Define Financial • @Investopedia Top 5 Advisor • Co-Founder @TheAdvisorGC • Stay Wealthy Retirement Podcast

Joined October 2012

- Tweets 7,649

- Following 940

- Followers 6,972

- Likes 67,798

718 Photos and videos

Pinned Tweet

28 Jun 2021

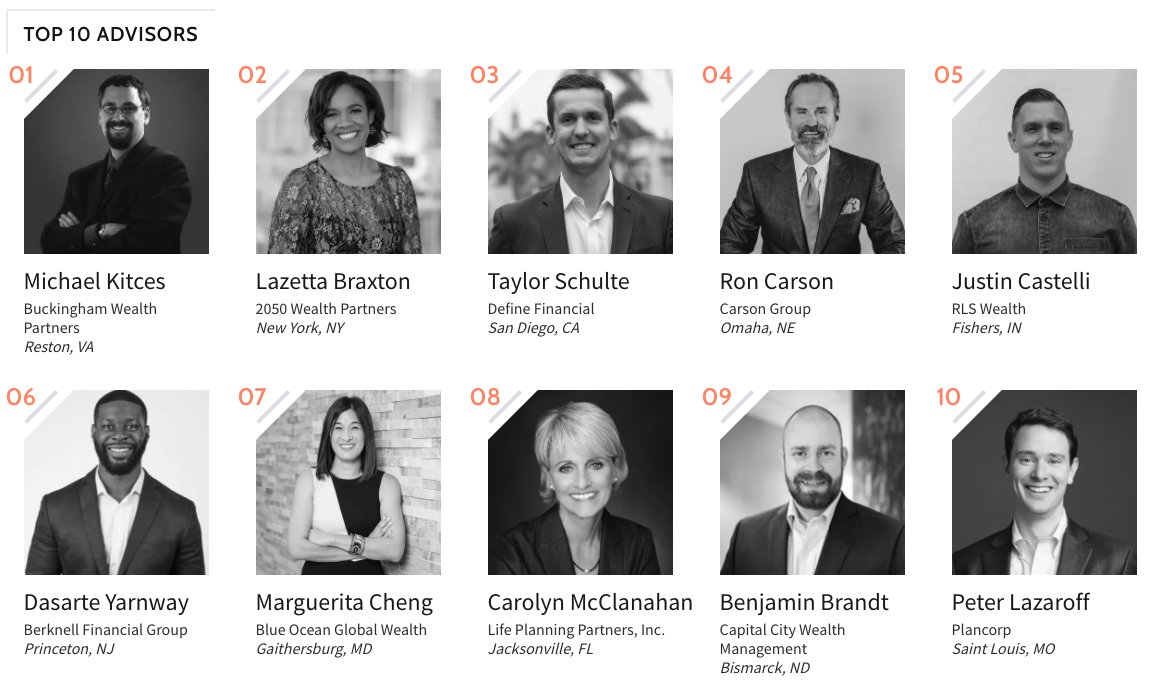

An amazing group of well-deserving advisors being recognized by @Investopedia today. A BIG congrats to all, I'm honored to be included.

👉 Check out the full list: investopedia.com/top-100-fin…

23

2

110

Taylor Schulte, CFP® retweeted

Mar 15

Oil is a global commodity.

U.S. oil companies can sell their oil to anyone in the world and they won't sell it to a local refinery for $70 if a buyer in Europe or Asia is willing to pay $100 because of a Middle East shortage.

You aren't paying more because the U.S. is running out of gas; you're paying more because U.S. oil is part of a global auction, and the auction just got a lot more expensive because of the war.

The more you know!

Mar 12

Only 2% of the oil used in U.S. domestic gas supplies comes through the Strait of Hormuz.

Are we being gouged at the pump?

Community note

Oil is a globally traded commodity, so any restriction on supply, without a decrease in demand, increases price.

With the Strait of Hormuz traffic restricted, the US and Canada may export more oil to countries that normally buy oil that passes through the strait.

eia.gov/outlooks/steo/…

eia.gov/energyexplaine…

reuters.com/markets/commod…

114

546

3,763

323,050

Taylor Schulte, CFP® retweeted

Mar 8

This is a compelling story, in part because it paints banking as a scam.

It's also completely wrong and based on myths that have been debunked a million times.

