Apr 12

1. Has nothing to do with dissatisfaction with the investment menu. She is ignorantly criticizing the vehicle.

2. They are too stupid to do anything themselves, I present this post as exhibit A. I would also assert it does not need to be exciting. It needs to be broadly diversified, and ultra low cost.

3. Research proves that fewer options allows people to make better choices.

crr.bc.edu/401k-investment-o…

4. Autoenrollment and autoescalation into a simple total market index fund is all that is necessary.

crr.bc.edu/401k-nudges-and-c…

2

45

Apr 3

We're about 50-75% of the way there with the autoenrollment system. Just need to remove to opt out, and allow people to choose their own pension providers and be allowed to take them from job to job rather than have to use whichever one gave your company the biggest backhander.

1

3

259

Proud to see Virginia once again on the exemplar states to look to list for a high expectations agenda and rigorous accountability systems to policies for sharing test results faster with parents & adopting autoenrollment policies for ready students to access advanced coursework.

If you’re running for one of 36 governor seats this fall, do yourself a favor: read @ChadAldeman’s low-cost, high-impact education playbook.

1

3

551

18 Dec 2025

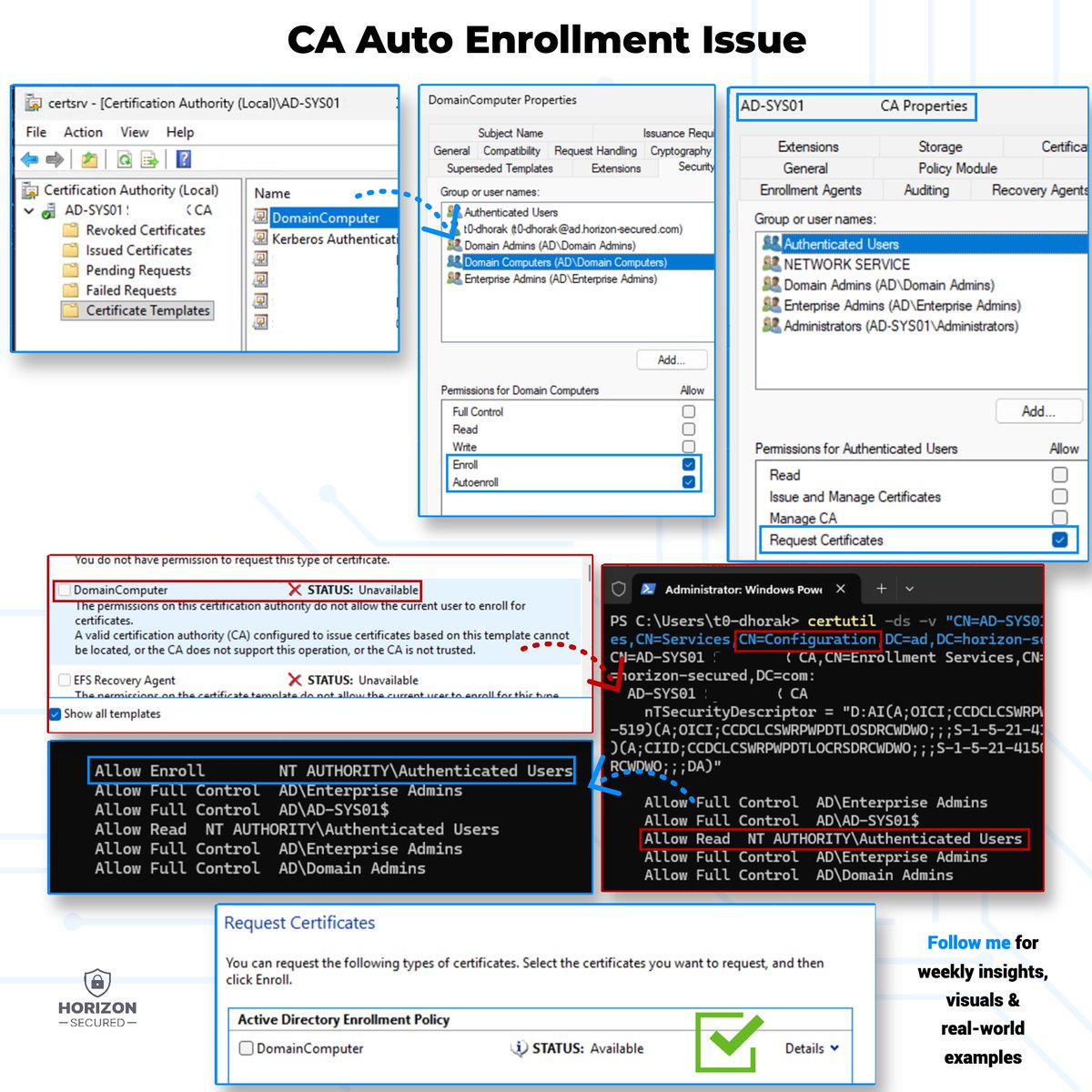

🔒 Secure Bits 💡

Weird 𝗶𝘀𝘀𝘂𝗲𝘀 𝘄𝗶𝘁𝗵 𝗔𝘂𝘁𝗼 𝗘𝗻𝗿𝗼𝗹𝗹𝗺𝗲𝗻𝘁 in Microsoft CA? Here’s one that cost me hours.

