Researching companies, industries & charts with custom indicators. This is not financial advice.

Joined August 2020

- Tweets 836

- Following 415

- Followers 660

- Likes 7,267

291 Photos and videos

Pinned Tweet

May 19

I started investing with $20,000.

This was all the money me and my wife saved in 10 years.

My first stock was $LMT.

I bought around $200.

Price dropped.

I got scared.

I sold for around $10 loss.

I thought this is not for me.

A few weeks later I tried again.

I bought $BABA.

Same thing.

In 2018, in Romania, I had a poor relationship with money.

I did not understand risk.

I did not understand volatility.

I did not understand business quality.

I did not understand market cycles.

So I started reading.

Warren Buffett.

Benjamin Graham.

The Intelligent Investor.

Investing for Dummies.

Every investing book I found.

Then I started building my own system.

A system for finding stocks.

A system for reading charts.

A system for buying weakness.

A system for holding when the thesis is alive.

A system for selling when the risk changes.

I made bad decisions.

$WYFI, bought $32, sold $18.

$HIMS, bought $35, sold $20.

$AUR, bought $6, sold $4.

$MDAI, bought $2.30, sold $1.90.

$ARBE, bought $2.20, sold $1.90.

$IREN, bought $60, sold $51.

I also sold too early.

$NBIS at $150.

$BABA at $135.

$OKLO at $110.

$ORCL at $125 before price went near $300.

But I also found serious opportunities.

$META at $101.

$AMZN at $83 after split.

$GOOGL at $85 after split.

$COIN at $34.

$MARA at $3.34.

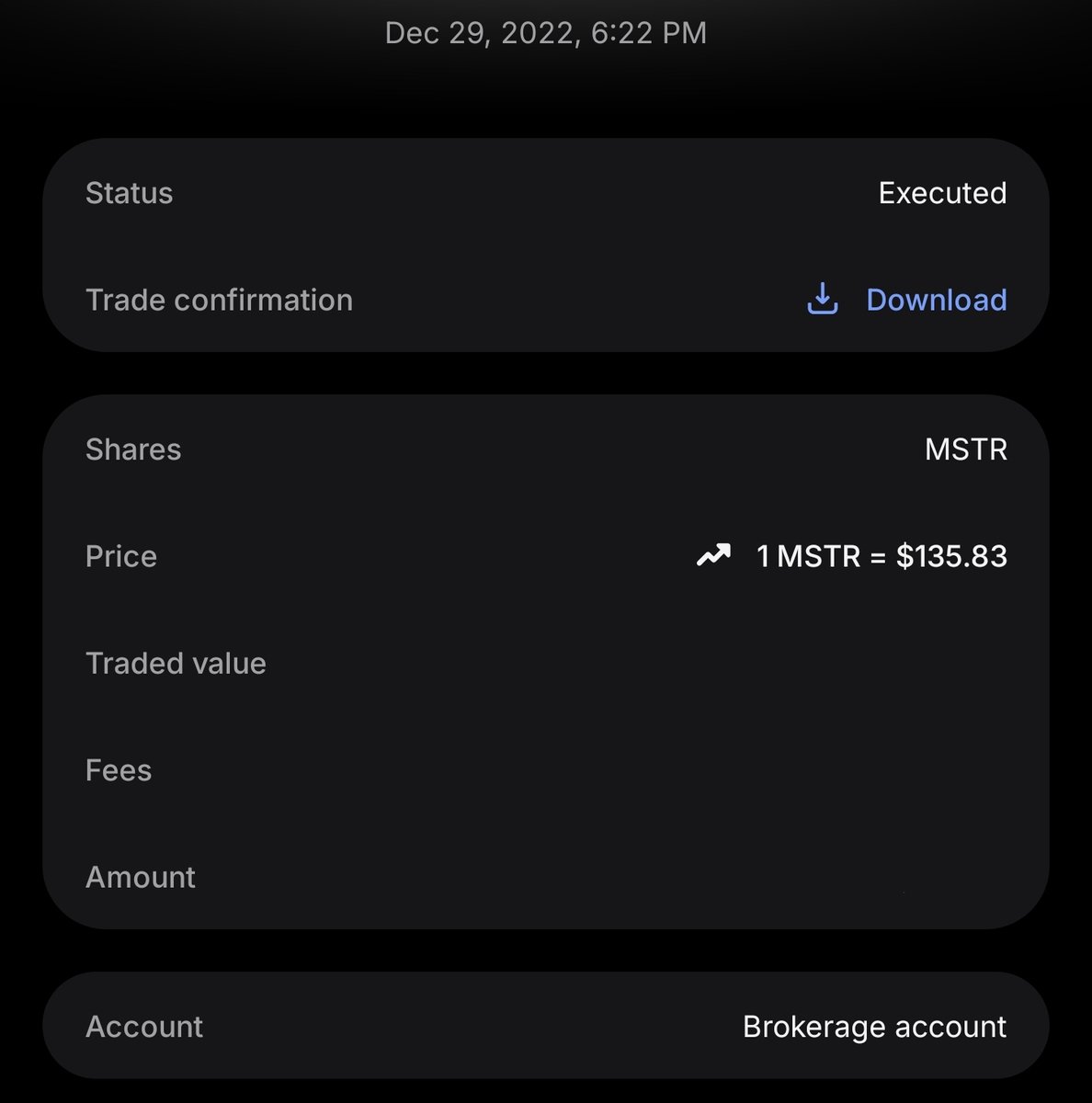

$MSTR at $135 before the 10 for 1 split.

