I decode the forces that shape our world before they shape us. finance, macro & geopolitics. check Highlights for my work🔖

Joined June 2021

- Tweets 19,352

- Following 1,176

- Followers 2,787

- Likes 22,771

1,356 Photos and videos

Markets have evolved, they are more efficient. Hence the person who waits for growth numbers and reports is usually is outperformed by someone who has anticipated growth and invested in it

Good that you pointed out market efficiencies and how inefficient the market was before 20 years

Please share your thoughts?

@sakshimiishra @hmalviya9 @YashasEdu @0xCheeezzyyyy @thelearningpill @satyaki44 @Tom_Degen68 @kenodnb

16h

some thoughts on Space $2T valuation, I still believe spaceX can justify its valuation in the future but something different is happening structurally across IPOs of such big companies

Earlier it was:

Company performs → revenue grows → valuation increases.

Now it’s:

Narrative builds → future gets priced in → and we wait for reality to catch up.

9

1

20

540

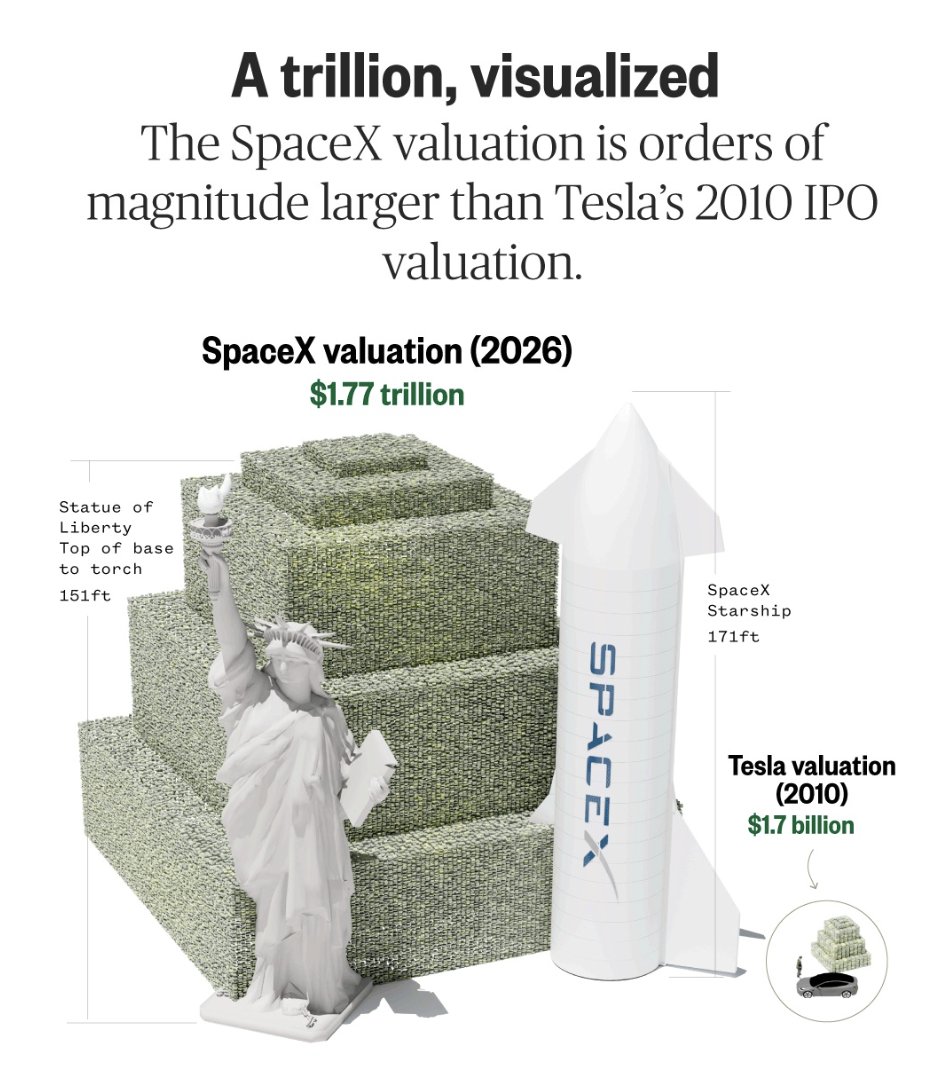

SpaceX crossed a $2 trillion valuation. The analysts are already out with their revenue comparisons.

Reliance Industries: $125B in revenue. SpaceX: under $20B . On that basis alone, the valuation looks absurd.

The problem with revenue-based comparisons

When analysts pull up a DCF on SpaceX and benchmark it against Reliance, Aramco, or any cashflow-generating conglomerate, they're doing something technically correct and intellectually lazy at the same time.

Revenue multiples are tools built for businesses operating inside established markets with known ceiling sizes.

What do you do when the market doesn't exist yet?

Reliance generates $125B in revenue serving an Indian economy that's been structurally growing for decades. Retail, telecom, petrochemicals. These are real businesses with real floors. But they have something else: a ceiling. The TAM is known. The competition is domestic and manageable. The margin expansion playbook is familiar.

SpaceX doesn't have a ceiling yet. That's the actual analytical challenge.

What SpaceX actually is

Three businesses, one company:

Space transportation is the foundational layer. This is the part that most people understand least because it's never existed at commercial scale before. @SpaceX has done something the entire aerospace industry spent 60 years claiming was either impossible or economically unviable, they've made rockets reusable.

To understand why this matters, think about what it would mean if commercial aircraft were thrown away after every flight. The entire economics of aviation would collapse. Airlines wouldn't exist. International trade wouldn't work the way it does. Reusability didn't just lower launch costs it changed the economic structure of what space access means.

Starship takes this further. It's the largest and most powerful rocket ever built. Fully reusable. Designed to carry 100-150 metric tons to low Earth orbit per launch. For reference, the Saturn V. the rocket that sent humans to the Moon could carry 130 metric tons but was fully expendable.

Starship, if it reaches full operational cadence, could bring launch costs down to $10-50 per kilogram to orbit. The current market average sits around $1,000-2,000 per kilogram.That's an order-of-magnitude shift.

@Starlink is the only segment generating meaningful profit today. Around 4.6 million subscribers globally as of early 2025. This is the segment that funds everything else. It also happens to be a strategic asset the US government has demonstrated serious interest in preserving. Ukraine used Starlink for battlefield coordination, But Starlink isn't the business that justifies a $2 trillion valuation.

@xai is still early. Elon's AI company sits adjacent to SpaceX in terms of corporate structure but is deeply interlinked through shared infrastructure priorities: compute, satellites, data. The integration thesis here is long-dated and speculative. Leave it aside for now.

The IPO mechanics deserve attention

The way this deal was structured matters more than most people realize.

Fidelity dropped its minimum IPO eligibility threshold to $2,000 specifically for this offering. The standard is $500,000. That's deliberate participation engineering to broaden the holder base and reduce concentration risk at launch.

The lockup terms were tighter than typical:

365-day lockup to bigger investors, The insider unlock schedule was staggered and designed to prevent the cliff-dump that usually follows 180-day lockup expirations.

Retail participation came with a 15-day flipper clause that came with a real consequence: sell early, get tagged, lose access to future IPO allocations at participating brokers.

SpaceX structured its offering to dampen that dynamic from the start. Whether it fully works is another question but the intent was clearly to manage float supply, not just raise capital.

How to think about the valuation

The $2 trillion number is the market pricing in a probability distribution, not a certainty. That's the part the revenue-comparison analysts skip.

In 2010, if you'd argued Bitcoin would become a trillion-dollar asset class, the response would have been laughter.

In 1993, if you'd said you could have a video call with someone 10,000 miles away for free, people would have questioned your judgment.

The investors who earned generational returns on those bets weren't wrong about the technology; they were early and tolerant of distributions that looked absurd at the time.

The SpaceX bet isn't that it will be a bigger Reliance or Aramco. It's that affordable space access creates new industries we can't currently name, the same way affordable internet access created Google, Amazon, Netflix, and the entire cloud infrastructure stack, industries that didn't exist before the cost of bandwidth collapsed.

