The Airbnb Story: Business Model That Made Airbnb Bigger Than Every Hotel Chain

Airbnb built a $100 billion hospitality empire without owning a single hotel room. How did two designers with no business background disrupt the entire travel industry?

This is the Airbnb story — not a startup pitch, but a masterclass in platform economics and asset-light scaling. While hotel chains were drowning in real estate debt, Airbnb monetized the one asset they couldn't compete with: unused living space.

The $100B Question

How Airbnb Started (The Air Mattress Pivot)

Platform Economics vs. Hotel Economics

The Millennial Travel Shift

Asset-Light Scaling: Why Owning Nothing Was The Advantage

The Network Effect That Killed Moats

What Smart Investors Saw That Others Missed

The real disruption wasn't technology. It was realizing that owning the network beats owning the buildings — every single time.

#Airbnb #BusinessModel #PlatformEconomics #StartupStory #AssetLight #HospitalityIndustry #TravelDisruption #BrianChesky #BusinessCaseStudy #WealthBuilding

1

138

Jun 10

RECODE STUDIOS ACCELERATES KIOSK-LED EXPANSION STRATEGY 🚀🛍️

• 📍 Plans to launch 6–8 new kiosks in strategic high-footfall locations

• ✅ Expansion follows encouraging customer response to the 2 recently launched Delhi kiosks

• 💡 Kiosk-led model supports an asset-light growth strategy with faster market penetration

• 🤝 Expansion to leverage the existing FOFO (Franchise-Owned, Franchise-Operated) partner network

• 📦 Local franchise partners to drive execution efficiency, working capital discipline and supply chain optimization

• 🏬 Kiosk format offers higher throughput, lower operating costs and stronger brand visibility in prime retail locations

• 📈 Strengthens Recode Studios' retail footprint and supports scalable long-term growth

#RecodeStudios #RetailExpansion #KioskModel #FOFO #AssetLight #Retail #GrowthStrategy #BusinessUpdate #StockMarketIndia #IndianMarkets

203

🚨 $VFS (VinFast) Q1 2026 Results

Revenue & deliveries keep growing…

but massive losses, cash burn, and debt reliance dominate the picture 👀

📊 KEY METRICS (Q1 2026)

🔹 Revenue: VND23.1T (~$921M) ( 41.7% YoY) 🟢

🔹 EV Deliveries: 58,577 ( 61% YoY, 32% QoQ) 🟢

🔹 Gross Loss: VND17.0T (~$677M) (worse YoY) 🔴

🔹 Operating Loss: VND22.9T (~$911M) 🔴

🔹 Net Loss: VND28.1T (~$1.12B) or $0.48/share (wider YoY) 🔴

🔹 Cash & Equivalents: ~$219M (down QoQ) 🔴

🔹 Total InterestBearing Debt: ~VND84.7T (~$3.37B) 🔴

👉 Core takeaway: Strong topline momentum in Vietnam/Asia, but unsustainable losses and cash burn persist

📈 GROWTH ENGINE (CORE STORY)

🟢 EV deliveries 61% YoY; strong Vietnam demand (No.1 OEM)

🟢 Escooter market share hit record 17% in March

🟢 Expanding in India, Indonesia, Philippines (top rankings in some)

🟢 New models and preorders (VF 8) showing traction

👉 This is:

Vietnamcentric EV growth story expanding across Southeast Asia

🚀 STRATEGIC MOVES

🟢 Framework deal with GSM affiliate: up to 1M EVs 4M escooters (2026–2030)

🟢 NVIDIA Autobrains MOU for Level 4 robotaxis

🟢 Shift to assetlight model in Vietnam (VFTP split potential $530M divestment)

🟢 Continued support from Vingroup/Mr. Pham (grants loans)

👉 Impact: Aiming for capital efficiency and lower future capex

⚡ WHAT’S HAPPENING?

