Jun 12

$CMPS

“The addressable market for treatment-resistant depression is expanding into a multi-billion-dollar opportunity, with Compass positioned to compete directly against existing therapies such as Spravato while offering potentially longer-lasting effects.

Strategically, the company is viewed as an attractive acquisition target for large pharmaceutical players seeking CNS exposure, with potential interest from AbbVie, AstraZeneca, and Johnson & Johnson. Overall, Compass Pathways represents a high-conviction opportunity with $19 to $22 price targets and substantial upside as commercialization approaches into 2027 period.

Phase 3 results across COMP005 and COMP006 showed clinically meaningful MADRS improvements with durable response signals and a strong safety profile, including low serious adverse event rates. These data support a high probability of regulatory approval and underpin a base-case valuation framework that suggests significant upside relative to the current share price.”

finance.yahoo.com/markets/st…

1

3

15

890

Compass Pathways shares fell sharply during afternoon trading, pulling back from recent highs despite the absence of any company-specific negative news. The stock had been trading near its 52-week high of $14.76 following a strong rally fueled by positive clinical and corporate developments in recent weeks. The decline appeared to coincide with a broader market selloff that weighed heavily on high-beta biotechnology stocks, particularly pre-revenue companies.

Investors may also be taking profits and reducing exposure ahead of the highly anticipated 26-week durability data from the Phase 3 COMP006 trial of COMP360, expected in early Q3 2026. The readout is considered a major catalyst that could significantly impact the stock in either direction. Earlier Phase 3 studies, including COMP005 and COMP006, met their primary endpoints at Week 6, demonstrating statistically significant improvements in treatment-resistant depression.

$CMPS

593

Jun 3

$CMPS $DFTX $ATAI

Psychedelics - A Multi-Billion Dollar Opportunity

Mental health is deteriorating on a massive scale. Depression, anxiety, PTSD, and related conditions affect hundreds of millions globally. At the same moment, psychedelics are entering the mainstream backed by rigorous clinical science. This creates a powerful alignment: real solutions for patients who have run out of options, and a clear commercial path for the companies executing at the highest level.

$CMPS – Compass Pathways

Lead candidate: COMP360 (proprietary synthetic psilocybin).

COMP360 has delivered positive results in two pivotal Phase 3 trials for treatment-resistant depression (TRD). COMP005 (single 25 mg dose vs placebo) and COMP006 (two 25 mg doses) both met primary endpoints with statistically significant MADRS reductions (~3.6–3.8 points at Week 6, p<0.001), rapid onset (often next-day), and generally favorable tolerability — most adverse events mild and resolving quickly. Longer-term durability data is pending. The company is advancing toward NDA submission (targeting late 2026) with Breakthrough Therapy Designation. An NDA, or New Drug Application, is the formal submission to the FDA requesting approval to market and sell a new drug in the United States after clinical trials demonstrate safety and efficacy.

Additional exploration in PTSD and anorexia nervosa (Phase 2). TRD affects millions with high unmet need; a fast-acting, infrequent-dosing therapy could transform care and generate peak sales potential in the billions as adoption scales in specialized settings.

$DFTX – Definium Therapeutics (rebranded from MindMed)

Lead candidate: DT120 (lysergide tartrate — pharmaceutical-grade LSD in orally disintegrating tablet form).

DT120 is advancing in a robust Phase 3 program: Emerge (major depressive disorder / MDD, with topline expected late Q2 2026), Ascend (second MDD study), and two generalized anxiety disorder (GAD) trials (Voyage and Panorama, with readouts across 2026). This creates multiple near-term catalysts. A separate asset, DT402 (R-enantiomer of MDMA), is in Phase 2a for autism spectrum disorder.

MDD and GAD represent enormous markets where daily medications leave many patients underserved. DT120’s profile — single/few administrations with potential for rapid, sustained relief — could differentiate strongly if Phase 3 data confirms earlier signals, supporting broad approval and significant commercial upside.