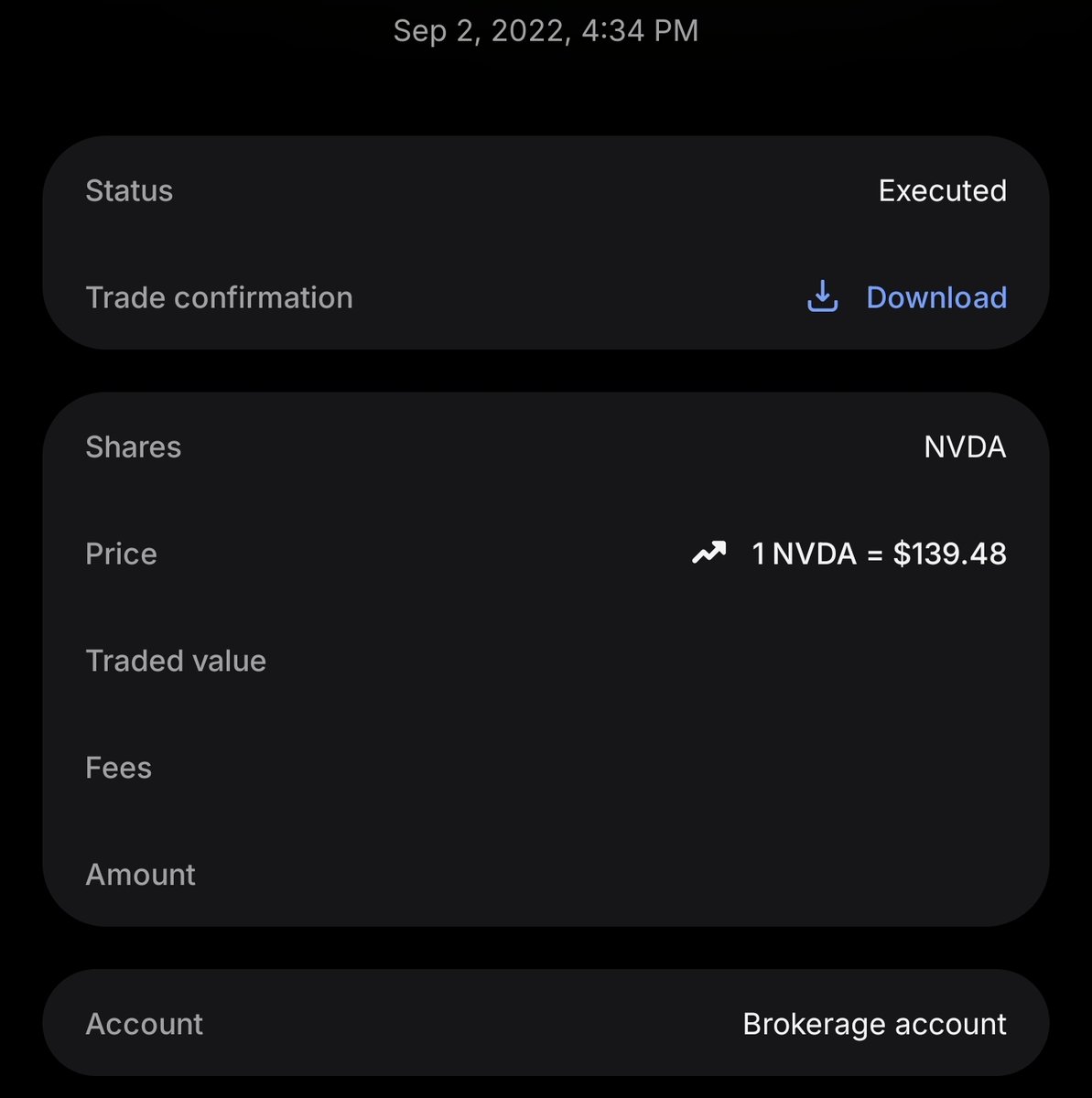

$NVDA at $139 before the 10 for 1 split.

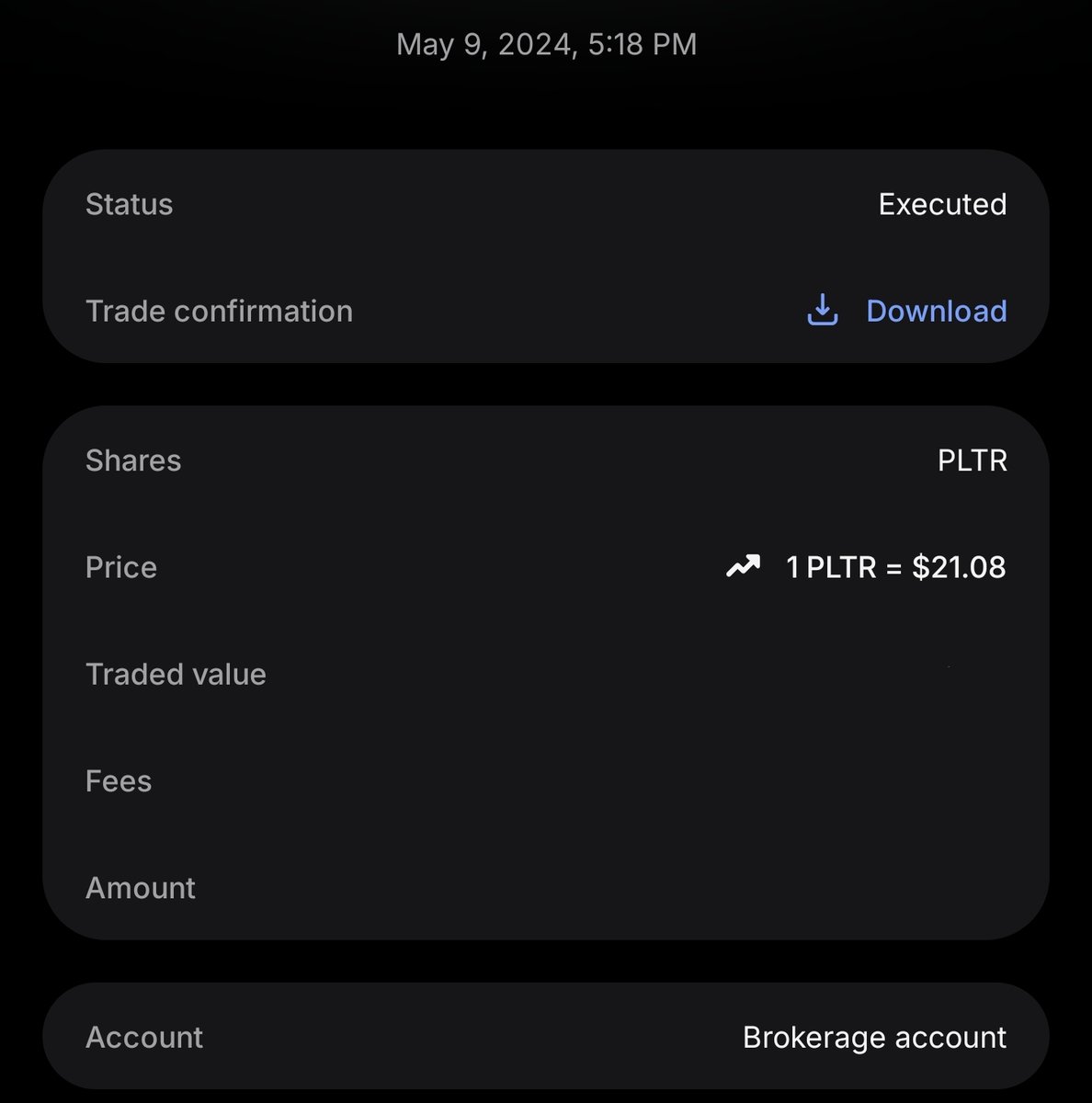

$PLTR at $21.

$ARM at $101.

$RKLB at $23.

$TSM at $64.

$AMD at $58.

$BABA at $64.

$NU at $3.70.

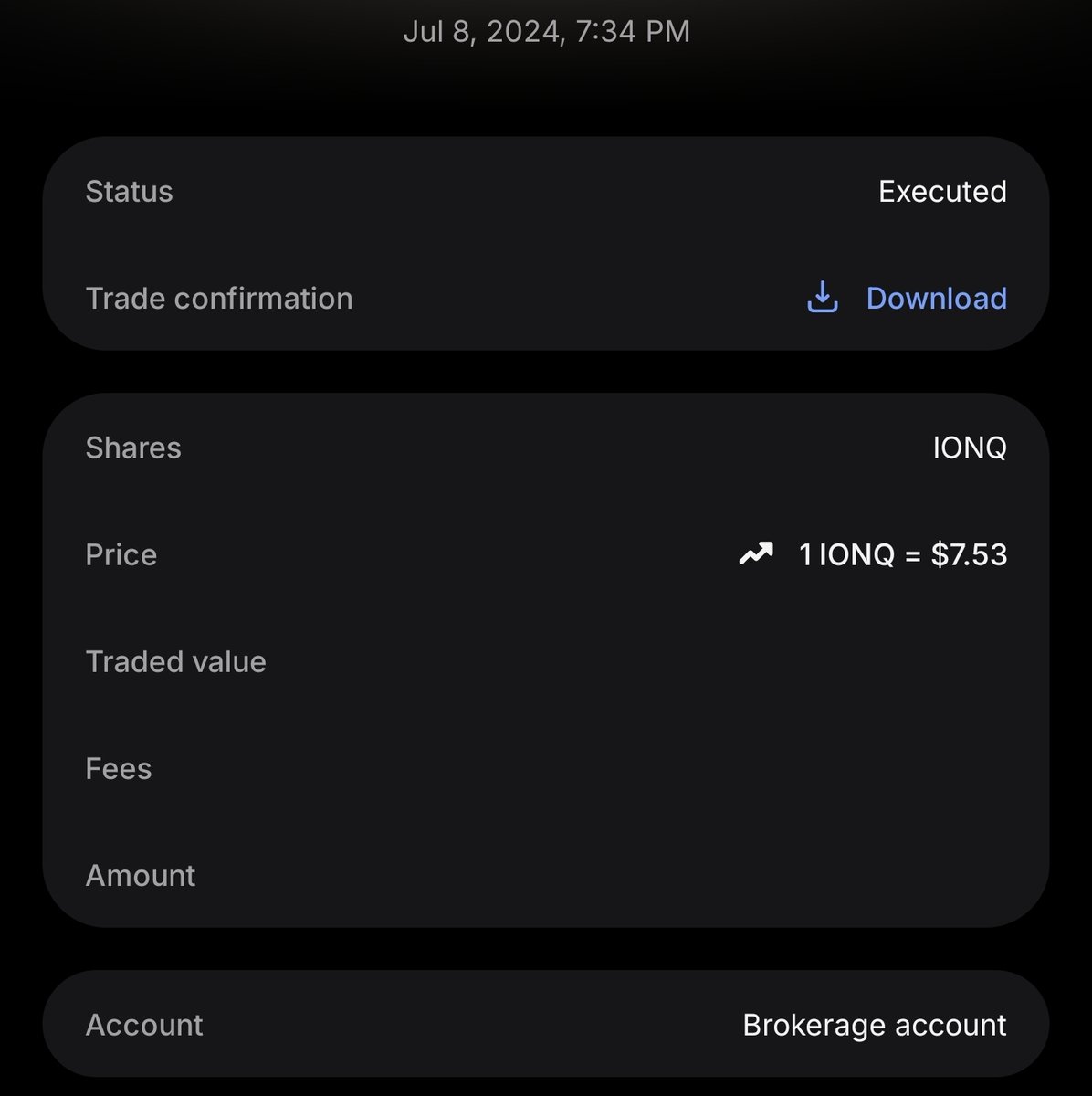

$IONQ at $7.53.

