Jun 12

The ACLP are gone. It will take them DECADES to clean up their act.

Jun 11

Does anyone think Albo will either resign or be overthrown within in order for them to try to “save” their 🤡 show of a party?

If yes, do you really think it will make a difference or is it too late for them no matter what they do?

1

16

Jun 10

#InitiativeDurabilité.

L’épouvantail Schengen, un mensonge de plus des opposants pour vous tromper !

Voilà des semaines que des conseillers d’Etat en charge de la sécurité, l’ancien Directeur du Réseau national de sécurité ou encore, malheureusement, la Fédération suisse des fonctionnaires de police, essaient de nous faire croire que si nous votons OUI le 14 juin, nous mettrions en péril la voie bilatérale en général et provoquerions la résiliation automatique de l’accord de Schengen et son système d’information, rendant nos policiers et nos douaniers « aveugles », le tout avec à l’appui l’utilisation abusive de photos de policiers.

Qu’en est-il donc ? C’est évidemment faux ! Dans la mesure où ces contre-vérités émanent de responsables ou d’anciens responsables de notre sécurité qui abusent de leur statut ou de leur ancienne position, il n’est pas exagéré de parler de mensonges.

La réalité ? En sus de l’excellent texte publié par un ancien officier de liaison des Douanes suisses, relisons donc le texte de l’initiative, qui prévoit de multiples paliers, à savoir :

•d’abord, mettre en place une politique visant à stopper l’explosion démographique dont la cause unique est l’immigration (c’est ça, la vraie durabilité !) ;

•si, néanmoins, la population résidante permanente (c’est important) dépasse 9,5 millions avant 2050, mandat au Conseil fédéral de renégocier tous accords internationaux favorisant la croissance démographique et d’abord, d’invoquer toutes exceptions ou clauses de sauvegarde ;

•si elle dépasse 10 millions, dénonciation du Pacte de l’ONU sur les migrations (heureusement pas encore signé par la Suisse) ;

•si, deux ans après le premier franchissement de ce seuil, celui-ci n’est toujours pas respecté, alors – et alors seulement – une résiliation de l’Accord sur la libre circulation des personnes (ACLP) peut entrer en ligne de compte – et encore, seulement en cas d’échec des négociations avec l’UE.

Pour plus de sécurité, OUI à l’initiative pour la durabilité

Non seulement, nous en sommes loin, mais à aucun moment, l’initiative n’évoque l’Accord de Schengen. Cet accord est-il juridiquement lié à la libre circulation par la fameuse « clause guillotine » ? La réponse est claire : non. Car Schengen, qui ne fait pas partie des Bilatérales I, n’est pas formellement lié à l’ACLP, comme le reconnaît le Conseil fédéral (FF 2025 1262).

Si vous dites OUI le 14 juin, vous ne rendrez aveugles ni nos policiers ni nos douaniers. Le syndicat des douaniers, Garanto, malgré la pression de l’Union syndicale suisse (USS), ne s’y est pas trompé : il a refusé toute contribution particulière à la campagne de la gauche, laissant en outre la liberté de vote à ses membres dont beaucoup, sur le terrain, comme nombre de policiers, diront OUI le 14 juin.

Vous n’avez pas encore voté et vous voulez plus de sécurité dans ce Pays ? Alors votez et faites voter un grand OUI à l’initiative contre une Suisse à 10 millions !

Jean-Luc Addor

conseiller national Savièse (VS)

udc.ch/actualites/publicatio…

5

23

51

539

I was unaware that carney was a salesman for ACLP. I am aware that Bombardier is a Canadian company that benefits from enormous taxpayer subsidies and that the government purposefully delays Canadian certification of other international business jets to benefit Bombardier.

