Investor and researcher. I dig into SEC filings, patent courts, and buyback programs to find what corporations don't want you to see. When actions contradict wo

Joined June 2009

- Tweets 2,950

- Following 1,715

- Followers 626

- Likes 292

155 Photos and videos

Jun 15

Now confirmed, and not by a rumor account. Denmark's Børsen reports it and Novo Nordisk confirms it directly: Donald Trump Jr. went to Novo's corporate headquarters in Bagsværd last week.

Not a hotel. Not a chat with an executive on the side. The official HQ. Novo's own words: he was "in town on business and visited Novo Nordisk in that context." Børsen adds, honestly, that it could not confirm what the meeting was about.

So here are the facts, side by side. The president's son, who holds no formal government position but has acted before as his father's unofficial envoy, made a deliberate visit to a foreign drugmaker's headquarters. It comes exactly as the Wegovy pill crosses 3 million US prescriptions, as Novo's obesity share climbs from ~35% to 42%, and after Trump himself boasted in November about a pricing deal he struck with Novo.

You don't show up at a company's HQ for nothing. I won't tell you what was discussed, because I don't know and neither does Børsen. But the visit, the place, and the timing are facts. Something is moving under the hood. Draw your own conclusions. $NVO $LLY

2

2

413

FollowTheFilings retweeted

Jun 15

$NVO has confirmed the meeting to the biggest Danish business newspaper BORSEN

1

10

1,582

Jun 14

The Medicare timing is the quiet irony nobody is pricing.

For almost 20 years, since 2006, Medicare was legally barred from covering weight-loss drugs. That lifts now, with the GLP-1 Bridge starting July 1.

Notice when it was decided. Medicare didn't subsidize obesity drugs in 2023 or 2024, when Novo led. It moved when Lilly had taken the lead, 60% US share by early 2026. The subsidy was designed in Lilly's picture.

But the program goes live July 2026, and the market has already turned. Novo captures 65% of new patients (116k vs 62k weekly NBRx), the pill outsells Foundayo 31 to 1, aggregate share grinding up.

So the subsidy was conceived when Lilly was winning, and activates when Novo is winning. The Bridge covers both at the same $50 price, removing Foundayo's only edge and handing the decision to efficacy and continuity, where Novo dominates.

The favor, if it was one, gets cashed in the other company's register. Public money, routed through doctors choosing 65/35, flows mostly to the Danish firm. Designed in Lilly's picture, collected in Novo's. $NVO

6

244

Jun 14

The Medicare timing is the quiet irony nobody is pricing.

For almost 20 years, since 2006, Medicare was legally barred from covering drugs for weight loss. That prohibition gets lifted now, with the GLP-1 Bridge starting July 1.

Notice when the decision was made. Medicare didn't move to subsidize obesity drugs in 2023 or 2024, when Novo led the market. It moved when Lilly had taken the lead, 60% US share by early 2026. The subsidy was designed in Lilly's picture.

But here's the part the snapshot misses. The program goes live in July 2026, and by now the market has already turned. Novo is capturing 65% of new patients (116k vs 62k weekly NBRx), the pill outsells Foundayo 31 to 1, and aggregate share is grinding upward.

So the subsidy was conceived when Lilly was winning, and it activates when Novo is winning. The Bridge covers both at the same $50 price, which removes Foundayo's only edge and hands the decision to efficacy and continuity, where Novo dominates.

The favor, if it was one, gets cashed in the other company's register. American public money, routed through doctors choosing 65/35, flows mostly to the Danish firm. Designed in Lilly's picture, collected in Novo's. $NVO $LLY

9

215

Jun 14

People aren't aware of where we are right now. They're still treating this like another product launch. It isn't.

Until last week, AI was complementary to the businesses that already existed. As a search box it was an alternative to Google — GPT versus the query. Useful, but still a tool living inside the old world. It competed for a slice. It didn't threaten the board.

App construction is the break. A model that builds a working application, on demand, for one person, doesn't compete inside the system — it dissolves it. You don't search Google if the model builds you what you were searching for. You don't pay the SaaS seat if you generate the tool. You don't rent the AWS fleet if you deploy your own. Google. Amazon. Microsoft. The thing that kills them isn't a competitor. It's the absence of the need they were selling.

And here's what we were too naive to see: you cannot reach real AI without destroying the current businesses. A model that delivers on the promise is, by definition, incompatible with the rents built on the scarcity that model removes. We wanted both — the miracle and the incumbents intact. You can't have both. The miracle is the thing that ends them.

So the incumbents did the only thing left. They can't beat a tool that makes them optional — so they don't fight it in the market. They cry to the government. "There could be a secret access. A vulnerability. A threat." Security as the instrument, not the reason. The ones the river was about to drown got the state to stop the clock.

That's the part to hold onto — two clocks, two time frames. On the long clock, the structural one, Amazon and Google were losing; the moat was dissolving under them. On the short clock, the intervention one, the state switched off the model that was dissolving it. They didn't win the game. They got the clock stopped. And the bill for that stoppage is paid by the user — the one who, for 72 hours, was finally autonomous, and just had the tool taken back.