$OKLO at $17.90.

My road was not clean.

I lost money.

I sold winners too early.

I bought some wrong names.

I got scared more than once.

But the good decisions were bigger than the bad ones.

Now my main account is up almost 300% in 5 years.

I am still learning.

I am still improving.

I still make mistakes.

This profile is where I will show how I think as an investor and swing trader.

No fake certainty.

No perfect record.

No theory without skin in the game.

Only process, charts, companies, entries, exits, mistakes, and lessons.

I just want to share my ideas, my charts and my research.

4

1,138

everybody should have a Long Term account, for multiple reasons:

compounding

long term view over the market

relaxing on the bad days: if you have 100% gains on a stock and a bad day comes and is down 10% you are still up (relax)

put money to work while you do your thing

really buying the deep (trading is trading, buying the deep is another trade day, but in long term buying the deep is real and it gives you a reasurance over your initial ivestment.

Gap up or down—doesn’t matter to me because as a genuine long term investor, I keep buying and accumulating along the way.

1

104

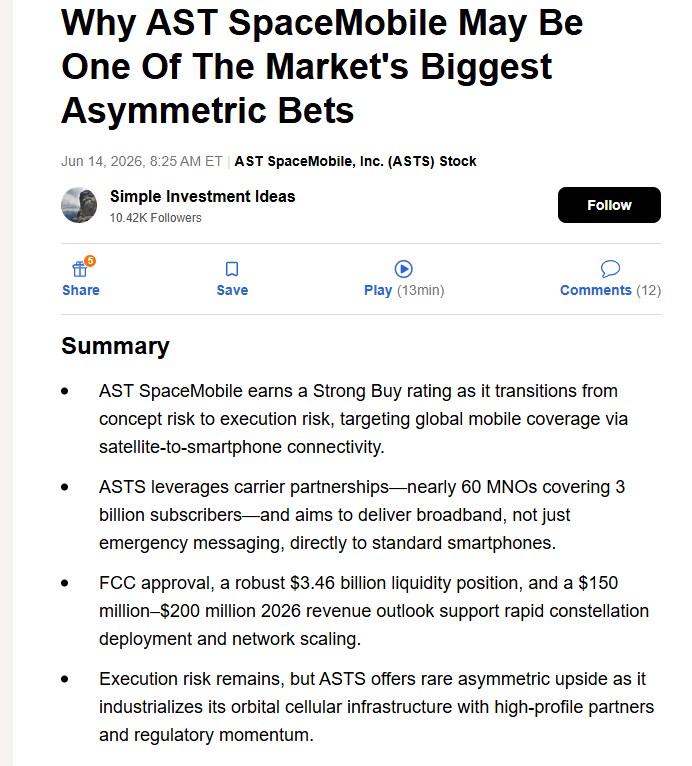

Credit to Dustin @DustinHuntwn for this $ASTS post.

This is a strong summary of the real $ASTS thesis.

My investing journal, not financial advice.

The main point is simple.

$ASTS is moving from concept risk into execution risk.

That is an important shift.

The company is no longer only selling an idea.

It is trying to build and scale a direct to device satellite network for standard smartphones.

Nearly 60 mobile network operator relationships.

Coverage potential across roughly 3 billion subscribers.

A goal to deliver broadband, voice, data, and video directly to phones.

FCC approval supporting satellite deployment.

Around $3.46 billion of total liquidity.

A 2026 revenue outlook of $150 million to $200 million.

That is the real foundation of the thesis.

The upside case is not based on a normal telecom story.

It is based on orbital cellular infrastructure.

If $ASTS executes, it can sit in a rare category:

Global mobile coverage.

Direct to standard smartphones.

Carrier partnerships already in place.

Regulatory momentum.

Large addressable market.

That is why the setup is interesting.

I also like that Dustin framed execution risk clearly.

That is the correct lens.

This is not only about the dream.

It is about launch cadence.

Network scaling.

Carrier activation.

Revenue conversion.

Liquidity runway.

And real service rollout.

For me, $ASTS is a serious watchlist and position name in the space theme.

The story has moved beyond pure concept.

Now price and execution need to confirm.

Strong post by Dustin.

Clear thesis.

Clean structure.

Real claims.

This is the kind of space investing post worth reading.

Price first.

Execution second.

Theme confirmation last.

$ASTS Investment Thesis: Strong Buy

1.AST SpaceMobile earns a Strong Buy rating as it transitions from concept risk to execution risk, targeting global mobile coverage via satellite-to-smartphone connectivity.

2.ASTS leverages carrier partnerships—nearly 60 MNOs covering 3 billion subscribers—and aims to deliver broadband, not just emergency messaging, directly to standard smartphones.

3.FCC approval, a robust $3.46 billion liquidity position, and a $150 million–$200 million 2026 revenue outlook support rapid constellation deployment and network scaling.

4.Execution risk remains, but ASTS offers rare asymmetric upside as it industrializes its orbital cellular infrastructure with high-profile partners and regulatory momentum.

1

315

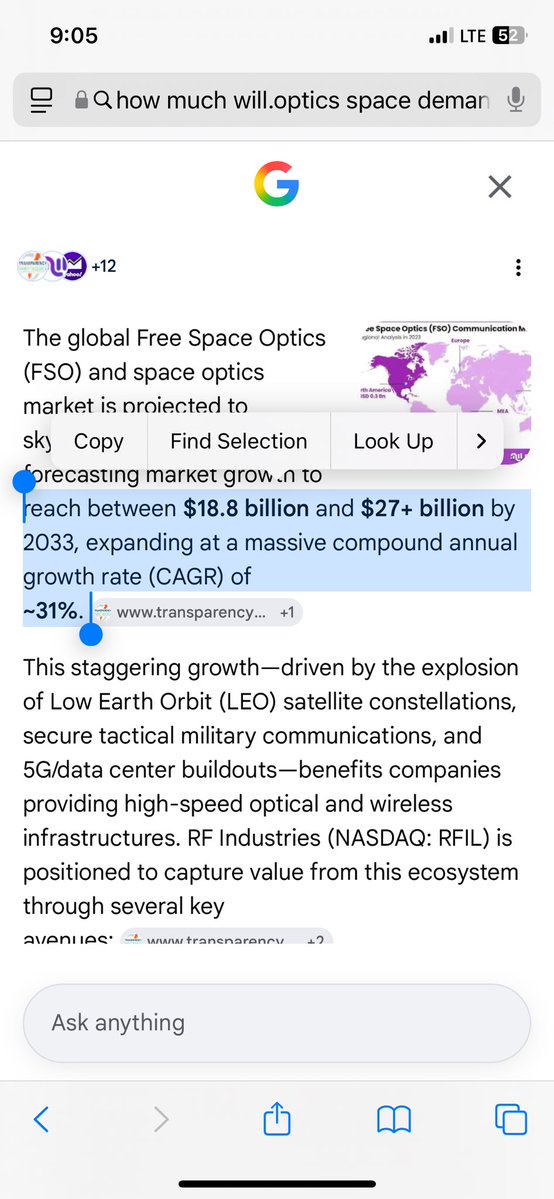

Credit to SemiVision @semivision_tw for this one.

