Joined November 2025

- Tweets 181

- Following 48

- Followers 10

- Likes 15

Photos and videos

Thorsten Huber retweeted

Jun 3

EU CHIPS Act 2.0 proposal is now released.

Great news: Photonics is now confirmed to be the new structural addition to EU policy.

This is thematically bullish for the EU photonics sector.

Thematically:

- "This new component of the Chips for Europe Initiative supports the development of photonic integrated circuits and associated technologies"

- "building and strengthening advanced design, prototyping, and industrial deployment capacities for photonic integrated circuit technologies and other photonic technologies across the Union"

- "extend the Union’s design capabilities, including in photonics"

- "strengthen existing and develop new pilot lines and open-access semiconductor manufacturing facilities for the prototyping and production of photonic integrated circuits and associated photonic technologies

- "develop and maintain design libraries and design automation tools for photonic integrated circuits, associated photonic technologies"

===

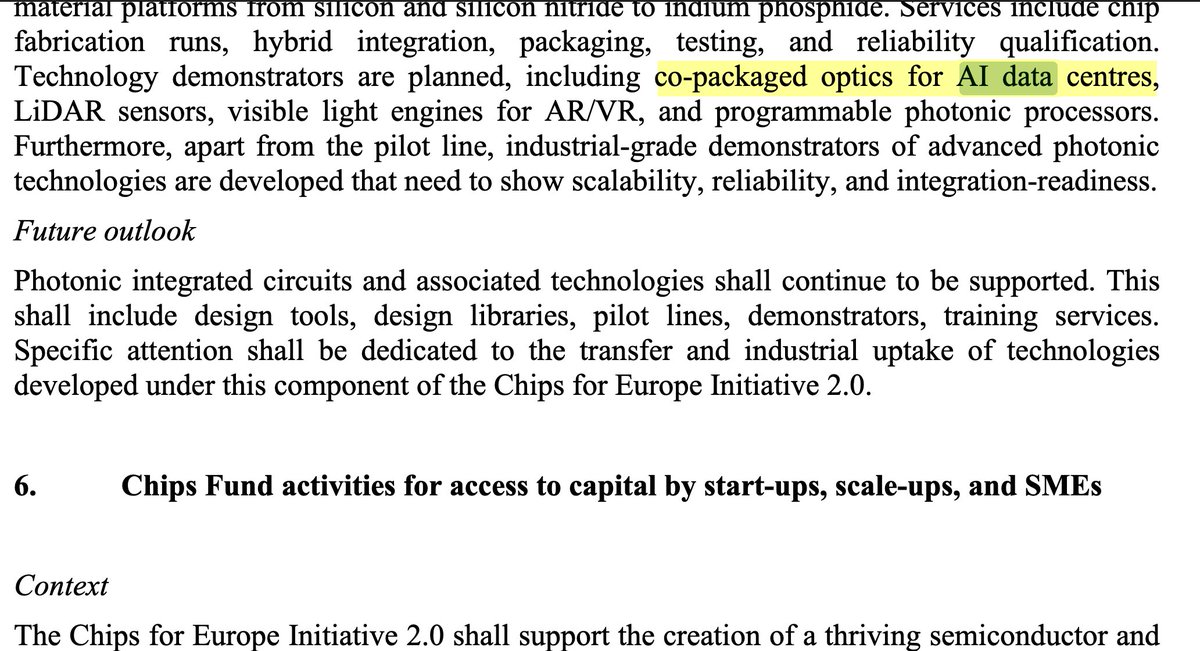

More specifically policy specifically focuses on

-> co-packaged optics for AI data centres (CPO/interconnects focus is bullish read through for $SIVE)

-> “Silicon photonics … applications in high-bandwidth data-centre interconnects…”

-> Capabilities in production technologies including co-packaging and heterogeneous integration with electronic chips, manufacturing equipment, and materials platforms for photonic integrated circuits shall be strengthened ( $XFAB)

-> $SOI directly mentioned in impact analysis regarding structural strengths of the EU. "The EU has a relatively strong global position in SOI wafers, with Soitec and Siltronic being notable players"

-> $XFAB also directly mentioned in impact analysis, as part of creating the current funding framework.