$ATAI – AtaiBeckley

A diversified pipeline with multiple assets and administration formats:

• BPL-003 (mebufotenin benzoate nasal spray): Positive Phase 2b in TRD showing rapid and durable antidepressant effects. Phase 3 program (ReConnection) on track to initiate in Q2 2026 following successful FDA End-of-Phase 2 meeting.

• VLS-01 (DMT buccal film): Phase 2 Elumina trial in TRD; topline data expected H2 2026.

• EMP-01 (oral R-MDMA): Positive Phase 2a in social anxiety disorder, with clinically meaningful improvements on LSAS scale and good tolerability.

This multi-shot strategy targets TRD, anxiety, and related disorders with convenient delivery (nasal/buccal/oral), potentially broadening patient access and peak revenue opportunities across indications.

Path to Multi-Billion Revenue

These psychedelic programs target massive MDD, GAD, and TRD markets where rapid-onset, durable therapies can command premium clinic-based reimbursement, driving potential peak sales into the billions per asset. Late-stage CNS biotechs have historically seen 3–10x market cap explosions on pivotal successes and approvals; currently mid-cap, $CMPS, $DFTX, and $ATAI could reach $8B–$20B valuations, implying major share price upside if these companies execute.

I’m optimistic and excited to see how this space evolves through the remainder of 2026.

2

3

31

1,777

May 27

Readouts and data for the next six months in case you forgot 👀

Definium Therapeutics $DFTX

——————————————

1. Emerge PH3 Readout (Major Depressive Disorder) - Late Q2 2026

2. Voyage PH3 Readout (Generalized Anxiety Disorder) - Early Q3 2026

3. Panorama PH3 Readout (Generalized Anxiety Disorder) - Late Q3 2026

Compass Pathways $CMPS

—————————————

1. COMP006 26-week Part B Data - Early Q3 2026

2. Expected Final FDA Submission - Early Q4 2026

ATAIBeckley $ATAI

—————————

1. PH3 Initation Expected in Q2 2026 for Treatment-Resistant Depression

2. Elumina PH2 Readout - Q4 2026

GH Research $GHRS

——————————

1. PH3 Initiation Expected in Late 2026

Helus Pharma $HELP

——————————

1. Approach PH3 Readout Expected for Major Depressive Disorder in Q4 2026

What a year 🙏

1

7

992

May 13

🚨 COMPASS PATHWAYS UP 14% ON EARNINGS

$CMPS is one of my two new positions from Q1 2026 (the second one being $NOW). Deep dive analysis coming this Friday!

EARNINGS

The company just moved one step closer to becoming the first real psychedelic blockbuster story.

This is no longer just “interesting science”. It is now a real regulatory, commercial, and financing story.

The News

Compass reported Q1 2026 results and confirmed that the FDA has granted a rolling NDA submission and review request for COMP360, its synthetic psilocybin therapy for treatment-resistant depression.

Sections of the NDA have already been submitted, with the final package still on track for Q4 2026. The next key catalyst is 26-week COMP006 Part B data, expected in early Q3 2026.

The company also received a Commissioner’s National Priority Review Voucher, which could compress FDA review to roughly 1-2 months after filing, while maintaining the standard FDA safety and efficacy review process.