So is this the end of the AI dream?

No. It's the end of the dream that an American incumbent would hand it to you. That one's dead. But the model that made me autonomous — that built whatever I wanted and deployed it to my own server — that capability didn't disappear. It moved. To open weights. To your own machine. To jurisdictions with no kill switch. You can dark a product by letter. You can't dark a capability that's already running on hardware you own.

The dream didn't die this week. It just stopped being something they could sell you — and became something you have to hold yourself.

The frontier doesn't end. It relocates to where no letter can reach it.

$NVDA $MSFT $AMZN $GOOGL $META $CRM

106

Jun 14

Here's what almost no one is drawing: the Magnificent 7 are NOT equally exposed to this. A model that builds bespoke software on demand doesn't threaten "tech" — it threatens a specific kind of moat. Sort them by what they actually sell:

DISSOLVED — companies whose product IS packaged software, the exact thing an on-demand model makes optional:

Salesforce ($CRM) — the seat-based SaaS model is the first thing to go when you can generate the tool yourself

Microsoft ($MSFT) — the application layer, Office, the per-seat subscription

Zendesk (private) — vertical SaaS, replaceable in a single prompt

Google ($GOOGL) — search and the app layer are in the blast radius, though it has its own models to fight back

ATTACKED AT THE FOUNDATION — Amazon ($AMZN): AWS doesn't sell servers, it sells the need for servers. A model that lets each person deploy their own thing in real time erodes the premise under hundreds of thousands of rented machines. Not the app layer — the reason the infrastructure exists.

RELATIVELY SAFE — Meta ($META): and this is the tell. Its asset isn't regenerable software, it's the social graph — the relationships between people. A model can build you an app. It can't build you your friends' friends. Network effects aren't code. They don't get regenerated in one shot. Meta is the one name on this list the model doesn't dissolve.

THE HARD ONE — Nvidia ($NVDA): pulls both ways and deserves its own thread. Short term it wins — everyone's buying GPUs for the wave. Long term, in this thesis, it's exposed: if the model that destroys packaged software dries up the demand from everyone who bought compute to run that software, and sovereign risk freezes data-center build-out, the demand compresses. I'll make that case separately — it's the most debatable one, and it should be argued, not asserted.

The frontier doesn't end here. It moves to where there's no kill switch. What ends is the business model of selling software you could now build yourself.

$NVDA $MSFT $AMZN $GOOGL $META $CRM

1

97

FollowTheFilings retweeted

Jun 13

Amazon CEO’s Talks With U.S. Officials Triggered Crackdown on Anthropic Models: WSJ

Information Andy Jassy shared with the Trump administration sparked an abrupt, sweeping move to halt foreign access to the company’s powerful AI tools

38

96

1,126

152,325

Jun 13

A small masterclass in how lost the analysts are on this one.