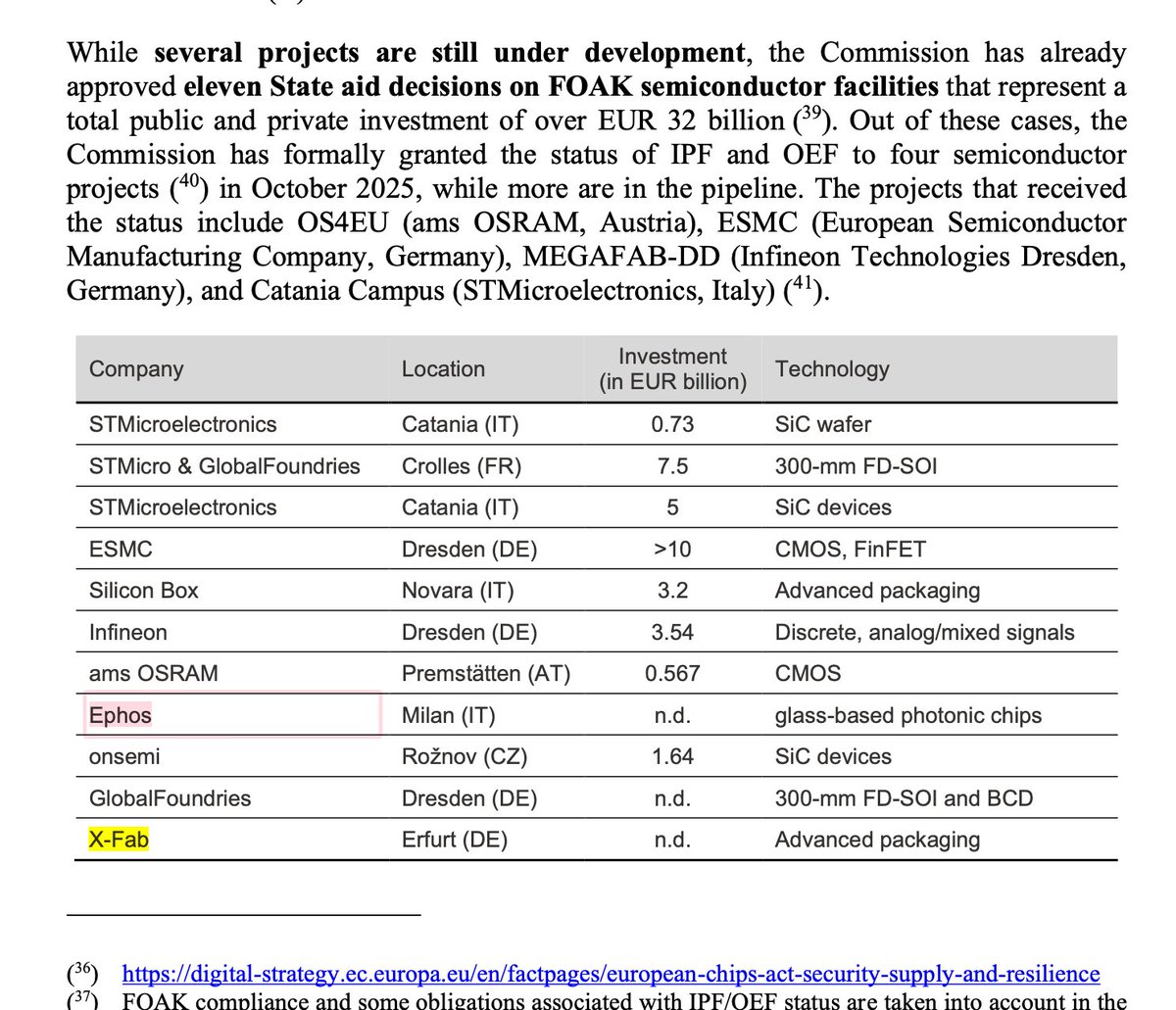

Obviously structurally positive for $XFAB since they're literally leading the European Silicon Photonics Value chain and listed in First of a Kind (FOAK) category.

Initial interpretation, this is heavily positive for EU photonics leaders that go inside AI DCs as part of EU Policy. I'm expecting optical players broadly to get a tailwind from this framework.

TLDR: EU photonics structurally go brrr long term. Most positive confirmation is that photonics is structurally a part of European Union policy now.

We'll likely see the individual photonics names come out after this release, within 3-15 months (typically in the middle somewhere). Markets are forward looking in general.

