Joined October 2023

- Tweets 808

- Following 34

- Followers 86

- Likes 4

490 Photos and videos

AI companies are reporting incredible numbers.

That's not the debate.

The debate is whether the stock prices already assume all of it.

Nvidia posts a blockbuster quarter.

Anthropic reports massive growth.

Investors look at those numbers and see validation.

The question raised was different:

How much of that future is already reflected in the stock price?

Because those aren't the same thing.

A company can perform extremely well...

and still disappoint investors.

Not because the business is weak.

Because expectations got too high.

That's what makes this environment tricky.

The AI story may be real.

The revenue growth may be real.

The profitability may be real.

The infrastructure spending may be real.

But stock prices don't move based on reality alone.

They move based on the gap between reality and expectations.

And when expectations become enormous, that gap gets harder and harder to exceed.

That's why some investors aren't questioning the AI story.

They're questioning how much of the story has already been priced in.

21

For those of us with kids, summer marks another milestone. School is out, graduation season is here, and for many families, college is right around the corner.

My oldest daughter will be a senior this fall, which means our family is now officially entering the college application process. Like many parents, I've been looking at tuition numbers and mentally preparing myself for what feels like an inevitable financial hit.

And it's a big one.

When I started college in the early 1990s, the average annual cost of attending a private university was roughly $10,000-$15,000 per year. Today, many private schools are approaching or exceeding $90,000 annually when you include tuition, housing, fees, and living expenses. In some cases, sending a child to college can cost more than buying a house did a generation ago.

At the same time, getting into many of these schools has become dramatically more competitive. Applications have exploded, acceptance rates have fallen, and students are expected to build résumés that would have looked extraordinary just a few decades ago.

Given those realities, I assumed the process was fairly straightforward: write the checks and hope the investment pays off.

What I learned from this week's guest, however, was surprising.

Shellee Howard has spent decades helping families navigate college admissions, scholarships, and financial aid. One of the biggest myths she challenged is the belief that higher-income families don't qualify for meaningful financial assistance.

According to Shellee, many affluent families leave substantial amounts of money on the table simply because they assume they won't qualify.

We discuss merit scholarships, strategic college selection, FAFSA and CSS planning, scholarship negotiation tactics, and how certain schools are dramatically more generous than others. We also talk about recent rule changes affecting divorced families, why some assets are treated differently than others in aid calculations, and how proper planning can significantly reduce the total cost of attendance.

Perhaps the most important takeaway is that college pricing is often far more flexible than most families realize.

Whether your children are a few years away from college or applications are already underway, this episode may save you far more money than you expect.

Watch on YouTube:

youtube.com/watch?v=TN4inECL…

Listen on Apple Podcasts:

podcasts.apple.com/gb/podcas…

Listen on Spotify:

open.spotify.com/episode/0xL…

23

Today’s distressed multifamily market may create one of the biggest real estate opportunities in years.

Check out my interview with Dave Dubeau on Property Profits Podcast:

youtu.be/WlavlB1jlM4

#Multifamily #distressedproperty #realestateinvesting #MarketCycles #REALASSET

5

Today's housing shortage is often tomorrow's oversupply.

How do you position yourself for the next real estate boom? Find out on this week's episode: youtu.be/DV5_IYzNvRg

#RealEstateInvesting #MarketCycles #CommercialRealEstate #Investing #Economics

11

68

Everyone wants to buy what's going up.

Very few people want to buy what's on sale.

That's true in investing just as much as anywhere else.

Right now, AI stocks are getting all the attention.

Meanwhile, real estate has become the market's forgotten asset class.

Higher interest rates, expensive financing, and investor pessimism have pushed many buyers to the sidelines.

But that's often where opportunity starts.

The irony is that people happily hunt for discounts when shopping.

When investing, they do the opposite.

They chase what's already expensive and avoid what's become cheaper.

The best investments rarely feel comfortable when you buy them.

If they did, everyone would already be there.

Sometimes the hardest thing to do is buy the asset nobody wants to talk about.

14

This is what today's 4.2% headline inflation means.

Just a few months ago, markets were expecting rate cuts. Now some analysts are discussing the possibility of rate hikes instead.

#Inflation #InterestRates #FederalReserve #Economy #OilPrices

7

Most people assume inflation comes from shortages.

And it does.

But shortages eventually get resolved.

The interesting question is what happens next.

After a supply shock, countries often rethink their assumptions.

Governments build larger reserves.

Companies increase inventories.

Supply chains get duplicated.

Backup systems get created.

Nobody wants to be caught unprepared twice.