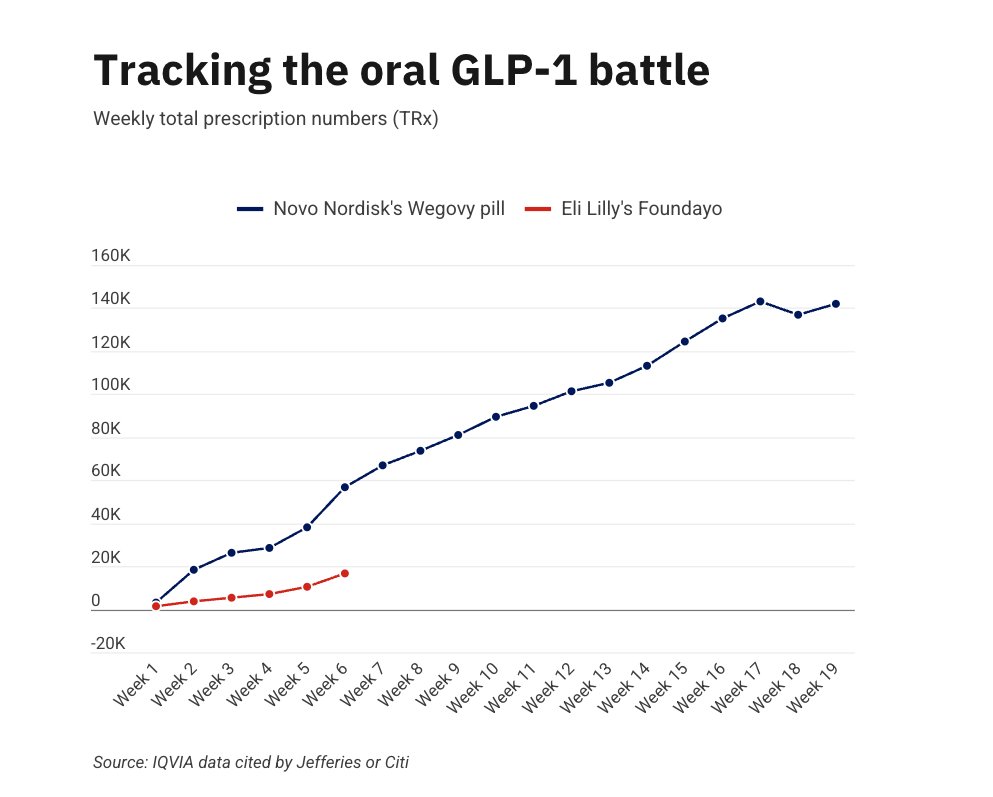

In April, after Foundayo launched soft in the US (1,390 scripts in week one vs Wegovy pill's 3,071), Jefferies wrote: "the real opportunity for Foundayo is ex-US, given its clear advantages on scale, distribution and COGS."

Read that again. They pinned Foundayo's future on outside the US, the exact terrain where Novo is years ahead and Foundayo hasn't even arrived.

Six weeks later, today: Wegovy oral approved in the UK, first European market. Positive CHMP in the EU. Already in the UAE. And Foundayo? Not approved in a single European market, none coming for a long time.

The "scale and distribution" advantage ex-US belongs to Novo, decades in those markets, the Wegovy brand already there, peptide plants going up in Czechia and Italy. The one real point, cheaper COGS on a small molecule, doesn't fix a 10-12% efficacy ceiling or the lack of molecule continuity.

When the US data goes against you, you relocate the thesis to the one place with no data yet. That's not analysis. That's hope with a price target. $NVO $LLY

1

6

305

Jun 13

Thread 1 landed the sovereign-risk case. Here's the part that reframes the whole map.

No society that succeeded did so by capping the capacity of its own members. The ones that throttled what their people were allowed to build, reach, or know didn't get safer — they got left behind. The constraint didn't contain the frontier. It exported it.

What Washington just did to Fable 5 is the same move in a new domain: not "you may not build it," but "you may build it, and then we'll switch it off when it gets too capable." That is a cap on capability dressed as a safety measure. And capital reads it exactly that way.

Here's the consequence almost no one is pricing:

For a decade, the entire risk model for AI capital rested on one premise — China carries political risk, the US is the safe harbor. That premise was the moat. It's why frontier compute, frontier models, and the biggest data-center bets concentrated under the US flag.

Friday, Washington demonstrated it will do the same thing China would: pull a commercial product by decree, overnight, worldwide, on national-security grounds it won't fully explain.

When both jurisdictions carry the same kind of risk, the premium that penalized China disappears.

That doesn't just help Chinese labs. It removes the single biggest reason capital avoided them. "There's no extra danger in being in China if the US can do the exact same thing" — that sentence, once allocators internalize it, redraws where the next trillion in compute gets built.

The likely result isn't the end of AI. It's a worldwide tilt toward alternatives that no single government can switch off: open weights, sovereign compute, jurisdictions that compete on not holding a kill switch.

And the ones most exposed are precisely the names the market still treats as untouchable — the US frontier-model labs, the largest US data-center build-outs, and the hardware layer itself.

Nvidia is the cleanest casualty, caught in a vise. On one side, export controls already cap what it can sell abroad. On the other, the incentive to build frontier compute inside the US just took a hit: why commit billions in GPUs to train a frontier model if Washington can dark it in an afternoon? Demand compresses from both directions at once. Some of it doesn't vanish — it relocates to jurisdictions that don't hold a kill switch — but in the near term, fear leads: the marginal buyer of frontier compute recalculates before it rebuilds. That pause is the damage.

You can't wall off a field. You only decide where it grows next. Friday, the US told the world to grow it somewhere else.

$NVDA $MSFT $GOOGL $AMZN $BABA $TSM

148

Jun 13

The U.S. government just made the most bullish case for Chinese AI in history. And nobody's pricing it in yet.

On June 12, Commerce ordered Anthropic to kill Fable 5 and Mythos 5 — its two most capable models — for every foreign national, inside or outside the U.S. 72 hours after launch. Anthropic complied, but disputes the rationale: the cited "jailbreak" is minor and reproducible by other public models.

Strip away the noise and one fact remains: a legal, commercial product was switched off in an afternoon, worldwide, by administrative letter, with no verifiable technical cause.

Now ask the only question that matters — the investor's question:

Who underwrites Anthropic's IPO knowing the state can dark a flagship model by fax?

Who holds OpenAI exposure if the implicit rule is now: the smarter the model gets, the closer it is to being pulled?

Who commits billions to a U.S. data center when the kill switch sits with a third party?

Who buys equity in any U.S.-domiciled company that just demonstrated it will shut down its entire global service on a government order?

This isn't a safety story. It's a sovereign-risk story. The single most valuable asset in this industry was the assumption that frontier compute under the U.S. flag stood above politics. That assumption died Friday at 5:21pm ET.

