Jun 3

𝗛𝗶𝗸𝗮𝗹 𝗟𝘁𝗱. 𝗤4 & 𝗙𝗬26 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗼𝗻𝗳𝗲𝗿𝗲𝗻𝗰𝗲 𝗖𝗮𝗹𝗹 𝗦𝘂𝗺𝗺𝗮𝗿𝘆 📈:

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀:

- 𝗤4 𝗙𝗬26: Revenue ₹519 Cr, EBITDA Margin 20.3%

- 𝗙𝗬26: Revenue ₹1,713 Cr, EBITDA Margin 12.9%

- 𝗘𝘅𝗰𝗲𝗽𝘁𝗶𝗼𝗻𝗮𝗹 𝗜𝘁𝗲𝗺𝘀: ₹47 Cr impairment for a part of the Panoli manufacturing plant & ₹85 Cr for labour code & impairment charges for FY26.

- 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗣𝗕𝗧 (𝗙𝗬26): ₹7 Cr (after exceptional items).

- 𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗘𝘅𝗽𝗲𝗻𝗱𝗶𝘁𝘂𝗿𝗲 (𝗙𝗬26): ₹149 Cr for debottlenecking, regulatory upgrades, & CDMO capacity expansion.

- 𝗗𝗲𝗯𝘁-𝘁𝗼-𝗘𝗾𝘂𝗶𝘁𝘆 𝗥𝗮𝘁𝗶𝗼: Reduced from 0.59 to 0.56.

𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 & 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆:

𝗢𝘃𝗲𝗿𝗮𝗹𝗹: Hikal is transitioning from remediation to sustainable, technology-led growth, focusing on strengthening quality systems, compliance, & operational discipline. Improved customer engagement & medium-term growth visibility are key focus areas. FY27 is expected to be stronger than FY26.

𝗣𝗵𝗮𝗿𝗺𝗮𝗰𝗲𝘂𝘁𝗶𝗰𝗮𝗹𝘀 💊:

- 𝗙𝗬26 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹1,021 Cr, EBIT Margin 5.7%

- 𝗤4 𝗙𝗬26 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹292 Cr, EBIT Margin 12% (sequential profit up 45%)

- Demand trends improved in H2 FY26 for APIs & CDMO segments.

- Capacity utilization at Panoli & Bangalore plants: 80-85%.

- 𝗙𝗼𝗰𝘂𝘀: Complex & niche therapeutic segments (oncology, CNS, gastroenterology, antidiabetics).

- 𝗗𝗠𝗙 𝗙𝗶𝗹𝗶𝗻𝗴𝘀: Targeting 5-6 annually (up from 2-3).

- 𝗖𝗗𝗠𝗢 𝗚𝗿𝗼𝘄𝘁𝗵: Driven by China Plus One strategy, with increasing RFPs & progression from development to scale-up.

- 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁𝘀: High-potency lab, expanded R&D in Pune, & new pilot plant in Panoli are operational, enhancing complex chemistry capabilities.

- 𝗙𝘂𝘁𝘂𝗿𝗲 𝗙𝗼𝗰𝘂𝘀: HPAPI manufacturing facility in Pune (targeted FY'28), geographic expansion in Japan, Brazil, & South Korea.

- 𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆: Remediation CAPAs nearing completion for USFDA; upcoming engagement expected to provide clarity.

𝗖𝗿𝗼𝗽 𝗣𝗿𝗼𝘁𝗲𝗰𝘁𝗶𝗼𝗻 🌾:

- 𝗙𝗬26 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹692 Cr, EBIT Margin 8.4%

- 𝗤4 𝗙𝗬26 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹228 Cr, EBIT Margin 17.1%

- Recovery driven by improved customer volumes & industry normalization; worst phase of the cycle is believed to be behind.

- 𝗙𝗼𝗰𝘂𝘀: Transitioning towards higher-value contract manufacturing, co-development R&D, & long-term supply agreements.

- 𝗗𝗶𝘃𝗲𝗿𝘀𝗶𝗳𝗶𝗰𝗮𝘁𝗶𝗼𝗻: Leveraging technology for Specialty Chemicals & Personal Care segments.

𝗔𝗻𝗶𝗺𝗮𝗹 𝗛𝗲𝗮𝗹𝘁𝗵 🐾:

- 𝗠𝗼𝗺𝗲𝗻𝘁𝘂𝗺: Sustained momentum driven by increasing global outsourcing & customer engagement.

- 𝗖𝗗𝗠𝗢 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀: Steady traction as customers outsource; validation completed, progressing to commercial phase.

- 𝗩𝗮𝗹𝘂𝗲 𝗣𝗿𝗼𝗽𝗼𝘀𝗶𝘁𝗶𝗼𝗻: Focusing on supply chain security, regulatory robustness, quality systems, & long-term manufacturing reliability.

- 𝗚𝗿𝗼𝘄𝘁𝗵: Medium-term trajectory expected to scale meaningfully, supported by commercialization of existing programs & new CDMO opportunities.

- 𝗣𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼: Strategically moving towards higher complexity & differentiated customers with lower competitive intensity & higher margin sustainability.

𝗞𝗲𝘆 𝗤&𝗔 𝗣𝗼𝗶𝗻𝘁𝘀:

- 𝗥𝗮𝘄 𝗠𝗮𝘁𝗲𝗿𝗶𝗮𝗹 𝗩𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆: Solvent prices (toluene, methanol, acetone, benzene) have increased significantly but availability is not an issue. Pass-through mechanisms for CDMO products are in place with a lag effect; negotiations are ongoing. Own product price increases are being pursued.

- 𝗖𝗵𝗶𝗻𝗮'𝘀 𝗜𝗺𝗽𝗮𝗰𝘁: No significant price increases observed from China for agrochemicals or raw materials, despite domestic input price hikes in India. Chinese manufacturers appear to be absorbing increases with government support.

- 𝗡𝗖𝗘 𝗣𝗿𝗼𝗱𝘂𝗰𝘁𝘀: Hikal is already commercializing NCE products in its current portfolio & has won new NCE RFPs for launch in FY27.

- 𝗣𝗵𝗮𝗿𝗺𝗮 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝗦𝗵𝗼𝗿𝘁𝗳𝗮𝗹𝗹: USFDA warning letter for the Bangalore site led to a slowdown in shipments & price releases in Q4 FY26, impacting YoY performance. This is expected to recover in subsequent quarters.