1

13

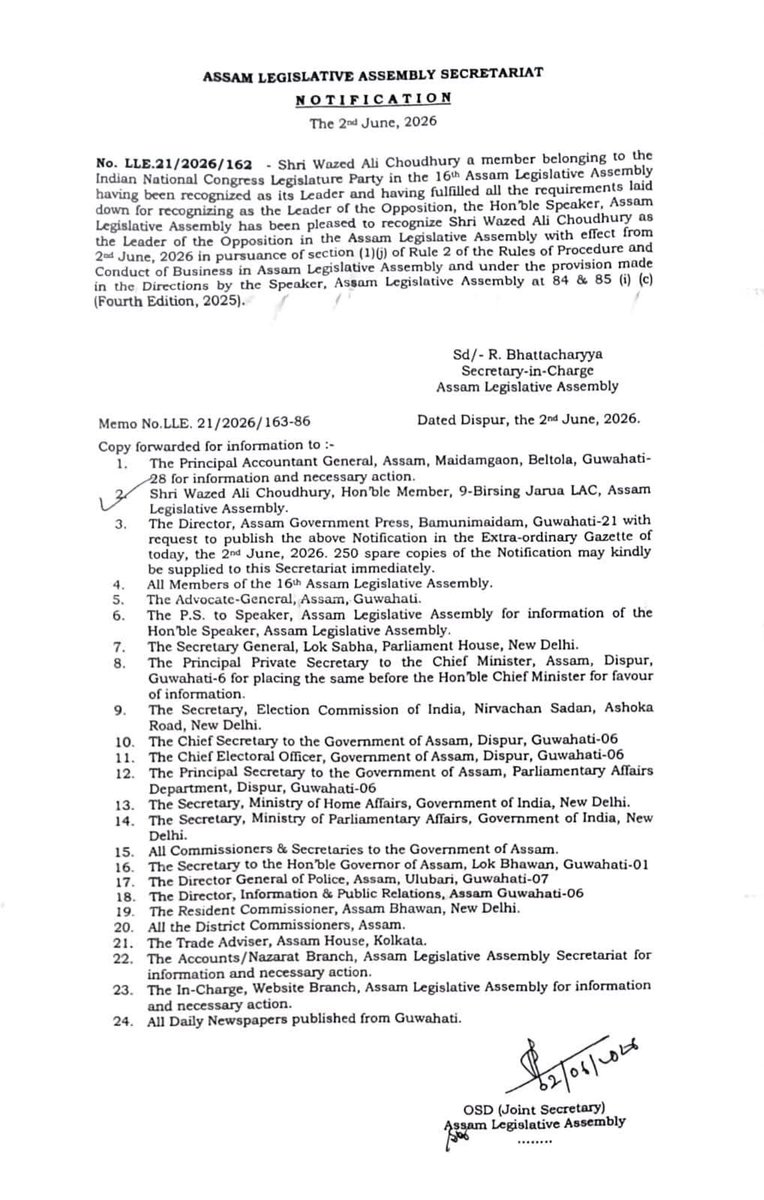

Congratulations to the Hon'ble MLA, Wazed Ali Choudhury (@WazedAliINC ) of Birsing-Jarua LAC of Dhubri District for getting the recognition for the Leader of the Opposition of the ACLP by the Hon'ble Speaker @RanjeetkrDass of Assam Legislative Assembly.

@INCIndia

@INCAssam

⤵️

4

70

Ol' Milty the Moron is just another ACLP wanker suckworth for the King Alko Junta.