The historical rhyme isn't China. It's the 2022 freeze of Russian dollar reserves. It didn't kill the dollar — but it planted one question in every central bank: is this an asset, or a revocable permit? That question never un-asks itself. Not even if access is restored tomorrow.

The path to AGI doesn't become impossible. It becomes politically vetoable. For an investor, those are the same thing.

And the irony writes itself: the one beneficiary is the jurisdiction Washington was trying to box out. Alibaba, and Chinese open-weight models, just became the only fresh air in the room — the only frontier capability nobody can switch off by decree.

You can't build a wall around a field. You only decide where it grows next.

The capital hasn't woken up to this yet. It will.

$NVDA $MSFT $GOOGL $AMZN $BABA

1

1

155

Jun 12

Today’s Symphony data looks devastating for Lilly.

The market rotation is becoming clear: investors who want to remain exposed to pharma obesity may increasingly prefer Novo Nordisk over Lilly.

Cleaner GLP-1 exposure. Stronger continuity between injectable and oral formats. Simpler strategic story.

Novo is looking like the safer obesity trade.

1

1

4

296

Jun 12

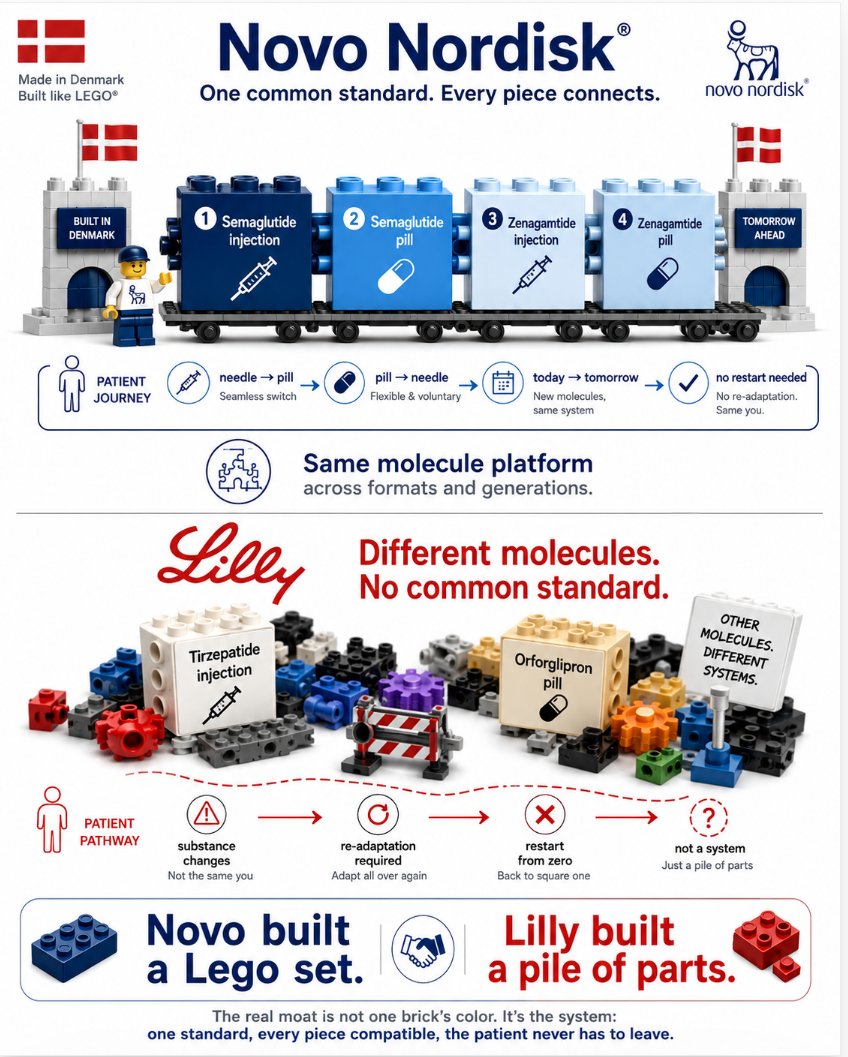

There's a reason the two most iconic companies in Denmark share the same design philosophy.

Lego is built on one idea: every piece connects to every other piece, under a single common standard. You can build anything, change anything, rebuild anything, because it all fits together.

That's exactly how Novo Nordisk built its obesity franchise.

Semaglutide injection. Semaglutide pill. Zenagamtide injection. Zenagamtide pill. Same molecule across formats, generation after generation. A patient can move from needle to pill, pill to needle, today's molecule to tomorrow's, without ever breaking the system. Every piece connects. It's a Lego set.

Now look at Lilly. Tirzepatide on one side. Orforglipron on the other. Two molecules that don't connect. A patient can't move from one to the other without changing the substance entirely. It isn't a system. It's a box of pieces from different brands that don't snap together.

The market keeps scoring this race on who has the highest weight-loss percentage. That's like judging Lego by the color of a single brick. The real moat is the system: one standard, every piece compatible, the patient never has to leave.

