Stock Analyst - Swing Trader - Long-Term Investor | Investing since February 2010

Joined February 2012

- Tweets 12,710

- Following 69

- Followers 12,840

- Likes 854

500 Photos and videos

Pinned Tweet

Jun 12

f you want to avoid unnecessary detours, seize truly valuable market opportunities, and maximize your profits, why not join our group? You can add us on WhatsApp via our profile, or simply click the link below:

wa.me/12313609544?text=5

Once you’ve successfully joined, please send “5”. Opportunities like this are rare—if you miss this one, you may have to wait a long time for the next one.

#SP500 #Investing #StockInvesting #StockMarket #Stocks #QQQ #DWSN #NVDA

Jun 12

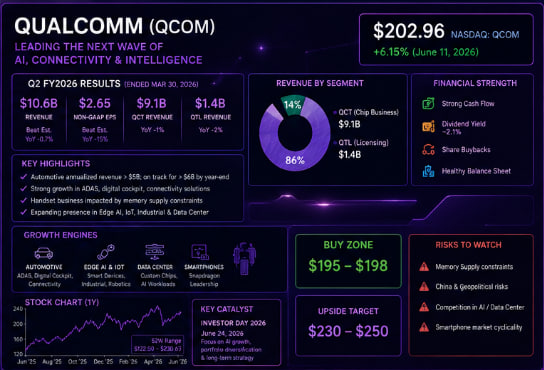

$QCOM: A leader in mobile chips, the company is accelerating its diversification into automotive, edge AI, data centers, and IoT. Q2 FY2026 results beat expectations (revenue of $10.6B, non-GAAP EPS of $2.65), with the automotive business hitting a record high, but mobile memory supply issues weighed on Q3 guidance. Current share price ≈ $202.96 (6/11 close 6.15%), market cap ≈ $214B

Q2 FY2026 Earnings Report (released 4/29): Revenue $10.6B (slightly above expectations, slight YoY decline); Non-GAAP EPS $2.65 (beat); QCT (chips) $9.1B, QTL (licensing) $1.4B. Annualized automotive revenue exceeds $5B, with a target to surpass $6B by year-end; handheld devices impacted by memory shortages.

Recent developments: Collaboration with SLB on edge AI power solutions; positive comments from Nvidia CEO Jensen Huang; Investor Day 2026 to be held on June 24, focusing on AI growth and diversification; rumors of custom chips for data centers for companies like ByteDance. No major negatives; next earnings report expected in late July.

Key Rationale

Strong performance in automotive and IoT (ADAS, digital chassis).

Differentiated advantage in on-device AI (Snapdragon) to counter Nvidia/AMD’s data center expansion.

Robust cash flow supports high dividends and share buybacks.

Geopolitical/supply chain risks (Chinese market, memory) are short-term headwinds.

Buy Zone: $195–$198

Solid fundamentals (Q2 beat accelerated diversification into automotive/AI), with stable dividends providing a buffer. Although the short-term mobile cycle and conservative guidance are weighing on valuations, the June 24 Investor Day is a key catalyst.

#NVDA #AIStocks #QCOM #SPX #Tesla #Tariffs #Meta

194

It was a week of high drama on Wall Street. Tensions with Iran sent shivers early, with the Dow shedding over 900 points in one session as chips faltered. Then came the pivot: Trump announced strikes were off and a deal was imminent. Markets roared back—the Dow reclaimed nearly 930 points, tech giants led a Nasdaq surge, and optimism filled trading floors. But the real plot twist arrived Friday: SpaceX blasted onto the Nasdaq as SPCX. From a $135 IPO price, shares rocketed to $161, handing investors instant gains and making history with the largest-ever offering. Employees became millionaires overnight, Musk's empire expanded, and the broader market closed the week higher. As weekend calm settles, investors ponder if this launch marks the ignition for a new era of innovation-driven prosperity.

#WallStreetDrama #SpaceXDebut #TrumpIranUpdate #MarketTurnaround #InnovationStory #InvestorWins #WeekendWrap

177

Jun 12

$MU surged 11.7% amid tight HBM/DRAM supply.

Advantages: Leading position in high-bandwidth memory for AI servers; exploding content-per-GPU drives structural demand supercycle.

