGUN private volume means a more robust privacy set which leads to support for more private volume. The strength of RAILGUN comes from the constant flow of activity through it.

7

22

155

6,129