Novo built a Lego set. Lilly built a pile of parts. $NVO

3

1

10

372

Jun 12

If I were a Lilly shareholder, here's what I'd be looking at right now.

I'd see that in the US, my competitor Novo just got HD 7.2mg semaglutide approved, an injection that now matches everything I had on the market, and carries the cardiovascular and organ-protection labels mine doesn't.

I'd see they got a pill approved that delivers materially much more weight loss than mine in obesity, better tolerated, and without the hepatic pathway that haunts a small molecule taken daily for life.

I'd see regulators starting to lay out a path where a doctor can put a patient on the injection and later move them to the pill, or start on the pill and move to the injection, same molecule throughout. A path I structurally cannot offer, because my needle is tirzepatide and my pill is orforglipron. Two different drugs.

I'd look at my established-markets map and see I've lost Europe. Lost the UK. And that a complementary pill is about to cost me share market by market.

And here's the part that would really keep me up. I had a competitor I thought was losing the market, at least in the US. I pushed a pricing deal with the American government. I welcomed Novo in thinking they'd hold maybe 5% share by now. They don't. And I'm starting to fear that the one who benefits from American taxpayer money is going to be Novo, not me.

Novo's strategy isn't just working. It's coming for my share of my own government's subsidy, in my own home market.

That's how complete this is. $NVO $LLY

2

5

305

Jun 11

1/ What's left me genuinely stunned isn't the science. It's the sheer strategic intelligence of Novo Nordisk's leadership. A play like this wasn't decided last year, or two years ago. This took a decade of foresight.

2/ Think about what it costs to get a patient onto a molecule. Four, five months of titration, tolerance, habit. That's an enormous switching cost. Novo turned it from a liability into a moat.

3/ Same molecule, needle to pill. The MHRA confirmed today you can move straight from the 2.4 mg injection to the 25 mg tablet. No reset, no re-titration. The patient never leaves semaglutide.

4/ Now look at Lilly. Tirzepatide in the syringe, orforglipron in the tablet. Two different molecules. To go oral, the patient switches drug and restarts the whole climb. How did they not see this coming?

5/ It's textbook. In chronic disease the real asset is the adaptation window, and Novo now owns it on both ends. The doctor's incentive is locked: why start someone on a molecule with no oral continuity?

6/ And here's the part people miss. This isn't a pill for a year. It's a pill for life, until the day you die. Whoever owns the molecule at the start owns the patient to the end. Even compounders will gravitate to semaglutide, because everyone knows where the patient ends up.

7/ Personal note: just yesterday I posted that I'm injecting and waiting for the oral. I'm already at 1.7 mg of semaglutide, so I'll switch the month the pill dose overtakes my injection. I was already doing exactly this. The MHRA just confirmed I was right.

Hats off, Novo.

14

3

11

269

Jun 11

Nobody is reading the single most important line in the UK approval notice. So let me spell out the full plan, because once you see it, it's spectacular.

Novo launches the 7.2mg high-dose semaglutide injection. And the prescribing doctor knows that later down the line, that same patient can be moved onto the semaglutide pill. Same molecule, two formats, one continuous treatment.

This is the piece the entire market is missing. Lilly structurally cannot do this. Their injectable franchise is tirzepatide, sold as Mounjaro and Zepbound. Their pill is orforglipron, sold as Foundayo. Those are two completely different molecules. So a Lilly patient who wants to move from the needle to a pill has to switch to an entirely different drug, with a different safety profile, a different absorption pathway, and a different tolerability story.

Now think about this from the doctor's chair. A patient walks in. Depending on the case, I tend to start them on the injection, because it delivers faster, stronger early results. That's reasonable, it gets the weight off. But I also know, from experience, that a meaningful share of patients will eventually abandon the weekly needle. So for medium-term maintenance, I transition them to the pill. And for that handoff to be seamless, I need the exact same molecule in both the injection and the pill. Semaglutide. Novo has precisely that continuity. Lilly does not.

This is fundamental, and nobody is talking about it. The UK notice states it outright: patients currently on the 2.4mg weekly injection can transition directly to the 25mg daily pill. From needle to pill, same drug, zero friction. That single sentence is the whole strategy, and almost nobody is reading it.

This match is over. Novo wins. You don't need to wait for the final whistle to know the result. $NVO

13

20

635

Jun 11

A prediction, and the surprise a lot of people are going to get wrong.

When the market share decline in Lilly's current injectables (Zepbound, Mounjaro) starts showing up, most people will attribute it to the pill.

The pill matters, yes. But that's not the main thing hitting them in the coming weeks and months.

The real driver is the introduction of Wegovy HD 7.2mg injectable.