11

248

May 30

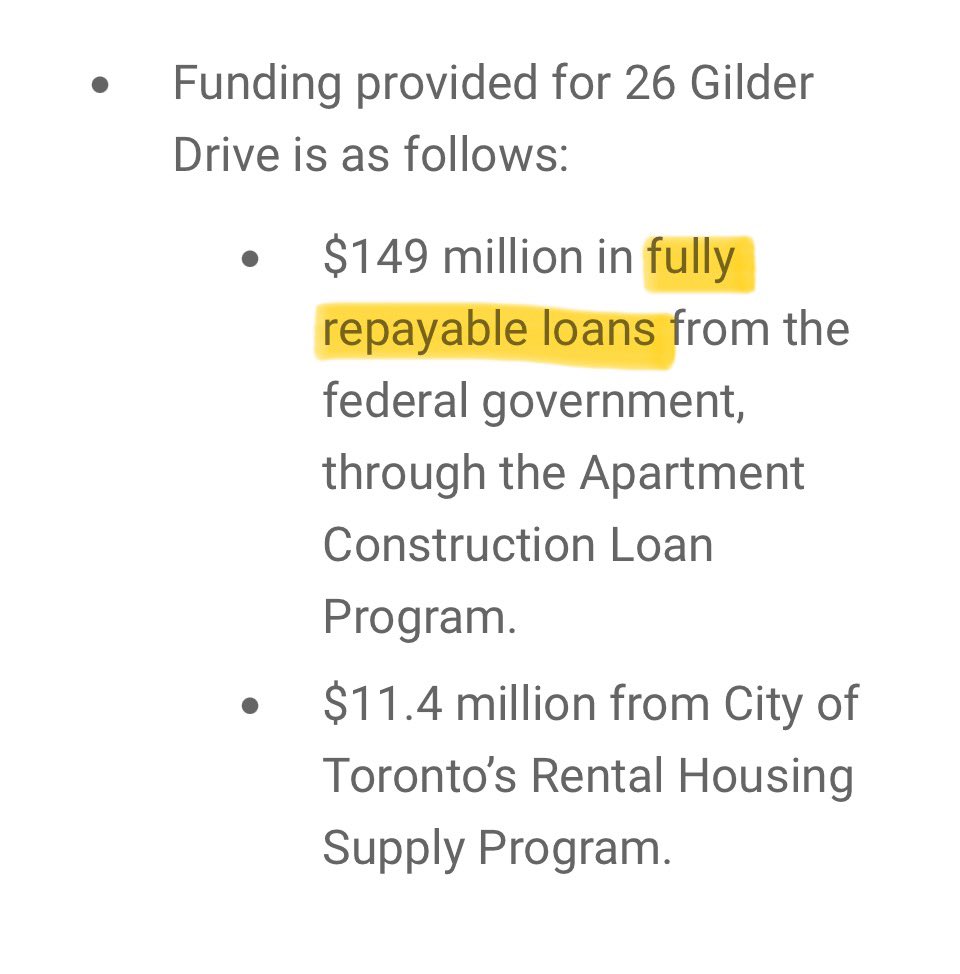

…also important to note that the $149-MILLION from the Federal Government via @CMHC_ca is a FULLY-REPAYABLE LOAN (w/ Interest) — so the Government(s) want these projects to be as high-spec and low-risk as possible.

Those ACLP design-specs drive higher construction costs…

1

2

30

May 28

Rents are dropping

Not surprising, because we're building more rental

If we want rents to drop more, we need to continue to build more rental, which will require government programs like MLI Select and ACLP to continue.

1

1

1,598

Apr 2

Well unfortunately due to all that happened with my YT channel and everything. I decided to call it a retirement for my channel. It been a good 6 year run of ACLP Films. ❤️🩵

.

.

.

.

.

.

.

And its all because its 1st of April lol 😂😂😂

1

12

411

Mar 28

ACLP Films channel is restored and back in business! Thank you @YouTube for recovering my channel and getting the hacker off my accounts. 🩵❤️😊

1

26

501

My heartiest thanks to leadership of @INCIndia Party including our National President @kharge ji, CPP Chairperson Smt. Sonia Gandhi ji, LOP, Lok Sabha @RahulGandhi ji, @INCAssam President @GauravGogoiAsm ji, ACLP Leader Debabrata Saikia ji, AICC GS @kcvenugopalmp ji ,

11

11

80

5,123

Jan 28

Toy Chica Being Adorable [FNAF SFM] (ACLP Films)

youtu.be/wchbkBJ1Y9E

#FiveNightsAtFreddys #FNAF2 #FNAF #Toychica #chica #fnafanimation #fnafsfm

2

11

1,453

Jan 27

My critique:

1) National housing policy secretariat.

I’m skeptical. These kinds of large bureaucratic coordination mechanisms seldom work. The problem is that you can’t “force” the market to build. Builders build when they see a profit. The challenge we face is that when the population was surging, builders bought a lot of land at an inflated price and now that prices have dropped, their projects are no longer profitable. They are land banking. High land costs take a long time to unwind.

