Predicting 1–2 mo stock moves via macro, float, catalysts & sentiment. Data → conviction trades. My posts are based on personal experience, Not financial advice

Joined September 2022

- Tweets 494

- Following 103

- Followers 36

- Likes 230

11 Photos and videos

Uncle Scrooge retweeted

Jun 8

Heard until end.

* An official Committee approved Jain request but this man still has problems.

* He was personally not consulted. So yeh gussa hain!

* Compared the White Line with animal sacrifice.

* Grinning & Laughing in between the interview but reporter remained serious.

Jun 8

Mumbai: A broad white line drawn from the road to the footsteps of a wing in a housing society has disturbed the peace that had existed for over two decades in Ghatkopar area. To find out what really is the issue, @journovidya spoke to residents of Kailas Avenue

#ReporterDiary

116

87

443

68,752

Uncle Scrooge retweeted

Jun 6

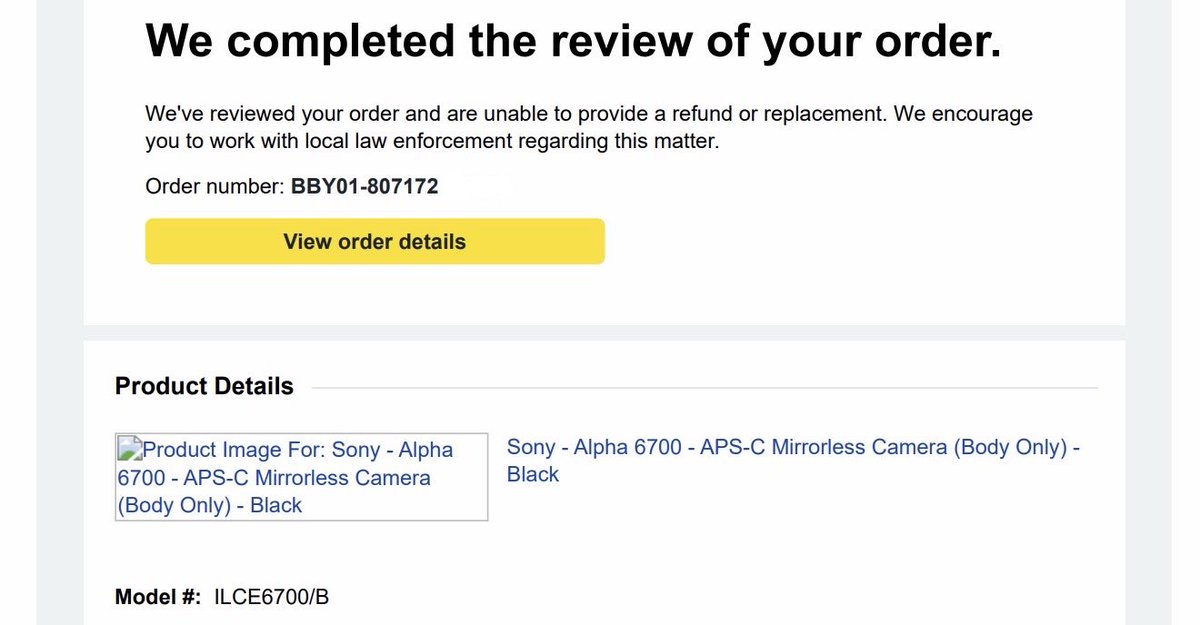

Bought a $1,742.80 camera online from BestBuy.

The FedEx delivery driver stole it. FedEx admitted it.

But BestBuy won’t give a refund. They said we need to “work with local law enforcement.”

Thought everyone should know if you buy from @BestBuy and a @FedEx driver steals what you paid for, your money is gone. Neither company will make it right.

I’ve spent over $30K at BestBuy and will never spend another penny there.

7,888

16,220

91,355

6,736,842

10 Nov 2025

GOOGL – Short-Term Outlook (4-8 wks)

“AI acceleration vs execution/macro drag — which side wins?”

Macro & Market Context

•Growth tech generally remains under pressure in a higher-rate, slower global growth environment. That means even top-tier names like GOOGL carry macro risk.

