Joined March 2020

- Tweets 7,543

- Following 316

- Followers 757

- Likes 53,196

1,794 Photos and videos

Pinned Tweet

Jun 10

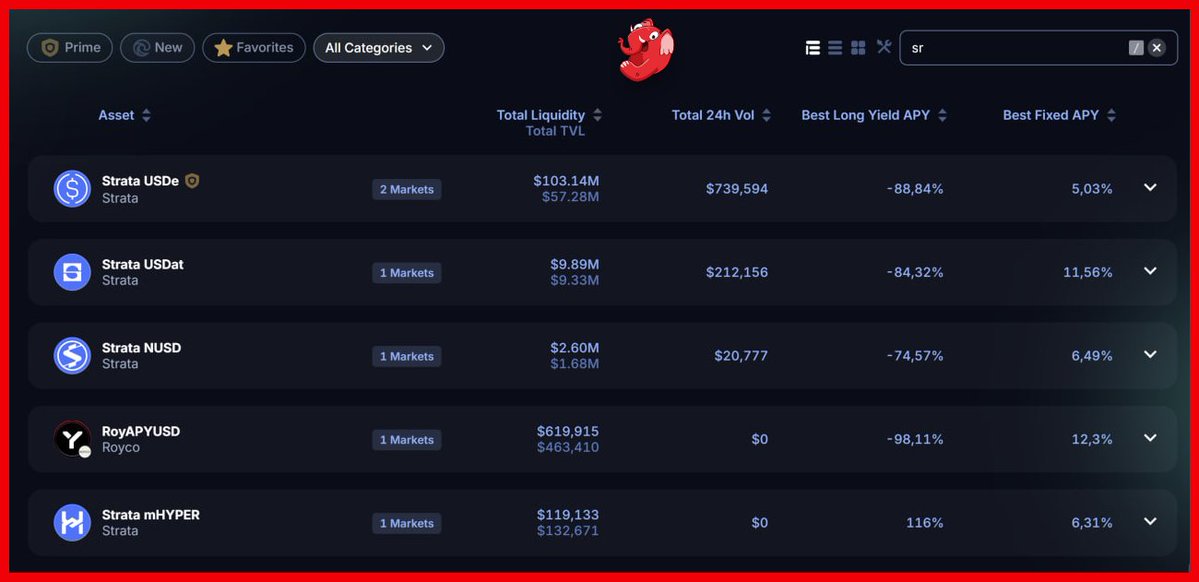

Pendle just listed 2 new maturities for @ethena_xyz's USDe yield, risk-tranched by @strata_markets

these markets existed before tho, users just roll over to the new one... but here's the part i only noticed:

almost every time Strata lists a new asset, 2 markets show up on Pendle shortly after, not a rule but it keeps happening

----------

To be specific:

1 tranched asset = 2 new Pendle markets, on top of the base market already live... so 1 asset = 3 markets, same yield source, same TVL bucket... but 3 separate fee lanes

Pendle's cost to host this basically zero and it gets better... the issuers themselves send extra rewards to push flow toward @pendle_fi

Neutrl x Strata

~ YT-srNUSD: 6.44% APY 40x Neutrl Points 60x Strata Points

~ LP-srNUSD: 5.77% APY 40x Neutrl Points 60x Strata Points

~ YT-jrNUSD: 8.2% APY 10x Neutrl Points 20x Strata Points

~ LP-jrNUSD: 7.91% APY 10x Neutrl Points 20x Strata Points

Ethena x Strata

~ YT- & LP-srUSDe: underlying yield 60x Strata 35x Ethena

~ YT- & LP-jrUSDe: underlying yield 20x Strata

----------

But tranching just re-slices existing yield and TVL, what's so special? fair point but it's only half the picture

capital does get split, fees dont... every market runs its own fee meter

that's why more ppl are watching Pendle rev lately, not just TVL... every maturity spawns a fresh market, like a subscription loop

srUSDe is the live case... literally where this post started

beyond Strata, @roycoprotocol runs the same playbook on apyUSD and Pendle already opened the srRoyAPYUSD market

one protocol is a niche, two starts looking like a category... especially when these tranching protocols keep expanding into tokenized deposits n other yield bearing assets

----------

zoom out, every yield source can be sliced into different risk profiles

➥ that's tranching-as-a-service

Strata already got a eal stress test with $STRC n $USDat ... the structure did what it was supposed to do

infras validation matters way more than yield marketing bc when institutions look at this space, they're gonna ask one thing:

did the risk segmentation actually work when things got ugly?

----------

If that thesis plays out, Pendle's tranching partners become its supply chain

someone else launches the product

someone else pays the incentives

Pendle gets another revenue line, not a bad setup tbh

Jun 9

New maturities for @strata_markets x @ethena pools:

🔹srUSDe (Oct 2026)

🔹jrUSDe (Oct 2026)

srUSDe for downside protection on sUSDe yields, jrUSDe to earn a risk premium as the insurance pool

Speculate, trade and fix their yields with Pendle

4

7

26

4,368

Decentralized Danny retweeted

Capital efficiency sounds like DeFi buzzword until u realize Goldman Sachs built a huge business around the exact same thing:

➥ getting more out of the same dollar

the DEX war is entering the same chapter

~ chapter 1 was liquidity or TVL

~ chapter 2 was volume and fees

~ chapter 3 is capital

and chapter 3 is just getting started ↓

9

3

8

347

Decentralized Danny retweeted

People saw @saylor sell 32 $BTC and immediately jumped to the collapse scenario.