• Revenue growth driven by higher volumes, but gross margin deeply negative due to free charging program, inventory writedowns, and high costs

• Heavy reliance on relatedparty funding and new borrowings

• Operating cash burn of ~$532M in the quarter

• Management focusing on discipline, productivity, and assetlight transition

👉 This is:

Highgrowth but cashintensive EV scaling phase

📉 PROFITABILITY (STILL CHALLENGING)

🔻 Gross margin: 73.6% (worse YoY)

🔻 Massive operating and net losses widening

🔻 High R&D and fixed costs weighing on results

👉 Translation: Volume growth not yet translating into positive unit economics

📅 OUTLOOK

🔹 FY2026 EV deliveries target: ≥300,000 (unchanged)

🔹 Twowheeler deliveries: ≥2.5x 2025 levels

🔹 Emphasis on new models, distribution expansion, and capital efficiency

👉 Note: Targets exclude potential GSM fleet volumes

🧠 WHAT’S ACTUALLY WORKING

🟢 Solid delivery growth and homemarket dominance

🟢 Expanding regional presence and new partnerships

🟢 Strategic pivot toward assetlight model

🟢 Strong backing from Vingroup ecosystem

⚠️ WEAK SPOTS

🔻 Extremely large and widening losses

🔻 Negative gross margins and heavy cash burn

🔻 High debt load and ongoing funding dependence

🔻 Regulatory/legal risk (e.g., North Carolina facility dispute)

👉 Still:

Preprofit, executionheavy story with significant financial risks

🧠 MARKET SIGNAL

👉 This is a highgrowth emergingmarket EV name with ambitious expansion plans but classic startuplevel cash consumption and losses.

🔥 BULL vs BEAR

🟢 Bull Case

• Volume ramp cost optimization → margin improvement

• GSM deal and new models accelerate growth

• Assetlight shift reduces capex and improves financials

• Vietnam/Asia EV adoption tailwinds

🔴 Bear Case

• Losses and cash burn continue or worsen

• Unit economics remain negative at scale

• Execution delays or funding gaps emerge

• Increased competition regulatory hurdles

💭 CONCLUSION

VinFast delivered strong revenue and delivery growth in Q1, but posted another quarter of massive losses and cash consumption…

👉 Progress on the top line and strategic repositioning, yet the path to profitability and selfsustaining cash flow remains distant.

👀 KEY QUESTION

Can VinFast improve unit economics and reduce cash burn as volumes scale, or will it continue relying heavily on relatedparty support?

1

2

176

VinFast’s move to reorganize its Vietnam business into an #assetlight structure, shift manufacturing into VFTP, and offload liabilities looks like a classic “survive now, scale smarter later” play in the #EV and #AutoOEM landscape. @VinFastofficial @CounterPointTR

1

1

48

🔄 Pourquoi Sofitel est parti — et ce que ça révèle sur les rapports de force

Sofitel n'a pas été "viré" au sens propre. Son contrat de management (même structure HMA) est arrivé à échéance naturelle — vers avril 2026 — et TMG a simplement choisi de ne pas renouveler.

La subtilité : quand l'État égyptien était propriétaire seul (EGOTH), Accor avait un contrat taillé en sa faveur — les États négocient mal les HMA face aux opérateurs professionnels. En rachetant 51 % les droits de gestion, TMG a changé le rapport de force du jour au lendemain.

Résultat : appel d'offres discret (Orient Express était aussi en lice), et victoire de MO sur la montée en gamme et la cohérence de l'offre Égypte (Old Cataract Winter Palace Shepheard Cairo croisière Nil = un circuit complet sous une seule marque).

À retenir pour tout deal en immobilier ou en services :

✦ La marque et la propriété sont deux choses séparables — et les valoriser séparément crée de la valeur

✦ Changer de propriétaire, c'est souvent changer d'opérateur

✦ Le vrai levier, c'est le droit de choisir son opérateur — pas les murs eux-mêmes

#RealEstate #HotelInvestment #AssetLight #Luxe

5

2

29

913

Mehul Telecom Limited IPO | Riding India’s Electronics Consumption Wave

Mehul Telecom, a Rajkot-based mobile and electronics retail chain, is building a strong presence in India’s fast-growing smartphone and consumer electronics market, particularly across Tier 2 and Tier 3 regions.

With a network of 80 stores (6 COCO stores, 74 FOFO stores)across 15 districts in Gujarat, the company offers a wide portfolio of 200 brands and over 1,600 SKUs . Notably, ~65% of its revenue comes from Rajkot , highlighting its deep-rooted regional dominance.