•At the same time, the broader AI & cloud theme remains strong — GOOGL is squarely positioned there. For example, cloud growth AI‐infrastructure tailwinds remain key.

•Market sentiment around tech growth is mixed: some rotation into value, some into “AI winners” — GOOGL could benefit if the latter dominates, but is vulnerable if risk-off sets in.

Company / Fundamental Lens

•Short interest is very low: ~0.5-1 % of float, days to cover ~1.7-2.2. This means limited short-squeeze potential — upside surprise isn’t likely to get a kicker from cover dynamics.

•Key upcoming catalysts:

•Further monetization of AI (e.g., its Gemini model, cloud AI services)

•Growth in cloud backlog (~$106 bn) and margin expansion in Google Cloud.

•Consumer device/AI integration (e.g., Pixel 10 launch embedding AI)

•Risk factors: margin pressure (capex is high, cloud is still investing hard) ; competition in AI & ads; macro slowdown hurting ad spend.

Technical / Sentiment Checklist

•With strong thematic support (AI/cloud) the stock has some structural tailwinds, but the short-term risk/reward is more balanced because much of the positive story may already be priced in.

•Because short interest is low, upside “pop” from a short squeeze is unlikely; downside risk could be more pronounced if catalysts disappoint or macro weakens.

•On the chart: if GOOGL breaks beneath key support levels (e.g., recent lows or 50-day SMA), that would signal a tactical shift to caution. Conversely, a clean breakout through resistance could open more upside.

Catalyst Behaviour & Historical Parallel

•Historically when GOOGL has delivered strong cloud/AI beats, the market tends to reward it moderately, but not in speculative fashion (given size and low float leverage).

•In previous periods of macro softness or high expectations, a “good but not great” result often led to consolidation rather than a strong breakout.

•With key AI/cloud catalysts already known, there is a risk of “sell the news” if execution or guidance falls short.

Short-Term Trade Outlook

•Base case: Range trade or modest upside — ~ 4% to -3% over next 4-8 weeks.

•Bull case: 7% to 10% if a clear surprise emerges on cloud margins or AI monetization.

•Bear case: -8% to -12% if macro weakens further (ad spend drops), or cloud margin/guidance disappoints.

•My lean: Slightly cautious neutral to modestly bullish, but on guard. The upside exists, but risk is more pronounced given low short float and high expectations.

81

10 Nov 2025

$AMZN – Short-Term (≈ 4-8 weeks) Outlook

“Built-to-scale vs growth deceleration — which wins?”

Macro & Market Context

•With global growth softness and consumer spending decelerating, retail/commerce names face a tougher backdrop. Amazon’s scale gives it resilience, but earnings expectations remain under pressure in a high-rate regime.

•The broader tech market is driven by AI-capex, cloud growth, and platform monetisation; Amazon straddles retail cloud, so it’s exposed both to upsides (AWS, Ads) and structural retail headwinds.

•Sentiment is relatively benign — the low short interest suggests fewer “upside surprises” via short-squeeze mechanics.

Company / Fundamental Lens

•AMZN’s short interest is just ~0.78% of float, with ~1.7 days to cover. That means limited fuel for a sharp squeeze.

•Key upcoming catalysts: holiday shopping season results (Q4), AWS margin expansion/AI infrastructure growth, international commerce recovery.

•But risks: margin compression in retail, FX/headwinds abroad, slower growth in ads. The market may be factoring in much of the “growth story” already.

•Historically when Amazon has delivered strong AWS/ads beats, the stock has out-performed; when it has been disappointing on margins or international growth, the reaction has been muted or negative.

Technical & Sentiment Checklist

•Technically, the stock appears extended from recent moves; potential for consolidation.

•Because short‐interest is low, a surprise upside may not be as amplified; downside may be stronger if catalyst disappoints.

•Watch for breaches of key support levels (e.g., 50-day / 200-day MA) as potential triggers for tactical pullbacks.

Catalyst Behaviour & Historical Parallel

•In past “holiday season AWS growth beat” scenarios, Amazon has rallied into the results and sometimes pulled back post-event on profit-taking.