170

124

1,568

370,973

Thorsten Huber retweeted

May 18

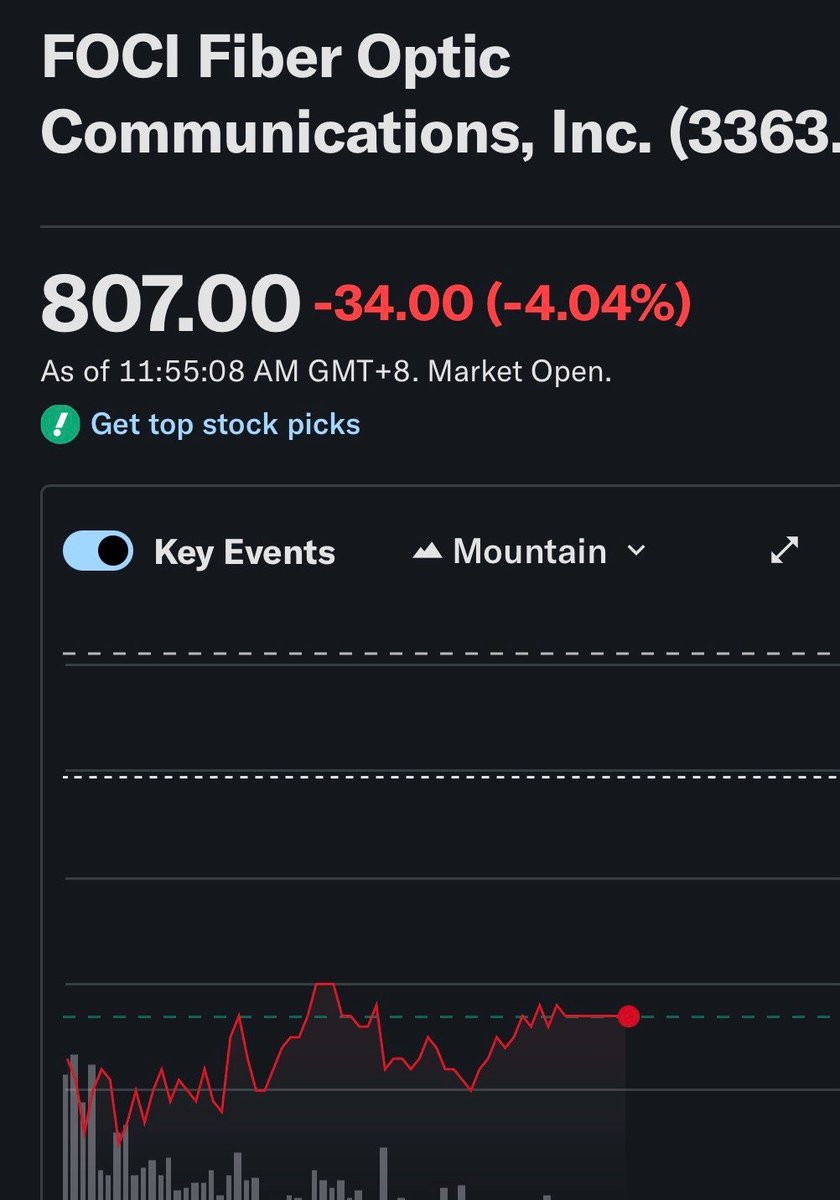

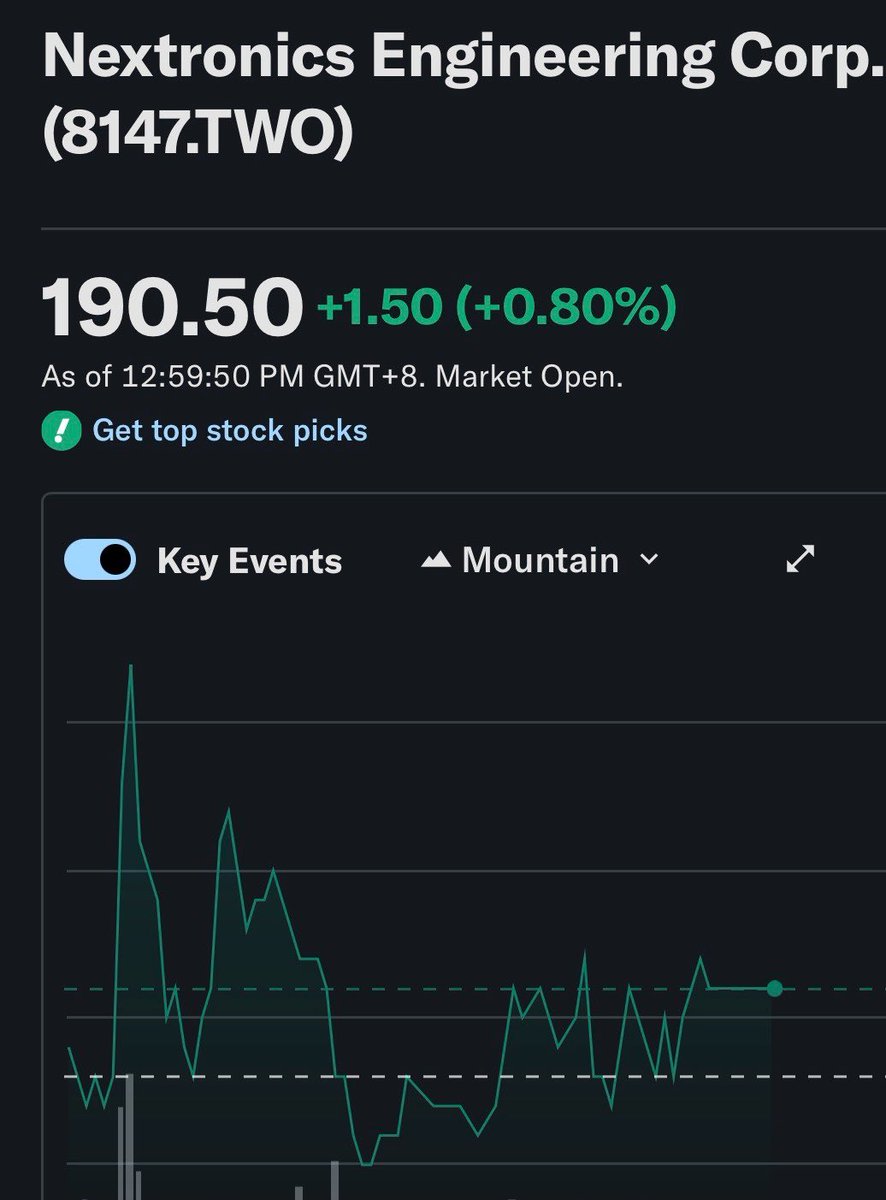

Next year… I’m expecting there to be many articles about FAU component bottlenecks.

Especially as the new CPO architecture led by $NVDA $TSM starts to scale.

Then a lot of these names like FOCI (~$2.8B MC) or Nextronics (~$246M MC) that I’m mentioning today will be in the center of it.

Despite many of these “commodity” labels… (just look at transformers/NAND)

And I’ll do a “Did you listen anon post” like $AXTI.

We’ll see if this is right.

