Healthcare Triangle raises $3.6m as HCTI investors weigh debt, dilution and growth business-news-today.com/heal… $HCTI #HealthcareTriangle #HealthTech #DigitalHealth #CloudComputing #HealthcareIT #NASDAQ #ConvertibleNotes #MicroCapStocks #HCTI

21

Jun 4

$KEEL ✨

KEEL Infrastructure has announced a proposed $350 million offering of Convertible Senior Notes.

Key facts:

• Offering size: $350M

• Institutional investors

• Convertible debt structure

• Proceeds intended for general corporate and strategic purposes

Convertible notes are initially treated as debt, but may be converted into common stock under certain conditions in the future.

Key investor considerations:

⚠️ Potential shareholder dilution

⚠️ Future conversion-related share issuance

On the positive side:

✔ Increased liquidity

✔ Funding for development projects

✔ Greater financial flexibility

This is a financing announcement, not a customer contract announcement. Investors will likely focus on how the proceeds are ultimately deployed across KEEL’s infrastructure strategy.

investor.bitfarms.com/news-r…

$KEEL #ConvertibleNotes #AIInfrastructure #DataCe

4

934

May 18

$HIMS Hims & Hers Announces $300M Convertible Senior Notes Offering

**Key Points:**

- Hims & Hers is offering $300M in convertible senior notes due 2032

- Additional $45M option for buyers (total potential $345M)

- Proceeds earmarked for:

- International expansion

- Planned Eucalyptus acquisition

- Technology and fulfillment infrastructure

- AI investments

This capital raise supports Hims’ aggressive growth strategy in telehealth and international markets.

#HIMS #HimsAndHers #ConvertibleNotes #CapitalRaise

2

523

May 18

🚨 MICROSTRATEGY GÂY SỐC: LÊN KẾ HOẠCH MUA LẠI 1,5 TỶ USD TRÁI PHIẾU, CÓ THỂ BÁN BITCOIN ĐỂ GÂY QUỸ! 📉💰

"Cá voi" lớn nhất thị trường doanh nghiệp – MicroStrategy của Michael Saylor – vừa kích hoạt một bước đi tái cấu trúc vốn cực kỳ táo bạo nhưng cũng đầy tranh cãi, khiến giá cổ phiếu MSTR ngay lập tức bốc hơi hơn 5% trong phiên giao dịch.

Dưới đây là chi tiết chiến lược đứng sau những con số:

🔄 Mua nợ giá rẻ (Discount): MicroStrategy thông báo sẽ mua lại 1,5 tỷ USD nợ gốc của loại Trái phiếu chuyển đổi lãi suất 0% đáo hạn năm 2029. Đáng chú ý, công ty chỉ cần chi khoảng 1,38 tỷ USD tiền mặt để xóa bỏ khoản nợ này nhờ các thỏa thuận mua lại riêng lẻ chiết khấu sâu. Vụ dàn xếp dự kiến hoàn tất vào ngày 19/5.

⚠️ Nguồn vốn từ đâu? Để có 1,38 tỷ USD tiền mặt, MicroStrategy tuyên bố sẽ dùng dự trữ tiền mặt hiện tại, số tiền thu được từ chương trình phát hành thêm cổ phiếu (ATM) và đặc biệt: Có thể bán một phần danh mục Bitcoin của mình!

⚡ Tâm lý thị trường: Việc một công ty vốn nổi tiếng với chiến lược "chỉ mua và hodl, không bao giờ bán" như MicroStrategy ẩn ý về khả năng bán BTC để trả nợ đã ngay lập tức tạo ra áp lực tâm lý, khiến Bitcoin quay đầu giảm nhẹ hơn 2% trong ngày.

📈 Nhưng nhìn rộng hơn: Đây là một bước cờ đi thông minh?

Việc tận dụng thanh khoản kỷ lục từ dòng cổ phiếu ưu đãi STRC (vừa đạt khối lượng giao dịch cao nhất lịch sử 1,53 tỷ USD vào thứ Năm) giúp MicroStrategy giảm bớt gánh nặng nợ phình to.

Mục tiêu dài hạn của Michael Saylor vẫn là chuyển đổi khoảng 6 tỷ USD nợ chuyển đổi thành vốn chủ sở hữu (equity) trong vòng 3-6 năm tới. Ngay trước tin này, họ vẫn âm thầm gom thêm 535 BTC (khoảng 43 triệu USD), nâng tổng tài sản lên 818.869 BTC!

💡 Góc nhìn: Liệu đây là một động thái quản trị rủi ro tài chính xuất sắc (mua lại nợ với giá rẻ) hay là tín hiệu cho thấy MicroStrategy đang bắt đầu cảm thấy áp lực từ đòn bẩy nợ quá lớn khi gom Bitcoin?