Tesla faced identical criticism. Overvalued relative to revenue. Revenue too small relative to the incumbents. No path to profitability that made sense under traditional automotive unit economics.

The counterargument that they were building a software-defined, direct-to-consumer, energy-integrated vehicle company turned out to be correct.

@elonmusk 's track record here is specific:

electric vehicles when the world was laughing, reusable rockets when aerospace said it was impossible, satellite internet when Iridium had already failed.

That's a consistent pattern of targeting markets where incumbents had structural incentives to not solve the problem.

Should you buy SpaceX now?

No. Not yet.

The market is pricing SpaceX on future business, but most of the current revenue comes from Starlink. The space transportation thesis, the one that actually justifies the order-of-magnitude valuation premium is still being proven. Starship has had successful test flights but hasn't demonstrated full operational reusability at commercial cadence. The point-to-point Earth transportation business (New York to Tokyo in under an hour) doesn't exist yet. The lunar economy doesn't exist yet. The Mars thesis is a decade-plus away.

Early investors are sitting on significant unrealized gains. The lockup structure held prices through the IPO window, but a $2T valuation with sub-$20B in current revenue means repricing will happen as the market gets more data on actual business execution versus the projected vision.

Watch the 365-day lockup expiry. Watch Starship's operational cadence through 2025-2026. Watch Starlink subscriber growth rates, if growth flattens, the bridge business starts looking expensive too.

The Tesla parallel is instructive: post-lockup drop, overvaluation criticism, then a long period of range-bound trading before the business caught up to the story.

Bunt's POV

I'm not dismissing SpaceX. I'm saying the entry point matters as much as the thesis.

The vision is real. Affordable space access is one of the few technological transitions that actually creates new industries rather than disrupting existing ones. If Starship reaches full operational cadence at the cost targets SpaceX has published, the downstream effects are difficult to model because the markets don't exist yet and that's the point.

But a $2T valuation on sub-$20B in revenue means you're paying for a future that hasn't been delivered yet. That future is plausible. Musk has earned credibility on exactly this kind of bet.

Wait for the lockup expiry. Track whether Starship actually hits its operational targets. Watch Starlink subscriber growth. If the business is executing, you'll get a better entry. If it isn't, you'll be glad you waited.

17

7

33

2,474

Hope y’all liked it

@hmalviya9

@thelearningpill

@0xspicexr

@Eli5defi

@YashasEdu

@satyaki44

@kenodnb

@0xCheeezzyyyy

@tradeguru

@RubiksWeb3

@SachinHMx

@TheDeFiKenshin

@Tom_Degen68

@_thespacebyte

@Kruys_Collins

SpaceX crossed a $2 trillion valuation. The analysts are already out with their revenue comparisons.

Reliance Industries: $125B in revenue. SpaceX: under $20B . On that basis alone, the valuation looks absurd.

The problem with revenue-based comparisons

When analysts pull up a DCF on SpaceX and benchmark it against Reliance, Aramco, or any cashflow-generating conglomerate, they're doing something technically correct and intellectually lazy at the same time.

Revenue multiples are tools built for businesses operating inside established markets with known ceiling sizes.

What do you do when the market doesn't exist yet?

Reliance generates $125B in revenue serving an Indian economy that's been structurally growing for decades. Retail, telecom, petrochemicals. These are real businesses with real floors. But they have something else: a ceiling. The TAM is known. The competition is domestic and manageable. The margin expansion playbook is familiar.

SpaceX doesn't have a ceiling yet. That's the actual analytical challenge.

What SpaceX actually is

Three businesses, one company:

Space transportation is the foundational layer. This is the part that most people understand least because it's never existed at commercial scale before. @SpaceX has done something the entire aerospace industry spent 60 years claiming was either impossible or economically unviable, they've made rockets reusable.

To understand why this matters, think about what it would mean if commercial aircraft were thrown away after every flight. The entire economics of aviation would collapse. Airlines wouldn't exist. International trade wouldn't work the way it does. Reusability didn't just lower launch costs it changed the economic structure of what space access means.

Starship takes this further. It's the largest and most powerful rocket ever built. Fully reusable. Designed to carry 100-150 metric tons to low Earth orbit per launch. For reference, the Saturn V. the rocket that sent humans to the Moon could carry 130 metric tons but was fully expendable.

Starship, if it reaches full operational cadence, could bring launch costs down to $10-50 per kilogram to orbit. The current market average sits around $1,000-2,000 per kilogram.That's an order-of-magnitude shift.

@Starlink is the only segment generating meaningful profit today. Around 4.6 million subscribers globally as of early 2025. This is the segment that funds everything else. It also happens to be a strategic asset the US government has demonstrated serious interest in preserving. Ukraine used Starlink for battlefield coordination, But Starlink isn't the business that justifies a $2 trillion valuation.

@xai is still early. Elon's AI company sits adjacent to SpaceX in terms of corporate structure but is deeply interlinked through shared infrastructure priorities: compute, satellites, data. The integration thesis here is long-dated and speculative. Leave it aside for now.

The IPO mechanics deserve attention

The way this deal was structured matters more than most people realize.

Fidelity dropped its minimum IPO eligibility threshold to $2,000 specifically for this offering. The standard is $500,000. That's deliberate participation engineering to broaden the holder base and reduce concentration risk at launch.

The lockup terms were tighter than typical:

365-day lockup to bigger investors, The insider unlock schedule was staggered and designed to prevent the cliff-dump that usually follows 180-day lockup expirations.

Retail participation came with a 15-day flipper clause that came with a real consequence: sell early, get tagged, lose access to future IPO allocations at participating brokers.

SpaceX structured its offering to dampen that dynamic from the start. Whether it fully works is another question but the intent was clearly to manage float supply, not just raise capital.

How to think about the valuation

The $2 trillion number is the market pricing in a probability distribution, not a certainty. That's the part the revenue-comparison analysts skip.

In 2010, if you'd argued Bitcoin would become a trillion-dollar asset class, the response would have been laughter.

In 1993, if you'd said you could have a video call with someone 10,000 miles away for free, people would have questioned your judgment.

The investors who earned generational returns on those bets weren't wrong about the technology; they were early and tolerant of distributions that looked absurd at the time.

The SpaceX bet isn't that it will be a bigger Reliance or Aramco. It's that affordable space access creates new industries we can't currently name, the same way affordable internet access created Google, Amazon, Netflix, and the entire cloud infrastructure stack, industries that didn't exist before the cost of bandwidth collapsed.

Tesla faced identical criticism. Overvalued relative to revenue. Revenue too small relative to the incumbents. No path to profitability that made sense under traditional automotive unit economics.

The counterargument that they were building a software-defined, direct-to-consumer, energy-integrated vehicle company turned out to be correct.

@elonmusk 's track record here is specific:

electric vehicles when the world was laughing, reusable rockets when aerospace said it was impossible, satellite internet when Iridium had already failed.

That's a consistent pattern of targeting markets where incumbents had structural incentives to not solve the problem.

Should you buy SpaceX now?

No. Not yet.

The market is pricing SpaceX on future business, but most of the current revenue comes from Starlink. The space transportation thesis, the one that actually justifies the order-of-magnitude valuation premium is still being proven. Starship has had successful test flights but hasn't demonstrated full operational reusability at commercial cadence. The point-to-point Earth transportation business (New York to Tokyo in under an hour) doesn't exist yet. The lunar economy doesn't exist yet. The Mars thesis is a decade-plus away.

Early investors are sitting on significant unrealized gains. The lockup structure held prices through the IPO window, but a $2T valuation with sub-$20B in current revenue means repricing will happen as the market gets more data on actual business execution versus the projected vision.

Watch the 365-day lockup expiry. Watch Starship's operational cadence through 2025-2026. Watch Starlink subscriber growth rates, if growth flattens, the bridge business starts looking expensive too.

The Tesla parallel is instructive: post-lockup drop, overvaluation criticism, then a long period of range-bound trading before the business caught up to the story.

Bunt's POV

I'm not dismissing SpaceX. I'm saying the entry point matters as much as the thesis.

The vision is real. Affordable space access is one of the few technological transitions that actually creates new industries rather than disrupting existing ones. If Starship reaches full operational cadence at the cost targets SpaceX has published, the downstream effects are difficult to model because the markets don't exist yet and that's the point.

