🆕 Hashdive added to #polymartapp

To find an informational edge, prediction market traders use Hashdive to track whale wallets and volume shi…

Support @hash_dive & @polymartapp — like & retweet 🙏

#Hashdive #Polymarket #PortfolioTrackers #SignalsAlerts #DataApis

2

4

158

Could've used Hashdive 🤿

Polymarket is partnering with blockchain analytics firm Chainalysis to help police its platform as prediction markets grapple with increased scrutiny over insider trading. bloomberg.com/news/articles/…

1

5

744

ℹ️ UK recession in 2026?

UK growth forecasts sit at just 0.8% for 2026 amid Middle East tensions and rising input costs. Yet Polymarket prices a 34% chance of recession. Is the market overreacting to headlines?

▫️Polymarket: Yes: 34% / No: 64%

▫️IQ Analytics: Yes: 29% / No: 71%

Why the gap?

1️⃣ Historical base rate for a technical recession in any given year is only 15–20% since 1955.

2️⃣ Ensemble of optimistic/realistic/pessimistic scenarios lands at 28–32%. We haircut to 29% due to the strong “Iran risk” narrative and thin liquidity.

3️⃣ Hashdive shows very low volume ($230) and neutral Smart Money positioning, suggesting the 34% price is driven more by fear than conviction.

🧊 The market is slightly overpricing recession risk. Small edge to No at current levels, but liquidity is thin and geopolitics hard to quantify. Not a screaming opportunity, more of a “wait and see” setup.

#Polymarket #UKRecession #Economy

ALT Polymarket - UK Recession in 2026?

2

56

Apr 11

不要再使用polymarket的官方数据了!

做的实在是太差了!我已经不知道踩了多少坑!

正常逻辑,官网或者官方api获得数据是最可靠的

唯独我们的polymarket,非常之不靠谱

比如说这个地址reachingthesky,官网现实就是个菜逼。总共亏了90刀!实际上polygen链上的数据显示是超级大聪明!交易了8个市场,利润高达370万刀!!

如果你觉得拔链上不方便,可以考虑下面几个网站,我验证下数据比较准确的吧。

polymarketanalytics.com/

这是一个专门针对去中心化预测平台 Polymarket 的数据分析平台。其核心功能是追踪链上地址的真实盈亏(PNL)、监控“聪明钱”动向,并解析复杂的链上交互操作。它的最大优点在于能够有效过滤套利机器人的干扰,提供比官方更精准的收益率维度,非常适合需要深度跟单和趋势研判的交易者。

