Author of The Owner's Memo

Joined April 2011

- Tweets 309

- Following 192

- Followers 792

- Likes 352

45 Photos and videos

Charlie Munger once read a single magazine article, spent ninety minutes thinking about it, and made $80 million investing in the idea.

The company looked like a disaster. It had a ton of debt after five spinoffs in six years, and its revenues shrunk because of the 2001 recession. Principal payments on its debt were coming due that the company couldn't make.

I spent weeks reconstructing what Munger actually saw, down to finding the exact article he likely read in 2001.

New series at The Owner's Memo.

open.substack.com/pub/theown…

1

8

87

56,658

I've been thinking about these Baupost posts. I don't know exactly why the firm has underperformed these past several years.

But they've been in business for 44 years. And in order to put up stellar returns for that long, a fund manager needs to be superhuman. He or she must:

1⃣ adapt over time as assets grow and as prior strategies fail to work at higher dollar amounts. This means understanding how to do well with a smaller opportunity set, learning about new asset classes, and being a great manager as new employees come in and start managing a portion of the book. (I suppose one alternative is to deliberately stay small and religiously return capital to limited partners.)

2⃣ love the game so much that they continue playing with ferocity and curiosity decade after decade as one's interests naturally drift, particularly after you have more than enough money for several lifetimes,

3⃣ do all this through life's many changes (inexperience at first, having kids, family crises, deaths, health issues, etc.).

x.com/rubicon59/status/20649…

Jun 11

Baupost Group (Seth Klarman’s fund) has significantly underperformed major indexes in recent years, especially since around 2014. bloomberg.com

4

10

3,525

Very nice summary showing that (1) individual LLM models perform better when they are allowed more test-time compute, (2) because of this, it is difficult or impossible to see the ceiling on performance for any given model, and (3) as long as ceilings are unknown, AI spending will likely continue.