I think that reaction misses the bigger point. @Strategy is not a “weeks away from failure” story.

The real question is how much runway the balance sheet still has.

And that runway is exactly why @saturn_credit becomes interesting.

Jun 13

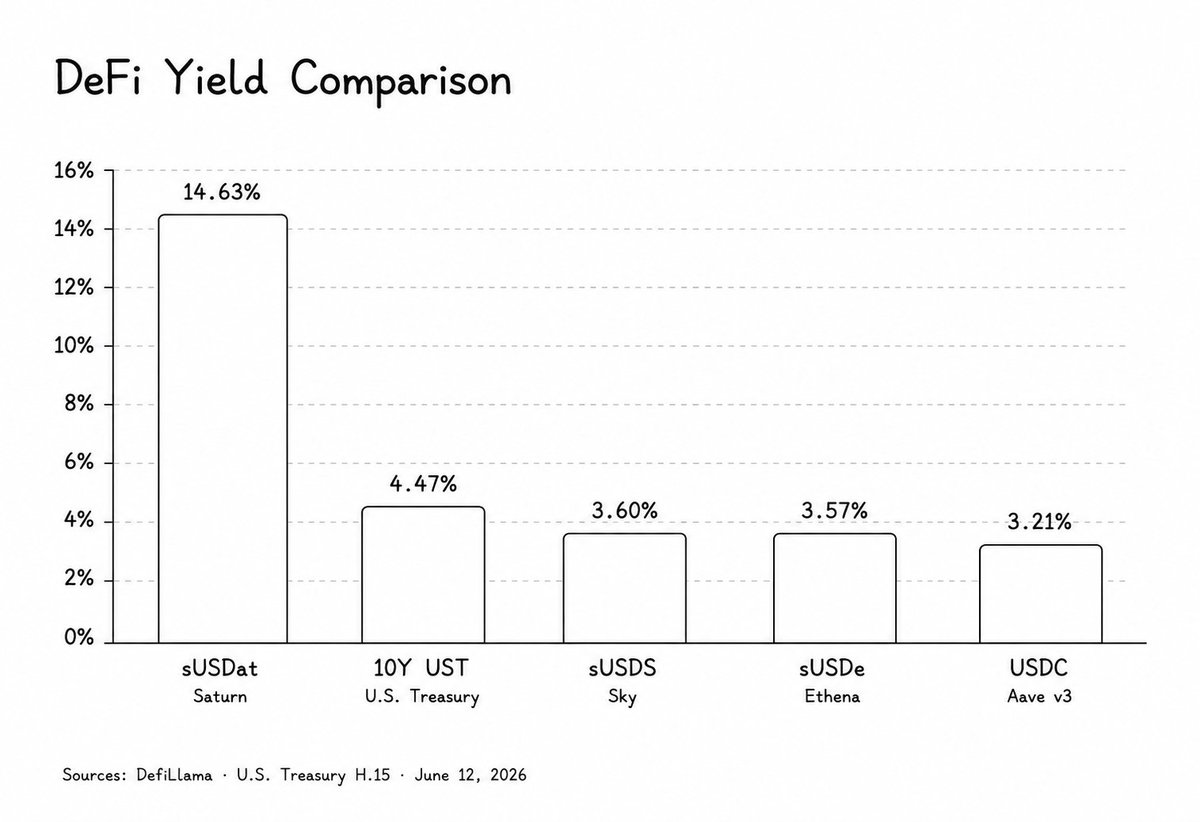

Everyone is focused on STRC's discount.

@saturn_credit is focused on what can be built on top of it.

Over the past few weeks, much of the discussion around STRC has centered on one question:

Will it return to par?

It's a reasonable question. STRC has been trading below its $100 par value, and naturally, many investors are focused on the risks and volatility surrounding the asset.

But there is another way to look at what's happening.

While the market debates STRC itself, Saturn is building a product on top of the cash flow STRC generates.

Today, sUSDat is offering 14.63% APY, making it one of the highest-yielding stablecoin products in DeFi.

That doesn't mean the risks around STRC disappear.

It means Saturn is taking an asset many investors view as a controversial credit instrument and transforming its underlying yield into something that can be used across DeFi.

- A stablecoin.

- A collateral asset.

- A source of on-chain yield.

This is what makes the story interesting.

3

2

5

225

Decentralized Danny retweeted

Jun 12

1/ Crypto adoption is entering a new phase.

For years, digital assets were largely viewed as experimental, speculative, or institutionally inaccessible.

But that narrative has changed meaningfully. BTC and particularly ETH, are increasingly being integrated into the product suites of major financial platforms, treasury companies, funds, and institutional trading venues.

As $ETH adoption deepens, the next question becomes less about whether institutions want ETH exposure, and more about how they should manage it.

Holding $ETH passively gives investors exposure to its long-term upside. But ETH is also a productive asset via PoS yield. For treasuries, funds, and sophisticated users, this creates an obvious opportunity: ETH should not simply sit idle.