IPO Snapshot

Issue Size: ₹27.73 Cr

Price Band: ₹96–₹98

Opens: April 17 | Closes: April 21

Listing: BSE SME

FY25 Margin Comparison: Highest among the Peer

- Mehul Telecom → EBITDA: 6.63% | PAT: 5.0%

- Fonebox Retail → EBITDA: 2.16% | PAT: 1.33%

- Jay Jalaram Tech → EBITDA: 2.11% | PAT: 1.01%

- Bhatia Communications → EBITDA: 4.94% | PAT: 3.11%

Consistent Financial Growth (₹ Lakhs):

* Revenue: 8,015 (FY23) → 10,720 (FY24) → 12,089 (FY25) → 15,199 (9M FY26)

* EBITDA: 73 → 304 → 802 → 971

* PAT: 51 → 219 → 604 → 707

#MehulTelecomIPO #IPO #SMEIPO #StockMarketIndia #Investing

#ElectronicsRetail #ConsumerElectronics #MobileRetail

#RetailExpansion #FranchiseModel #AssetLight

#SmartphoneMarket #DigitalIndia #IndiaGrowthStory #ConsumptionStory

5

2,350

Apr 8

India's hospitality boom is going "asset-light!" 🏨🚀

says @VaruniKhosla in @livemint:

🔹 Hotel chains signed ~550 new pacts in 2025—double the 2019 rate.

🔹 Focus is shifting to management contracts over ownership to scale faster.

🔹 Demand is surging in pilgrimage sites, hill stations, and industrial hubs.

🔹 Branded room supply is expected to hit 350,400 by 2030.

Major players like Marriott, Radisson, and IHCL are racing to lock in inventory as demand continues to outpace supply. 📈

#Hospitality #RealEstate #IndiaGrowth #TravelTourism #AssetLight

4

192

schon vom #HALO trade gehoert?

focus.de/finanzen/boerse/nun…

war mir neu ...

#KI #AI #assetLight #Boerse #Software

3

21

Tout ce sujet est assetlight va souffrir en terme de valo global du marché

Franchement vaut se tenir très éloigné de ce genre de marché actuellement jusque tout cela se calme

Certaines valeurs commencent à ne vraiment pas être cher, mais c'est juste pas le moment

2

103

Feb 16

ไมเนอร์ อินเตอร์เนชั่นแนล (MINT) โชว์กำไรจากการดำเนินงานไตรมาส 4 ปี 2568 โต 21% ตอกย้ำคุณภาพกำไรและฐานะการเงินแข็งแกร่ง เดินหน้าขยายธุรกิจโรงแรมและอาหารด้วยโมเดล Asset-Light #MINT #ไมเนอร์อินเตอร์เนชั่นแนล #AssetLight #ธุรกิจโรงแรม #ผลประกอบการ #ไมเนอร์โฮเทลส์ #ไมเนอร์ฟู้ด #ฐานเศรษฐกิจ

thansettakij.com/business/to…

1

7

870

Feb 12

Google’s parent company, Alphabet, is reportedly considering a 100-year bond to help fund AI infrastructure. That’s unusual for an asset-light tech firm.

It suggests something bigger is underway.

#assetlight #alphabet #AI #artificialintelligence #bonds #markets #spotprice #finance #economics

13

37

142

7,264

Jan 28

à lire en anglais la synthèse de @0xtechquity pour $MSCI

de mon point de vue après analyse des résultats:

beat sur l'ebidta ajustée, les cashflow et le bénéfice ajustés (hors hausse des impôts).

principalement grâce aux indices.

Guidance 2026 : plutôt moyenne 6% sur les cashflow opéationnels, 30% de Capex, à surveiller.

réaction du marché: -3% en prévisionnel, je m'attends honnetement à une baisse de 10% sur plusieurs jours, les résultats sont bons mais la hausse des capex est très importante pour MSCI habitué à une croissance interne et assetlight.

je ne compte pas agir sur mes positions, ni vendre ni renforcer.

j'attends le call vers 15h.