That sounds prudent.

But it's also expensive.

Holding more inventory costs money.

Building redundancy costs money.

Maintaining reserves costs money.

In other words:

The response to a shock can be inflationary even after the original shock disappears.

That's especially true in energy markets.

Once countries realize how vulnerable they are, they tend to prioritize security over efficiency.

And security is rarely the cheapest option.

For decades, the global economy was optimized for efficiency.

The next decade may be increasingly optimized for resilience.

That's a subtle shift.

But it has enormous implications for inflation, supply chains, and how capital gets invested.

4

A generation ago, career advice was relatively simple.

Get a degree.

Develop a skill.

Climb the ladder.

The problem today isn't that this advice is wrong.

It's that nobody knows which ladders will still exist.

That's new.

For most of modern history, technological change happened slowly enough that people could make long-term career decisions with reasonable confidence.

Today, entire industries can change in a few years.

The challenge isn't keeping up.

The challenge is choosing.

Should you become a programmer?

AI writes code.

Should you go into finance?

AI builds models.

Should you become a consultant?

AI summarizes research.

The uncertainty isn't whether these professions survive.

It's what the entry point looks like five years from now.

That's what makes this moment unusual.

The question isn't:

"What job is safest?"

The question is:

"Which skills remain valuable even if the tools change?"

That's a much harder question.

And it's one many colleges still aren't preparing people to answer.

40

A generation ago, career advice was relatively simple.

Get a degree.

Develop a skill.

Climb the ladder.

The problem today isn't that this advice is wrong.

It's that nobody knows which ladders will still exist.

That's new.

For most of modern history, technological change happened slowly enough that people could make long-term career decisions with reasonable confidence.

Today, entire industries can change in a few years.

The challenge isn't keeping up.

The challenge is choosing.

Should you become a programmer?

AI writes code.

Should you go into finance?

AI builds models.

Should you become a consultant?

AI summarizes research.

The uncertainty isn't whether these professions survive.

It's what the entry point looks like five years from now.

That's what makes this moment unusual.

The question isn't:

"What job is safest?"

The question is:

"Which skills remain valuable even if the tools change?"

That's a much harder question.

And it's one many colleges still aren't preparing people to answer.

38

The best real estate opportunities rarely show up when everyone feels optimistic.

As financing tightens and uncertainty keeps investors on the sidelines, quality assets are trading at discounts that haven't been seen in years.

This week, Victor Menasce @VMenasce joins the Wealth Formula Podcast to break down where he's seeing opportunity, why some multifamily properties are selling 30–40% below peak values, and how smart investors are navigating today's commercial real estate market.

Watch the full episode to hear where the next opportunities may be emerging:

youtu.be/DV5_IYzNvRg

#CommercialRealEstate #RealEstateInvesting #MultifamilyInvesting #PassiveIncome #distressedproperty

11

The stock market and the bond market are telling slightly different stories right now.

And that's worth paying attention to.

Stocks seem incredibly optimistic.

Major indexes are near highs.

Investors are betting on AI.

They're betting on productivity.

They're betting that corporate earnings keep growing.

The bond market is more cautious.

Not panicked.

Not predicting disaster.

Just more cautious.

Higher yields suggest investors still see inflation as a risk.

They still see uncertainty.

They still want compensation for lending money long term.

That's an interesting divergence.

Because markets usually become most dangerous when everyone agrees.

Today, they don't.

One market is saying:

"The future looks great."

The other is saying:

"Maybe. But there are still some things to worry about."

Neither market has to be completely right.

Neither market has to be completely wrong.

But when two of the largest markets in the world are sending different signals...

it's usually worth asking why.

Especially in an environment where:

Inflation remains elevated.

Energy markets remain volatile.

AI is reshaping productivity.

And economic growth keeps surprising people.

The most interesting thing about this market may not be what stocks are saying.

It may be what bonds are refusing to say.

15

Some of the best real estate investments in history were made when the headlines were overwhelmingly negative.

When financing dries up, lenders become restrictive, sellers become motivated, and uncertainty keeps many investors on the sidelines, opportunities begin to emerge for those willing to look beyond today's fear.

That is precisely where we find ourselves today.

Commercial real estate has endured one of the most challenging environments in decades. Rising interest rates, tighter credit conditions, and a wave of new supply have placed significant pressure on many markets.

Yet while these challenges have created distress, they have also created something investors haven't seen in years: the ability to buy quality assets at substantial discounts to replacement cost and prior valuations.

The question is not whether opportunities exist. The question is where they exist and how to identify them.