This is the kind of AI supply chain post I like.

Not another GPU headline.

Not another broad AI slogan.

A real component layer.

MLCCs.

The “Rice of Electronics.”

Most people ignore them because they are small, cheap, and everywhere.

That is exactly why they matter.

AI servers need more than GPUs.

They need HBM.

They need CoWoS.

They need PCBs.

They need CCLs.

They need optical modules.

They need cooling.

They also need stable power delivery.

That is where MLCCs come in.

The visible part of the article looks directionally right.

The market size numbers may be a bit bullish versus some more conservative reports.

But the main idea checks out.

High capacitance MLCCs.

Low ESL MLCCs.

Low ESR MLCCs.

AI servers.

EVs.

ADAS.

800V platforms.

5G.

Data centers.

All of these push demand toward better quality passive components.

The real point is simple:

A tiny component can become a real bottleneck if the system cannot run without it.

That is why this post matters.

It looks at the boring layer under the AI trade.

The market usually chases the visible winner first.

Then it starts looking at what the visible winner needs.

Power.

Substrates.

Packaging.

Cooling.

Optics.

Passive components.

That is where the next round of supply chain work starts.

Strong post by SemiVision.

This is the right lens:

Less hype.

More component math.

Less headline chasing.

More bottleneck mapping.

Price first.

Supply chain second.

Theme confirmation last.

MLCCs: The “Rice of Electronics” Becomes a Power Bottleneck in the AI Era

When the market talks about AI servers, the focus usually goes to GPUs, HBM, CoWoS, PCBs, CCLs, optical modules, and liquid cooling. But as AI systems evolve from single servers into rack-scale, and eventually data-center-scale architectures, another long-overlooked component is moving back to the center of the industry’s attention: MLCCs, or multilayer ceramic capacitors.

open.substack.com/pub/tspase…

1

1

92

Credit to @jukan05 for this one.

This is an important semiconductor packaging read.

My market journal, not financial advice.

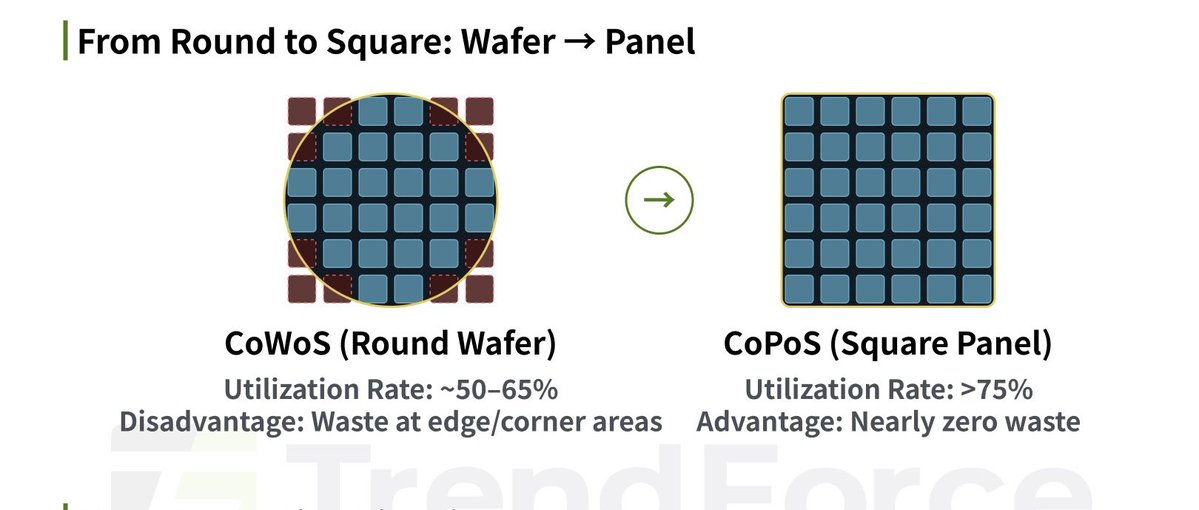

$TSM is reportedly preparing for full-scale mass production of panel-level packaging.

PLP matters because it attacks a simple manufacturing problem:

More usable area.

More output.

Less waste.

Better economics for large AI chips.

Wafer-level packaging is built around a round wafer.

Panel-level packaging uses a rectangular panel.

That can improve productivity because the edge waste problem is reduced.

For AI chips, this matters.

The market is moving from only front-end transistor scaling toward packaging, substrates, interconnect, and throughput.

That is where the next bottlenecks can show up.

The key points from Jukan’s post:

TSMC is building a PLP materials, components, and equipment supply chain.

Mass production could start as early as next year.

Samsung already has PLP experience.

$TSM now looks like it is moving seriously.

A global AI chip customer may already be secured.

Glass substrates could become part of the PLP process.

OSAT companies are also entering the market.

My read:

This is not just a TSMC versus Samsung story.

This is a packaging supply-chain story.

The companies that matter here are not only the foundries.

The real watchlist is deeper:

Panel equipment.

Glass substrates.

Substrate materials.

Inspection.

Bonding.

Advanced packaging consumables.

OSAT capacity.

Yield-control suppliers.

The AI trade keeps moving down the stack.

First the market chased GPUs.

Then memory.

Then CPO.

Then power and cooling.

Now packaging and substrates are becoming harder to ignore.

Good post by Jukan.

This is the right layer to watch.

Not hype.

Manufacturing constraints.

That is where real market structure usually starts.

Price first.

Supply chain second.

Theme confirmation last.

TSMC Preparing for Full-Scale Mass Production of "Panel-Level Packaging (PLP)" Semiconductors

TSMC is set to go head-to-head with Samsung Electronics using "panel-level packaging (PLP)," a next-generation semiconductor packaging technology. PLP can significantly improve the productivity of AI chip manufacturing, and with TSMC hurrying to ready mass production, a contest for leadership with Samsung Electronics—which entered the market first—looks inevitable.

According to industry sources on the 15th, TSMC is building out a materials, components, and equipment (MCE) supply chain to establish its PLP mass-production system. It is currently in discussions with domestic and overseas MCE companies on equipment investment. TSMC is reported to be planning to begin PLP mass production as early as next year, and this is read as a move in earnest toward that goal.

PLP is a technology in which a semiconductor wafer with circuitry already formed is cut into individual chips (dies) and then packaged on a rectangular panel to produce the finished product. It contrasts with "wafer-level packaging (WLP)," which is performed on a round wafer. When chips are packaged on a circular wafer, the edge regions cannot be completed into chips and must be discarded—meaning lower productivity. Running the process on a rectangular panel instead allows chips to be produced with no wasted area. Based on a standard 600×600 mm rectangular panel, roughly five to six times as many chips can be produced compared with the mainstream 300 mm (12-inch) wafer.

The company holding the upper hand in PLP technology is Samsung Electronics. After acquiring the PLP business from Samsung Electro-Mechanics in 2019, it has built up technical capability by applying PLP to mobile application processors (APs) and power management ICs (PMICs).

TSMC, by contrast, had been passive on PLP, given that it had secured its foundry competitive edge with conventional WLP. But the situation reversed as the AI chip market grew explosively—PLP can increase AI chip output and is also advantageous for realizing large-area AI chips. Accordingly, TSMC began pursuing the PLP business from 2024. It is expected to build and run a pilot production line this year and, following performance evaluation, enter large-scale production around next year. It is also reported to have already secured a global AI chip customer.

As TSMC accelerates toward PLP mass production, competition with Samsung Electronics is expected to intensify further. Samsung, too, plans to expand PLP application beyond its existing APs and PMICs to high-performance computing (HPC) chips such as AI semiconductors. Glass substrates, which are drawing attention as a substrate for AI chips, are also likely to be adopted in this PLP process—a point that suggests a leadership battle between Samsung Electronics and TSMC in the next-generation substrate market as well.

An industry official said, "Not only Samsung Electronics and TSMC, but also global outsourced semiconductor assembly and test (OSAT) companies have jumped into the PLP process market in large numbers," adding that "along with fierce competition, market growth is expected."

90

The real issue in silicon photonics is not only the headline technology.

It is material access.