Jan 28

🌍 MSCI $MSCI

Q4 2025

• Operating revenues of $822.5 million, up 10.6%; Organic operating revenue growth of 10.2%

• Recurring subscription revenues up 7.5%; Asset-based fees up 20.7%

• Operating margin of 56.4%; Adjusted EBITDA margin of 62.2%

• Diluted EPS of $3.81, down 2.3%; Adjusted EPS of $4.66, up 11.5%

• New recurring subscription sales up by 11.7%; Organic recurring subscription Run Rate growth of 7.7%; Retention Rate of 93.4%

• In full year 2025 and through January 27, 2026, a total of $2,470.0 million or 4,411,907 shares were repurchased at an average repurchase price of $559.85

• In fourth quarter 2025, dividends of $134.7 million were paid to shareholders; Cash dividend of $2.05 per share declared by MSCI Board of Directors for first quarter 2026, an increase of 13.9%

1

5

799

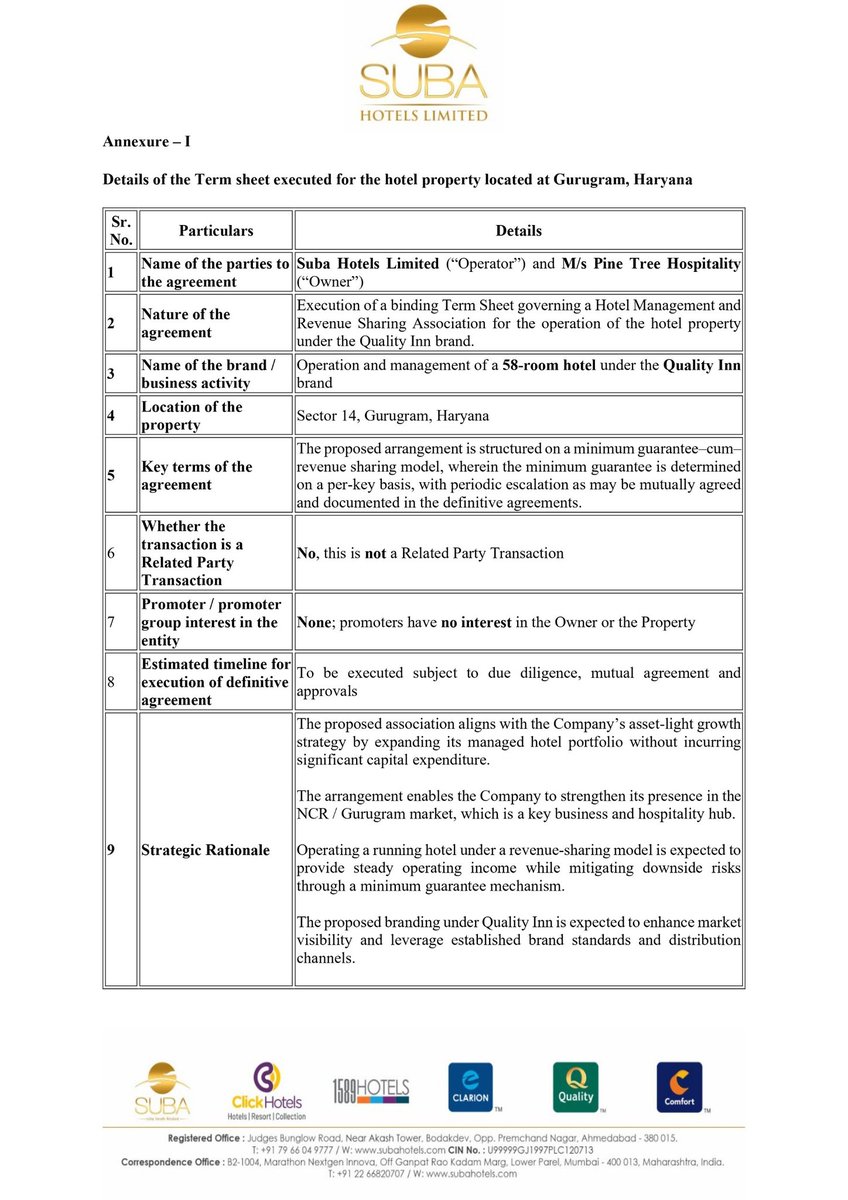

*Suba Hotels – Gurugram Hotel Term Sheet*

* Executed a binding term sheet with M/s Pine Tree Hospitality

* Property: 58-room hotel at Sector 14, Gurugram (Haryana)

* Brand to operate under: Quality Inn

#SubaHotels #Hospitality #AssetLight #HotelManagement #RevenueShare #NCR #Gurugram #QualityInn #Expansion

