Stay Hungry Stay Foolish

Joined April 2020

- Tweets 10,534

- Following 1,032

- Followers 2,004

- Likes 78,094

1,144 Photos and videos

I sold my flat in 2015, moved to Japan, lived there for 3y. Joined all tech events in Tokyo btw 2015-2018. I learned a lot about blockchains, i lost money in 2018 dump, I started following @el33th4xor. Sometimes i wondered why i was in Japan anyways. Now i am all in for $Avax ❤️

13

8

107

I think this proves where the crypto liquidity went for sure 🤷♂️

Jun 13

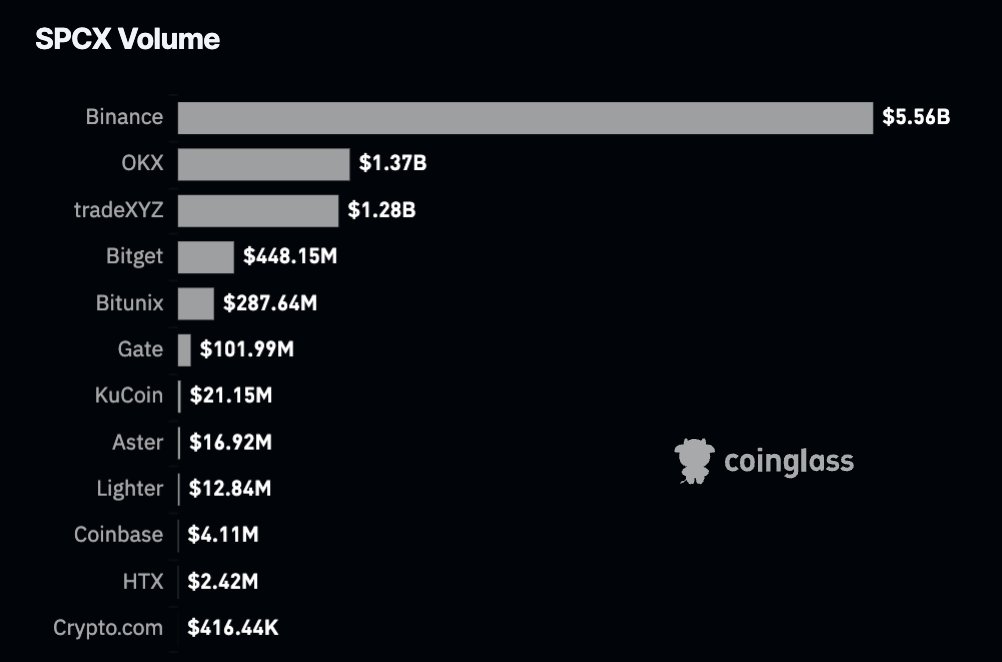

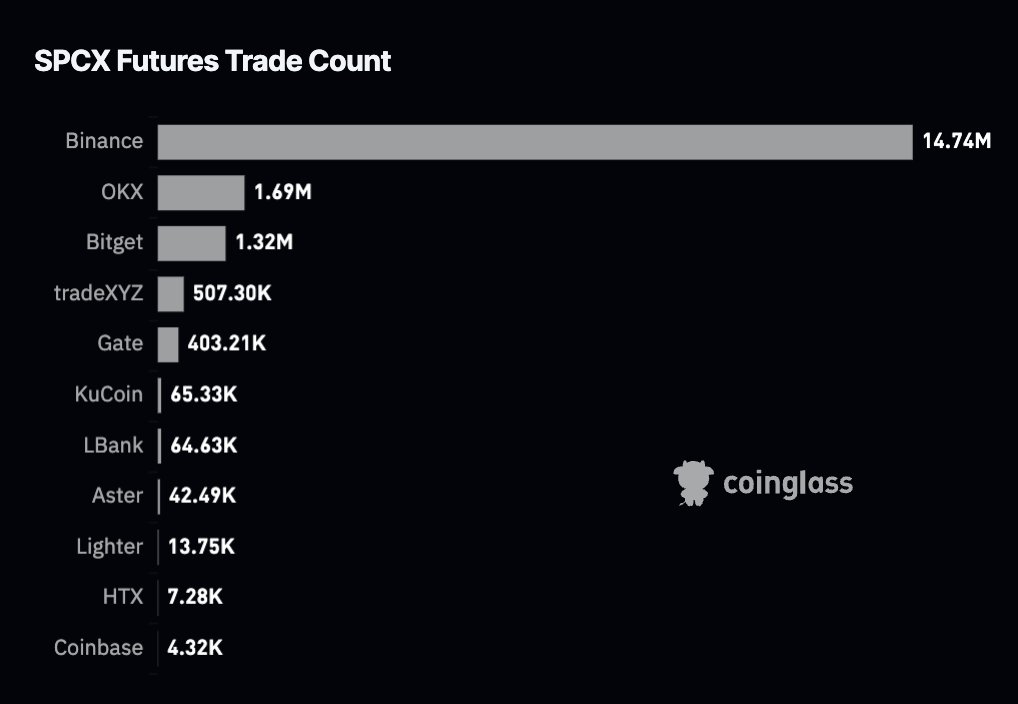

⚡️SPACEX BECOMES BINANCE’S NO. 2 MOST-TRADED PRODUCT