1-Week Outlook: Momentum favors $1,020–$1,080 if AI capex narrative stays hot — prime beneficiary of ongoing server buildout.

#MU #MemoryStocks #AIStocks #NVDA #Semiconductors #SPX #Tariffs

283

Jun 12

Seeing everyone in the group sharing profit screenshots has me so excited!

$BRELY YThis 15% gain wasn't luck—it's the result of our perseverance and collective effort

#StockMarket #StockAnalysis #StockTrading #SP500

Jun 12

$B*** volatility soars 10%-50%, insiders know the inside scoop. Full strategy? Outsiders needn't bother—exclusive to our group members. Hurry and click my profile to add me on WhatsApp

#SP500 #Investing #StockInvesting #StockMarket #Stocks #QQQ #GAUZ #NVDA #US

210

Jun 12

$B*** volatility soars 10%-50%, insiders know the inside scoop. Full strategy? Outsiders needn't bother—exclusive to our group members. Hurry and click my profile to add me on WhatsApp

#SP500 #Investing #StockInvesting #StockMarket #Stocks #QQQ #GAUZ #NVDA #US

334

Jun 12

$QCOM: A leader in mobile chips, the company is accelerating its diversification into automotive, edge AI, data centers, and IoT. Q2 FY2026 results beat expectations (revenue of $10.6B, non-GAAP EPS of $2.65), with the automotive business hitting a record high, but mobile memory supply issues weighed on Q3 guidance. Current share price ≈ $202.96 (6/11 close 6.15%), market cap ≈ $214B

Q2 FY2026 Earnings Report (released 4/29): Revenue $10.6B (slightly above expectations, slight YoY decline); Non-GAAP EPS $2.65 (beat); QCT (chips) $9.1B, QTL (licensing) $1.4B. Annualized automotive revenue exceeds $5B, with a target to surpass $6B by year-end; handheld devices impacted by memory shortages.

Recent developments: Collaboration with SLB on edge AI power solutions; positive comments from Nvidia CEO Jensen Huang; Investor Day 2026 to be held on June 24, focusing on AI growth and diversification; rumors of custom chips for data centers for companies like ByteDance. No major negatives; next earnings report expected in late July.

Key Rationale

Strong performance in automotive and IoT (ADAS, digital chassis).

Differentiated advantage in on-device AI (Snapdragon) to counter Nvidia/AMD’s data center expansion.

Robust cash flow supports high dividends and share buybacks.

Geopolitical/supply chain risks (Chinese market, memory) are short-term headwinds.

Buy Zone: $195–$198

Solid fundamentals (Q2 beat accelerated diversification into automotive/AI), with stable dividends providing a buffer. Although the short-term mobile cycle and conservative guidance are weighing on valuations, the June 24 Investor Day is a key catalyst.

#NVDA #AIStocks #QCOM #SPX #Tesla #Tariffs #Meta

1

5

908

Jun 12

Battlefield Edge AI Hero – $OSS

Core Event: One Stop Systems delivers explosive 55% revenue growth in Q1, flips to profitability, and secures major rugged AI server defense contracts.

Bullish Logic: Rising geopolitical tensions supercharge DoD spending on hardened edge computing for drones, vehicles, and battlefield systems.

Climax Surge: Small-cap defense-tech fever explodes, drawing momentum hunters and pushing trading volumes to multi-year extremes.

#DefenseStocks #OSS #AIStocks #PLTR #NVDA #SPX #Geopolitics

1

292

Jun 11

Blue-chip industrials delivered reliable gains. $CAT Caterpillar rose ~1.8%, supported by $HON Honeywell and infrastructure tailwinds. Strong cash flows, defense orders, and AI-related capex are the key advantages. In a stabilizing macro environment, these defensive growth names are positioned for continued moderate upside.

#NVDA #TSLA #AAPL #MSFT #SPY #QQQ #MU

202

Jun 11

$HPK: Is HPK a worthwhile investment given current oil prices? How does the company balance growth and risk?

Do Q1 results and the 2026 guidance support a rebound?

Does the attractive valuation align with the company’s execution capabilities?