Anh em nghĩ Michael Saylor có thực sự xuống tay bán bớt Bitcoin không, hay đây chỉ là "bài binh bố trận" trên sổ sách? 👇💬

Nguồn: theblock

#MicroStrategy #MSTR #MichaelSaylor #Bitcoin #BTC #CryptoNews #ConvertibleNotes #Finance #WallStreet

15

4,579

📊 IREN has officially closed its massive $3.0bn convertible notes offering, securing approximately $2.96bn in net proceeds to fuel its aggressive growth in Bitcoin mining and AI data center infrastructure. #IREN #BitcoinMining #AIInfrastructure #ConvertibleNotes 🚀

Read more: 🔗 poweranalysis.io/iren

IREN has closed its $3.0bn convertible notes offering

Key details of the transaction:

- 1.00% coupon convertible senior notes due 2033

- $2.6bn offering plus fully exercised $400m greenshoe

- $2.96bn net proceeds, after deducting the initial purchasers’ discounts and commissions and IREN’s estimated offering expenses

- Capped call transactions expected to provide a hedge upon conversions up to an initial cap price of $110.30 per share

- No put option for investors in the notes other than a customary put right in the case of certain fundamental changes

Read more: iren.gcs-web.com/static-file…

1

446

很多人对 $IREN 很失望,但我想说的是根据推断好日子快要来了

大家失望的心情我能理解,隔壁的 $NBIS 都涨冒烟了,很多人说nbis已经是推理之王(确实是)。他的这个团队是为ai云服务而生的。不是其他那些,就是裸金属gpu出租生意。准备从iren和crwv换到iren。我想说的是iren走的是underdog逆袭的故事。目前 $IREN 只是小涨,但要给他点耐心,技术分析来说非常乐观,其他一切看空的观点都是noise。我今天就专门写一篇iren的分析来稳住大家心态。

去年10月IREN发了$10亿可转债。 一个月后宣布了$97亿的微软合同。这次他们刚刚关闭了$30亿、1%利率的可转债——规模是去年的3倍,利率几乎是白送,greenshoe全额行使,$110以下几乎不稀释,那么1个月后是不是也有大合同要宣布呢?换句话说他们看好未来公司几乎是必到110以上,这就跟我的技术分析呼应了,我的图年底会到150。历史会重演吗?

现在的数字是这样的:

$30亿新可转债 $10亿ATM增发 $15亿手头现金 = 可用资金接近$55亿。

正常公司不会提前囤这么多钱。资本是有成本的。除非他们已经知道这笔钱要花在哪里了。

可能性1: 超级hyperscaler合同在几周或者几个月内会宣布。

可能性2: IREN有更大的AI云平台战略。最近收购Mirantis,拿到Nvidia合作,Sweetwater通电,强化software stack。

市场现在把IREN当比特币矿企定价。

但它已经是:Nvidia战略合作伙伴、微软$97亿合同执行方、可再生能源AI云平台。上次Nvidia合作消息带来的那根大阳线,可能只是前菜。 $30亿不是融资,是在为某个还没公布的东西做准备。

技术分析:

周线(图1):盘整了6 7个月的上涨中继放巨量突破,确认是真突破,ai浪潮第一浪gpu cpu 存储刚走了一大半,第二浪轮动到数据中心,电力和储能,你猜猜是会涨还是跌?资金轮动过去的时候要有耐心才能吃到肉。

日线(图2):短期走了个higher low higher high的结构,如果大盘回调,49 50这个位置是有概率再来一次,那么这个位置是仓位加满的位置。如果真回调了下,不要恐慌,只是上涨过程中的小回调,不是反转。

时间线:

$IREN 这个融资节奏我觉得越来越像“重大合同前的提前备战”:

• 2025年6月:融资 5亿美元

• 2025年10月:融资 10亿美元(原计划8.75亿,后来超额扩大)

• 2025年11月:融资 20亿美元 → 随后不久宣布微软97亿美元AI合同

• 2026年5月:再次融资 30亿美元,利率低到只有1%,而且稀释限制在110美元以上

• 2026年6月:???(宣布大合同吗)

总结:

不得不佩服iren管理层,这融资结构设计真厉害。可转债 capped call 对冲结构主要是为了低成本拿钱和尽量减少短期稀释。为什么这种手法很高明?因为他同时融资拿到30亿现金,延后稀释不用像atm那样砸盘,然后又给市场信号convertible note转换价在 $73,保护做到 $110。这基本上是管理层告诉股东他们认为未来股价可能远高于现在。1%利率借的基本上是白借钱。Best finance team in the sector!

#IREN #AIInfrastructure #Nvidia #Microsoft #ConvertibleNotes #美股 #AI基建 #数据中心 #USStocks