But a $2T valuation on sub-$20B in revenue means you're paying for a future that hasn't been delivered yet. That future is plausible. Musk has earned credibility on exactly this kind of bet.

Wait for the lockup expiry. Track whether Starship actually hits its operational targets. Watch Starlink subscriber growth. If the business is executing, you'll get a better entry. If it isn't, you'll be glad you waited.

4

266

Last week, @maplefinance announced an integration with @tempo, a payments blockchain incubated by @stripe and @paradigm.

Fintechs building on Tempo's infrastructure can now offer their customers yield on stablecoin balances through syrupUSDC.

There are thousands of fintechs sitting on stablecoin balances right now.

Most know their customers expect yield on those balances.

The demand and product gap are obvious.

But building a yield product in-house means sourcing counterparties, managing collateral, handling margin calls, writing the credit infrastructure, and taking on the risk decisions yourself.

That is not a fintech problem. That is a lending problem. And most fintechs are not lenders.

So they either launch something fragile, do nothing, or wait for someone to solve it cleanly.

Maple just handed them the solution.

The fintech gets to offer a product their customers actually want.

Maple handles the underwriting, collateral, and risk underneath.

Think about what Tempo represents: infrastructure for enterprise fintechs building financial products at scale.

Maple just got a direct line into that entire stack.

That is what distribution at this layer looks like.

And it is exactly what separates the protocols that matter in five years from the ones that get forgotten.

@syrupsid said something worth sitting with: "Every fintech will offer yield on stablecoin balances within the next two years."

The market will price this in eventually.

The only question is whether you understand it before that happens.

29

5

50

2,378

When centralised exchanges failed, ONDO Delivered. shows their readiness and i believe they'll lead the tokenised equities segment as well

Jun 14

Another big week for tokenization.

Tokenized stocks made headlines as SpaceX was successfully tokenized on IPO day, Fortune launched their inaugural Crypto 100, and more.

Latest tokenization news ↓

1️⃣ Tokenized SpaceX (SPCXon) launched on Solana, Ethereum, & BNB Chain

For the first time, a trillion-dollar IPO is onchain on the same day it goes public.

x.com/OndoFinance/status/206…

2️⃣ Citigroup is rolling out tokenized shares of private companies

High net worth individuals and institutions will be able to access the offerings, starting with tokenized Kaleido stock.

wsj.com/finance/banking/citi…

3️⃣ DBS to launch tokenized physical gold for Singapore retail investors

DBS is also exploring listing the token on its DBS Digital Exchange (DDEx) for accredited and institutional investors.

ledgerinsights.com/dbs-to-la…

4️⃣ Uniswap now supports tokenized stocks

RWAs are now live on Uniswap's Web App, Wallet, and API, bringing tokenized assets to one of the most widely used platforms in onchain finance.

x.com/OndoFinance/status/206…

5️⃣ Fortune launches their inaugural Crypto 100

It ranks the most influential companies shaping the digital asset ecosystem, including Coinbase, Franklin Templeton, and Ondo.

x.com/OndoFinance/status/206…

3

10

338

BUNT retweeted

Jun 12

1/ Crypto adoption is entering a new phase.

For years, digital assets were largely viewed as experimental, speculative, or institutionally inaccessible.

But that narrative has changed meaningfully. BTC and particularly ETH, are increasingly being integrated into the product suites of major financial platforms, treasury companies, funds, and institutional trading venues.

As $ETH adoption deepens, the next question becomes less about whether institutions want ETH exposure, and more about how they should manage it.

Holding $ETH passively gives investors exposure to its long-term upside. But ETH is also a productive asset via PoS yield. For treasuries, funds, and sophisticated users, this creates an obvious opportunity: ETH should not simply sit idle.

The challenge is that native staking is not always operationally simple.

The rabbit hole goes deep → Validator management, withdrawal queues, liquidity constraints, custody requirements & exchange collateral limitations all create friction.

This is esp. true for institutions, where operational resilience, risk management, and liquidity access matter as much as headline yield.

This is where liquid staking becomes increasingly important.

And in 2026, @mETHProtocol $mETH is positioning itself as one of the key yield layers for ETH 🧵

Jun 11

ETH staking is moving beyond yield alone.

“The next phase is about stronger security, deeper liquidity, and better distribution.” - @Defi_Maestro

Read more below on how mETH Protocol is building for 2026.

37

18

90

4,758

BUNT retweeted

Jun 11

Maple has been named to Fortune's Crypto Innovators list, the only onchain credit platform among 30 companies recognized for pushing the digital asset ecosystem forward.

Institutional credit, onchain.

42

30

162

8,567

BUNT retweeted

Jun 11

Market Outlok #8

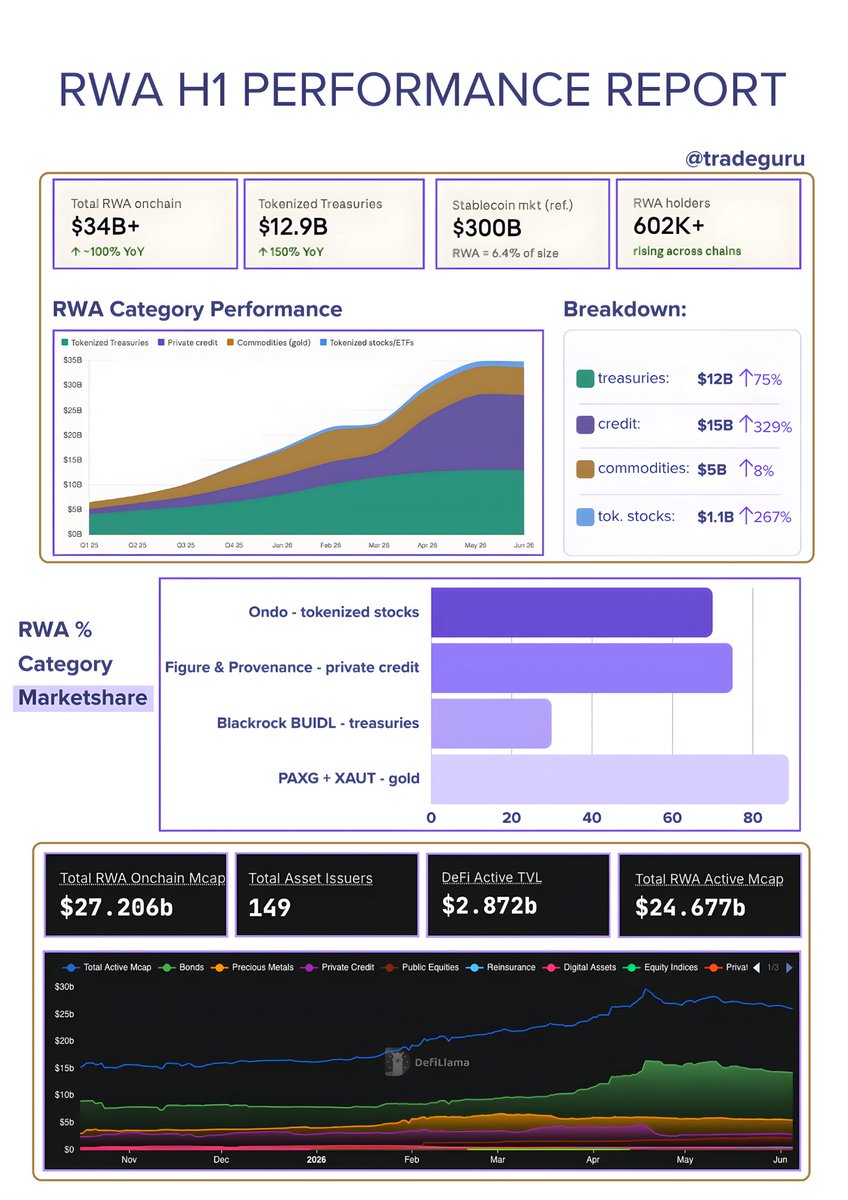

1/8 On-chain RWAs have surpassed $34B, up roughly 100% Year-over-Year.