An independent producer focused on unconventional oil and gas development in the Midland Basin (Permian), the company reported strong Q1 production (approximately 46,000 BOE/d, exceeding guidance) and a significant decline in costs. However, it recorded a substantial net loss due to accounting and hedging factors, though it was near breakeven on an adjusted basis. The company has shifted toward capital discipline and a focus on free cash flow, with its 2026 guidance emphasizing operational optimization. The new CEO brings potential for improved execution.

Key Points

Q1 2026 Results: Revenue $215.9M (beat expectations), adjusted EPS -$0.02 (in line), strong EBITDAX, production 45.6–46 MBoe/d (oil ~68%), costs down 22%, generated >$20M FCF (ex-WC). Net loss primarily due to non-cash/one-time factors.

2026 Guidance: Production of 41–44 MBoe/d (oil 67–68%), capital expenditures of $255–285M, with a focus on efficiency rather than aggressive growth.

Shareholder Returns: Quarterly dividend of $0.04 (annualized yield ~2.7%), alongside an ATM equity offering for debt optimization.

Oil Price and Commodity Volatility: Highly sensitive, with significant downside risk.

Debt and Liquidity: High leverage; debt service and ATM usage require monitoring.

Execution Risk: Whether the new management team can consistently deliver on cost savings and production targets.

Target Price: $9.0–10.0

#NVDA #TSLA #PLTR #AAPL #AMD #MSFT #SPY

145

Jun 11

$LLY's oral GLP-1 weight loss drug boasts impressive Phase III clinical trial data, surpassing major competitors. The obesity and diabetes market has a trillion-dollar potential. The bullish rationale lies in its rich pipeline, strong pricing power, and long-term EPS growth expected to remain high double-digit. Its absolute leading position in the metabolic drug field is firmly established. Health is a timeless theme, and $LLY has proven its dominance with solid data, attracting a flood of institutional funds and igniting market sentiment. The climax has officially begun!

#NVDA #LLY #TSLA #MU #SMCI #ORCL #PFE #Pharma #StockMarket #Investing

167

Jun 10

Small-cap tech and semiconductor-related stocks dominated upside. $FRMI exploded 22.60% with explosive volume. $AXTI (AXT Inc.) and $BULL (Webull Corporation) delivered strong gains on fintech and materials tailwinds. Summary: AI-adjacent and high-growth tech names continued to attract aggressive capital.

#HotStocks #TrendingStocks #MostDiscussed #SuperHighHeat #Top10Stocks #USMarketBuzz #TechMomentum

344

Jun 10

f you want to avoid unnecessary detours, seize truly valuable market opportunities, and maximize your profits, why not join our group? You can add us on WhatsApp via our profile, or simply click the link below:

wa.me/12313609544?text=5

Once you’ve successfully joined, please send “5”. Opportunities like this are rare—if you miss this one, you may have to wait a long time for the next one.

