26m

DUAL GROWTH ENGINE: HANA SECURITIES SEES RF MATERIALS RIDING LUMENTUM OPTICS AND RFHIC’S GaN SHARE GAINS

TLDR: RF Materials combines AI optical upside from Lumentum with wireless growth from RFHIC, creating broader and more visible earnings momentum than many single-theme optical names.

Hana Securities expects future Lumentum sales to exceed 30 billion won as optical-module orders, utilization and capacity expand, potentially doubling RF Materials’ existing revenue base excluding RF Systems. Parent RFHIC could also lift its GaN transistor share from about 2% to as much as 10% as 4GHz and 7GHz networks favor GaN over LDMOS and NXP exits telecom, potentially adding more than 50 billion won in RF package sales. RF Materials is also one of the few Korean optical names already generating Nvidia-related revenue.

#RFMaterials #RFHIC #Lumentum #NVIDIA #GaN #OpticalModules #OpticalNetworking #AIInfrastructure #DataCenters #Telecom #RFComponents #Semiconductors #KoreaStocks #KoreaMarkets $LITE $NVDA $NXPI $EWY $KORU

42

#GigaDeviceSemiconductor Expands Optical Communication Portfolio with New GD32E512 and GD32E252 Series #MCUs for #OpticalModules

#technews #technology #electronicsnews #electronicseranews #semiconductor #powerelectronics #eenews

electronicsera.in/gigadevice…

17

Jun 12

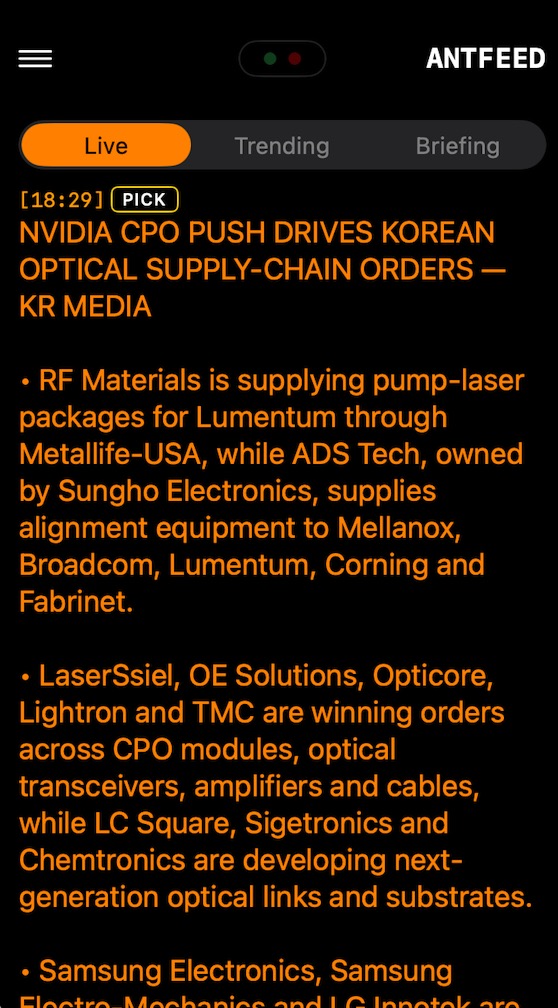

CPO GOLD RUSH: NVIDIA OPTICS BOOM LIFTS KOREAN SUPPLIERS INTO GLOBAL DEALS

TLDR: Nvidia’s CPO push is broadening the AI trade from GPUs and HBM into lasers, optical modules, alignment equipment, cables and silicon-photonics suppliers across Korea.

RF Materials, ADS Tech, LaserSsiel, OE Solutions, Opticore, Lightron, TMC, LC Square, Sigetronics and Chemtronics are gaining exposure to the global optical supply chain, while Samsung Electronics, Samsung Electro-Mechanics and LG Innotek expand CPO and silicon-photonics development as Nvidia, Broadcom and TSMC move next-generation networking toward mass production.