- 𝗨𝗦𝗙𝗗𝗔 𝗜𝘀𝘀𝘂𝗲: Remediation efforts are ongoing, with CAPAs nearing completion. A meeting with the FDA is planned in the coming months, with an inspection expected towards the end of the year. It typically takes 18-24 months to resolve such issues.

- 𝗖𝗗𝗠𝗢 𝗚𝗿𝗼𝘄𝘁𝗵 𝗜𝗺𝗽𝗮𝗰𝘁: The USFDA issue primarily impacts CDMO growth, particularly for new NCEs, as volumes are split among suppliers. The Panoli site, being FDA-approved, offers an alternative.

- 𝗙𝘂𝘁𝘂𝗿𝗲 𝗢𝘂𝘁𝗹𝗼𝗼𝗸: Company confident of resolving FDA issues & returning to historical growth levels. Focus on CDMO, Pharma, Animal Health, & Specialty Chemicals for future growth. FY27 is anticipated to show growth, with detailed guidance to be provided after Q1 results.

- 𝗙𝗬30 𝗧𝗮𝗿𝗴𝗲𝘁𝘀: Medium-term targets (₹3,500-4,000 Cr) are still achievable, though delayed by 2-3 years due to recent challenges.

- 𝗔𝗻𝗶𝗺𝗮𝗹 𝗛𝗲𝗮𝗹𝘁𝗵 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀: On track to build a ₹500 Cr business in 4-5 years; FY27 revenue guidance will be provided later.

- 𝗦𝘁𝗲𝗿𝗼𝗶𝗱𝘀/𝗛𝗼𝗿𝗺𝗼𝗻𝗲𝘀: Hikal is not currently involved in steroids or hormones for animal health due to facility requirements; past information may be outdated.

- 𝗢𝗻𝗰𝗼𝗹𝗼𝗴𝘆 & 𝗔𝗗𝗖𝘀: Company is developing capabilities in HPAPIs & ADC payload/linker synthesis, a long-term opportunity (3-5 years).

📊 HIKAL LTD | 🏷️ Earnings Call Transcript

🌐 Details: wegro.app/usOiSV

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

4

5

208

May 29

Hikal Ltd Concall Summary for Q4FY26

MANAGEMENT COMMENTARY

• Operational momentum improving steadily

• Technology-led growth strategy emphasized

• Compliance systems significantly strengthened

• FDA remediation remains top priority

• HPAPI and ADC focus increasing

OUTLOOK

• FY27 expected stronger overall

• Growth visibility improving gradually

• Historical growth levels targeted again

• Animal Health scaling aggressively

• DMF filings set to increase

INDUSTRY

• China 1 trend benefiting India

• Crop cycle showing recovery signs

• Chinese pricing pressure persists

• Raw material inflation intensified

• Logistics disruptions impacting supply

COMPETITIVE POSITION

• Complex chemistry capabilities differentiating

• Integrated CDMO offerings expanding

• Oncology and CNS focus rising

• Animal Health positioning strengthening

• Reliable global supplier reputation maintained

RISKS

• FDA warning letter remains concern

• Shipment delays impacting operations

• ₹85 Cr impairment booked FY26

• Fuel and solvent inflation rising

• Price pass-through lag persists

GROWTH DRIVERS

• High-potency lab operational now

• Panoli pilot plant commissioned

• Specialty chemicals expansion underway

• Backward integration reducing dependence

• ₹149 Cr capex deployed

PRODUCT MIX

• Specialty pharma mix improving

• Innovator CDMO focus increasing

• Capacity utilization stayed 80-85%

• Animal Health commercialization starting

• Higher-value products prioritized

FINANCIALS

• FY26 revenue stood ₹1,713 Cr

• Q4 revenue reached ₹519 Cr

• Q4 EBITDA margin at 20.3%

• FY26 EBITDA margin at 12.9%

• Debt-equity improved to 0.56

SENTIMENT

• Overall tone cautiously positive

• Medium-term confidence remains strong

• Near-term volatility acknowledged clearly

• Recovery phase visibly progressing

CONCLUSION

• Hikal transitioning toward recovery phase

• FDA resolution remains critical trigger

• China 1 trend supports growth outlook

• Complex chemistries driving future focus

• FY27 recovery expected volume-led

#q4results #stockmaket

1

6

437

May 27

Hikal Ltd.📞 Q4 & FY26 Concall Summary #HIKAL

🟡 MANAGEMENT PROJECTION :

Management expects FY27 to be a recovery and transition year with growth returning across pharma, crop protection, and animal health. Pharma plants at Panoli and Bangalore are already operating at 80-85% utilization. The company is targeting 5-6 DMF filings annually versus 2-3 historically. Key projects include a new HPAPI manufacturing facility planned for FY28, expanded Pune R&D infrastructure, a new pilot plant at Panoli, and deeper CDMO engagement across Japan, Brazil, South Korea, and regulated markets. Animal health is targeted to become a 500 crore business over the next 4-5 years. Management also reiterated that long-term revenue targets of 4,000 crores remain intact but delayed by around 2 years because of the recent slowdown.

🔴 Red Alert :

The biggest challenge remains the US FDA warning letter at the Bangalore site, which slowed batch releases, customer shipments, and new CDMO opportunities. Pharma revenue growth remained weak despite high utilization because additional compliance checks increased production cycle times. FY26 also included 85 crores exceptional charges and 47 crores impairment related to retooling a multipurpose Panoli plant into a pharma facility. Raw-material inflation in solvents like Toluene, Methanol, Acetone, and Benzene continues pressuring margins, while price pass-throughs happen with a lag. Crop protection pricing also remains weak because Chinese competitors continue holding prices despite rising global input costs.

🟢 Green Alert :

Q4 FY26 showed strong operational recovery with revenue at 519 crores and EBITDA margins improving sharply to 20.3%. Crop protection delivered particularly strong Q4 EBIT margins of 17.1% while pharma EBIT margins improved to 12%. The company spent 149 crores capex during FY26 focused on debottlenecking, CDMO expansion, and regulatory upgrades. Hikal also reduced debt-to-equity from 0.59x to 0.56x. The biggest operational positive remains improving CDMO traction driven by China-plus-one outsourcing, increasing RFP activity, and new NCE projects entering pilot-trial phases. Panoli remains FDA-clear and is now becoming the key site for new pharma filings and product launches.