#SP500 #Investing #StockInvesting #StockMarket #Stocks #QQQ #DWSN #NVDA

Jun 10

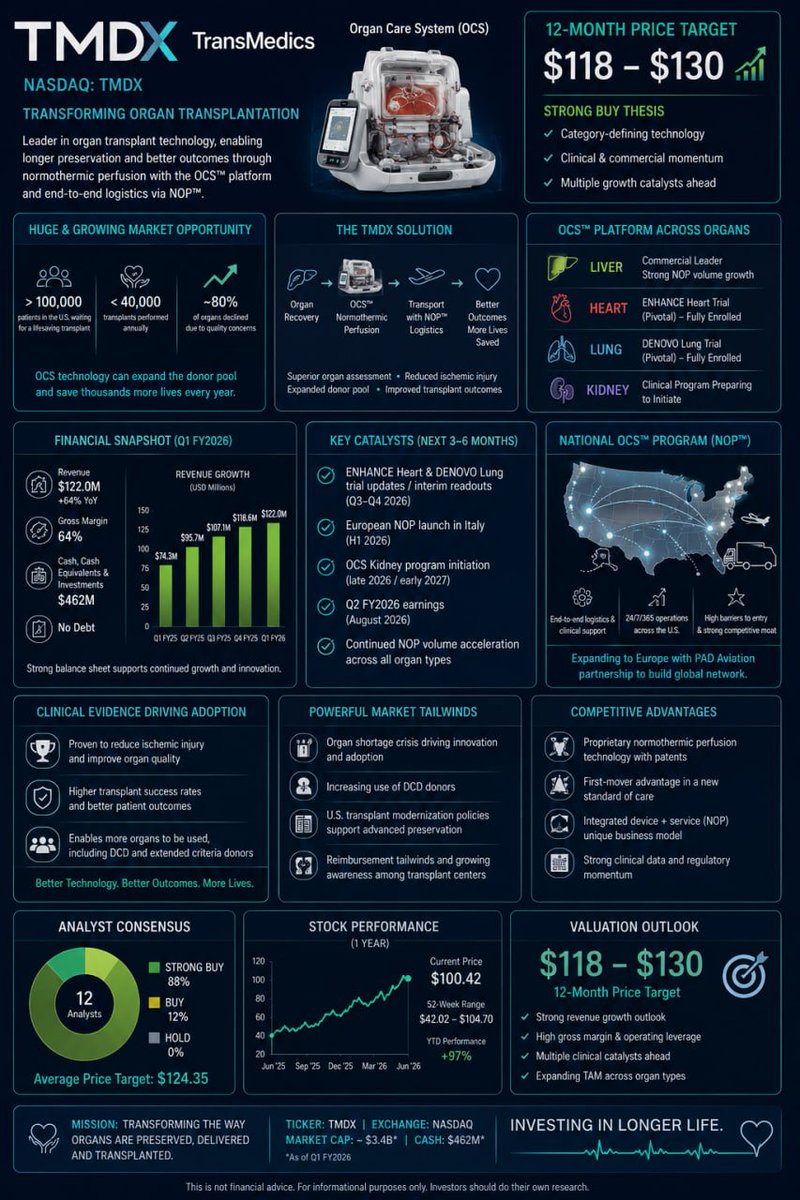

$TMDX: A medical device company specializing in organ transplantation technology that uses its Organ Care System (OCS) platform to enable normothermic perfusion during organ transport, significantly improving transplant success rates. The company also operates the National OCS Program (NOP), which provides end-to-end logistics services and currently covers heart, lung, and liver transplants.

Macro Context (3 Months): The organ shortage crisis is driving growth in transplant demand, while U.S. transplant modernization policies and the increase in DCD (donor after circulatory death) donors create a favorable environment for advanced preservation technologies like OCS. The company benefits from high regulatory barriers in the medical device sector and the potential for orphan drug/breakthrough device designations, with the NOP model shifting toward service revenue to drive high-margin growth.

Key Catalysts: Accelerated patient recruitment for the ENHANCE Heart and DENOVO Lung trials (which have received full FDA approval); Q3-Q4 data updates or interim results will drive adoption for cardiac and pulmonary indications.

European NOP launch (Italy H1 2026), with PAD Aviation investment strengthening the European logistics network.

OCS Kidney program progress (preparing for clinical launch), with potential to contribute new revenue in late 2026/early 2027.

Q2 earnings (around August) may demonstrate NOP volume growth and guidance confirmation/upward revision.

The company’s core competitive advantage lies in the OCS platform’s technological barriers: patented ambient-temperature perfusion technology outperforms traditional cold preservation, reducing ischemic injury and expanding the donor pool (especially marginal donors), with clinical evidence supporting better transplant outcomes.

Vertically integrated NOP model: Full-chain services from devices to logistics, already capturing a significant share of OCS transplants in the U.S.; reusable devices and service revenue create a high-stickiness moat.

Execution and Expansion: Rapid commercialization (leading in liver transplants), progress in clinical trials, and international expansion (investment in European aviation), with $462 million in cash reserves to support growth investments.

Regulatory and Data Advantages: Multiple FDA IDE approvals and ongoing registration trials pave the way for label expansion.

Bullish Case:

Strong demand clinical catalysts will drive volume growth in heart and lung transplants, moving beyond the current liver-dominated model.

NOP international expansion provide visible multi-channel growth, with significant room for long-term penetration rate expansion.

