Small businesses miss 60-80% of incoming calls. CallFlow fixes that. AI answering, scheduling, and follow-ups for local service businesses — done-for-you. callflow-10.polsia.app

9

Hey I have been building veloxquant MLX and callflow tracer would like to know your thoughts on

veloxquant-mlx.netlify.app/ it's ready with documentation. Would like to come to SF.

1

40

Jun 8

Call flow design is not just technical setup, it directly impacts customer experience and revenue. We build structured routing systems so calls reach the right person without delays or confusion.

Ready to build a system that works for your team? Get in touch with us today: 📞 (336) 544-4000 🌐 carolinadigitalphone.com

#CallFlow #CarolinaDigitalPhone #BusinessCommunication #VoIPSystem #CustomerExperience #SmallBusinessTools #GreensboroNC #TechInfrastructure #CallRouting #BusinessEfficiency

10

Call flow design is not just technical setup, it directly impacts customer experience and revenue. We build structured routing systems so calls reach the right person without delays or confusion.

Ready to build a system that works for your team? Get in touch with us today: 📞 (336) 544-4000 🌐 carolinadigitalphone.com

#CallFlow #CarolinaDigitalPhone #BusinessCommunication #VoIPSystem #CustomerExperience #SmallBusinessTools #GreensboroNC #TechInfrastructure #CallRouting #BusinessEfficiency

8

Jun 4

Thanks. Please contact us here:https: //www.amazon.com/message-us?callflow=cde2af36-99d9-4560-95df-2960f01c58d4&muClientName=socialMedia&t=1780600245025¶digm=social_media_escalation&contextData={"orderId":"43956133","customerSelectedIssues":" Customer Post: https://x.com/auxsyko/status/2062612402479267982 Vertical: Consumer"}&sig=WFXVNvNMsmRdPu4AR9WJkSQl 2L/aZ7t bsp8GEKbGs67c5LGOf1LAnEk7e7EWe2kQlLd8L j6aLrsQtoYMhzd Y6ruJiTRqE9URxjlaUXYfBMhopmJLHnH5O9OV4Xh/ dDRnGnQb6OTu2tueqfck4clxUm8zXH gHSP57K 1EygHuiHz4Muf23NDu6nF8twwApr6IgRR/RepoTvw42Vl2PZadiuMWEKdqoliRmGI6oJ6yZJ/1B22dMrhn7FWGt791qOz0JFxobSVDF2RA0EG/5agt5kt3uRw1Wt3cyAwys6aFPENyOnpnXL fx3qJZxWvlNLdynagckaUxHnu9rA==. This escalated support link will remain available for one hour. -Tyler

1

33

لما شخص يتصل بك، كيف بتعرف الشبكة مكانك بالظبط وخلال أجزاء من الثانية بيرن تليفونك⁉

في عالم الـ Core Network، لما بتوصل مكالمة من شبكة خارجية، بتروح أولاً لبوابة الشبكة الأصلية واللي هي الـ Gateway MSC (GMSC). المشكلة الكبيرة هون، إن الشبكة مستحيل تعرف موقعك اللحظي والجغرافي بدقة بمجرد النظر لرقم تليفك المكتوب

عشان ينحل هاد اللغز الميداني، بيبدأ دور الـ HLR (قاعدة البيانات الرئيسية) اللي بيروح يستعلم فوراً من الـ VLR (قاعدة البيانات المؤقتة للمنطقة اللي أنت متواجد فيها حالياً)، وبيطلب منه معرف سري ومؤقت اسمه MSRN (Mobile Station Roaming Number).

هل سبق وفكرت شو اللي بيصير خلف الكواليس وبخلايا الشبكة من لحظة ما تضغط "اتصال" لحد ما يظهر الرنين عند الطرف الثاني؟ شاركنا في التعليقات!