🔵 Blue Alert :

Hikal is transforming from a traditional API and agrochemical company into a diversified specialty chemistry and CDMO platform spanning pharma APIs, crop protection, animal health, HPAPIs, ADC payloads and linkers, specialty chemicals, and personal care ingredients. Management is increasingly focusing on higher-value complex chemistries, long-term innovator partnerships, and differentiated CDMO opportunities rather than commoditized products. Animal health, oncology APIs, and specialty chemistry are emerging as the next long-term growth pillars.

🧠 Deep Insight :

The key structural story at Hikal is not short-term revenue growth but the strategic repositioning toward complex chemistry and innovation-led CDMO opportunities. Over the last 3-4 years, the company invested heavily into R&D, pilot plants, HPAPI capabilities, and regulated manufacturing infrastructure, but returns were delayed because of the agrochemical downturn and FDA setback. Now management believes the worst of both cycles is behind them. The Panoli site is especially important because it de-risks the Bangalore FDA issue and becomes the launchpad for future filings and CDMO scale-up. The animal health and oncology platforms could also become meaningful long-term value drivers because competition is lower and margins are structurally better than commoditized APIs. However, execution over the next 12-18 months remains critical. If Hikal successfully resolves the FDA issue, scales new CDMO programs, and improves utilization across its recent capex base, the company could re-enter a much stronger growth phase after several stagnant years.