12-Month Target: $118–$130

#TMDX #OrganTransplant #OCSPlatform #NOPGrowth #ENHANCEHeart #DENOVOLung #BiotechMedTech

220

Jun 10

$TMDX: A medical device company specializing in organ transplantation technology that uses its Organ Care System (OCS) platform to enable normothermic perfusion during organ transport, significantly improving transplant success rates. The company also operates the National OCS Program (NOP), which provides end-to-end logistics services and currently covers heart, lung, and liver transplants.

Macro Context (3 Months): The organ shortage crisis is driving growth in transplant demand, while U.S. transplant modernization policies and the increase in DCD (donor after circulatory death) donors create a favorable environment for advanced preservation technologies like OCS. The company benefits from high regulatory barriers in the medical device sector and the potential for orphan drug/breakthrough device designations, with the NOP model shifting toward service revenue to drive high-margin growth.

Key Catalysts: Accelerated patient recruitment for the ENHANCE Heart and DENOVO Lung trials (which have received full FDA approval); Q3-Q4 data updates or interim results will drive adoption for cardiac and pulmonary indications.

European NOP launch (Italy H1 2026), with PAD Aviation investment strengthening the European logistics network.

OCS Kidney program progress (preparing for clinical launch), with potential to contribute new revenue in late 2026/early 2027.

Q2 earnings (around August) may demonstrate NOP volume growth and guidance confirmation/upward revision.

The company’s core competitive advantage lies in the OCS platform’s technological barriers: patented ambient-temperature perfusion technology outperforms traditional cold preservation, reducing ischemic injury and expanding the donor pool (especially marginal donors), with clinical evidence supporting better transplant outcomes.

Vertically integrated NOP model: Full-chain services from devices to logistics, already capturing a significant share of OCS transplants in the U.S.; reusable devices and service revenue create a high-stickiness moat.

Execution and Expansion: Rapid commercialization (leading in liver transplants), progress in clinical trials, and international expansion (investment in European aviation), with $462 million in cash reserves to support growth investments.

Regulatory and Data Advantages: Multiple FDA IDE approvals and ongoing registration trials pave the way for label expansion.

Bullish Case:

Strong demand clinical catalysts will drive volume growth in heart and lung transplants, moving beyond the current liver-dominated model.

NOP international expansion provide visible multi-channel growth, with significant room for long-term penetration rate expansion.

12-Month Target: $118–$130

#TMDX #OrganTransplant #OCSPlatform #NOPGrowth #ENHANCEHeart #DENOVOLung #BiotechMedTech

2

1

7

1,363

Jun 10

$HAE: The Hidden Champion of Blood Management Upgrades Efficiency

Key Developments: Q4 earnings exceeded expectations; the company announced a restructuring of its Apheresis and MedSurg divisions, significantly enhancing strategic transparency and focus. Bullish Rationale: Plasma collection demand remains robust, new vascular closure products are accelerating market penetration, ERP system optimization is delivering long-term efficiency gains, and cash flow remains strong. Elevation Market Sentiment (Peak): In the low-profile medical device sector, $HAE has announced its triumphant return with a masterful restructuring! Smart money has already positioned itself in advance; this hidden champion’s moment in the spotlight has officially begun, and its story of steady growth is being enthusiastically embraced by the market!

#HAE #Apheresis #BloodManagement #MedSurgDevices #HealthcareEfficiency #MedicalTech #StableGrowthStocks

181

Jun 9

$LITE leads the rally, $AXTI surges significantly, $VECO follows with strong gains, and $CIEN rises in tandem.

Bullish rationale: The upgrade cycle for 800G/1.6T optical modules has begun, with severe shortages of key materials such as InP; capacity expansion and order backlogs jointly support high growth expectations.

Synergy Market Sentiment (Peak): The invisible, light-speed neural network is underpinning the future of AI—$LITE and $AXTI stand at the forefront of the photonics revolution! Infrastructure capital is quietly awakening and aggressively positioning itself.

