Oil: $WTI ▼>4% to $75/bbl, extending its losing streak to 4 sessions & hitting its lowest level since Mar as traders bet a US-Iran deal will restore Strait of Hormuz supply flows. $GOOG 1.5% after unveiling a $1.5bn Alabama data centre expansion through 2027. ACFview

ACFMarketWrap: Dow hits fresh records while AI trade cools: Markets continued to digest the US-Iran peace agreement, with expectations that the Strait of Hormuz will reopen helping ease inflation fears, push bond yields lower and support risk sentiment ahead of the Fed decision. The Dow surged 400 points to a record high, but profit-taking across AI infrastructure and semiconductor names dragged the Nasdaq -0.49% and left the S&P 500 hovering around flat.

Chip stocks led the retreat, with $AVGO, $MU, $AMD and $INTC falling by as much as 6%. Financials provided support as $JPM ( 3.2%) and $V ( 2.0%) advanced.

SpaceX ($SPCX ) ▲ another 8%, extending gains to 40% since its IPO on Friday after reports it will acquire Cursor in a $60bn deal.

The Mag 7 were mixed: $NVDA (-1.44%), $AMZN ( 0.91%), $META ( 0.38%), $GOOG ( 1.5%), $AAPL ( 0.39%), $MSFT (-1.61%) and $TSLA (-1.13%). FTSE 100 0.6%, $WTI $75.2/bbl.

Next in focus: API Crude Oil Stock Change & UK Inflation Rate y/y. ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

55

ACFMarketWrap: Dow hits fresh records while AI trade cools: Markets continued to digest the US-Iran peace agreement, with expectations that the Strait of Hormuz will reopen helping ease inflation fears, push bond yields lower and support risk sentiment ahead of the Fed decision. The Dow surged 400 points to a record high, but profit-taking across AI infrastructure and semiconductor names dragged the Nasdaq -0.49% and left the S&P 500 hovering around flat.

Chip stocks led the retreat, with $AVGO, $MU, $AMD and $INTC falling by as much as 6%. Financials provided support as $JPM ( 3.2%) and $V ( 2.0%) advanced.

SpaceX ($SPCX ) ▲ another 8%, extending gains to 40% since its IPO on Friday after reports it will acquire Cursor in a $60bn deal.

The Mag 7 were mixed: $NVDA (-1.44%), $AMZN ( 0.91%), $META ( 0.38%), $GOOG ( 1.5%), $AAPL ( 0.39%), $MSFT (-1.61%) and $TSLA (-1.13%). FTSE 100 0.6%, $WTI $75.2/bbl.

Next in focus: API Crude Oil Stock Change & UK Inflation Rate y/y. ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

7

10

712

ACFMorningMeeting - A-Page-and-a-Half - This is the apparent length of the solution to Iran and Hormuz agreed with the USA. Perhaps there is still more work to be done? Perhaps shipping costs (insurance et al) will 'never' return to normal? The market has priced the US-Iran deal fast, but shipping through Hormuz is still not normal, oil is below $83 bbl not back to boring, and Europe opens cautious but positive after Monday’s record relief rally. SpaceX $SPCX keeps sucking oxygen from everything else, while Nvidia $NVDA throwing $25bn at the bond market says AI still needs funding, not just faith.

Opens - Europe / UK - flat to slightly softer indicated. USA ftrs mixed after record highs. Asia mixed: Japan hikes to 1%, Korea firm, Hong Kong hit by weak China retail sales. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - SpaceX $SPCX remains the market circus after its post-IPO surge, ( 10% in this morning's grey market) and coming index flows. it is Nvidia $NVDA bond sale is the AI-capex tell. SoftBank $SFTBY steady despite Vision Fund CFO exit. Airlines and consumers keep the oil-relief bid; energy loses the war premium. $TSLA $GOOG $EZJ.L $IAG.L $SHEL.L $BP.L

Commods - Brent $82.6 bbl, WTI $80.4 bbl, GOLD $4,324 toz. COPPER $6.43 lb. COCOA high-$3k MT, still a reset trade.

Data Focus - German ZEW today; Fed and BoE this week. The market question is simple: is this peace tradable, or just another headline with a signature still missing? ACFView.