Predictfolio predictfolio.com/

核心功能是帮助用户一站式汇总和管理在各个预测事件中的仓位、历史记录及预期收益。

Hashdive

hashdive.com/。它的核心功能侧重于追踪特定哈希值的交易流向、智能合约交互细节以及资金的底层异动。

11

32

183

21,367

Apr 10

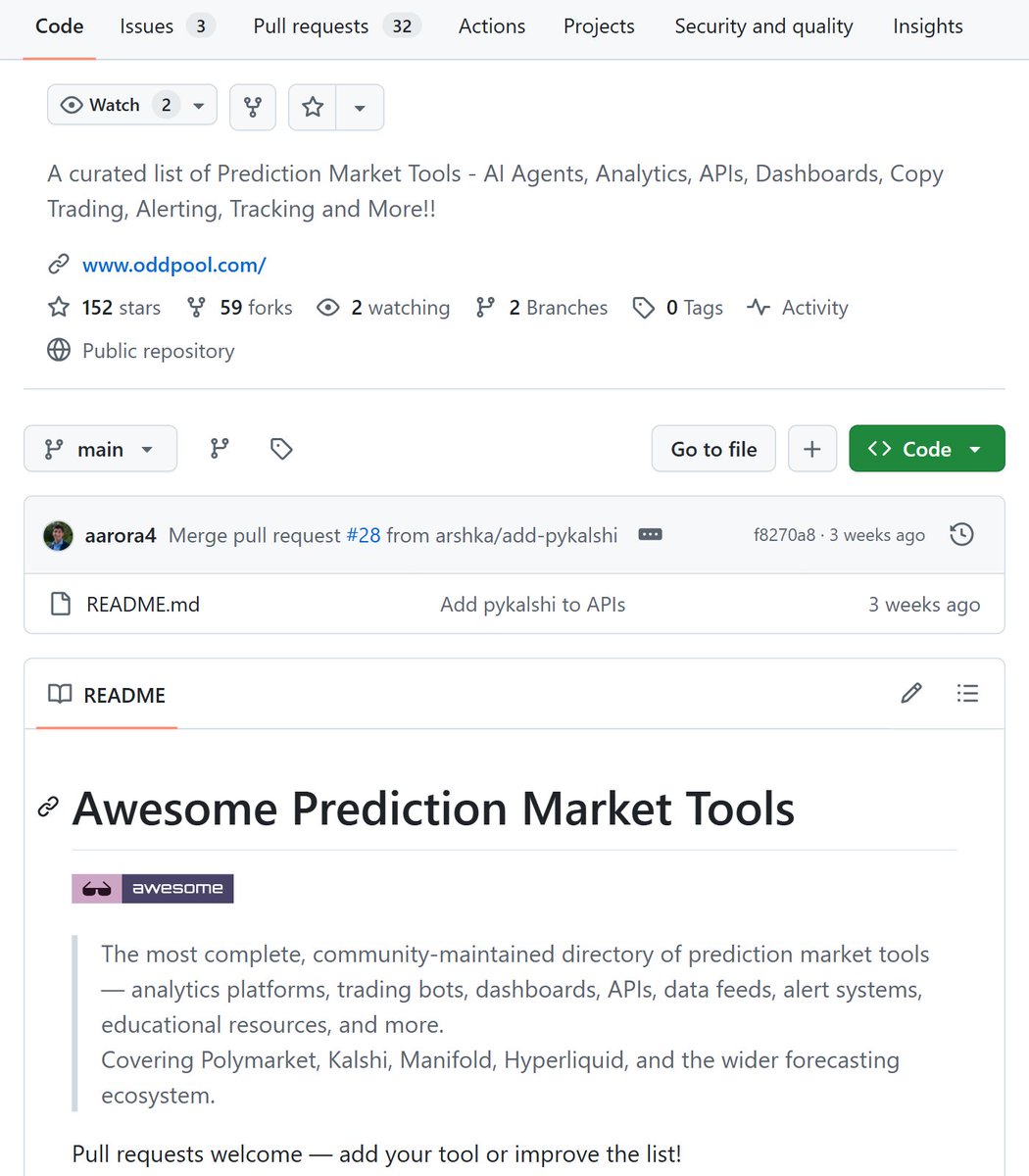

Found one GitHub repository that replaces 50 separate searches for Polymarket tools

aarora4/Awesome-Prediction-Market-Tools - a community-maintained directory of everything that exists in the prediction market ecosystem

Covers Polymarket, Kalshi, Manifold, Hyperliquid, and more

Here's what's inside:

> AI Agents - 30 tools: from Alphascope (real-time signals) to Polybro (an agent that researches data on its own and outputs trading decisions)