Binance recorded $5.6 BILLION n in SpaceX perpetual volume in 24 hours and over $9 BILLION across the pre-IPO and Nasdaq listing period.

The exchange captured over 60% of volume across CEX and DEX venues, while leading SPCX/USDT open interest at $167.2 MILLION.

Binance also processed 14.74 million SPCX futures trades, nearly 9 times OKX’s 1.69 million, per Coinglass.

1

127

Now we can buy some shares , well done 👍

Jun 12

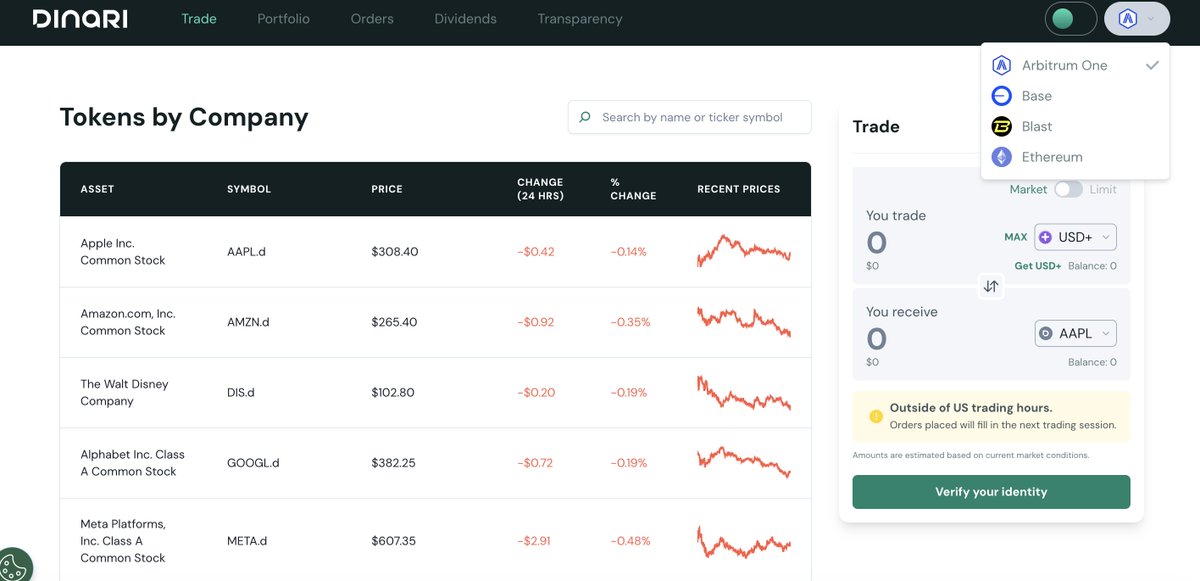

BREAKING NEWS: @DinariGlobal dShares™ are live on Avalanche C-Chain.

The full dShares™ catalog brings tokenized U.S. equities, backed by real shares, into Avalanche’s broader ecosystem.