5

1,271

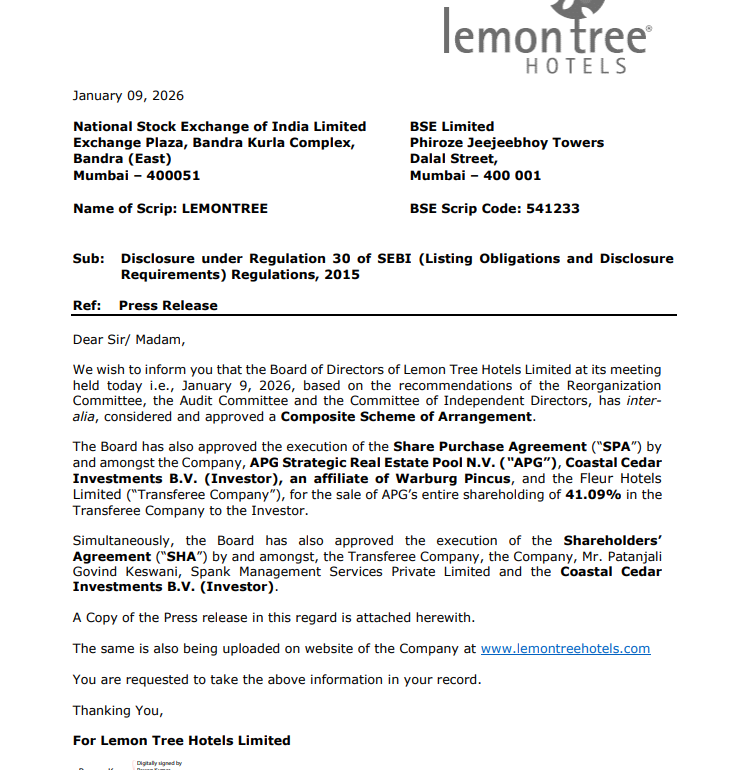

🍋 Lemon Tree Hotels: Big Strategic Trigger Unlocked

The long-awaited restructuring is finally executed.

Lemon Tree Hotels has approved a Composite Scheme of Arrangement along with a 41.09% stake sale in Fleur Hotels to APG (Warburg Pincus affiliate).

🔑 Why this matters:

• Clear separation of asset-light vs asset-heavy businesses

• Capital unlocking & cleaner structure

• Better focus on ROCE & scalability

• Strategic investor validation

📌 This is not a quarterly event —

👉 it’s a structural value-unlock story.

#LemonTree #ValueUnlock #AssetLight #IndianStocks #Investing

2

629

SAYAJI HOTELS – 15-Year HMA Signed for Somnath

• Asset-light expansion: 4-star hotel in Somnath, Gujarat under management agreement with Mahavan Resort LLP.

• 15-year tenure from operations; renewal option available.

• Branded as “The Forest Chapter” by Sayaji; ~50 keys with banquets, restaurants, gym & spa.

• Strengthens presence in pilgrimage & leisure destinations.

Impact: Positive – boosts management fee income and brand visibility with low capex.

#SayajiHotels #Hospitality #AssetLight #Somnath #Tourism #HotelIndustry #IndiaTravel

287

30 Dec 2025

Lemon Tree Hotels expands its Andhra Pradesh footprint

✅ Launches 228-key Lemon Tree Suites, Tirupati under the managed model

✅ Strengthens asset-light growth strategy and presence in key pilgrimage destinations

#LemonTreeHotels #Hospitality #AndhraPradesh #Tirupati #AssetLight #Expansion

2

75

22 Dec 2025

#WATCH | Indian Hotels exits its 25.5% stake in Taj GVK Hotels for ₹592 crore, selling to Shalini Bhupal at ₹370 per share, making her the largest shareholder and reinforcing IHCL’s asset-light strategy

@SnehiShah11 breaks down key details

#IndianHotels #IHCL #TajGVKHotels #AssetLight #Hospitality #StakeSale #BusinessNews

1

7

1,854

14 Nov 2025

The Praveg MultiX Potential: Why it’s NOT just another hotel stock. 🧵👇

Praveg Ltd. isn’t competing with Indian Hotels, Chalet, or Thomas Cook.

It’s created an entirely new category:

👉 Asset-Light, Experiential Eco-Luxury — that scales fast, earns faster, and taps into India’s booming spiritual & eco-tourism wave.