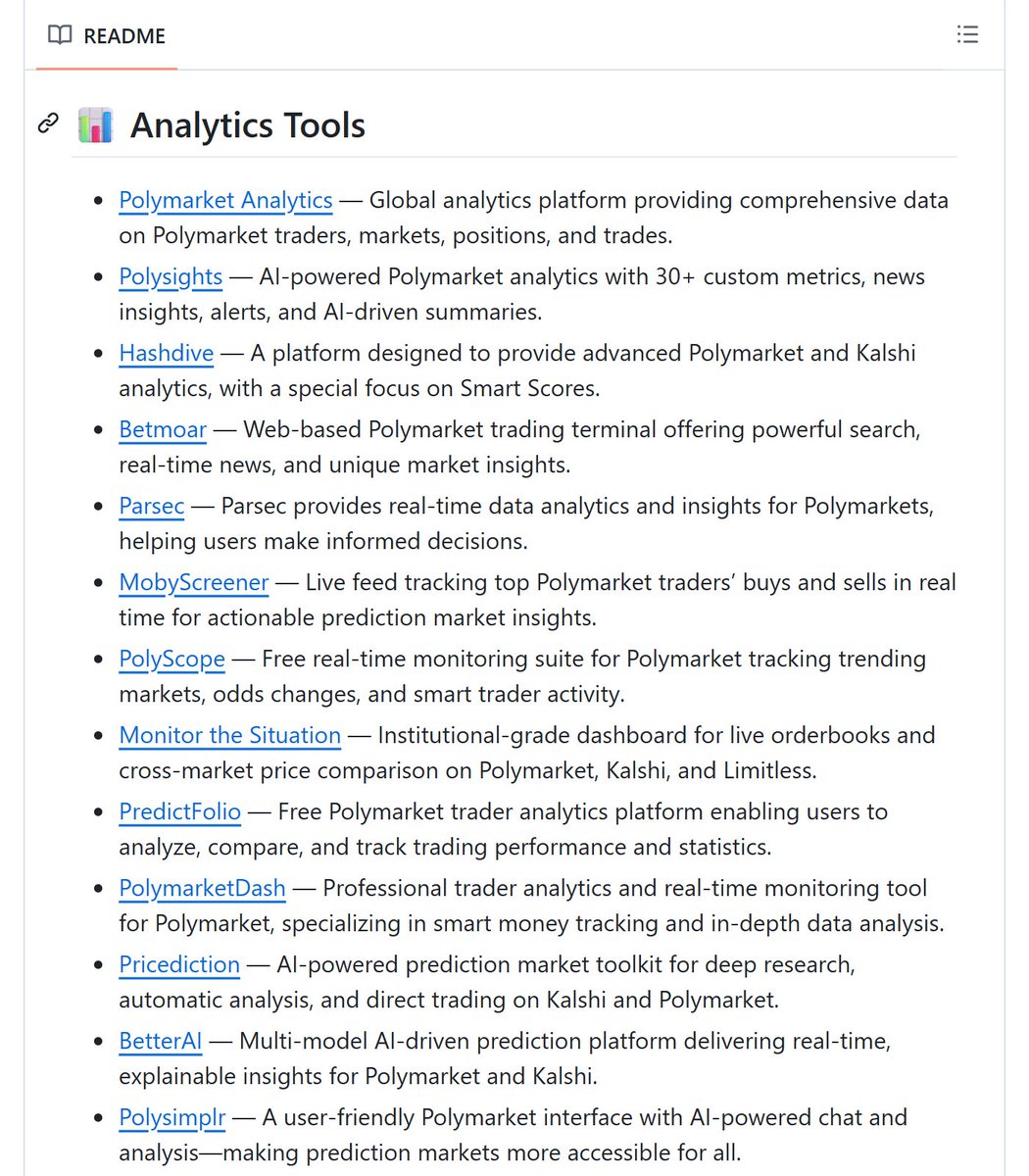

> Analytics - Polymarket Analytics, Hashdive, EventWaves, TREMOR with SQL queries across 140k markets, and dozens more

> Alerts - Whale Tracker Livid, PolyIntel, PolySpy, YN Signals. If a big player enters a market - you're the first to know

> Arbitrage - ArbBets, Eventarb, PolyScalping, Polytrage. Automated alerts on price discrepancies between Polymarket and Kalshi

> Trading Bots - Sharpe Terminal, Converge, Rainmaker, Polycule, and ~25 more of varying complexity

> Data - TREMOR, Artemis, Blockworks, several Dune dashboards with on-chain data

> DeFi - Gondor (loans against Polymarket positions), Robin (yield on open positions), HyperOdd (20x leverage)

> Infrastructure - SEDA, OrderbookTrade, Compose for those building their own tools

The repo is actively maintained: 10 contributors, 12 open PRs - people keep adding new tools constantly