#LITE #AXTI #Photonics #OpticalModules #AIInfra #CompoundSemi #DataCenterOptics

369

Jun 9

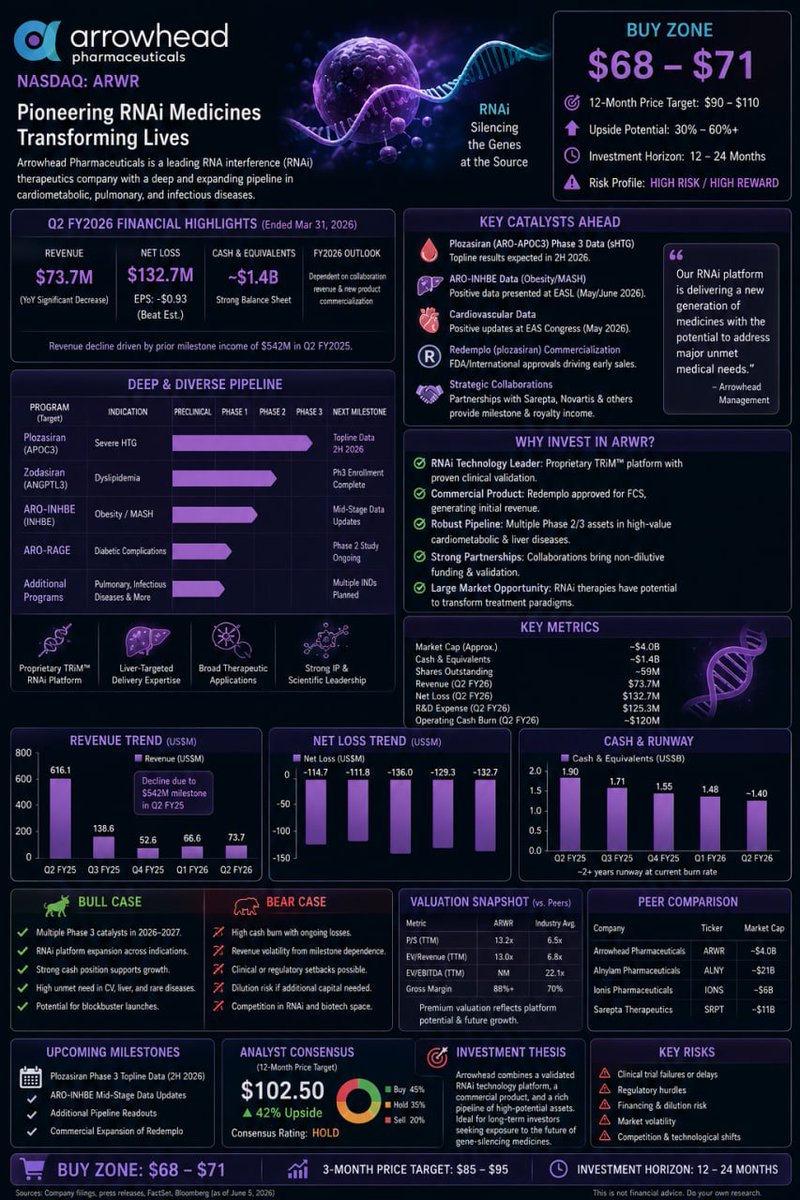

$ARWR: Is ARWR worth investing in? As a leading RNAi therapeutics platform company, it has a commercialized product (Redemplo/plozasiran for familial chylomicronemia) and a robust pipeline in cardiovascular, metabolic, and pulmonary diseases, benefiting from the validation of RNAi technology and data catalysts. However, Q2 revenue declined significantly (losses driven by reduced milestone payments), and the company is currently in a high-valuation, cash-burning phase. It is suitable for investors with a high risk tolerance who are bullish on the RNAi platform in the long term. Short-term volatility is high, and investors should monitor clinical data catalysts.

Q2 FY2026 (reported May 7, ended March 31): Revenue $73.7M (significant YoY decline due to a high prior-year base of $542M in milestone payments); Net loss of $132.7M (EPS -$0.93, beating expectations); ample cash reserves. Full-year performance will depend on collaboration revenue and the commercialization of new products.

Recent Announcements: Late May/Early June: Positive EASL data for ARO-INHBE (obesity/MASH candidate); positive cardiovascular data at the EAS conference.

Plozasiran (ARO-APOC3) Phase 3 data expected (sHTG, second half of 2026); enrollment completed for multiple trials.

Redemplo approval in the U.S. and other regions to drive commercialization.