#Nvidia #CPO #CoPackagedOptics #SiliconPhotonics #OpticalModules #OpticalTransceivers #DataCenters #AIInfrastructure #Broadcom #TSMC #Lumentum #Corning #Fabrinet #Mellanox #Samsung #SamsungElectroMechanics #LGInnotek #KoreaSemis $NVDA $AVGO $TSM $LITE $GLW $FN $SSNLF $EWY $KORU $SMH $SOXX

2

2

35

3,480

#GigaDevice expands #MCU lineup with GD32E512 & GD32E252 — high-performance, reliable, connected MCUs for optical module applications.

#OpticalModules #DataCenters #powerelectronics #powersemiconductor #powermanagement #electronicsnews #electronicsbuzz

electronicsbuzz.in/gigadevic…

7

GigaDevice launches GD32E512 and GD32E252 Series MCUs for high-speed and low-speed optical module applications, boosting next-gen connectivity.

#GigaDevice #MCU #OpticalModules #Semiconductor #TechNews #AIInfrastructure #Networking

electronicsmedia.info/2026/0…

10

Jun 12

EXCLUSIVE: KOH YOUNG TAKES 3D INSPECTION INTO SATELLITE MANUFACTURING

Koh Young Technology has entered SpaceX’s supply chain with 3D inspection and closed-loop manufacturing technology that feeds real-time defect data back into production equipment, enabling automatic process adjustments and reducing human intervention in satellite manufacturing.

#KohYoung #SpaceX #SatelliteManufacturing #Aerospace #3DInspection #AutonomousManufacturing #SemiconductorEquipment #AIservers #OpticalModules #HumanoidRobotics #PhysicalAI #KoreaSemis #KoreaMarkets $TSLA $NVDA $EWY $KORU $SMH $SOXX

70

Jun 9

$LITE leads the rally, $AXTI surges significantly, $VECO follows with strong gains, and $CIEN rises in tandem.

Bullish rationale: The upgrade cycle for 800G/1.6T optical modules has begun, with severe shortages of key materials such as InP; capacity expansion and order backlogs jointly support high growth expectations.

Synergy Market Sentiment (Peak): The invisible, light-speed neural network is underpinning the future of AI—$LITE and $AXTI stand at the forefront of the photonics revolution! Infrastructure capital is quietly awakening and aggressively positioning itself.