First, the 10% reserve ratio is a relic. Today, reserve requirements in the USA are 0%, yet banks didn't magically start making infinite loans. Why? Because solvent banks are capital constrained, not reserve constrained.

This is where the original story is most misleading.

When a bank receives a $10k deposit (a liability), the sending bank also sends $10k of reserves (an asset). The recipient bank’s Equity (assets minus liabilities) is unchanged. Their lending capacity hasn't improved because their Capital Adequacy Ratio hasn't moved an inch. They don't suddenly have the regulatory room to add $9k of risky new loans to their balance sheet just because they have more cash in the vault.

A bank's capacity to lend is actually contingent on its profitability. If these new deposits are less expensive than their previous funding sources, the bank’s Net Interest Margin improves. Those profits eventually flow into Retained Earnings, which increases their capital. That is what actually creates the capacity to lend more.

This isn't a scam; it's capitalism. Well-managed, profitable banks grow their capital base, which allows them to safely expand their lending to the economy.

The multiplier story is popular because it's simple and cynical. But if you want to understand how the plumbing actually works, follow the capital, not the reserves. 👍

A man deposits $10,000 in a bank.

The bank thanks him and records the deposit on its balance sheet. But not where you might expect. For the bank, that $10,000 is actually a liability – because technically it belongs to the customer and might have to be returned.

So the bank does what banks do. It lends $9,000 of that money to someone buying a car.

Now something interesting happens. The $9,000 loan appears on the bank’s books as an asset – because someone now owes the bank money.

So the same $10,000 is doing two jobs at once. The depositor believes he has $10,000 safely in the bank. The borrower now has $9,000 to spend.

That $9,000 gets deposited somewhere else. The next bank lends $8,100. That gets deposited again. Then $7,290 gets lent out.

Soon the original $10,000 has quietly turned into tens of thousands of dollars of loans scattered across the economy.

Everyone believes they have money. Depositors see balances in their accounts. Borrowers have the money they spent. Banks show healthy assets on their balance sheets because people owe them money.

And here’s the best part.

Banks charge interest on all those loans – maybe 7%. But the depositor who supplied the original money might earn only 0.5% on their savings account.

So banks collect interest on money that mostly wasn’t theirs to begin with – and keep the difference.

The system works beautifully.

As long as nobody asks for the money back at the same time.

43

47

376

81,175

7 Aug 2025

Marketing not working?

Join @kendrarockslife & me LIVE on stage at @FutureProof_HQ Festival ☀️

We're selecting ONE advisor for a live podcast recording, where we'll solve your biggest marketing challenge in 30 min.

Requirements:

✅ At Future Proof (in person)

✅ Ready to share on stage

Apply: taylorschulte.com/apply (mention "FUTURE PROOF")

Real solutions. No fluff. Let's fix your marketing 💯

5

2

28

2,295

7 Aug 2025

Attending Future Proof? Play golf?

I have room for THREE more to join us at the (unofficial) 4th Annual Future Proof Golf Outing.

▸ When: Sunday, September 7th (consecutive tee times beginning at 7:45am PST)

▸ Where: Pelican Hill (North Course)

▸ What: Casual round of ocean-view golf with your peers (all skill levels welcome)

▸ Cost: $525/person (includes caddy and gratuity)

👉 Send me a DM if you would like to join!

3

14

644

Taylor Schulte, CFP® retweeted

29 Jul 2025

Is AI really your thought partner, or are you just offloading your thinking to AI?

One is active, the other is passive.

One makes you a better thinker, one makes you worse.

10

3

31

2,709

24 Jul 2025

What if everything you’ve learned about money completely changes once you cross the $1 million mark?

I had a blast chatting with @dollarsanddata this week about his new book, The Wealth Ladder.

We discussed:

→ Why retirement savers with $1-10 million often feel financially stuck

→ The surprising reason wealthy retirees are more likely to lose wealth than those with less money

→ Why your investment portfolio becomes more important than your income as net worth grows

Check it out on your favorite podcast app 👇

youstaywealthy.com/podcasts/…

1

9

543

Taylor Schulte, CFP® retweeted

23 Jul 2025

If you know, you know:

geni.us/wealthladderhardcove…

1

6

16

8,894

Taylor Schulte, CFP® retweeted

23 Jul 2025

Shout out to all the advisors listening to my podcast with @DefineFinancial “Advisor Marketing Made Simple.”