24/7 access to U.S. markets for eligible users from 85 countries. More 👇

2

57

Disinformation era!

What’s right what’s wrong who knows 🤷♂️

Jun 12

This is completely false. All reports claiming a deal has been reached, including Trump's claims yesterday are market manipulation ahead of today’s SpaceX IPO. Iran has explicitly rejected that any deal has been finalized.

1

110

BitMani retweeted

Jun 12

IRAN CONFIRMS US IRAN DEAL

#BREAKING

Community note

Iran has not confirmed any US-Iran deal, with officials stating no agreement has been finalized and reports are "merely speculation." cnn.com/2026/06/11/wor… reuters.com/world/middle-e…

413

747

5,941

1,792,145

Don’t buy more, just hodle as you said.

And exit slowly in a bull market.

Very simple, to hodle you just have to NOT sell , ok?

In the depths of the 2022 crypto winter, our average cost basis was $30K while $BTC traded nearly 50% below it at $16K. What did we do? We bought more.

1

3

146

Not sure if this is real and holds but if it is, it's great for everyone.

LFG.

Jun 11

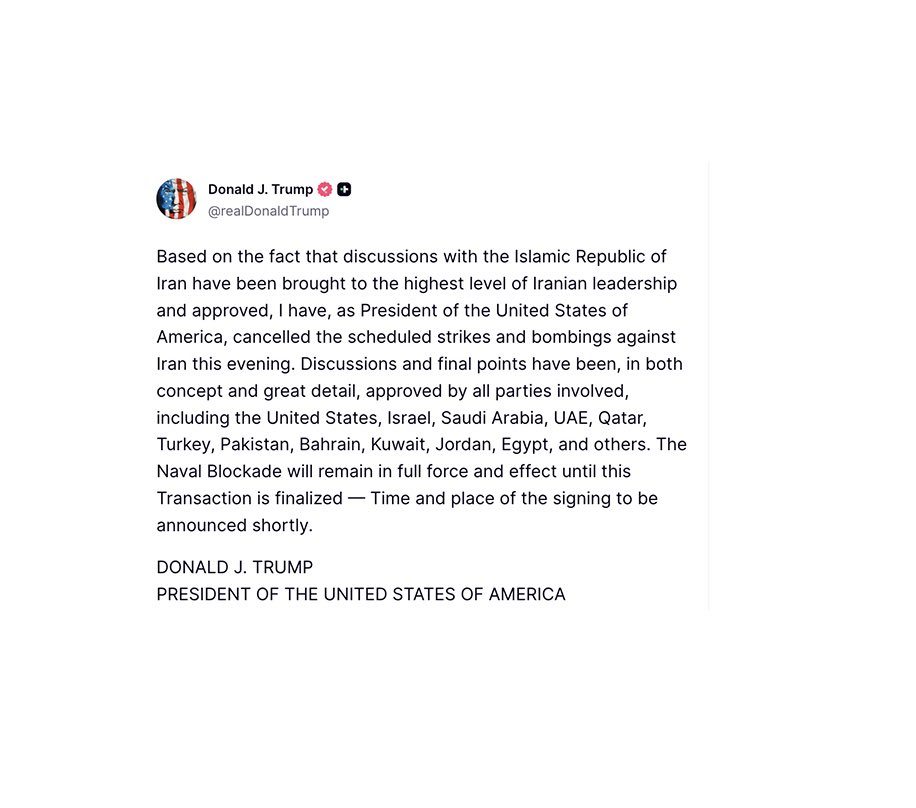

🇺🇸 PRESIDENT TRUMP JUST POSTED!!

The strikes on Iran are OFF

A final deal has been approved by all parties. The blockade stays until it's signed.

1

4

71

61% of all DeFi Active Loan share.

$1 billion FDV.

that's it, that's the tweet.