I recently set up a 𝗳𝗿𝗲𝘀𝗵 𝗜𝘀𝘀𝘂𝗶𝗻𝗴 𝗖𝗔 on Windows Server 2025 in a brand-new Active Directory domain:

✔️ Auto-enroll GPO? ✅

✔️ Certificate template published & configured for domain computers? ✅

✔️ ACLs set up? ✅

𝗬𝗲𝘁 — 𝗻𝗼 𝗰𝗲𝗿𝘁𝗶𝗳𝗶𝗰𝗮𝘁𝗲. Not after a reboot. Not after waiting. Nothing.

After 𝗵𝗼𝘂𝗿𝘀 𝗼𝗳 𝘁𝗿𝗼𝘂𝗯𝗹𝗲𝘀𝗵𝗼𝗼𝘁𝗶𝗻𝗴, I stumbled upon Uwe Gradenegger’s great blog:

🔗 gradenegger.eu/en/the-reques…

𝗛𝗲𝗿𝗲’𝘀 𝘄𝗵𝗮𝘁 𝘄𝗮𝘀 𝘄𝗿𝗼𝗻𝗴 ⬇️

💥 The ACL about who can actually request certificates 𝗼𝗻 𝗖𝗔 𝗹𝗲𝘃𝗲𝗹 was not synced.

𝗥𝗲𝗾𝘂𝗲𝘀𝘁 𝗖𝗲𝗿𝘁𝗶𝗳𝗶𝗰𝗮𝘁𝗲𝘀 𝗔𝗖𝗘 (𝗘𝗻𝗿𝗼𝗹𝗹) 𝘀𝗵𝗼𝘂𝗹𝗱 𝗯𝗲 𝗶𝗻 𝘁𝘄𝗼 𝗽𝗹𝗮𝗰𝗲𝘀:

1️⃣ The registry of the CA (you can see this in CA console)

2️⃣ The Configuration partition in Active Directory (query this with certutil)

Somehow — and I still don’t know why — the AD Config partition was 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 the Request Certificates ACE (Enroll) for Authenticated Users.

✅ Re-added the Read Enroll rights

✅ Waited a minute

✅ Auto-enroll worked perfectly

Just wanted to share this with you — in case you ever run into the same headache.

#MicrosoftCA #ActiveDirectory #AutoEnrollment #Certificates #SecureBits #HorizonSecured @BlueTeamDave

1

8

44

2,317

16 Dec 2025

Do you get a lump sum from auto-enrolment?

gov.ie currently says you can take up to 25% as a lump sum at retirement.

We’re getting full clarity on this soon - and we’ll share it as soon as we have it.