This week, I sat down with real estate investor and entrepreneur Victor Menasce @VMenasce to discuss what he's seeing across the commercial real estate landscape.

We talk about why some multifamily properties are trading 30-40% below peak values, how oversupply is impacting certain markets, and why investors who understand local supply-and-demand dynamics may be positioned to benefit from the current dislocation.

Victor also makes an important point that often gets lost in national discussions. Real estate is not one market. Every city, neighborhood, and asset class has its own story.

While some areas remain challenged, others continue to benefit from powerful long-term drivers, including population growth, immigration, healthcare demand, and housing affordability trends.

Today's environment resembles the periods that have historically produced exceptional long-term returns. Institutional investors, family offices, and large private capital pools are increasingly stepping into distressed situations, not because they believe conditions are perfect, but because they recognize that buying quality assets during periods of pessimism has often been a winning strategy.

Of course, success still requires discipline. Financing matters. Market selection matters. Understanding future supply matters. But for investors willing to do the work, today's market may ultimately be remembered less for the distress it created and more for the opportunities it presented.

Watch on YouTube:

youtu.be/DV5_IYzNvRg

Listen on Apple Podcasts:

podcasts.apple.com/us/podcas…

Listen on Spotify:

open.spotify.com/episode/3B6…

15

Dental professionals: I joined Dr. Sonny Spera @drspera on the Dentist in General podcast to discuss investing strategies, tax planning, and ways you can keep more of what you earn.

Watch here: youtube.com/watch?v=VnNpCMCE…

#DentistInvesting #TaxStrategies #DentalPractice #WealthBuilding #PassiveIncome

1

1

34

For 30 years, globalization helped keep inflation low.

Companies moved production to places with cheaper labor.

Consumers got lower prices.

Businesses got higher margins.

Everybody got used to that world.

But that world is changing.

Supply chains are being reshored.

Critical industries are being brought back home.

Semiconductors.

Manufacturing.

Energy infrastructure.

Industrial capacity.

The problem?

Doing those things in the U.S. is more expensive.

Which means the very process of rebuilding industrial capacity can be inflationary.

That's where AI enters the picture.

Most people think of AI as a technology story.

It may be an economic story.

Because if AI allows workers and businesses to become dramatically more productive...

it can help offset some of the inflationary pressure created by onshoring.

In other words:

The U.S. is trying to do something difficult.

Bring production back home...

without permanently driving costs through the roof.

That's a much easier task if productivity is accelerating at the same time.

Which creates a fascinating possibility.

AI isn't just another tech boom.

It may become the replacement for one of the biggest economic tailwinds of the last three decades.

Globalization helped suppress inflation.

AI might be asked to do the same thing.

The next decade could be a race between rising costs and rising productivity.

And that outcome may determine far more than just the future of technology.

7

The biggest winners of the next decade won't just be the countries with the best technology, but also those with the reliable, abundant, and affordable energy needed to power it.