What makes it unique?

Let’s compare:

🏨 Hotels (IHCL, Lemon Tree):

• Asset-heavy, concrete

• 5–10 yrs ROI cycle

🏕️ Praveg:

• Luxury tents/cottages on leased land

• Payback in 18–24 months

• Rapid deployment into high-demand zones

🧭 Praveg ≠ Mahindra Holidays

• No timeshare lock-ins

• Fully flexible, pay-per-use model

• Targets HNIs, families, and international eco-luxury seekers

🛫 Praveg ≠ Thomas Cook

• Not a travel agent

• Praveg owns the premium destination experience

What’s the real moat?

🧱 Speed

📉 Lower CapEx

📈 Higher RoCE

🤝 Gov’t partnerships in high-potential eco & spiritual hubs (e.g., Ayodhya, Lakshadweep, Kutch)

🎪 Events Synergy = Growth Flywheel

• Runs Rann Utsav with state support

• Launches luxury tents alongside events

• Events bring footfall → Hospitality captures high-margin spend → Next event builds brand

= Self-reinforcing loop

🧠 Management Vision

“Vision 2028” =

• 65 locations

• 2,500 rooms

• International expansion: Serengeti, Masai Mara

= A pan-global operator of niche, eco-luxury tourism infrastructure

📈 Why 50X/100X is not a fantasy:

If they scale this model:

• No big debt

• High operating margins

• Blue-ocean markets (zero competition in many geographies)

They could rerate from ₹1,000 Cr to ₹50,000–₹100,000 Cr mcap range over time.

🧮 Think like a VC

You’re not buying a hotel chain.

You’re buying into the platform for scalable, asset-light, luxury tourism — across deserts, coasts, hills, and jungles — in a climate-aware world.

This is a category creator.

💡 In conclusion:

Praveg is not just a stock.

It’s a bet on the future of travel:

• Experiential

• Sustainable

• Scalable

• Story-driven

And it’s already building India’s version of Aman Resorts — just smarter and faster.

#Praveg #TravelStocks #EcoLuxury #AssetLight #Hospitality #100XIdeas #Vision2028 #XPost

2

1

4

561

10 Oct 2025

Grand Continent Hotels (GCH) on an Expansion Spree! 🏨🚀. Got listed in March '25

Key takeaways from their recent interaction at Bharat Conference reveal a disciplined, asset-light strategy for explosive growth. Here’s the full breakdown:

🎯 The Asset-Light Blueprint

GCH is focused on a leasehold model, avoiding heavy asset ownership. This allows for rapid scaling with a disciplined investment cap of just ₹7-8.5 lakhs per room key. The target ROI is a swift 24 months for corporate hotels, showcasing good capital efficiency.

📈 Growth Roadmap: Doubling the Keys

The expansion pipeline is aggressive and well-defined:

•Current: 24 hotels (~1,350 keys).

•FY26 Target: Crossing 1,600 keys from 1300 now

•FY28 Ambition: Reaching a massive 3,000 keys.

•Immediate Pipeline: 6 new hotels are set to open this year alone.

💡 Strategic Portfolio & Geographic Focus

The portfolio will be strategically weighted towards high-demand segments:

•Corporate Hotels: The backbone, making up 60-70% of the portfolio.

•Pilgrimage Properties: A growing focus, expanding to 20-25%.

•Leisure: A niche 10% of the portfolio.

Expansion is centered on high-potential Tier 2 Indian cities like Pune, Rajkot, and Indore, where the economics are most favorable.

💰 Profitable & Prudent Financials

Management is guiding for a stable and impressive EBITDA margin of ~26%.

Mature properties, stabilized after 5-6 months, are expected to deliver robust margins above 30%, supported by a lean staffing model of 0.5-0.6 staff per room.

My Take: GCH's strategy is a clear playbook for disciplined, scalable growth. By combining an asset-light model with a sharp focus on high-margin segments and Tier 2 cities, they are building a resilient and profitable hospitality portfolio.

And yes, they scan the social media write ups about them. Did not take it well when social media handles compared Suba Hotels with their business.

#IndianHospitality #HotelIndustry #AssetLight #Expansion #Investing #BusinessStrategy #Tier2Cities

1

5

1,382