217

120

1,605

279,863

Thorsten Huber retweeted

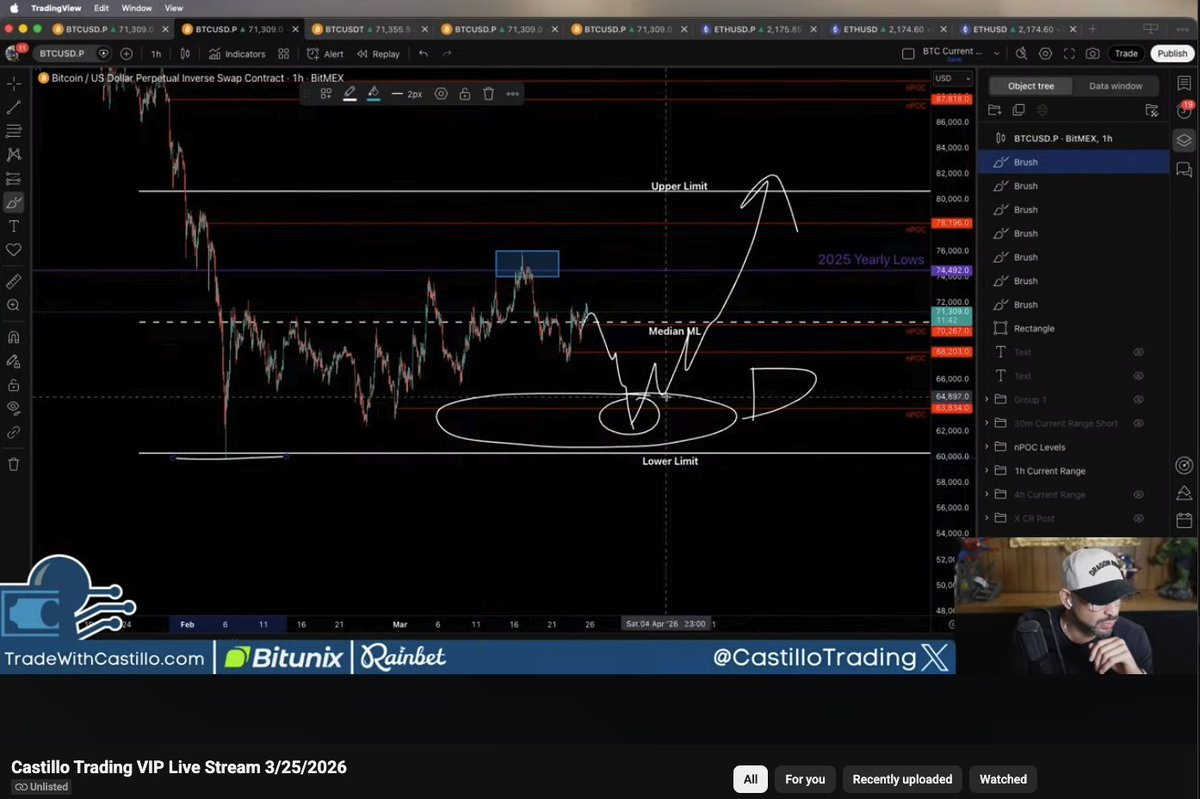

Discounted levels is where we were buying $BTC. We go over this every week during our livestreams and many VIP Members were able to capitalize on the most recent #Bitcoin move because they were ready for it.

During streams we talk in-depth on our analysis for each trade and why.

Access to VIP is 100% free, just DM if interested! We are streaming in about 1hr!

8

8

78

7,992

Thorsten Huber retweeted

Amazing to see that some people understand. This is why posts on X can be so surface, they lack context within setups and structures.

VIP Telegram fixes this to get the full picture day in and day out. 🫡

May 7

1. Higher timeframe bullish doesn’t mean you ignore resistance levels 😅 You can expect 90k eventually and still take profit short term at premium pricing. Smart trading is adapting, not marrying one bias. Castillo did mention it on his Telegram CASTILLOTRADE too — de-risking

3

3

28

8,077

Thorsten Huber retweeted

May 4

Glad to see $NBIS finally return 100% since my original thesis post back at ~$87.

I covered Nebius a ton late last year and at the start of this year.

Focusing on sum of parts from Avride to Clickhouse to how their balance sheet help them scale up their AI Cloud.

Was a little disappointed with timing, in terms of the massive drop in Dec/Jan.

But glad to see the company keep on delivering as Nebius is my favorite Neocloud in the entire sector.

I think we’re witnessing the rise of the next hyperscaler.

137

84

1,669

200,823

Thorsten Huber retweeted

Apr 18

$SPY my risk management is the only thing that’s keeping me profitable, happy and enjoying my weekend despite the nasty drawdown I’ve had over two weeks.

The angry salty ones are the ones that don’t have risk management so they blew up, and now blaming others for it.

This is how you stay poor. Have predictions on price instead of just risk management

18

3

152

24,190

Thorsten Huber retweeted

Apr 10

Yeah… I’m cooking super hard.

$AAOI 10.65%

People aren’t bullish enough after the new $LITE backlog report.

The demand visibility lasts past 2029 for optical companies…

Apr 10

I'm not sure people understand yet:

$LITE backlog order fill into 2028 signals extreme demand. And a lack of capacity.

Then by second order effect of hyperscaler demand spillover:

Guess who is projected to have the largest 800G/1.6T capacity in America?

$AAOI.

They fab their own inp lasers, design their own transceivers, and assemble it.

If $AAOI can execute on capacity ramp, that likely all translates into revenue due to everything being sold out.