16

20

107

28,429

May 14

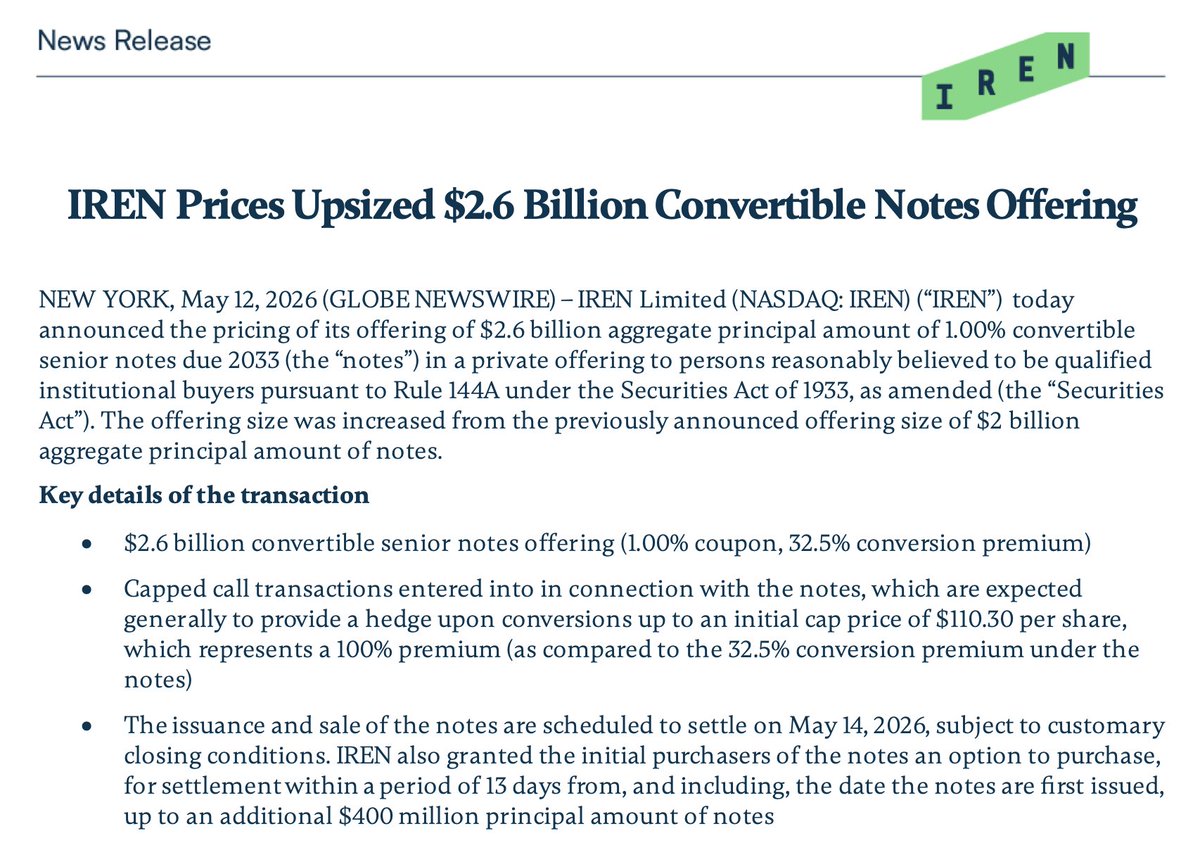

BREAKING: $IREN IREN Closes $3.0 Billion Convertible Notes OfferingIREN has successfully closed its $3.0 billion convertible notes offering.This significant capital raise provides the company with substantial funding for its ongoing expansion, particularly in AI data centers and Bitcoin mining infrastructure.#IREN #IREN #ConvertibleNotes #CapitalRaise #BREAKING

2

165

May 12

🚨 @IREN_Ltd upsizes convertible notes offering to $2.6 BILLION — demand was overwhelming 🚨

⚡ Originally announced at $2.0B — upsized to $2.6B on strong institutional demand — with option to purchase an additional $400M (total potential $3.0B)

⚡ 1.00% coupon — remarkably low cost of capital for a company of IREN's scale and growth profile

⚡ 32.5% conversion premium — initial conversion price of $73.07/share vs $55.15 last close

⚡ Capped call transactions entered into at $110.30/share cap — representing a 100% premium to current share price — significant dilution protection for existing shareholders

⚡ Net proceeds: ~$2.57B (up to $2.96B if overallotment exercised) — after deducting $174.5M for capped call transactions

⚡ Settles May 14, 2026 — proceeds deployed toward general corporate purposes and working capital across the 5 GW global pipeline

$2.6B raised at 1% coupon. $600M upsized from initial announcement. Capped call protection at $110/share.

Institutional investors are not just buying the story — they are funding the buildout at scale

$2.6B $3.4B NVIDIA contract $9.7B Microsoft contract 5 GW pipeline Mirantis Nostrum...

Is $IREN the most aggressively funded AI infrastructure company in the public markets? 👇

$IREN $NVDA #AIInfrastructure #ConvertibleNotes #DataCenter #AICloud

3

13

153

17,851

May 11

🚨 @IREN_Ltd announces $2 BILLION convertible notes offering 🚨

⚡ $2B aggregate principal of convertible senior notes due 2033 — with option for initial purchasers to purchase an additional $300M (total potential $2.3B)

⚡ Notes offered to qualified institutional buyers only — Rule 144A private offering — senior unsecured obligations maturing December 1, 2033

⚡ Capped call transactions to be entered into concurrently — designed to reduce potential dilution to ordinary shareholders upon conversion

⚡ Proceeds used for general corporate purposes and working capital — funding the continued buildout of the 5 GW global pipeline alongside the @nvidia partnership

⚡ This follows last week's announcements: — $3.4B @nvidia AI Cloud contract— 5 GW strategic partnership with $NVDA — $2.1B NVIDIA investment option— @MirantisIT acquisition— Nostrum acquisition (490 MW Spain GW pipeline)

The capital markets are telling you everything you need to know about what $IREN is building

$2B convertible note. $3.4B NVIDIA contract. $9.7B Microsoft contract. 5 GW global pipeline.

Is $IREN the most aggressively capitalized AI infrastructure company in the public markets right now? 👇

$IREN $NVDA #AIInfrastructure #ConvertibleNotes #DataCenter

3

1

52

3,044

May 11

🚨 $IREN ACABA DE ANUNCIAR EMISIÓN DE BONOS CONVERTIBLES

IREN Limited (NASDAQ: $IREN) ha lanzado hoy la oferta propuesta de 2 Bn$ en bonos convertibles senior con vencimiento el 1 de diciembre de 2033 (más opción de hasta 300 Mn$ adicionales).

