Jun 14

Space X IPO, hilarious.

Preference shares with 30x voting rights. 5 percent of shares available for the public. Charter bans class actions litigation. Texas law, you have to have 3% stake before you can even file a shareholder proposal.

Banker bookbuild humiliation.

1

1

1

51

Freshfields Advised The Placing Banks In Solaria’s €300M Accelerated Bookbuild Offering

Link to read full News: legaleraonline.com/global-de…

#LegalEra #DealNews #Freshfields #Solaria #AcceleratedBookbuild #CapitalMarkets #RenewableEnergy #Spain #EquityOffering

16

เห็น $SPCX ที่หลายๆ คนมีกันแล้วผมอิจฉาเลย.. ได้หุ้น $SPCX แบบ grade สูงๆ…

『Super Extreme Ultra Nova Diamond Luxury Prestige Reserve Grand Master Emperor’s Collection Platinum Signature Heritage Limited Edition Ceremonial Grade』

ของผมงบน้อย ซื้อ $SPCX มาแต่ grade ราคาถูกๆ..

『Early Institutional Bookbuild Allocation Grade』

🥺🥲

5

8

47

9,879

Jun 12

Hyperliquid's SPCX does not give holders SpaceX shares, allocation rights or any claim on the company. It is a cash-settled derivative. But because SpaceX priced its IPO at a fixed $135 a share, it has become one of the few live markets showing where traders think the stock could open.

Blockchain-based prediction markets have recently emerged as the go-to-place for investors to bet on the SpaceX IPO, offering a decentralized alternative to traditional pre-IPO markets. Unlike private equity deals that require accreditation and high minimums, these onchain markets are accessible to retail investors with minimal capital, creating 24/7 price discovery on IPO odds.

At Wednesday’s level near $157, SPCX implied only a roughly 16% premium to the $135 IPO price, down from about 60% when the contract briefly traded near $216 in May. At $183, the implied premium is back near 36%.

Other shadow markets are now pointing the same way. Bloomberg reported Friday that IG International derivatives implied a SpaceX valuation of about $2.4 trillion, more than 35% above the $1.77 trillion valuation set by the IPO price.

Elsewhere, Polymarket traders put 70% odds on SpaceX closing its first trading day above $2 trillion.

The reversal comes as pre-IPO SPCX has shown caution in the market, falling by about 30% over the past few weeks. It suggested traders still expected SpaceX to trade above the offer price, but not at the explosive premium implied by the bookbuild. And Friday’s bounce now says that discount is closing.

2

2

5

444

555,555,555 shares at a fixed $135. SpaceX never ran a bookbuild, the price was take it or leave it, so today's Nasdaq opening cross is the first public market-set price the company has ever had.

The order book: roughly $250B of demand against the $75B on offer, retail orders above $100B, with retail's allocation cut to the low 20s percent range. Caveat: hot-deal books carry inflated bids from buyers anticipating cutbacks, so reported demand is an upper bound, not a measurement.

At $135 the implied valuation is about $1.77T (outlets reported $1.75T to $1.77T on share-count assumptions), about 40% above the $1.25T private mark set by the February xAI merger. One ticker, $SPCX, holds launch, Starlink, and xAI.

Full breakdown: kresmion.com/learn/spacex-ip…

66

Jun 11

that triggered immediate panic-selling.

SpaceX broke all Wall St conventions by refusing to offer a price range. They went straight to a fixed price of $135 per share. Before marketing even officially finished, the bookbuild attracted over $250 billion in institutional demand

1

1

41

Jun 11

BLAST-OFF: Elon Looks to Army of Loyalists to Help Make Him Trillionaire

The SpaceX IPO is expected to set records Friday and mark a new pinnacle in Wall Street’s retail revolution...

wsj.com/articles/musk-spacex…

THE RED FLAGS... Say what you like about Elon Musk, but you have to give him credit for his vision and his chutzpah.

The self-appointed technoking, last year’s supposed U.S. budget czar, is the talk of the town thanks to his forthcoming Space Exploration Technologies — aka SpaceX...

marketwatch.com/story/here-a…

BLOOMBERG: Wall St braces for SPACEX with stress test, 'watch parties'...

Wall Street has spent months debating how much SpaceX is worth. Behind the scenes, a different challenge has occupied the institutions responsible for bringing it public: preparing the plumbing systems needed to support what could become the largest IPO in history.