7

1,275

May 27

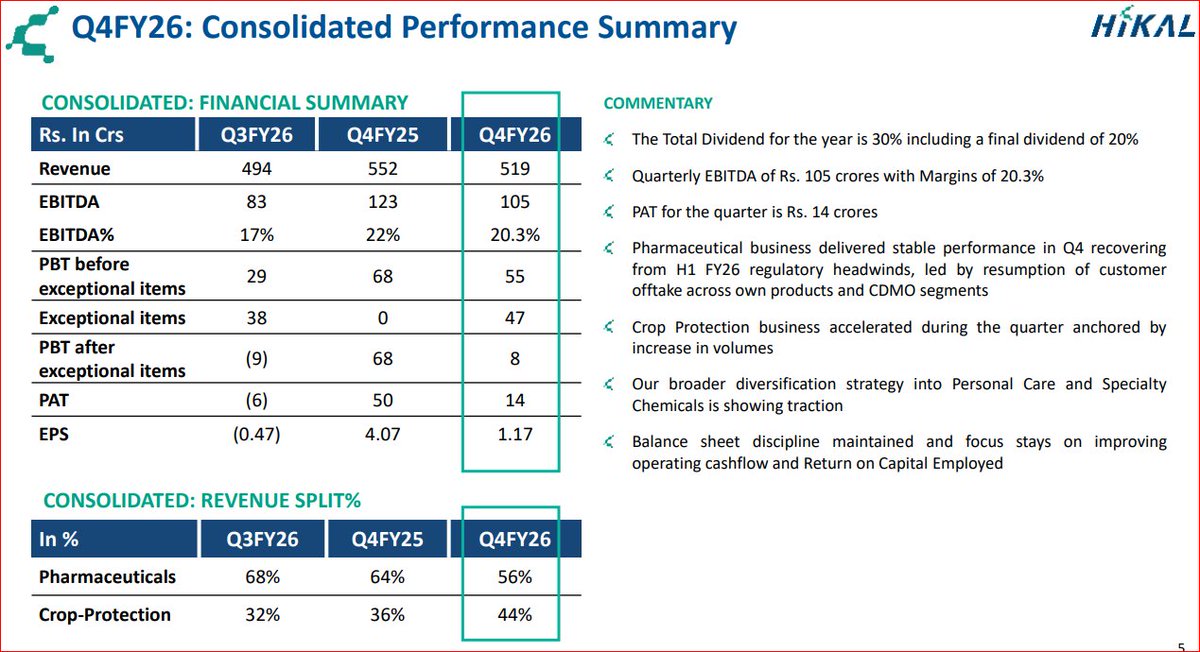

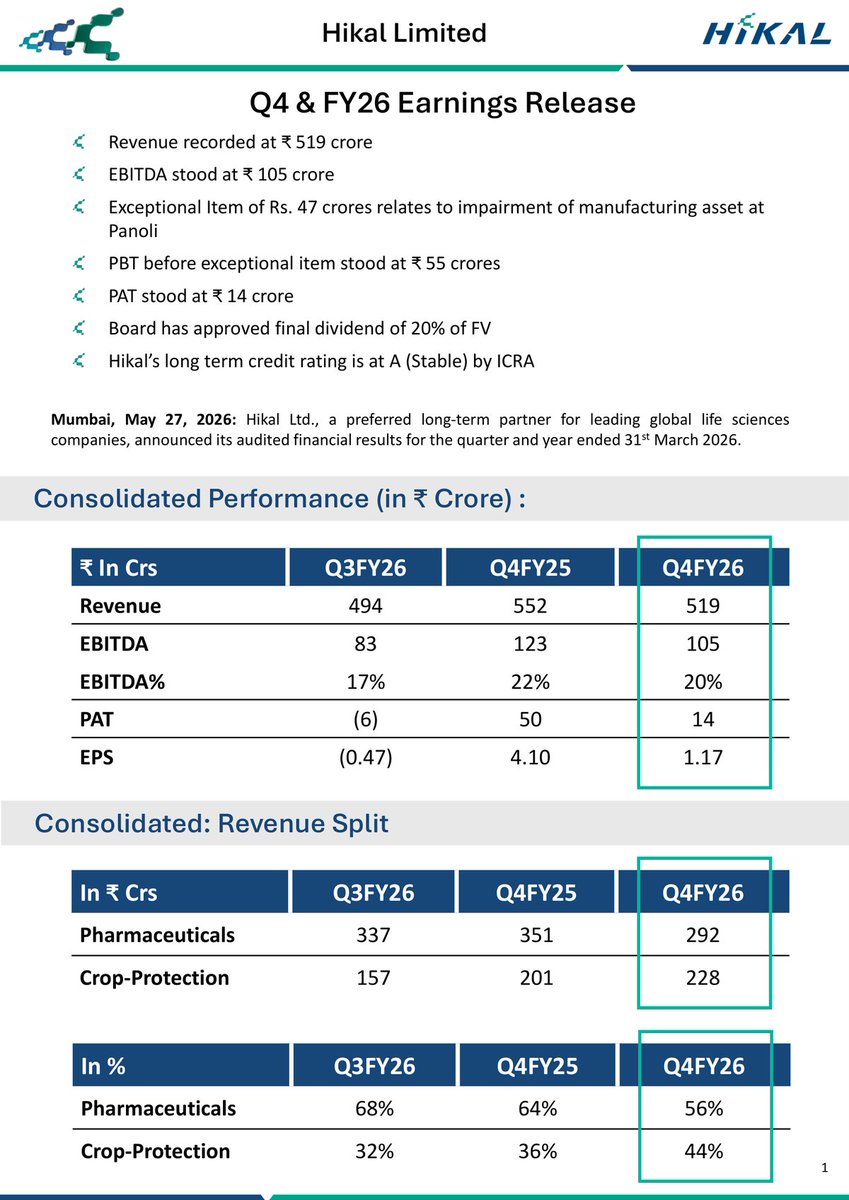

Hikal Ltd Q4 FY26 Results: Revenue at ₹519 Cr, EBITDA Margin 20.3% 📊 | MCap 2,491.29 Cr

- Q4 FY26 Revenue: ₹519 crore

- Q4 FY26 EBITDA: ₹105 crore (20.3% margin)

- Q4 FY26 PAT: ₹14 crore

- Exceptional item: ₹47 crore (impairment at Panoli)

- PBT before exceptional items: ₹55 crore

- Final dividend: 20% (total FY26 dividend: 30%)

- Pharma revenue: ₹292 crore (56% of total, recovering from regulatory challenges)

- Crop Protection revenue: ₹228 crore (44% of total, 45% QoQ, 13% YoY)

- H2 FY26 Pharma growth: 60% vs H1 FY26

- H2 FY26 Crop Protection growth: 25% vs H1 FY26

- Full-year FY26 Revenue: ₹1,713 crore (EBITDA margin: 12.9%)

- Strategic focus: HPAPI & ADC-related chemistries

- Personal Care & Specialty Chemicals diversification progressing (commercialization expected FY27)

- Credit rating: 'A (Stable)' by ICRA

- Operational improvements noted, shift toward sustainable growth

Disc: Information provided in this tweet can be inaccurate, verify through the source in reply before making any investment decision.

Preview 👇 (First 4 out of 5 pages)

1

2

408

May 27

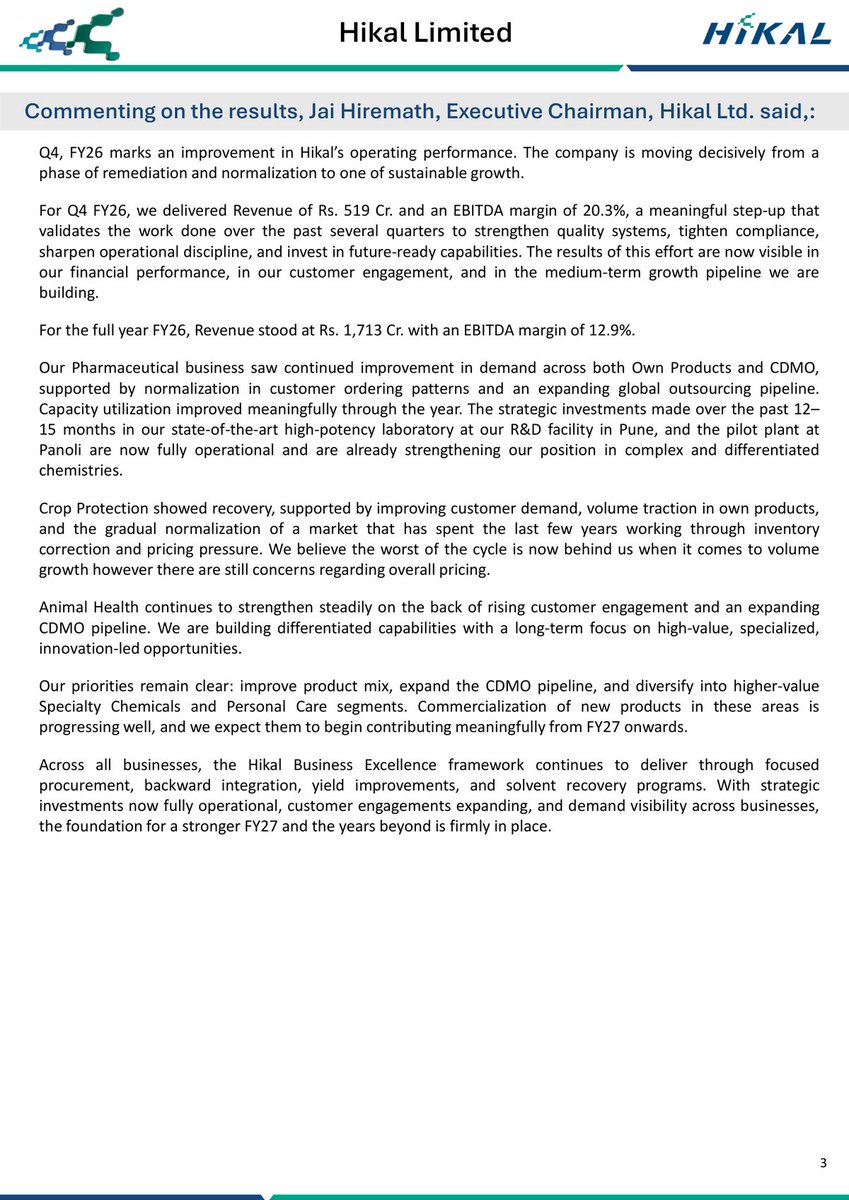

Hikal Ltd. announced its audited financial results for the quarter & year ended March 31, 2026. 📊