¿Qué significa esto?

• Bonos senior no garantizados, colocación privada a inversores institucionales cualificados (Rule 144A).

• Interés semi-anual (tasa a determinar en el pricing).

• Los proceeds se destinarán principalmente a:

• Capped call transactions → para reducir significativamente la dilución en caso de conversión.

• Working capital y expansión de su infraestructura AI Cloud (data centers y clústeres GPU).

Se trata de una jugada estratégica para financiar el fuerte crecimiento de IREN en IA Bitcoin mining sin diluir tanto a los accionistas de inmediato. Fuerte señal de que el mercado institucional sigue apostando por su modelo de data centers de alto rendimiento.

¿Buena noticia para el largo plazo o te preocupa la deuda convertible? 🔥

Yo sinceramente, veo la noticia como algo esperado pero ya empieza a desesperar. Se esperaba un gran acuerdo, y lo de $NVDA la semana pasada no es lo que quería el mercado ( ni yo ). La llevo hace bastantes meses, pero cada dia me está convenciendo menos.

¿Qué opinas de $IREN? Comenta abajo 👇

#IREN #ConvertibleNotes #AI #BitcoinMining #DataCenters

2

2

27

5,937

$CRWV ripping 4% on a $3B convertible note raise — and the market loves it.

CoreWeave's offering convertible senior notes due 2031, with underwriters holding a 13-day option to tack on another $450M. Total potential raise: $3.45B. They're funding capped calls to limit dilution — smart structure that's being rewarded in real time.

AI infrastructure buildout needs capital, and $CRWV is making it clear they're not slowing down. Watch for momentum continuation if broader AI names stay bid.

#CRWV #AIStocks #ConvertibleNotes

1

5

295

Mar 18

$NBIS just raised the bar — $4B convertible note offering, upsized from $3.75B. Demand was clearly there.

This comes on the heels of Meta's $27B AI deal and Nvidia's $2B investment. Smart money is stacking into this name fast. Convertible notes = dilution risk, but also signals massive capex ambitions.

Stock barely moved premarket — market digesting or coiling? Watch for a breakout above recent highs as a catalyst trigger. 👀

#NBIS #AIStocks #ConvertibleNotes

5

107

Mar 17

Context on the $3.75B $NBIS Convertible Offering:

As I mentioned about a month ago, this financing move by Nebius was expected and is no reason for panic. The company has supported its rapid growth so far using equity financing with zero debt, but to maintain this pace, the company has to look at external funding sources.During the Q4-2025 earnings call, the COO stated that 60% of the projected 2026 CapEx ($16B–$20B) is covered by operating cash flows and existing cash reserves. For the remaining 40%, management is evaluating several financing options.

This move is essential to maintaining the company’s current rapid growth trajectory. As I noted in the same post, Nebius currently serves its clients through a mix of proprietary data centers and colocation sites. By phasing out colocation, Nebius expects to lower its TCO by 20%, a move that will boost long-term revenue. Funding will help complete these proprietary facilities and capture those higher margins.

"Know why you own what you own and ignore the noise"

#NBIS #Nebius #AIInfrastructure #ConvertibleNotes #AIGrowth #DataCenters #AIStocks #Investing #StockMarket #DipBuy #GrowthStock

Feb 23

While the market fixates on a revenue “miss,” this dive into $NBIS latest earnings and strategic moves reveals a far more bullish story unfolding beneath the surface!

Before diving into the company’s financials, it is essential to evaluate the broader industry. Demand for AI infrastructure has exceeded all forecasts, while GPU shortages and power requirements are spiking. Research indicates that the combined CapEx of hyperscale companies is projected to reach approximately $700B in 2026, representing a 74% increase from 2025, whereas demand for AI data center power is projected to quadruple over the next decade, according to Bloomberg. This supply-demand imbalance makes companies like Nebius incredibly relevant, particularly as the market grows wary of heavy CapEx, as they offer the most efficient and affordable method for firms to delegate their computational needs.

Nebius addresses these market shortages through its strategic partnership with Nvidia, which grants early access to next-generation chips like the “Rubin Chips”, providing a GPU Advantage. Furthermore, the company is rapidly securing power agreements to support its growth, more than doubling its contracted power from 1GW to 2.5GW in less than a year.