S&P Global Inc.’s Equity Bookbuild group, which helps underwriters capture and allocate investor demand during initial public offerings, has spent weeks expanding the efficiency and capacity of its infrastructure ahead of SpaceX’s Friday trading debut.

At Depository Trust & Clearing Corp., staff plan to spend the weekend monitoring systems and communicating with industry peers.

A blockbuster IPO is not just a test of investor demand. It is also a test of the technology, communications networks and risk-management systems responsible for processing millions of orders, messages and transactions at near-instantaneous speeds.

Brokers, exchanges, market makers and clearing firms must all operate in sync as orders are routed, trades executed and transactions settled.

SpaceX amplifies those demands.

The company is expected to attract outsized interest from institutions, retail investors and exchange-traded funds alike.

The offering has already generated more orders than shares available, according to people familiar with the matter, raising expectations that trading volumes could rank among the largest ever seen for a newly public company.....

msn.com/en-us/money/markets/…

FILED UNDER:

#SpaceXIPO, #ElonMusk, #SpaceXPublic, #LargestIPO, #MuskTrillionaire, #SpaceXStock, #RetailInvestors, #WallStreetIPO, #SpaceXDebut, #TechIPO, #MuskEmpire, #RecordIPO, #SpaceEconomy, #ElonVision, #SpaceXTrading, #IPO2026, #TrillionDollarCompany, #RetailRevolution, #MuskLoyalists, #SpaceXValuation, #HistoricIPO, #ElonChutzpah, #SpaceXfrenzy, #MuskArmy, #WallStreetPrep, #IPOstressTest, #SpaceXLaunch, #TechStocks, #AerospaceIPO, #MuskCompanies, #PublicOffering, #InvestorDemand, #BlockbusterIPO, #SpaceXnews, #ElonTrillionaire, #RetailTrading, #SpaceXhype, #MuskSuccess, #IPOrecords, #Elon2026, #SpaceXloyalists, #MuskRedFlags, #TechRevolution, #WallStreetWatch, #SpaceXfriday, #MuskVision, #IPOplumbing, #SpaceXrevolution, #ElonIPO

6

253

Jun 10

SpaceX is not really pitching Wall Street a rocket company anymore. It is pitching the first vertically integrated AI infrastructure company with access to orbit.

That is the real story behind this IPO.

The headline numbers are already historic: a $75B raise, a $135 share price, a roughly $1.75T valuation, and about $150B in institutional demand. The largest IPO ever, about 2x oversubscribed.

But the more important shift is buried underneath the bookbuild.

SpaceX is no longer just selling launches, Starlink subscriptions, or Mars optionality. It is now selling compute.

Google is reportedly paying SpaceX $920M per month from October 2026 through June 2029 for access to around 110,000 Nvidia GPUs and related infrastructure.

Anthropic is reportedly paying another $1.25B per month for compute capacity.

Together, those two contracts alone imply roughly $26B in annualized AI compute revenue - more than SpaceX’s reported 2025 revenue.

That is why the market suddenly has to reprice the company.

The bull case is no longer “rockets are cool.”

It is: SpaceX controls the launch layer, the satellite layer, the communications layer, the compute layer, and potentially the orbital data-center layer.

Reuters now reports that SpaceX is aiming to begin orbital AI compute demonstrations by late 2027, ahead of the “as early as 2028” deployment timeline disclosed in its IPO materials.

The ambition is staggering: space-based AI computing infrastructure, with Starship as the cost-reduction engine that makes mass deployment possible.

In other words, SpaceX is trying to turn orbit into the next data-center geography.

Not Virginia.

Not Arizona.

Not Abu Dhabi.

Orbit.

That is why this IPO matters beyond finance. It is a market event, but also an infrastructure event. If SpaceX can make orbital compute economically viable, it changes the geography of AI power.

Power constraints, cooling constraints, land constraints, sovereignty questions, and latency trade-offs all enter a new regime.

The bear case is obvious too.

Starship is still the bottleneck. Orbital compute at scale is not proven. A $1.75T valuation assumes execution across rockets, satellites, AI infrastructure, and public-market discipline. That is a lot to believe at once.

And 2x oversubscription is solid for the biggest IPO in history, but not euphoric by normal hot-IPO standards.

Still, the market is no longer valuing SpaceX as a launch company.

It is valuing it as the company trying to fuse rockets, satellites, GPUs, cloud contracts, and orbital infrastructure into one stack.

The question is not whether SpaceX is expensive.

Of course it is.

The question is whether Wall Street is watching the first AI infrastructure company whose data centers may eventually leave the planet.