The challenge is that native staking is not always operationally simple.

The rabbit hole goes deep → Validator management, withdrawal queues, liquidity constraints, custody requirements & exchange collateral limitations all create friction.

This is esp. true for institutions, where operational resilience, risk management, and liquidity access matter as much as headline yield.

This is where liquid staking becomes increasingly important.

And in 2026, @mETHProtocol $mETH is positioning itself as one of the key yield layers for ETH 🧵

Jun 11

ETH staking is moving beyond yield alone.

“The next phase is about stronger security, deeper liquidity, and better distribution.” - @Defi_Maestro

Read more below on how mETH Protocol is building for 2026.

35

17

81

4,265

Decentralized Danny retweeted

Jun 11

The PT side of @pendle_fi 's story is pretty obvious but i'm more interested in who ends up buying the YT

historically that was mostly yield tourists:

~ yield speculators

~ point farmers

~ guys betting SSR goes higher

but @SkyMoney might be creating a completely different YT buyer

yes, its own Primes

they're basically borrowing at variable rates n deploying into fixed-rate strategies... works great until SSR starts moving higher

~ funding cost goes up

~ yield stays where it is

~ margin gets squeezed

classic duration mismatch, banks have been dealing with this for decades

Sky's framework basically forces Primes to hedge it or hold extra capital against it and one of the cleanest ways is... YT-sUSDS

PT gets distribution, YT gets a reason to exist... that's a lot more interesting than another fixed-yield integration imo

Jun 11

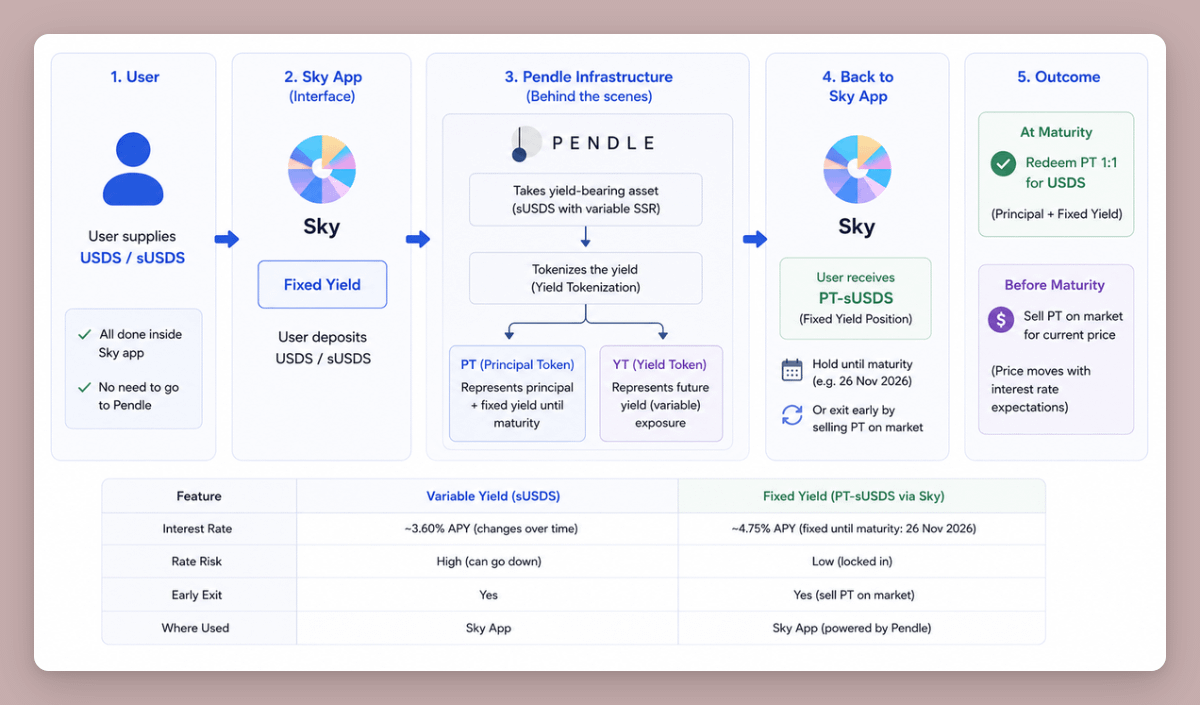

Pendle: B2C → Infrastructure Layer

This is actually the most interesting part of the integration.

Previously, if you wanted fixed yield through @pendle_fi , you had to:

- Go to Pendle.

- Buy PT-sUSDS.

- Understand how PT and YT work.

- Manage the position until maturity.

Now, with @SkyMoney

- Users simply open the Sky app.

- Click "Fixed Yield."

- Deposit USDS or sUSDS.

Everything else is handled by Pendle behind the scenes.

Technically, users are still holding PT-sUSDS, but Sky has packaged the experience into a simple native product. Most users may not even realize they are using Pendle infrastructure.

This matters because it shows Pendle evolving from a consumer application into an infrastructure layer.

In the past, users had to come to Pendle.

Now, Pendle is going to where the users already are.