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

8

11

351

Oil crashes as peace deal nears: $WTI ▼ >5% to ~$80/bbl, a 2-mth low, after US and Iran agreed a deal to reopen the Strait of Hormuz and restore Gulf oil flows. Meanwhile, $META 5.89% as investors weighed its $14bn AI push against growing pressure to deliver returns. ACFview

Jun 15

ACFMarketWrap: Peace deal sparks risk-on rally - Global markets surged after the US and Iran agreed a deal to end the conflict and restore Persian Gulf energy exports, with the agreement reportedly set to be signed Friday. Lower oil prices and bond yields fuelled a rush into growth stocks, sending the S&P 500 1.5%, the Nasdaq 2.99% and the Dow 1%. AI and tech led the charge as $NVDA ( 3.4%), $AMZN ( 3.06%), $META ( 5.89%), $GOOG ( 3.18%), $AAPL ( 2.01%), $MSFT ( 2.53%) and $TSLA ( 1.03%) all advanced, while $ORCL gained around 3%.

Newly listed SpaceX ($SPCX) climbed another 10% after soaring 20% on its IPO debut, helped by Elon Musk's projection of potential $1trn revenue by 2031. AI infrastructure and semiconductor names extended gains as fresh capital flows into the sector continued to drive demand expectations. Defensive sectors lagged, with $JNJ falling 2.5%.

In Europe, the Euro STOXX 50 hit a record 6,236 ( 0.8%) and the STOXX 600 rose 0.3% as easing energy risks and lower rate expectations boosted sentiment. Banks led the rally, with $SAN, $DBK and $BBVA gaining between 3%-4.56%, while industrials benefited from lower energy costs, including $SAF ( 3.5%) and $SIE ( 2.2%).

The FTSE 100 bucked the trend, slipping 0.3% as energy majors $SHEL (-4.4%) and $BP (-3.4%) tracked falling crude prices. Healthcare and defence names also weakened, including $AZN (-1.7%), $GSK (-1.0%), $BA (-4.6%) and $BAB (-1.1%). Miners shone as metals rallied, with $EDV and $FRES up nearly 7%, $ANTO 5%, and $AAL and $RIO both gaining over 1%. $WTI $80/bbl.

Next in focus: BoJ Interest Rate Decision. ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

3

3

186

Jun 15

ACFMarketWrap: Peace deal sparks risk-on rally - Global markets surged after the US and Iran agreed a deal to end the conflict and restore Persian Gulf energy exports, with the agreement reportedly set to be signed Friday. Lower oil prices and bond yields fuelled a rush into growth stocks, sending the S&P 500 1.5%, the Nasdaq 2.99% and the Dow 1%. AI and tech led the charge as $NVDA ( 3.4%), $AMZN ( 3.06%), $META ( 5.89%), $GOOG ( 3.18%), $AAPL ( 2.01%), $MSFT ( 2.53%) and $TSLA ( 1.03%) all advanced, while $ORCL gained around 3%.

Newly listed SpaceX ($SPCX) climbed another 10% after soaring 20% on its IPO debut, helped by Elon Musk's projection of potential $1trn revenue by 2031. AI infrastructure and semiconductor names extended gains as fresh capital flows into the sector continued to drive demand expectations. Defensive sectors lagged, with $JNJ falling 2.5%.

In Europe, the Euro STOXX 50 hit a record 6,236 ( 0.8%) and the STOXX 600 rose 0.3% as easing energy risks and lower rate expectations boosted sentiment. Banks led the rally, with $SAN, $DBK and $BBVA gaining between 3%-4.56%, while industrials benefited from lower energy costs, including $SAF ( 3.5%) and $SIE ( 2.2%).

The FTSE 100 bucked the trend, slipping 0.3% as energy majors $SHEL (-4.4%) and $BP (-3.4%) tracked falling crude prices. Healthcare and defence names also weakened, including $AZN (-1.7%), $GSK (-1.0%), $BA (-4.6%) and $BAB (-1.1%). Miners shone as metals rallied, with $EDV and $FRES up nearly 7%, $ANTO 5%, and $AAL and $RIO both gaining over 1%. $WTI $80/bbl.