1

3

4

2,009

Oversubscribed IPOs are almost always the default for a hyped name like SpaceX, so that part alone doesn’t say much. The real signal is allocation quality and post-listing price action. Demand at the bookbuild stage is optimism, not proof the valuation holds.

90

Risk appetite for scarce private growth is alive when the book can close ahead of schedule. A compressed bookbuild shifts focus from valuation debate to allocation pressure.

1

385

the other tell: the book reportedly filled within days at a price nobody negotiated. open question is whether any private mega-cap bothers with a traditional bookbuild after this.

12

spacex set a fixed $135 ipo price a week before the book opened. no range, no bookbuild, take it or leave it.

the raise is $75b, about 2.5x the largest ipo ever priced (aramco, $29.4b in 2019). at that price it lists as the seventh largest company in the us, above tesla.

when the seller can dictate terms on the biggest raise in history, that tells you where the leverage sits between issuers and wall street right now.

1

51

The SpaceX IPO on June 12 is going to be a generational short opportunity.

Ticker $SPCX on Nasdaq:

> Fixed price of $135/share (no traditional bookbuild range)

> 555.6M shares, $75B raise = largest IPO in history (Aramco raised $29.4B in 2019).

> Valuation at $1.75T . Underwriter greenshoe of an additional 83.3M shares ($11.2B) if it trades above issue.

> 94x trailing revenue ($18.67B FY2025). No precedent at mega-cap scale.

> Morningstar fair value is $780B, roughly 55% below the ask.

> December 2025 tender implied $800B valuation. So $135 is a 61% premium to a valuation set six months earlier.

> 2025 net loss of $4.94B (swung from $791M profit).

> Starlink is the only profitable segment.

> Dual-class structure: Musk 42% equity, 85% votes. (Retail gets limited say.)

> Up to 30% retail allocation, 3x the typical 5–10%. (Unusually large retail absorption.)

> Pre-IPO perps (Coinbase, Binance, Phemex) exist outside the US; secondaries via Forge/EquityZen/Hiive for accredited investors.

> After Q1-as-public-company earnings (quarter through June), insiders can sell up to 20% of eligible locked shares.

> Rolling unlocks of 7% each at 70/90/105/120/135 days post-IPO.

> After second earnings (quarter

through Sept), another 28% unlocks. Full release at 180 days.

Opportunities like this don’t come often. Not FA, but the smartest thing you can do is create a Hyperliquid account so you have the freedom to short this IPO’s price action early.