GitHub: github.com/aarora4/Awesome-P…

If you're building a bot or looking for trading tools - start here

Apr 4

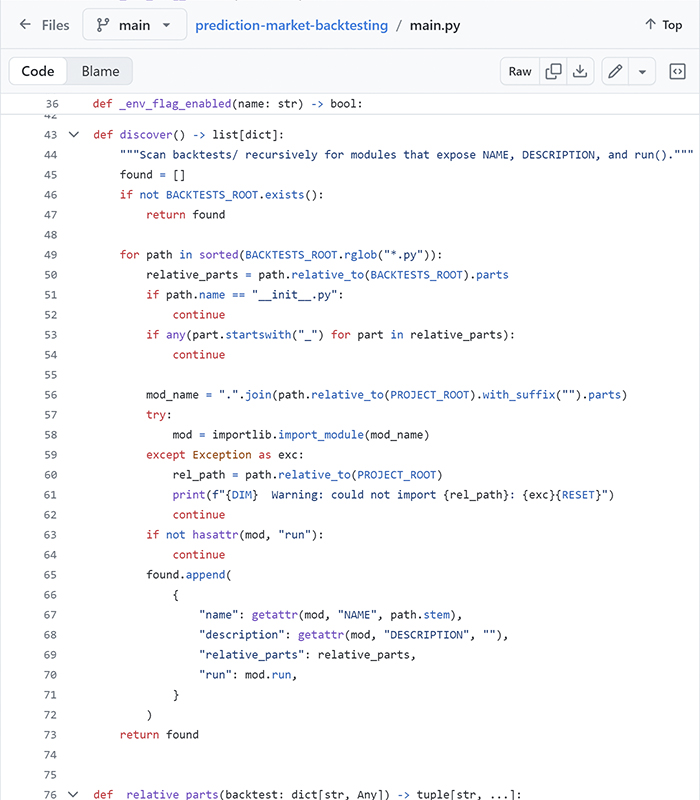

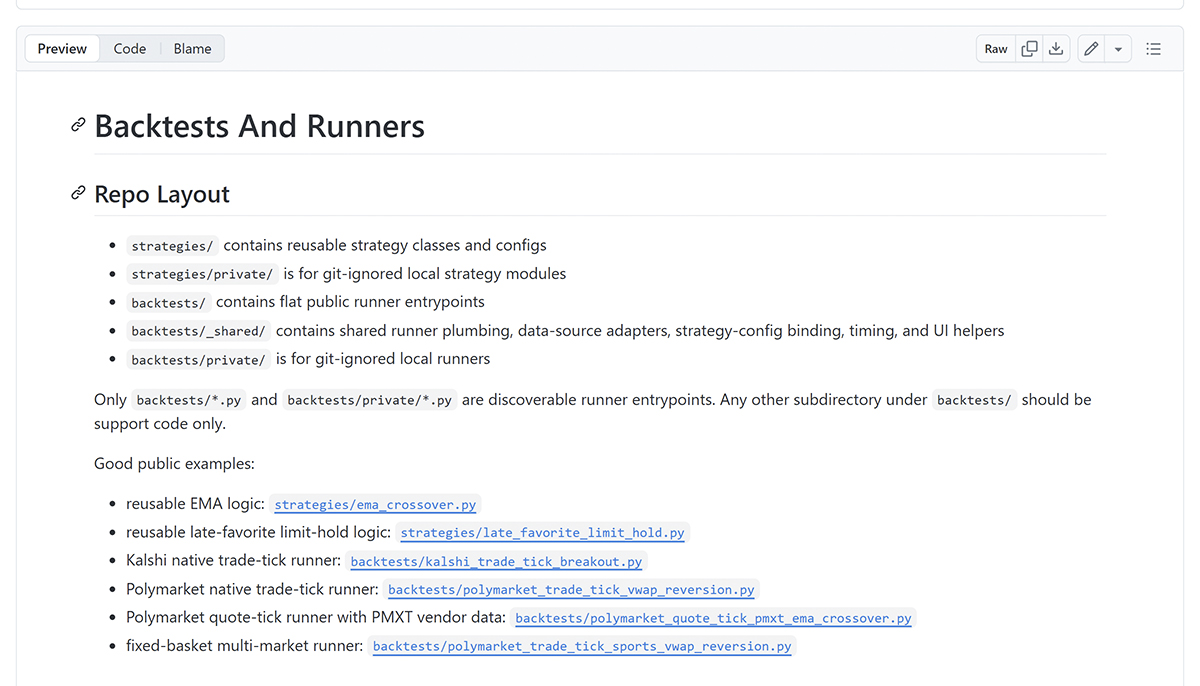

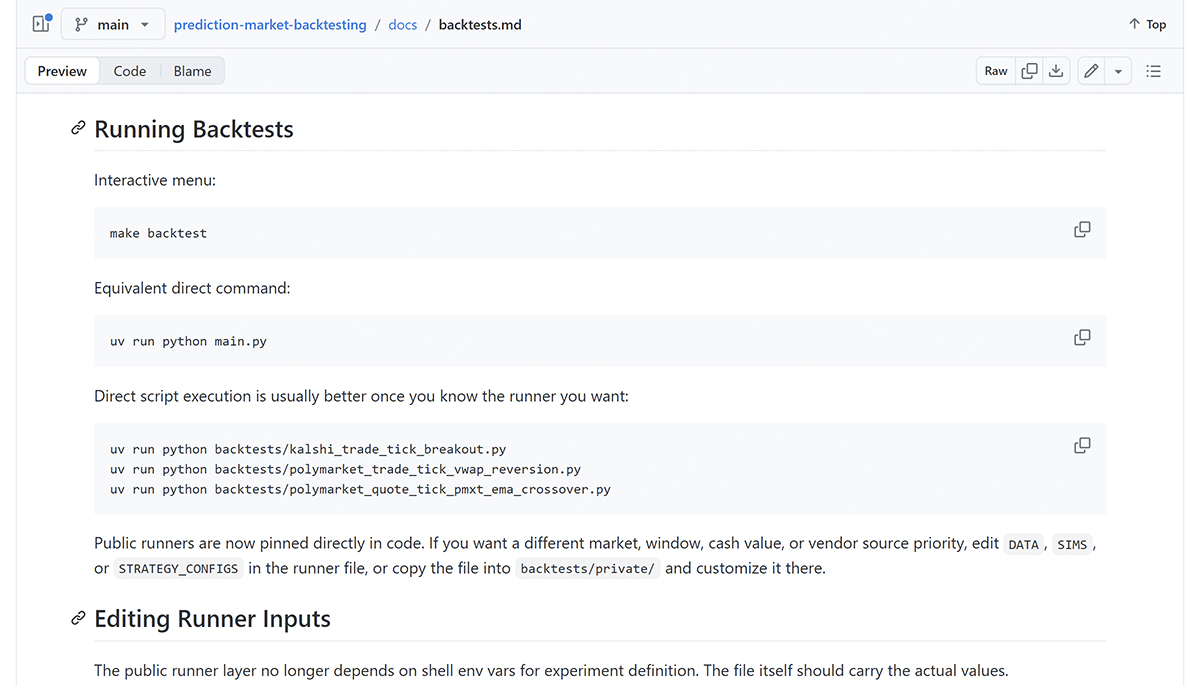

This GitHub repository lets you backtest trading strategies on real Polymarket and Kalshi data

An event-driven engine that replays historical trades in chronological order - simulating order fills, portfolio tracking, and market lifecycle events

Built on top of Jon-Becker's dataset with 36GB of real trade history

What's inside:

> Three ready-to-use strategies: buying at low prices, calibration arbitrage, and martingale with mean-reversion

> Detailed charts: equity curve, P&L, drawdown, Sharpe, monthly returns

> Polymarket and Kalshi support out of the box

> Simple API for writing your own strategies - drop a file in the folder and it appears in the menu automatically

> Hooks for every event: market open, close, resolution, order fill

Most people test strategies on paper or go straight to live trading

This engine lets you run a strategy through millions of real trades before spending a single dollar

You see the drawdown, Sharpe, monthly returns - all on real data, not synthetics

Repo is in active development, full release planned in 1-2 months. Good time to get in early and star it while there's still barely anyone there

GitHub: github.com/evan-kolberg/pred…

8

12

147

29,441

Mar 27

Every Polymarket tool worth bookmarking right now

PolyHelper - browser extension built by @0xd1namit. LP calculator, top holders PnL, TradingView charts, deep analytics - all inside Polymarket

Link > polyhelper.io

Polymarket Decoder - paste any wallet, get full breakdown: what they trade, when they're active, how they make money

Link > polymarketdecoder.com

Polymarket Analytics - leaderboards, top trader profiles, arb screener across Polymarket and Kalshi

Link > polymarketanalytics.com

Kreo - copy trading platform. pick a wallet, mirror entries automatically.