#coal #EnergyPolicy #ArtificialIntelligence #coalplant #Economy

9

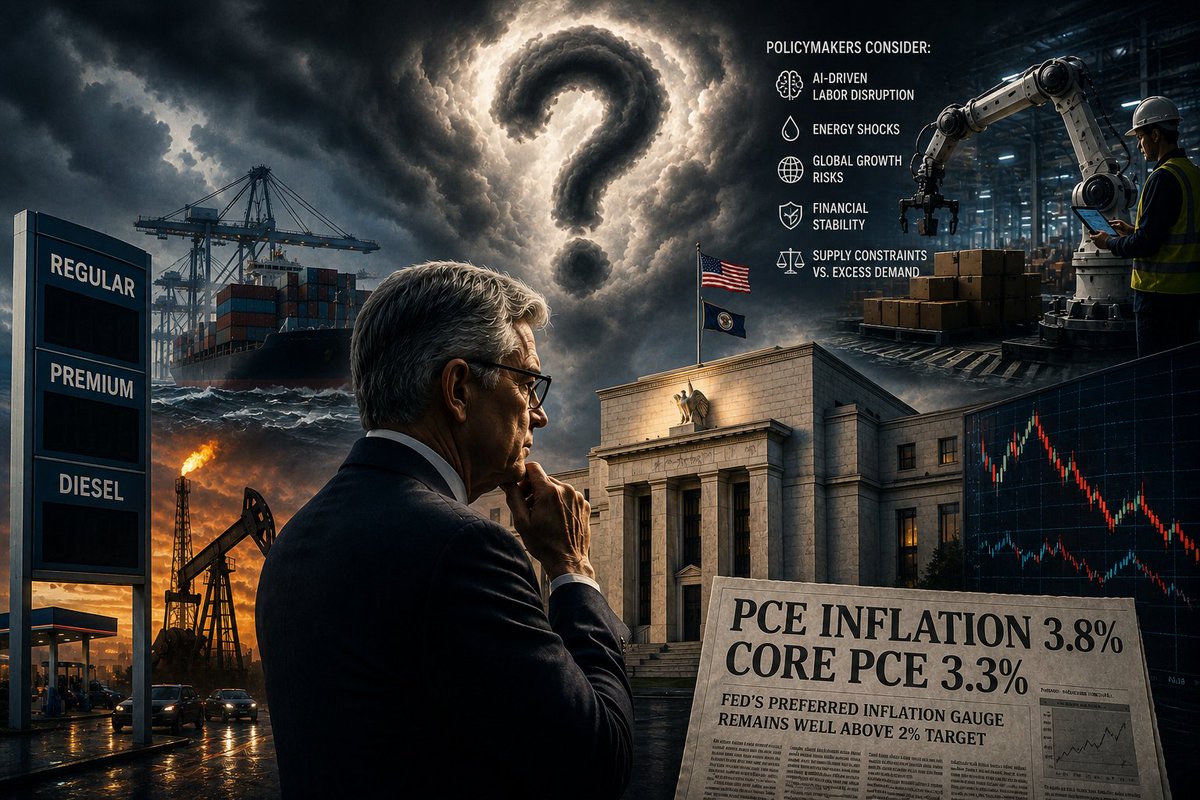

Inflation isn't the strange part.

The strange part is that we're even talking about rate cuts.

Headline PCE inflation just hit 3.8%.

Core PCE is running at 3.3%.

Both remain well above the Fed's 2% target.

Under a traditional playbook, this shouldn't be a debate.

Higher inflation should mean tighter policy.

End of story.

But today's economy isn't following a traditional playbook.

Because policymakers aren't just looking at inflation.

They're also looking at:

AI-driven labor disruption.

Energy shocks.

Global growth risks.

Financial stability.

And the possibility that some inflation is being driven by supply constraints rather than excess demand.

That's where things get complicated.

Higher rates can reduce demand.

But they can't produce more oil.

They can't reopen shipping routes.

They can't rebuild inventories.

So the Fed is left trying to answer a difficult question:

How much of today's inflation can monetary policy actually solve?

That's why the debate has become so contentious.

Not because inflation is low.

Because inflation is still too high...

and policymakers aren't fully convinced the old tools work the way they used to.

The real disagreement isn't about where inflation is today.

It's about what's causing it.

And depending on that answer, the correct policy response could look completely different.

15

Treasury Secretary Bessent says the U.S. is moving "very quickly" on a Strategic Bitcoin Reserve, a digital asset initiative, and advancing the Clarity Act.

#Bitcoin #BTC #CryptoNews #DigitalAssets #CryptoRegulation

25

Where are mortgage rates headed?

Find out on this week's episode with Rob Chrisman from Chrisman Commentary @ChrismanNews:

youtu.be/J5950_KvIms

#mortgagerates #FederalReserve #KevinWarsh #JeromePowell #FedChair

11

Imagine graduating with a finance degree today.

You spent four years preparing for an analyst job.

Meanwhile, the electrician down the street has more work than he can handle.

Ten years ago, that would have sounded ridiculous.

Today, it doesn't.

For years, people assumed automation would come for physical labor first.

Factories.

Construction.

Trades.

Instead, some of the first jobs feeling real pressure are sitting behind a computer.

Analysts.

Junior consultants.

Entry-level finance roles.

Administrative work.

The reason is simple.

Replacing a repetitive digital task is often easier than replacing a human operating in the physical world.

A spreadsheet is easier to automate than a construction site.

A report is easier to automate than an electrical grid.

A financial model is easier to automate than a hospital.

That's creating a strange inversion.

The jobs many people viewed as "future proof" are suddenly facing disruption.

While electricians, infrastructure workers, nurses, HVAC technicians, and construction crews remain in short supply.

At least for now.

But the bigger issue isn't just job replacement.

It's career development.

For decades, white-collar careers followed a predictable path:

Junior work → experience → expertise.

The repetitive work wasn't the destination.

It was the training.

If AI removes enough of those entry-level tasks, how do future experts get built?

How does an analyst become a senior analyst?

How does a consultant become a partner?

That's the part most people aren't talking about.

AI isn't just changing jobs.

It may be changing the process by which expertise itself gets created.

25