1

3

370

Jun 5

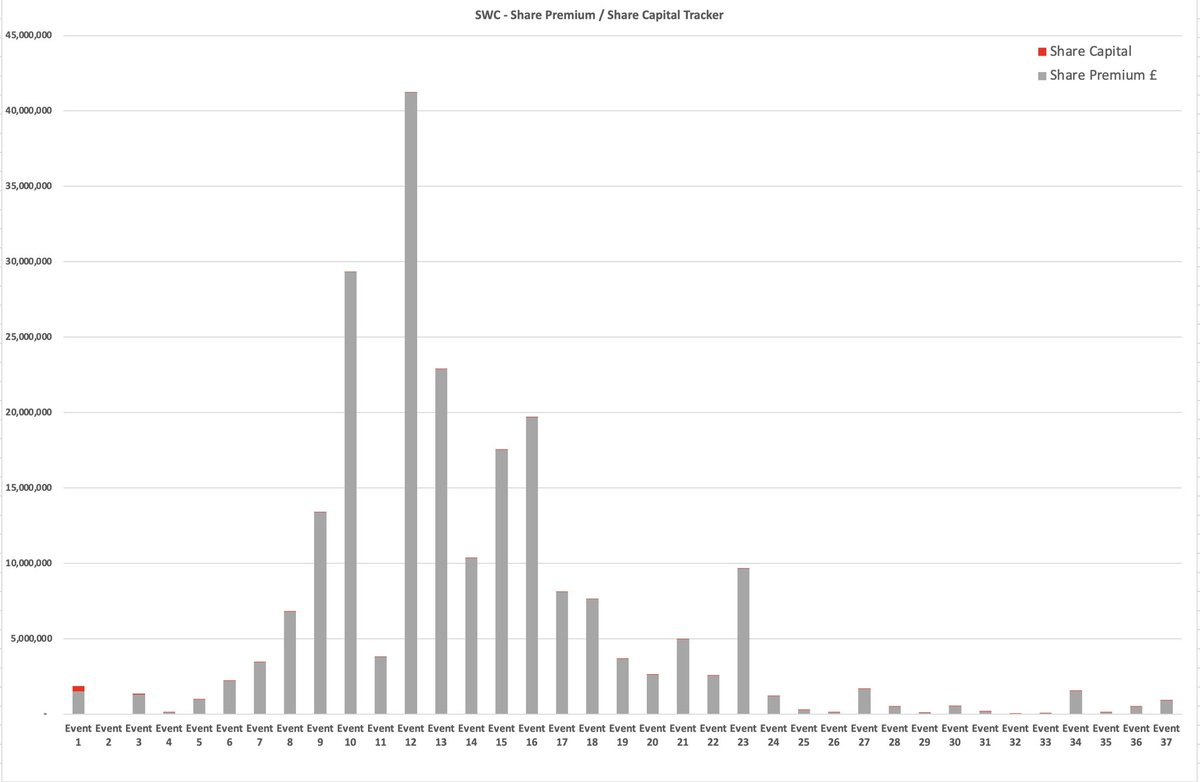

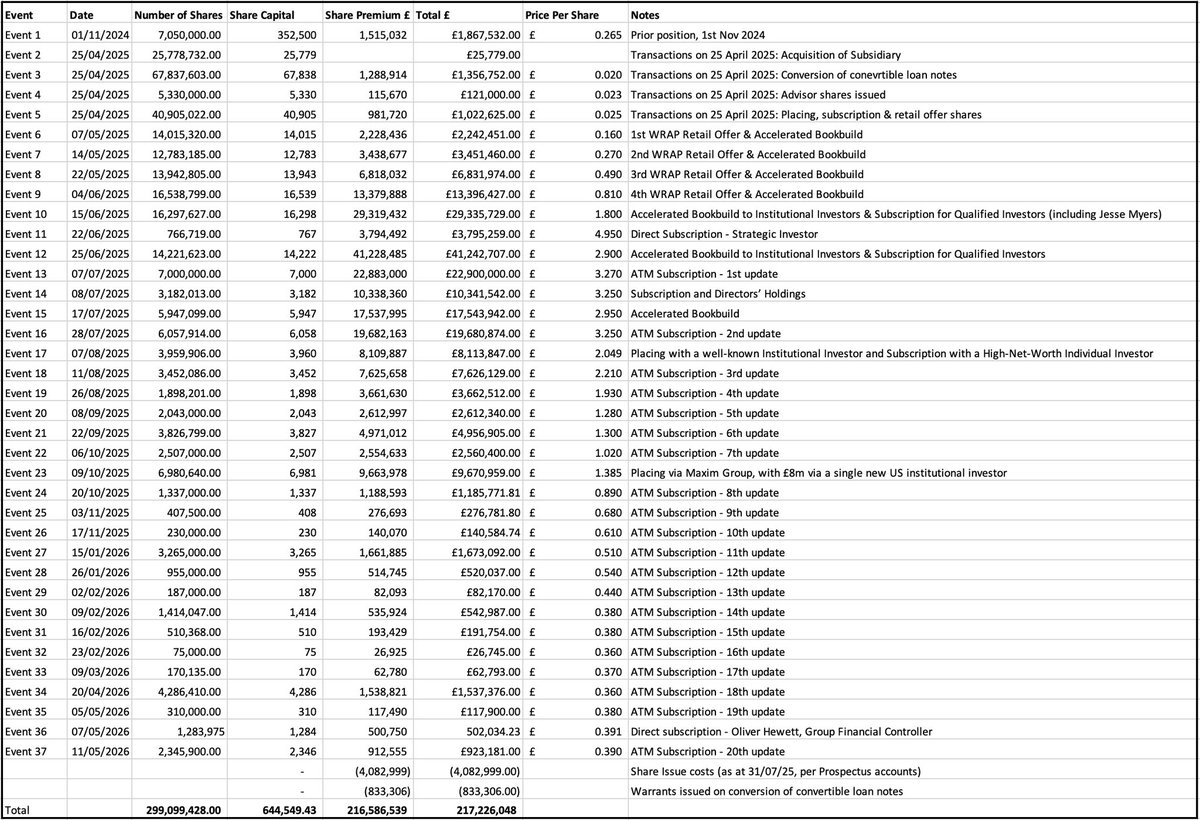

Great article from @medc3005 on @smarterwebuk’s announcement this week.