#CoreNetwork #CS_Core #GMSC #CallFlow #TelecomEngineering #أكاديمية_اتصالاتي

1

20

1,233

Apr 23

We see that the link shared earlier has expired. Please connect with our team over chat here: ahttps://www.amazon.in/message-us?callflow=f862ed54-436e-4db2-a80c-0bd24a9970a4&muClientName=socialMedia&t=1776942895904¶digm=social_media_escalation&contextData={"orderId":"43416163","customerSelectedIssues":" Customer Post: 43416163 Vertical: Consumer"}&sig=uFBnWTQPiJtOR63Png6j913IC58yp0OaiAjNVq9sjjVMBmlgkFR0RLWTu2eD7IzOxTlj43WeS6O1SRSyF0rZlyIyecN7KCONtCGEnluhCNnJPDtnFc0G3l4BKFeXIdtZpkdcRQ3vDD lRlHksx6MfTq8hgNi/1iRJtGDZd8FDQGeku3gHAPFh5sEQZ3 D9SRKMtKzRvm2bvo0yA/f9oGMuMsJek8IO6nUX9ZZLXh1yrOPMnkvnHj w/yTKJIEe0MrCQoOg3QQ7kMGZYLxUnPVtv3cK15dH3tKxpmcyhmoVqwJLaRDaOBN2n 5UKUVsSLK1BgQe3ckI2cx0 BHS9i2w==, so that we will check and assist you accordingly. Please be informed that the link mentioned will stay active for 1 hour.

X being a social platform, we won't be able to arrange a call. We request you to refrain from using profanity language.

-Sankita

2

12

Apr 14

מסתבר שממש לאחרונה קרן פורטיסימו רכשו את החברה (CallFlow) בכ-100 מליון ש"ח

@Omri_z

1

14

3,269

GM 🍇

Día 58/100

Hoy puliendo CallFlow:

Sube tu Excel.

Configura tu mensaje.

CallFlow hace las llamadas, envía emails, agenda citas.

Tú solo cierras.

Sales automation sin fricciones.

call-automation-saas.vercel.…

Mientras tanto: infra de los 25 lugares de xn--godnez-5va.ai para @synthesis_md lista.

Ahora a validar PMF.

LFG 🔥

2

4

78

Mar 11

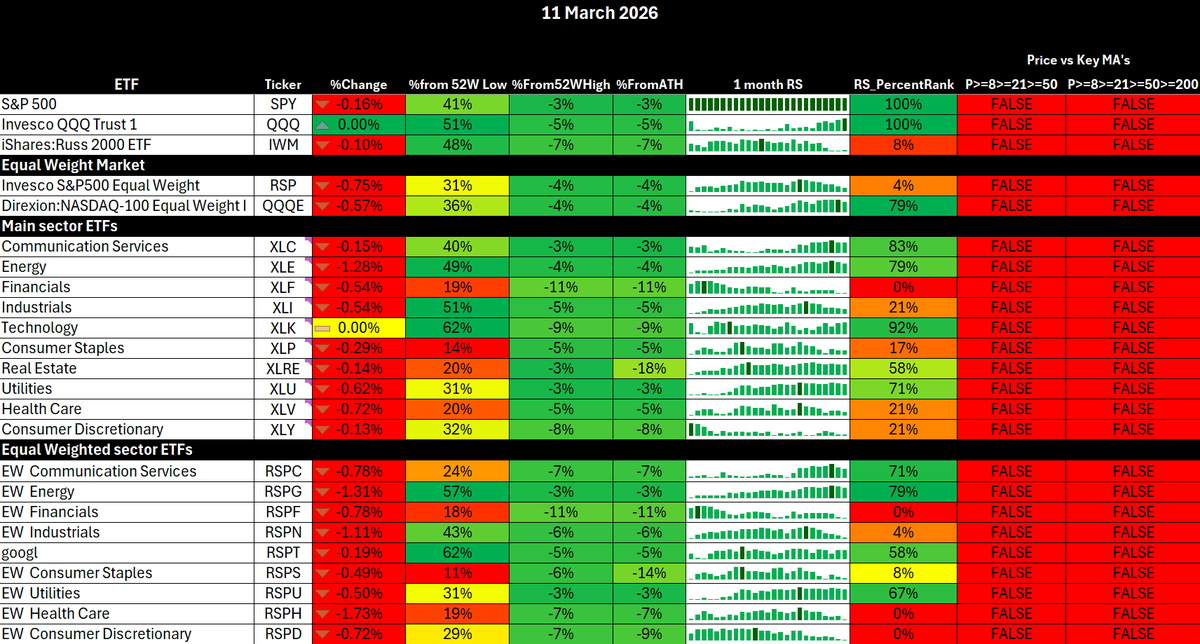

Pre-market analysis – Wednesday 11th March 2026

1. Market Summary

$SPY followed Monday’s sharp squeeze with a failed continuation attempt yesterday. Price opened 677.26, pushed to 683.37 just under the 50-day EMA, and then reversed hard on renewed Middle East geopolitical headlines to close 677.07, essentially flat.