This is similar to:

- Users don't need to visit Aave directly if lending is integrated into wallets or other apps.

- Users don't need to open Chainlink's website to use oracle data.

Pendle is moving in the same direction for fixed-income products.

What's even more important is that Sky is not creating the fixed yield itself.

The Sky Savings Rate (SSR) remains a variable yield product.

Pendle creates a marketplace where:

- Users who want fixed yield buy PT.

- Users who want exposure to future yield buy YT.

As a result, the fixed rate is determined by market supply and demand.

I think Sky is only the beginning.

If this model proves successful, we'll likely see more protocols integrate fixed yield directly into their products instead of forcing users to leave the app.

Aave and GHO are a natural example.

Imagine being able to lock a fixed yield on GHO directly inside the Aave interface, powered by Pendle infrastructure in the background.

2

2

4

556

Decentralized Danny retweeted

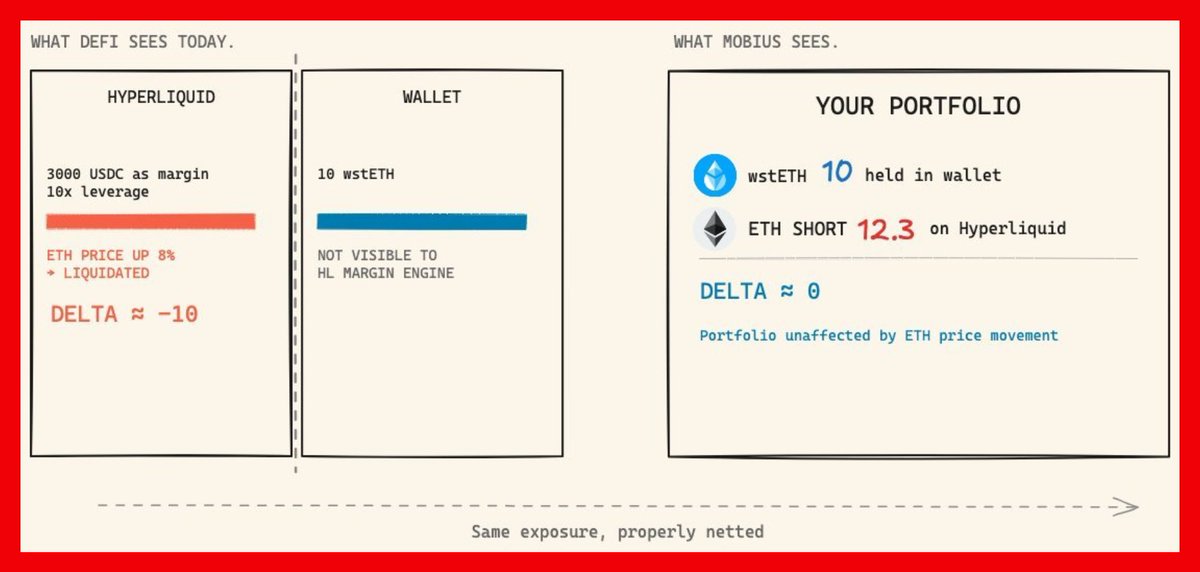

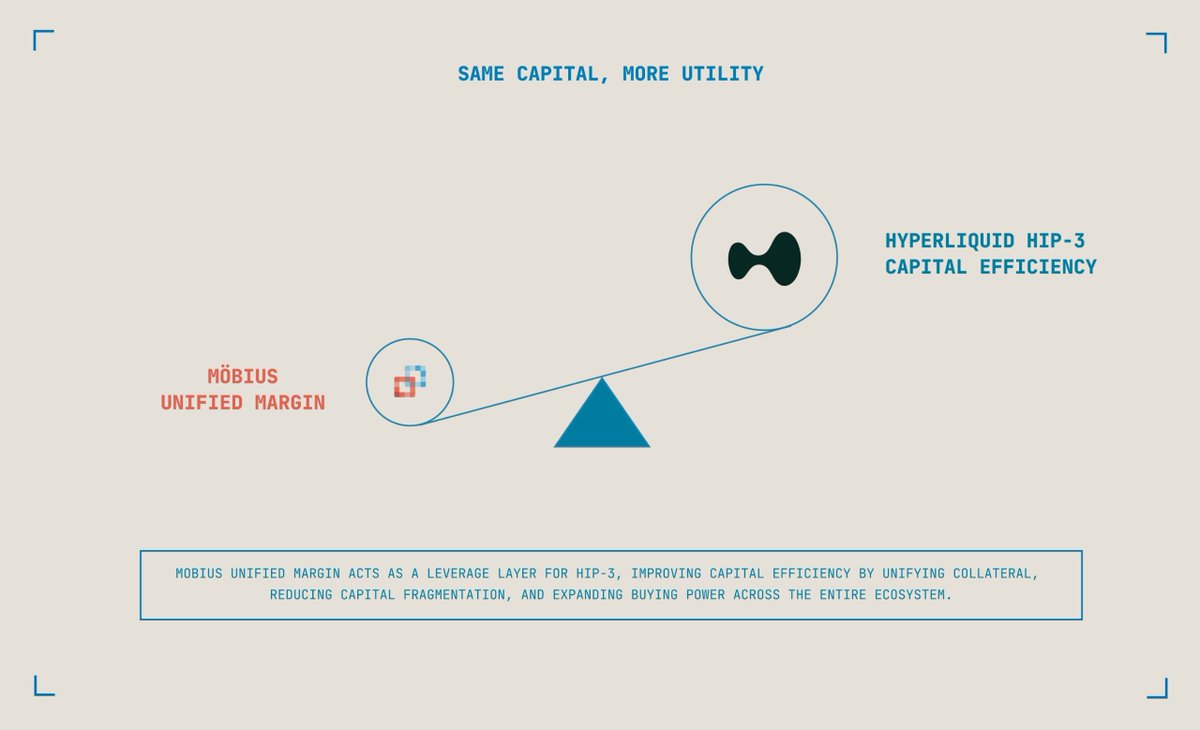

HIP-3 may need Unified Margin to truly scale

HIP-3 is quickly becoming one of the biggest growth stories on @HyperliquidX. HIP-3 markets now account for roughly 35–45% of total volume, with cumulative volume already surpassing $300B