2

379

Tim Isgro retweeted

Jun 10

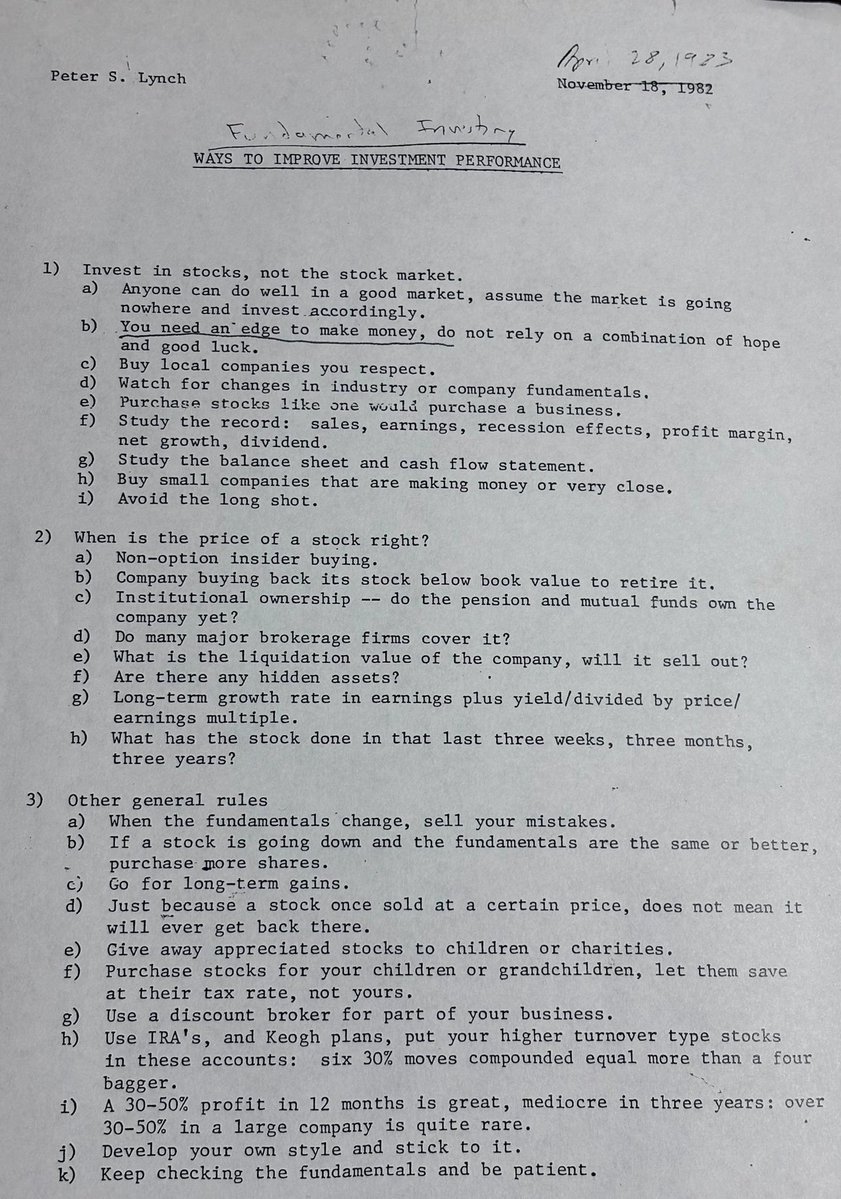

I was 26 years old when Peter Lynch handed me this.

April 28, 1983. I was the auto and retail analyst at Fidelity.

Peter was in his prime, on his way to building the greatest mutual fund track record in history:

29.2% annual returns for 13 YEARS STRAIGHT, growing Magellan from $18 million to $14 billion. The Babe Ruth of investing.

I'm looking at the principles he had typed up on a single sheet of paper that I've kept in my files for 42 years and I believe now is the perfect time to revisit them again.

Let me walk you through a few:

Rule 1B: "You need an edge to make money. Do not rely on a combination of hope and good luck."

Today's retail investor has no edge. He has Reddit, Robinhood, zero-DTE options and a TikTok algorithm pushing him into whatever stock just ripped 200% the day before.

That's hope and good luck wearing a fancy costume.

Rule 1E: "Purchase stocks like one would purchase a business."

Tesla trades at over 360 times earnings on a business deteriorating in real time, Oracle has $206 billion in liabilities against $39 billion in equity, MicroStrategy is a leveraged Bitcoin holding company priced like a software firm, and don't even get me started on SpaceX, that piece of garbage you'll be able to trade tomorrow...

Nobody in their right mind would buy these as actual businesses. They buy them as stories, narratives, and lottery tickets.

Peter would have called it the same way I do - these are not investments. They are speculations. GAMBLING.

Rule 1G: "Study the balance sheet and cash flow statement."

The hyperscalers spent over $380 billion on AI capex in 2025. Goldman says the measurable productivity payoff does not arrive until 2027 at the earliest.

Oracle just reported NEGATIVE $23.7 billion in free cash flow for fiscal 2026 while borrowing at a pace that would make a leveraged buyout firm nervous. The cash flow statements are screaming but nobody is reading them.

Rule 1I: "Avoid the long shot."

This one cuts the deepest.

The entire market has become a long shot.

OpenAI is projected to post roughly $74 billion in operating losses in 2028 ALONE while priced for transformation tomorrow. Bitcoin treasury companies are multiplying off thin air.

The retail investor of 2026 is making one long-shot bet after another and calling it a portfolio.

Rule 3A: "When the fundamentals change, sell your mistakes."

Tesla's fundamentals have changed.

California registrations are down 24% year over year and inventory days went from 10 to 27. Musk himself admitted on the last earnings call that Hardware 3 cannot achieve unsupervised FSD, breaking a promise made to 4 million customers.

The fundamentals have screamed change. But the stock is still at $385.

The mistakes are not being sold. They are literally being doubled down on with leverage.

Rule 3I: "A 30-50% profit in 12 months is great. Mediocre in three years."

Today's retail crowd expects 30-50% in a WEEK. Then they wonder why they get wiped out the second the hype stops.

And my favorite - Rule 3J: "Develop your own style and stick to it."

That is the entire game right there.

I developed mine sitting across the hall from Peter Lynch in 1983, watching him work, reading his notes, getting my own research handed back to me covered in his pencil marks. Then in 1984, my first full year managing money, I ran the #1 mutual fund in America. The Fidelity Overseas Fund was top 2 for the next six years running.

I did not get there by chasing narratives. I got there by following the sheet of paper you are looking at right now.

42 years later, this single page contains more wisdom than every Fintwit thread, CNBC segment, and Wall Street price target combined.

Peter retired in 1990 with the greatest mutual fund record in history. Then he sat down and wrote books explaining exactly how he did it.

Only a few "investors" these days read them.

And almost nobody is reading the balance sheets, the cash flow statements, or studying actual businesses today either.

They are chasing AI, crypto, and whatever pumped yesterday.

The wisdom on this page is timeless and it's more important than ever.

51

302

1,501

231,306

Tim Isgro retweeted

Jun 10

I asked Fable 5 why people should still read books in the age of AI.