•Given today’s elevated expectations, the risk of “good but not great” results leading to “sell the news” is higher.

•Example: When prior quarters saw strong AWS growth retail beat, the stock rallied ~10-15% ahead, then flatlined. In contrast when growth slowed, it fell ~8-12% short term.

Short-Term Trade Outlook

•Base case: Range bound, maybe 3% to -5% over next 4-8 weeks.

•Bull case: 7% to 10% if AWS/ads beat meaningfully and holiday ramp strong.

•Bear case: -8% to -12% if margin/macro disappoint or weak guidance emerges.

•My lean: modestly cautious – with upside possible but risk-reward tilting slightly to the downside given elevated expectations and low short interest.

101

10 Nov 2025

$TSLA – Short-Term Outlook (≈ 4-8 weeks)

“Fade the hype or position ahead of delivery?”

Macro & Market Context

•With interest rates still elevated and global growth softening, capital‐intensive growth stocks like Tesla are under pressure; research shows macro indicators carry meaningful weight in TSLA’s volatility.

•The EV market is increasingly competitive, especially in Europe and China, which is a headwind for Tesla’s growth narrative.

•Sentiment is fragile: given the stretched valuation and lofty expectations, any incremental miss or guidance cut could trigger outsized downside.

Company / Fundamental Lens

•Short interest is modest: ~2.7 % of float, days to cover ~0.8. That means fewer forced short squeezes, so upside from a short‐squeeze event is limited in the near term.

•Upcoming catalysts: the roll-out of the robotaxi service in Austin, and updates on the lower‐cost EV strategy. However, past similar «big ideas» (e.g., new model launches) have often been already priced in.

•Execution risks are high: declining market share in Europe, pricing pressure and margin erosion are real issues.

Technical / Market Sentiment

•TSLA recently hit a 2025 high (up ~70% year-to-date) which suggests much of the good news is in the price.

•Given the elevated valuation and sentiment, the risk-reward in the short term leans to the downside unless a fresh positive catalyst fires.

•Watch for support zones: if price breaks below key moving averages (say 50-day or 200-day) that would signal a tactical downgrade.

Catalyst Behaviour & Historical Parallel

•Historically when Tesla has previewed major new business units (e.g., robo-taxi), the stock rallied ahead of the announcement, but then entered consolidation unless execution visible.

•In the current environment, with expectations high, the risk is that a “good but not great” catalyst triggers a “sell the news” reaction.

My Short-Term Trade Outlook

•Base case: TSLA trades in a range, maybe ~ -5% to 5% over next 4-8 weeks.

•Bull case: 8-10% if the robotaxi launch or lower-cost model announcement delivers above expectations.

•Bear case: -10% to -15% if guidance is light, macro data weakens further, or margin pressure intensifies.

•Given the modest short float and high expectation set, the lean here is slightly bearish: fading into strength and being cautious ahead of key announcements.

134

9 Nov 2025

🧬 Pfizer snapshot

🎯 Earnings update: PFE delivered adjusted EPS of $0.87 for Q3 2025, beating estimates, while revenue declined approx. 7% operationally (mainly on lower COVID-product demand).

🔼 Bull thesis:

•Non-COVID portfolio growing: e.g., key drugs such as the Vyndaqel family and Nurtec showed solid growth.

•Cost-efficiency & margin improvement: management emphasised manufacturing optimisation and cost savings through 2027.

•Undervalued by some analysts: e.g., price-target upgrades to ~$33 seen despite challenging backdrop.

⚠️ Bear thesis:

•Declining tailwind from COVID products: revenues from treatments like Paxlovid are fading, leaving Pfizer to rely more on non-COVID growth.

•Patent expirations & pricing/policy risk: high exposure to regulatory/pricing pressures in pharma market, which may constrain upside.

•Revenue growth remains uneven: while EPS beat, the revenue decline raises questions about top-line momentum.

🔮 2-year view (2026-2027):

•If Pfizer executes on its cost-savings plan and its non-COVID growth accelerates (say 5-8% annually), EPS could rise modestly (e.g., mid-$3s) and valuation could re-rate.