1)Revenue Analysis

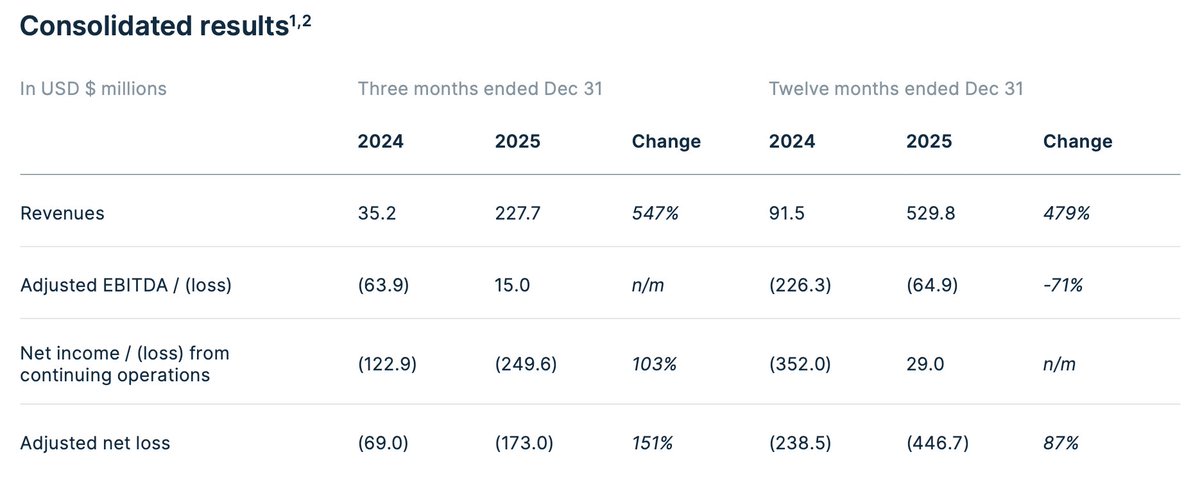

Many investors are concerned about Nebius' Q4 revenue as it fell short of analyst expectations, coming in at $227.7M versus the projected $243M (-8%). Despite the miss, revenue reflects explosive 547% year-over-year growth and a 56% increase compared to the previous quarter. With AI Cloud revenue exploding by 800% YoY, it’s clear that Nebius isn’t facing a demand problem. Τhey are simply scaling as fast as their capacity allows.

At this point, it is crucial to understand the company’s revenue recognition policy. Under IFRS and the accrual principle, Nebius enters into agreements for AI Cloud services but cannot recognize revenue until the corresponding computing power is delivered to the customer. This means revenue is only recognized as capacity comes online and power is consumed at the facilities. Nebius has already secured the components needed for its Microsoft and Meta partnerships, insulated itself from price volatility.

Guidance:

Nebius forecasts 2026 revenue of $3B–$3.4B, falling slightly below Bloomberg's $4B consensus. As previously noted, Nebius is scaling as fast as its capacity allows. According to management, the expansion will truly impact the bottom line in the second half of 2026. Smaller colocation sites will come online in Q2 and Q3, but the larger-scale projects, which offer better long-term margins, are set to deliver in late 2026 and 2027. This suggests a quieter H1, but in no way compromises the company's long-term growth story.

2)Annualized Recurring Revenue (ARR)

For companies with a profile like Nebius, analyzing ARR provides far more reliable insights. In Q4, the company smashed analyst expectations by reporting an ARR of $1.25B, significantly outperforming the projected $900M–$1B range. This reveals the true growth of the business, which standard reported revenue tends to hide.

3)Cash Flow

Nebius closed 2025 with $3.7B in cash and cash equivalents, $1.57B in deferred revenue, $834M in operating cash flow generated in Q4 alone, and zero debt. This liquidity allows for a disciplined execution of its $16B–$20B CapEx plan for 2026.

4)CapEx

In its 2026 guidance, $NBIS projects CapEx of $16B–$20B, which serves as the company's primary investment pillar. During the earnings call, COO Ophir Nave noted that less than 1% of this CapEx is allocated to securing energy, about 20% to data center construction, and approximately 80% to GPU acquisition (this high GPU concentration is considered low-risk, as it is strictly demand-driven).

Alongside its Q4 results, Nebius unveiled nine new data center locations, a combination of owned campuses and colocation partnerships, which exemplify the company’s rapid expansion. The firm utilizes leased data centers to provide clients with immediate infrastructure as per existing agreements, while simultaneously developing its proprietary facilities to transition them over in the long term. Management also highlighted a pipeline of ongoing projects that are expected to be unveiled during 2026.

5)Adjusted EBITDA Analysis

The company achieved positive adjusted EBITDA for the first time, reaching $15M—a 123.5% YoY increase, despite a full-year loss of $64.9M in 2025. For 2026, management targets a 40% margin, as the AI Cloud business continues to operate with high profitability margins.

EBIT is projected to remain negative in 2026 due to significant R&D investments.

A key announcement is the extension of the depreciation period from 4 to 5 years. This change reduces annual depreciation expense, resulting in a positive impact on EBIT and Net Income. This adjustment was made to ensure alignment with industry peers and is treated as a change in accounting estimate under IFRS guidelines.

6)Funding the Growth

Nebius has supported its rapid growth so far using equity financing with zero debt. To maintain this pace, the company is now looking to external funding sources. The COO stated that 60% of the projected CapEx ($16B–$20B) is covered by operating cash flows and existing cash reserves. For the remaining 40%, management is evaluating several financing options, including debt financing—potentially collateralized by major contracts with $MSFT & $META —equity issuance, or the liquidation of holdings in subsidiaries such as ClickHouse and Avride.

We can expect to see these figures materialize throughout the fiscal 2026 reporting cycle.