Next in focus: BoJ Interest Rate Decision. ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

1

3

394

Jun 15

ACFMorningMeeting - Risk appetite is firmer at the London open, with Europe indicated higher, U.S. futures positive, Asia strong, and oil softer after the Iran peace headline; this is still a hope trade, not a done deal.

Opens - Europe / UK - sharply firmer. USA ftrs ve. Asia strong, led by Korea and Japan. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - BAE Systems $BA. in focus after the UK-Japan tech partnership and GCAP update, with aerospace/defence names firmer on the strategic backdrop. In the US, watch: $TSLA, $NVDA, $AAPL, $JPM and $CVX at the open for the main read-throughs on AI, megacap tech, financials and energy.

Commods - Brent $83.18 bbl, WTI $79.20 bbl, GOLD spot $4,327.46 toz. COPPER $6.52 lb. Oil is at a three-month low, copper is at a more than one-week high, and gold is up over 2%.

Data Focus - US Industrial Production: 0.7% MoM (May) vs 0.3% forecast. NY Empire State manufacturing also strong at 19.6. ACFView.

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

6

8

418

Jun 12

ACFMorningMeeting - Spaced Race. SpaceX $SPCX starts trading today after the biggest IPO ever, raising $75bn at $135/share and a $1.77trkn valuation, while Trump’s Iran peace-deal tease has crushed oil to two-month lows. Asia ripped, Europe opened strongly, and whilst this is still hope and SpaceX IPO excitement, it is not peace in the bank (yet, notwithstanding breaking news).

Opens - Europe / UK - sharpkly firmer indicated. USA ftrs ve after Wall St rally. Asia strong, led by Korea and Japan. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - SpaceX $SPCX is the market event. Tesla $TSLA and Alphabet $GOOG watch for read-across / ownership optics. AI and IPO animal spirits are alive, but flag rotation risk for yourself as investors make room for $SPCX. Healthcare still has a live UK angle: Spire $SPI deadline extended and GSK $GSK still digesting Nuvalent $NUVL.

Commods - Brent $88.3 bbl, WTI $85.8 bbl, GOLD spot $4,182 toz. COPPER $6.35 lb, still rich. COCOA $3,798 MT, still heavy.

Data Focus - UK GDP -0.1% in April, but 0.7% over three months, Keir Starmer UK defence credibility crisis, probably is the last stumble. Michigan sentiment later. Today’s real equation: SpaceX animal spirits plus oil relief versus whether the Iran deal is actually real. ACFView.

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

5

10

952

Jun 12

See @Mayhem4Markets repots below on SpaceX relative valuation, it is sobering - At the end of market fashion booms many companies lose around 98% of their value, the majority of which never recover much of that. It does not mean the boom does not deploy capital that changes the world, it just means that in that process a vast amount of capital is also completely wasted. ACFView

1

3

37

ECB turns hawkish again: ECB ▲rates 25bps, its 1st hike since 2023, citing Iran-driven energy inflation risks from Hormuz Strait disruptions.

Inflation frcsts ▲to 3.0% for 2026 & 2.3% for 2027. $INTC 9% on BofA upgrade to Buy & ▲ its price target to $135 from $96. ACFview

Jun 11

ACFMarketWrap: Markets shake off rate fears, but geopolitics keeps traders on edge - US equities bounced from one-month lows, with the S&P 500, Dow and Nasdaq ~( 0.45%) as strength in tech offset concerns over higher rates.

Fresh PPI data signalled accelerating price pressures in May, reinforcing expectations that the Fed could still hike this year, while President Trump said the US will resume strikes on Iran tonight and target Kharg Island, raising the stakes in the Middle East.

AI-linked infrastructure names remained resilient as anticipation builds ahead of the SpaceX IPO, highlighting continued hyperscalers’ spending on compute capacity. $INTC surged 9% after a BofA upgrade tied to strong CPU demand, while $ORCL tumbled 12% as investors reacted to plans for increased borrowing to fund data centre expansion despite flat sales. The Mag 7 were mixed: $TSLA ( 1.17%), $NVDA ( 0.15%), $AMZN (-0.34%), $GOOG (-2.38%), $META (-1.78%), $AAPL ( 0.01%) and $MSFT (-2.39%).