•Conversely, if growth remains sluggish and policy/pricing headwinds bite, the stock may largely move sideways with dividend representing the key return.

📌 Bottom line: PFE is a strategic play on transition from pandemic-era revenue to a more sustainable product mix — the upside hinges on execution, the downside on external risks. #Pfizer $PFE #pharma #Earnings

261

9 Nov 2025

Next week’s U.S. equity market snapshot — key themes to watch:

1️⃣ Volatility remains elevated. The S&P 500 breadth is weakening and the Russell 2000 has failed to regain its prior highs — warning signs of near-term fragility.

2️⃣ Fundamental bones remain solid. About 82% of S&P 500 firms beat earnings expectations, with tech earnings still outperforming.

3️⃣ Key catalysts ahead: the Federal Reserve policy meeting, major tech reports, and geopolitical/trade headlines. These could trigger meaningful swings.

4️⃣ Outlook: With high expectations baked in, the market may struggle to gain momentum unless all go-signals align. Best case: range-bound to modest upside. Tail risk: pullback if any catalyst disappoints.

5️⃣ Tactical takeaway: For the week ahead think “selectively bullish but cautiously positioned” — focus on high-quality names, manage exposure, and expect sharper swings than normal.

#Stocks #Markets #investing #WallStreet

46

6 Nov 2025

$ONC (BeOne Medicines) — post-earnings setup worth watching:

• Q3 EPS $2.65 vs $0.80 est → massive beat

• Rev 📈 $1.41 B ( 41% YoY)

• Brukinsa BTKi sales up ~51% to $1.0 B, now clear global class leader

Tech setup:

• Support: $316-$322 (demand zone / 20-DMA)

• Breakout trigger: > $355 (52-wk high)

• Next resistance: $382 then $425

• Stop-loss: < $305 (close below 50-DMA)

🚀 Bias: Bullish continuation if BTKi momentum sustains — guided FY rev $5.1-5.3 B adds conviction.

📅Near-term catalysts: China label expansions new BTKi combo data (ASH ’25).

#stocks #biotech #ONC #BTKi #technicalanalysis

Why BTKi dominance matters:

ONC’s Brukinsa isn’t just another cancer drug — it’s now outselling Imbruvica globally, seizing >50% BTKi market share.

That means recurring, high-margin revenue validation of ONC’s R&D engine. Every new BTKi combo = optionality for $ONC’s next S-curve.

BTKi = cash flow moat → fuels pipeline runway.

151

5 Nov 2025

The AI → Quantum rally made trillion-$ winners.

But markets always rotate.

The next mega wave is forming — maybe in bio-AI, energy storage, or real-world robotics.

What sector do you think leads 2026?

Comment your top ticker.

#AI #Quantum #NextBigThing

1

72

5 Nov 2025

Boom or bubble? PLTR just crushed earnings & raised its full-year target… yet shares dropped ≈ 9%. Why? Because after a ~150% YTD run, Wall Street says the valuation is “extreme.” #AI #tech

Choose your side: • Believer – “best-in-class AI enabler” per BofA • Skeptic Jefferies says target $70

TL;DR: Major moment for PLTR either the launchpad or the top of the launch. #stocks #investing

56

5 Nov 2025

Bubble watch : When the heads of Goldman Sachs & Morgan Stanley are flashing “10-20% correction” warning signs and Michael Burry is shorting the AI giants, it’s not hype—it’s a red flag.

Tech rally = cooling. Time to ask: what’s next?

#stocks #AI #bubblealert

116

30 Oct 2025

1️⃣ PayPal ChatGPT = first real bridge between AI assistants and e-commerce.

2️⃣ Think of ChatGPT as the next-gen shopping mall, and $PYPL as its cash register.

3️⃣ Rollout 2026 → incremental $30B TPV by 2028 = EPS $1-2.

4️⃣ If Wall St re-rates PayPal at 20× P/E → $140 target.

5️⃣ The era of agentic commerce just started.