**Not Financial Advice**

1

3

6

316

Feb 27

6 of 11

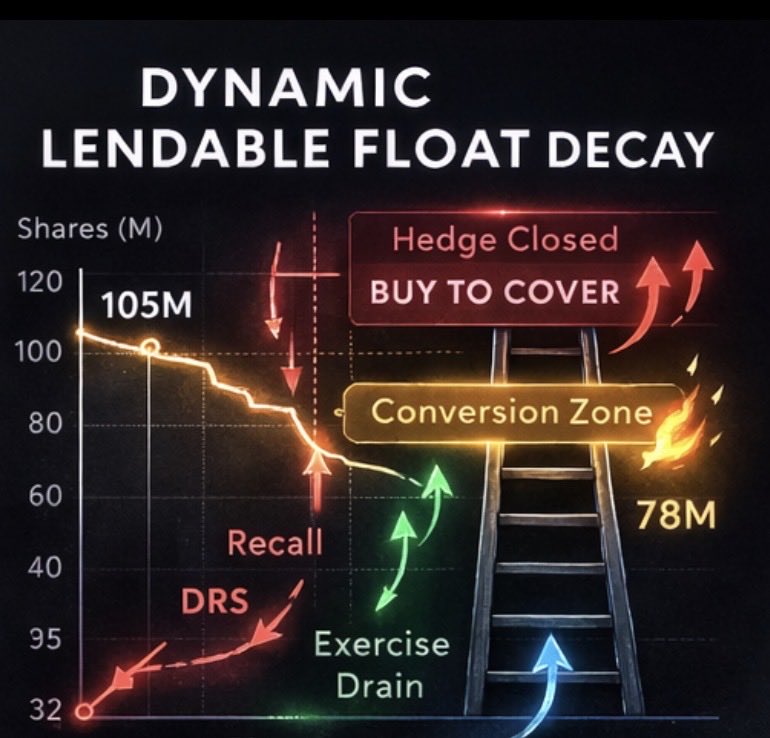

Layer 3: Ryan Cohen Margin Repayment Large-Block Share Recall

Verified Context:

• Cohen stake: ~41.6M beneficial shares (~9.2–9.3% of outstanding)

• Historical pledge: 22.34M shares pledged in April 2025

• Current borrow market: ~0.35–0.45% fee, ~2.6–3.0M visible availability

Model Parameters (Illustrative):

• Recallable portion: 10 / 20 / 30 million shares

• Aggregate lendable pool: ~105M

• Currently borrowed: ~68M (utilization ~65%)

Base-Case Results (70% of recalled shares were lendable):

• 10M recall → new utilization 69.4%

• 20M recall → new utilization 74.7%

• 30M recall → new utilization 81.0%

Interpretation: A 20–30M recall pushes utilization into the convex fee region (75–87% ), triggering borrow-fee spikes and potential forced buy-ins — without changing reported short interest.

This occurs without any increase in reported short interest — the same borrowed shares now chase a smaller pool of lendable shares.

What Actually Happens in the Real-World Securities-Lending Plumbing:

1. Prime broker/custodian notification: The shares are withdrawn from the lending program.

2. Locate & replacement obligation: The prime broker must immediately locate replacement borrows.

3. Fee auction & re-pricing: If replacement supply is tight, the broker auctions the borrow at higher rates.

4. Forced buy-in cascade: If no replacement is found, buy-in notices are issued to the shortest/weakest counterparties first.

5. Re-routing from weaker hands: Brokers pull borrows from less-protected accounts to protect larger clients.

This is why borrow-fee spikes frequently occur without a corresponding rise in reported short interest — the numerator stays flat while the denominator shrinks.

Convexity & Timing Sensitivity (This Layer Only):

• Below ~70–75% utilization: fees remain low (~0.3–1%).

• Above ~80%: fees enter the “special” regime (5% , sometimes 20–100% annualized on portions).

A single 20–30 million recall from a name like Cohen can push the entire market lendable pool into that convex zone within days.

Standalone Market Implications:

• No new shares created: Pure supply contraction in the borrow market.

• Disproportionate impact: One concentrated block (2.4–7.3% of float) can tighten the entire ~105 million lendable pool.

• Observable signals: Sudden drop in visible availability, borrow-fee step-up, increased FTDs.

• Reversibility: Cohen could re-pledge later, but a prolonged recall removes supply permanently.

#ConvertibleNotes #BondholderFlow #WarrantExercise #EquityIssuance #FloatLock #DemandShock #DilutionMath #CapitalStructure

1

2

71

Feb 27

2 of 11

Additional structural participants include:

Point72 Asset Management, holding the largest institutional warrant block (445,196 units per recent 13F) alongside direct shares, implying convertible note participation that could enable a financed flip — unwinding hedges, retaining converted shares, and exercising warrants to lock approximately 8.77 million shares (~2.14% of float). At prices above $33, carry dynamics turn favorable, creating positive feedback.

Ryan Cohen’s potential margin repayment and recall of 10–30 million pledged shares, contracting the lendable pool without altering reported short interest and pushing utilization into the convex zone where borrow fees inflect sharply and forced buy-ins cascade from weaker counterparties.

Scaled participation from other convertible bondholders (totaling some 14 million warrants and ~140 million as-converted equivalents), which amplifies demand shocks post-$32 breach.

Gamma dynamics on the clean GME chain: surges in call volume, implied volatility expansion to 200–600% or higher on short-dated options, and positive dealer hedging that multiplies upward velocity by 1.5–3× once momentum ignites.

The result is a nonlinear, reflexive structure — convex, with downside buffered near current levels by cash reserves and no forced selling pressures, yet asymmetric upside contingent on breaching the $32 catalyst.

Each component interlocks mechanically, concentrating behavior around the hard warrant expiration deadline and amplifying self-reinforcing cascades through scarcity, delivery friction, and hedging flows.