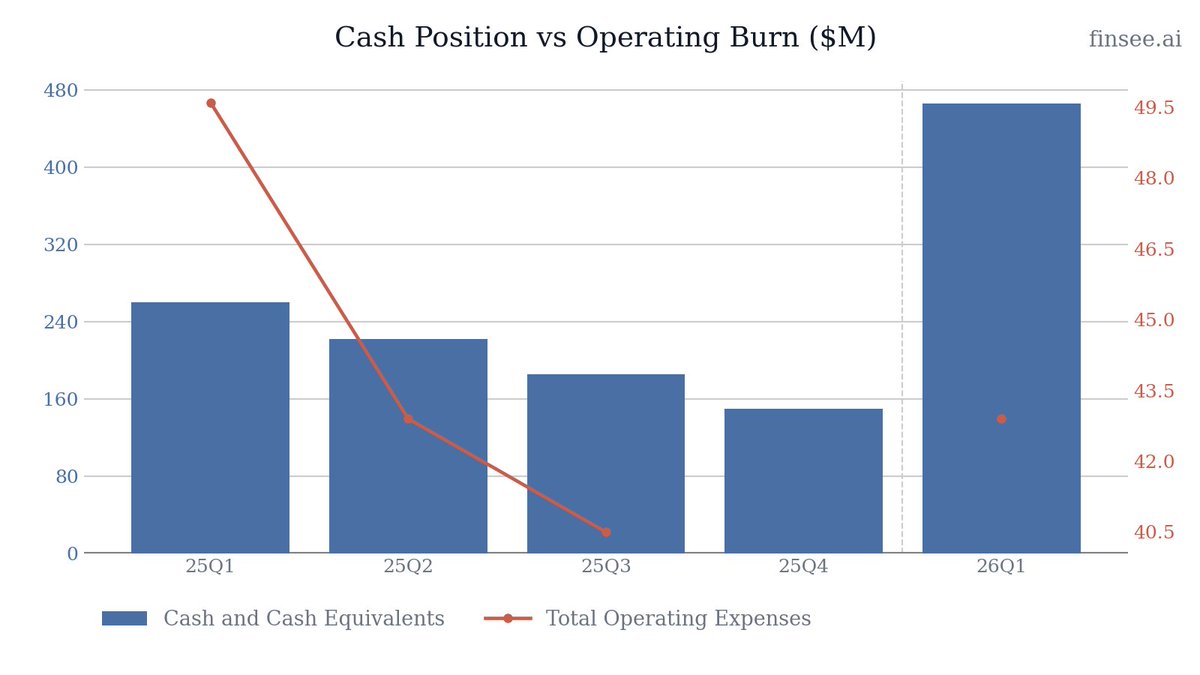

Financially, Compass ended Q1 with $466 million in cash, up from $149.6 million at year-end 2025, giving it runway into 2028, i.e. well beyond a potential launch window.

Net income of $91.2 million looks optically strong, but it was mainly driven by a $130.9 million non-cash warrant fair value gain, not recurring operating profitability (we'd be much higher in that case :).

My Take

This is a genuinely important update.

For a long time, CMPS was a high-risk psychedelic biotech with promising data, massive theoretical upside, and major uncertainty around regulation, funding, infrastructure, and commercial adoption.

Today’s update does't really eliminate those risks but it clearly reduces several of them.

The FDA path is moving faster than expected. The company is not running out of cash before the critical moment. The launch machine is already being built. And COMP360 now has one of the cleanest shots at becoming the first major approved classic psychedelic therapy in the US.

The key distinction which one needs to bear in mind is that this is still not a “safe” biotech. Approval, scheduling, payer coverage, physician adoption, and real-world treatment logistics all remain serious hurdles. This is still just the beginning, way too early to be safe.

But the story has undoubtedly shifted. The question is becoming less of a typical biotech "Can Compass survive long enough to get there?”, aand more of “How large can the COMP360 commercial opportunity actually become if approval lands?”

Verdict: Bullish, but still high-risk bullish

This is a major regulatory and balance sheet de-risking event. Not quite a victory lap yet. But definitely a thesis-strengthening update for me.

The full analysis coming this Friday to SS!

1

6

1,528

May 13

$CMPS Q1 2026 earnings: Massive Cash Influx Secures Launch Runway as Regulatory Path Accelerates

Compass Pathways drastically altered its risk profile this quarter. A successful financing pushed cash reserves to $466M, extending its operational runway into 2028 and erasing near-term dilution fears. On the regulatory front, the FDA granted a rolling NDA submission and a Priority Review Voucher (CNPV), clearing the path for a Q4 2026 final submission. While reported Net Income was a positive $91.2M, this is purely an accounting illusion driven by a $130.9M warrant valuation gain. The core story is strong: operating burn is decelerating, and the company is fully funded for its commercial launch.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐅𝐮𝐥𝐥𝐲 𝐅𝐮𝐧𝐝𝐞𝐝 𝐓𝐡𝐫𝐨𝐮𝐠𝐡 𝐋𝐚𝐮𝐧𝐜𝐡 — The $466M cash balance eliminates near-term financing overhang. The company is now comfortably funded into 2028, well past the anticipated COMP360 commercial rollout.