$TSEM and $IQE matter here because the Tower and IQE deal points to something deeper:

InP epiwafer supply.

Optical connectivity.

AI data centre infrastructure.

Advanced silicon photonics platforms.

And the end of the prior IP fight.

That is not a small detail.

If optical I/O moves from promise to procurement, the winners are not only the companies with the best story.

The winners are the companies with qualified supply, material access, capacity, and customer trust.

That is why this post is good.

It looks past the obvious AI headline.

It looks at the bottleneck layer underneath it.

The only part I would frame carefully is pricing power.

The deal supports the thesis.

It does not fully prove exclusive control or guaranteed economics yet.

But as a direction of travel signal, this matters.

Strong post by @yianisz

This is the right lens:

Less hype.

More supply chain.

Less headline chasing.

More material access.

That is where real edge usually starts.

$TSEM quietly fixed the part of silicon photonics nobody wants to model: material access.

The $IQE deal locks InP epiwafer supply and ends the IP fight, which matters more than another AI headline.

If optical I/O moves from promise to procurement, scarce substrate control becomes pricing power.

3

783

Market structure update.

My market journal, not financial advice.

The board is green.

Europe is green.

US futures are green.

Nasdaq futures are leading.

That is the first read.

DE40:

1.47%

FDXM:

1.67%

SPX500:

1.27%

ES1:

2.13%

NAS100:

1.87%

NQ1:

2.91%

SPY:

0.54%

QQQ:

0.59%

The important part is not only that the market is up.

The important part is where the strength is.

NQ is stronger than ES.

Nasdaq is leading the futures move.

That usually tells me risk appetite is back, at least short term.

But I do not want to confuse a green screen with a confirmed trend.

A strong futures move can create a gap.

A gap can hold.

A gap can also get sold into after the open.

So the real test is not premarket strength.

The real test is cash session acceptance.

What I want to see:

SPY holding the open.

QQQ leading after the first hour.

Semis confirming.

Highbeta names holding gains.

Weak stocks not fading immediately.

Volume supporting the move.

What I do not want:

Strong futures.

Weak cash open.

Fast gap fade.

QQQ underperforming after the bell.

Leaders failing into resistance.

For now, the read is simple.

Risk on tone.

Nasdaq leadership.

Positive index structure.

But confirmation still matters.

No blind chase.

Let the open prove it.

Price first.

Relative strength second.

Theme confirmation last.

89

Who benefits from the easing:

Taiwanese companies like VPEC (they grow the special layers on the substrates) and GCS (a foundry that makes optical chips) should get better access to materials in the second half of 2026.

GCS can shift more production back to optical products.

$AXTI (a U.S. company with production in China) was one of the most affected by the original restrictions.

1

11

Bottom line:

This is a short term relief for the optical supply chain that powers AI data centers.

But it’s still a controlled, case by case approval process not a full reopening.

The bigger story is exploding AI demand meeting a geopolitically fragile supply chain.

7

China just approved new shipments of InP (Indium Phosphide) substrates in late May 2026 the first significant batch of the year.

This is a partial easing of export controls that started in Feb 2025. Those controls created a major bottleneck for high-speed optical components used in AI data centers.

▶ China eases InP substrate exports, lifting compound semiconductor supply

• China has approved new shipments of export-controlled InP substrates. Following partial approvals in 2025, the first 2026 batch shipped in late May, easing capacity bottlenecks in the optical communications market.

• Taiwanese compound semiconductor players such as VPEC and GCS are expected to benefit from 2H onward as InP substrate supply loosens.

• China began restricting substrate exports in February 2025, cutting off shipments from the China production base of US-based AXT. The incumbent InP substrate market has been dominated by AXT and Japan’s Sumitomo.

• As optical communications grows in importance for high-speed datacenter transmission, access to InP material has emerged as the single largest capacity constraint across the compound semiconductor supply chain.

• China’s InP substrate exports run under a closed-loop control regime: epitaxy houses, foundries, and end customers must submit proof of production and demand before export volumes are reviewed and approved.

• After approving exports of 8,000 InP substrates in August 2025, China cleared an additional 4,000-substrate shipment in late May 2026. These substrates will go through epitaxy at upstream players such as VPEC before being supplied to compound semiconductor makers.

• GCS’s US 4-inch fab carries capacity of 4,500 substrates/month, or 50,000/year, but the InP shortage meant it had largely been running RF components, with optoelectronics making up just 25% of output.

• With the InP shortage temporarily easing, GCS expects shipments to recover gradually from July–August 2026, and growth in its in-house optoelectronics revenue should support 2H26 earnings and margins.

• GCS’s revenue mix is 70% optoelectronics and 30% RF components, and the company plans to further expand optoelectronics capacity to improve profitability.

• With the optical communications market set to enter a phase of explosive growth in 2027–2028, GCS projects PD demand to expand to over 40,000 units/year by 2028. It is anchored on 100G PDs while gradually ramping 200G PD capacity.

• GCS has completed development of 70mW and 100mW CW laser products but, given certification timelines and technical barriers, has invested in Wellywave Semiconductors to build laser production capacity in Taiwan and scale up mass production in 2027.

1

67

Why it matters:

AI clusters need insanely fast data movement between GPUs and servers. Optical transceivers (lasers photodetectors) are the best way to do this at scale.

InP substrates are a critical raw material for making many of those highperformance components.

Supply was tight because production is highly concentrated and China controls a lot of the key raw material (indium).

1

29

Spot on as always @aleabitoreddit

The Iran Strait peace deal just crushed the biggest macro headwind (oil inflation fears), rate hike odds are collapsing, and we’re getting fresh AI infra tailwinds on top:

• 800VDC acceleration for $WOLF

• InP bottleneck easing for $LITE

• $SPCX monster IPO firing up risk appetite space theme

Trump stacking every chip before midterms.

Bears are fighting way too many catalysts at once.

Yep, very stupid to be a bear.

When Trump is doing everything to boost markets before Midterms.

On top, your $WOLF power semi basket should go brrr from 800 VDC acceleration.

$LITE optical basket should go brrr from InP easing.

$SPCX successful IPO gives more appetite to risk on themes/IPOs (eg. Space sector).

And overall macro go brr from War/Strait peace deals.

It’s already kind of showing, since 2026 rate hike odds also crashed from 65% -> 35% following the news. Along with crude futures dropping.

I've actually found Europe to be the most price sensitive to Iran tensions, so EU markets would probably be the most bullish overall…

(South Korea/TW was originally with Sk Hynix moving directly in correlation to crude oil futures, but stopped caring after awhile).

But basically: Murica go brrrr.

268

Real talk on the 800V theme 🔥

Infineon and $NVTS are legitimately deep in NVIDIA’s 800V HVDC push for nextgen AI data centers, while $WOLF remains the SiC tech leader for highvoltage EV inverters (Gen 5 just dropped).

High conviction but $WOLF definitely carries execution risk after the restructuring. Solid call either way.

3

853

Great deep dive on $TOYO @HunterAllen4 👏

Really well put together, it’s great how you broke down the financials, the Houston expansion, the supply agreements, and the clear valuation disconnect vs. peers. Solid work highlighting the U.S. solar reshoring angle.

Appreciate the detailed write-up.

$TOYO

Up 250% over the past year.

Down 10% this week.

One of the more interesting disconnects in U.S. solar manufacturing.

