$OSCR has the cleanest breakout setup I've seen in weeks.

Oscar Health. Insurtech. Not a household name.

What I'm watching:

• Highest conviction bullish score in the financial sector screen

• Volume confirmed the move — not a fake-out

• Bullish momentum intact

Only risk: volatility has increased. I'd be tightening stops here.

This is the kind of name that gets crowded fast once it starts trending.

It hasn't trended yet.

2

179

Insurers are beginning to use AI to handle policyholders’ first notices of loss (FNOLs) for claims, for greater efficiency and empathy, executives from @bhtp @BranchInsurance and Liberate say. bit.ly/4g862fE #ITI2026 #AI #InsuranceClaims #CustomerService #insurtech #FNOL #DigitalInsuranceNews

1

69

. Insurance2025 life policies use advanced data to offer personalized, flexible coverage.

#insurance2025_ife

#Insurance

#FinTech

#ClimateRisk

#CyberInsurance

#InsurTech

#HomeInsurance

#Liability

#CustomerExperience (#CX)

#FinancialLiteracy

insurance2025.com/

3

Insurance2025 life policies use advanced data to offer personalized, flexible coverage.

#insurance2025_ife

#Insurance

#FinTech

#ClimateRisk

#CyberInsurance

#InsurTech

#HomeInsurance

#Liability

#CustomerExperience (#CX)

#FinancialLiteracy

insurance2025.com/

2

Michael Skok explains the business model mistake most founders never recover from.

His example is antivirus software.

The product looked obvious: sell software that protects computers.

But Skok says the customer did not actually want software.

"What do they want to stop? Viruses. It's just protection for them."

That one sentence changes the whole business.

If the customer is buying software, the company optimizes for boxes, licenses, features, and distribution.

If the customer is buying protection, the company optimizes for a different outcome: fewer viruses, less downtime, less fear, less operational loss.

Same market.

Different object.

Different business model.

This is why Skok says they could rewrite the rules and take out competitors within a year.

They were not just changing packaging.

They were changing what the customer was really paying for.

Most industries make this mistake when the category gets complex.

They sell the visible artifact instead of the invisible outcome.

Software instead of protection.

Reports instead of decisions.

Checklists instead of risk reduction.

Premiums instead of insurability.

I see the same mistake in wildfire insurance.

A property owner thinks the work is the product: defensible space, vents, roof work, clearance, documentation, inspections.

But carriers are not buying effort.

They are buying proof that the property is a different risk than the average property in the same ZIP code.

That is the hidden translation problem.

Mitigation work does not automatically become underwriting evidence.

A cleaner property does not automatically become a better-priced risk.

The market cannot reward what it cannot see, verify, and trust.

After 20 years in insurtech, from Allstate to Argo to Kettle and RockRose, this is the pattern I keep coming back to.

Insurance systems do not break only because risk is high.

They break because the evidence layer is weak.

At McCloud/Tahoe, the important work was not just helping the association improve wildfire resilience.

It was turning that work into something underwriters could use.

Premiums moved from more than $1.3M to about $913K, over $400K in savings, with roughly $120K reinvested into mitigation.

That is Skok's lesson in a different market.

The customer does not want a checklist.

The customer wants protection that the insurance market can recognize.

For wildfire-exposed owners and managers, the next advantage is not doing random mitigation and hoping the carrier notices.

It is building a repeatable proof system around the property.

RockRose helps owners turn verified mitigation into underwriting evidence and potential premium savings.

Average FAIR Plan savings across RockRose clients: 21%.

Start here: rockroserisk.com/start

6

9

890

From orbital geospatial data to ecommerce returns: how a software engineer built an 8-figure insurtech in 5 years

yespress.io/zack-peng?utm_so… via Yespress

4

Insurance is the only product you hope you’ll never use—yet it quietly funds economies, rebuilds cities, and prices the future in real time. The real disruption isn’t insurtech apps. It’s better risk data. Whoever understands risk best wins everything.