Here's what it said:

59

160

1,058

84,130

Mag 7 concentration has been a hot topic for a few years now. After listening to the latest @InvestLikeBest, instead of leaving the idea of concentration to continue to fester in my brain, I prompted Fable to create a report with analogies of equity concentration in history.

You can find it live at my next comment below.

Most of all, it's another testament to how LLM's can take my passive "that's interesting" reactions or worries and allow me to learn more right at the moment.

2

1

487

Inspired by @nikunj …

x.com/nikunj/status/20645065…

Jun 10

I was listening to the latest episode of @InvestLikeBest and it talked a lot about S-curves..

So I had Fable one shot a website that talked about all the S-curves, their inflection point & commentary on each being a bubble in the last 200 years.

Live now on escurves dot com 🌊

210

If you’re interested in the investment Munger is talking about here, I wrote a deep dive study of it here:

x.com/timisgro/status/205921…

Charlie Munger read Barron’s for 50 years and only found one investment

That investment made him $80million, which he gave to Li Lu, who turned it into $400 million

6

1,167

What @adamshuaib says here (and in many other tweets) is fascinating. I need to consider it more. Recommend following him.

May 24

After 15 years of investing, we realised that truly exceptional founders have something impossible to fake: deeply unconventional lives.

We analysed 15,000 founders using five binary signals to measure this: odd hobbies, early signs of exceptionalism, extreme life choices, unusual geographies, non-linear careers. These sum to give a 0-5 score per founder. Whether someone started coding at 10, speaks five languages, climbed Everest or quit a safe job to live in Chile, the signal was deviation from the mean.

Rather than focusing on IQ or EQ, we call this metric the Outlier Quotient, or “OQ”. When forecasting founder success, it turns out that OQ was the single most predictive variable in our entire classification model, trained on ~70 different factors.

Our OQ score had zero correlation with having worked at a top-tier company or attending an elite university. The signals most VCs rely on aren’t just noisy, they’re blinding. The best founders don’t signal like everyone else, they don’t think like everyone else, and they certainly don’t build like everyone else.

If you want to spot breakout talent before the rest of the market, stop screening for conformity. Back the founders the system was built to filter out.

2

385

Most of the time, I’m in awe of what the LLM’s can do and excited for the future. Sometimes, I find a little, vague, AI anxiety creep up. I’ve found a great way to quell that is to use the models more.

Over the past few months, I’ve vibe coded about six or seven pieces of custom software and I use three or four almost every day. Makes me feel empowered to know I can now spin up and deploy any simple software I can think of.

2

328

“The Jevon's paradox kicks in and I feel my own demand for software growing substantially.”

It is now within reach of almost anyone to create and deploy their own custom software.

Jun 9

This is a super exciting release - Claude Fable 5 is the same underlying model as Mythos but with added safeguards. The benchmarks are great and it's SOTA on everything by a margin but I'll add that *qualitatively* also, this is a major-version-bump-deserving step change forward (imo of the same order as Claude 4.5 was in November), peaking especially for long problem-solving sessions on very difficult problems. You can give it a lot more ambitious tasks than what you're used to, the model "gets it" and it will just go, and it's never felt this tempting to stop looking at the code at all (but don't do this in prod!). The model still has quirks that people will run into and the safeguards are configured to be a little too trigger happy for launch, which can hopefully be tuned over time.

I feel a lot of things changing as working software increasingly comes out on a tap. The Jevon's paradox kicks in and I feel my own demand for software growing substantially. You can ask for anything - explainers, visualizers, dashboards, bespoke single-use apps (e.g. a full wandb that is hyper-specific just for your project), you can 10X your test suite, auto-optimize code, run giant research projects with custom HTML for the results, anything! "Free your mind" (Matrix ref). Really looking forward to all the things people build!

2

491

The Owner's Memo #9 is live.