• 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐃𝐞-𝐑𝐢𝐬𝐤𝐢𝐧𝐠 — Securing a rolling NDA and the Commissioner's National Priority Review Voucher (CNPV) shortens the FDA review timeline by 1-2 months and reflects high agency willingness to advance the therapy.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐅𝐢𝐧𝐚𝐥 𝐃𝐚𝐭𝐚 𝐆𝐚𝐭𝐢𝐧𝐠 𝐈𝐭𝐞𝐦 — The final NDA submission remains contingent on the 26-week (Part B) data from the COMP006 trial, expected in early Q3 2026. Any safety signals or durability drop-offs here could derail the Q4 timeline.

• 𝐑𝐞𝐬𝐜𝐡𝐞𝐝𝐮𝐥𝐢𝐧𝐠 𝐑𝐞𝐥𝐢𝐚𝐧𝐜𝐞 — Even with FDA approval, commercialization hinges on swift DEA rescheduling. Delays at the federal or state level could create a frustrating gap between approval and revenue generation.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. For a pre-revenue biotech, cash runway and regulatory momentum are the only metrics that matter. Compass secured both this quarter. The massive cash injection and rolling NDA status shift the narrative from 'will they survive to launch?' to 'how big will the launch be?'.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐓𝐢𝐦𝐞𝐥𝐢𝐧𝐞𝐬 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 [NEW]

Management confirmed that approval timelines are tracking to their fastest projected expectations. The FDA granted a rolling New Drug Application (NDA) submission, meaning sections are already being reviewed. Crucially, COMPASS was awarded a CNPV, which could shave 1-2 months off the final review time. This regulatory tailwind is a massive de-risking event.

🟢 𝐌𝐚𝐜𝐫𝐨 𝐒𝐮𝐩𝐩𝐨𝐫𝐭: 𝐖𝐡𝐢𝐭𝐞 𝐇𝐨𝐮𝐬𝐞 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐯𝐞 𝐎𝐫𝐝𝐞𝐫 [NEW]

In a significant macro development, a White House Executive Order on psychedelic treatments now directs the DEA to initiate and complete its review of successfully tested therapies to proceed with rescheduling as quickly as possible. This directly addresses one of the largest systemic bottlenecks for psychedelic commercialization.

🟢 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐃𝐢𝐬𝐜𝐢𝐩𝐥𝐢𝐧𝐞

Operating burn is decelerating. R&D expenses fell to $26.5M from $30.9M YoY, driven by the wind-down of Phase 3 clinical trial costs and the termination of non-core discovery programs. G&A expenses also dropped to $16.4M from $18.7M. This leaner cost structure extends the impact of their new funding.

⚪ 𝐖𝐢𝐥𝐝 𝐄𝐚𝐫𝐧𝐢𝐧𝐠𝐬 𝐕𝐨𝐥𝐚𝐭𝐢𝐥𝐢𝐭𝐲 𝐟𝐫𝐨𝐦 𝐖𝐚𝐫𝐫𝐚𝐧𝐭𝐬 [NEW]

Reported Net Income swung to a massive $91.2M profit (vs an $17.9M loss last year), entirely due to a $130.9M non-cash fair value adjustment on warrant liabilities. Because these liabilities fluctuate with the stock price, investors should expect significant, confusing variability in GAAP net income going forward. This optical noise masks the underlying core cash burn.

🟢 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐨𝐧

Management notes COMP360 is expected to fit into an existing infrastructure of over 7,300 centers capable of multi-hour treatments. However, transitioning from clinical trials to a massive commercial rollout requiring highly trained facilitators and physical space will be capital intensive and carries high execution risk.