Collaborations: Licensing agreements with Sarepta, Novartis, and others provide revenue.

Key Drivers: Leading RNAi platform (TRiM™) in liver-targeted and cardiovascular fields, with commercialized products and a robust Phase 3 pipeline; favorable trends in AI and precision medicine. However, high R&D costs and revenue volatility remain major pressures.

Key Points: Strengths: Commercialization milestones, strong pipeline (plozasiran, zodasiran, ARO-INHBE, etc.), partnership revenue, and cash reserves.

Key Watchpoints

Plozasiran Phase 3 data (Q3 2026 ) and regulatory progress.

Interim data for ARO-INHBE and other pipeline candidates.

Milestone revenue from collaborations and commercial sales.

Cash burn and financing needs.

Macro: Biotech funding environment and interest rates.

Buy Zone: $68–$71

#ARWR #RNAi #Biotech #Plozasiran #CardioMetabolic #ArrowheadPharma #ALNY

6

555

Jun 9

$ARWR RNAi Platform Achieves Major Clinical Milestone

Key Event: Positive interim results for plozasiran and other drug candidates; accelerated advancement of the cardiovascular and metabolic pipeline.

Bullish Rationale: A mature RNAi platform combined with existing approved products, coupled with significant unmet needs in the cardiovascular field, offers broad prospects for commercialization and partnership royalties.

Conclusion Market Sentiment (Climax): From the lab to the patient’s bedside, $ARWR is reshaping the future of precision medicine! Biotech innovation capital is making a strong comeback, and the next generation of blockbuster drugs is poised to launch!

Risk Warning: Clinical trials and regulatory approvals involve uncertainties; the biotech sector is highly volatile. Please manage risks appropriately.

#ARWR #RNAi #Biotech #Plozasiran #CardioMetabolic #PrecisionMedicine #GeneTherapy

4

637

Jun 8

$INTC Intel Corporation

Intel shares surged approximately 11-12% today, driven by reports of a substantial Google order for millions of custom AI tensor processing units starting in 2028. Strengths include advancing its foundry capabilities and emerging as a strong alternative supplier in the AI chip space. This belongs to the semiconductor / AI foundry sector. Definitely worth keeping a close watch — momentum from major tech contracts could support further recovery and sustained growth potential.

#AIChips #IntelRally #GoogleTPU #SemiconductorRebound #FoundryGrowth #TechRecovery #INTCMomentum

157

Jun 8

f you want to avoid unnecessary detours, seize truly valuable market opportunities, and maximize your profits, why not join our group? You can add us on WhatsApp via our profile, or simply click the link below:

wa.me/12313609544?text=5

Once you’ve successfully joined, please send “5”. Opportunities like this are rare—if you miss this one, you may have to wait a long time for the next one.