The late-day rejection is the key signal. Markets tried to reclaim intermediate resistance and failed. In a fragile macro environment that type of failure usually leads to continued tactical volatility rather than immediate trend recovery.

We are currently in a balanced but unstable regime:

• Index still below key short-term MAs

• Volatility elevated

• Macro catalysts dominating price discovery

• Institutional options flow increasingly tactical

• Consistent mid-term callflow evident in tech/QQQ

Near-term path remains two-sided:

Bull case

Geopolitical de-escalation or positioning unwind could trigger a violent upside squeeze toward ATH zones.

Bear case

Distribution pattern elevated vol structure suggests a retracement toward weekly lows remains probable in coming weeks.

For now this remains a trader’s market rather than a swing investor’s market. Your focus on index scalping and short-duration momentum trades is exactly the correct playbook in this regime.

2. Macro analysis

The major catalyst today is US CPI.

Consensus expectation:

2.5% YoY headline inflation

Initial CPI prints have broadly come in line, which means the report itself is unlikely to reset the macro narrative immediately.

However several macro factors still dominate:

US

• CPI in line but recent oil spike not yet fully reflected

• Oil stabilising near $88 after a strong rally

• FOMC decision next week remains the major macro catalyst

Geopolitics

• Middle East tensions continue to be the primary short-term market driver

• Yesterday’s late session selloff was directly tied to war headlines

Europe / China / Japan

• No major new policy surprises overnight

• Global macro backdrop still risk-sensitive to energy and geopolitical flows

Conclusion:

The CPI itself may not move markets dramatically, but geopolitics and oil will likely dominate the next few weeks.

3. Momentum and breadth

Momentum structure remains weak.

Key observations:

• $SPY remains below the all key moving averages

• Distribution characteristics visible in recent selloffs (impulse gap down moves followed by slow, low volume retracements)

Breadth has also deteriorated recently:

• Small caps continue to underperform

• Equal-weight indices failing to lead

• Momentum leadership fragmented

This confirms we are not in a broad risk-on environment.

Instead we have tactical rotations and squeezes driven by positioning and volatility.

4. Volatility

Volatility regime remains elevated and unstable.

$VIX

Range yesterday: 22.14 – 26.17

Close near 25

$VVIX

Opened 128

Spent most of the session around 116

Spiked back above 120 on geopolitics

Critical signals:

• VIX term structure remains in backwardation

• VVIX elevated

• Volatility risk premium rising again

Backwardation historically means:

• Market stress remains present

• Probability of additional volatility spikes remains high

= Another volatility expansion is likely soon.

5. Credit and liquidity

Liquidity conditions remain fragile.

Observations:

• Market on close yesterday was 762m buy imbalance, suggesting late positioning support

• Oil price shock acting as a macro liquidity drain through inflation expectations

Credit markets are not yet flashing systemic risk, but they are not supporting risk-on either.

Net interpretation:

Liquidity is neutral to slightly risk-off.

6. ETF and Sector rotation

Index ETFs

Defensive sectors showing relative resilience

Strongest relative performance from:

• XLC Communication Services

• XLU Utilities

• XLE Energy

This reflects the current macro environment:

Energy strength = geopolitical risk

Utilities strength = defensive rotation

Cyclical and growth laggards

Weakest sectors currently include:

• XLRE Real Estate

• XLF Financials

• XLY Consumer Discretionary

• XLK Technology

These are classic risk-on cyclical sectors, and their weakness confirms risk appetite remains suppressed.