#AutoEnrollment

2

2

741

13 Dec 2025

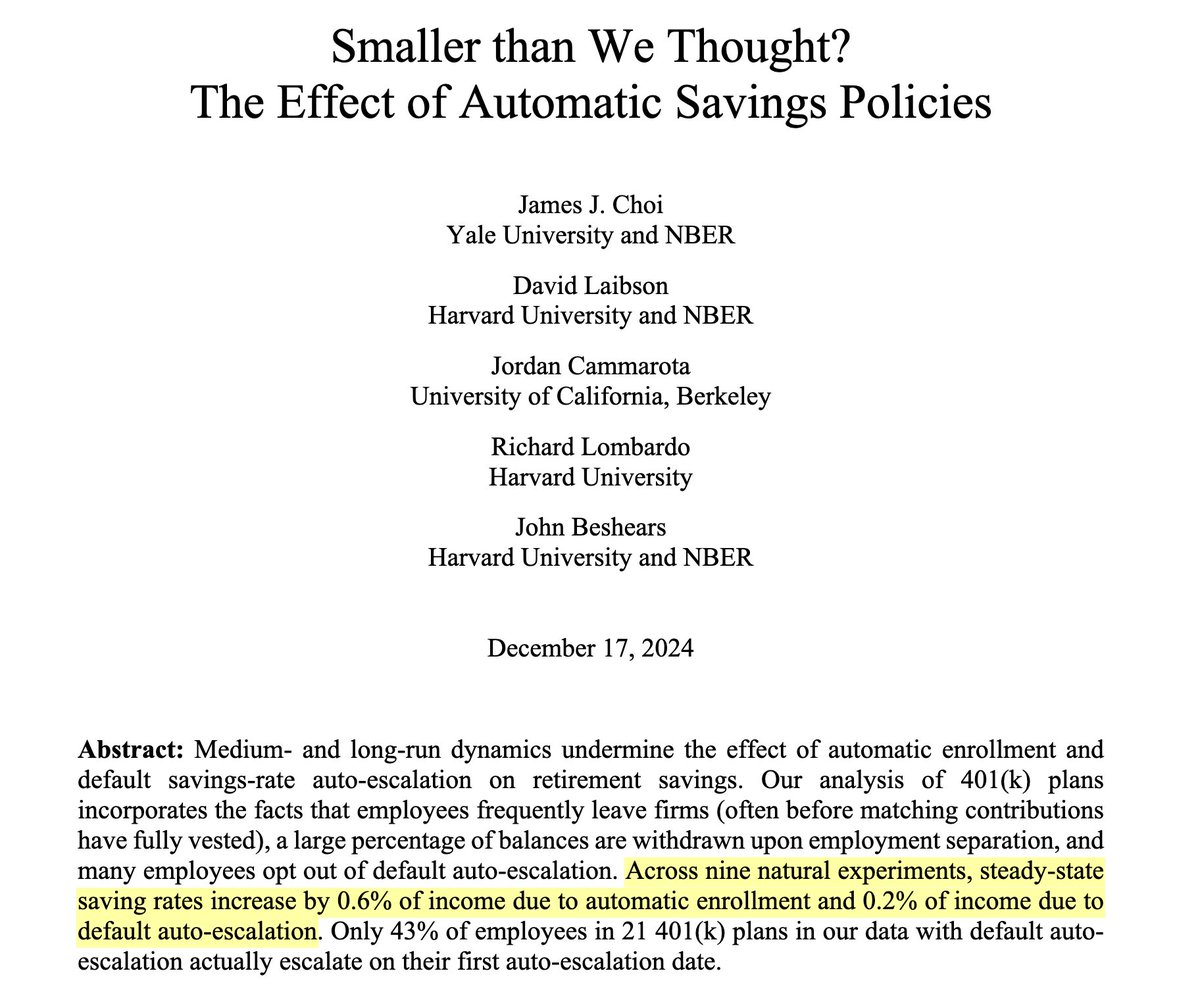

Love this paper! The effect of autoenrollment isn't static, it erodes over time due to leakage, job transitions, etc. A lifecycle model matching this attenuation job transition effect predicts 3% AE in all jobs ↑ retirement consumption by just ~0.3% (though 2x for low-earners)

11 Dec 2025

The most famous "nudge" example -- defaulting to 401k enrollment with auto-escalation -- doesn't actually do very much it turns out.