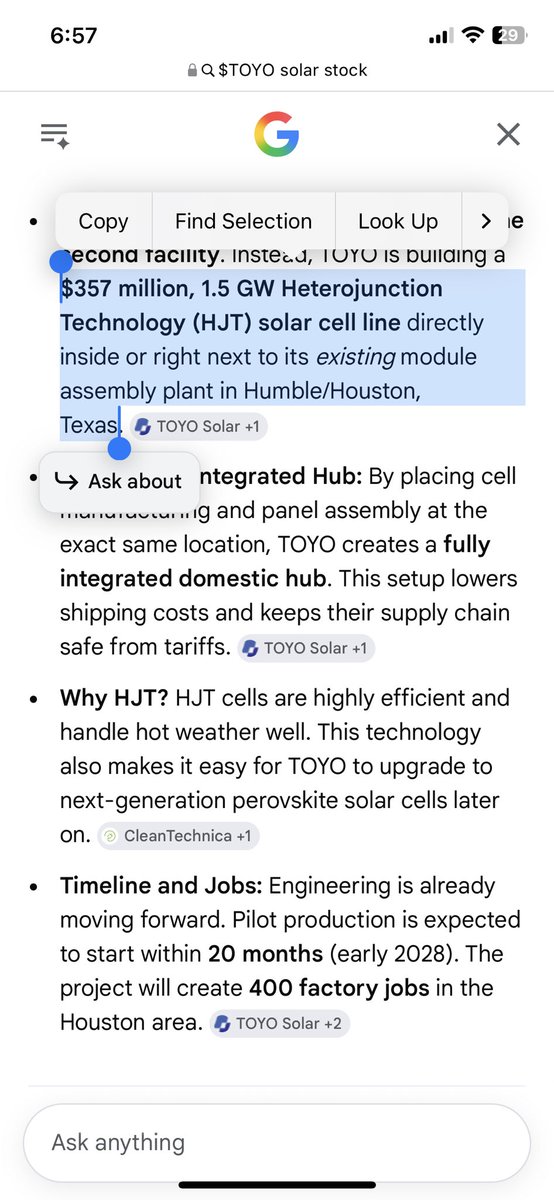

Last week A company valued at roughly $500M just announced a $357M investment into a new 1.5GW HJT solar cell facility in Houston.

That’s more than 60% of its entire market cap being deployed into expansion.

Here I am reminding you about this company again.

Repost. Bookmark. Subscribe to support.

Everyone talks about $FSLR, $CSIQ, tariffs, domestic content requirements, and the future of U.S. solar manufacturing.

Almost nobody talks about $TOYO.

That’s what makes it interesting.

At roughly a $500M market cap, TOYO remains one of the smallest publicly traded ways to gain exposure to the reshoring of solar manufacturing in the United States.

The market currently values TOYO like a small solar manufacturer.

Management increasingly sounds like a company trying to build a vertically integrated U.S. solar platform.

And the numbers are starting to support that narrative.

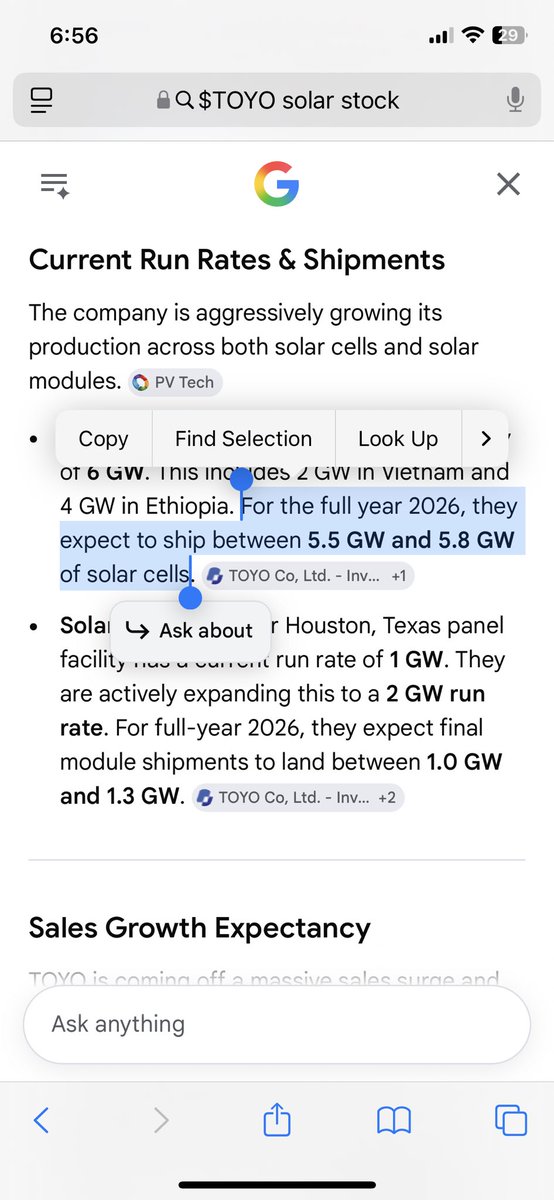

Q1 2026 revenue grew 177% YoY to $142.8M.

Net income improved to $28.4M.

Gross margins remained strong at roughly 33.5%.

Management reaffirmed 2026 guidance for:

• 5.5–5.8GW of solar cell shipments

• 1.0–1.3GW of solar module shipments

• $90–100M adjusted net income

More importantly, demand continues to accelerate.

Last week TOYO announced approximately $185.6M in master supply agreements with major U.S. solar developers.

Projects span Texas, New York, and Maine.

Those orders provide visibility into future revenue while supporting the company’s module shipment ramp.

The market tends to focus on reported revenue.

The smart money watches future revenue.

That’s where backlog, purchase agreements, and production capacity become important.

The bigger catalyst may be TOYO’s decision to aggressively expand U.S. manufacturing.

The company plans to build a 1.5GW HJT solar cell facility adjacent to its Houston module operations.

HJT technology is expected to be among the highest-efficiency solar technologies deployed in the U.S.

The facility could also generate up to $60M annually in IRA production tax credits at full capacity.

That’s a meaningful number relative to the company’s current valuation.

The strategy is becoming increasingly clear.

Build a domestic supply chain.

Utilize non-Chinese wafer sourcing.

Position products for domestic content requirements and FEOC compliance.

Capture demand from developers seeking U.S.-friendly solar solutions.

This is where the valuation disconnect starts becoming noticeable.

$FSLR carries a market cap measured in the tens of billions.

$CSIQ is valued around $1B.

Many solar and energy-transition names command significantly higher valuations despite slower growth.

$TOYO sits around $500M.

Not $5B.

Not $10B.

Around half a billion dollars.

The market is effectively assuming TOYO remains a niche solar manufacturer.

The bull case is that management successfully executes the Houston expansion, converts growing demand into revenue, scales domestic manufacturing capacity, and becomes one of the more important U.S.-focused solar supply chain players over the next several years.

If analyst estimates near $830–850M of 2026 revenue prove accurate, the stock appears inexpensive relative to its growth profile.

That’s why some investors see asymmetric upside here.

Not because TOYO is already operating at First Solar’s scale.

@Twills08 @TapeVector

Not because execution risk doesn’t exist.

But because the valuation remains small compared to the opportunity management is pursuing.

$SEDG $FSLR $TYGO $EOSE $NBIS $FCEL $FRMI $OKLO $HYLN $IREN

But at roughly a $500M valuation, the market may not be fully pricing in what successful execution could look like.

That’s the disconnect worth watching.

1

1

2

336

Jun 14

This is a good lesson for everyone no matter how experienced you are, you can make mistakes, but the biggest mistake of all would be holding desperate to stock that may never come back.

Just move on because the faster move on the faster you recuperate, and the fester you learn the lesson the faster you grow.

@TT_stocks_ is one of the greats from whom you can learn a lot just by following and reading his posts, this is all real no bs.

@TT_stocks_ you are great man even on your bad days you still find the power to learn and to teach. In one word #awesome

Jun 14

I want to make one thing clear about what happened last week with $MMA ..

I alerted this in the .60s and it ended up running to 1.06 in a few days on nice volume.

I was up over $250,000 and then Moomoo took away the buy button and the stock fell off the face of the earth.

I ended up losing $162,000 on the play total, but it’s more than less another lesson that greed will kill you every single time.

I could’ve at any time took $50,000/$100,000/$150,000/$200,000 profits, but I went with my own conviction and wanted more.. unfortunately some serious bad luck happened (it happens more often that you think in this industry) and I got myself bagged.

The next part is the most important here.. no I am not holding this and bag holding and praying it comes back. I had hundreds of thousands into it and believe me when I tell you that I can find better opportunities to get my money back rather than bag holding a stock im red in.

There are 10 opportunities per day to take advantage of, go find them instead of bag holding a play that may never come back.

3

1

10

1,633

Jun 14

Great find @HunterAllen4

Really solid and well-researched breakdown on $RFIL

The financials, backlog numbers, and aerospace orders all check out nicely.