🟢 𝐂𝐎𝐌𝐏𝟑𝟔𝟎 𝐓𝐫𝐚𝐧𝐬𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐯𝐞 𝐏𝐫𝐨𝐟𝐢𝐥𝐞 𝐕𝐚𝐥𝐢𝐝𝐚𝐭𝐢𝐨𝐧

COMP360 remains the first classic synthetic psychedelic to achieve highly statistically significant results in large late-stage trials (1,000 participants). Management emphasized durability lasting at least 6 months after one or two doses. This specific technological profile—rapid onset with long durability—is what will differentiate it economically from frequent treatments like Spravato.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 & 𝐃𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬: $26.5 million

Decelerating. R&D dropped 14% YoY from $30.9M. The decrease reflects the natural tapering of clinical trial costs as the Phase 3 TRD program nears completion, as well as the successful execution of corporate restructuring and pipeline pruning initiated in late 2024.

𝐖𝐚𝐫𝐫𝐚𝐧𝐭 𝐋𝐢𝐚𝐛𝐢𝐥𝐢𝐭𝐢𝐞𝐬: $131.9 million

Down significantly from $203.7M at year-end 2025. This liability sits on the balance sheet and creates wild swings in the P&L depending on CMPS stock price movement, representing a non-cash accounting dynamic rather than a fundamental operational risk.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐂𝐚𝐬𝐡 𝐑𝐮𝐧𝐰𝐚𝐲: Into 2028

Accelerating. The company drastically upgraded its cash runway guidance from 'into 2027' to 'into 2028' following a successful financing round and warrant exercises that tripled their cash on hand to $466M.

𝐂𝐎𝐌𝐏𝟎𝟎𝟔 (𝐏𝐚𝐫𝐭 𝐁) 𝟐𝟔-𝐖𝐞𝐞𝐤 𝐃𝐚𝐭𝐚: Early Q3 2026

Stable. The final gating clinical milestone remains on track. This data will unblind the long-term durability and safety metrics necessary to complete the NDA submission.

𝐅𝐢𝐧𝐚𝐥 𝐍𝐃𝐀 𝐒𝐮𝐛𝐦𝐢𝐬𝐬𝐢𝐨𝐧: Q4 2026

Stable. The company remains aligned with previously defined accelerated timing to be 'launch ready' by the end of 2026, leveraging the rolling NDA framework to submit modules sequentially.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐑𝐞𝐬𝐜𝐡𝐞𝐝𝐮𝐥𝐢𝐧𝐠 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲

With the White House Executive Order directing the DEA to move quickly, what is your internal base-case timeline for DEA scheduling post-FDA approval, and how does this impact the 2027 commercial launch curve?

𝐒𝐩𝐞𝐜𝐢𝐚𝐥𝐭𝐲 𝐏𝐡𝐚𝐫𝐦𝐚 𝐏𝐚𝐫𝐭𝐧𝐞𝐫𝐬𝐡𝐢𝐩𝐬

As launch readiness accelerates toward the end of the year, how close are you to finalizing a specialty pharma partner to manage distribution, and what specific economics are you targeting?

𝐏𝐫𝐢𝐜𝐢𝐧𝐠 𝐏𝐨𝐰𝐞𝐫

Given the durability profile (up to 6 months) compared to frequent-dosing alternatives, how are early payer discussions shaping your initial pricing and reimbursement strategy?