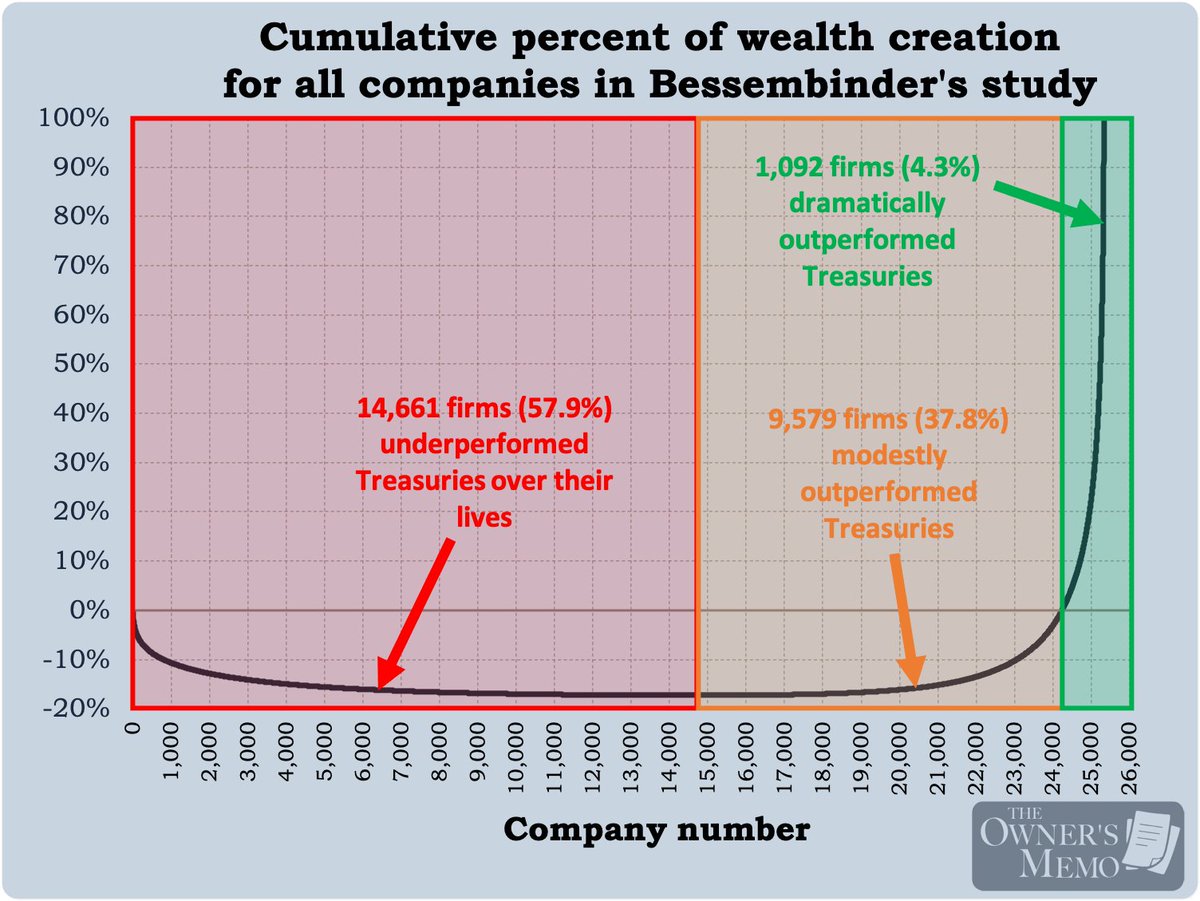

Since 1968, Reece Duca has compounded a personal $75,000 stake into what is reportedly several billion dollars at The Investment Group of Santa Barbara, never once taking outside money. In a 2023 interview, he names one principle he believes is critical: concentration in a small number of truly exceptional businesses.

To make the case, Duca cites a popular 2017 study by Hendrik Bessembinder of Arizona State, who examined the returns of every US stock traded between 1926 and 2016. Of those 25,332 names, just 4.3% produced all of the stock market's net dollar wealth. The other 95.7%, in aggregate, did no better than one-month Treasury bills.

The extreme concentration of returns among the very top companies is stunning. In addition, many eventual winners spend a long time looking like losers, which implies that the enterprising investor should focus on controlling his or her temperament and engaging in constant work.

Today's piece works through Bessembinder's study, where I think his diversification prescription falls short, and what it all suggests for the investor trying to identify the next great investment.

1

1

21

2,565

Seth Klarman on evaluating money managers:

"How do you begin to evaluate stockbrokers and money managers? There are several important areas of inquiry, and one or more personal interviews are absolutely essential. There is no better place to begin one’s investigation than with personal ethics. Do they “eat home cooking” - managing their own money in parallel with their clients? I can think of no more important test of the integrity of a manager and the likelihood of investment success than his or her own confidence in the approach pursued on behalf of clients. It is interesting to note that few, if any, junk-bond managers invested theirown money in junk bonds. In other words, they ate out."

Source: Do They Eat At Home?, Barron's, 1991.

11

52

8,731

“I have found that you have to take that one step toward the gods, and they will then take ten steps toward you. That step, the heroic first step of the journey, is out of, or over the edge of, your boundaries and it often must be taken before you know that you will be supported.”

- Joseph Campbell

7

270