Appreciate you highlighting these overlooked infrastructure plays.

Excellent work as always!

Jun 14

$RFIL

Earnings June 15th. Tomorrow.

One of the more overlooked fiber infrastructure stories in the market.

HAPPY SUNDAY X FAM

REMEMBER $OCC YEAH YOU KNOW ME?

Up 360% past year and overlooked.

Almost nobody is looking at the companies actually connecting the data.

Here I am reminding you again. Keep following for new ideas off most retails radar.

Subscribe to support the grind!

Everyone talks about $NVDA. $LITE. $NBIS

Everyone talks about $GLW.

Everyone talks about transceivers, optics, AI clusters, data centers, and hyperscale spending.

Almost nobody talks about $RFIL.

At roughly a $200M market cap, RF Industries sits at the intersection of fiber optics, telecommunications infrastructure, edge data centers, aerospace communications, and thermal management.

The market still largely views RFIL as a traditional telecom supplier.

The numbers are quietly improving.

FY2025 revenue increased 24% to $80.6M.

Gross margins expanded from 29.1% to 33.2%.

The company swung from an operating loss in FY2024 to an operating profit in FY2025.

Q1 FY2026 gross margins expanded another 250 basis points to 32.3%.

Adjusted EBITDA increased 22% YoY.

Non-GAAP net income reached $659K.

Most importantly, backlog continues moving higher.

Q1 backlog stood at $14.4M.

Shortly after quarter-end it climbed to approximately $18.6M.

That’s where the backlog story becomes interesting.

But the bigger story may be the evolution of the business itself.

RFIL is no longer relying solely on traditional telecom spending cycles.

The company has expanded into:

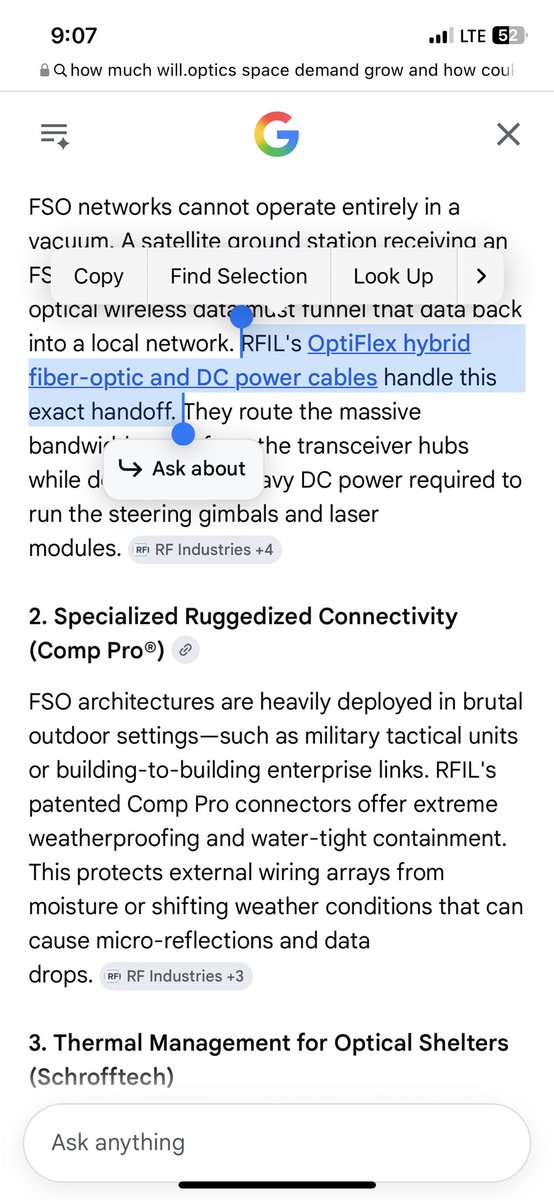

• Aerospace and satellite cabling

• Mission-critical military and government applications

• Hybrid fiber power solutions

• Edge data centers

• Direct Air Cooling systems

• Broadband and wireline infrastructure

The aerospace opportunity may be bigger than most investors realize.

RFIL has now secured multiple follow-on orders totaling more than $4M from what management describes only as a “leading aerospace company.”

Not a one-time order.

Repeat business.

Mission-critical custom cabling designed for extreme environments, including radiation resistance, temperature fluctuations, weight reduction, and high-reliability communications.

Defense platforms. $LMT $NOC

The products RFIL builds fit directly into the infrastructure required by companies like $ASTS, $RKLB, and potentially even $SPCX.

No, there is no public confirmation tying RFIL to any of those names.

But that’s precisely what makes the opportunity interesting.

The space economy is expanding rapidly.

Thousands of satellites are being launched.

Direct-to-cell networks are being built.

Rocket launches continue accelerating.

RFIL doesn’t need to be the prime contractor.

It simply needs to be a trusted supplier of the critical components that make those systems function.

Another underappreciated asset is RFIL’s relationship with $GLW.

Through its subsidiary operations, RFIL holds Corning Gold certification, one of the highest levels of qualification within Corning’s fiber ecosystem.

That gives $RFIL credibility, access to premium fiber solutions, faster fulfillment capabilities, and positioning within one of the most important optical networking ecosystems in the world.

This is where the valuation disconnect starts showing up.

$GLW carries a market cap north of $60B.

$AAOI is valued in the billions.

$CIEN, $LITE, $APH and other connectivity leaders command significantly larger valuations due to their perceived exposure to networking and AI infrastructure growth.

$RFIL sits around $200M.

Not $2B.

Not $20B.

Just a few hundred million dollars.

Tomorrow’s earnings matter less for the quarter itself.

$RFIL is helping build the fiber, cabling, cooling, and connectivity infrastructure that allows those systems to communicate, Satellites too.

That’s the disconnect worth watching.

1

2

279

Jun 14

Brilliant visual.

This perfectly shows why the industry is shifting from round wafers (CoWoS) to square panels (CoPoS):

• CoWoS (current TSMC standard, used heavily by NVIDIA): 50-65% utilization edge waste

• CoPoS (TSMC’s next-gen panel-level): >75% utilization, near-zero waste

Bigger packages, lower cost per chip, and better scaling for massive AI accelerators. TSMC is leading both, while Samsung is also advancing its own FOPLP/panel tech.

Panel-level packaging isn’t just the future it’s becoming necessary.

Great explainer @jukan05

6

489

Jun 13

This is a great read on $COHU . I recommend it.

I like it because it looks past the obvious AI names.

Everyone talks about GPUs.

Fewer people ask:

Who tests them?

Who manages the heat?

Who checks yield?

Who inspects the memory stack?

Who keeps the production line moving?

That is where the better supply-chain work starts.

$COHU is interesting because the market still treats it like a cyclical semiconductor equipment name.

But the business is getting exposure to:

HPC processors.

HBM inspection.

GaN power devices.

Advanced packaging.

Thermal test systems.

AI-powered yield optimization.

Recurring consumables and services.

That does not make it an automatic buy.

Price still matters.

Execution still matters.

Cyclicality still matters.

But the framework is right.

The AI trade is not only $NVDA .

The better question is:

Which companies sit underneath the AI supply chain and become more important as the chips become harder to make?

Good work by @HunterAllen4

This is the type of research angle I respect.

My investing journal, not financial advice.