More builders are launching new markets every month.

At first glance, this looks like a resounding success.

But success at this scale is creating a new, deeper challenge.

In TradFi, when financial products exploded through stock futures, index futures, commodities, and options, the industry did not solve the problem by building more exchanges.

It solved it through Prime Brokers, a unified layer that allowed traders to access hundreds of products through a single margin account.

It is the core thesis behind Mobius.

Hyperliquid's HIP-3 is beginning to follow a similar path.

7

7

19

2,015

Decentralized Danny retweeted

Jun 12

26

7

34

2,068

Capital efficiency sounds like DeFi buzzword until u realize Goldman Sachs built a huge business around the exact same thing:

➥ getting more out of the same dollar

the DEX war is entering the same chapter

~ chapter 1 was liquidity or TVL

~ chapter 2 was volume and fees

~ chapter 3 is capital

and chapter 3 is just getting started ↓

9

3

8

347

Tagging some CTs

@Jonasoeth

@MahoneDeFi

@nhatminheth_

@DeFi_Andree

@Eli5defi

@0xCheeezzyyyy

@SachinHMx

1

97

Decentralized Danny retweeted

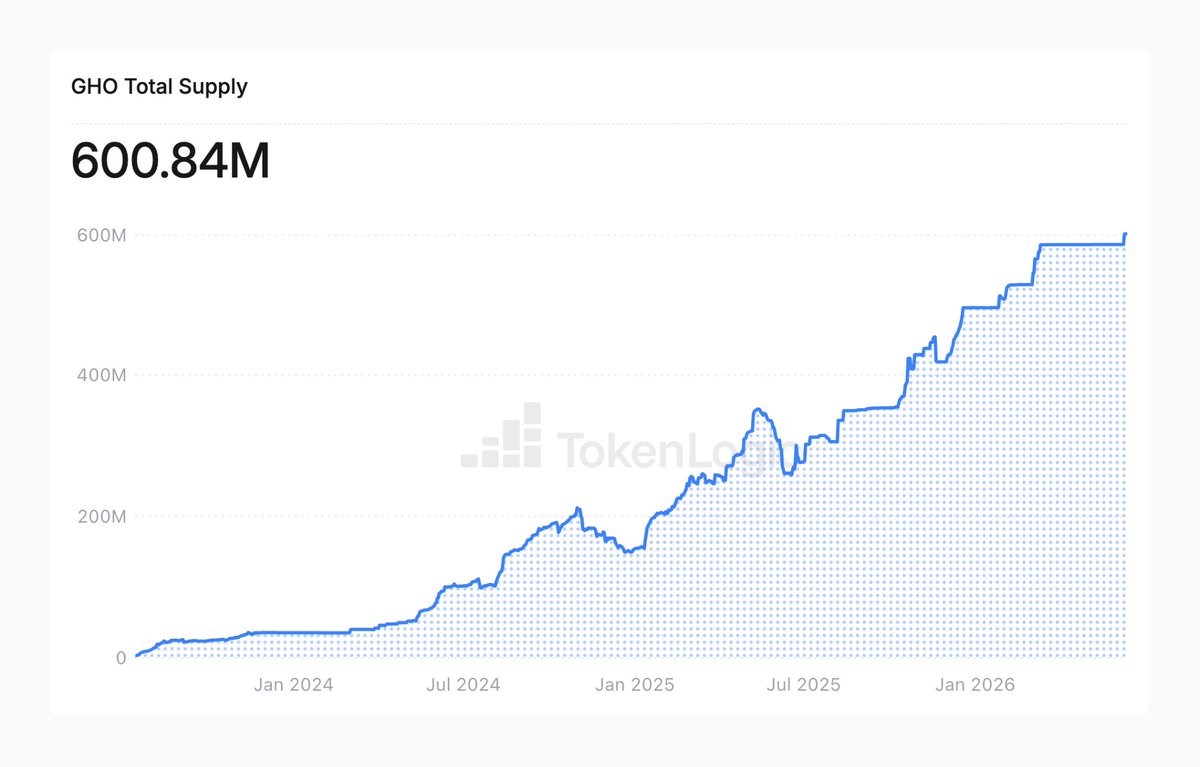

GHO has crossed 600M supply.