1

5

1,319

$CMPS 𝐂𝐨𝐦𝐩𝐚𝐬𝐬 𝐏𝐚𝐭𝐡𝐰𝐚𝐲𝐬: 𝐅𝐃𝐀 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐨𝐧 𝐒𝐭𝐫𝐨𝐧𝐠 𝐂𝐚𝐬𝐡 𝐏𝐨𝐬𝐢𝐭𝐢𝐨𝐧 𝐏𝐮𝐭 𝐂𝐎𝐌𝐏𝟑𝟔𝟎 𝐎𝐧 𝐅𝐚𝐬𝐭 𝐓𝐫𝐚𝐜𝐤

📊 𝐑𝐞𝐬𝐮𝐥𝐭𝐬

• R&D expenses: $26.5M vs $30.9M YoY

• G&A expenses: $16.4M vs $18.7M YoY

• Net income: $91.2M vs net loss of $(17.9)M YoY

• Cash & equivalents: $466.0M vs $149.6M at FY25 end

• Debt: $50.5M vs $31.6M at FY25 end

⠀

🎯 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

• Final COMP360 NDA submission remains on track for Q4 2026

• Company expects current cash position to fund operations into 2028

• Launch readiness targeted by year-end 2026

⠀

📌 𝐊𝐞𝐲 𝐓𝐚𝐤𝐞𝐚𝐰𝐚𝐲𝐬

• FDA granted rolling NDA submission and review request for COMP360

• CNPV awarded, potentially reducing NDA review time to 1–2 months

• 26-week COMP006 Phase 3 data expected in early Q3 2026

• COMP360 showed rapid and durable efficacy across 3 late-stage TRD trials

• Strong financing activity boosted cash runway well beyond launch

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 𝐂𝐨𝐦𝐦𝐞𝐧𝐭𝐚𝐫𝐲

“COMP360 represents a fundamentally different approach for patients with treatment resistant depression.”

5

1,072

Put a 5x buyout multiple on $CMPS peak sales of $1.9B and ?

B.Riley analyst Madison El-Saadi noted that Compass Pathways has a more than two-year lead over psychedelic peers and projected fiscal year 2028 revenue of approximately $221 million compared to a peer median of $106 million. The firm’s two positive Phase 3 trials achieved placebo-adjusted MADRS results in line with Johnson & Johnson’s SPRAVATO while requiring only one to two doses versus eight to ten.

B.Riley set a non-risk-adjusted peak revenue estimate of $1.9 billion based on SPRAVATO’s commercial template. SPRAVATO reached a $2 billion fourth quarter 2025 run-rate.

The firm identified the COMP006 Part B 26-week durability readout in early third quarter 2026 as the most important near-term catalyst, stating a successful print and subsequent NDA submission in fourth quarter 2026 could drive upside of more than 50% from current levels.

2

351

Mar 31

I updated the plots with more data and separated the distributions for major depressive disorder (#MDD) / treatment-resistant depression (#TRD) in #psychedelic vs non-psychedelic interventions. In both cases, the control arms of psychedelic trials show a substantially LOWER #placebo response. This finding is particularly strange when considering that psychedelic trials also involve #therapy (unlike the non-psychedelic interventions), so one would expect elevated placebo responses! How low the placebo response would be without therapy?!

Data sources (sample size is used as weights):

- Non-psychedelic MDD trials: the Cipriani 2018 dataset, e.g. SSRIs/SNRIs

- Psychedelic MDD trials: Griffiths 2016, Ross 2016, Erritzoe 2026, Raison 2023, Rotz 2023

- Psychedelic TRD trials: COMP005 & COMP006, Palhano-Fontes 2019, Mertens 2026, Goodwin 2022, Cubała 2026 (GH001)