2) Annual federal housing starts broken down by unit type.

Does the setting of targets actually do anything? We do not have a command and control economy. If builders still face high land costs, regulatory red tape, or unprofitable market conditions, how does this help. Wouldn’t it be better to focus on incentive structures and price dynamics rather than nominal targets?

3) New ACLP loan stream for small builders.

Maybe. Access to capital for small builders might improve liquidity, how will this impact affordability. It is the fundamentals — land pricing, developer incentives, and market demand — that drives price.

4) Lower new home prices by removing interest costs, junk fees, and taxes.

The market price is the market price regardless of the inputs. These actions might make it more profitable for developers — incentivizing them to build — but it does not mean they will sell at a lower price.

5) Federal down-payment assistance for first-time homebuyers

We’ve seen this play before. Buyer subsidies only serve to drive up prices unless they are coupled with supply structures that change market fundamentals (e.g., strong public housing provision). Without that, assisting buyers merely bumps up purchasing power against persistent pricing pressures.

6) Index Home Buyers’ Plan & FHSA to inflation

Again, this just boosts buyer demand without impacting affordability. It could even exacerbate price pressures if the market doesn’t expand supply in a sustainable, way.

7) Expand GST/HST new housing rebate

This might reduce costs in part, but house price will simply create a higher equilibrium. It has to be tied to structural change in how housing investment returns are realized.

8) Federal strategy for seniors’ housing to unlock large homes.

Older Canadians are not going to move out of their larger homes unless there is a clear financial value in doing so. The transfer costs, including new refurnishing, are often more than if they stay put.

9) MURB tax provision consultations for rental construction

Capital markets favour resale value increases. It’s hard to see tax incentives channelling investor dollars. Investor behaviour is driven by expected returns. Tax incentives must be designed carefully — not just to reduce costs but to change investment dynamics.

10) Incentives for investors to sell to non-investors and reinvest

Why would non-investors do this? Investors can still realize strong price appreciation through other housing assets.

1

3

64

Jan 26

Happy 77th Republic Day to you all

Today we honour our Constitution, freedom, unity in diversity, and the Indian flag with pride, faith, and responsibility

Attended Republic Day program today at @INCAssam HQ Rajiv Bhawan where ACLP Shri @DsaikiaOfficial unfurled the National Flag

2

110

Jan 24

Sunsettrap | Not Cute Anymore | FNAP Animation (ACLP Films)

#mylittlepony #notcuteanymore #mlp #springtrap #pinkiepie #sunsetshimmer #sfmponies

youtube.com/shorts/11-fGPZL9…

3

34

1,042

Jan 21

ASMR Ruler [Ponies Edition] (ACLP Films)

A ponies reaction to an ASMR Ruler LOL!

youtube.com/watch?v=cjfiTzeq…

Video reference:

youtube.com/watch?v=38sCwpv_…

#mylittlepony #asmrruler #asmr #mlpsfm #sfmponies #rainbowdash #pinkiepie

2

77

549

10,902

Jan 18

Chica's Dinner [FNAF SFM] (ACLP Films)

Video reference: SpongeBob Dinner 🥺

youtube.com/shorts/8u3f0SBqb…

Don't wake me, I'm not dreaming! Chica is definitely not dreaming.

youtu.be/n7bWPL14P04

#FiveNightsAtFreddys #fnaf #fnafsfm #chica #fnafchica #chicasfm

1

5

499

Jan 17

How Life Starts: [SFM Ponies] (ACLP Films)

Video reference: by Ryan HD youtube.com/watch?v=rRmzD_dc…

#mlpsfm #mlpfim #twilightsparkle #twilightsparklesfm #mylittlepony

7

61

1,334

Jan 15

Fluttershy's Relaxing Nature [SFM Ponies]

ACLP Films

#mlpsfm #mlpfim #fluttershy #fluttershysfm #mylittlepony

2

8

733