This is one of the most important signals for Aave right now. It is not a short-term spike. It is a multi-year expansion of Aave-native stablecoin liquidity.

GHO is more than another stablecoin. It is the monetary layer of the Aave economy.

Every new unit of GHO strengthens the system: more collateral utility, more borrowing demand, deeper liquidity, and more value flowing through Aave.

The key part is where this growth happens. GHO is scaling inside the largest DeFi lending network, backed by real credit demand, collateral depth, risk infrastructure, and governance-controlled expansion.

That is a very different foundation from a stablecoin relying only on temporary incentives.

@aave is no longer just building lending markets. It is building an onchain financial system where credit, stablecoin liquidity, and future payments can compound around the same network.

GHO crossing 600M supply is not the final milestone. It is proof that Aave’s stablecoin strategy is starting to scale.

22

10

74

2,806

and there's still a gap... Coinbase and Ripple mainly target institutions meanwhile HIP-3 still operates inside a single venue

the harder problem is making collateral work across venues without handing custody to a middleman

the gap that's still open:

~ decentralized

~ cross-venue

~ retail accessible

~ no rehypothecation

that's the bet @MobiusExchange is making

not another exchange, not another market, just a way to make the same collateral work across all of them

~ one account, multiple venues

~ portfolio-level risk instead of position-level risk

1

2

44

so to me the thesis is pretty simple

chapter 1 was who could pull liquidity

chapter 2 was who could pull volume

chapter 3 is who can turn fragmented collateral into unified buying power

@MobiusExchange is just one of the teams taking a shot at it

might work, might not but a few yrs from now, i dont think the thing worth remembering will be any single project

it'll be the moment DeFi stopped optimizing trades and started optimizing balance sheets.

1

39

Decentralized Danny retweeted

Jun 13

47

10

113

6,985

Decentralized Danny retweeted

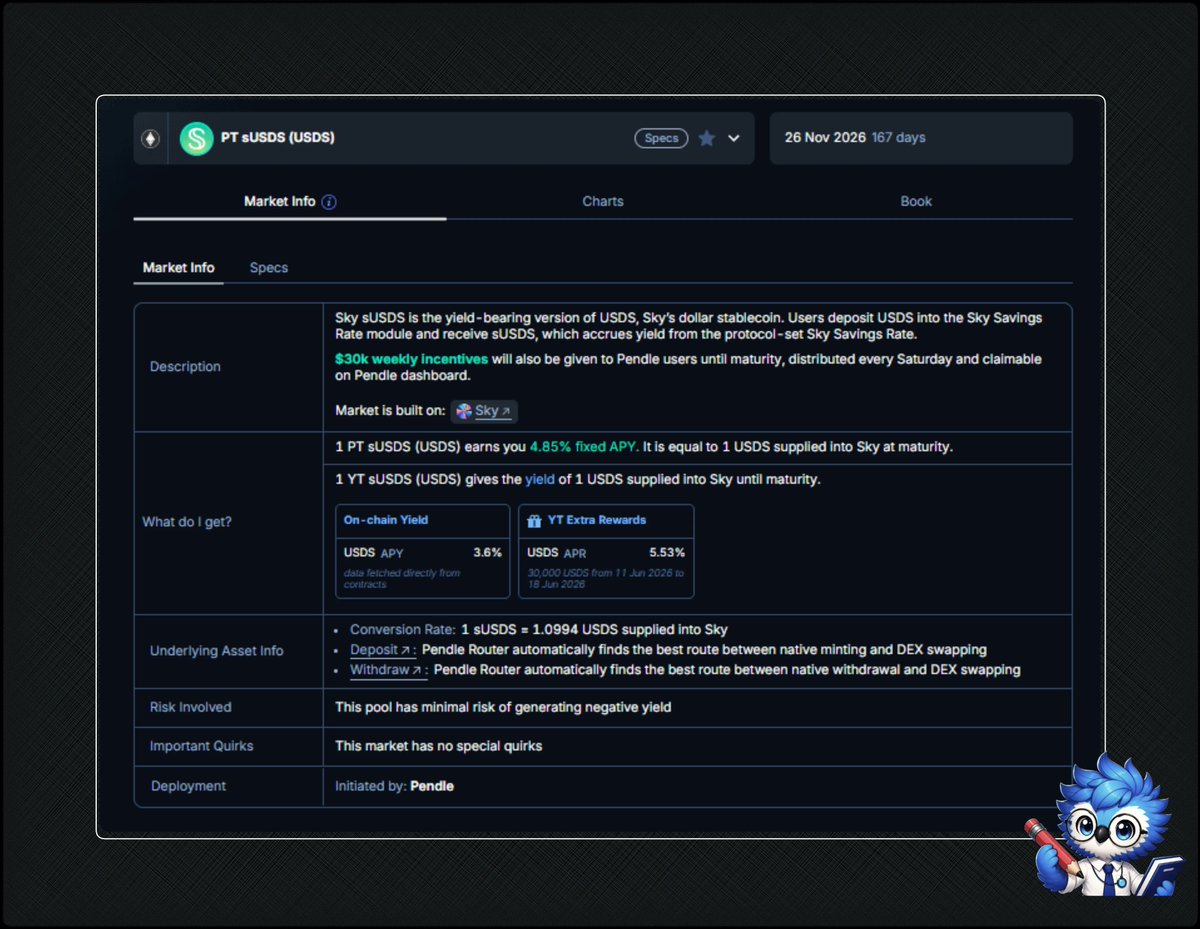

Jun 12

Fixed yield is now natively embedded into DeFi’s largest savings product

@SkyMoney took a major step forward integrating native Fixed Yield directly inside app for sUSDS the yield-bearing stablecoin with over $6.1 billion in TVL.