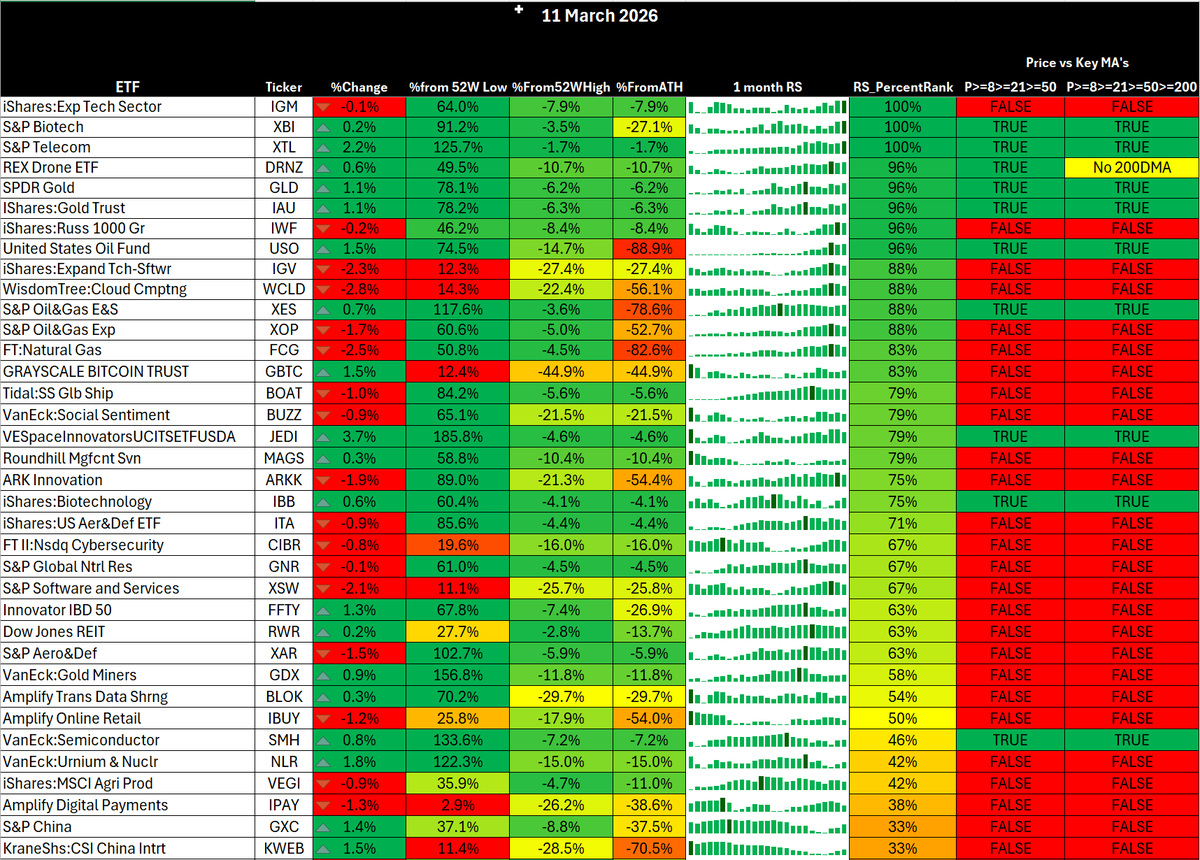

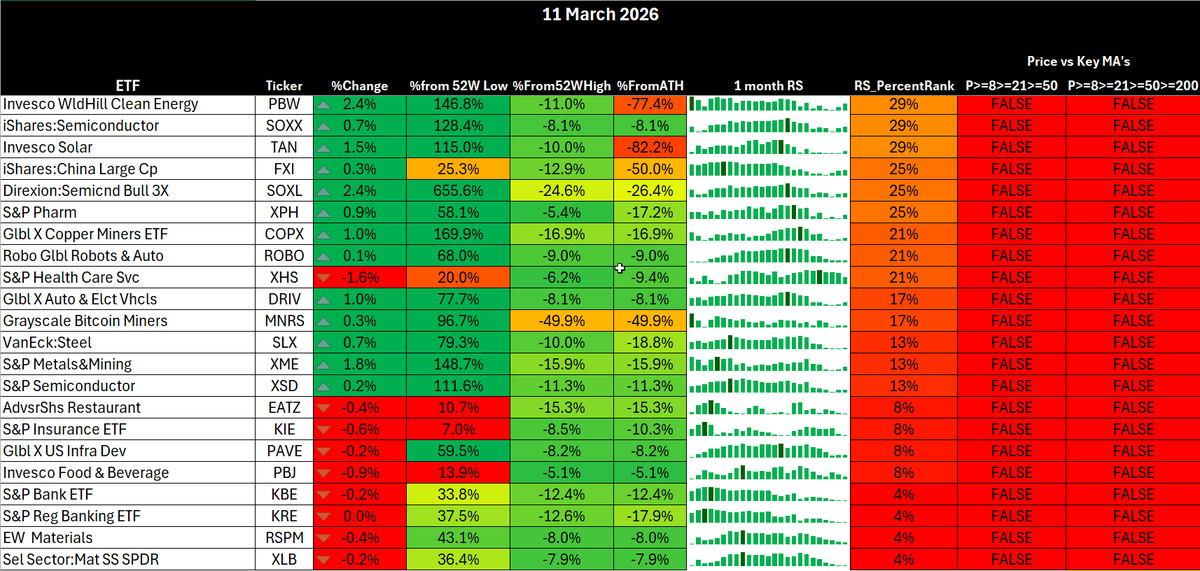

High RS thematic sectors

Relative pockets remain in:

• Telecom / communications

• defence and drone ETFs

• energy complex

Meanwhile large drawdowns are visible in:

• cloud software

• biotech

• speculative growth

Key takeaway

The rotation profile remains defensive and macro-driven, not growth driven.

7. Summary

Market regime remains high volatility and tactical.

Key signals:

• $SPY failed reclaim of 50DMA

• Volatility structure still stressed

• Geopolitics dominating price discovery

• Sector leadership defensive

This aligns strongly with what I've been trading: short-duration index momentum trades rather than directional swings.

My bias:

Short term

Neutral to slightly bearish.

Medium term

High probability of a deeper corrective move to backtest recently lows near the 200DMA within the coming weeks.

However the path there will likely include violent squeezes and positioning unwinds.

Tactical framework

Best strategies in this environment:

• Index scalping ($SPX, $NQ)

• Tactical options flow tracking

• Relative strength setups only

• Reduced size due to volatility

2

1

5

248

13 Oct 2025

I cannot share much about my callflow but im straight up not having a good time

3

321

11 Oct 2025

Days like today hurt alot of the momo #CallFlow traders.

The theta acceleration and delta drops are hard to come back from unless you have longer dated expirations, like 180 days

Was saying last night on The Wheelers Live event with @TJTheWheelDeal that we really need a healthy pullback for the market to level off some of the froth since April's lows.

Today, the #Market found it's reason to sell and it was harsh.

Size-management is the best #defense in sell-offs.

Continuously paying for #hedge trades depletes valuable cash. Sizing is the key.

Let's see what Monday and next week brings before we start worrying about anything more than just a heathy pullback.

2

4

1,138

7 Oct 2025

$EBS

A name we entered off #UnusualOptionsActivity is finding some hefty buying today.

Beautiful looking chart with room to go to $12-15

We are very picky with #UOA and #CallFlow

I really like this one higher

6

536

28 Sep 2025

Been in $RR since February. Love the chart and #CallFlow.

You seem conservative with the $7 price target.

ATH is $12.29 and that is just one really good news event away.

I'd say $20-30 by this time next year is very possible if not sooner.

Huge short float and only 103M shares outstanding.

2

10

1,206

27 Sep 2025

👀 Aot of players eyes on $RR and now posting on it.

🤗 That's GREAT.

📅 We've been in since February and been adding.

🐳Huge #CallFlow in the last 10 minutes today.

📢 Feels like a news event on the horizon.

👔 They have ties to $NVDA.

🤝#Event coming up in October has potential to SEND IT.

📈 Recently had Options made available and now it's game on.

💰 We are sitting on huge gains and expecting more.

👉👉👉Possibly #PreMarket Monday

👇 Here are some Trade fills from 1 of MANY accounts that hold in over here.

3

581

21 Sep 2025

$DDD a smallie we are in off #UnusualOptionsActivity for a few weeks now.

We are patient.

We don't chase just any #CallFlow

Chart is looking primed for the #200sma attack very soon(imho)

Position is already 350% but the TA suggests we have more to get out of it.

Running with 401 deltas

Anyone in this?

#OptionsSellingInstitute

1

2

1,205

16 Sep 2025

🚀 $RR

✅ This is from May.

👉 Gave this to you at $2

💰 Today, pushing $4.25 here

🏃♂️ We are in #Stock, #Calls, #CallSpreads

AND... the #CallFlow is flying in.

Like it to $6-8 area

27 May 2025

29% today. Great little company with huge potential.

Great sector which is heating up. I like Robotics in 2025 and there's a multitude of names to choose from to play.

Hope you got in on this post a month ago. ⬇️

$RR

1

2

708

15 Sep 2025

$RR 64 million shares trading her at 3:30pm.

~16.5% #shortinterest

4.12x #RelativeVolume

#CallFlow on multiple strikes / expiries

#Breakout on the daily of prior #Resistance

#OptionsSellingInstitute

#UnusualOptionsActivity

1

9

674