My $40B MC price target from $5B is starting to look more and more likely?

73

45

710

165,922

Thorsten Huber retweeted

Mar 30

And... this is why I don't like Jane Street owning the same stocks I do like $AAOI.

They trade volatility, especially with retail favorite names and trigger stop losses/panic.

If you know what you own though:

$6.69B for a US company that makes the entire transceiver supply chain:

From Laser -> Design -> Assembly.

With likely $MSFT, $AMZN, $ORCL buying anything they can make, is a steal for me personally.

With high beta stocks, it's really important to build conviction and manage sizing correctly before entering a trade.

Otherwise you'll end up capitulating the bottom and buying the top over and over.

93

54

834

257,454

Thorsten Huber retweeted

Mar 21

I just realized…

Am I the most subscribed to finance account on X right now?

Kinda surreal so many funds and companies started reaching out for requests recently.

That aside; not planning on changing anything when I was 300 followers and now 100k .

Just having fun sharing my thoughts with everyone.

86

12

1,122

67,351

Thorsten Huber retweeted

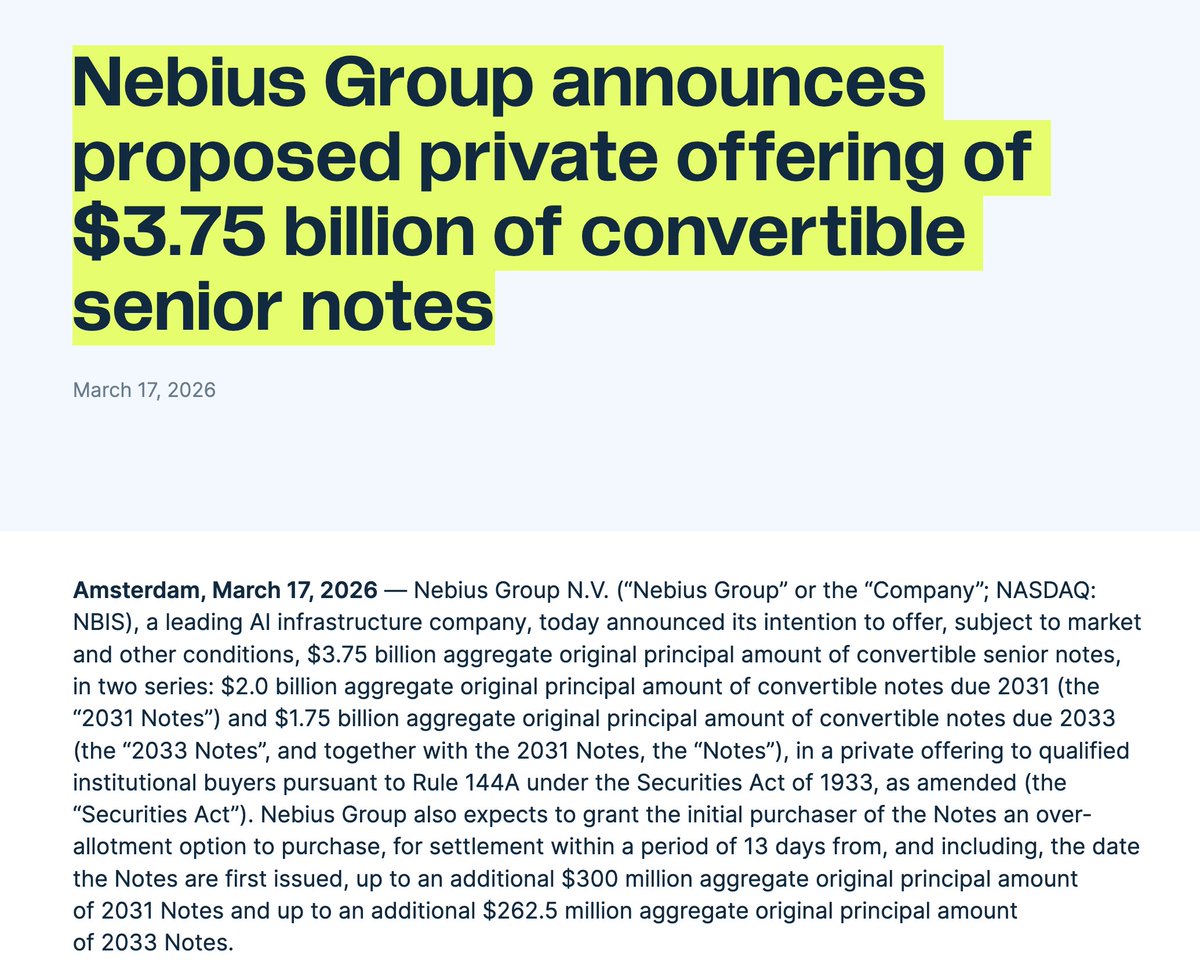

Mar 17

Just in: Following the new $27B Hyperscaler Cumulative Deal with $META.

$NBIS launches a proposed $3.75B in convertible note offerings to fund the buildout.

Markets view this as vastly superior to straight equity ATM dilutions.

As the debt only converts to equity if the company successfully drives the stock price up past that high strike.

More details for Nebius are likely to come soon.