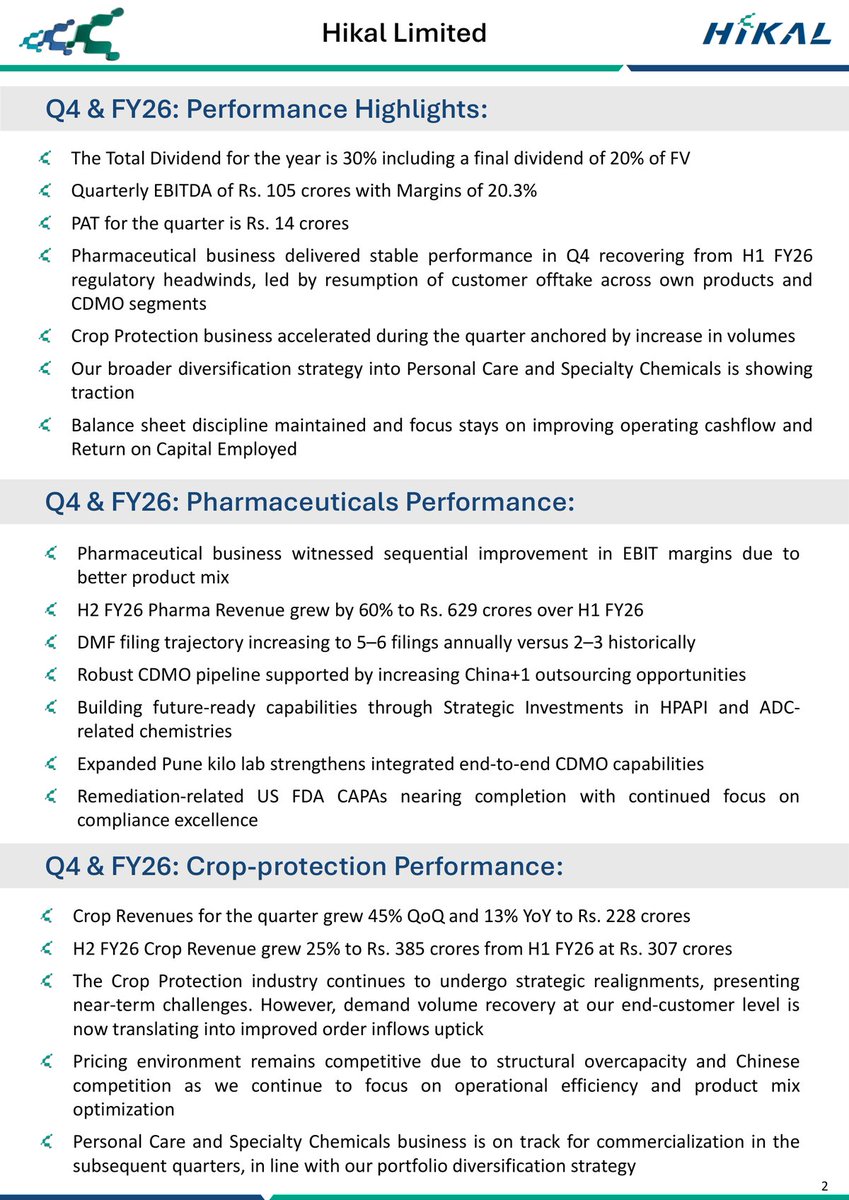

𝗤4 𝗙𝗬26 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀:

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹519 Cr (YoY growth of 13% for Crop Protection, sequential improvement in Pharma).

- 𝗘𝗕𝗜𝗧𝗗𝗔: ₹105 Cr, with margins at 20.3% (a significant step-up).

- 𝗣𝗔𝗧: ₹14 Cr.

- 𝗘𝘅𝗰𝗲𝗽𝘁𝗶𝗼𝗻𝗮𝗹 𝗜𝘁𝗲𝗺: ₹47 Cr related to impairment of manufacturing asset at Panoli.

- 𝗣𝗕𝗧 (𝗯𝗲𝗳𝗼𝗿𝗲 𝗲𝘅𝗰𝗲𝗽𝘁𝗶𝗼𝗻𝗮𝗹 𝗶𝘁𝗲𝗺): ₹55 Cr.

- 𝗗𝗶𝘃𝗶𝗱𝗲𝗻𝗱: Board approved a final dividend of 20% of FV. Total dividend for the year is 30%. 💰

- 𝗖𝗿𝗲𝗱𝗶𝘁 𝗥𝗮𝘁𝗶𝗻𝗴: Long-term credit rating remains A (Stable) by ICRA. ⭐

𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗦𝗲𝗴𝗺𝗲𝗻𝘁 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- 𝗣𝗵𝗮𝗿𝗺𝗮𝗰𝗲𝘂𝘁𝗶𝗰𝗮𝗹𝘀:

▸ Delivered stable performance in Q4, recovering from H1 FY26 regulatory headwinds.

▸ Sequential improvement in EBIT margins due to better product mix. 📈

▸ H2 FY26 Pharma Revenue grew by 60% over H1 FY26.

▸ DMF filing trajectory increasing to 5–6 filings annually.

▸ Robust CDMO pipeline supported by increasing China 1 outsourcing opportunities.

▸ Strategic investments in HPAPI & ADC-related chemistries are building future-ready capabilities.

▸ US FDA CAPAs nearing completion.

- 𝗖𝗿𝗼𝗽 𝗣𝗿𝗼𝘁𝗲𝗰𝘁𝗶𝗼𝗻:

▸ Accelerated during the quarter, with revenues growing 45% QoQ & 13% YoY to ₹228 Cr.

▸ H2 FY26 Crop Revenue grew 25% over H1 FY26.

▸ Demand volume recovery translating into improved order inflows.

▸ Focus on operational efficiency & product mix optimization amidst competitive pricing.

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝗶𝘁𝗶𝗮𝘁𝗶𝘃𝗲𝘀 & 𝗢𝘂𝘁𝗹𝗼𝗼𝗸:

- 𝗗𝗶𝘃𝗲𝗿𝘀𝗶𝗳𝗶𝗰𝗮𝘁𝗶𝗼𝗻: Broader diversification strategy into Personal Care & Specialty Chemicals is showing traction, with commercialization expected from FY27 onwards. 🌱

- 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝗘𝗳𝗳𝗶𝗰𝗶𝗲𝗻𝗰𝘆: Hikal Business Excellence framework continues to deliver through focused procurement, backward integration, yield improvements, & solvent recovery programs.

- 𝗚𝗿𝗼𝘄𝘁𝗵 𝗢𝘂𝘁𝗹𝗼𝗼𝗸: Company is moving from remediation to sustainable growth, with a strong foundation for FY27 & beyond, driven by operational improvements, expanded customer engagements, & demand visibility.