More importantly, RWA growth is now outpacing stablecoin growth by 6.4%, up from 2.7% in 2025.

The data is becoming impossible to ignore.

A breakdown of where that growth is coming from🧵

May 18

Market Outlook Series #7

1/4 30 days post-Kelp hack, the cross-chain map has redrawn itself.

Solv, Re, Kraken, Lombard, and others, gone from LayerZero. All now live on CCIP.

Despite @PrimordialAA's public mea culpa, L0 has bled $4B in TVL. So why CCIP specifically?

21

23

110

5,249

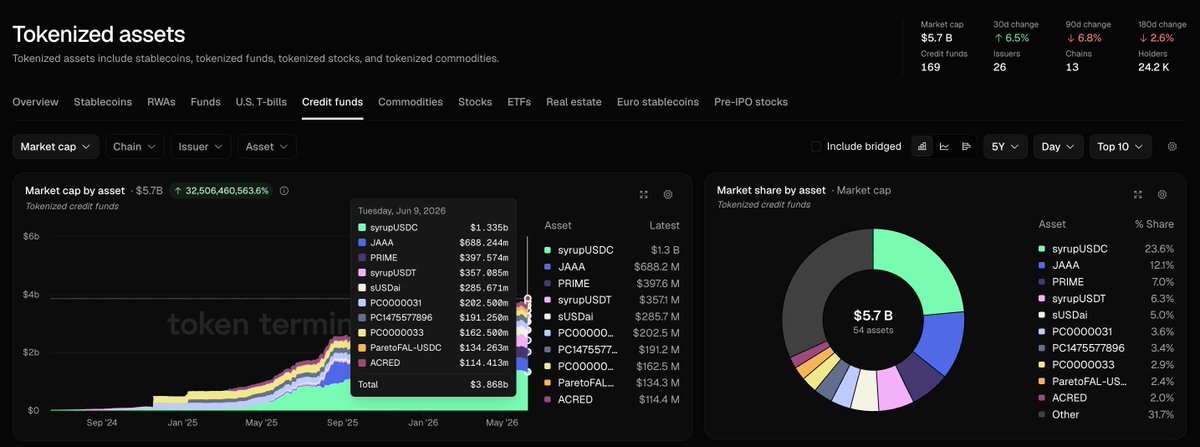

Tokenized Credit Is a $5.7 Billion Market. One Protocol Controls Nearly 30% of It.

As per @tokenterminal The tokenized credit market crossed $5.7 billion in total assets under management as of June 2026. That number is real, on-chain, and verifiable. It spans 54 discrete assets, 169 credit funds, 26 issuers, and 13 chains, with 24,200 unique holders.

The Market Structure

Tokenized credit funds are not a monolith. The category spans institutional fixed-income tokenizations (JAAA Janus Henderson's AAA CLO ETF on-chain), private credit vehicles (PRIME, Pareto), DeFi-native yield instruments (sUSDai), and protocol-issued credit pools (Maple's syrup products).

The capital sitting across these structures has fundamentally different risk profiles, underlying collateral, and liquidity mechanics.

What they share: on-chain issuance, 24/7 transferability, and the ability to deploy yield-bearing exposure at a fraction of the friction traditional credit requires.

The distribution of capital, however, is not even.

syrupUSDC leads the entire category at $1.3 billion a 23.6% market share by itself. The second-largest asset, JAAA, holds $688.2 million (12.1%). PRIME sits third at $397.6 million (7.0%). Everything after that drops below single-digit share.

@maplefinance 's Position in the Market

Maple Finance operates two assets in the top 10👇

syrupUSDC at $1.3 billion and syrupUSDT at $357.1 million. Combined, those two positions represent approximately $1.657 billion in tokenized credit AUM roughly 29.9% of the entire $5.7 billion market.

No single issuer comes close to that concentration. The next largest individual issuer presence is JAAA at $688.2 million, a product backed by Janus Henderson, one of the largest institutional asset managers globally.

Maple, a DeFi-native credit protocol, holds nearly 2.5x that position in on-chain credit.

How Maple Built This Position

The structure matters here. syrupUSDC and syrupUSDT are not yield-bearing wrappers around idle stablecoin reserves. They are direct claims on Maple's active lending book.

The same book that has processed hundreds of millions in institutional credit since 2021 with zero defaults on its core secured lending pools.

That track record is load-bearing. When a credit market expands rapidly as this one has, the question capital managers ask is not "what is the APY" but "what happens when a borrower misses a margin call."

Maple's answer has been structural: overcollateralized borrowing requirements, sub-3-hour margin call cure windows, and a credit committee that selects borrowers by identity, not just collateral ratios.

The result is a product that institutional allocators can underwrite. syrupUSDC's $1.391 billion peak in the week of May 25, 2026 was not retail-driven volume. That capital concentration reflects professional allocation behavior.

The Structural Tension in the Market

The protocol that holds market leadership is the one whose credit quality is not in question. Maple's zero-default record and its position as the clear #1 and #4 assets in the category are the relevant facts.

Competitors are Pareto, sUSDai, PRIME, but none have demonstrated the combination of scale, credit discipline, and product surface area that Maple currently holds.

The more precise read is that a single DeFi-native credit protocol controls nearly 30 cents of every dollar in this market.

BUNT's POV

I've been tracking Maple since before syrup existed. The core question I had and a lot of people had was whether institutional credit could actually scale on-chain without a defaults event eventually blowing up the thesis. That hasn't happened. And now the data shows Maple isn't just surviving in a $5.7B market, it's effectively setting the floor for what the category looks like.

What I find interesting is the gap between Maple's market position and the narrative coverage it gets. JAAA gets cited constantly because it's a Janus Henderson product there's a TradFi trust signal attached to it. Maple's numbers are larger, the credit record is cleaner, and it's running on-chain infrastructure. The coverage hasn't caught up.

syrup isn't a yield product. It's a credit product with yield attached. That distinction matters when everything else in the category hits turbulence.

21

10

38

2,267

Hope y’all liked it

@glebshumakov

@syrupsid

@Castanoartzz

@thelearningpill

@0xspicexr

@Eli5defi

@YashasEdu

@satyaki44

@kenodnb

@0xCheeezzyyyy

@tradeguru

@RubiksWeb3

@SachinHMx

@TheDeFiKenshin

@Tom_Degen68

@_thespacebyte

@Kruys_Collins

Tokenized Credit Is a $5.7 Billion Market. One Protocol Controls Nearly 30% of It.

As per @tokenterminal The tokenized credit market crossed $5.7 billion in total assets under management as of June 2026. That number is real, on-chain, and verifiable. It spans 54 discrete assets, 169 credit funds, 26 issuers, and 13 chains, with 24,200 unique holders.

The Market Structure

Tokenized credit funds are not a monolith. The category spans institutional fixed-income tokenizations (JAAA Janus Henderson's AAA CLO ETF on-chain), private credit vehicles (PRIME, Pareto), DeFi-native yield instruments (sUSDai), and protocol-issued credit pools (Maple's syrup products).

The capital sitting across these structures has fundamentally different risk profiles, underlying collateral, and liquidity mechanics.

What they share: on-chain issuance, 24/7 transferability, and the ability to deploy yield-bearing exposure at a fraction of the friction traditional credit requires.

The distribution of capital, however, is not even.

syrupUSDC leads the entire category at $1.3 billion a 23.6% market share by itself. The second-largest asset, JAAA, holds $688.2 million (12.1%). PRIME sits third at $397.6 million (7.0%). Everything after that drops below single-digit share.

@maplefinance 's Position in the Market

Maple Finance operates two assets in the top 10👇

syrupUSDC at $1.3 billion and syrupUSDT at $357.1 million. Combined, those two positions represent approximately $1.657 billion in tokenized credit AUM roughly 29.9% of the entire $5.7 billion market.

No single issuer comes close to that concentration. The next largest individual issuer presence is JAAA at $688.2 million, a product backed by Janus Henderson, one of the largest institutional asset managers globally.

Maple, a DeFi-native credit protocol, holds nearly 2.5x that position in on-chain credit.