1

5

477

Many Americans risk outliving their retirement savings. @Wharton Professor @OS_Mitchell recommends making annuities the default option for #401(k) plans, to change that, just as #autoenrollment boosted saving.

whr.tn/4746vut

1

1

2

298

14 Oct 2025

The AutoEnrollment Pension has taken Decades of Incompetence & Political objection to be delivered

Claiming credit for inflicting yet another Stealth Tax when you simply rubber stamped the work done by others, is typical Political Spin

PaYe, PRSI, USC, LPT "pension" Tax

1

4

159

26 Sep 2025

美股指数为何越来越难跌下去了?背后是7万亿退休金的“长期买盘”长期托底。

美股为何在高利率、通胀和地缘风险的阴影下,依然表现坚挺?答案不仅仅在华尔街的交易大厅,而是在制度深处——7万亿美元的401(k)退休金,正在为美股指数基金源源不断输送“长期买盘”。

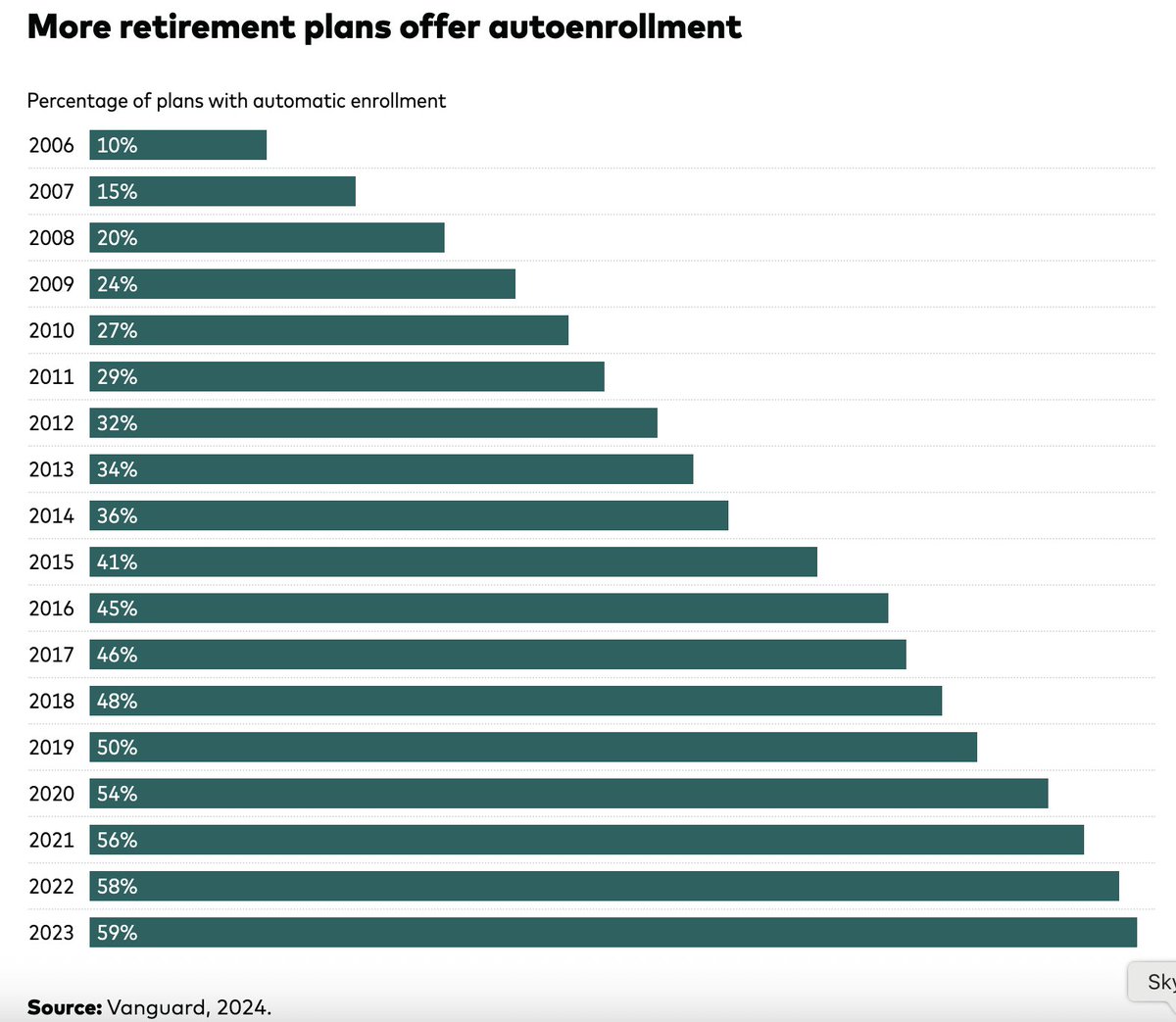

截至2023年底,美国401(k)计划总资产已接近7.6万亿美元。更关键的是,自2006年《养老金保护法》推动自动登记(autoenrollment)以来,退休计划参与率大幅提升。