3

Your weekly tech recap

•Privacy concerns grow around AI facial recognition

•Nigerian insurtech Myka secures pre-seed fundin... and more

The world is moving. Stay plugged in.

#WeeklyTechNews #TechRecap #StrivonTech #NaijaTech #AINews #MetaAI #NigeriaStartup #InsurTech

1

8

Move 74,000 fresh Florida leads to your CRM seamlessly. 🚀 Our CSV workflow & Recruiter Readiness Score power the Insurance Producer Intelligence Platform. Work smarter! jonlynchfinancial.com #Insurance #InsurTech #CRM #Recruiting

2

Spinnaker Acquisitions retweeted

Jun 12

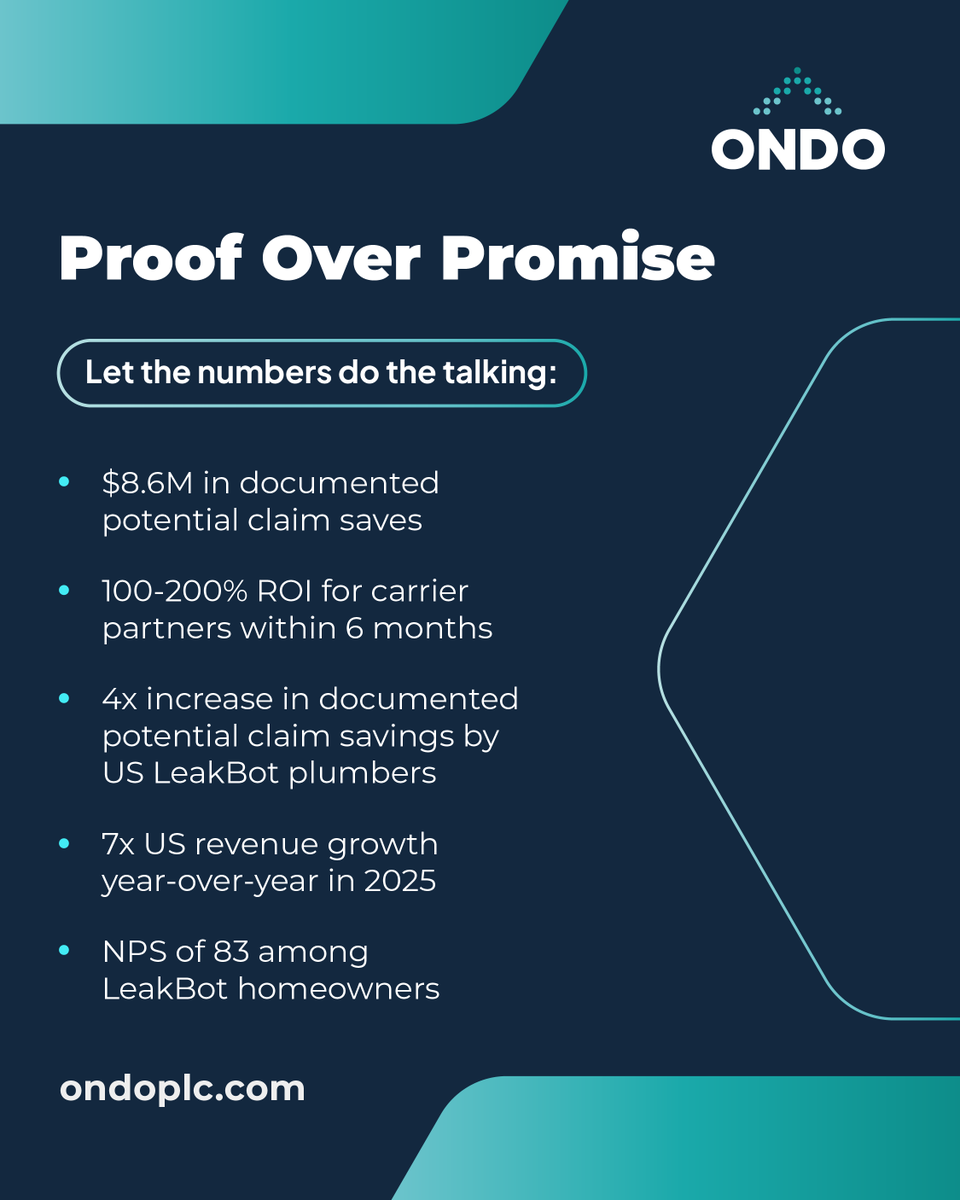

In insurtech, everyone has a pitch. Not everyone has proof. 📊

is delivering:

• $8.6M in potential claim saves

• 100–200% ROI in 6 months

• 7x US revenue growth in 2025

• NPS of 83

Prevention works. 💧

#Ondo #LeakBot #Insurtech #ClaimsPrevention

1

4

94

Jun 13

🔐 Threeam #Ransomware Group Claims Attack on BSynchro Holding, Raising Fresh Concerns for Germany’s Insurtech Sector – Dark Web Recent Claims Video

-Fact Checker: ✅: 3 ❌: 0 || 3/3 → Score: 100% 🦾

-Prediction: 📈 3 Positive | 📉 4 Negative

undercodenews.com/threeam-ra…

19

Threeam claims a ransomware attack on BSynchro Holding in Germany, disrupting insurtech operations and CORA configuration tools used by insurers, brokers, and reinsurers. #Germany #Insurtech #Ransomware

ift.tt/voKcbEJ

119

Jun 13

📋 Watchlist ของผม | 12 มิ.ย.

(ไม่ใช่คำแนะนำทางการเงิน)

🖥️ $NOW — บวกวันที่ 2 ต่อเนื่อง

💊 $HIMS — Long-term ถือต่อ

⚡ $IREN — ดีลอิหร่าน >80% ดีต่อทุกอย่าง 🔥

🐂 $BULL — Dow บวก Day 2 ได้ประโยชน์ ⚡

💳 $SOFI — แพลตฟอร์มขาย SPCX! 19% วันนี้ 🚀🚀

🤖 $PLTR — รอ $130-135

📡 $ONDS — Drone กลาโหม Long-term

🏠 $LMND — InsurTech AI Long-term

🌟 SPCX ปิดวันแรก $161 ( 19% จาก IPO!)

ยังไม่เข้า Watchlist รอดู Price Action ก่อน

ได้ Allocation SPCX วันนี้ไหมครับ? 👇

#หุ้นเมกาง่ายๆ #Watchlist #SpaceX #SOFI

351

Jun 13

Duck Creek expands global platform strategy with London Market push and Lloyd’s certification plans dlvr.it/TT1Rb4 #insurance #innovation #insurtech

1

Jun 13

Insured.vc – The ultimate premium .vc domain for insurance tech, insurtech platforms and smart protection solutions.

Insured.vc – Instantly conveys trust, security and coverage – perfect for digital insurance, DeFi protection or risk management funds.

Insured.vc – Short, authoritative and screams reliability in the booming insurtech and financial protection space.

Insured.vc – Ideal for policy platforms, claims automation, crypto insurance or venture-backed insurance startups.

Insured.vc – Own this high-value domain and position your brand as the trusted leader in insured innovation.

#InsurTech #FinTech #VCDomain #DomainForSale #PremiumDomain #Brandable #InsuranceTech

For more Brandable domains please visit iMunther.com

*** Feel free to reach out for exclusive discounts! ***

1

24

Jun 12

🎥 Periodista: José Roberto Arteaga en Forbes.

🚀 La tecnología está transformando la industria de seguros en México: desde pólizas digitales hasta productos personalizados y más accesibles para todos. 📲🛡️

Lee más aquí: efinf.com/clipviewer/files/b…

#Seguros #Insurtech #Tecnología

5

Jun 12

Ageas UK to deliver embedded motor insurance in deal with Wrisk dlvr.it/TT1KFY #insurance #innovation #insurtech

1

Jun 12

MetLife launches new deferred payment option for non-physical injury claims fintechnews.org/metlife-laun… a través de @fintechnews.org #InsurTech #insurance

3