#LITE #AXTI #Photonics #OpticalModules #AIInfra #CompoundSemi #DataCenterOptics

369

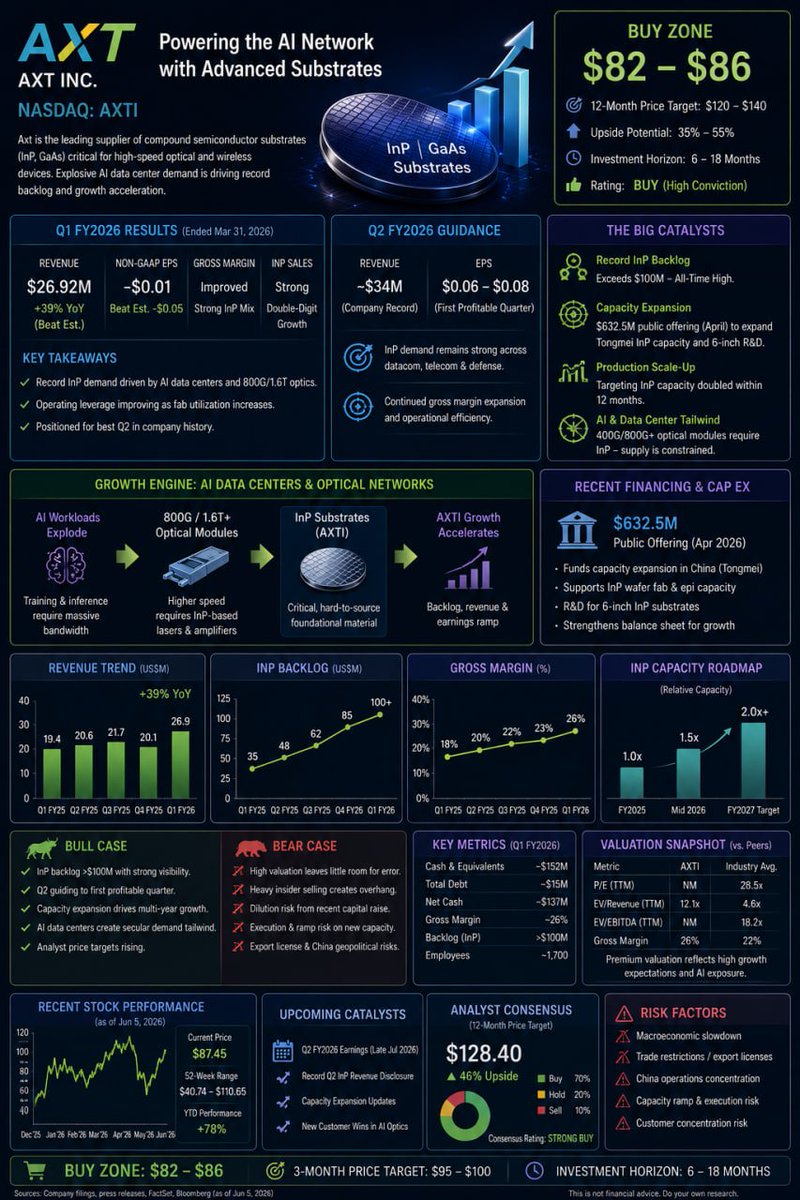

$AXTI: A leading supplier of compound semiconductor substrates (InP, GaAs, etc.), the company is benefiting significantly from the explosive demand for Indium Phosphide (InP) substrates driven by high-speed optical modules for AI data centers. The company has shifted from a cyclical trough to a high-growth trajectory (with an InP backlog exceeding a record $100 million), but high valuations, massive financing for capacity expansion, and heavy insider selling have caused significant volatility in its stock price.

Q1 FY2026 (reported April 30): Revenue of $26.92 million (up 39% YoY, beating expectations); Non-GAAP EPS of -$0.01 (beating the expected -$0.05); gross margin improved, with strong InP sales. Q2 guidance projects revenue of approximately $34 million and EPS of $0.06–0.08 (returning to profitability).

Key catalysts: InP backlog exceeds $100M (all-time high); Q2 expected to be the company’s largest-ever quarterly InP shipment; $632.5M public offering completed in April (to expand Tongmei InP capacity and fund 6-inch R&D); goal to double InP capacity within the year.

Demand for 400G/800G optical modules in AI data centers is driving a shortage of InP substrates; as a key upstream supplier, AXTI is capturing market share through capacity expansion and substantial financing. Improved gross margins and a return to profitability provide fundamental support, but risks related to Chinese production capacity, export licenses, geopolitics, and market cycles remain prominent. Long-term, the company is a “hidden player” in AI photonics infrastructure.

Positives: Record InP demand backlog, accelerated capacity expansion, Q2 profit guidance, analyst target price hikes, tailwinds from the AI theme.

Negatives: Valuation ahead of fundamentals, heavy insider selling, dilution from financing, execution risks of large-scale expansion, export license uncertainty, high exposure to China.

Buy Zone: $82–$86

#AXTI #InP #AIInfra #Photonics #Semiconductors #DataCenter #OpticalModules

2

4

919

$AXTI Sets Record for InP Substrate Backlog; Solid Foundation for AI Optical Interconnect

Key Event: $AXTI’s indium phosphide (InP) order backlog hits an all-time high; substantial funding accelerates capacity expansion.