- Non-psychedelic TRD trials: Jones 2021 dataset

2

2

19

1,165

Mar 26

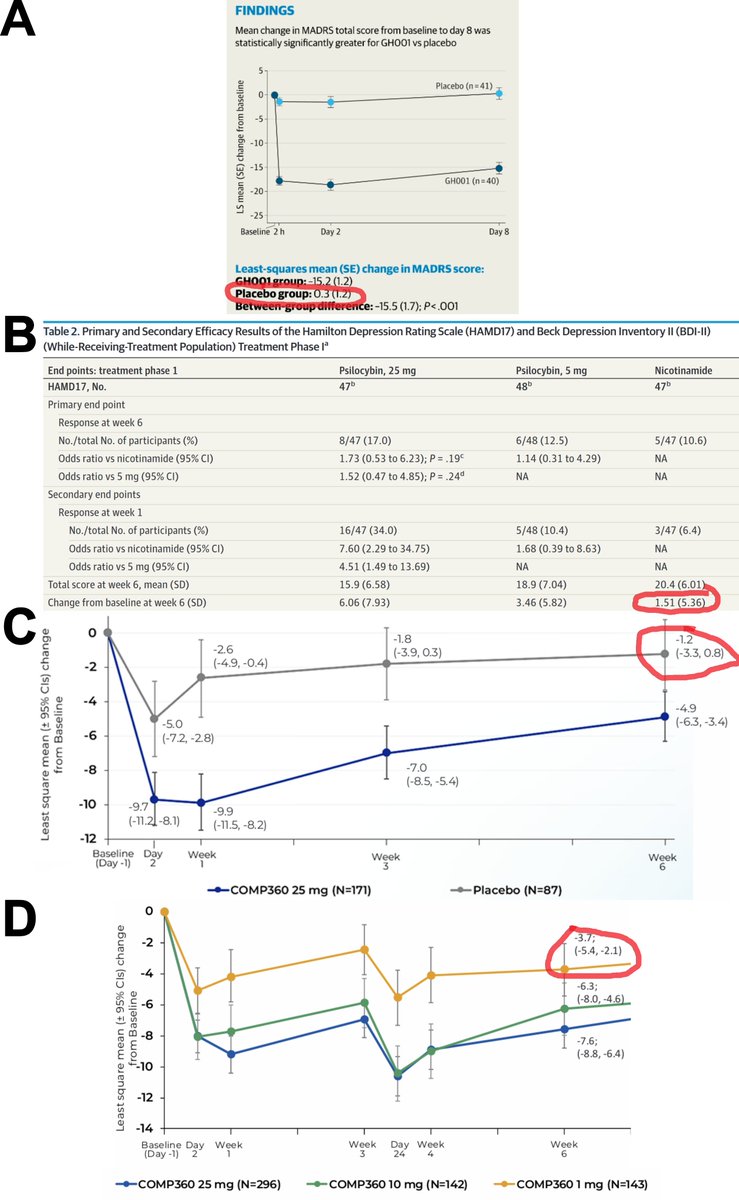

Another day, another psychedelic trial with missing placebo response (tinyurl.com/3pzpxpac), this time with 5-MeO-DMT. In this case the patients actually got WORSE in the placebo group. In the past month, 4 high profile psychedelic trials came out, all on treatment-resistant depression, all showing the same phenomena: there is virtually no placebo response in the control arm of psychedelic studies, see image below (negative values indicate improvement as you want less depression):

A: 5-meo vs PL, placebo response is 0.3 MADRS units (tinyurl.com/3pzpxpac)

B: psilocybin vs active PL (nicotinamide), placebo response is -1.5 MADRS units (tinyurl.com/yueyphn5)

C: psilocybin vs PL, placebo response is -1.2 MADRS units (COMP005 tinyurl.com/cjjmh8x7)

D: psilocybin vs active PL (1mg psilocybin), placebo response -3.7 MADRS units (COMP006 tinyurl.com/cjjmh8x7)

The typical placebo response in trials on major depression of antidepressants is -9 MADRS points (shorturl.at/fwTNs). The typical placebo response in trials on TRD with ketamine -7 MADRS points (shorturl.at/ZS0QQ).

8

13

68

12,703

Mar 19

$CMPS

“Compass is pursuing a rolling submission to the FDA for COMP360 after sharing recent data and meeting with the agency, targeting an NDA late this year with Breakthrough Therapy status potentially accelerating review and an approval decision “end of the year into next year.”

The upcoming 26-week COMP006 results, expected early Q3, are the final durability and safety data for the submission and will be critical to labeling and dosing decisions (e.g., one vs. two doses).