In Europe, investors digested escalating US-Iran tensions and an ECB rate hike @ 2.4% (vs 2.15% prev.) alongside higher inflation forecasts and weaker growth projections. $SAP (-4.5%) remained under pressure, $DTE.DE (-3.0%) on a potential combination with $TMUS ( 0.8%).

Energy and utilities outperformed, led by $ENR.DE ( 6.0%) and $BAYN.DE ( 1.19%). $SAP (-4.5%) remained under pressure, while chipmakers outperformed with $ASML ( 5%), $IFX.DE ( 2.6%) and $STM ( 5.9%) advancing on continued AI optimism. Luxury names also found buyers, with $MC ( 1.5%) higher and $BOSS.DE ( 9%) surging after major shareholder $FRAS.L launched a $2bn takeover bid. FTSE 100 0.7%

Next in focus: UK GDP ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

2

2

111

Jun 11

ACFMarketWrap: Markets shake off rate fears, but geopolitics keeps traders on edge - US equities bounced from one-month lows, with the S&P 500, Dow and Nasdaq ~( 0.45%) as strength in tech offset concerns over higher rates.

Fresh PPI data signalled accelerating price pressures in May, reinforcing expectations that the Fed could still hike this year, while President Trump said the US will resume strikes on Iran tonight and target Kharg Island, raising the stakes in the Middle East.

AI-linked infrastructure names remained resilient as anticipation builds ahead of the SpaceX IPO, highlighting continued hyperscalers’ spending on compute capacity. $INTC surged 9% after a BofA upgrade tied to strong CPU demand, while $ORCL tumbled 12% as investors reacted to plans for increased borrowing to fund data centre expansion despite flat sales. The Mag 7 were mixed: $TSLA ( 1.17%), $NVDA ( 0.15%), $AMZN (-0.34%), $GOOG (-2.38%), $META (-1.78%), $AAPL ( 0.01%) and $MSFT (-2.39%).

In Europe, investors digested escalating US-Iran tensions and an ECB rate hike @ 2.4% (vs 2.15% prev.) alongside higher inflation forecasts and weaker growth projections. $SAP (-4.5%) remained under pressure, $DTE.DE (-3.0%) on a potential combination with $TMUS ( 0.8%).

Energy and utilities outperformed, led by $ENR.DE ( 6.0%) and $BAYN.DE ( 1.19%). $SAP (-4.5%) remained under pressure, while chipmakers outperformed with $ASML ( 5%), $IFX.DE ( 2.6%) and $STM ( 5.9%) advancing on continued AI optimism. Luxury names also found buyers, with $MC ( 1.5%) higher and $BOSS.DE ( 9%) surging after major shareholder $FRAS.L launched a $2bn takeover bid. FTSE 100 0.7%

Next in focus: UK GDP ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

5

11

954

Jun 11

Defence - European Defence sector, an ACF favourite since Trump first made legitimate critiques on NATO kit and cash - What's to like at Defence Holdings $ALRT.L?

It is a UK-based software-led platform for modern warfare/defence (not tanks) which is software, AI, digital infrastructure. $ALRT key activities include AI-driven military intelligence, Cybersecurity, Autonomous systems / drone tech, power grid protection, telecoms and ports protection.

So its 'miltech' without a silly Lord of the Rings like boy-in-bedroom name $PLTR Anduril. So quite a lot to generate interest/worthy of further research in $ALRT. ACFView

Defence Holdings is today, proud to announce a partnership with @Oracle in support of the Defence Holdings Accelerator Programme.

Under the partnership, Oracle will serve as the programme's hyper scale cloud partner.

#ALRT

$ALRDF

🧵

1

3

146

Inflation reaccelerates: US May CPI ▲ to 4.2% y/y (vs 3.8%), the highest since Apr-23, driven by energy ( 23.5%) as Iran-related supply shocks pushed gasoline up 40.5%. Core CPI ▲to 2.9% y/y, but ▲ just 0.2% m/m. $AMZN -1.51% expands LTL shipping. ACFview

Jun 10

ACFMarketMeeting: Risk-off tone grips markets - AI valuation concerns sparked another wave of selling across tech, pushing US and European equities lower as investors weighed softer-than-feared inflation data against rising oil prices and escalating US-Iran tensions.