Link > kreo.app/@neyaroslav

Merlin Trade - another copy trading with stacked reward streams on top. good for airdrop farming

Link > t.me/merlin0_bot?start=ref_n…

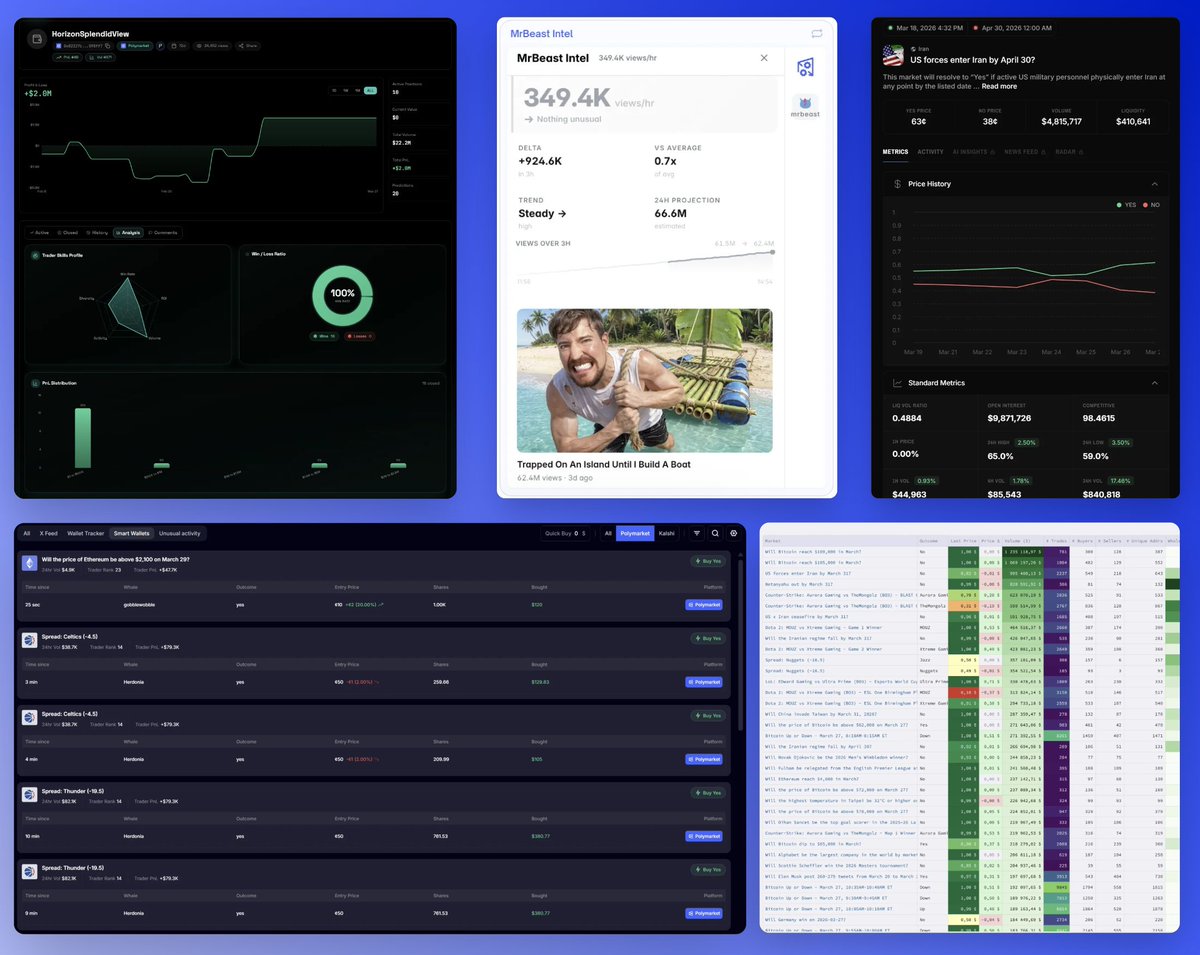

Hashdive - Smart Scores, whale tracker, market screener, bot detection, candlestick charts with RSI/MACD

Link > hashdive.com

Polysights - 30 custom metrics, AI summaries, insider finder, order book, news feed

Link > polysights.xyz

Pretracer - built by @igor_mikerin. fast copy trading plus cross-market arb between Polymarket and others

Link > t.me/pretracer_bot?start=ref…

PolyNoob - if you're just starting out. guides, strategy breakdowns, trader spotlights, monthly recaps

Link > polynoob.com

save this thread

9

1

36

1,651

Mar 18

Here's the bot mentioned in the first link in the comments, you can check out its detailed stats on hashdive.

I didn't believe it at first either, but its stats are just too good to be true.

2

19

13,387

Mar 4

didn’t know what hashdive was before i read your post so i checked it out and i made $1k today. definitely not a coincidence

1

2

136