Users can now simply select the Fixed tab to lock in ~4.85% APY fixed (maturity: Nov 26, 2026), which is higher than the current variable Sky Savings Rate (SSR) of ~3.6%.

Powered by @pendle_fi with $30k USDS weekly incentives for YT holders until maturity. It’s proof that institutional-grade fixed yield is becoming a native feature in top stablecoin ecosystems.

> Sky’s mass users get easy access to fixed income without complex PT/YT learning curves

> Pendle acts as powerful fixed-rate infrastructure

> Win-win for the ecosystem: Sky brings distribution & capital, Pendle brings the tech, users win with better options

Sky Savings Rate has long been a bluechip yield source.

With seamless Fixed Yield embedded, DeFi savings are becoming more mature, flexible, and predictable than ever.

Jun 10

Sky has integrated Fixed Yield natively, powered by Pendle.

Users can now lock Sky Savings Rate to a fixed maturity at 4.75% APY, against a 3.60% variable rate, directly within the @SkyMoney app.

This integration embeds Pendle’s infrastructure inside the product surface of one of DeFi’s largest stablecoin protocols, extending Pendle from a standalone venue to a fixed-income layer that other protocols can integrate to expand their own offerings 🤝

30

2

45

3,365

Decentralized Danny retweeted

Jun 12

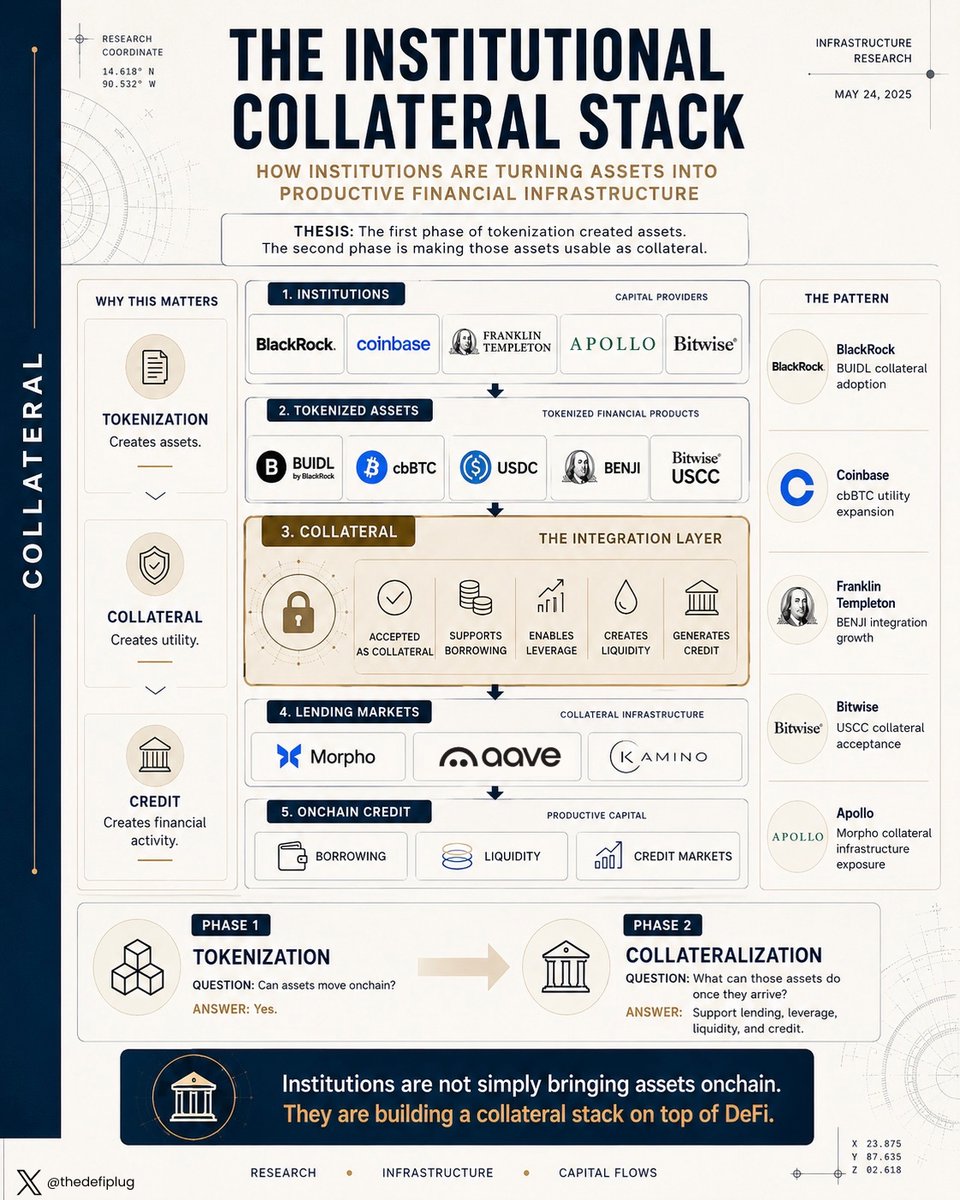

Over the past year, several large institutions have expanded their presence in DeFi.