The S&P 500 ▼ 0.89%, the Nasdaq ▼ 1.35% and the Dow ▼280 points, with $NVDA (-2.4%), $AVGO (-3.9%), $MU (-3.5%) and $ORCL (-2.4%) among the notable laggards. The Mag 7 were broadly weaker, with $TSLA (-2.96%), $AMZN (-1.81%), $GOOG (-0.34%), $META (-1.33%), $AAPL (-0.13%) and $MSFT (-0.11%) all trading in the red.

While May CPI ▲ 4.2% y/y as expct and core CPI ▲ just 0.2% m/m, helping ease concerns that higher energy costs are spreading through the economy, markets continue to fully price in a 25bp Fed rate hike in December.

In Germany, the DAX ▼ below 24,270 to its lowest level since mid-May, led lower by $SAP (-5.0%), while $DTE ( 1.4%), $FRE ( 1.4%) and $ADS ( 1.3%) bucked the trend.

Energy stocks outperformed as $WTI climbed to $90.34/bbl following a larger-than-expected 7.228m barrel draw in US crude inventories, extending a seven-week streak of declines.

FTSE 100 0.27%.

Next in focus: ECB Interest Rate Decision📈 ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

79

Jun 10

ACFMarketMeeting: Risk-off tone grips markets - AI valuation concerns sparked another wave of selling across tech, pushing US and European equities lower as investors weighed softer-than-feared inflation data against rising oil prices and escalating US-Iran tensions.

The S&P 500 ▼ 0.89%, the Nasdaq ▼ 1.35% and the Dow ▼280 points, with $NVDA (-2.4%), $AVGO (-3.9%), $MU (-3.5%) and $ORCL (-2.4%) among the notable laggards. The Mag 7 were broadly weaker, with $TSLA (-2.96%), $AMZN (-1.81%), $GOOG (-0.34%), $META (-1.33%), $AAPL (-0.13%) and $MSFT (-0.11%) all trading in the red.

While May CPI ▲ 4.2% y/y as expct and core CPI ▲ just 0.2% m/m, helping ease concerns that higher energy costs are spreading through the economy, markets continue to fully price in a 25bp Fed rate hike in December.

In Germany, the DAX ▼ below 24,270 to its lowest level since mid-May, led lower by $SAP (-5.0%), while $DTE ( 1.4%), $FRE ( 1.4%) and $ADS ( 1.3%) bucked the trend.

Energy stocks outperformed as $WTI climbed to $90.34/bbl following a larger-than-expected 7.228m barrel draw in US crude inventories, extending a seven-week streak of declines.

FTSE 100 0.27%.

Next in focus: ECB Interest Rate Decision📈 ACFview

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

5

10

556

Jun 10

ACFMorningMeeting - 'Now you see it...no you don't' - Global magic show hides the peace rabbit again. Fresh U.S.-Iran strikes push oil back up, Asia takes another bruising, and Europe opens into a market that wants less risk, more liquidity and fewer 'promises'. AI is still able to pose as a long-term bid, but this morning geopolitics is naturally enough the dominant part of the tape's equation.

Opens - Europe / UK - weaker tone. USA ftrs softer. Asia hit hard, led by Korea and tech. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - Watch the AI complex for whether buyers defend the theme after another ugly Asia session. In Europe, banks and defensives may hold up better than cyclicals if the oil/dollar squeeze persists. Healthcare stays live in the wake and wash of the GSK $GSK’s $10bn cash Nuvalent $NUVL deal put pipeline M&A back on the screen. $NVDA $AMD $TSM $ASML $GSK

Commods - Brent $92.1 bbl, $WTI $88.8 bbl, GOLD $4,205 toz. COPPER $6.2 lb area, still rich but off the highs. COCOA around $3.7k MT, still a reset trade not a squeeze trade.