How Maple Built This Position

The structure matters here. syrupUSDC and syrupUSDT are not yield-bearing wrappers around idle stablecoin reserves. They are direct claims on Maple's active lending book.

The same book that has processed hundreds of millions in institutional credit since 2021 with zero defaults on its core secured lending pools.

That track record is load-bearing. When a credit market expands rapidly as this one has, the question capital managers ask is not "what is the APY" but "what happens when a borrower misses a margin call."

Maple's answer has been structural: overcollateralized borrowing requirements, sub-3-hour margin call cure windows, and a credit committee that selects borrowers by identity, not just collateral ratios.

The result is a product that institutional allocators can underwrite. syrupUSDC's $1.391 billion peak in the week of May 25, 2026 was not retail-driven volume. That capital concentration reflects professional allocation behavior.

The Structural Tension in the Market

The protocol that holds market leadership is the one whose credit quality is not in question. Maple's zero-default record and its position as the clear #1 and #4 assets in the category are the relevant facts.

Competitors are Pareto, sUSDai, PRIME, but none have demonstrated the combination of scale, credit discipline, and product surface area that Maple currently holds.

The more precise read is that a single DeFi-native credit protocol controls nearly 30 cents of every dollar in this market.

BUNT's POV

I've been tracking Maple since before syrup existed. The core question I had and a lot of people had was whether institutional credit could actually scale on-chain without a defaults event eventually blowing up the thesis. That hasn't happened. And now the data shows Maple isn't just surviving in a $5.7B market, it's effectively setting the floor for what the category looks like.

What I find interesting is the gap between Maple's market position and the narrative coverage it gets. JAAA gets cited constantly because it's a Janus Henderson product there's a TradFi trust signal attached to it. Maple's numbers are larger, the credit record is cleaner, and it's running on-chain infrastructure. The coverage hasn't caught up.

syrup isn't a yield product. It's a credit product with yield attached. That distinction matters when everything else in the category hits turbulence.

6

203

BUNT retweeted

Jun 9

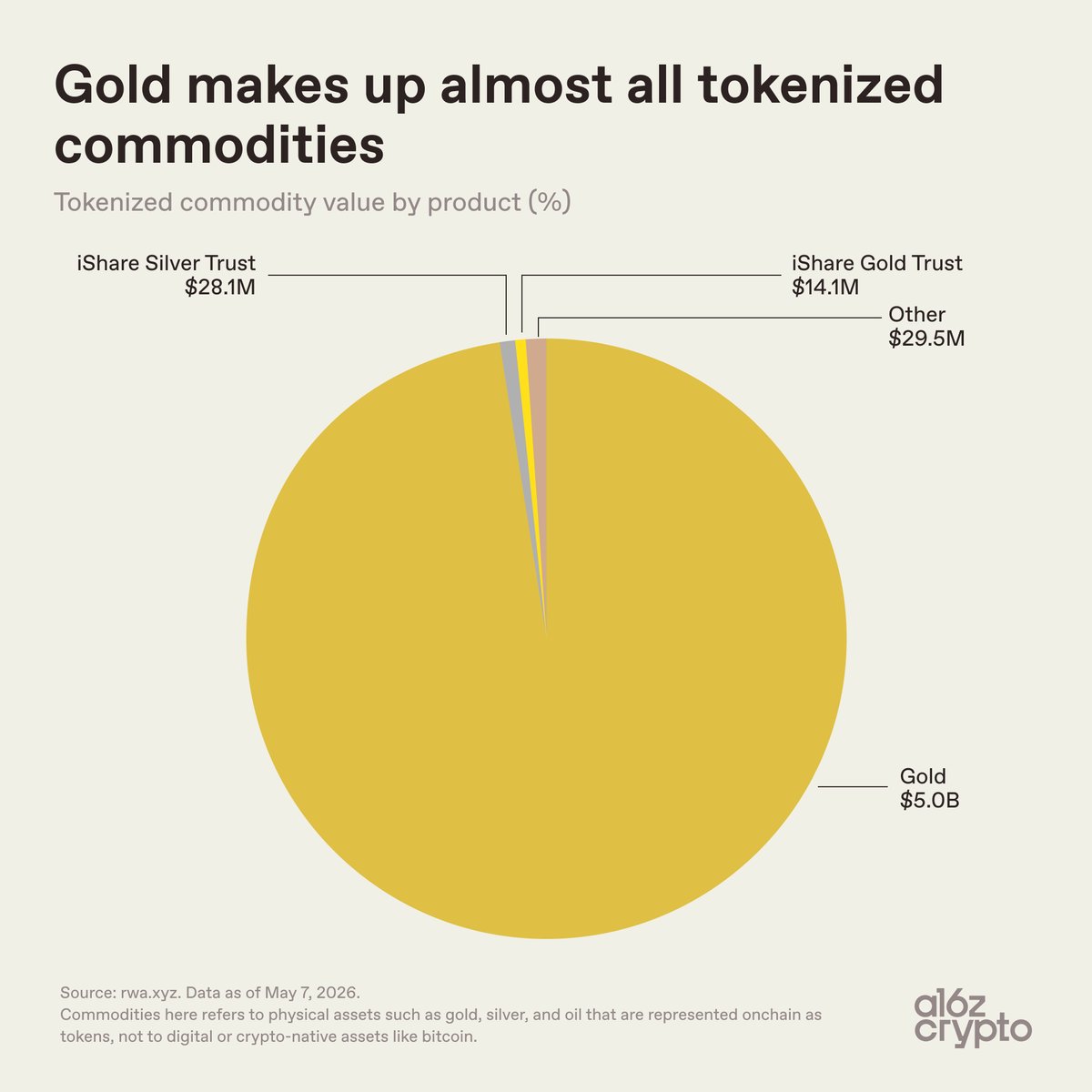

RWA-Fi now sits at ~$34B in distributed assets, growing ~420% in just ~1.25 years (h/t @RWA_xyz), with commodities already accounting for ~20% of that stack.

Within this ~$7.1B segment, gold dominates almost entirely.

That alone is honestly telling, tokenised gold has already achieved a state primed to be one of the next major primitives on-chain.

As the world’s primary SoV asset, gold has always been positioned for preservation and not productivity. But that dynamic starts to change the moment it enters DeFi.

The real unlock isn’t just access, but what you can do with it.

Through composability, gold can evolve from a passive reserve into a capital-efficient asset that can be:

1. deployed as collateral

2. structured into yield strategies

3. integrated into broader financial workflows

And this shift is inevitable imo esp. as liquidity from established issuers continues to scale.

The constraint today isn’t supply.

It’s the lack of on-chain financialisation and meaningful DeFi opportunities around it.

That’s where I personally think @Theo_Network starts to stand out.

With $thGOLD and $thUSD, it introduces structured exposure derived from gold-linked strategies which effectively turning gold into a yield-bearing primitive rather than just a tokenised wrapper.

More interestingly, the yield itself isn't dependent on crypto market activity.

Under the hood, thUSD monetises three long-standing sources of return within institutional gold markets:

🔸 Physical gold leasing demand from refiners, dealers and retailers

🔸 CME futures basis capture, where gold futures trade in contango ~99.5% of the time and converge toward spot at expiry

🔸 Treasury collateral yield from the underlying reserve assets

The result is a DN structure where returns are derived primarily from carry rather than directional exposure to gold itself.

This is an important distinction because the yield originates from established real-world market activity that has existed for decades across commodity and treasury markets which makes it both scalable sustainable.

Early signals already reflect strong demand w/ $100M cap filled in under 14 hours, with DeFi integrations on the horizon.

That positions it as a potential first strong mover in defining how gold behaves within DeFi. This isn't just mirroring TradFi exposure, but extending it.

If this direction holds, the implication is clear:

Gold doesn’t just remain a SoV, it becomes a productive unit of capital within a programmable financial system.

And whichever protocols successfully bridge that gap will likely set the precedent for this entire vertical moving forward.