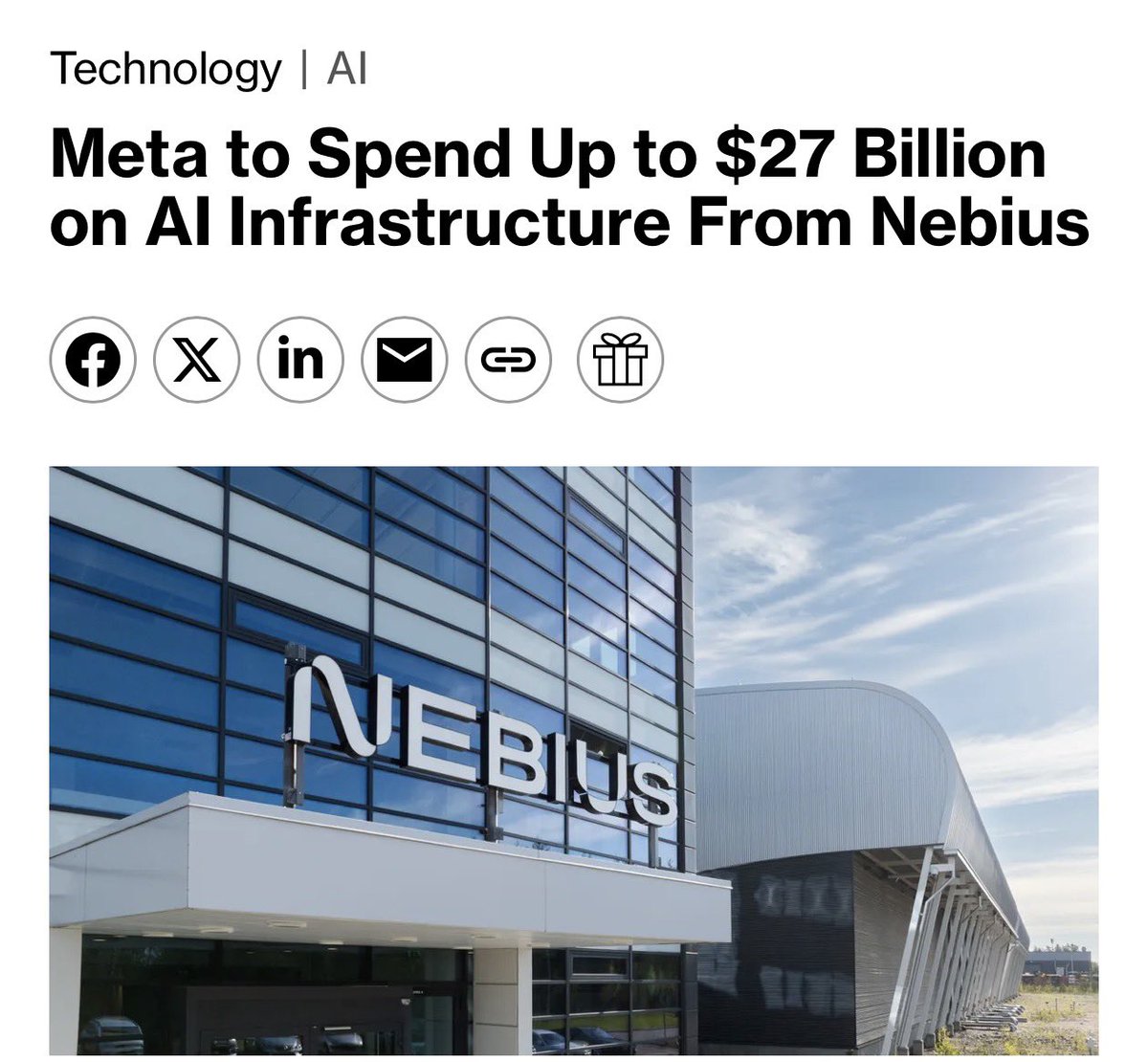

Mar 16

Just in: $META signs an enormous $27 Billion cumulative AI spend contract with $NBIS.

Nebius was my top Neocloud AI Infrastruture DC pick.

Glad management is executing toward their $7-9B ARR target.

Nebius is up 14.79% premarket to $129.66.