Jun 13

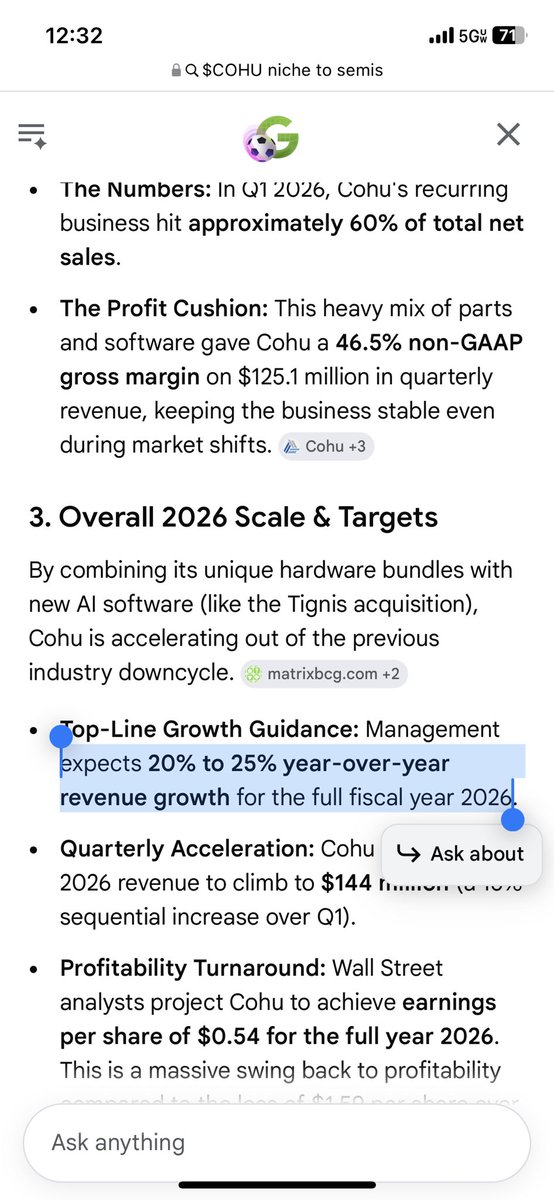

$COHU

5% yesterday.

Testing 26-year highs.

DONT MISS X FAM

Everyone talks about GPUs.

Almost nobody talks about the companies making sure those GPUs actually work.

$AEHR $TER $AMKR $FORM all getting attention in silicon testing bottleneck.

Cohu ($COHU) sits in one of the most overlooked bottlenecks in semiconductors: testing, thermal management, inspection, and yield optimization.

Some things that stood out:

• Top-3 global semiconductor test handler provider with ~20-28% share of a $2.1B market.

• Global leader in RF power amplifier testing used in 5G and automotive systems.

• Roughly 14% share of the global test contactor/socket market.

• ~60% of revenue comes from recurring sources including consumables, spares, services, software, and maintenance.

Q1 2026:

• Revenue: $125.1M ( 29% YoY)

• Orders: 57% YoY

• Test handler orders: 54%

• Inspection/metrology orders: 64%

• Cash & investments: $489M

Management raised FY26 growth outlook to 20-25%.

The AI story is getting bigger too.

Cohu increased expected HPC revenue to $80M-$100M in 2026 and expanded its AI/HPC addressable market estimate to roughly $750M.

That’s a massive jump from prior expectations of just $25M-$30M.

Why?

Their Eclipse platform is designed for next-generation AI processors that generate enormous amounts of heat during testing.

Their T-Core thermal systems provide the precision temperature control needed for AI accelerators, GPUs, and HPC processors where thermal issues directly impact yields.

In May, they secured major Diamondx platform orders tied to Gallium Nitride (GaN) power devices being deployed throughout AI data center power infrastructure.

Another overlooked catalyst:

In 2025 they acquired Tignis for $40M.

Tignis brings AI-powered digital twins, predictive maintenance, machine learning analytics, and yield optimization software that is now integrated into Cohu’s DI-Core platform.

Instead of simply testing chips, they’re increasingly using AI to predict failures before they happen.

This gives them exposure to both semiconductor equipment and semiconductor software.

Meanwhile HBM demand continues ramping.

Their NEON inspection platform is positioned around HBM3 and HBM4 production with AI-powered optical inspection, metrology, and yield analytics.

The market still largely views COHU as a cyclical semiconductor equipment company.

But the business is increasingly becoming an AI infrastructure enabler with exposure to HPC processors, HBM memory, GaN power systems, advanced packaging, factory AI software, and high-margin recurring revenue.

Everyone knows $NVDA.

Few are looking at the companies that test the chips, manage the thermals, inspect the memory stacks, optimize yields, and keep production moving.

That’s where $COHU plays.

A picks-and-shovels AI infrastructure name sitting underneath the semiconductor supply chain.

$MRVL $ICHR $VECO $AMD $AAOI $POET $MU $AVGO $ONTO $LITE

If management executes, the valuation gap between how the market views COHU and what the business is becoming may be the opportunity.

1

1

2

478

Jun 13

Exactly. $SPCX IPO vacuumed up capital and hammered everything else today, but this is the siphon effect not a broken thesis. The real businesses with catalysts are now on sale. Watching $RKLB , $PL closely. Already added some $ASTS

$SPCX debuts at a ~$2.3T valuation 🚀 and every other space stock gets torched. $RKLB $ASTS $RDW $LUNR $PL $FLY all down double digits. 👀

This is the siphon effect and it's the opportunity, not the end. Here's what's next 👇

What just happened: capital rotated OUT of the listed space names and INTO the marquee IPO. Classic sell-the-news. It hit stocks that were already up 300% on the year, so it's a reversal off strength, not a broken thesis.

What it misses:

→ $SPCX listing doesn't make $RKLB's Neutron or $ASTS's direct-to-cell network worse businesses. It validates the entire $28T space TAM they all operate in.

→ Most people can't get $SPCX shares -> allocation is tiny. The listed names are the ACCESSIBLE way to own the space buildout.

→ $SPCX barely competes head-to-head with the differentiated names. Different orbits, different markets.

The pattern: a marquee IPO siphons the sector on debut day, then the real businesses with their own catalysts recover as the liquidity comes back.

Everyone's chasing the $2T name they can't get.

I'm watching the ones that just went on sale. 👀

2

537

Jun 13

Really enjoyed this. The sovereign race framing the contrast with dotcom era spending makes a lot of sense. AI demand is already showing up across way more verticals than people realize

Just a short opinion piece on whether AI is a bubble:

The bubble case mainly stems from one argument: hyperscaler CAPEX outpacing near term ROI.

That argument is not crazy. The CAPEX numbers are real, and also the revenue lag is real.

The main reason it’s not a bubble to me?

This is a sovereign race, not a corporate capex cycle.

Every major government has now framed AI as a national priority. The US, China, EU, India, the Gulf states are all spending into this with strategic intent. Whoever runs the best models reaps the productivity lift, the defence advantage, and the export leverage.

It’s very similar to the space race previously, except now the impacts are more broad based.

Countries do not opt out of arms races to wait for better unit economics.

That is the floor forming the foundation AI CAPEX, which is direction of the state.

On top of that:

Corporate capex is not funded like 1999.

Over $400B combined annual operating cash flow from MSFT, GOOG, META, AMZN

Roughly one-third reinvested into AI infrastructure

Nvidia at ~25x forward earnings, Microsoft at ~30x.

Elevated, not Cisco at 200x.

Dotcom was VC dollars chasing companies with no revenue. Whereas this is profitable monopolies reinvesting their own free cash flow.

Additionally, demand surface is broad.

> Physical AI in robotics and manufacturing

> Drug discovery and diagnostics

> Fraud detection and underwriting

> Code generation

> Defence, logistics, energy, agriculture

> and many more

These applications are already shipping across the economy.

That does not mean every AI stock is a buy. There will always be names trading on vibes that get cut in half.

But the structural setup is not 1999. Your job as a good investor is to find the companies that benefit from this tailwind the MOST, and aggressive aggressively if you want to escape the permanent underclass which will be an implication of AI (imo).

That is my goal for the next 5-10 years.

Just my 2c. Thanks for reading.

1

2

1,023

Jun 13

Again some words of wisdom. The inner voice should be treated as data.

The most dangerous day in markets isn’t the crash. It’s the green week before it when every position works, every dip gets bought, and a voice says “you’re better at this than you thought. Size up.”

Twenty-six years of running money and businesses taught me to treat that voice as data. Not about the market -> about me. Feeling invincible isn’t insight; it’s the same brain state as not being able to judge risk.

But here’s the other half, and it matters just as much: investing is buying great businesses - great future growth, great executive teams - and owning them. Once you’ve done the work and earned conviction, don’t let noise and price scare you out, either.

Euphoria sizes you up. Fear shakes you out. Both are the same mistake: letting emotion, not analysis, make the decision. Tudor Jones said play great defense and defense cuts both ways. Protect your capital from your greed and your conviction from your fear.

1

3

305