Data Focus - U.S. CPI is the next macro hurdle, but today the market is trading strikes, stockpiles and whether Hormuz gets any closer to normal. ACFView

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

4

9

736

US trade deficit ▼ to $55.9bn, beating frcsts as record exports ($327.1bn) were driven by capital goods, energy and consumer products, while imports hit a 1-yr high on demand for chips, computers telecom equipment; $TSLA -4.57% despite $SPACEX IPO and merger chatter. ACFview

Jun 9

ACFMarketMeeting: AI revival meets reality check: $SPX, $NDX and $DJI 0.6% as easing Middle East tensions send WTI to $88.88/bbl and support Treasuries ahead of CPI, while OpenAI’s reported confidential IPO filing and fresh funding for Anthropic keep AI spending expectations elevated with $NVDA 1% , $MU 4% and $ORCL 1% extending their rebound;

Europe reversed lower as a rotation out of tech hit AI-linked names $IFX, $SAP, $SU and $ENR (-2% to -5.5%), while banks softened ahead of the ECB with $SAN, $ING and $NDA -1%;

the FTSE 100 fell >1% to a 3-week low as $HSBA -4%, $STAN -5%, $SHEL -1.8%, $BP -2.6%, $AZN -1.1% and $GSK -0.3% weighed, with $BT.A -3% on TalkTalk bid reports, though $WPP 5% jumped on an upgrade and UK retail sales surprised to the upside ( 3.4% vs 0.8% est.);

Mag 7 tumble: $TSLA -4.57%, $AMZN -1.39%, $GOOG -0.65%, $META -0.22%, $AAPL -3.86% and $MSFT -2.72% lag;

Nasdaq -2.6%, FTSE100 -1.4%;

Next in focus: ECB President Lagarde Speech & API Crude Oil Stock Change📈

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

1

75

Jun 9

ACFMorningMeeting - eMerging Medicine - Europe opens steady after Iran and Israel pause attacks, oil gives back some of yesterday’s jump, and the AI trade is back and whilst there keeness it is not quite the swagger of previous days. The twist this morning is healthcare: GSK $GSK has gone all guns for oncologist biotech Nuvalent in a $10.5bn agreed cash deal and reminded the market that pipeline M&A is still very much alive.

Opens - Europe / UK - steady to slightly firmer under the surface. USA ftrs mixed. Asia bounced, with AI and tech finding buyers again. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC KS200 9%.

Stock Watch - Healthcare and tech are the live tells. GSK $GSK fell (obviously) after agreeing the US$10.6bn Nuvalent cash deal, while UBS $UBS is firmer on softer Swiss capital fears. Tech is back in demand after yesterday’s AI wobble. $NVDA $AMD $TSM $ASML

Commods - Brent $93.1 bbl, $WTI $90.0 bbl, GOLD ftrs $4,350 toz. COPPER $6.3 lb area, still rich but calmer. COCOA $3,831 MT, still heavy.

Data Focus - ECB hike expectations remain in play on Thursday, today China exports, Germany BoT and USA existing home sales. But today the market is trading ceasefire credibility, Hormuz access and whether this AI rebound has real legs.

ACFView

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

1

3

228

$MRVL steals the spotlight ( 14%) after securing a spot in $SPX, extending a blistering run of 230% YTD and 450% over 5 yrs as AI infrastructure demand fuels momentum; WTI eases to ~$91/bbl on renewed US-Iran ceasefire hopes, higher OPEC output and softer CN imports. ACFview

Jun 8

ACFMarketWrap. Risk-on returns as Middle East tensions cool and AI buyers step back in: $SPX 0.8%, $NDX 1.5% and $DJI 0.4% climb as Iran signals its military operation against Israel has ended and Trump strikes an optimistic tone on negotiations, easing pressure on oil (WTI $91.82/bbl) and yields;

Chip stocks rebound after last week’s $AVGO-led selloff with $NVDA 1.83%, $MU 4% , $MRVL 14% on its S&P 500 inclusion, while $ORCL 2% rises into a key earnings report that could test AI infrastructure demand;

Mag 7 mostly green with $AAPL 2.36%, $TSLA 3.17%, $AMZN 0.59%, while $GOOG -1.42%, $META -0.41% and $MSFT -0.9% lag;

Nasdaq 1.7%, FTSE100 -0.06%;

Next in focus: Germany Balance of Trade

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

2

158

Jun 8

ACFMorningMeeting - Space the Final IPO Frontier - Europe opens on the back foot as Israel and Iran trade fire again, oil jumps, and the AI unwind spills from Wall Street into Asia and now Europe. SpaceX formal marketing has started this week as the date appears to have been set for 12 June 26 and pricing the day before.