90

30 Oct 2025

$AMZN ahead of Q3 2025 earnings: Street looks for ~US$174-180B revenue & US$1.57 EPS. Key themes: strong AWS growth, ad momentum, but margin/guidance risk looms. A beat positive guide = 5%- 6% move; weak forward snip could cost

My prediction for tomorrow’s release

I expect Amazon to beat or meet consensus on revenue (~US$175-179b) and EPS (~US$1.55-1.65) given the positive lead indicators. However, the stock reaction will depend heavily on forward guidance and AWS margin commentary.

So they, likely issue cautious guidance / margin remains weak → possible muted or even negative reaction despite the beat.

Not financial advice

123

30 Oct 2025

“GOOGL smashes into six-figure quarter: Q3 revenue hits ~$102.3B ( 16 % YoY), cloud leaps to ~$15.2B, ad/search momentum still solid. CapEx raised to ~$91-93B for 2025 to fuel AI infrastructure. $GOOGL

Key assumptions:

•Top-line growth ~15-20% YoY in near term as cloud, search & YouTube all deliver double-digit expansions.

•Heavy capital expenditures (~US$90B ) in 2025 to build AI/Cloud infrastructure.

•Margin and earnings improvement expected once scale of AI infrastructure begins to pay off.

•Valuation multiple may expand if growth is sustained and risks (competition, regulation) are managed.

Stylised Price-Target Forecast:

•End 2026: ~$340-380

•End 2027: ~$400-460

•End 2028: ~$500-580

Upside scenario (strong AI monetisation, regulatory tailwinds): end-2028 could reach ~$650

Downside scenario (cost burden persists, ad/search slows, regulatory drag): end-2028 might stay around ~$300-350

70

30 Oct 2025

Microsoft posts Q4 FY25 revenue up 18% to ~$76.4 B, EPS up 24% to $3.65, with Azure growing ~39% and annual Azure revenue now >$75 B. Heavy cap-ex (over $30 B next quarter) as it doubles down on cloud AI. $MSFT

Key assumptions:

•Double‐digit revenue growth in the cloud/AI segments (~15-20% overall) assuming MSFT executes well.

•Heavy capital investment now will pay off via higher margins and platform leverage in years ahead.

•Valuation multiple stays elevated (say 25-30× EPS) if growth remains strong; could compress if margin pressure or spending drags.

•No major disappointments in cloud/AI or gaming that derail the narrative.

Stylised Price‐Target Forecast:

•End 2026: ~$650-700

•End 2027: ~$750-850

•End 2028: ~$900-1,000

Upside scenario (strong AI monetisation, margin expansion): end-2028 could hit $1,100

Downside scenario (cap-ex drags, cloud growth slows): end-2028 might be ~$650-700

171

30 Oct 2025

Meta delivered strong top-line: Q3 revenue rose ~26% to ~$51.2B, but an ~$16B one-time tax hit cut EPS to ~$1.05 (vs ~$7.25 adj) while AI-capex guidance was raised to ~$70-72B. Growth remains real, but cost & return timing questions linger. $META

Key assumptions:

•Revenue and ad growth remain strong (~20-30% YoY) driven by AI-enhanced ad tools and global expansion.

•Heavy capex and elevated expense base (2025 capex raised to $70-72B).

•Investors will focus increasingly on margin recovery, ROIC (return on invested capital), and monetisation payoff from AI investments.

•Valuation multiple may compress somewhat if spending outweighs near-term return, or expand if earnings acceleration is clear.

Stylised Price-Target Forecast:

•End 2026: ~US$880-950

•End 2027: ~US$1,000-$1,100

•End 2028: ~US$1,150-$1,300

Upside scenario (strong earnings beat, AI pay-off early): end-2028 could reach ~$1,400

Downside scenario (cost burden persists, return delayed): end-2028 might stay ~$800-900

Not financial advice

109

29 Oct 2025

Solid beat from UnitedHealth: Q3 revenue 12% to $113.2 B, adjusted EPS $2.92▴, full-year guidance raised to at least $16.25/share. CEO Hemsley eyes 2026 as stepping-off point for margin improvement and growth revival. $UNH #HealthCare

Projection assumptions:

•FY 2025 adjusted EPS guidance of at least $16.25/share (raised today).