May 22

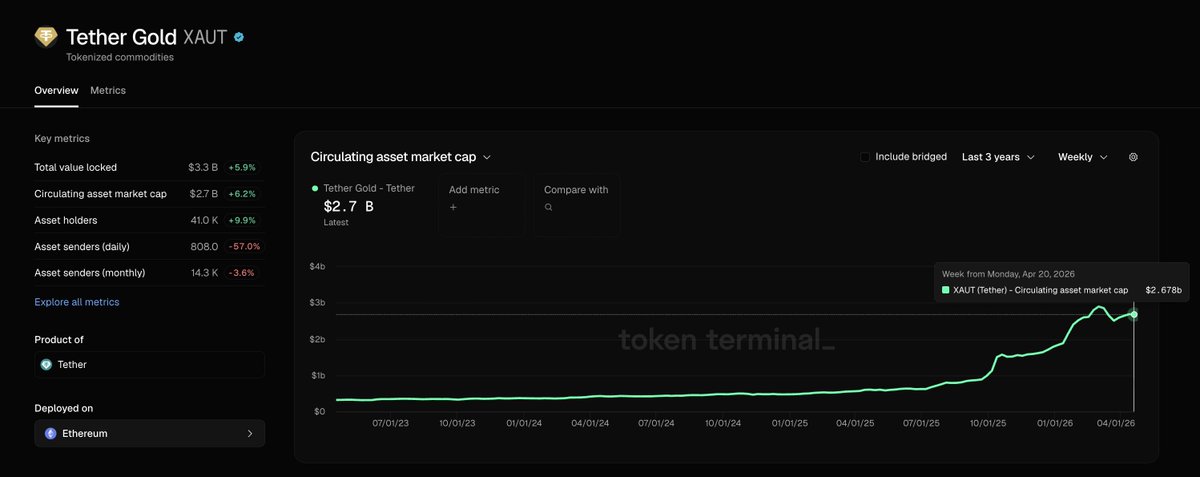

The tokenized commodity market is almost entirely gold.

Gold is an obvious fit for tokenization: It’s global, standard, and already tracked through paper claims

Plus, crypto investors already get it. Bitcoin was called “digital gold” long before tokenized gold took off.

XAUt and PAXG translate a familiar ownership model to blockchains, turning claims on gold held in vaults into onchain tokens held in wallets.

Everything else (tokenized oil, crops, energy, compute, etc.) is much earlier and has a smaller market share.

36

14

71

4,158

62% of Americans hold equities through direct ownership, mutual funds, or retirement accounts. Outside the US, that number drops below 20%.

The largest and most liquid equity market in the world remains structurally inaccessible to most of the global population.

It is a distribution and infrastructure problem. And it is the exact gap @OndoFinance has spent the last two years building rails to close.

The RWA tokenization sector has scaled to $31.2B in circulating asset market cap. As per @tokenterminal , Ondo Finance holds $3.7B of that, commanding 11.8% market share across all RWA issuers.

But that number understates Ondo's real dominance. In tokenized equities specifically, Ondo controls over 70% of the market.

To understand why, you need to understand Ondo's product architecture. This is not a single-product protocol. It is a layered financial infrastructure stack with three distinct verticals, each targeting a different capital pool with different compliance requirements.

1⃣OUSG provides institutional-grade tokenized US Treasury exposure for accredited investors. It is permissioned, KYC-gated, and SEC Reg D compliant.

2⃣USDY is a yield-bearing dollar token backed by short-term Treasuries and bank deposits. Unlike OUSG, USDY trades freely after initial settlement, making it composable across DeFi lending markets, collateral pools, and cross-chain settlements.

3⃣Ondo Global Markets is the tokenized equities arm: 200 US stocks and ETFs live across Ethereum, BNB Chain, and Solana. TVL crossed $1.5B by May 2026, doubling since January.

OUSG captures institutional treasury management. USDY captures non-US retail and DeFi-native yield seekers. Ondo Global Markets captures the 4.5 billion people globally who want equity exposure but lack brokerage access. Three products, three capital pools, one protocol.

Now the newest layer: @OndoPerps .Goes live today, June 9.

Non-US users can trade perpetual futures on tokenized US stocks and ETFs with up to 20x leverage. NVIDIA, Apple, Microsoft, Tesla, Amazon, Meta, Google, Intel, AMD, plus gold and silver. 24/7 access, onchain settlement, and tokenized securities accepted as margin.

The capital efficiency argument is where @OndoPerps separates from existing platforms. Today, running a delta-neutral hedge on NVDA requires two separate accounts: an offchain broker like Interactive Brokers for the spot long, and a perps platform like Hyperliquid for the short. Capital is fragmented across two venues with two different settlement systems.

On Ondo Perps, you buy NVDAon through Ondo Global Markets, use that tokenized equity as collateral on Ondo Perps, and open the short in the same ecosystem. Unified capital. 2x capital efficiency.

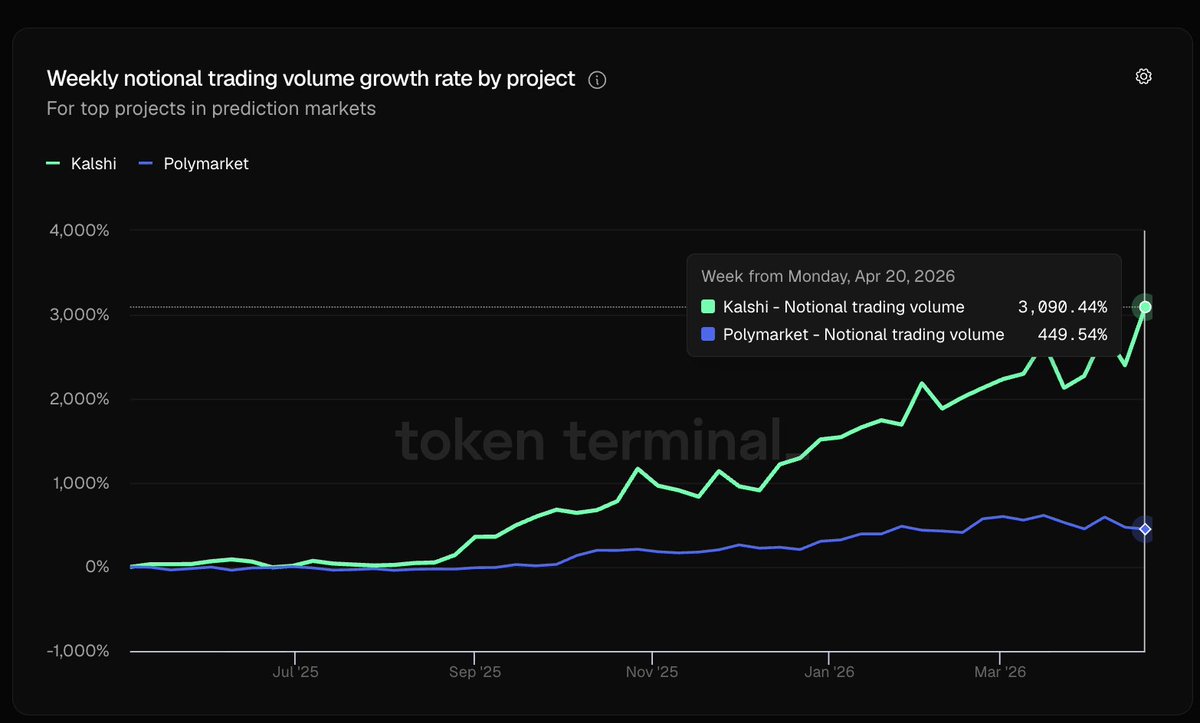

The CFTC recently approved Kalshi's BTCPERP, the first perpetual futures contract on a regulated US exchange. Different scope from Ondo Perps, which targets non-US equity perps, but the regulatory signal is directional: perpetual contracts on real-world assets are gaining institutional legitimacy.

As per @BinanceResearch 's "Equity Layer: From Tokens to Tickers" report published June 4, crypto exchanges could channel $2T in incremental capital into global equities by 2031 in the base case. Bull case: $5T annually within five years.

93% of Binance's initial stock trading users already come from emerging markets, where geographic constraints and limited brokerage access have historically restricted equity participation. The demand side is real. The infrastructure side is what Ondo is building.

Beyond products, Ondo is constructing its own settlement layer. Ondo Chain, an L1 blockchain purpose-built for institutional-grade RWA, is targeting mainnet launch in 2026.