#OptionsFlow #ConvertibleNotes #GammaExposure

1

1

4

1,644

Feb 19

Bitdeer Plans New $300M Convertible Bonds Aimed at Deleveraging $BTDR #ConvertibleNotes #PrivatePlacement theenergymag.com/news/market…

4

1,735

CEO STRATEGY: "BITCOIN MUSIAŁBY SPAŚĆ DO $8,000 I TAM ZOSTAĆ DO 2032, ZANIM BĘDZIEMY MIELI PROBLEM"💪

CEO Strategy (dawniej MicroStrategy) Phong Le właśnie powiedział coś, co powinno uspokoić wszystkich niedźwiedzi (chociaż wątpie) :

"Bitcoin musiałby spaść do $8,000 za sztukę i siedzieć tam przez pięć lat aż do 2032, zanim naprawdę będziemy mieli problem"

Q4 2025 earnings wywołał panikę

Strategy zgłosiło:

- 17,4 miliarda dolarów straty operacyjnej (głównie niezrealizowane straty na posiadanych BTC)

- 12,6 miliarda straty netto dla akcjonariuszy zwykłych.

Market zareagował paniką:

"MicroStrategy bankrutuje! Muszą sprzedać Bitcoin!"

"Na pewno tajemniczy ONI chcą zlikwidować Saylora!"

Phong Le odpowiada: "Spokojnie. Oto matematyka."

Najgorszy scenariusz:: $8k BTC przez 5 lat

Le wyjaśnił "scenariusz skrajnie niekorzystny":

"W najbardziej ekstremalnym scenariuszu, gdyby Bitcoin doświadczył 90% spadku i ustabilizował się na $8,000, to byłby punkt, w którym nasze rezerwy Bitcoin zrównają się z naszym net debt. W tym momencie nie moglibyśmy wykorzystać naszych rezerw Bitcoin do rozliczenia "convertibles", co zmusiłoby nas do rozważenia restrukturyzacji, emisji nowego equity lub zaciągnięcia dodatkowego długu."

Dlaczego Strategy jest bezpieczny?

1. Długoterminowy dług – żadnej presji refinansowania

Strategy ma $8.2 miliarda zadłużenie zamiennego, który zapada między 2028-2032.

To oznacza: Firma ma lata, żeby obserwować jak Bitcoin się zachowuje, zanim będzie musiała spłacić cokolwiek.

2. Średni koszt nabycia: ~$74,000

Strategy kupowało Bitcoin po średniej cenie około $74k.

Bitcoin obecnie: ~$69k

3. Nawet 25 tys. dolarów za BTC = do zniesienia, nie katastrofalne

Le powiedział, że nawet jeśli Bitcoin spadnie do $25,000 (czyli -67% z ATH), sytuacja byłaby "difficult but manageable rather than catastrophic".

Dopiero $8k przez 5 lat = realny problem.

Czy Strategy będzie sprzedawać Bitcoin?

Le przyznał w listopadzie 2025: Tak, sprzedaż Bitcoin jest "na stole", ale tylko jako ostatnia deska ratunku.

Dwa warunki muszą być spełnione jednocześnie:

1. Cena akcji < 1x mNAV (kapitalizacja rynkowa poniżej wartości aktywów BTC)

2. Brak dostępu do nowego kapitału (zamknięte rynki akcji i obligacji)

Obecnie:

- MSTR stock premium do NAV = nadal pozytywny

- Capital markets = otwarte (Strategy non-stop emituje equity i convertibles)

Więc.

NIE, Strategy nie sprzedaje Bitcoin teraz.

Le: „Mamy większą elastyczność niż kiedykolwiek wcześniej”

W podcaście „What Bitcoin Did” Le powiedział:

„Nasza struktura kapitałowa jest bardzo silna. Pierwszy termin spłaty zadłużenia przypada dopiero w grudniu 2027 r. Mamy większą elastyczność niż kiedykolwiek wcześniej, aby kontynuować gromadzenie bitcoinów”.

Strategy może:

- Emitować equity przez programy rynkowe

- Emitować "zero-coupon" lub "low-coupon convertibles"

- Wybierać timing obu, w zależności od warunków rynkowych

A tymczasem Strategy nadal kupuje

Mimo Q4 loss $17.4B, Strategy:

-Nie sprzedał ani jednego satoshi

-Nadal planuje emisje equity i debt

Ale spece na X już podają dalej FUD, że tajemniczy "ONI" chcą likwidacji Saylora.

Są spadki i oczywiście już lecimy na 0$.

Wierzycie mu ?

A może tak gadają tylko, bo ... co innego mają mówić ?