📊 HIKAL LTD | 🏷️ Press Release / Media Release

🌐 Details: wegro.app/JpR0oN

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

2

188

May 20

Ajinomoto Bio-Pharma ServicesのHPAPI製造Brochure

ajibio-pharma.com/wp-content…

HPAPI製造選定の記事として、OEB/OEL設定、封じ込め、作業者訓練、spill response、PAT、in-house analytical developmentまで触れており、実務的なチェックリストとして使えそうですね。

設備だけでなく、toxicologist/hygienist、模擬作業訓練、swab後のQC release、設備メンテナンスまで確認すべきという点が挙げられています

なお、HPAPIでは「isolatorがある」や「PPEを使う」だけでは不十分です。実際には、どのOELレンジまで実績があるか、containment performanceをどう実測しているか、洗浄バリデーション、交叉汚染、surface/air monitoring、廃棄物処理まで気にすると安全ですね。

ADC payloadやdrug-linkerでは、作業者の安全だけでなく、conjugatable impurityやfree drug-related impurityの管理にも直結しえます。CDMO選定では、HPAPI単体の合成能力に加えて、封じ込め下での分析・サンプリング・精製・ADC工程へのワークフローまで見て評価すべきだと思います。

3

1,267

Apr 22

The Chemistry Expertise:- Where the Real Moat Lies

In the CRDMO business, the #1 factor MNCs evaluate is: can this partner independently solve complex chemistry problems and come up with creative solutions the MNC hadn't thought of?

Usually in Indian CRDMO & CDMO landscape companies usually have expertise in one / two chemistries but Sai posses expertise across variable chemical chemistry and is not confined to a particular chemistry this is attributed by continuous work on building new capabilities over the years.

Sai's chemistry capability stack is among the broadest in India:

> Complex Chiral Chemistry: The gepant intermediates (Qulipta/Ubrelvy) involve chiral centres and complex ring systems at ~₹3 lakh/kg realisations. This isn't commodity chemistry.

> Photo-flow Chemistry: Successfully scaled late-phase photo-flow bromination to GMP plant scale for a large pharma client. This is cutting-edge — very few Indian CDMOs can do continuous photochemistry at manufacturing scale.

> Electrochemistry: Centralised group created to enable broader adoption across Discovery and CMC. This is an emerging reaction technology that reduces waste and improves selectivity.

> High-Potency API (HPAPI): OEB-6 labs operational for Discovery, process development labs coming by Oct 2026. Containment validated down to 1 µg/m³. Essential for next-gen ADC payloads and potent oncology compounds.

> Macrocyclic Peptide Synthesis: Successfully delivered a full library of AI-designed macrocyclic peptides demonstrating capability in one of the hardest synthetic chemistry challenges.

> Amidite Chemistry: Already commercially manufacturing phosphoramidites (oligonucleotide building blocks) at $50,000 /kg unit rates. Sai is executing 3-4 years ahead of key Indian peers in this space.

The average realisation across Sai's molecule portfolio has jumped from ~₹3,000/kg to ₹8,500 /kg post FY23, a 3x step-up reflecting the shift from commodity intermediates to complex chemistry. This realisation improvement drives both revenue growth AND margin expansion simultaneously.

1

1

10

3,332

Apr 21

TCIのバイオコンジュゲーション受託サービス。私がまだ日本にいた時はそこまで目立っていなかった印象ですが、最近広告をよく目にします。

ここで書かれているようなキレーター分子やスペーサー分子を含む低分子合成はイメージがわきますが、Bioconjugationのサービスも行うとのこと。

HPAPI対応や、たんぱく質取り扱い、cGxP対応などいろいろ気になるところではあります。

Apr 21

【バイオコンジュゲーション受託サービス】

バイオコンジュゲーションは、低分子化合物とリンカー、抗体やタンパク質を結びつける技術で、ADC(抗体薬物複合体)や創薬などの分野で注目されています。

弊社では、この3段階のプロセスを一貫してサポートします。

buff.ly/nfhr99J

1

1

5

2,514

Hi there hpapi, sorry to hear the game is too dark for you. There are a few things which may be causing this - can you let us know which platform you play on, and if any particular settings seem to affect it, such as HDR?

23

Apr 6

As per my limited knowledge capacity already build, HPAPI lab also there but Due to USFDA issue stock down still not resolved, & major pharma CDMO Project in early stage management comment on recent concall 2-3 project can enter into commercial stage.

3

906

Apr 6

👉 Hikal ne new capacity add ki hai (HPAPI pilot plant), but abhi focus hai:

existing plants ka utilization badhana

new product pipeline ko scale karna

FY27 se new segments (personal care) ka contribution”

👉 Large-scale expansion announcement nahi hai (abhi tak)

7

1,747

Mar 31

Who benefits?

Divi’s Labs — custom synthesis GLP-1

Syngene — end-to-end CRDMO

Piramal Pharma — HPAPI injectables

Cohance — ADC complex pipeline

These are not generic companies anymore.

1

1

2

288

Mar 28

Contract Pharma recently caught up with Arul Ramadurai, Chief Commercial Officer, Axplora, to discuss the company’s investment in expanding its HPAPI development and manufacturing capabilities. ➡️ hubs.li/Q048Gzv90

#pharmanews #HPAPI #DCATWeek

1

3

139

Mar 21

2026 Market Trends Affecting Selection :

"China Plus One" Opportunity: The Biosecure Act is driving a significant shift in, or expansion of, manufacturing contracts to Indian and other emerging markets.

Capacity Constraints: As specialized unit operations (e.g., OEB-4/HPAPI) become bottlenecks, early planning and securing slots for 2026 is necessary.

Shift from Volume to Value: Top players are moving toward specialized capabilities rather than just low-cost, high-volume generic production.

2

367

Axplora Expands Manufacturing Facilities at Its Italian Farmabios Site

Construction is already underway at #Axplora's Farmabios HPAPI manufacuring facility in Italy, with completion targeted for February 2027

#biomanufacturing #biopharma #drugdevelopment

hubs.li/Q047Kcl00

1

3

442

#Ipsen and #QuotientSciences have extended a commercial supply partnership to manufacture a treatment for the ultra-rare disease #FibrodysplasiaOssificansProgressiva. Ipsen has invested in new equipment at Quotient's Boothwyn, PA facility. pharmamanufacturing.com/indu… #CRDMO #HPAPI

2

71

#ALIVUS

#ValueInvesting #GrowthInvesting #ValueGrowthPredictorSetup

Alivus Life Sciences Ltd (formerly Glenmark Life Sciences) presents a compelling case for investors who balance steady cash flow (Value) with structural expansion (Growth). Following its acquisition by the Nirma Group, the company is pivoting toward significant capacity expansion and a higher-margin CDMO (Contract Development and Manufacturing) play.