Opens - Europe / UK - weaker. USA ftrs softer. Asia ugly led by Korea's KS200 down -8.5% and tech. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - Europe has real pain in cyclicals and tech: Lufthansa $LHA.DE and Air France-KLM $AF.PA are hit by oil, while Infineon $IXF.DE, BE Semiconductor $BSI.DE, Legrand $LR.PA and Schneider Electric $SU.PA all feel the AI wobble. Monte dei Paschi is the outlier on M&A after Intesa’s $ISP.MI bid. ut Today’s tape is uncomplicated: oil up, AI down, dollar up, nerves up.

Commods - Brent $97.2 bbl, $WTI $94.6 bbl, GOLD $4,316 toz. COPPER $6.27 lb, still expensive but cooling. COCOA $3,762 MT, still heavy.

Data Focus - ECB this week, U.S. CPI ahead, and SpaceX IPO still waiting in the wings. ACFView

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

1

7

10

1,099

Jun 4

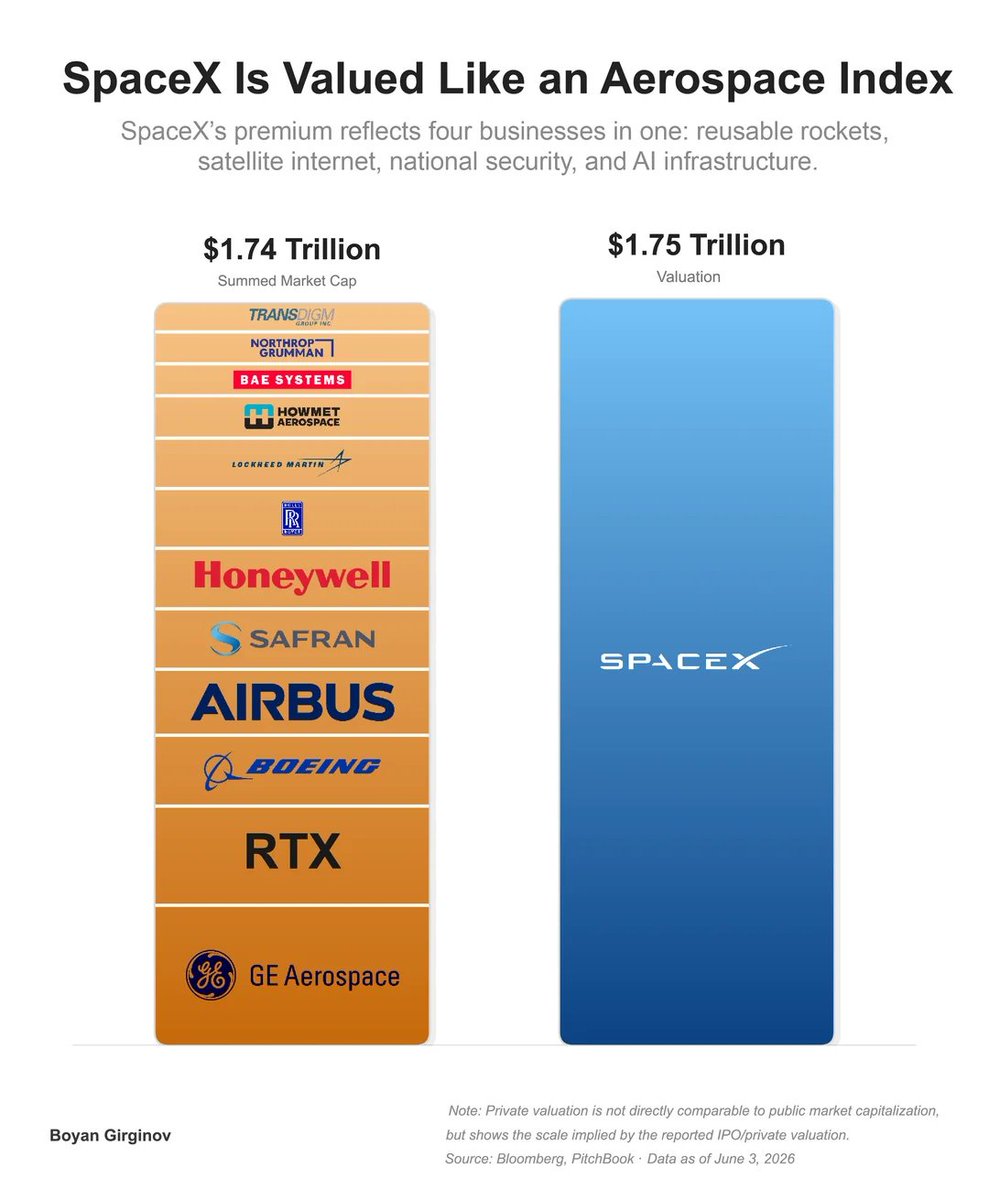

ACFMorningMeeting - Space Invaders - Elon's messy IPO with its $1.75trn 'valuaiton' is over every retail and a lot of institutional screens. Europe is steadier in the morning session than the futures messaging suggested, oil is easing after the US 'brokered' Israel-Lebanon ceasefire (which feels pretty febrile and insecure), and the market is buying the breathing space but does not believe war risk is over. This is not a clean risk-on tape; it is just less-panicked as the morning session evidences.

Opens - Europe / UK - steady to slightly firmer after weaker futures, but not a lot of long confidence. USA ftrs -ve. Asia hit with Koriea most bruised as is now the way. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - SpaceX resets the global risk conversation. Europe single-name action: Remy Cointreau $RCO.PA rallies on a new turnaround plan, while Universal Music $UMG slips after rejecting Pershing Square and agreeing a buyback. The AI trade is quieter, but still the only real global growth crutch though Space is the fresher growth story, at least for this morning. $NVDA $AMD $TSM $ASML