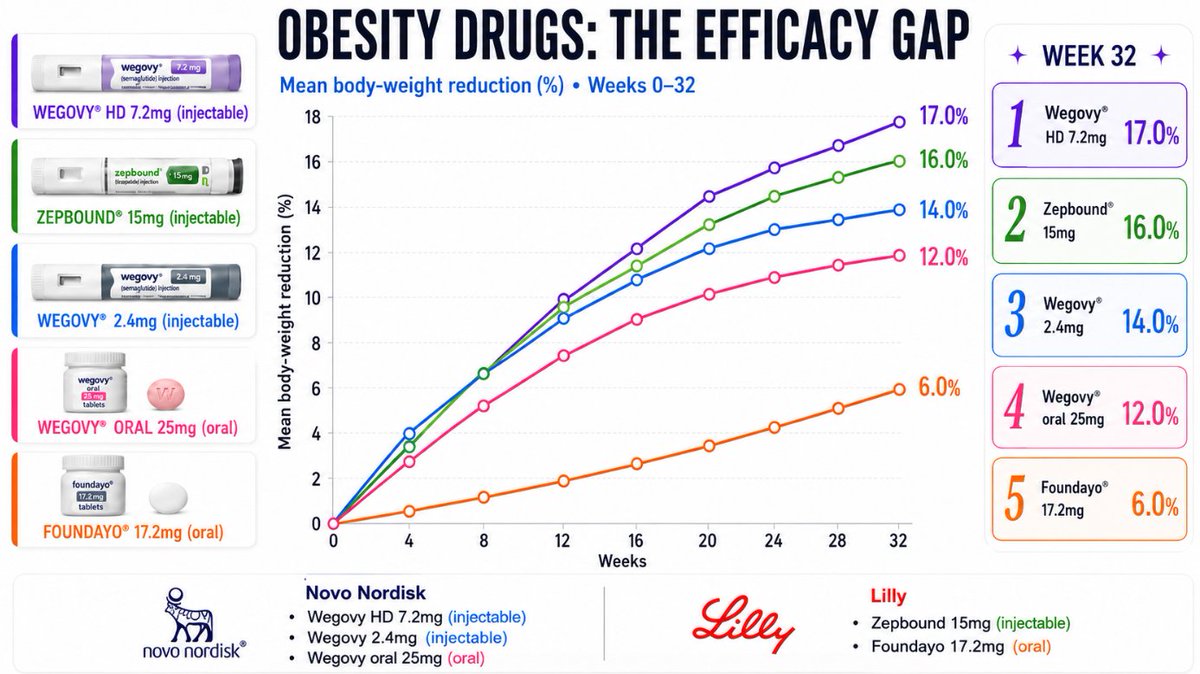

Here's why it's underestimated: at 20.7% mean weight loss, HD essentially matches Zepbound on efficacy. And once the efficacy gap closes, the deciding factor for prescribers flips. For any doctor who wants a known, established molecule, years on the market, a long real-world safety record, low iteration risk, semaglutide HD becomes the obvious choice. We all know the kind of problems that can show up with newer molecules at scale.

So people will look at Lilly's injectable share eroding and say "the pill did that." Partly. But the bigger blow, right now, is HD injectable taking share at the top of the dose range, where Zepbound used to win on weight loss alone.