1. Value Investment Perspective -

From a value standpoint, Alivus is characterized by financial discipline and efficient capital usage.

* Valuation vs. Industry: Trading at a P/E of ~21.2x, it is relatively undervalued compared to the pharmaceutical industry average of ~39x. This discount offers a margin of safety for value-oriented investors.

* Debt-Free Status: The company is net debt-free and has maintained this status for five years. This provides a fortress balance sheet, allowing it to fund future expansions without interest burden.

* Efficient Returns: It boasts strong return ratios, with ROE at 18.86% and ROCE at 24.97%. This indicates a high efficiency in generating profits from shareholders' equity and capital employed.

* Dividend Potential: While the current yield is modest at ~0.53%, its robust cash flow from operations (historically over ₹300–400 Cr annually) suggests a sustainable capacity for payouts.

2. Growth Investment Perspective -

The growth narrative centers on Alivus evolving from a pure-play API manufacturer to a diversified life sciences partner.

* Capacity Expansion: The management has a roadmap to increase reactor capacity from 1424 KL to 2650 KL by FY28. This brownfield expansion at Dahej and Ankleshwar is a major long-term growth lever.

* CDMO Pivot: Currently contributing ~7% of revenue, the CDMO segment is expected to scale as the company wins more high-value contracts (the 5th contract is expected to commercialize in H2FY26).

* Pipeline & High-Potency APIs (HPAPI): The company has 586 DMF and CEP filings globally. It is specifically focusing on the HPAPI portfolio (Oncology, etc.), which has a total addressable market (TAM) of $66 billion.

* Independence from Glenmark: While the transition led to some inventory rationalization (de-growth in GPL segment), the management expects this to be transitory. Post-acquisition, Alivus has the "liberty for capex" under Nirma to pursue independent growth.

3. Technical Analysis (Short-to-Medium Term) -

As of early February 2026, the stock exhibits a neutral-to-bullish technical setup with signs of a bottoming-out process. Indicator | Value/Status | Interpretation Current

Price | ₹943.00 | Trading near a recovery zone after a 20% correction over the last year.

RSI (14) | ~53.5 | "Neutral. It is neither overbought nor oversold, leaving room for upward movement."

MACD | 6.8 (Positive) | "Bullish. The MACD line is above the signal line and the center line, indicating gaining upward momentum."

Moving Averages | Mixed | "The stock is attempting to cross its 50-day and 200-day EMAs, which would act as a confirmation of a trend reversal." 52-Week Range | "₹819 – ₹1,251" | "Currently trading at the lower end of its range, providing a potential entry point for a ""mean reversion"" trade."

Key Levels to Watch -

* Resistance: ₹980–₹1,000. A sustained close above ₹1,000 could trigger a fresh rally toward ₹1,150.

* Support: ₹900 is a psychological floor, with strong structural support at the 52-week low of ₹819.

Summary Recommendation -

Alivus Life Sciences is a "Quality Value" play. It suits investors looking for a stable, zero-debt company that is currently available at a discount to its peers while sitting on the cusp of a multi-year capacity expansion phase.

1

325

Jan 14

楽天メディカルとロッテバイオロジクス:グローバル製造委託契約を締結

lottebiologics.com/en/public…

楽天メディカルつづきですね

JP Morganで発表されたばかりの非常にタイムリーなニュースです。

先ほどポストした「1億ドルの資金調達」に続き、今度は製造体制についての発表です。

楽天メディカルと、韓国のロッテグループ傘下でCDMOを手掛けるロッテバイオロジクス(LOTTE Biologics)が、光免疫療法のためのバイオ医薬品製造の受託契約を結びました。要はアキャルックスの製造 と捉えてよいのかなと。

製造拠点は 米国ニューヨーク州にあるシラキュース・バイオキャンパスになります

先程のポストにある1億ドルの資金調達を活かして、アキャルックスの製造を米国のロッテバイオロジクスのサイトで行い、2028年の米国承認というゴールへ向かう、という楽天メディカルの非常に明確なロードマップが見えてきました。

楽天メディカルの薬剤(ASP-1929/アカルックス)は、ADCに非常に近いため、ADCの製造ノウハウを持つロッテバイオロジクスとの相性が非常に良いと言えます。

Non-HPAPIのADCと考えればよいわけですからね。理にかなった戦略かなと思います。

Jan 14

楽天メディカル、シリーズFラウンドでの1億ドルの資金調達完了

rakuten-med.com/us/news/pres…

日本発の治療法である「光免疫療法」のグローバル展開に向けた進展ですね。ASP-1929(すでに日本ではアキャルックスとして承認済み)の米国承認を加速させる予定。

リンク元によると2028年の米国FDA承認申請を目指すようです

なお、こちらのADCは Cetuximabと、光に反応する色素IR700をConjugateさせたもの。近赤外線(690nm)を照射することで、光に反応した薬剤が癌細胞の細胞膜を物理的に壊死させます。

9

1,773

Jan 4

少し前までは安定供給の観点からバイオ医薬品の製造分散が必要だと捉えていましたが、最近は需要・設備の問題に加えて、地政学的リスクや各国規制、輸送制約も無視できない論点になってきました。

ADCのような複合モダリティは、抗体、linker-payload(多くはHPAPI)、コンジュゲーションと、工程ごとに要求されるケイパビリティが異なります。CDMOで分散生産を設計する場合、エンドツーエンドで完結できる拠点を複数持つのか、各工程を複数社で二重化してつなぐのか、いずれにしても分散の単位を揃える必要があります。後者では工程間の技術移管・品質責任の切り分け・物流(規制対応や温度管理を含む)が複雑化しやすく、そこがボトルネックになり得ます。

一方で、この複雑性をマネージし、統合的に提供できるCDMOにとっては差別化要因になり得るので、投資余力のあるプレイヤーには追い風だと思います。

Jan 3

第一三共、抗がん剤増産へ日米独中に3000億円

nikkei.com/article/DGXZQOUC2…

「抗体薬物複合体(ADC)」と呼ぶ技術を使う医薬品の製造工場を新設します。治験で特に乳がんに効果を示したADC薬の主力抗がん剤「エンハーツ」は、需要の高まりが予想されます。

6

49

13,026

المخاطر المتعلقة بالسلامة في تصنيع الأدوية

أهم المخاطر المتعلقة بالسلامة في تصنيع الأدوية:

تُعد صناعة الأدوية من أكثر الصناعات حساسية ودقة، نظرًا لارتباطها المباشر بصحة الإنسان. ورغم التطوّر الكبير في التكنولوجيا، لا تزال بيئة التصنيع الدوائي تواجه مجموعة من المخاطر التي تتطلّب ضوابط صارمة وإجراءات سلامة عالية المستوى.