The design uses permissioned validators from financial institutions, tokenized asset staking instead of native token staking, proof-of-reserve for real-time backing verification, and native cross-chain bridging. Design advisors include BlackRock, Franklin Templeton, Wellington Management, WisdomTree, Morgan Stanley, Google Cloud, and McKinsey. When you have that roster advising your L1 architecture, the institutional intent is clear.

As per @tokenterminal , Ondo's token holder base has grown steadily to 195.4K, while TVL has scaled from near zero in mid-2023 to $3.7B today. The growth curve shows clear step-function increases, particularly around product launches and institutional onboarding events.

Bunt's POV

Ondo's product surface area is now wider than any other RWA protocol: tokenized Treasuries, tokenized equities, yield-bearing stablecoins, perpetual futures, and a dedicated L1 in development. The institutional backing from BlackRock, Franklin Templeton, State Street, and J.P. Morgan is unmatched in the sector.

That said, risks remain visible. The token sits around $0.35, well below its December 2024 highs, partly due to the 1.94B token unlock in January 2026 that added significant supply pressure.

Ondo Chain mainnet has been "early-to-mid 2026" for months without a confirmed date. Ondo Perps launching for non-US users only limits initial addressable market. And competition is intensifying: Binance just listed 7,000 US stocks and ETFs directly on its exchange on June 1, and BlackRock's BUIDL continues to scale on the institutional side.

The thesis is straightforward. Ondo is positioning itself as the full-stack financial infrastructure layer for onchain capital markets: issuance, yield, trading, derivatives, and settlement. Whether execution matches ambition at this scale is what the next 12 months will answer.

18

10

22

1,516

BUNT retweeted

Jun 9

$HYPE is accepted collateral at Maple.

Institutions holding it can borrow against their position on tailored, overcollateralized terms, structured and managed by the Maple credit team.

No selling required.

maple.finance/#borrow

21

27

186

10,158

62% of Americans hold equities through direct ownership, mutual funds, or retirement accounts. Outside the US, that number drops below 20%.

The largest and most liquid equity market in the world remains structurally inaccessible to most of the global population.

It is a distribution and infrastructure problem. And it is the exact gap @OndoFinance has spent the last two years building rails to close.

The RWA tokenization sector has scaled to $31.2B in circulating asset market cap. As per @tokenterminal , Ondo Finance holds $3.7B of that, commanding 11.8% market share across all RWA issuers.

But that number understates Ondo's real dominance. In tokenized equities specifically, Ondo controls over 70% of the market.

To understand why, you need to understand Ondo's product architecture. This is not a single-product protocol. It is a layered financial infrastructure stack with three distinct verticals, each targeting a different capital pool with different compliance requirements.

1⃣OUSG provides institutional-grade tokenized US Treasury exposure for accredited investors. It is permissioned, KYC-gated, and SEC Reg D compliant.

2⃣USDY is a yield-bearing dollar token backed by short-term Treasuries and bank deposits. Unlike OUSG, USDY trades freely after initial settlement, making it composable across DeFi lending markets, collateral pools, and cross-chain settlements.

3⃣Ondo Global Markets is the tokenized equities arm: 200 US stocks and ETFs live across Ethereum, BNB Chain, and Solana. TVL crossed $1.5B by May 2026, doubling since January.

OUSG captures institutional treasury management. USDY captures non-US retail and DeFi-native yield seekers. Ondo Global Markets captures the 4.5 billion people globally who want equity exposure but lack brokerage access. Three products, three capital pools, one protocol.

Now the newest layer: @OndoPerps .Goes live today, June 9.

Non-US users can trade perpetual futures on tokenized US stocks and ETFs with up to 20x leverage. NVIDIA, Apple, Microsoft, Tesla, Amazon, Meta, Google, Intel, AMD, plus gold and silver. 24/7 access, onchain settlement, and tokenized securities accepted as margin.

The capital efficiency argument is where @OndoPerps separates from existing platforms. Today, running a delta-neutral hedge on NVDA requires two separate accounts: an offchain broker like Interactive Brokers for the spot long, and a perps platform like Hyperliquid for the short. Capital is fragmented across two venues with two different settlement systems.

On Ondo Perps, you buy NVDAon through Ondo Global Markets, use that tokenized equity as collateral on Ondo Perps, and open the short in the same ecosystem. Unified capital. 2x capital efficiency.

The CFTC recently approved Kalshi's BTCPERP, the first perpetual futures contract on a regulated US exchange. Different scope from Ondo Perps, which targets non-US equity perps, but the regulatory signal is directional: perpetual contracts on real-world assets are gaining institutional legitimacy.

As per @BinanceResearch 's "Equity Layer: From Tokens to Tickers" report published June 4, crypto exchanges could channel $2T in incremental capital into global equities by 2031 in the base case. Bull case: $5T annually within five years.

93% of Binance's initial stock trading users already come from emerging markets, where geographic constraints and limited brokerage access have historically restricted equity participation. The demand side is real. The infrastructure side is what Ondo is building.

Beyond products, Ondo is constructing its own settlement layer. Ondo Chain, an L1 blockchain purpose-built for institutional-grade RWA, is targeting mainnet launch in 2026.

The design uses permissioned validators from financial institutions, tokenized asset staking instead of native token staking, proof-of-reserve for real-time backing verification, and native cross-chain bridging. Design advisors include BlackRock, Franklin Templeton, Wellington Management, WisdomTree, Morgan Stanley, Google Cloud, and McKinsey. When you have that roster advising your L1 architecture, the institutional intent is clear.

As per @tokenterminal , Ondo's token holder base has grown steadily to 195.4K, while TVL has scaled from near zero in mid-2023 to $3.7B today. The growth curve shows clear step-function increases, particularly around product launches and institutional onboarding events.

Bunt's POV

Ondo's product surface area is now wider than any other RWA protocol: tokenized Treasuries, tokenized equities, yield-bearing stablecoins, perpetual futures, and a dedicated L1 in development. The institutional backing from BlackRock, Franklin Templeton, State Street, and J.P. Morgan is unmatched in the sector.

That said, risks remain visible. The token sits around $0.35, well below its December 2024 highs, partly due to the 1.94B token unlock in January 2026 that added significant supply pressure.

Ondo Chain mainnet has been "early-to-mid 2026" for months without a confirmed date. Ondo Perps launching for non-US users only limits initial addressable market. And competition is intensifying: Binance just listed 7,000 US stocks and ETFs directly on its exchange on June 1, and BlackRock's BUIDL continues to scale on the institutional side.

The thesis is straightforward. Ondo is positioning itself as the full-stack financial infrastructure layer for onchain capital markets: issuance, yield, trading, derivatives, and settlement. Whether execution matches ambition at this scale is what the next 12 months will answer.

18

10

22

1,516

Hope y’all liked it

@thelearningpill

@Eli5defi

@YashasEdu

@satyaki44

@kenodnb

@0xCheeezzyyyy

@tradeguru

@RubiksWeb3

@SachinHMx

@TheDeFiKenshin

@Tom_Degen68

@_thespacebyte

@Kruys_Collins

62% of Americans hold equities through direct ownership, mutual funds, or retirement accounts. Outside the US, that number drops below 20%.

The largest and most liquid equity market in the world remains structurally inaccessible to most of the global population.

It is a distribution and infrastructure problem. And it is the exact gap @OndoFinance has spent the last two years building rails to close.

The RWA tokenization sector has scaled to $31.2B in circulating asset market cap. As per @tokenterminal , Ondo Finance holds $3.7B of that, commanding 11.8% market share across all RWA issuers.

But that number understates Ondo's real dominance. In tokenized equities specifically, Ondo controls over 70% of the market.

To understand why, you need to understand Ondo's product architecture. This is not a single-product protocol. It is a layered financial infrastructure stack with three distinct verticals, each targeting a different capital pool with different compliance requirements.

1⃣OUSG provides institutional-grade tokenized US Treasury exposure for accredited investors. It is permissioned, KYC-gated, and SEC Reg D compliant.

2⃣USDY is a yield-bearing dollar token backed by short-term Treasuries and bank deposits. Unlike OUSG, USDY trades freely after initial settlement, making it composable across DeFi lending markets, collateral pools, and cross-chain settlements.