Commods - Brent $96.9 bbl, WTI $95.2 bbl, GOLD $4,490 toz. COPPER $6.57 lb, still rich. COCOA $4,072 MT, softer again but holding above the spring washout.

Data Focus - ECB Lagarde, BoE speech days, but geopolitics remains the overlay. If ceasefires spread, inflation fear cools. If Hormuz stays impaired, it comes straight back. Australian BoT is the most important data point, it was in line at A$1.79bn and beat forecast A$-1.3bn (yes negative).

ACFView

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

5

10

511

Jun 3

ACFMorningMeeting - Diplomacy Diesel - is again in short supply. Europe morning session trade is softer as Middle East talks stall, oil climbs again, and the market is busy pricing conflict and escalation risk rather than diplomacy and peace. AI is still doing its best to hold up the global tape in the face of encroaching geopolitics.

Opening sessions - Europe / UK - softer. USA ftrs flat to slightly lower. Asia firmer, with AI and semis still supporting/carrying the mood. $STOXX $FTSE $FTMC $DAX $CAC $DJI $GSPC $IXIC

Stock Watch - Europe single-name action: $IDEXY jumps on a strong start to summer sales, while airlines and autos feel the oil squeeze again. AI remains the global cushion, with $MRVL Marvell and the broader semi trade keeping sentiment alive. $MRVL $NVDA $AMD $TSM

Commods - Brent $97.6 bbl, $WTI $95.4 bbl, GOLD $4,430s toz. COPPER $6.57 lb, still near record highs. COCOA $4,108 MT, rebounding again but still miles below peak panic.

Data Focus - today is more about conflict risk than calendar risk. If talks stay frozen and Hormuz stays impaired, inflation pressure splashes straight back across trading screens. ACFView

@WizardBattery @EU_Startups @Share_Talk @ZaksTradersCafe @zakmir @VOXmarkets @focusIR @LondonSouthEast @BullsNBearsWA @ArthurBenta

4

9

679