1- مخاطر التعرض للمواد الكيميائية والفعالة:

تتعامل المصانع الدوائية مع مركّبات شديدة الفعالية، قد تشكّل خطورة على العمال إذا لم تُدار بشكل صحيح.

مخاطر محتملة:

تهيّج أو تلف الجهاز التنفسي.

حساسية جلدية.

تأثيرات سمّية طويلة الأمد.

.(Airborne API) انتقال الجزيئات النشطة عبر الهواء

إحصائيات:

" (Active Pharmaceutical Ingredient)"API

تشير تقارير مهنية إلى أن 37% من العاملين في مصانع الأدوية تعرّضوا لمستويات أعلى من الحدود المسموح بها في حال غياب وسائل الحماية.

"المكونات الصيدلانية النشطة عالية الفعالية (Highly Potent Active Pharmaceutical Ingredients)، " (HPAPI)

يعمل أكثر من 65% من مصانع الدواء عالمياً على تصنيع مركّبات عالية الفعالية ما يزيد من مخاطر التعرّض.

:(Microbial & Cross Contamination) 2- مخاطر التلوث

التلوث المتبادل أحد أخطر التحديات، وقد يؤدي إلى سحب منتجات من الأسواق أو إصابات صحية خطيرة.

أمثلة للمخاطر:

انتقال بكتيريا أو فطريات لخط الإنتاج.

تسرّب جسيمات من معدات غير معقمة.

تلوّث بسبب اختلاف المنتجات في خطوط مشتركة.

إحصائيات:

تمثل قضايا التلوث ما يقارب 27% من أسباب سحب الأدوية من الأسواق سنويًا.

تشير التحليلات إلى أن 70% من أخطاء التلوث سببها مشاكل في النظافة أو الإجراءات التشغيلية.

3- المخاطر الميكانيكية داخل خطوط الإنتاج:

التجهيزات الضخمة والمتقدمة قد تسبّب إصابات مباشرة.

مخاطر تشمل:

انحشار الأيدي في آلات الضغط والتحبيب.

مخاطر السقوط والانزلاق.

انفجار المواد عند ضغط غير مناسب (مثل المساحيق الغباريّة).

إحصائية عالمية:

حوالي 14% من إصابات مصانع الدواء تعود لمخاطر ميكانيكية في خطوط الإنتاج.

4- مخاطر الحريق والانفجار:

رغم أن المنشآت تكون مصممة بتقنيات سلامة عالية، فإن بعض مراحل الإنتاج تعتمد على مذيبات قابلة للاشتعال.

أسباب شائعة:

تخزين خاطئ للمذيبات العضوية.

. "من الكلمة الفرنسية "ATmosphères EXplosibles" (أجواء قابلة للانفجار)" ATEX شرارة كهربائية داخل مناطق

سوء التهوية في غرف التحبيب أو التجفيف.

إحصائيات:

تُسجّل سنويًا أكثر من 120 حادث حريق في مصانع أدوية حول العالم نتيجة مذيبات قابلة للاشتعال.

5- المخاطر البيولوجية (خصوصًا في اللقاحات والمستحضرات الحيوية):

تستخدم بعض خطوط الإنتاج كائنات حية دقيقة أو بروتينات معقدة.

تشمل المخاطر:

تسرب فيروسات مخبرية.

تفاعل مناعي للعمال.

تلوث بيئي.

أحدث التقنيات المستخدمة لتعزيز السلامة في تصنيع الأدوية:

:(Isolators & ""نظام الحواجز ذات الوصول المقيد" (Restricted Access Barrier Systems""RABS) 1- أنظمة العزل

.% تقلل تعرّض العمال للمواد عالية الفعالية بنسبة قد تصل إلى 99.9

:(Pharma Automation) 2- الروبوتات والأتمتة

تستخدم الروبوتات في تعبئة الحقن، نقل المواد، وتنظيف المعدات.

.% تقلل الأخطاء البشرية بنسبة 40–60

:(Environmental Management System EMS) 3- تقنيات مراقبة البيئة

أنظمة ذكية تراقب الجسيمات والحرارة والرطوبة.

تعتمد على الذكاء الاصطناعي لتحسين جودة الهواء في غرف التصنيع.

:(""High Efficiency Particulate Air"،"جسيمات عالي الكفاءة"" & " Ultra-Low Particulate Air، فلاتر هواء فائقة الكفاءة " Ultra-Low Particulate Air، فلاتر هواء فائقة الكفاءة ULPA") 4- أنظمة الترشيح المتقدمة

.% إزالة الجسيمات الدقيقة بنسبة تصل إلى 99.999

:(Continuous Manufacturing) 5- تقنيات الإنتاج المستمر

.% تقلل زمن الإنتاج بنسبة 50

تقلل معدلات التلوث لغياب النقل بين المراحل.

الأكواد والمعايير الدولية المعتمدة في تصنيع الأدوية:

:((Good Manufacturing Practices)، GMP) 1- ممارسات التصنيع الجيد

الدستور الأهم لضمان جودة وسلامة المنتجات، وتشرف عليه جهات مثل:

" "Food and Drug Administration" (إدارة الغذاء والدواء FDA" – 21 " قانون اللوائح الفيدرالية" (Code of Federal Regulations

CFR" Part 210/211

" "Good Manufacturing Practices" (ممارسات التصنيع الجيدة) الخاصة بـ"الاتحاد الأوروبي EU GMP"

" Good Manufacturing Practices" (ممارسات التصنيع الجيدة) التي تضعها منظمة الصحة العالمية World Health Organization) WHO "WHO-GMP""

:ISO2-

5

3

7

210