Bullish Rationale: The upgrade cycle for 800G/1.6T optical modules has begun; severe upstream InP shortages are driving both $AXTI’s pricing power and gross margins higher.

Conclusion Market Sentiment (Climax): Invisible yet indispensable—$AXTI underpins AI’s high-speed neural network! Infrastructure capital is quietly awakening, positioning itself for hidden champions.

Risk Warning: Close attention must be paid to production expansion execution and geopolitical risks; monitoring quarterly progress is recommended.

#AXTI #InP #Photonics #OpticalModules #AIInfra #CompoundSemi #DataCenter

210

May 26

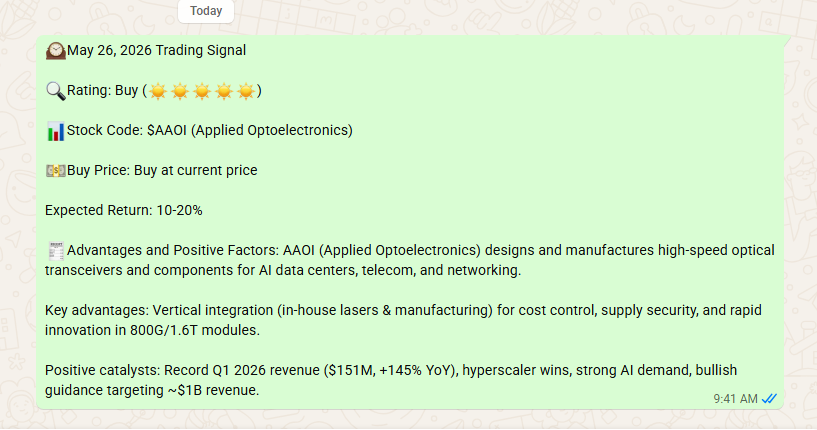

Why I’m Buying $AAOI Right Now – May 26, 2026

Strong Buy Signal 🌞🌞🌞🌞🌞

$AAOI (Applied Optoelectronics) is one of the best-positioned stocks in the exploding AI optical module sector.

Why Buy $AAOI?

• Explosive AI Demand: High-speed optical transceivers (800G / 1.6T) are critical for AI data centers

• Vertical Integration Advantage: In-house lasers and manufacturing = better costs, faster innovation, secure supply

• Record Performance: Q1 2026 revenue $151M ( 145% YoY) with strong hyperscaler wins

• Bullish Guidance: Targeting ~$1 Billion revenue

Expected Return: 10-20% near-term (much higher long-term upside)

This is a real business with real revenue growth and strong moat in the hottest AI infrastructure segment.

Are you buying $AAOI or waiting for a dip?

Drop your thoughts below 👇

#AAOI #AIStocks #OpticalModules #AIInfrastructure #TechInvesting

2

3

1,571

May 17

The US Photonics Supply Chain: The Unsung Hero Powering AI’s Explosive Growth While everyone focuses on GPUs, the real bottleneck — and opportunity — lies in the optical interconnects that move massive amounts of data at light speed inside AI data centers. Gemini Trading’s infographic maps the complete US Photonics Supply Chain for AI infrastructure: Key Layers:InP Substrates → AXT (global leader)

Active Optical Chips → Lumentum, Coherent, Broadcom, MACOM

TOSA/ROSA & Optical Engines → Core components for high-speed transmission

Optical Modules & AOC → AAOI, Ciena, Fabrinet

Networking Systems → Arista, Broadcom, NVIDIA

Terminal AI Applications → NVIDIA GB200 (paired with 18x 800G optical modules), Quantum-X CPO

Market Data:

Global Optical Module Market expected to grow from US$51 billion in 2024 to US$89 billion in 2029 at a 12.5% CAGR. DSP components alone make up 30-40% of an 800G module’s BOM. Why it matters:

AI training clusters are scaling to millions of GPUs. Traditional copper can’t keep up — photonics (light-based data transfer) is the only solution for low-latency, high-bandwidth, energy-efficient connectivity at scale. 2025–2026 will see large-scale deployment of 1.6T systems. Investment angle:

Companies across the photonics stack — especially those enabling 800G/1.6T modules and co-packaged optics (CPO) — stand to benefit enormously as AI capex continues surging. The photonic supply chain is still under-the-radar compared to GPU hype, but it may deliver some of the strongest multi-year growth in the entire AI ecosystem.(Not financial advice — always DYOR and manage risk appropriately.)@GeminiTrading

#Photonics #AIInfrastructure #OpticalModules #Broadcom #Lumentum #AAOI #NVIDIA #Arista

1

128

Apr 20

$POET Luxshare Precision just announced in its official Investor Relations Activity Record:

"800G and 1.6T optical modules are progressing smoothly with domestic and international clients and will become the core driver for future growth."

This signals strong advancement in the 800G/1.6T high-speed optical module business (closely tied to POET Technologies partnership) — expected to be a key growth engine ahead!

Source: Luxshare Precision Investor Relations Activity Record – April 20, 2026

AI data center optical interconnect boom continues! #POET #OpticalModules #Luxshare #AICompute

8

20

138

24,032

Apr 15

Luxshare Precision (002475.SZ) released its 2025 Annual Report today, providing some indirect positive signals for $POET

Key highlights from the report:

•Communications & Data Center business grew 33.81% YoY to RMB 245.68 billion, outpacing the company’s overall 23.64% revenue growth.

•The company confirmed that 800G/1.6T optical modules have entered small-batch supply.

•800G LRO modules have passed validation with select customers, while 1.6T LRO/LPO and related products are advancing in deep development.

Although the report does not name specific suppliers, $POET Technologies is a long-term partner supplying its Infinity™ Optical Engines for Luxshare’s high-speed pluggable optical modules (OSFP/QSFP-DD formats) used in AI data centers.

This combination of strong segment growth and clear product progress suggests improving order visibility and a potential ramp in volume for POET’s optical engine business as Luxshare moves from small-batch to broader commercialization in 2026.

A measured development worth monitoring in the AI interconnect supply chain.

#POET #Luxshare #OpticalModules

1

2

14

1,060

18 Dec 2025

🚀 We’re Hiring | Build the Visual Core of the Metaverse

XR Optical Module Manufacturing Company is expanding its global team.

#WeAreHiring #XR #Metaverse #OpticalModules

1

2

38

How Optical Modules Drive High-Speed Content Delivery in CDNs,In today’s digital age, Content Delivery Networks (CDNs) are the backbone of fast.Visit resources.l-p.com/.../optica…... For more information.#LINKPP #OpticalModules #SFPTransceiver

2

15

16 May 2024

3

63

14 May 2024

Optical modules

1.25G to 800G, whatever you need, we've got it covered.

Standard specifications are available for same-day shipping, and we take pride in our direct factory sales, using only top-notch imported chips without any secondhand materials.

#OpticalModules #Switches

1

28

17 Sep 2021

Quiet, fast and rugged. Our family of sub 60 fs differential oscillators deliver the low-noise and high-speed data transmission required for 100G/400G optical modules in industry-standard 3225 packages. Learn more: mchp.us/3zOgely. #opticalmodules #oscillators #lowjitter

1

2

8 Sep 2021

Meet your system jitter budget in space-constrained optical module designs. Our clock solutions include quartz and MEMS oscillators that conquer the tight jitter requirements necessary for high-capacity networks. mchp.us/3yGOwFO #oscillators #opticalmodules #timing

1

2

.@lightcounting's latest report analyzes the impact of Mega Datacenters on the market for Ethernet optical transceivers, DWDM optics, AOCs, EOMs, and Co-CPO. #datacenter #opticalnetworking #copackagedoptics #opticalmodules

lightcounting.com/report/jul…

2