•Revenue growth ~10-12% in 2025, albeit margin pressures due to elevated medical cost trends.

•Margin turnaround and stronger growth expected from 2026 onward.

•Price-to-earnings (P/E) multiple normalizing toward peers (e.g., ~18-22×) as business stabilizes.

•Market sentiment remains cautious given regulatory/medical cost headwinds.

Stylised Price-Target Forecast:

•End-2026: ~US$440–480

•End-2027: ~US$500–550

•End-2028: ~US$560–650

Upside scenario (margin recovery faster, growth stronger): End-2028 could reach ~$700 .

Downside scenario (cost pressures persist, growth sluggish): End-2028 might remain ~$450-500.

Not a financial advice.

178

29 Oct 2025

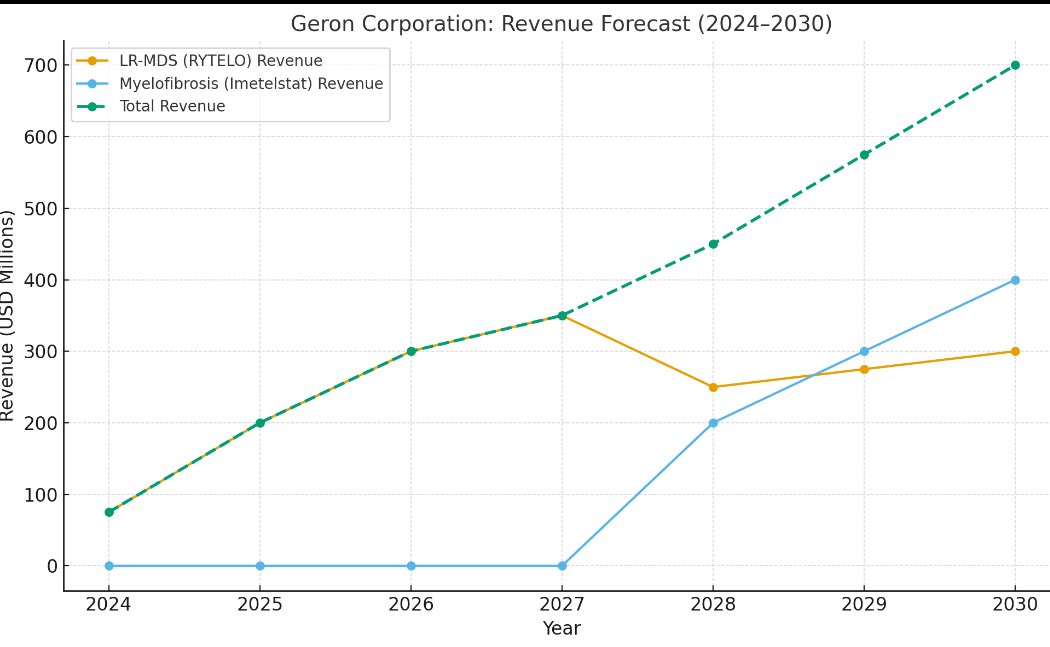

Geron’s approval of RYTELO opens the door but is it the real driver? If imetelstat succeeds in MF (myelofibrosis) and captures ~US$600M global sales by ~2030, I estimate company revenues reaching ~US$700M-US$1B/year. With MF launch around 2028, that year could hit ~US$450M. Watch upcoming data read-out in IMpactMF and label expansion. #biotech #hematology $GERN ”

Analyst consensus 12-month target: ~US$3.60-US$3.80 (implies ~ 180-200% upside).

•Given our revenue ramp scenario (MF launch ~2028), here’s a stylised projection:

•End-2026: ~US$2.50

•End-2027: ~US$3.50

•End-2028: ~US$5.00-US$6.50 (if MF commercialisation is on-track)

•Note: If trial setbacks or uptake are slow, price could stay under US$2 or even lower.

•Upside scenario (strong MF uptake label expansion): end-2028 could approach US$8-10.

•Downside scenario (delayed data/regulatory risk): end-2028 might still be <US$2.

1

113