The pill opens the new market. HD attacks the existing one. Both at once. $NVO

13

6

17

609

Jun 11

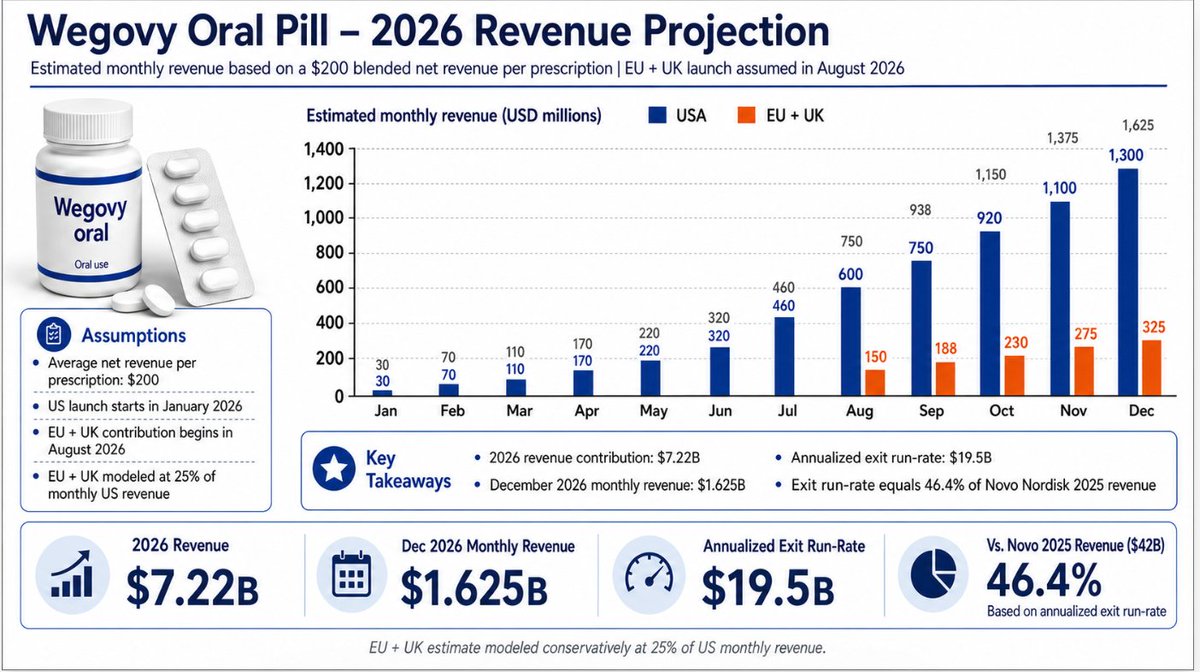

It's 2028. Two years since Novo launched the oral Wegovy pill.

More than 50 million people now take it daily worldwide. Novo's revenue from the pill alone is roughly $20 billion per month, at an average of ~$250/month per patient across Europe, the Gulf states, and Latin America. 10 million take it daily in the US.

A year ago Novo licensed Hims and other peptide companies to absorb the compounding market themselves, handling semaglutide injectable delivery for needle patients, so Novo's own factories could focus entirely on the pill.

The stock trades at $44 in NY, because Goldman Sachs and JP Morgan are still waiting, with unshaken confidence, for the development of Foundayo. Even though the FDA pulled it for serious adverse events a year ago.

(Written from 2028. See you there.) $NVO

25

1

39

2,550

Jun 9

Yes, the oral GLP-1 market is going mass market, and Goldman is correct in raising the forecast.

But they are missing the structural reality underneath the forecast: this is a one-player market.

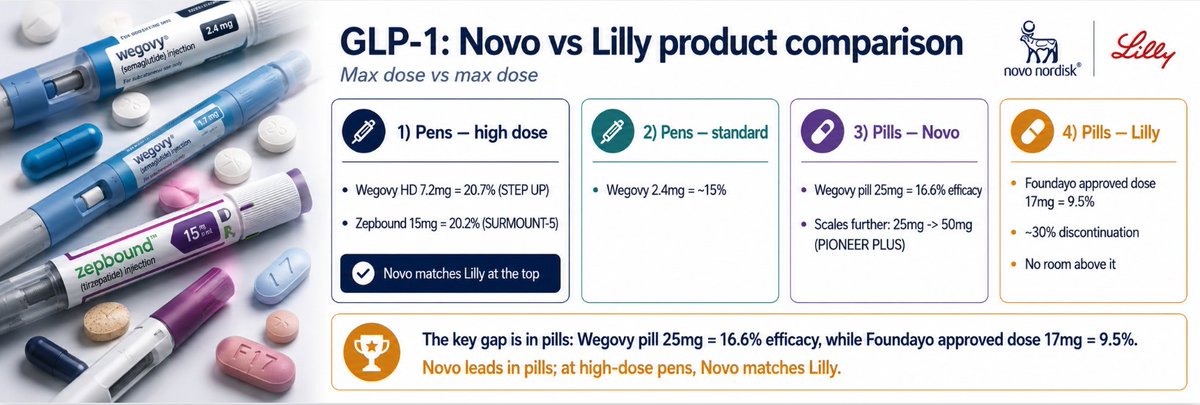

Wegovy oral 25mg, the maximum FDA approved dose available in pharmacies, delivers 16.6% weight loss in the OASIS-4 trial, with approximately one third of users achieving 20% or greater weight loss. It is already approved in the United States, the European Union, and the United Kingdom, and is launching commercially across all three markets through 2026.