#Strategy #MSTR #Bitcoin #PhongLe #ConvertibleNotes #BullishBearCase

3

2

25

4,195

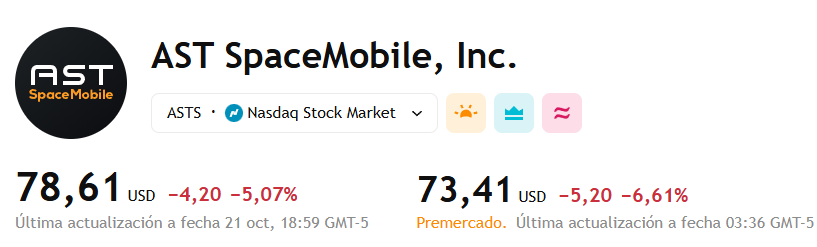

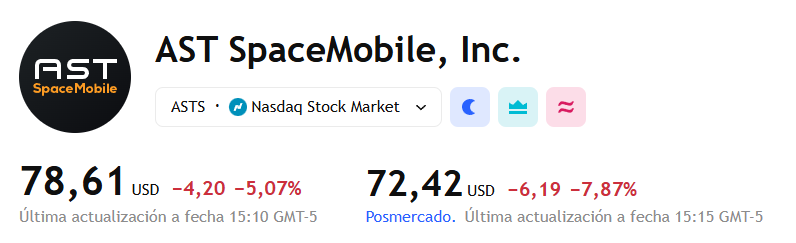

22 Oct 2025

🛰️ AST SpaceMobile Inc $ASTS priced a $1.0B private offering of convertible senior notes due 2036, upsized from $850M, targeting qualified institutional buyers under Rule 144A.

The notes carry an initial conversion price of ~$96.30/share, a 22.5% premium to ASTS’s Oct. 21 close, and include an option for an additional $150M in notes.

Net proceeds of ~$981.9M (up to $1.13B if fully exercised) will fund the deployment of its satellite constellation and expansion into new strategic markets 🌐🚀 #ASTSpaceMobile #Satellites #ConvertibleNotes

21 Oct 2025

🚀 AST SpaceMobile $ASTS Announces $850 Million Private Offering of Convertible Senior Notes Due 2036

📅 October 21, 2025 – Midland, TX

🔍 AST SpaceMobile (NASDAQ: ASTS), the company developing the world’s first space-based cellular broadband network accessible directly by standard smartphones, announced plans to offer $850 million in convertible senior notes due 2036 in a private placement to qualified institutional buyers under Rule 144A of the U.S. Securities Act.

The company may also grant initial purchasers an option to buy up to an additional $150 million in notes within 13 days of issuance.

💵 Key Terms (to be finalized upon pricing)

Principal amount: $850 million (plus potential $150 million upsizing)

Maturity: January 15, 2036

Type: Senior, unsecured, convertible notes

Interest: Payable semiannually (rate TBD)

Conversion: Into cash, Class A shares, or a mix—at ASTS’s discretion

📈 Use of Proceeds

Funds will support general corporate purposes, primarily the deployment of AST SpaceMobile’s global satellite constellation and expansion into new strategic markets for its SpaceMobile Service.

⚖️ Structure and Compliance

Notes are unregistered under the Securities Act and may only be sold to qualified institutional buyers.

Conversion shares (if any) are also restricted securities until registered or exempted.

🛰️ Concurrent Transactions

1️⃣ Registered Direct Stock Offering

AST SpaceMobile also plans to issue new Class A common shares through a registered direct offering, separate from the convertible notes transaction.

Proceeds: Along with cash on hand, will fund the repurchase of up to $50 million of its existing 4.25% convertible senior notes due 2032.

2️⃣ Existing Convertible Notes Repurchase

ASTS expects to negotiate privately with select holders to buy back up to $50 million of its 2032 notes for cash.

The repurchase terms will depend on market prices of both the notes and ASTS shares.

Following this deal, ASTS may continue repurchasing additional existing notes.

📊 Market Impact

Holders participating in the repurchase may buy or sell ASTS shares or adjust derivative hedges, potentially causing significant volatility in ASTS stock and note prices due to the transaction’s scale relative to daily trading volumes.

⚠️ Key Clarifications

The convertible notes offering and registered direct offering are not contingent upon each other.

This announcement does not constitute an offer or solicitation to sell or buy securities in any jurisdiction.

💡 Summary Insight

This dual financing move strengthens AST SpaceMobile’s balance sheet ahead of large-scale satellite deployment, while optimizing its debt maturity profile by repurchasing earlier 2032 convertible notes. The strategy reflects management’s confidence in upcoming commercial launches and the scalability of its direct-to-smartphone satellite network for both commercial and government clients.

9

3,359

22 Oct 2025

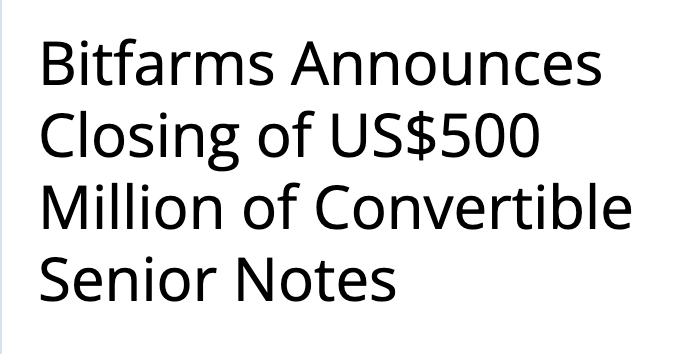

💰 @Bitfarms_io closes US$500M convertible notes (incl. full greenshoe)

🔹 1.375% coupon, due 2031

🔹 Conversion price ≈ $6.86/share (30% premium)

🔹 125% capped call to limit dilution

🔹 Strengthens liquidity > US$1 B for HPC/AI growth

$BITF #Bitcoin #AI #DataCenters #ConvertibleNotes

Read more: powermininganalysis.com/bitf

1

1

6

716