56

31

538

202,420

Thorsten Huber retweeted

Mar 17

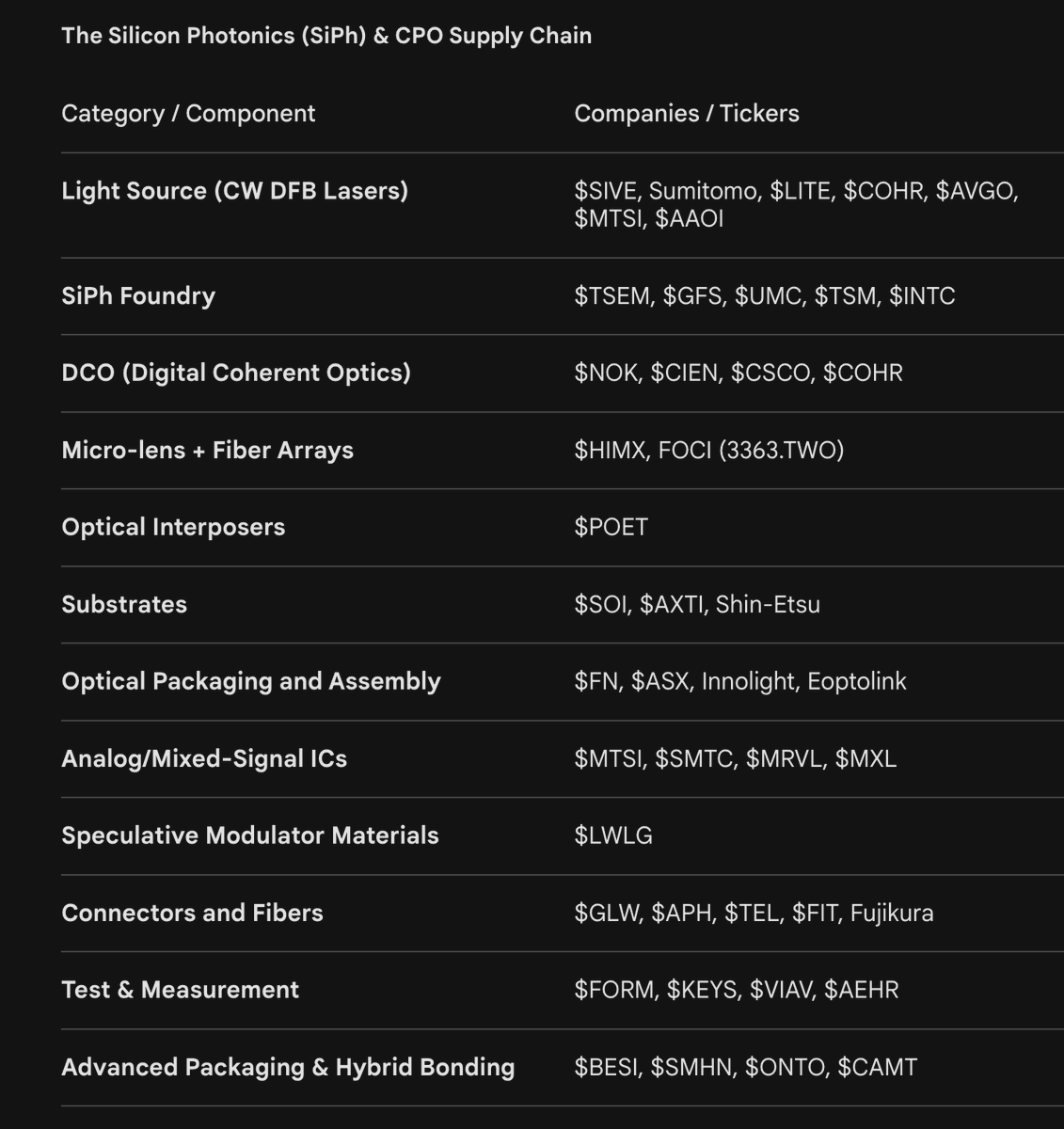

The upcoming CPO / Silicon Photonics Bottleneck Cheat Sheet:

$SIVE, Sumitomo, $LITE, $COHR, $AVGO, $MTSI, $AAOI - Light Source (CW DFB Lasers)

$TSEM, $GFS, $UMC, $TSM, $INTC - SiPh foundry

$NOK, $CIEN, $CSCO, $COHR - DCO

$HIMX, FOCI (3363.TWO) - Micro-lens Fiber Arrays

$POET - Optical Interposers

$SOI, $AXTI, Shin-Etsu - Substrates

$FN, $ASX, Innolight, Eoptolink - Optical Packaging and Assembly

$MTSI, $SMTC, $MRVL, $MXL - Analog/Mixed-Signal ICs

$LWLG - Speculative Modulator Materials.

$GLW, $APH, $TEL, $FIT, Fujikura - Connectors and Fibers

$FORM, $KEYS, $VIAV, $AEHR- Test & Measurement

$BESI, $SMHN, $ONTO, $CAMT - Advanced Packaging & Hybrid Bonding

Many are private companies from Lightmatter, Ayar, Ranovus and others.

Now... Everyone is asking... How do you profit?

If you look at the forecast for CPO TAM, it's a straight line up, and next year is inflection point for CPO mass deployment.

The alpha is capturing the rotation:

From the current EML bottlenecks ( $LITE, $COHR type) to SiPh / CW DFB architectural winners for CPO.

Highest upside potential are the ones that aren't included in current cycles.

But that are in the next.

Companies like $SOI, $SIVE, or $AEHR are perfect examples.

Ride the current pluggable bottleneck like $AAOI.

But the alpha is frontrunning institutions with the next CPO bottleneck.

The capital rotation is inevitable.