It highlights just how successful #SWC has been at harnessing investor appetite for a UK-listed Bitcoin treasury over the past 13.5 months. (List of raises in the graph and table below!)

With a nominal share value of just 0.1p for an SWC share, to date each and every WRAP, Accelerated Bookbuild, Direct Subscription and ATM-style share issue has done two things simultaneously:

- Raised cash to acquire more Bitcoin.

- Reflected positively on the Share Premium account, with virtually all of the funds raised being credited there rather than to Share Capital.

£0.001 into the Share Capital column on the books, and then anything between £0.279 and £4.949 into the Share Premium columns on the accounts, for every share sold! (ie upwards of 99.97% of a share is booked as Share Premium)

That Share Premium balance has now (subject to GM vote and the formalising process of court order) helped create £132m of distributable reserves through the proposed capital reduction.

What’s fascinating is that the process is renewable. Every future equity raise has the potential to grow both the Bitcoin treasury and the reservoir from which future distributable reserves may ultimately be created in future rounds.

Watching that reservoir refill could become almost - almost!- as entertaining as watching the Smarter Dashboard’s percolator.

#Bitcoin #SWC #TSWCF #3M8

Jun 4

@smarterwebuk is cancelling £210M of share premium.

A dividend war chest, for a share class that will never get a dividend.

So who’s it really for? 🤔

The RNS doesn’t say “preferred” - but @asjwebley says Q4 is “a long time to wait.”

I break the situation down below for @BTCtreasuries 👇

Thank you to @ZynxBTC and @0xbenharvey for your analysis which is included in the article.

2

23

1,229

Jun 5

Δημοσιεύματα αναφέρουν ότι η SpaceX φέρεται να έχει θέσει όρους για πιθανή IPO στα 135 δολάρια ανά μετοχή, με στόχο άντλησης περίπου 75 δισ. δολαρίων μέσω 555,6 εκατ. μετοχών, που θα αποτιμούσαν την εταιρεία στα 1,75 τρισ. δολάρια.

Σύμφωνα με τις ίδιες πληροφορίες, η διαδικασία προσέλκυσης επενδυτών (roadshow) θα ξεκινήσει μέσω θεσμικών εντολών στο σύστημα Equity Bookbuild της S&P Global, με ισχυρή ζήτηση να αναμένεται και δυνατότητα υπερδιάθεσης μετοχών.

Αναφέρεται επίσης ότι η διαπραγμάτευση θα μπορούσε να ξεκινήσει γύρω στις 12 Ιουνίου, με πιθανή ένταξη σε δείκτες και αυξημένη πίεση στα συστήματα των αγορών κεφαλαίου.

Δεν υπάρχει μέχρι στιγμής επίσημη επιβεβαίωση για τα παραπάνω στοιχεία.

#SpaceXIPO #StockMarket #InvestingNews

2

50

El roadshow comienza con órdenes institucionales procesadas a través de la plataforma Equity Bookbuild de S&P Global.

Se espera una demanda histórica, con posibilidad de sobre asignación disponible. Es probable que el listado inicie alrededor del 12 de junio, con posible inclusión en índices y una fuerte tensión anticipada sobre los principales sistemas de los mercados de capitales.

1

2

499

Jun 4

$SPCX

스페이스X IPO가 750억 달러 기록을 세운 상장 조건 설정

스페이스X는 주당 135달러로 IPO 조건을 설정하여 5억 5,560만 주를 통해 약 750억 달러를 조달했으며

이는 1조 7,500억 달러의 기업 가치를 암시합니다.

로드쇼는 S&P Global의 Equity Bookbuild 플랫폼을 통해 기관 주문이 처리되면서 시작됩니다.

수요는 기록을 세울 것으로 예상되며, 선택적 주식 초과 배정이 가능합니다.

거래는 6월 12일경 시작될 가능성이 있으며, 잠재적 지수 편입과 주요 자본 시장 시스템 부하가 예상됩니다.

6/12 위아래위아래 차트 예정

Jun 4

$SPCX - SPACEX IPO SETS $75B RECORD LISTING TERMS

SpaceX set IPO terms at $135 per share, raising about $75 billion through 555.6 million shares, implying a $1.75 trillion valuation. The roadshow begins with institutional orders processed via S&P Global’s Equity Bookbuild platform. Demand is expected to be record-setting, with optional share over-allotments available. Trading is likely to start around June 12, with potential index inclusion and major capital markets system strain anticipated.

1

4

2,168