Jun 11

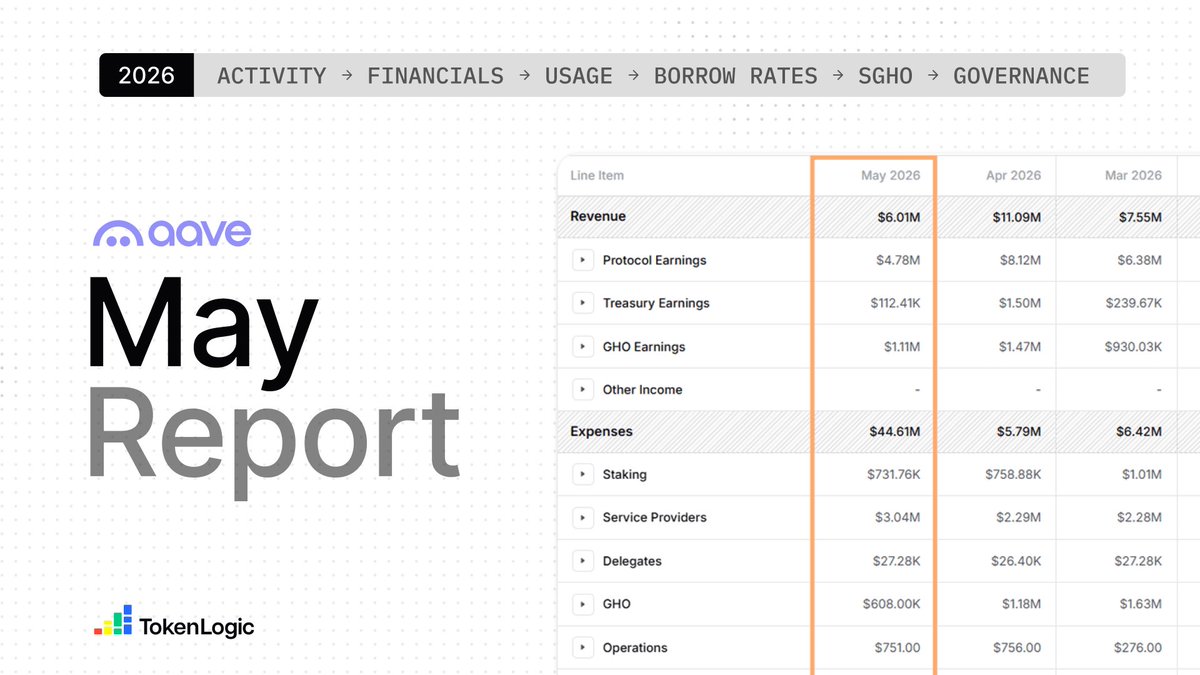

1/ The @aave May 2026 Report is live 👻

Key metrics for May:

▪️ $26B user deposits

▪️ $11B active loans

▪️ $6M protocol revenue

▪️ 60.7% active loans market share

▪️ 116k active users

Full breakdown ↓

1

8

623

Aave FDV $1billion

Aave annual revenue $1billion (most likely)

wtf 🤔

Jun 10

Aave's protocol revenue over the past few years:

2020: $177.12K

2021: $252.45M

2022: $137.41M

2023: $105.26M

2024: $456.47M

2025: $907.70M

2026 YTD: $333.14M

All onchain.