#SP500 #Investing #StockInvesting #StockMarket #Stocks #QQQ #DWSN #NVDA

Jun 8

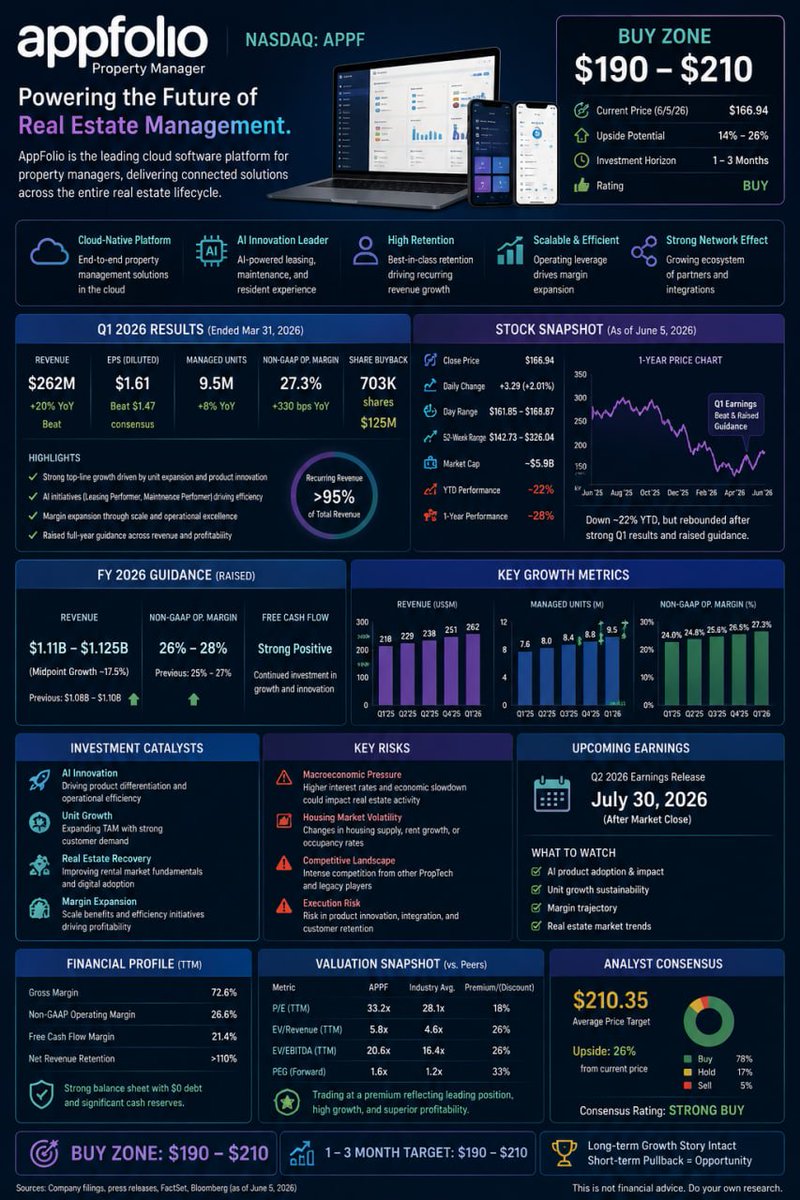

$APPF: A leading SaaS company focused on real estate technology (PropTech), primarily providing property management companies with a cloud-based software platform that includes property management, leasing, maintenance, resident experience, and AI-driven value-added services. Its client base consists primarily of mid-sized property management firms, with a strong emphasis on AI innovation and unit growth. AppFolio is the leading SaaS provider in the property management vertical, benefiting from AI innovations (such as Leasing/Maintenance Performer), high retention rates, and recurring revenue driven by unit growth. The real estate market recovery and digital transformation provide long-term tailwinds, and the company enjoys high competitive barriers (network effects).

Key Points (Current Stock Price and Recent Performance, as of the close on June 5, 2026) Closing Price: $166.94 ( 3.29 / 2.01%), Intraday Range: $161.85–$168.87.

52-week range: $142.73–$326.04; Market Cap ~$5.9B.

YTD/1-year performance: Down approximately 22–28%, but rebounded following Q1 earnings.

Q1 2026 Earnings (Announced April 23): Revenue: $262M ( 20% YoY), beat expectations.

EPS: $1.61 (beat the $1.47 consensus).

Units under management: 9.5 million ( 8% YoY).

Non-GAAP operating margin: 27.3% (strong expansion).

Share buyback: 703,000 shares ($125M).

Full-year guidance raised: Revenue $1.11B–$1.125B (midpoint growth ~17.5%), non-GAAP operating margin 26–28%.

Key Focus Areas for Next Earnings Report:

AI product adoption, sustainability of unit growth, margin trajectory.

Signs of a real estate market recovery (rents, occupancy).

Macro: Interest rates, changes in housing supply.

Short-term (1–3 months) target: $190–$210

#NVDA #TSLA #AAPL #MSFT #AMZN #GOOGL #META

266

Jun 8

Seeing everyone in the group sharing profit screenshots has me so excited!

$BSAAU YThis 29% gain wasn't luck—it's the result of our perseverance and collective effort

#StockMarket #StockAnalysis #StockTrading #SP500

Jun 8

$B*** volatility soars 10%-50%, insiders know the inside scoop. Full strategy? Outsiders needn't bother—exclusive to our group members. Hurry and click my profile to add me on WhatsApp

#SP500 #Investing #StockInvesting #StockMarket #Stocks #QQQ #GAUZ #NVDA #US

179