Commercial preparations focus on the TRD market with plans for ~90-day federal rescheduling and a goal of state rescheduling covering ~90% of the U.S. within 30 days, plus site enablement and reimbursement planning (Category III CPT codes); Compass also raised $$150M and says runway extends into 2028.”

marketbeat.com/instant-alert…

3

422

COMP006, CYB003, GH001, BPL-003 — if none of these mean anything to you, you're not paying close enough attention to what's coming in psychedelic pharma.

psymarketcap.com

4

174

$CMPS Compass Pathways just released topline data from two pivotal Phase 3 trials (COMP005 & COMP006) for COMP360 (psilocybin) in Treatment-Resistant Depression.

Bottom line: The trials worked. Both met their primary endpoints with high statistical significance (p<0.001). 🧵👇

6

3

531

Compass Pathways plc $CMPS priced a $150M public offering of 17.5M ADSs at $8.00 per share plus 1.25M pre-funded warrants, with a 30-day option for up to 2.8M additional ADSs, strengthening its balance sheet to fund Phase 3 COMP005 and COMP006 trials, advance its Phase 2b/3 COMP360 PTSD program, and support commercial readiness activities.

2

135

Feb 18

$CMPS

RBC Capital raised the firm's price target on Compass Pathways to $22 from $21 and keeps an Outperform rating on the shares after the company announced that it has achieved primary endpoint in Phase 3 trial of COMP006 for treatment-resistant depression. There were no red flags in the data and the firm sees COMP360 as effective in treating treatment-resistant depression, with durable long-lasting effects out to 6 months in patients who respond with just 1 or 2 doses and all with a simple dosing schedule and clean safety profile, the analyst tells investors in a research note.

Feb 18

$CMPS

Canaccord 20 from 15

Morgan Stanley 18 from 11

Canaccord analyst Sumant Kulkarni raised the firm's price target on Compass Pathways to $20 from $15 and keeps a Buy rating on the shares. The firm noted they announced the much-awaited Phase 3 data for COMP360 (psilocybin) in treatment-resistant depression (TRD). With these results, CMPS has now reported two Phase 3 trials (COMP005/006) in which COMP360 met its primary endpoints and hit statistical significance. We view these data, which were consistent across both Phase 3 trials, as bolstering CMPS' case as it pertains to what could become the first FDA approval for a classical psychedelic molecule.

1

12

7,174

Probably more de-risked in terms of approval but am currently questioning its’ efficacy against TMS and Spravato in TRD. The MADRS deltas look good but total reduction from baseline MADRS in the active treatment arms isn’t as good as I had hoped. Dissapointed to not really see much of a dose-response in COMP006. Still need to spend much more time looking through the data tonight!

3

127

Feb 17

COMP006, had a smart design. Roughly 1/2 patients in the trial took two 25 mg doses of the drug three weeks apart. A quarter of the trial’s subjects received two doses of 10 mg, another quarter two doses of 1 mg. Compass Pathways meets primary for MDD. endpoints.news/compass-pathw…

1

4

429

🚨Stock Update:

Compass Pathways $CMPS shares surged 35.35% to $8.80, hitting a 52-week high, the company announced highly significant Phase 3 results for COMP360, its psilocybin-based therapy for treatment-resistant depression (TRD).

In the COMP006 trial, the therapy met its primary endpoint, showing a statistically significant reduction in depression symptoms. Specifically, two 25mg doses of COMP360 produced a mean MADRS score difference of -3.8 points compared to the 1mg dose (p<0.001), confirming strong efficacy.

Moreover, 39% of participants receiving 25mg achieved clinically meaningful improvement by Week 6. The treatment acted rapidly, with effects evident the day after administration, and notably, benefits were sustained throughout the six-week evaluation period.

Overall, COMP360 was generally well tolerated across trials, with most side effects—including headache, nausea, and visual hallucinations—occurring on dosing days and resolving within 24 hours. Consequently, Compass Pathways plans to submit an NDA in Q4 following FDA discussions.

Source: abbo.news/4aDzmXd

1

1

141