3⃣Ondo Global Markets is the tokenized equities arm: 200 US stocks and ETFs live across Ethereum, BNB Chain, and Solana. TVL crossed $1.5B by May 2026, doubling since January.

OUSG captures institutional treasury management. USDY captures non-US retail and DeFi-native yield seekers. Ondo Global Markets captures the 4.5 billion people globally who want equity exposure but lack brokerage access. Three products, three capital pools, one protocol.

Now the newest layer: @OndoPerps .Goes live today, June 9.

Non-US users can trade perpetual futures on tokenized US stocks and ETFs with up to 20x leverage. NVIDIA, Apple, Microsoft, Tesla, Amazon, Meta, Google, Intel, AMD, plus gold and silver. 24/7 access, onchain settlement, and tokenized securities accepted as margin.

The capital efficiency argument is where @OndoPerps separates from existing platforms. Today, running a delta-neutral hedge on NVDA requires two separate accounts: an offchain broker like Interactive Brokers for the spot long, and a perps platform like Hyperliquid for the short. Capital is fragmented across two venues with two different settlement systems.

On Ondo Perps, you buy NVDAon through Ondo Global Markets, use that tokenized equity as collateral on Ondo Perps, and open the short in the same ecosystem. Unified capital. 2x capital efficiency.

The CFTC recently approved Kalshi's BTCPERP, the first perpetual futures contract on a regulated US exchange. Different scope from Ondo Perps, which targets non-US equity perps, but the regulatory signal is directional: perpetual contracts on real-world assets are gaining institutional legitimacy.

As per @BinanceResearch 's "Equity Layer: From Tokens to Tickers" report published June 4, crypto exchanges could channel $2T in incremental capital into global equities by 2031 in the base case. Bull case: $5T annually within five years.

93% of Binance's initial stock trading users already come from emerging markets, where geographic constraints and limited brokerage access have historically restricted equity participation. The demand side is real. The infrastructure side is what Ondo is building.

Beyond products, Ondo is constructing its own settlement layer. Ondo Chain, an L1 blockchain purpose-built for institutional-grade RWA, is targeting mainnet launch in 2026.

The design uses permissioned validators from financial institutions, tokenized asset staking instead of native token staking, proof-of-reserve for real-time backing verification, and native cross-chain bridging. Design advisors include BlackRock, Franklin Templeton, Wellington Management, WisdomTree, Morgan Stanley, Google Cloud, and McKinsey. When you have that roster advising your L1 architecture, the institutional intent is clear.

As per @tokenterminal , Ondo's token holder base has grown steadily to 195.4K, while TVL has scaled from near zero in mid-2023 to $3.7B today. The growth curve shows clear step-function increases, particularly around product launches and institutional onboarding events.

Bunt's POV

Ondo's product surface area is now wider than any other RWA protocol: tokenized Treasuries, tokenized equities, yield-bearing stablecoins, perpetual futures, and a dedicated L1 in development. The institutional backing from BlackRock, Franklin Templeton, State Street, and J.P. Morgan is unmatched in the sector.

That said, risks remain visible. The token sits around $0.35, well below its December 2024 highs, partly due to the 1.94B token unlock in January 2026 that added significant supply pressure.

Ondo Chain mainnet has been "early-to-mid 2026" for months without a confirmed date. Ondo Perps launching for non-US users only limits initial addressable market. And competition is intensifying: Binance just listed 7,000 US stocks and ETFs directly on its exchange on June 1, and BlackRock's BUIDL continues to scale on the institutional side.

The thesis is straightforward. Ondo is positioning itself as the full-stack financial infrastructure layer for onchain capital markets: issuance, yield, trading, derivatives, and settlement. Whether execution matches ambition at this scale is what the next 12 months will answer.

4

129

BUNT retweeted

Jun 8

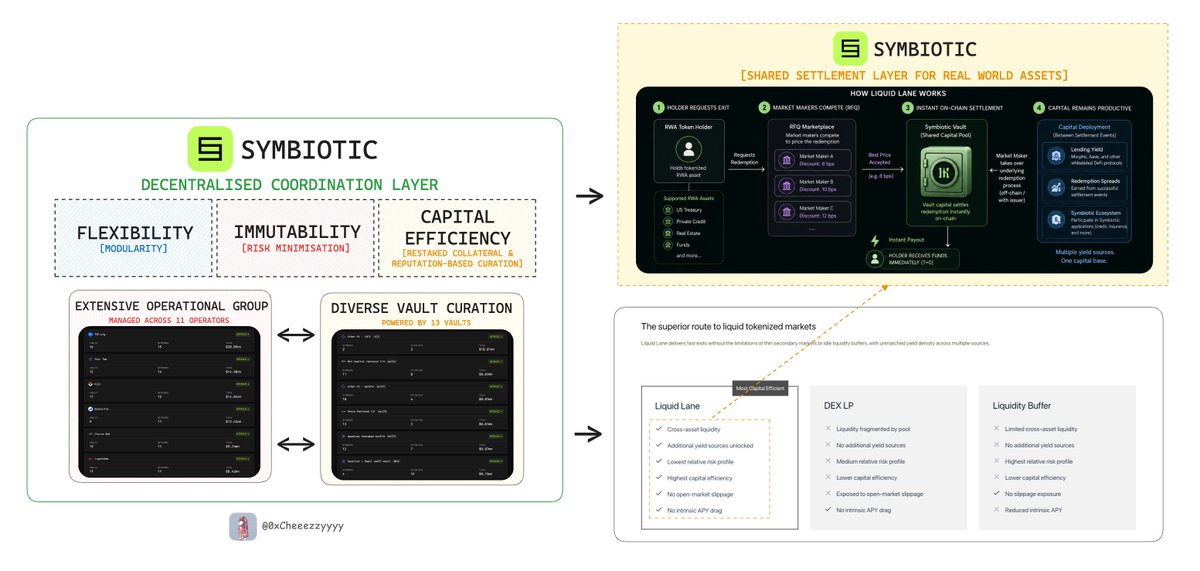

What happens when tokenised assets can be issued on-chain, but still cannot move efficiently?

Most people think tokenisation's biggest challenge is issuance.

It's not, it's liquidity.

RWA-Fi has grown to ~$34B and continues expanding rapidly, yet many tokenised assets still operate with redemption windows ranging from T 1 to 180 days.

This creates a structural problem.

An asset without a reliable exit is harder to hold, harder to lend against, and harder to integrate into broader DeFi markets.

And the market naturally prices this in as investors demand a liquidity premium, protocols become hesitant to accept RWAs as collateral which causes capital efficiency to suffer.

This is precisely why only a small fraction of tokenised RWAs are actively utilised throughout DeFi today.

The bottleneck is no longer asset issuance, but settlement infrastructure.

This is where @symbioticfi Liquid Lane's design becomes interesting. Rather than forcing every issuer to maintain dedicated liquidity buffers or rely on fragmented OTC markets, Liquid Lane introduces a shared settlement layer powered by Symbiotic vaults.

The mechanism is conceptually simple:

1️⃣ A holder wants to exit a tokenised asset.

2️⃣ Market makers compete through an RFQ process to price the redemption discount.

3️⃣ Once accepted, vault capital settles the redemption instantly on-chain while the market maker assumes the underlying redemption process.

4️⃣ Between settlement events, vault capital remains productive through lending venues such as @Morpho @aave , while simultaneously earning redemption spreads and participating across the broader Symbiotic ecosystem.

In effect: Future liquidity gets pulled forward into the present.

This effectively creates a new market for settlement itself.

🔸 Investors receive instant exits

🔸 Issuers gain broader distribution and deeper liquidity

🔸 Market makers capture settlement spreads

🔸 LPs earn from multiple yield sources simultaneously

And that's the bigger unlock.

Tokenisation solved ownership years ago, and the next frontier is mobility.

Because the future of RWA-Fi won't be determined by how many assets come on-chain, it will be determined by how efficiently those assets can move once they're there.

And sooner or later, instant liquidity won't be a competitive advantage.

It'll simply be the industry standard 🫡

42

14

67

3,566