Vanguard 的数据显示:2006年仅有10%的计划采用自动登记,而到2023年,这一比例已攀升至59%。这意味着,超过一半的美国职工在未做任何选择的情况下,都会自动开始为退休储蓄。

资金又流向哪里?答案非常集中:标普500指数基金。大多数自动登记的默认选项是目标日期基金(Target Date Funds),而这些基金的核心配置正是标普500成分股。以Vanguard为例,其VOO ETF和对应的共同基金VFIAX,已经成为401(k)账户中最常见的配置之一。

这就造就了一个长期的“被动买盘”现象。无论市场如何震荡,每个月都有数以亿计的美元自动流入这些指数基金,形成制度性的资金托底。换句话说,VOO、IVV等低成本S&P 500指数基金背后,站着的不是短期投机者,而是数千万美国工薪阶层的退休储蓄。

美股之所以“跌不下去”,并不是完全依赖华尔街的热钱,而是有一套长期制度安排:7万亿美元的退休金,每月、每年都在稳定注入,成为美股最大的底层买盘。

28

59

342

63,520

17 Jul 2025

🚨The main Virginia teachers union organization awarded the legislative sponsor of Virginia’s new advanced math autoenrollment law for her work on that law. 🍎🧮 Great to see such a broad coalition of Virginia stakeholders support this common sense law. Congrats @DelegateCallsen!

16 Jul 2025

Honored to be named a Rookie Legislator of the Year by the Virginia Education Association for my work on math auto-enrollment. Supporting teachers, funding schools, and fighting for excellent outcomes for our children is lifelong work. 🍎🍎🍎Thank you to the VEA and to our local educators in attendance! (And a flashback photo to when I was a math teacher!) 👩🏽🏫

5

305

11 Jul 2025

This was set to be a classic example of "Everythingism" - conflating a decision on framing good investment choices where too much cash accrual is an inefficient use of tax relief, and likely (over any reasonable horizon) to lowball saver returns. It was wrapped up as an effort to get more investment in UK companies - but the stocks & shares ISA already has a big home bias (HL, AJBell estimate about 40%) that does not need amplifying. The latter objective is far better addressed through levelling the stamp duty playing field, reforming Solvency 2, and promoting a retail investment culture (autoenrollment is likely to help this over time).

10 Jul 2025

Reeves puts reform of UK cash ISAs on hold following backlash on.ft.com/4lwzGer

2

1

12

4,368

10 Jul 2025

Todo lo cual conduce a la imperiosa necesidad de establecer medidas como el autoenrollment para pensiones de pilar 2 y eliminar los límites absurdos de las pensiones de pilar 3. Si además hay incentivos fiscales de verdad, ni te cuento ya.

1

1,025

24 Jun 2025

The new VA advanced math autoenrollment law is a bipartisan model for other states. We had a true leader with D @DelegateCallsen as its sponsor, overwhelming bipartisan majorities pass it, R @GovernorVA sign it & his appointee @GullyoftheSun now faithfully implementing it 👏 6/6

1

2

292

24 Jun 2025

Virginia’s implementation guidance of its new advanced math autoenrollment law is 🔥. This evidence-based statement in the implementation documentation looks like it's from @JonathanPlucker (I've confirmed it's not) 1/6

1

2

14

2,176

Ubuntu 25.04 is on the way, and joining Ubuntu machines into Windows estates is made even easier through support for the latest Polkit and with improvements to certificates enrollment.

Listen to our product team talk about what features sysadmins can use to integrate with Active Directory, like Group Policy Objects, privilege management, and remote script execution through our ADsys tool.

To learn more about these features, plus certificate autoenrollment, network shares, and apparmor profiles, you can read our whitepaper below:

ubuntu.com/engage/microsoft-…

#Ubuntu #Linux #OpenSource #NobleNumbat

7

44

283

18,437

15 Mar 2025

We firmly support @PeterKLamb’s autoenrollment bill. Government bureaucracy is stopping children from getting the food they need by forcing families to navigate barriers of technology, language, and stigma.

Peter is right: the government could cut through this by automatically enrolling eligible children for Free School Meals. Health and education outcomes are suffering, and autoenrollment must be introduced without delay.

parliamentlive.tv/Download/I…

3

5

2,162