A quick review means a lot to let us know you are listening, what you enjoy most, and what makes the show stand out to you.

🙏

2

5

428

Taylor Schulte, CFP® retweeted

22 Jul 2025

My book, The Wealth Ladder, is now available:

geni.us/wealthladderhardcove…

71

59

554

494,810

Taylor Schulte, CFP® retweeted

20 Jul 2025

I've been thinking a lot about Scottie's comments this week, and I'm not sure anyone has viewed them the way I did, so if you don't mind, I want to share why they resonated with me:

Don't let your job define who you are.

190

292

6,354

1,522,321

9 Jul 2025

I've been using Exhibit A (custom chart-building service by @mattcerminaro and @michaelbatnick ) since its launch in March.

Since adopting it, I've identified two very specific use cases for it in my practice.

If you're interested in learning more about the service how I'm using it, join Michael Batnick, Matt Cerminaro, and me on July 23rd @ 1pm ET.

👉 Register to join and learn more: us06web.zoom.us/meeting/regi…

17

14

24

10,072

15 May 2025

Does anyone use the YouTube Music app as their primary source for listening to podcasts? If so, please send me a DM—I have a quick question for you. Thanks!

1

2

534

Just crossed a billion congrats @Perth_Tolle !!!

Would be surprised if FRDM isn't a $500m fund soon.

@Perth_Tolle been@banging the drum for a long time...

mebfaber.com/2021/06/07/e318…

32

2

94

20,359

Taylor Schulte, CFP® retweeted

2 May 2025

🚨 Last chance! Registration for #JoltConference closes TONIGHT at midnight.

✅ The only marketing conference in finserve

✅ 40 speakers from top firms

✅ Real strategies for AUM growth, AI, video, niche marketing & more

Use my code ROBERTSOCIAL for 30% off: JoltConference.com

1

3

8

6,483

Taylor Schulte, CFP® retweeted

29 Apr 2025

Name a bigger lie.

I'll wait.

1,311

10,222

166,016

6,551,104

Taylor Schulte, CFP® retweeted

11 Apr 2025

As I said in my recent interview with Taylor, China would just raise their tariffs again by today. The US is underestimating China. They are our economic and military equal. They will not be bullied. We're doing this ALL wrong.

x.com/spectatorindex/status/…

10 Apr 2025

Big thanks to @cullenroche for joining me on the pod to chat tariffs, markets, and kids preventing us from taking naps.

Listen here: youstaywealthy.com/podcasts/…

43

17

114

26,228

10 Apr 2025

Big thanks to @cullenroche for joining me on the pod to chat tariffs, markets, and kids preventing us from taking naps.

Listen here: youstaywealthy.com/podcasts/…

4

3

19

29,821

Taylor Schulte, CFP® retweeted

19 Mar 2025

Outside of our awesome Practice Manager Cathy, every other member of our awesome team (client-facing as well as back-stage) has come from networking and socials. I'm confident that our next unicorn rockstar team members is out there. Please view and share or apply as you see fit.

4

1

9

2,661

Taylor Schulte, CFP® retweeted

13 Mar 2025

There's a reason you're seeing more and more financial advisor communities pop up.

Clearly, being a part of a community is proving to be an essential component to financial advisor success.

And while I can't tell you if @theadvisorgc is the right community for you, I can tell you this:

We're made up of some REALLY amazing people.

Our advisors LOVE the support they get.

EVERYONE feels welcome and connected.

NO ONE disagrees that joining the AGC is one of the best career moves they've made to date.

Interested in learning more?

The rockstar AGC leadership team and I— @DefineFinancial, @jus10castelli, Haley Marx, & Brian Thorp—are hosting a FREE DISCOVERY SESSION on March 24th at 1 pm ET.

Save your spot here: theagc.kit.com/springdiscove…

This session marks the kickoff of our next open enrollment period, where we welcome new financial advisors to join us! 👋

The enrollment closes on April 4th, so if you've been thinking about joining a community, now's your chance to check us out. ⏱️

Or maybe...you've just been a little lonely.

Perhaps a little lost.

Feeling unsupported at times.

Wishing you had a collective group of over 170 advisors to tap into with your questions whenever they come up....

That's exactly why The AGC™ exists!

Come find out what we're all about. I promise it'll be a really good use of your time!

2

1

565