@BlackRock launched BUIDL. @Coinbase expanded cbBTC and USDC integrations. @FTI_US expanded BENJI’s onchain reach. @apolloglobal and @Morpho announced a strategic partnership that includes up to 90 million MORPHO tokens vesting over 48 months.

At first glance, these look like separate initiatives.

The common thread is easy to miss.

The easiest way to interpret these developments is through adoption.

Institutions are entering DeFi.

The more important question is integration.

How are institutions choosing to participate once they arrive?

A pattern is starting to emerge.

Institutions are not entering DeFi by becoming crypto-native.

They are entering by making their assets usable as collateral.

That distinction matters because financial systems are built around collateral, not assets.

The first phase of tokenization focused on issuance.

Can Treasuries be tokenized?

Can institutional funds exist on public blockchains?

Can private credit move onchain?

The answer is increasingly yes.

The more important question now is:

What can those assets do once they arrive?

Several developments point in the same direction:

➤ Apollo: Strategic partnership with Morpho involving up to 90 million MORPHO tokens over 48 months

➤ BlackRock: BUIDL accepted as collateral across lending venues

➤ Coinbase: Expanding cbBTC and USDC integrations

➤ Franklin Templeton: Expanding BENJI’s utility across public blockchains

➤ Bitwise: USCC fund tokens accepted as collateral across Morpho, Aave, and Kamino

Different firms.

Different products.

Same objective.

Make institutional assets usable inside DeFi.

This is why the Apollo-Morpho relationship stands out.

The market tends to view it as a token investment.

It is better viewed as exposure to collateral infrastructure.

Morpho provides modular lending infrastructure that allows credit markets to be built around specific collateral assets.

The opportunity is not tokenization itself.

The opportunity is collateralized credit.

BlackRock’s BUIDL illustrates the same shift.

The interesting development is not that BUIDL exists.

It is that BUIDL can now secure loans and participate in lending markets.

Once an asset can support borrowing, leverage, and liquidity, it stops behaving like a passive investment product.

It becomes infrastructure.

The same logic applies to cbBTC.

The value is not issuance alone.

The value comes from expanding where Bitcoin can be deployed productively.

The market still underestimates this distinction.

Most tokenization discussions focus on assets.

Financial systems focus on collateral.

An institutional asset sitting in a wallet creates limited value.

An institutional asset that can secure credit and circulate through lending markets becomes significantly more useful.

That is why collateral integrations may ultimately matter more than token issuance.

The first phase of tokenization created assets.

The second phase is turning those assets into productive financial infrastructure.

Viewed through that lens, the Apollo-Morpho relationship is important not because Apollo is simply buying a token.

It is important because it signals institutional interest in the infrastructure layer that makes collateral productive.

The easiest interpretation is that institutions are entering DeFi.

The more useful interpretation is that they are building a collateral stack on top of it.

54

17

95

6,554

Decentralized Danny retweeted

Jun 12

With SpaceX finally going IPO today, i kinda want more ppl to pay attention to a much bigger piece of news for tokenized stocks...

SEC just proposed removing Rule 611 and Rule 610(e) from Reg NMS, sounds boring but ...

you may not know these rules, they've been a core part of US market structure since 2005... they require all stock trades to respect the National Best Bid and Offer (NBBO)

simple version: you weren't allowed to buy or sell a stock at a worse price if a better one was available on another exchange

----------

So what matters most for crypto and DeFi is this:

AMMs or lending markets simply can't comply with these rules... they operate on bonding curves, slippage n block times

they dont route orders through traditional exchanges to constantly seek the best quote across the entire market

as a result, tokenized stocks were never really able to trade, lend or borrow freely across DeFi

----------

what i find interesting is that this same week, Stani published a very insightful article about @aave V4's market structure

~ Hub-and-Spoke architecture

~ credit lines

~ exposure caps for each asset

one of the examples he explicitly mentioned was equities... his exact quote:

"RWAs particularly benefit from this model, since onboarding them requires both capital bootstrapping and a carefully designed market structure for risk controls. For example, a Hub could include Spokes for specific asset classes such as equities, private credit, and alternative funds, each with carefully tailored risk parameters and limited credit lines from the Hub.

legal trading venue → onchain liquidity → reliable oracles → equities become viable collateral → lending markets open up

that's where things get really compelling

----------

Aave V4's Hub-Spoke-credit line structure suddenly looks like the ideal framework for onboarding tokenized stocks and RWAs in a way that's safer, more capital efficient n easier to control from a risk perspective

probably not a coincidence that Horizon is already running $470M in RWA markets

IMO this is exactly what "Project Crypto" looks like in practice

4

2

6

782