88

252

1,755

350,179

Thorsten Huber retweeted

Jan 17

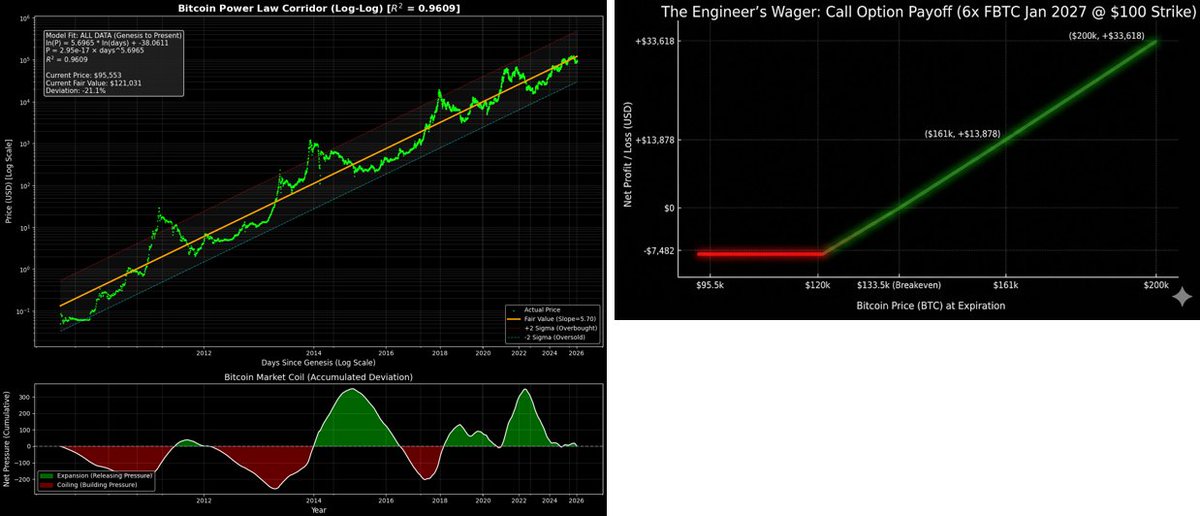

The Engineer’s Wager: Buying a Dollar for 34 Cents

Greg is an engineer, not a gambler.

In his day job managing energy infrastructure, he deals with "bounded systems." If you pump gas into a fixed volume, pressure rises. It’s not random; it’s structural.

Last week, Greg sat in his home office, running a simulation on his custom Robust Forecast Suite (v3.1).

On his left monitor: The model’s probability density for Bitcoin in 2027.

On his right monitor: The options market’s pricing for the same date.

The two screens were describing two different universes. In the gap between them, Greg found a "ghost" position that Wall Street was practically giving away.

The Signal: 78% vs. 34%

Greg’s model wasn’t running on hype. It was running on a Power Law backbone with a Huber loss function to filter out extreme days. It had an R^2 of 0.96 over 15 years, describing Bitcoin not as a stock, but as a biological network filling a capacity.

The output from the simulation was startling:

Model's Probability (Bitcoin > $109k): 78%

Market's Probability (Bitcoin > $109k): 34%

The options market (using the Black-Scholes model) was pricing $109,000 as a "long shot" a 1-in-3 chance. Greg’s power law model treated it as the base case a 4-in-5 certainty.

The Disconnect: Wall Street was pricing the option like a lottery ticket. Greg knew it was a distinct probability arbitrage.

The Engineer’s Problem

Greg owned $300,000 of Bitcoin exposure via FBTC. He wanted 20% more exposure (roughly $60,000 notional) to capture the reversion to the mean.

The standard tool is margin. Borrow $60,000. Pay 11% interest. Risk liquidation.

Greg rejected that. Margin introduces a "critical failure mode" if price wicks down, you get wiped out. An engineer doesn't build systems that explode under stress. He wanted the exposure without the fragility.

The "Ghost" Position (Synthetic Leverage)

He didn’t need to own another $60,000 of Bitcoin today. He only needed to rent the variance for the next 12 months.

He bought 6 January 2027 Call Contracts (FBTC $100 Strike).

The Cost (Max Risk): $7,482 (Calculation: 6 contracts × 100 shares × $12.47 premium)

The Exposure: 600 Shares (Equivalent to ~0.5 – 0.6 BTC depending on the ratio, controlling ~$48k–$60k of notional value).

This $7,482 was his maximum liability. If Bitcoin flatlines or crashes, the money is gone. That is the cost of the bet. But unlike margin, the risk is capped. He cannot lose his spot position. He cannot lose his house.

The Payoff: The "Hockey Stick"

The trade boiled down to one specific structural threshold.

ETF Breakeven: Strike ($100) Premium ($12.47) = $112.47 per share

BTC Equivalent Breakeven: ~$133,500

Below $100/share, the contracts expire worthless. Between $100 and $112.47, Greg recoups his premium. Above $112.47, the system enters net profit. From that point on, the payoff is linear (slope = 600), but the ROI becomes convex.

He ran this logic against his structural targets.

Scenario A: Power Law ($161k BTC)

If Bitcoin simply reverts to the calibrated model's median projection:

Implied FBTC Price: ~$135.60

Intrinsic Value: ($135.60 - $100) × 600 shares = $21,360

Net Profit: $21,360 - $7,482 = $13,878

ROI: 186%

Scenario B: Power Law × 1.25 Value ($200K BTC)

If Bitcoin follows the slope of the last 15 years to its projected "Overbought" rail:

Implied FBTC Price: ~$168.50

Intrinsic Value: ($168.50 - $100) × 600 shares = $41,100

Net Profit: $41,100 - $7,482 = $33,618

ROI: 449%

Why This Matters

He secured significant upside exposure for a fixed maximum loss of $7,482.

In the "Bull Case" ($200k), his ROI is 449%, whereas holding spot Bitcoin from $95k to $200k would yield only 109%.

He isn't defying the laws of finance. He simply realized that paying a fixed premium to rent the future is smarter than borrowing money to fear it.

Margin makes you a prisoner of the path one bad wick, and the system fails. The option makes you the owner of the destination. By capping his loss at the start, Greg purchased the rarest luxury in investing: the ability to be wrong for 364 days, so long as he is right on the 365th.

The gambler pays to play. The investor pays to survive and thrive.

#DYOR

20

35

258

25,099