1

3

466

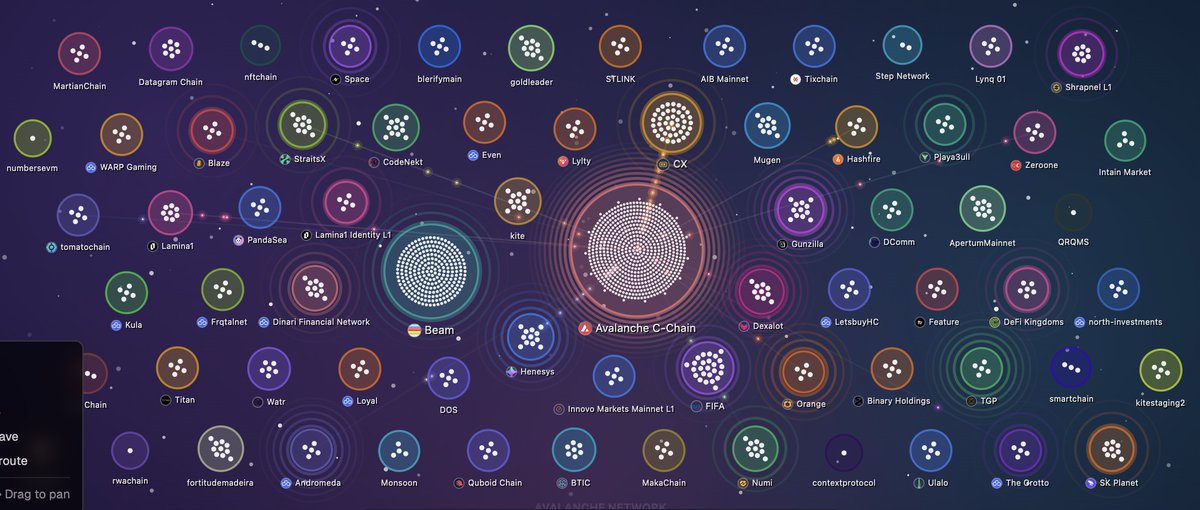

When you see an interesting news/announcement about something coming to on chain yet it doesn’t mention which chain, be sure it’s on Avalanche 👌

Invisible and invincible Avalanche 🔺🚀

A trillion-dollar industry behind the US manufacturing and solar buildout still runs on paperwork.

A deal in a market with <2% delinquency can take up to 6 months to close.

Trad•Fi and W3 are bringing composability to capital workflows behind a $650M private credit pipeline.

1

1

7

783

BitMani retweeted

the best settlement rail is the one no one notices

> Axiym: $1.4B cross-border on Avalanche, Tether-backed, MSBs never touch crypto

> Tassat: $2.5T of proven bank-grade settlement, now on a dedicated L1

> KBank <> StraitsX corridor under MAS

the pattern: @avax as invisible settlement underneath rails that already exist

7

13

87

7,371

BitMani retweeted

More private credit is coming to Avalanche.

Trad.Fi is bringing up to $650M in private credit onto programmable rails, with @w3arew3 powering the capital workflows behind it leveraging @avax.

This marks another practical private credit application: US equipment financing across manufacturing, industrial, and residential solar, with core capital workflows moving onto programmable infrastructure. Another example of onchain rails being applied to real financing activity.

The private credit, asset-backed finance, and fintech lending ecosystem continues to grow on Avalanche.

coindesk.com/business/2026/0…

15

25

169

10,114

👀

Jun 9

Iran has sent its draft agreement to the US, and early signs suggest the Trump administration finds it acceptable.

1

74

Well well well, now you are talking but what was that you were praising Morpho’s mcap vs tvl compared to Aave’ s just a few weeks ago when I also argued with you?

I agree with your below take it’s just that how come you posted some terrible take a few weeks ago that I didn’t understand.

Jun 9

aave generates $948m in annualized fees at a $949m market cap. that's a 1.0x price-to-sales ratio. morpho generates $202m in fees, retains $0 for token holders, and trades at $1.27b. the market is paying a 6.3x premium for morpho's growth narrative over aave's proven revenue machine. aave V4 just shipped hub-and-spoke architecture copied directly from morpho. if the DAO turns on aggressive buybacks with that fee revenue the re-rating from 1x to even 3x P/S is a 3x. morpho's entire bull case requires tokenomics that literally do not exist yet. it is incredibly embarrassing that the market prices $0 in retained revenue higher than $948m in retained revenue

1

195

Awesome article, it's very well worth reading.

7

581

BitMani retweeted

Jun 6

Ghotemin

Let’s build for the summer 🥵🔺

131

48

272

6,934

BitMani retweeted

Jun 6

Hot Emin in control. 🫡

8

17

90

2,532

This is true and the question is why the correlation couldn’t be established even after 8 months 🤔

Jun 4

OCTOBER 10TH COMPLETELY F*CKED THE MARKETS.

$BTC and the Nasdaq were moving in sync until the October 10th crash.

Since then, BTC is down 47% while the Nasdaq is up 20%.

If Bitcoin had kept up with the Nasdaq, it would be around $140,000 today.

4

389