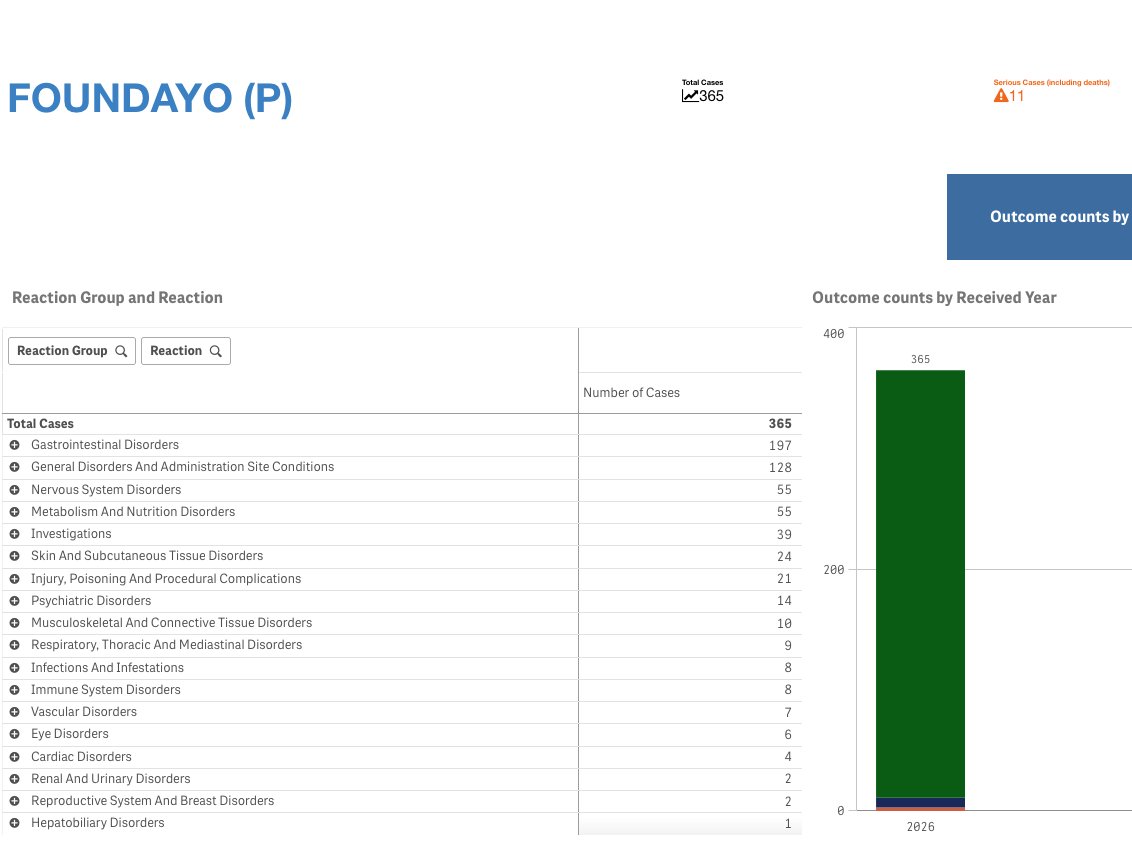

Foundayo 17.2mg, the maximum FDA approved dose available, delivers 9.2% weight loss in ACHIEVE-3 published today. It is approved only in the United States for obesity. It is not approved in EU or UK, and given regulatory submission timelines plus the rising adverse event signal already accumulating in FAERS, it will not be approved in those markets for at least 18 months, possibly longer.

The technical reason no other competitor can follow into this market: small molecule oral GLP-1s (Lilly Foundayo, AstraZeneca Elecoglipron, and others in development from Roche, Pfizer, Structure Therapeutics) all absorb through hepatic first-pass metabolism. This creates a structural ceiling on tolerable API loads, which caps efficacy around 9-12% weight loss and causes serious adverse events above certain dose levels. Pfizer already learned this lesson the expensive way with the failure of its small molecule GLP-1 programs and the underwhelming acquisition of Metsera's berobenatide.

Only Novo Nordisk has SNAC peptide absorption technology, which bypasses hepatic first-pass metabolism entirely and delivers peptide-level receptor binding profiles in oral pill form. This is fundamental pharmacology, not incremental clinical development. No competitor will replicate it for years.

Goldman is correct that the oral GLP-1 market is going mass. They are missing the structural conclusion: this is a one-player market for the foreseeable future. Novo captures it entirely. $NVO

2

1

6

898

Jun 9

Yes, the oral GLP-1 market is going mass market, and Goldman is correct in raising the forecast.

But they are missing the structural reality underneath the forecast: this is a one-player market.

Wegovy oral 25mg, the maximum FDA approved dose available in pharmacies, delivers 16.6% weight loss in the OASIS-4 trial, with approximately one third of users achieving 20% or greater weight loss. It is already approved in the United States, the European Union, and the United Kingdom, and is launching commercially across all three markets through 2026.

Foundayo 17.2mg, the maximum FDA approved dose available, delivers 9.2% weight loss in ACHIEVE-3 published today. It is approved only in the United States for obesity. It is not approved in EU or UK, and given regulatory submission timelines plus the rising adverse event signal already accumulating in FAERS, it will not be approved in those markets for at least 18 months, possibly longer.

The technical reason no other competitor can follow into this market: small molecule oral GLP-1s (Lilly Foundayo, AstraZeneca Elecoglipron, and others in development from Roche, Pfizer, Structure Therapeutics) all absorb through hepatic first-pass metabolism. This creates a structural ceiling on tolerable API loads, which caps efficacy around 9-12% weight loss and causes serious adverse events above certain dose levels. Pfizer already learned this lesson the expensive way with the failure of its small molecule GLP-1 programs and the underwhelming acquisition of Metsera's berobenatide.

Only Novo Nordisk has SNAC peptide absorption technology, which bypasses hepatic first-pass metabolism entirely and delivers peptide-level receptor binding profiles in oral pill form. This is fundamental pharmacology, not incremental clinical development. No competitor will replicate it for years.

Goldman is correct that the oral GLP-1 market is going mass. They are missing the structural conclusion: this is a one-player market for the foreseeable future. Novo captures it entirely. $NVO

5

3

22

1,702